Socially Responsible Human Resource Management as a Concept of Fostering Sustainable Organization-Building: Experiences of Young Polish Companies

Abstract

:1. Introduction

- (1)

- Ecological—which involves a reduction of environmental degradation;

- (2)

- Economic—expressed by satisfying basic material human needs with the application of technology and techniques which do not destroy the environment;

- (3)

- Social—which assumes the maintenance of a social minimum (eradication of hunger and poverty), health protection, development of human spiritual sphere (culture), safety and education.

- —Which SRHRM practices are most often implemented in young Polish enterprises?

- —Which SRHRM practices are key to the sustainable development of organizations in the Polish reality?

- —Is there a correlation between the assessment of the relation of SRHRM practices with the sustainable development of organizations and its practical implementation in the young Polish enterprises analyzed?

2. Literature Review

2.1. The Role of HRM in the Creation of Sustainable Organizations Development

- just treatment, commitment to employee development and welfare;

- building employee trust and increasing their motivation to work for the benefit of sustainable development;

- taking care of internal stakeholders’ (employees) and external stakeholders’ health;

- fostering environment-friendly practices.

2.2. The Essence and Benefits of SRHRM Implementation

- —CSR supported by HRM (HRM practices used to involve employees in CSR implementation);

- —HRM supported by CSR (CSR practices used to attract, keep and motivate employees).

3. Materials and Methods

- Acknowledgement of the Polish managers’ opinions concerning the meaning of particular socially responsible human resource practices in shaping sustainable development of young enterprises

- Identification of practices which are key to sustainable enterprise-building in the opinion of Polish managers;

- Diagnosis of practices which in the opinions of respondents have a marginal role to play in sustainable enterprise-building;

- Determination of the frequency of implementation of individual socially responsible activities in the field of human resource management within the studied enterprises;

- Identification of practices most popular under Polish conditions;

- Diagnosis of practices which are rarely implemented by young enterprises under Polish conditions;

- Analysis of the correlation between the assessment of the relation of SRHRM practices with the sustainable development of organizations and their practical implementation in young Polish enterprises;

- Description of the above-mentioned correlation with the application of a mathematical model and a calculation of standard errors of the estimates.

4. Results and Discussion

4.1. Assessment of the Relationship between SRHRM Practices and the Sustainable Development of Young Organizations

- —commitment to fairness of one’s employment offer (activity no. 1), with an impact average of 4.36;

- —equal access to training (activity no. 9), with an impact average of 4.33;

- —investment in employee development (activity no. 8), with an impact average of 4.31;

- —provision of generous remuneration (activity no. 12), with an impact average of 4.29;

- —just and clear dismissal procedures (activity no. 17), with an impact average of 4.11.

- —drafting reports on social responsibility in HRM (activity no. 35);

- —support for dismissed employees (activity no. 10);

- —measurement of effectiveness of environmental actions in HRM (activity no. 32);

- —employee involvement in social projects as part of corporate volunteering (activity no. 29);

- —HRM socially responsible action progress monitoring (activity no. 34);

- —provision for socially responsible HRM activities-related expenditure in the budget (activity no. 23);

- —ethical code training organization (activity no. 33).

- —HRM socially responsible action progress monitoring;

- —drafting reports on social responsibility in HRM;

- —measurement of effectiveness of environmental actions in HRM; and

- —provision for socially responsible HRM activities-related expenditure in the budget.

4.2. Evaluation of the Scope of SRHRM Concept Implementation in Polish Enterprises

- Activity no. 11, i.e., Compliance with industrial health and safety, was implemented by the greatest number of entities: 149 (99.33% of the total)

- Activity no. 1, i.e., Commitment to fairness of one’s employment offer and activity no. 13, i.e., Transparent rules of remuneration, accomplished by 147 enterprises (98% of the total);

- Activity no. 6, i.e., Facilitating new employee adaptation, implemented by 146 companies (97.33% of the total);

- Activity no. 2, i.e., Commitment to nondiscrimination in vacancy advertising, i.e., Eliminating elements which could discriminate because of sex, age, appearance, disability, etc., declared by 143 companies (95.33% of the total);

- Activity no. 8, i.e., Investment in employee development, and activity no. 9, i.e., Equal access to training, pursued by 142 enterprises (94.67% total);

- Activity no. 12, i.e., Providing generous remuneration, implemented by 141 of the studied entities (94% of the total).

- Activity no. 20, i.e., The award of ethical certificates, implemented by a mere 25 entities (16.67% of the population);

- Activity no. 10, i.e., Supporting employees who are made redundant (help with finding a new job, psychological support), declared by 47 enterprises (31.33% of the group).

- Activity no. 35, i.e., Drafting reports on social responsibility in HRM, pursued by 49 companies (32.67% of the population);

- Activity no. 19, i.e., The conduct of ethical audits, implemented by 50 entities (33.33% of the population);

- Activity no. 32, i.e., Measurement of effectiveness of environmental actions in hrm; and activity no. 29, i.e. Employee involvement in social projects as part of corporate volunteering, implemented by 56 enterprises (37.33& of the group);

- Activity no. 34, i.e., Hrm socially responsible action progress monitoring and activity no. 29, i.e., Ethical code workshop organization, implemented by 62 enterprises (41.33% of the group).

