Which Corporate Governance Mechanisms Drive CSR Disclosure Practices in Emerging Countries?

Abstract

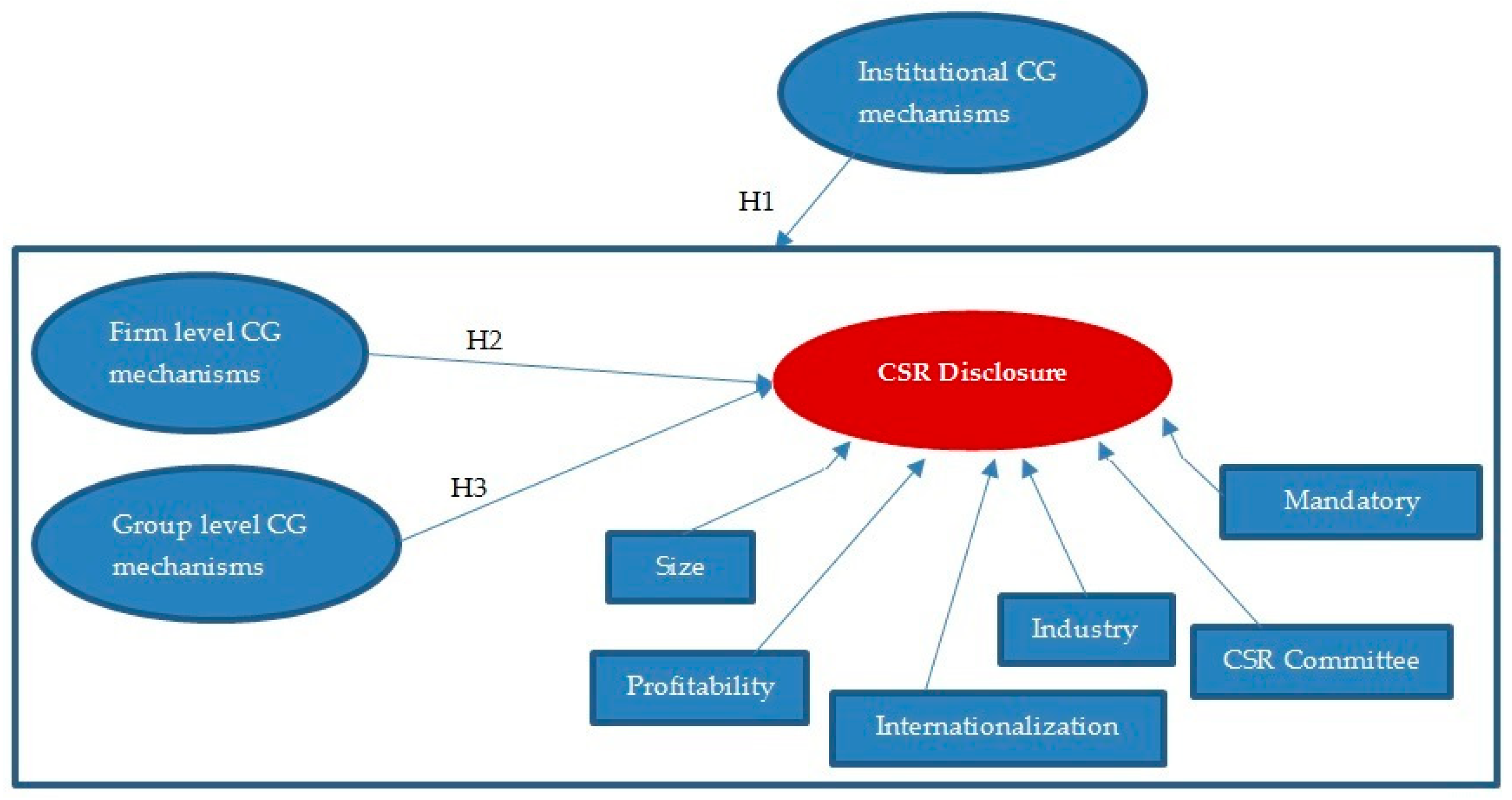

:1. Introduction

2. Determinants of CSR Reporting and Hypotheses Development

2.1. Institutional-Level CG Mechanisms

2.2. Firm-Level CG Mechanisms

2.3. Group-Level CG Mechanisms

3. Data Sources and Methodology

3.1. Sample

3.2. Variables

3.2.1. Dependent Variables: CSR Reporting Practices

3.2.2. Corporate Governance Mechanism: Group, Firm, and Institutional Levels

3.2.3. Control Variables

3.3. Regression Model Proposed

4. Results and Discussion

5. Conclusions

Author Contributions

Acknowledgments

Conflicts of Interest

References

- Aguinis, H.; Glavas, A. What we know and don’t know about corporate social responsibility: A review and research agenda. J. Manag. 2012, 38, 932–968. [Google Scholar] [CrossRef]