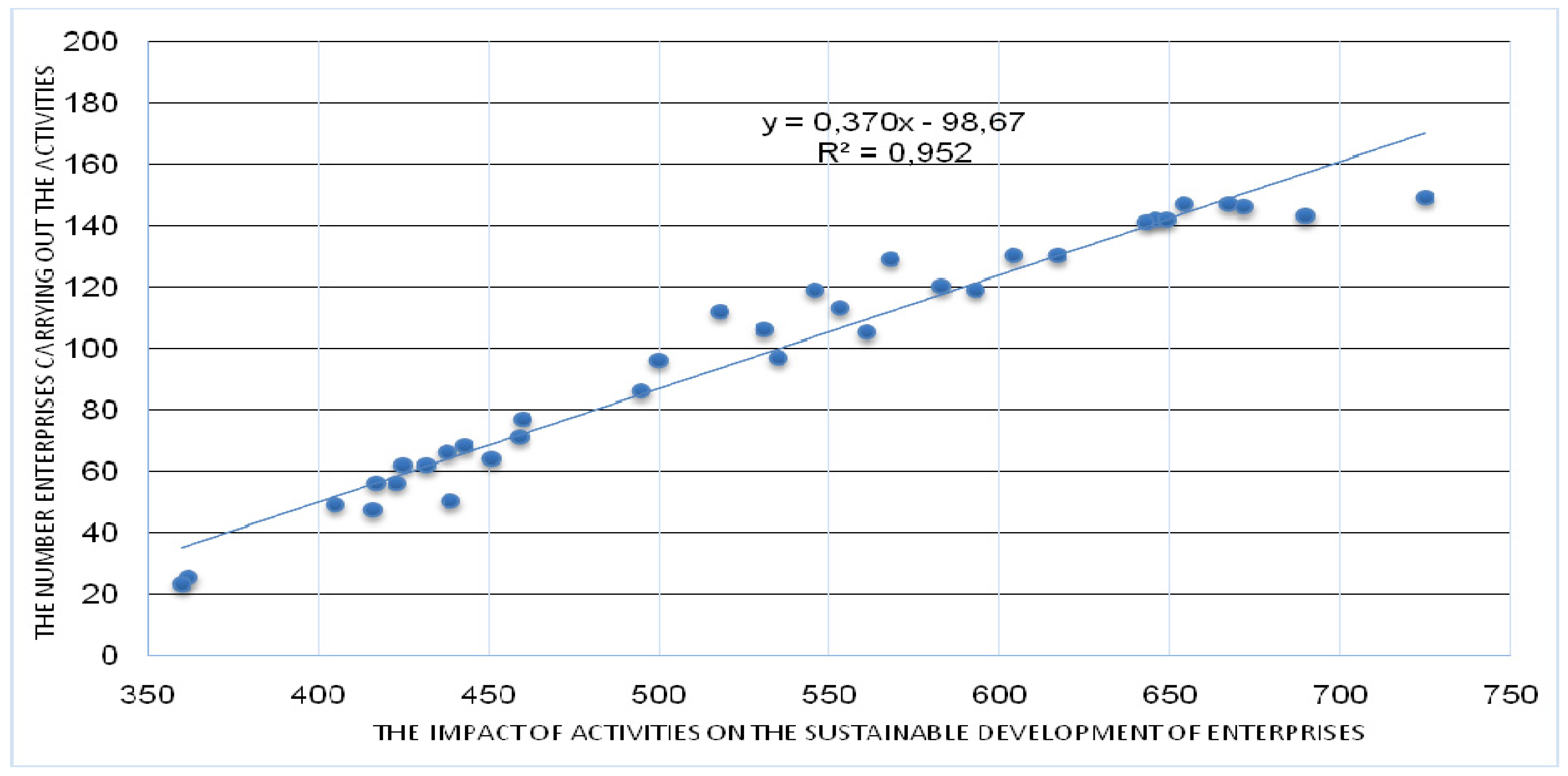

4.3. The Correlation Between the Assessment of the Relation of SRHRM Practices with the Sustainable Development of Organizations and Their Realization in Young Enterprises

5. Conclusions

- —the focus of a significant rate of the studied entities on obligatory practices, i.e., Those required by law;

- —a low rate of entities which hold ethical certificates;

- —low interest in the issue of compliance with ethical requirements by contractual partners;

- —a widespread lack of developed measurement and reporting procedures regarding SRHRM.

Author Contributions

Acknowledgments

Conflicts of Interest

References

- Rosińska-Bukowska, M. Społeczna odpowiedzialność biznesu w procesie kreacji wartości dodanej przedsiębiorstwa. In Kreacja Wartości Przedsiębiorstw. Nowe Trendy i Kierunki Rozwoju; Jabłoński, M., Zamasz, K., Eds.; WSB: Dąbrowa Górnicza, Poland, 2012; pp. 331–357. ISBN 978-83-62897-34-6. [Google Scholar]

- Jastrzębska, E. Ewolucja społecznej odpowiedzialności biznesu w Polsce. Kwartalnik Kolegium Ekonomiczno-Społecznego Studia i Prace SGH 2016, 4, 85–101. [Google Scholar]

- Jabłoński, A. Zrównoważony Rozwój a Zrównoważony Biznes w Budowie Wartości Przedsiębiorstw Społecznie Odpowiedzialnych; Zeszyty Naukowe Wyższej Szkoły Humanitas; Oficyna Wydawnicza Humanitas: Zarządzanie, Poland, 2010; Volume 2, pp. 15–30. [Google Scholar]

- Report of the World Commission on Environment and Development: Our Common Future. Available online: http://www.un-documents.net/our-common-future.pdf (accessed on 27 August 2018).

- Mazur-Wierzbicka, E. Koncepcja zrównoważonego rozwoju jako podstawa gospodarowania środowiskiem przyrodniczym. In Funkcjonowanie gospodarki polskiej w warunkach integracji i globalizacji; Kopycińska, D., Ed.; Katedra Mikroekonomii Uniwersytetu Szczecińskiego: Szczecin, Poland, 2005; pp. 33–44. ISBN 9788391748763. [Google Scholar]

- Colbert, B.A.; Kurucz, E.C. Three conceptions of triple bottom line business sustainability and the role of HRM. Hum. Resour. Plan. 2007, 30, 21–29. [Google Scholar]

- Rimanoczy, I.; Pearson, T. Role of HR in the new world of sustainability. Ind. Commer. Train. 2010, 42, 11–17. [Google Scholar] [CrossRef]

- Skowroński, A. Zrównoważony rozwój perspektywą dalszego postępu cywilizacji. Probl. Ekorozw. 2006, 2, 47–57. [Google Scholar]

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of Twenty-First Century Business; Capstone: Mankato, MN, USA, 1997. [Google Scholar]

- ISO 26000:2010 Guidance on Social Responsibility. Available online: https://www.iso.org/standard/42546.html (accessed on 17 May 2018).