- Elkington, J. Governance for sustainability. Corp. Gov. 2006, 14, 522–529. [Google Scholar] [CrossRef]

- Du, S.; Bhattacharya, C.B.; Sen, S. Maximizing business returns to corporate social responsibility (CSR): The role of CSR communication. Int. J. Manag. Rev. 2010, 12, 8–19. [Google Scholar] [CrossRef]

- Bushman, R.; Piotroski, J.D.; Smith, A.J. What determines corporate transparency? J. Account. Res. 2004, 42, 207–252. [Google Scholar] [CrossRef]

- Dienes, D.; Velte, P. The impact of supervisory board composition on CSR reporting. Evidence from the German two-tier system. Sustainability 2016, 8, 63. [Google Scholar] [CrossRef]

- Crowther, D. Corporate reporting, stakeholders and the internet: Mapping the new corporate landscape. Urban Stud. 2000, 37, 1837–1848. [Google Scholar] [CrossRef]

- Ihlen, Ø.; Bartlett, J.; May, S. The Handbook of Communication and Corporate Social Responsibility, 1st ed.; John Wiley & Sons: Hoboken, NJ, USA, 2011; ISBN 978-1-444-33634-4. [Google Scholar]

- Jensen, J.C.; Berg, N. Determinants of Traditional Sustainability Reporting Versus Integrated Reporting. An Institutionalist Approach. Bus. Strategy Environ. 2012, 21, 299–316. [Google Scholar] [CrossRef]

- KPMG. The KPMG Survey of Corporate Responsibility Reporting 2017; KPMG International Global Sustainability Services: Amsterdam, The Netherlands, 2017; Available online: https://home.kpmg.com/content/dam/kpmg/campaigns/csr/pdf/CSR_Reporting_2017.pdf (accessed on 16 October 2018).

- Baskin, J. Corporate responsibility in emerging markets. J. Corp. Citizensh. 2006, 24, 29–47. [Google Scholar] [CrossRef]

- Amran, A.; Lee, S.P.; Devi, S.S. The influence of governance structure and strategic corporate social responsibility toward sustainability reporting quality. Bus. Strategy Environ. 2014, 23, 217–235. [Google Scholar] [CrossRef]

- Fifka, M. Corporate responsibility reporting and its determinants in comparative perspective-a review of the empirical literature and a meta-analysis. Bus. Strategy Environ. 2013, 22, 1–35. [Google Scholar] [CrossRef]

- Dienes, D.; Sassen, R.; Fischer, J. What are the Drivers of Sustainability Reporting? A Systematic Review. Sustain. Account. Manag. Policy J. 2016, 7, 154–189. [Google Scholar] [CrossRef]

- Ali, W.; Frynas, J.G.; Mahmood, Z. Determinants of corporate social responsibility (CSR) disclosure in developed and developing countries: A literature review. Corp. Soc. Responsib. Environ. Manag. 2017, 24, 273–294. [Google Scholar] [CrossRef]

- Michelon, G.; Parbonetti, A. The effect of corporate governance on sustainability disclosure. J. Manag. Gov. 2012, 16, 477–509. [Google Scholar] [CrossRef]

- Rodríguez-Ariza, L.; Frias, J.V.; García, R. El consejo de administración y las memorias de sostenibilidad. Revista de Contabilidad—Span. Account. Rev. 2014, 17, 5–16. [Google Scholar] [CrossRef]

- Martínez-Ferrero, J.; García-Sánchez, I.M. Sustainability assurance and assurance providers: Corporate governance determinants in stakeholder-oriented countries. J. Manag. Organ. 2017, 23, 647–670. [Google Scholar] [CrossRef]

- Miras, M.M.; Di Pietra, R. Corporate Governance mechanisms as drivers that enhance the credibility and usefulness of CSR disclosure. J. Manag. Gov. 2018, 22, 565–588. [Google Scholar] [CrossRef]

- Adnan, S.M.; Hay, D.; Van Staden, C.J. The influence of culture and corporate governance on corporate social responsibility disclosure: A cross country analysis. J. Clean. Prod. 2018, 198, 820–832. [Google Scholar] [CrossRef]

- Jain, T.; Jamali, D. Looking inside the Black Box: The Effect of Corporate Governance on Corporate Social Responsibility. Corp. Gov. 2016, 24, 253–273. [Google Scholar] [CrossRef]

- Belal, A.R.; Momin, M. Corporate social reporting (CSR) in emerging economies: A review and future direction. In Research in Accounting in Emerging Economies—Accounting in Emerging Countries; Tsamenyi, M., Uddin, S., Eds.; Emerald: Bingley, UK, 2009; pp. 119–143. ISBN 978-1-84950-625-0. [Google Scholar]

- Khan, A.; Muttakin, M.B.; Siddiqui, J. Corporate Governance and Corporate Social Responsibility Disclosures: Evidence from an Emerging Economy. J. Bus. Ethics 2013, 114, 207–223. [Google Scholar] [CrossRef]

- Adams, C.A. Internal organisational factors influencing corporate social and ethical reporting. Account. Audit. Account. J. 2002, 15, 223–250. [Google Scholar] [CrossRef]

- Claessens, S.; Yurtoglu, B.B. Corporate governance in emerging markets: A survey. Emerg. Mark. Rev. 2013, 15, 1–33. [Google Scholar] [CrossRef]

- Fan, J.P.; Wei, K.J.; Xu, X. Corporate finance and governance in emerging markets: A selective review and an agenda for future research. J. Corp. Financ. 2011, 17, 207–214. [Google Scholar] [CrossRef]

- Reverte, C. Determinants of corporate social responsibility disclosure ratings by Spanish listed firms. J. Bus. Eth. 2009, 88, 351–366. [Google Scholar] [CrossRef]

- Kansal, M.; Joshi, M.; Batra, G.S. Determinants of corporate social responsibility disclosures: Evidence from India. Adv. Account. 2014, 30, 217–229. [Google Scholar] [CrossRef]

- Sweeney, L.; Coughlan, J. Do different industries report corporate social responsibility differently? An investigation through the lens of stakeholder theory. J. Mark. Commun. 2008, 14, 113–124. [Google Scholar] [CrossRef]

- Lattemann, C.; Fetscherin, M.; Alon, I.; Li, S.; Schneider, A.M. CSR communication intensity in Chinese and Indian multinational companies. Corp. Gov. 2009, 17, 426–442. [Google Scholar] [CrossRef]

- Miras, M.M.; Escobar, B. Does the Institutional Environment affect CSR Disclosure? The Role of Governance. Rev. Adm. Empres. 2016, 56, 641–654. [Google Scholar] [CrossRef]

- Arrive, J.T.; Feng, M. Corporate social responsibility disclosure: Evidence from BRICS nations. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 920–927. [Google Scholar] [CrossRef]

- Chapple, W.; Moon, J. Corporate social responsibility (CSR) in Asia a seven-country study of CSR web site reporting. Bus. Soc. 2005, 44, 415–441. [Google Scholar] [CrossRef]

- Araya, M. Exploring Terra Incognita: Non-financial Reporting in Latin America. J. Corp. Citizensh. 2006, 21, 25–38. [Google Scholar] [CrossRef]

- Haniffa, R.M.; Cooke, T.E. The impact of culture and governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef] [Green Version]

- Li, Q.; Luo, W.; Wang, Y.; Wu, L. Firm performance, corporate onwnership, and corporate social responsibility disclosure in China. Bus. Eth. A Eur. Rev. 2013, 22, 159–173. [Google Scholar] [CrossRef]

- Ntim, C.G.; Soobaroyen, T. Corporate Governance and Performance in Socially Responsible Corporations: New Empirical Insights from a Neo-Institutional Framework. Corp. Gov. 2013, 21, 468–494. [Google Scholar] [CrossRef] [Green Version]

- Aguilera, R.V.; Desender, K.; Bednar, M.K.; Lee, J.H. Connecting the dots: Bringing external corporate governance into the corporate governance puzzle. Acad. Manag. Ann. 2015, 9, 483–573. [Google Scholar] [CrossRef]

- Di Maggio, P.J.; Powell, W.W. The iron cage revisited institutional isomorphism and collective rationality in organizational fields. Am. Sociol. Rev. 1983, 48, 147–160. [Google Scholar] [CrossRef]

- Baughn, C.C.; Bodie, N.L.; McIntosh, J.C. Corporate Social and Environmental Responsibility in Asian Countries and Other Geographical Regions. Corp. Soc. Responsib. Environ. Manag. 2007, 14, 189–205. [Google Scholar] [CrossRef]

- Ferri, L.M. The influence of the institutional context on sustainability reporting. A cross-national analysis. Soc. Responsib. J. 2017, 13, 24–47. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Pitman: Boston, MA, USA, 1984; ISBN 978-0273019138. [Google Scholar]

- Orij, R. Corporate social disclosures in the context of national cultures and stakeholder theory. Account. Audit. Account. J. 2010, 23, 868–889. [Google Scholar] [CrossRef] [Green Version]

- Deegan, C. The legitimising effect of social and environmental disclosures—A theoretical foundation. Account. Audit. Account. J. 2002, 15, 282–311. [Google Scholar] [CrossRef]