- Adamczyk, J.; Nitkiewicz, T. Programowanie Zrównoważonego Rozwoju Przedsiębiorstw; PWE: Warszawa, Poland, 2007; ISBN 83-208-1705-8. (In Polish) [Google Scholar]

- Porter, M.E.; Kramer, M.R. Tworzenie wartości dla biznesu i społeczeństwa. Harv. Bus. Rev. Polska 2011, 5, 80–87. (In Polish) [Google Scholar]

- Rok, B. Odpowiedzialny Biznes w Nieodpowiedzialnym Świecie; Akademia Rozwoju Filantropii w Polsce, Forum Odpowiedzialnego Biznesu: Warszawa, Poland, 2001. (In Polish) [Google Scholar]

- Carroll, A.B. Carroll’s Pyramid of CSR: Taking Another Look. 2016. Available online: https://doi.org/10.1186/s40991-016-0004-6 (accessed on 15 February 2019).

- Hart, S. Capitalism at the Crossroads: Aligning Commerce, Earth, and Humanity, 2nd ed.; FT Press: Upper Saddle River, NJ, USA, 2007. [Google Scholar]

- Pichola, I.; Nocoń, A. Jak Angażować Interesariuszy Firmy do Budowania jej Wartości, Odpowiedzialny Biznes; Harvard Business Review: Warszawa, Poland, 2008. (In Polish) [Google Scholar]

- Szumiak-Samolej, J. Odpowiedzialny Biznes w Gospodarce Sieciowej; Poltext: Warszawa, Poland, 2013; ISBN 978-83-7561-360-5. (In Polish) [Google Scholar]

- Hys, K.; Hawrysz, L. Corporate Social Responsibility Reporting. China-USA Bus. Rev. 2012, 11, 1515–1524. [Google Scholar]

- Hediger, W. Welfare and capital-theoretic foundations of corporate social responsibility and corporate sustainability. J. Socio-Econ. 2010, 39, 518–526. [Google Scholar] [CrossRef]

- Cohen, E.; Taylor, S.; Muller-Camen, M. HRM’s Role in Corporate Social and Environmental Sustainability; SHRM Report: Alexandria, VA, USA, 2012. [Google Scholar]

- Jamali, D.; Safieddine, A.M.; Rabbath, M. Corporate Governance and Corporate Social Responsibility Synergies and Interrelationships. Corp. Gov. Int. Rev. 2008, 16, 443–459. [Google Scholar] [CrossRef] [Green Version]

- Buchholz, A.K.; Brown, J.; Shabana, K. Corporate governance and corporate social responsibility. The Oxford Handbook of Corporate Social Responsibility; Crane, A., McWilliams, A., Matten, D., Moon, J., Siegel, D.S., Eds.; Oxford University Press: New York, NY, USA, 2008; pp. 327–345. ISBN 9780199211593. [Google Scholar]

- Harjoto, M.A.; Jo, H. Corporate Governance and CSR Nexus. J. Bus. Ethics 2011, 100, 45–67. [Google Scholar] [CrossRef]

- Wilewska, M. Corporate governance i corporate social responsibility—Powiązania i wzajemne relacje. Zarządzanie Finans. 2013, 2, 67–75. [Google Scholar]

- Giroud, X.; Mueller, H. Corporate governance, product market competition, and equity prices. J. Financ. 2011, 66, 563–600. [Google Scholar] [CrossRef]

- Coles, J.L.; Li, Z.; Wang, A.Y. Industry Tournament Incentives. Rev. Financial Stud. 2018, 31, 1418–1459. [Google Scholar] [CrossRef]

- Core, J.; Guay, W. The use of equity grants to manage optimal equity incentive levels. J. Account. Econ. 1999, 28, 151–184. [Google Scholar] [CrossRef] [Green Version]

- Li, Z. Mutual monitoring and corporate governance. J. Bank. Financ. 2014, 45, 255–269. [Google Scholar]

- Dyllick, T.; Hockerts, K. Beyond the Business Case for Corporate Sustainability. Bus. Strategy Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Spreitzer, G.; Porath, C.L.; Gibson, C.B. Toward Human Sustainability: How to Enable More Thriving at Work. Organ. Dyn. 2012, 41, 155–162. [Google Scholar] [CrossRef]

- Wilkinson, A.; Hill, M.; Gollan, P. The sustainability debate. Int. J. Oper. Prod. Manag. 2001, 12, 1492–1502. [Google Scholar] [CrossRef]

- Ehnert, I. Sustainability and Human Resource Management: Reasoning and Applications on Corporate Websites. Eur. J. Int. Manag. 2009, 4, 419–438. [Google Scholar] [CrossRef]

- Renwick, D.; Redman, T.; Maguire, D. Green HRM: A Review, Process Model, and Research Agenda. Discussion Paper No 2008.01. The University of Sheffield, April 2008. Available online: https://www.sheffield.ac.uk/polopoly_fs/1.120337!/file/Green-HRM.pdf (accessed on 27 August 2018).

- Jabbour, J.; Santos, F. The Central Role of Human Resource Management in the Search for Sustainable Organizations. Int. J. Hum. Resour. Manag. 2008, 12, 2133–2154. [Google Scholar] [CrossRef]

- Wirtenberg, J.; Harmon, J.; Fairfield, K.D. HR’s Role in Building a Sustainable Enterprise: Insights from Some of the World’s Best. Hum. Resour. Plan. 2007, 30, 10–20. [Google Scholar]

- Spooner, K.; Kaine, S. Defining Sustainability and Human Resource Management. Int. Employ. Relat. Rev. 2010, 2, 70–81. [Google Scholar]

- Obrad, C.; Gherhes, V. A Human Resources Perspective on Responsible Corporate Behavior. Case Study: The Multinational Companies in Western Romania. Sustainability 2018, 10, 726. [Google Scholar] [CrossRef]

- Harmon, J.; Fairfield, K.D.; Wirtenberg, J. Missing an Opportunity: HR Leadership and Sustainability. People Strategy 2010, 33, 16–21. [Google Scholar]

- Glade, B. Human Resources: CSR and Business Sustainability-HR’s Leadership Role. N. Z. Manag. 2008, 9, 51–52. [Google Scholar]