- Clarkson, P.M.; Overell, M.B.; Chapple, L. Environmental reporting and its relation to corporate environmental performance. Abacus 2011, 47, 27–60. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Aguilera, R.V.; Jackson, T. The cross-national diversity of corporate governance: Dimensions and determinants. Acad. Manag. Rev. 2003, 28, 447–466. [Google Scholar] [CrossRef]

- Luoma, P.; Goddstein, J. Stakeholders and corporate boards: Institutional influences on board composition and structure. Acad. Manag. J. 1999, 42, 553–563. [Google Scholar]

- Chiu, T.K.; Wang, Y.H. Determinants of social disclosure quality in Taiwan: An application of stakeholder theory. J. Bus. Eth. 2015, 129, 379–398. [Google Scholar] [CrossRef]

- Alon, I.; Lattemann, C.; Fetscherin, M.; Li, S.; Schneider, A.M. Usage of Public Corporate Communications of Social Responsibility in Brazil, Russia, India and China (BRIC). Int. J. Emerg. Mark. 2010, 5, 6–22. [Google Scholar] [CrossRef]

- Li, S.; Fetscherin, M.; Alon, I.; Lattemann, C.; Yeh, K. Corporate social responsibility in emerging markets: The importance of the Governance Environment. Manag. Int. Rev. 2010, 50, 635–654. [Google Scholar] [CrossRef]

- Said, R.; Zainuddin, Y.H.; Haron, H. The relationship between corporate social responsibility disclosure and corporate governance characteristics in Malaysian public listed companies. Soc. Responsib. J. 2009, 5, 212–226. [Google Scholar] [CrossRef]

- Haji, A.A. Corporate social responsibility disclosures over time: Evidence from Malaysia. Manag. Audit. J. 2013, 28, 647–676. [Google Scholar] [CrossRef]

- Esa, E.; Zahari, A.R. Corporate social responsibility: Ownership structures, board characteristics & the mediating role of board compensation. Procedia Econ. Financ. 2016, 35, 35–43. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef] [Green Version]

- Fama, E.F.; Jensen, M.C. Separation of ownership and control. J. Law Econ. 1983, 26, 301–326. [Google Scholar] [CrossRef]

- Ullmann, A.A. Data in search of a theory: A critical examination of the relationships among social performance, social disclosure, and economic performance of US firms. Acad. Manag. Rev. 1985, 10, 540–557. [Google Scholar]

- Hu, K.H.; Lin, S.J.; Hsu, M.F. A Fusion Approach for Exploring the Key Factors of Corporate Governance on Corporate Social Responsibility Performance. Sustainability 2018, 10, 1582. [Google Scholar] [CrossRef]

- Barnett, M.L. Stakeholder influence capacity and the variability of financial returns to corporate social responsibility. Acad. Manag. Rev. 2007, 32, 794–816. [Google Scholar] [CrossRef]

- Prado-Lorenzo, J.M.; Gallego-Alvarez, I.; Garcia-Sanchez, I.M. Stakeholder engagement and corporate social responsibility reporting: The ownership structure effect. Corp. Soc. Responsib. Environ. Manag. 2009, 16, 94–107. [Google Scholar] [CrossRef]

- Rizk, R.; Dixon, R.; Woodhead, A. Corporate social and environmental reporting: A survey of disclosure practices in Egypt. Soc. Responsib. J. 2008, 4, 306–323. [Google Scholar] [CrossRef]

- Panwar, R.; Paul, K.; Nybakk, E.; Hansen, E.; Thompson, D. The legitimacy of CSR actions of publicly traded companies versus family-owned companies. J. Bus. Eth. 2014, 125, 481–496. [Google Scholar] [CrossRef]

- Huafang, X.; Jianguo, Y. Ownership structure, board composition and corporate voluntary disclosure: Evidence from listed companies in China. Manag. Audit. J. 2007, 22, 604–619. [Google Scholar] [CrossRef]

- Zheng, L.; Balsara, N.; Huang, H. Regulatory pressure, blockholders and corporate social responsibility (CSR) disclosures in China. Soc. Responsib. J. 2014, 10, 226–245. [Google Scholar] [CrossRef]

- Maier, S. How Global Is Good Corporate Governance; Ethical Investment Research Services: London, UK, 2005; Available online: www.eiris.org/files/research%20publications/howglobalisgoodcorpgov05.pdf (accessed on 10 October 2018).

- Hung, H. Directors’ roles in corporate social responsibility: A stakeholder perspective. J. Bus. Eth. 2011, 103, 385–402. [Google Scholar] [CrossRef]

- Velte, P. Does board composition have an impact on CSR reporting. Probl. Perspect. Manag. 2017, 15, 19–35. [Google Scholar] [CrossRef]

- Waddock, S.A.; Graves, S.B. The corporate social performance-financial performance link. Strateg. Manag. J. 1997, 18, 303–319. [Google Scholar] [CrossRef]

- Brennan, N. Boards of directors and firm performance: Is there an expectations gap? Corp. Gov. 2006, 14, 577–593. [Google Scholar] [CrossRef]

- Hussain, N.; Rigoni, U.; Orij, R.P. Corporate Governance and Sustainability Performance: Analysis of Triple Bottom Line Performance. J. Bus. Eth. 2018, 149, 411–432. [Google Scholar] [CrossRef]

- Giannarakis, G. Corporate governance and financial characteristic effects on the extent of corporate social responsibility disclosure. Soc. Responsib. J. 2014, 10, 569–590. [Google Scholar] [CrossRef]

- Hillman, A.J.; Keim, G.D. Shareholder value, stakeholder management, and social issues: What’s the bottom line? Strateg. Manag. J. 2001, 22, 125–139. [Google Scholar] [CrossRef]

- Jensen, M.C. The modern industrial revolution, exit, and the failure of internal control systems. J. Financ. 1993, 48, 831–880. [Google Scholar] [CrossRef]

- Coles, J.L.; Daniel, N.D.; Naveen, L. Boards: Does one size fit all? J. Financ. Econ. 2008, 87, 329–356. [Google Scholar] [CrossRef]

- Mahmood, Z.; Kouser, R.; Ali, W.; Ahmad, Z.; Salman, T. Does corporate governance affect sustainability disclosure? A mixed methods study. Sustainability 2018, 10, 207. [Google Scholar] [CrossRef]

- Liu, X.; Zhang, C. Corporate governance, social responsibility information disclosure, and enterprise value in China. J. Clean. Prod. 2017, 142, 1075–1084. [Google Scholar] [CrossRef]

- Liao, L.; Lin, T.P.; Zhang, Y. Corporate board and corporate social responsibility assurance: Evidence from China. J. Bus. Eth. 2018, 150, 211–225. [Google Scholar] [CrossRef]

- Sial, M.S.; Zheng, C.; Khuong, N.V.; Khan, T.; Usman, M. Does firm performance influence corporate social responsibility reporting of Chinese listed companies? Sustainability 2018, 10, 2217. [Google Scholar] [CrossRef]

- Majeed, S.; Aziz, T.; Saleem, S. The effect of corporate governance elements on corporate social responsibility (CSR) disclosure: An empirical evidence from listed companies at KSE Pakistan. Int. J. Financ. Stud. 2015, 3, 530–556. [Google Scholar] [CrossRef]

- Lone, E.J.; Ali, A.; Khan, I. Corporate governance and corporate social responsibility disclosure: Evidence from Pakistan. Corp. Gov. Int. J. Bus. Soc. 2016, 16, 785–797. [Google Scholar] [CrossRef]

- Shamil, M.M.; Shaikh, J.M.; Ho, P.L.; Krishnan, A. The influence of board characteristics on sustainability reporting: Empirical evidence from Sri Lankan firms. Asian Rev. Account. 2014, 22, 78–97. [Google Scholar] [CrossRef]

- Esa, E.; Ghazali, N.A.M. Corporate social responsibility and corporate governance in Malaysian government linked companies. Corp. Gov. Int. J. Bus. Soc. 2012, 12, 292–305. [Google Scholar] [CrossRef]

- Janggu, T.; Darus, F.; Zain, M.M.; Sawani, Y. Does good corporate governance lead to better sustainability reporting? An analysis using structural equation modelling. Procedia Soc. Behav. Sci. 2014, 145, 138–145. [Google Scholar] [CrossRef]

- Sahin, K.; Basfirinci, C.S.; Ozsalih, A. The impact of board composition on corporate financial and social responsibility performance: Evidence from public-listed companies in Turkey. Afr. J. Bus. Manag. 2011, 5, 2959–2978. [Google Scholar] [CrossRef]

- Kiliç, M.; Kuzey, C.; Uyar, A. The impact of ownership and board structure on Corporate Social Responsibility (CSR) reporting in the Turkish banking industry. Corp. Gov. 2015, 15, 357–374. [Google Scholar] [CrossRef]

- Chen, C.J.P.; Jaggi, B. Association between independent non-executive directors, family control and financial disclosures in Hong Kong. J. Account. Public Policy 2000, 19, 285–310. [Google Scholar] [CrossRef]

- Jizi, M.; Salama, A.; Dixon, R.; Stratling, R. Corporate governance and corporate social responsibility disclosure: Evidence from the US Banking Sector. J. Bus. Eth. 2014, 125, 601–615. [Google Scholar] [CrossRef]

- Webb, E. An examination of socially responsible firms’ board structure. J. Manag. Gov. 2004, 8, 255–277. [Google Scholar] [CrossRef]