- Jabbour, C.J.C.; Santos, F.C.A.; Nagano, M.C. Environmental Management System and Human Resource Practices: Is there a link between them in four Brazilian Companies? J. Clean. Prod. 2008, 17, 1922–1925. [Google Scholar] [CrossRef]

- Liebowitz, J. The role of HR in achieving a sustainability culture. J. Sustain. Dev. 2010, 3, 50–57. [Google Scholar] [CrossRef]

- Kramar, R. Beyond strategic human resource management: Is sustainable human resource management the next approach? Int. J. Hum. Resour. Manag. 2014, 25, 1069–1089. [Google Scholar] [CrossRef]

- Ehnert, I.; Harry, W.; Zink, K.J. Sustainability and HRM: An introduction to the field. In Sustainability and Human Resource Management: Developing Sustainable Business Organizations; Ehnert, I., Harry, W., Zink, K.J., Eds.; Springer: Heidelberg, Germany, 2014; pp. 3–32. ISBN 978-3-642-37524-8. [Google Scholar]

- Pabian, A. Zrównoważone zarządzanie zasobami ludzkimi. Zarys problematyki. Zesz. Nauk. Politech. Częstochowskiej Zarządzanie 2015, 17, 7–16. (In Polish) [Google Scholar]

- Pocztowski, A. Zrównoważone zarządzanie zasobami ludzkimi w teorii i praktyce. Zarządzanie Finans. 2016, 2, 303–314. (In Polish) [Google Scholar]

- Pabian, A. Sustainable personnel—Pracownicy przedsiębiorstwa przyszłości. Zarządzanie Zasobami Ludzkimi 2011, 5, 9–18. (In Polish) [Google Scholar]

- Cohen, S. Sustainability Management; Columbia University Press: New York, NY, USA, 2011; ISBN 9780231152587. [Google Scholar]

- Majewski, D. Zrównoważeni pracownicy i ich satysfakcja z pracy. Edukacja Ekonomistów i Menedżerów 2012, 2, 155–167. (In Polish) [Google Scholar] [CrossRef]

- Hart, S.L.; Milstein, M.B. Creating sustainable value. Acad. Manag. Executive 2003, 2, 56–67. [Google Scholar] [CrossRef]

- Grudzewski, W.M.; Hejduk, I.K.; Sankowska, A.; Wańtuchowicz, M. Sustainability w Biznesie, Czyli Przedsiębiorstwo Przyszłości: Zmiany Paradygmatów i Koncepcji Zarządzania; Warszawa: Poltext, Poland, 2010; ISBN 978-83-7561-257-8. (In Polish) [Google Scholar]

- Abidin, N.Z.; Pasquire, Ch.L. Revolutionize value management: A mode towards sustainability. Int. J. Proj. Manag. 2007, 25, 275–282. [Google Scholar] [CrossRef]

- Burchard-Dziubińska, M. Zrównoważony biznes-dlaczego tak trudno o sukces? In Przedsiębiorstwo w Warunkach Zrównoważonej Gospodarki; Powichrowska, B., Ed.; Wyższa Szkoła Ekonomiczna: Białystok, Poland, 2011; ISBN 978-83-61247-38-8. (In Polish) [Google Scholar]

- Vickers, M.R. Business Ethics and the HR Role: Past, Present, and Future. Hum. Resour. Plan. 2005, 28, 26–32. [Google Scholar]

- Taylor, S.; Osland, J.; Egri, C.P. Guest Editors’ Introduction: Introduction to HRM’s Role in Sustainability: Systems, Strategies, and Practices. Hum. Resour. Manag. 2012, 5, 789–798. [Google Scholar] [CrossRef]

- Haugh, H.M.; Talwar, A. How Do Corporations Embed Sustainability Across the Organization? Acad. Manag. Learn. Educ. 2010, 9, 384–396. [Google Scholar] [CrossRef]

- Sharma, S.; Sharma, J.; Devi, A. Corporate social responsibility: The key role of human resource management. Bus. Intell. J. 2009, 2, 205–213. [Google Scholar]

- Jang, S.; Ardichvili, A. The Role of HRD in Embedding Corporate Social Responsibility (CSR) in Organizations Working Paper submitted to the 17th International Research Conference on HRD across Europe 2016, Stream: Scholarly Practitioner Research. Available online: https://www.ufhrd.co.uk/wordpress/wp-content/uploads/2016/10/paper_125.pdf (accessed on 30 August 2018).

- Fenwick, T. Corporate Social Responsibility and HRD. In Handbook of Human Resource Development; Chalofsky, N.E., Rocco, T.S., Morris, M.L., Eds.; John Wiley: Hoboken, NJ, USA, 2014; pp. 164–179. ISBN 978-1-118-45402-2. [Google Scholar]

- Pfeffer, J. Building sustainable organizations: The human factor. Acad. Manag. Perspect. 2010, 24, 34–45. [Google Scholar]

- Ardichvili, A. The Role of HRD in CSR, Sustainability, and Ethics a Relational Model. Hum. Resour. Dev. Rev. 2013, 4, 456–473. [Google Scholar] [CrossRef]

- Garavan, T.; McGuire, D. Human resource development and society: Human resource development’s role in embedding corporate social responsibility, sustainability, and ethics in organizations. Adv. Dev. Hum. Resour. 2010, 5, 487–507. [Google Scholar] [CrossRef]

- Wilcox, T. Human Resource Development as an Element of Corporate Social Responsibility. Asia Pac. J. Hum. Resour. 2006, 44, 184–196. [Google Scholar] [CrossRef]

- Inyang, B.J.; Awa, H.O.; Enuoh, R.O. CSR-HRM Nexus: Defining the Role Engagement of the Human Resources Professionals. Int. J. Bus. Soc. Sci. 2011, 5, 118–126. [Google Scholar]

- Boudreau, J.W.; Ramstad, P.M. Talentship. Talent Segmentation and Sustainability: A New HR Decision Science Paradigm for a New Strategy Definition. Hum. Resour. Manag. 2005, 2, 129–136. [Google Scholar] [CrossRef]

- Ehnert, I. Sustainable Human Resource Management: A Conceptual and Exploratory Analysis from a Paradox Perspective; Physica-Verlag: Heidelberg, Germany, 2009; ISBN 978-3-7908-2187-1. [Google Scholar]

- Guest, D.E. Human Resource Management and Performance: Still Searching for Some Answers. Hum. Resour. Manag. J. 2011, 21, 3–13. [Google Scholar] [CrossRef]

- Thom, N.; Zaugg, R. Nachhaltiges und innovatives Personalmanagement: Spitzengruppenbefragung in europäischen Unternehmungen und Institutionen. In Nachhaltiges Innovationsmanagement; Schwarz, E.J., Ed.; Gabler: Wiesbaden, Germany, 2004; pp. 217–245. [Google Scholar]

- Voegtlin, Ch.; Greenwood, M. Corporate social responsibility and human resource management: A systematic review and conceptual analysis. Hum. Resour. Manag. Rev. 2016, 3, 181–197. [Google Scholar] [CrossRef]

- Ardichvili, A. Sustainability of nations, communities, organizations and individuals: The role of HRD. Hum. Resour. Dev. Int. 2011, 4, 371–374. [Google Scholar] [CrossRef]

- Shen, J. Developing the concept of socially responsible international human resource management. Int. J. Hum. Resour. Manag. 2011, 6, 1351–1363. [Google Scholar] [CrossRef]

- Greenwood, M. Ethics and HRM: A review and conceptual analysis. J. Bus. Ethics 2002, 3, 261–278. [Google Scholar] [CrossRef]

- Cooke, F.L.; He, Q.L. Corporate social responsibility and HRM in China: A study of textile and apparel enterprises. Asia Pac. Bus. Rev. 2010, 3, 355–376. [Google Scholar] [CrossRef]

- Dupont, C.; Ferauge, P.; Giuliano, R. The Impact of Corporate Social Responsibility on Human Resource Management: GDF SUEZ’s Case. Int. Bus. Res. 2013, 12, 145–155. [Google Scholar] [CrossRef]

- De Stefano, F.; Bagdadli, S.; Camuffo, A. The HR role in corporate social responsibility and sustainability: A boundary-shifting literature review. Hum. Resour. Manag. 2018, 2, 549–566. [Google Scholar] [CrossRef]

- Jamali, D.R.; Dirani, A.E.; Harwood, I.A. Exploring Human Resource Management Roles in Corporate Social Responsibility: The CSR-HRM Co-creation Model. Bus. Ethics A Eur. Rev. 2015, 2, 125–143. [Google Scholar] [CrossRef]

- Becker, W.S.; Carbo, J.A.; Langella, I.M. Beyond self-interest: Integrating social responsibility and supply chain management with human resource development. Hum. Resour. Dev. Rev. 2010, 2, 144–168. [Google Scholar] [CrossRef]

- Becker, W.S. Are you leading a socially responsible and sustainable human resource function? People Strategy 2011, 34, 18–23. [Google Scholar]

- Preuss, L.; Haunschild, A.; Matten, D. The rise of CSR: Implications for HRM and employee representation. Int. J. Hum. Resour. Manag. 2009, 4, 953–973. [Google Scholar] [CrossRef]

- Garavan, T.N.; Heraty, N.; Rock, A.; Dalton, E. Conceptualizing the behavioral barriers to CSR and CS in organizations: A typology of HRD interventions. Adv. Dev. Hum. Resour. 2010, 5, 587–613. [Google Scholar] [CrossRef]

- Bhattacharya, C.B.; Sen, S.; Korschun, D. Using corporate social responsibility to win the war for talent. Sloan Manag. Rev. 2008, 2, 37–44. [Google Scholar]

- Davies, I.A.; Crane, A. Corporate social responsibility in small-and medium-size enterprises: Investigating employee engagement in fair trade companies. Bus. Ethics A Eur. Rev. 2010, 2, 126–139. [Google Scholar] [CrossRef]

- Gond, J.P.; Igalens, J.; Swaen, V.; El Akremi, A. The human resources contribution to responsible leadership: An exploration of the CSR−HR interface. J. Bus. Ethics 2011, 98, 115–132. [Google Scholar] [CrossRef]

- Wachowiak, P. Wrażliwość Społeczna Przedsiębiorstwa. Analiza i Pomiar; Oficyna Wydawnicza SGH: Warszawa, Poland, 2013; ISBN 978-83-7378-851-0. (In Polish) [Google Scholar]

- Paliszkiewicz, J. Zaufanie w Zarządzaniu; PWN: Warszawa, Poland, 2013; ISBN 978-83-01-19371-3. (In Polish) [Google Scholar]

- Greening, D.W.; Turban, D.B. Corporate social Performance as a competitive advantage in attracting a quality workforce. Bus. Soc. 2000, 39, 254–280. [Google Scholar] [CrossRef]

- Odriozola, M.D.; Martín, A.; Luna, L. The relationship between labour social responsibility practices and reputation. Int. J. Manpow. 2015, 36, 236–251. [Google Scholar] [CrossRef] [Green Version]

- Valentine, S.; Fleischman, G. Ethics programs, perceived corporate social responsibility and job satisfaction. J. Bus. Ethics 2008, 77, 159–172. [Google Scholar] [CrossRef]

- Lindgreen, A.; Swaen, V. Corporate social responsibility. Int. J. Manag. Rev. 2010, 12, 1–7. [Google Scholar] [CrossRef]

- Fapohunda, T.M. The Human Resource Management Dimensions of Corporate Social Responsibility. Eur. J. Res. Reflect. Manag. Sci. 2015, 2, 1–14. [Google Scholar]

- Bombiak, E.; Marciniuk-Kluska, A. Green Human Resource Management as a Tool for the Sustainable Development of Enterprises: Polish Young Company Experience. Sustainability 2018, 10, 1739. [Google Scholar] [CrossRef]

- Rogowski, R. Praktyka wdrażania CSR w polskich przedsiębiorstwach w opinii doradców. Ann. Ethics Econ. Life 2016, 19, 37–54. (In Polish) [Google Scholar] [CrossRef]

- Himmelberg, C.; Hubbard, R. Incentive Pay and the Market for CEOS: An Analysis of Pay-for-Performance Sensitivity (June 2000). Presented at Tuck-JFE Contemporary Corporate Governance Conference; 2000. Available online: https://ssrn.com/abstract=2360891 (accessed on 2 January 2019).