- Muttakin, M.B.; Subramaniam, N. Firm ownership and board characteristics: Do they matter for corporate social responsibility disclosure of Indian companies? Sustain. Account. Manag. Policy J. 2015, 6, 138–165. [Google Scholar] [CrossRef]

- Pistoni, A.; Songini, L.; Bavagnoli, F. Integrated Reporting Quality: An Empirical Analysis. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 489–507. [Google Scholar] [CrossRef]

- Moneva, J.M.; Rivera-Lirio, J.M.; Muñoz-Torres, M.J. The corporate stakeholder commitment and social and financial performance. Ind. Manag. Data Syst. 2007, 107, 84–102. [Google Scholar] [CrossRef]

- Muñoz, M.J.; Rivera, J.M.; Moneva, J.M. Evaluating sustainability in organisations with a fuzzy logic approach. Ind. Manag. Data Syst. 2008, 108, 829–841. [Google Scholar] [CrossRef] [Green Version]

- Li, S. Managing International Business in Relation-Based versus Rule-Based Countries; Business Expert Press: New York, NY, USA, 2009; ISBN 978-1-60649-084-6. [Google Scholar]

- Wu, J.; Li, S.; Samsell, D. Why some countries trade more, some trade less, some trade almost nothing: The effect of the governance environment on trade flows. Int. Bus. Rev. 2012, 21, 225–238. [Google Scholar] [CrossRef]

- KPMG. Carrots and Sticks. Sustainability Reporting Policies Worldwide—Today’s Best Practice, Tomorrow’s Trends; KPMG International Global Sustainability Services: Amsterdam, The Netherlands, 2013; Available online: https://www.globalreporting.org/resourcelibrary/Carrots-and-Sticks.pdf (accessed on 8 March 2017).

- Birkey, R.; Michelon, G.; Patten, D.M.; Sankara, J. Does assurance on CSR reporting enhance environmental reputation? An examination in the US context. Account. Forum 2016, 40, 143–152. [Google Scholar] [CrossRef]

- Li, S.; Filer, L. The effects of the governance environment on the choice of investment mode and the strategic implications. J. World Bus. 2007, 42, 80–98. [Google Scholar] [CrossRef]

- Chatterjee, B.; Mir, M.Z. The current status of environmental reporting by Indian companies. Manag. Audit. J. 2008, 23, 609–629. [Google Scholar] [CrossRef]

- Lu, F.; Kozak, R.; Toppinen, A.; D’Amato, D.; Wen, Z. Factors influencing levels of CSR disclosure by forestry companies in China. Sustainability 2017, 9, 1800. [Google Scholar] [CrossRef]

- Goncalves, R.; Medeiros, O.; Weffort, E.; Niyama, J. A social disclosure index for assessing social programs in Brazilian listed firms. In Research in Accounting in Emerging Economies—Accounting in Latin America; De Araujo, C., Frezatti, F., Eds.; Emerald: Bingley, UK, 2014; pp. 75–103. ISBN 978-1-78441-068-1. [Google Scholar]

- Loprevite, S.; Ricca, B.; Rupo, D. Performance Sustainability and Integrated Reporting: Empirical Evidence from Mandatory and Voluntary Adoption Contexts. Sustainability 2018, 10, 1351. [Google Scholar] [CrossRef]

- KPMG. The KPMG Survey of Corporate Responsibility Reporting 2015; KPMG International Global Sustainability Services: Amsterdam, The Netherlands, 2015; Available online: https://home.kpmg.com/xx/en/home/insights/2015/11/kpmg-international-survey-of-corporate-responsibility-reporting-2015.html (accessed on 16 October 2018).

- Mobus, J.L. Mandatory environmental disclosures in a legitimacy theory context. Account. Audit. Account. J. 2005, 18, 492–517. [Google Scholar] [CrossRef]

- Miras-Rodríguez, M.M.; Carrasco-Gallego, A.; Escobar-Pérez, B. Has the CSR engagement of electrical companies had an effect on their performance? A closer look at the environment. Bus. Strategy Environ. 2015, 24, 819–835. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Factors influencing social responsibility disclosure by Portuguese companies. J. Bus. Eth. 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Chan, J.H.; Welford, R. Assessing Corporate Environmental Risk in China: An Evaluation of Reporting Activities of Hong Kong Listed Enterprises. Corp. Soc. Responsib. Environ. Manag. 2005, 12, 88–104. [Google Scholar] [CrossRef]

- Frias-Aceituno, J.V.; Rodriguez-Ariza, L.; Garcia-Sanchez, I.M. The Role of the Board in the Dissemination of Integrated Corporate Social Reporting. Corp. Soc. Responsib. Environ. Manag. 2013, 20, 219–233. [Google Scholar] [CrossRef]