- Dang, C.; Li, F. Measuring Firm Size in Empirical Corporate Finance. J. Bank. Financ. 2018, 86, 159–176. [Google Scholar] [CrossRef]

- Stankevičiūtė, Ž.; Savanevičienė, A. Designing Sustainable HRM: The Core Characteristics of Emerging Field. Sustainability 2018, 10, 4798. [Google Scholar] [CrossRef]

- Raport Odpowiedzialny Biznes w Polsce 2017. Dobre Praktyki. Available online: http://odpowiedzialnybiznes.pl/publikacje/raport-2017/ (accessed on 7 September 2018). (In Polish).

- Wolska, G. Zaangażowanie przedsiębiorstw w realizację koncepcji społecznej odpowiedzialności biznesu. Studia Ekonomiczne. Zeszyty Naukowe Uniwersytetu Ekonomicznego w Katowicach 2015, 236, 85–95. (In Polish) [Google Scholar]

- Furmańska-Maruszak, A.; Sudolska, A. Relacje z pracownikami jako obszar wdrażania CSR. Organ. Kier. 2017, 2, 253–267. (In Polish) [Google Scholar]

- Raport Odpowiedzialny Biznes w Polsce 2016. Dobre Praktyki. Available online: http://odpowiedzialnybiznes.pl/publikacje/raport-2016/ (accessed on 7 September 2018). (In Polish).

- Raport Odpowiedzialny Biznes w Polsce 2011. Dobre Praktyki. Available online: http://odpowiedzialnybiznes.pl/wp-content/uploads/2014/01/Raport2011.pdf (accessed on 7 September 2018). (In Polish).

- Głuszek, E. Wykorzystywanie inicjatyw społecznych w budowaniu atrybutów dobrej reputacji przedsiębiorstwa. Prace Naukowe Uniwersytetu Ekonomicznego we Wrocławiu 2013, 288, 22–36. (In Polish) [Google Scholar]

- Raport Odpowiedzialny Biznes w Polsce 2010. Dobre Praktyki. Available online: http://odpowiedzialnybiznes.pl/wp-content/uploads/2014/02/Raport_odpowiedzialny_biznes_w_Polsce_2010-1301645271.pdf (accessed on 7 September 2018). (In Polish).

- Wojtysiak-Sowa, E. Obowiązkowy Raport CSR? Polskie Firmy nie są na Niego Gotowe! Available online: http://jbcomm.pl/aktualnosci/obowiazkowy-raport-csr-polskie-firmy-nie-sa-na-niego-gotowe/ (accessed on 28 August 2018).

- Ehnert, I.; Parsa, S.; Roper, I.; Wagner, M.; Muller-Camen, M. Reporting on sustainability and HRM: A comparative study of sustainability reporting practices by the world’s largest companies. Int. J. Hum. Resour. Manag. 2016, 27, 88–108. [Google Scholar] [CrossRef]

- Partnerstwo na rzecz realizacji celów zrównoważonego rozwoju w Polsce. Ministerstwo Przedsiębiorczości i Technologii. Available online: https://www.mpit.gov.pl/strony/zadania/zrownowazony-rozwoj/agenda-2030/partnerstwo-na-rzecz-realizacji-celow-zrownowazonego-rozwoju-w-polsce/ (accessed on 24 August 2018).

- Wróbel, M. Raportowanie społecznej odpowiedzialności w Polsce w świetle unormowań Dyrektywy Parlamenty Europejskiego i Rady 2014/95/UE. Zesz. Nauk. Wyższej Szkoły Humanit. Zarządzanie 2016, 2, 83–94. (In Polish) [Google Scholar] [CrossRef]

{kind=link}

| Area | Examples of Practices |

|---|---|

| Employee selection (recruitment, selection, adaptation) | —honest, non-discriminating job offers —ethical job interview —implementation of the “candidate experience” concept —friendly employee adaptation |

| Employee motivation | —generous remuneration —transparent and objective criteria of gratification —timely payment of remunerations —comprehensive social package (extra insurance, healthcare, pension plans) —employee participation in management |

| Employee assessment | —transparency of the system of period performance appraisals —objectivity of evaluation criteria —elimination of errors in the process of periodic appraisals —conduct of constructive assessment interviews |

| Employee development | —investment in employee development —assurance of equal access to training —employee development support (mentoring, coaching) —counseling and support with respect to professional career management |

| Health prophylaxis and work safety | —workshops on coping with stress —training and workshops on healthy eating —vaccinations —health-oriented modifications of working places —sport activities —relax rooms at the workplace —additional health leaves —compliance with periodic health examinations of employees —compliance with the industrial health and safety law —commitment to ergonomic work space design |

| Diversity Management | —integration programmes —equal opportunities programmes —improvements for persons with disabilities —multicultural teams —work-life balance programmes (nonstandard forms of employment, improvements for parents, additional parental leaves) |

| Developing relations and attitudes | —transparent rules of communication —corporate volunteering (voluntary participation in social campaigns) —prevention of mobbing and discrimination —development and implementation of ethical codes |

| Employment restructuring | —dismissal having regard to the values of respect for human dignity and employee rights —just and clear disciplinary procedures —outplacement |

| Activity Number | Activities |

|---|---|

| 1 | Commitment to fairness of one’s employment offer |

| 2 | Commitment to non-discrimination of vacancy advertising, i.e., eliminating elements which could discriminate because of sex, age, appearance, disability, etc. |

| 3 | Employing persons with disabilities |

| 4 | Employing people from the age group of 50 and above |

| 5 | Commitment to good relations with candidates who have not been employed (candidate experience) |

| 6 | Facilitating new employee adaptation |

| 7 | Transparent system of periodic performance appraisals |

| 8 | Investing in employee development |

| 9 | Commitment to equal access to employee training |

| 10 | Supporting employees who are made redundant (helping to find accommodation, psychological support) |

| 11 | Compliance with the industrial health and safety law |

| 12 | Providing generous remuneration |

| 11 | Transparent rules of remuneration |

| 14 | Comprehensive social benefits |

| 15 | Applying solutions facilitating the attainment of a work-life balance (such as flexible working hours) |

| 16 | Ability of employees to co-decide on matters relating to company operation (participation) |

| 17 | Just and clear dismissal procedures |

| 18 | Development and implementation of an ethical code |

| 19 | Conduct of environmental audits |

| 20 | Award of ethical certificates |

| 21 | Cooperating only with those business partners who are certified to be in compliance with ethical requirements |

| 22 | Implementing procedures for combating discrimination, mobbing and harassment at work |

| 23 | Ethical Code training organization |

| 24 | Organization of training sessions on combating discrimination, mobbing and harassment |

| 25 | Promoting a healthy lifestyle and civilization disease prevention among employees |

| 26 | Conducting health-oriented training and workshops (such as coping with stress, etc.) |

| 27 | Financial support for employees with respect to healthy lifestyles (such as money to buy sportswear, sports equipment, gym or swimming-pool memberships, etc.) |

| 28 | Investment in infrastructure promoting a healthy lifestyle (such as bicycle parking stations, healthy food canteens) |

| 29 | Employee involvement in social projects (aiding shelters, renovating preschools) as part of corporate volunteering |

| 30 | Adjustment of working conditions to meet the needs of various employee groups (such as people from the age group of 50 and above, the disabled) |

| 31 | Inclusion of social goals of HRM in company strategy |

| 32 | Measurement of effectiveness of environmental actions in HRM |

| 33 | Provision for socially responsible HRM activities-related expenditure in the budget |

| 34 | HRM socially responsible action progress monitoring |

| 35 | Drafting reports on social responsibility in HRM |

| Criterion | Number of Enterprises | Percentage |

|---|---|---|

| Time on the market: | ||

| up to 1 year | 14 | 9.3 |

| 1–3 years | 136 | 90.7 |

| Employment number: | ||

| 50–249 employees | 100 | 66.7 |

| 250–499 employees | 42 | 28.0 |

| More than 500 employees | 8 | 5.3 |

| Main type of activity: | ||

| production | 43 | 28.7 |

| services | 99 | 66.0 |

| trade | 8 | 5.3 |

| Scope of operations | ||

| local | 37 | 24.7 |

| regional | 20 | 13.3 |

| national | 44 | 29.3 |

| international | 49 | 32.7 |

| Respondent’s position: | ||

| HR Director | 8 | 5.3 |

| Head of HR Department | 126 | 84.0 |

| CEO | 12 | 8.0 |

| other | 4 | 2.7 |

| Activity No. | Total (Points) | The Average Strength of the Relation (Points) | Mode (Points) | Median (Points) | Standard Deviation (Points) | Coefficient of Variation (Points) | Strength of Asymmetry (Points) | Kurtosis (Points) |