{kind=link}

| Variables | Measures | ||

|---|---|---|---|

| Dependent variable | Corporate Social Responsibility (CSR) reporting complexity [90] | Index formed by: CSR information in a report GRI adoption Getting a GRI “in accordance” level Assurance of the CSR report | |

| GRI levels [16] | 0—non-GRI application level 1—GRI level C 2—GRI level B 3—GRI level A | ||

| Independent variables | Group-level corporate governance (CG) mechanisms | Board size [76] | Number of directors |

| Independent directors [88] | % of independent directors | ||

| Firm-level CG mechanisms | Reference shareholder * | Dummy variable [26,59] | |

| Institutional-level CG mechanism | GEI [92,93]: rule-based, family-based or relation-based | ||

| Control variables | Organizational characteristics | Size | Total assets [11,51] |

| Profitability | ROA [16,35] | ||

| International sales | Dummy variable [32] | ||

| CSR committee | Dummy variable [11,15] | ||

| Mandatory | Dummy variable [94]: 0 (Voluntary), 1 (Mandatory) ** | ||

| Industry sensitivity [95] | ASSET 4 | ||

| Relation-Based | Family-Based | Rule-Based | |||

|---|---|---|---|---|---|

| China | −5.92 | Russia | −4.34 | South Africa | 3.11 |

| Brazil | −2.06 | ||||

| India | −0.85 | ||||

| Complete Sample N = 281 | Brazil N = 44 | China N = 47 | India N = 76 | Russia N = 24 | South Africa N = 90 | |

|---|---|---|---|---|---|---|

| Total assets (millions) | 592.520 | 57.301 | 1066.461 | 724.523 | 2196.530 | 67.473 |

| ROA | 7.878 | 6.352 | 3.846 | 9.638 | 6.134 | 9.709 |

| International sales (millions) | 68.183 | 3.380 | 24.025 | 112.762 | 353.637 | 9.157 |

| Board size | 10.94 | 9.02 | 11.08 | 10.89 | 11.16 | 11.76 |

| Independent directors (%) | 37.612 | 22.47 | 24.90 | 44.75 | 37.46 | 45.65 |

| Complete Sample N = 281 | Brazil N = 44 | China N = 47 | India N = 76 | Russia N = 24 | South Africa N = 90 | |

|---|---|---|---|---|---|---|

| Complexity of the CSR reporting | ||||||

| Opaque Pro-translucid Translucid Pro-transparent Transparent | 18.1% 45.2% 7.8% 13.2% 15.7% | 20.5% 11.4% 11.4% 22.7% 34.1% | 27.7% 63.8% 4.3% 0% 4.3% | 22.4% 47.4% 1.3% 6.6% 22.3% | 33.3% 20.9% 12.5% 33.3% 0% | 4.4% 56.7% 12.2% 15.6% 11.1% |

| GRI level | ||||||

| A B C Non-GRI | 16.0% 13.2% 6.0% 64.8% | 29.5% 25% 13.6% 31.8% | 2.1% 2.1% 0% 95.8% | 27.6% 1.3% 0% 71.1% | 16.6% 25% 4.2% 54.2% | 6.7% 20% 11.1% 62.2% |

| Reference shareholder (%) | 0.36 | 0.50 | 0.43 | 0.37 | 0.70 | 0.44 |

| CSR committee (%) | 0.61 | 0.75 | 0.30 | 0.47 | 0.33 | 0.88 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) Reporting complexity | 1 | ||||||||||

| (2) GRI level | 0.89 ** | 1 | |||||||||

| (3) Board size | 0.17 ** | 0.13 * | 1 | ||||||||

| (4) Board independence | 0.02 | 0.04 | 0.01 | 1 | |||||||

| (5) CSR committee | 0.46 ** | 0.38 ** | 0.22 ** | 0.05 | 1 | ||||||

| (6) Reference Shareholder | 0.13 * | 0.15 * | −0.02 | −0.24 ** | −0.06 | 1 | |||||

| (7) Mandatory | 0.04 | −0.06 | −0.01 | −0.20 ** | 0.26 ** | −0.15 * | 1 | ||||

| (8) Institutional CG mechanism | −0.05 | −0.17 ** | 0.21 ** | 0.17 ** | 0.29 ** | −0.29 ** | 0.67 ** | 1 | |||

| (9) Size | 0.03 | 0.02 | 0.25 ** | −0.07 | 0.010 | 0.14 * | −0.19 ** | −0.15 * | 1 | ||

| (10) Profitability | 0.14 * | 0.09 | −0.05 | 0.12 | 0.04 | −0.04 | −0.09 | 0.08 | −0.13 * | 1 | |

| (11) Internationalization | 0.15 * | 0.12 * | 0.18 ** | 0.16 ** | 0.08 | −0.01 | 0.04 | 0.21 ** | 0.05 | −0.04 | 1 |