|---|---|---|---|---|---|---|---|---|

| 11 | 725 | 4.83 | 5 | 5 | 0.424 | 8.78 | −0.39 | 6.24 |

| 2 | 690 | 4.6 | 5 | 5 | 0.835 | 18.16 | −0.48 | 6.12 |

| 6 | 672 | 4.48 | 5 | 5 | 0.739 | 16.50 | −0.70 | 5.13 |

| 13 | 667 | 4.45 | 5 | 5 | 0.710 | 15.96 | −0.78 | 2.66 |

| 1 | 654 | 4.36 | 5 | 5 | 0.813 | 18.65 | −0.79 | 2.99 |

| 9 | 649 | 4.33 | 5 | 5 | 0.901 | 20.83 | −0.75 | 2.92 |

| 8 | 646 | 4.31 | 5 | 4 | 0.835 | 19.39 | −0.83 | 2.47 |

| 12 | 643 | 4.29 | 5 | 4 | 0.814 | 18.98 | −0.88 | 0.63 |

| 17 | 617 | 4.11 | 5 | 4 | 1.053 | 25.59 | −0.84 | 1.47 |

| 14 | 604 | 4.03 | 5 | 4 | 1.080 | 26.83 | −0.90 | 0.83 |

| 22 | 593 | 3.95 | 5 | 4 | 1.200 | 30.36 | −0.87 | 0.50 |

| 7 | 583 | 3.89 | 5 | 4 | 1.207 | 31.06 | −0.92 | 0.23 |

| 4 | 568 | 3.79 | 5 | 4 | 1.097 | 28.96 | −1.11 | −0.11 |

| 18 | 561 | 3.74 | 5 | 4 | 1.353 | 36.18 | −0.93 | −0.50 |

| 3 | 553 | 3.69 | 5 | 4 | 1.221 | 33.13 | −1.08 | −0.37 |

| 5 | 546 | 3.64 | 4 | 4 | 1.166 | 32.03 | −0.309 | −0.17 |

| 30 | 535 | 3.57 | 3 | 4 | 1.228 | 34.44 | 0.46 | −0.53 |

| 31 | 531 | 3.54 | 3 | 4 | 1.145 | 32.34 | 0.47 | 0.03 |

| 16 | 518 | 3.45 | 3 | 3 | 1.267 | 36.69 | 0.36 | −0.70 |

| 15 | 500 | 3.33 | 3 | 3 | 1.278 | 38.34 | 0.26 | −0.62 |

| 25 | 495 | 3.30 | 3 | 3 | 1.309 | 39.68 | 0.23 | −0.72 |

| 24 | 460 | 3.07 | 3 | 3 | 1.299 | 42.35 | 0.05 | −0.86 |

| 27 | 459 | 3.06 | 3 | 3 | 1.352 | 44.19 | 0.04 | −0.96 |

| 28 | 451 | 3.01 | 3 | 3 | 1.363 | 45.35 | 0.00 | −1.04 |

| 26 | 443 | 2.95 | 3 | 3 | 1.372 | 46.47 | −0.03 | −1.06 |

| 19 | 439 | 2.93 | 3 | 3 | 1.296 | 44.28 | −0.06 | −0.84 |

| 33 | 438 | 2.92 | 3 | 3 | 1.282 | 43.92 | −0.06 | −0.84 |

| 23 | 432 | 2.88 | 3 | 3 | 1.295 | 44.96 | −0.09 | −0.97 |

| 34 | 425 | 2.83 | 3 | 3 | 1.255 | 44.31 | −0.13 | −0.82 |

| 29 | 423 | 2.82 | 3 | 3 | 1.336 | 47.39 | −0.13 | −1.03 |

| 32 | 417 | 2.78 | 3 | 3 | 1.268 | 45.63 | −0.17 | −0.85 |

| 10 | 416 | 2.77 | 3 | 3 | 1.275 | 45.98 | −0.18 | −0.86 |

| 35 | 405 | 2.70 | 3 | 3 | 1.225 | 45.36 | −0.24 | −0.87 |

| 20 | 362 | 2.41 | 3 | 3 | 1.275 | 52.85 | −0.46 | −0.92 |

| 21 | 360 | 2.40 | 3 | 3 | 1.221 | 50.86 | −0.49 | −0.93 |

| Activity No. | Number of Young Enterprises Performing the Activity | Percentage of Young Enterprises Performing the Activity (%) |

|---|---|---|

| 1 | 147 | 98.00 |

| 2 | 143 | 95.33 |

| 3 | 113 | 75.33 |

| 4 | 129 | 86.00 |

| 5 | 119 | 79.33 |

| 6 | 146 | 97.33 |

| 7 | 120 | 80.00 |

| 8 | 142 | 94.67 |

| 9 | 142 | 94.67 |

| 10 | 47 | 31.33 |

| 11 | 149 | 99.33 |

| 12 | 141 | 94.00 |

| 13 | 147 | 98.00 |

| 14 | 130 | 86.67 |

| 15 | 96 | 64.00 |

| 16 | 112 | 74.67 |

| 17 | 130 | 86.67 |

| 18 | 105 | 70.00 |

| 19 | 50 | 33.33 |

| 20 | 25 | 16.67 |

| 21 | 23 | 15.33 |

| 22 | 119 | 79.33 |

| 23 | 62 | 41.33 |

| 24 | 77 | 51.33 |

| 25 | 86 | 57.33 |

| 26 | 68 | 45.33 |

| 27 | 71 | 47.33 |

| 28 | 64 | 42.67 |

| 29 | 56 | 37.33 |

| 30 | 97 | 64.67 |

| 31 | 106 | 70.67 |

| 32 | 56 | 37.33 |

| 33 | 66 | 44.00 |

| 34 | 62 | 41.33 |

| 35 | 49 | 32.67 |

| Activity No. | The Assessment of the Strength of the Relation 1 (Variable X) | Activities Pursued in Enterprises 2 (Variable Y) | Rank X 3 | Rank Y 4 | Di Distance | Square of Distance di 2 |

|---|---|---|---|---|---|---|

| 1 | 654 | 147 | 5 | 2 | 3 | 9 |

| 2 | 690 | 143 | 2 | 5 | −3 | 9 |

| 3 | 553 | 113 | 15 | 15 | 0 | 0 |

| 4 | 568 | 129 | 13 | 11 | 2 | 4 |

| 5 | 546 | 119 | 16 | 13 | 3 | 9 |

| 6 | 672 | 146 | 3 | 4 | −1 | 1 |

| 7 | 583 | 120 | 12 | 12 | 0 | 0 |

| 8 | 646 | 142 | 7 | 6 | 1 | 1 |

| 9 | 649 | 142 | 6 | 7 | −1 | 1 |

| 10 | 416 | 47 | 32 | 33 | −1 | 1 |

| 11 | 725 | 149 | 1 | 1 | 0 | 0 |

| 12 | 643 | 141 | 8 | 8 | 0 | 0 |

| 13 | 667 | 147 | 4 | 3 | 1 | 1 |

| 14 | 604 | 130 | 10 | 9 | 1 | 1 |

| 15 | 500 | 96 | 20 | 20 | 0 | 0 |

| 16 | 518 | 112 | 19 | 16 | 3 | 9 |

| 17 | 617 | 130 | 9 | 10 | −1 | 1 |

| 18 | 561 | 105 | 14 | 18 | −4 | 16 |

| 19 | 439 | 50 | 26 | 31 | −5 | 25 |

| 20 | 362 | 25 | 34 | 34 | 0 | 0 |

| 21 | 360 | 23 | 35 | 35 | 0 | 0 |

| 22 | 593 | 119 | 11 | 14 | −3 | 9 |

| 23 | 432 | 62 | 28 | 27 | 1 | 1 |

| 24 | 460 | 77 | 22 | 22 | 0 | 0 |

| 25 | 495 | 86 | 21 | 21 | 0 | 0 |

| 26 | 443 | 68 | 25 | 24 | 1 | 1 |

| 27 | 459 | 71 | 23 | 23 | 0 | 0 |

| 28 | 451 | 64 | 24 | 26 | −2 | 4 |

| 29 | 423 | 56 | 30 | 29 | 1 | 1 |

| 30 | 535 | 97 | 17 | 19 | −2 | 4 |

| 31 | 531 | 106 | 18 | 17 | 1 | 1 |

| 32 | 417 | 56 | 31 | 30 | 1 | 1 |

| 33 | 438 | 66 | 27 | 25 | 2 | 4 |

| 34 | 425 | 62 | 29 | 28 | 1 | 1 |

| 35 | 405 | 49 | 33 | 32 | 1 | 1 |

| Sum | - | - | - | - | - | 116 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bombiak, E.; Marciniuk-Kluska, A. Socially Responsible Human Resource Management as a Concept of Fostering Sustainable Organization-Building: Experiences of Young Polish Companies. Sustainability 2019, 11, 1044. https://doi.org/10.3390/su11041044

Bombiak E, Marciniuk-Kluska A. Socially Responsible Human Resource Management as a Concept of Fostering Sustainable Organization-Building: Experiences of Young Polish Companies. Sustainability. 2019; 11(4):1044. https://doi.org/10.3390/su11041044

Chicago/Turabian StyleBombiak, Edyta, and Anna Marciniuk-Kluska. 2019. "Socially Responsible Human Resource Management as a Concept of Fostering Sustainable Organization-Building: Experiences of Young Polish Companies" Sustainability 11, no. 4: 1044. https://doi.org/10.3390/su11041044