| Complete Sample | Family-Based (N = 144) | Relation-Based (N = 47) | Rule-Based (N = 90) | |||||

|---|---|---|---|---|---|---|---|---|

| Constant | −4.894 *** | −4.883 *** | −6.062 *** | −5.744 *** | −2.773 * | −2.941 * | −2.138 | −2.181 |

| Board size | 0.029 | - | 0.067 † | - | -0.019 | - | 0.006 | - |

| Board independ. | 0.002 | - | 0.003 | - | -0.023 * | - | 0.003 | - |

| Ref. shareholder | - | 0.107 | - | 0.006 | - | 0.217 | - | −0.042 |

| Size | 0.240 *** | 0.254 *** | 0.262 *** | 0.287 *** | 0.223 *** | 0.187 * | 0.170 | 0.186 * |

| Profitability | 0.043 *** | 0.042 *** | 0.060 *** | 0.061 *** | 0.025 | 0.020 | 0.016 | 0.015 |

| Internationalization | 0.462 *** | 0.481 *** | 0.443 * | 0.496 * | 0.308 | 0.283 | 0.666 * | 0.682 * |

| Industry sensitivity | 0.191 | 0.164 | 0.413 * | 0.401 * | −0.374 † | −0.379 † | −0.561 | −0.563 |

| CSR committee | 0.977 *** | 0.999 *** | 1.235 *** | 1.293 *** | 0.341 | 0.371 | 0.249 | 0.243 |

| Mandatory | 1.742 *** | 1.722 *** | 1.767 *** | 1.644 *** | - | - | - | - |

| Country (controlled) | *** | *** | - | - | - | - | - | - |

| R2 | 0.393 | 0.391 | 0.500 | 0.488 | 0.433 | 0.382 | 0.180 | 0.177 |

| Complete Sample | Family-Based (N = 144) | Relation-Based (N = 47) | Rule-Based (N = 90) | |||||

|---|---|---|---|---|---|---|---|---|

| Constant | −4.097 *** | −4.181 *** | −5.749 *** | −5.625 *** | −1.557 | −1.255 | −3.530 * | −3.241 † |

| Board size | 0.023 | - | 0.072 † | - | -0.016 | - | −0.026 | - |

| Board independ. | 0.004 | - | 0.007 | - | -0.005 | - | 0.001 | - |

| Ref. shareholder | - | −0.048 | - | −0.212 | - | 0.231 | - | 0.007 |

| Size | 0.187 *** | 0.211 *** | 0.219 ** | 0.267 *** | 0.100 † | 0.064 | 0.223 † | 0.192 † |

| Profitability | 0.037 *** | 0.038 *** | 0.047 *** | 0.050 *** | 0.013 | 0.011 | 0.023 | 0.022 |

| Internationalization | 0.421 *** | 0.447 *** | 0.320 † | 0.389 * | 0.177 | 0.187 | 0.781 * | 0.781 * |

| Industry sensitivity | 0.354 * | 0.348 * | 0.548** | 0.574 *** | −0.180 | −0.217 | −0.178 | −0.162 |

| CSR committee | 0.662 *** | 0.671 *** | 0.850 *** | 0.904 *** | −0.070 | −0.047 | 0.242 | 0.200 |

| Mandatory | 1.460 *** | 1.438 *** | 1.815 *** | 1.712 *** | - | - | - | - |

| Country (controlled) | *** | *** | - | - | - | - | - | - |

| R2 | 0.342 | 0.338 | 0.434 | 0.419 | 0.144 | 0.177 | 0.159 | 0.156 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Miras-Rodríguez, M.d.M.; Martínez-Martínez, D.; Escobar-Pérez, B. Which Corporate Governance Mechanisms Drive CSR Disclosure Practices in Emerging Countries? Sustainability 2019, 11, 61. https://doi.org/10.3390/su11010061

Miras-Rodríguez MdM, Martínez-Martínez D, Escobar-Pérez B. Which Corporate Governance Mechanisms Drive CSR Disclosure Practices in Emerging Countries? Sustainability. 2019; 11(1):61. https://doi.org/10.3390/su11010061

Chicago/Turabian StyleMiras-Rodríguez, María del Mar, Domingo Martínez-Martínez, and Bernabé Escobar-Pérez. 2019. "Which Corporate Governance Mechanisms Drive CSR Disclosure Practices in Emerging Countries?" Sustainability 11, no. 1: 61. https://doi.org/10.3390/su11010061

APA StyleMiras-Rodríguez, M. d. M., Martínez-Martínez, D., & Escobar-Pérez, B. (2019). Which Corporate Governance Mechanisms Drive CSR Disclosure Practices in Emerging Countries? Sustainability, 11(1), 61. https://doi.org/10.3390/su11010061