Investment Valuation Model of Public Rental Housing PPP Project for Private Sector: A Real Option Perspective

1

School of Economics and Management, Tongji University, Shanghai 200092, China

2

Institute of Remote Sensing and Digital Earth, Chinese Academy of Sciences, Beijing 100101, China

3

University of Chinese Academy of Sciences, Beijing 100049, China

*

Author to whom correspondence should be addressed.

Sustainability 2019, 11(7), 1857; https://doi.org/10.3390/su11071857

Submission received: 4 March 2019

/

Revised: 20 March 2019

/

Accepted: 25 March 2019

/

Published: 28 March 2019

(This article belongs to the Special Issue Sustainable Habitat)

Abstract

:Public rental housing (PRH) in China is mainly invested by the government at present. The huge capital demand brings it great pressure and a series of problems appear meanwhile. Public–private partnership (PPP) has been regarded as a way to solve the funding dilemma of PRH. However, the PRH project is not attractive for the private sector since the expected profit seems unsatisfactory based on traditional valuation methods. To improve this situation, this paper proposed an investment valuation model from a real option perspective. For the private sector, three types of options, including deferral option, abandonment option, and expansion option, were identified during the concession period of a PRH PPP project. On this basis, a two-stage binomial tree model was constructed for estimating the investment value. Then, the proposed model was tested in a hypothetical example of a typical PRH PPP project in Chongqing, China. The result shows that great potential value can be excavated through flexible strategies and adaption to uncertainties. This paper provides a deep analysis on the gaps of the real option application in public housing investment assessment, which is meaningful for improving the supply efficiency and financial sustainability of PRH.

1. Introduction

Public rental housing (PRH) is one new type of affordable housing in China renting to medium–low-income groups at a below-market price [1,2,3]. Recently, it has been gradually developing into a national strategy and been vigorously promoted. At present, PRH is mainly invested by the government and huge capital demand brings it great pressure. A series of problems appear such as financial deficit of local government, high construction costs, and supply inefficiency of PRH, which need to be solved urgently. Public–private partnership (PPP) has been broadly regarded as a way to involve the private sector with abundant capital and managerial experience to share the financial burden of the government [4,5,6,7] and improve the supply efficiency and sustainability of PRH. Accordingly, since 2015, the Chinese central government has encouraged the adoption of PPP to absorb social resources for PRH development [8].

Although a series of incentives (e.g., land supply and tax relief) has been released to promote PPP adoption in the delivery of PRH, few private enterprises are active to invest in PRH projects. One of the main reasons is that their investment decision-making is mainly based on traditional valuation methods to a large extent [9]. In the investment valuation of a PPP project, conventional methods, particularly the net present value (NPV) method, are the most widely used [10]. However, due to high uncertainties of PPP projects, this kind of method is unable to scientifically evaluate the real value of a PRH PPP project for ignoring the impact of financial uncertainty on the project [11]. The rent of PRH is lower than market rent, so the investment return seems not satisfactory based on traditional valuation methods. Additionally, compared with traditional outsourcing, privatization, and public procurement projects, PPP projects may involve more kinds or higher level of risk [12,13,14]. This “high risk and low returns” makes a PRH PPP project lack attractiveness to the private sector.

The real option approach (ROA) is a modern investment decision approach that can explore the project’s potential opportunity value brought by uncertainties via flexible management. In the real option theory, the risk of the project can be reduced by changing the exposure to external uncertainties through flexible strategies [15]. It provides the investor an idea of dynamic decision making, and helps to find out the optimal investment strategies for value added of the project. In this paper, the real option viewpoint is introduced into the investment valuation of a PRH PPP project for the private sector. It can provide a novel perspective for the investment valuation of the PRH PPP project with theoretical guiding significance to some extent to promote the private sector’s confidence to participate in PRH provision, thus alleviating government financial pressure and improving the supply efficiency and sustainability of the PRH project.

2. Literature Review

2.1. PPP Ideology for Affordable Housing Financing

The private sector has capital and professional advantages, as it can share risk with the public sector, reduce operation cost, and improve service quality [16,17]. It is widely considered to be beneficial to the improvement of the provision of affordable housing. Recently, private enterprises are encouraged worldwide to provide affordable housing. As mentioned by Blessing (2015), affordable housing provision has been moved further into the private realm [18]. Many scholars have paid attention to this aspect of research. For example, Vale and Freemark (2012) stated that public housing in the United States has gradually transformed from sole public efforts to a public–private endeavor [19]. Lima (2017) analyzed the social housing elaboration and implementation in Brazil and noted the prominent role of private sectors in the development of social housing [20].

Given the important role of private sector, the “PPP ideology” has been seen as a strategy to provide affordable housing without adding public debt and actively explored by scholars in this field from all over the world. For instance, Kwofie et al. (2016) identified the critical success factors that influence PPP public housing delivery in Ghana [21]. Guarini and Battisti (2017) established a feasibility assessment model for social housing PPP project in Italy [22]. Sani et al. (2018) investigated the impact factors affecting the implementation of PPP housing scheme for providing affordable housing in Bauchi State, Nigeria [23]. Bockman (2018) studied the impact of PPP on American public housing via a case study [24]. Regarding Chinese researchers, Yuan et al. (2012) proposed the methodology of quantitative SWOT analysis and studied the strategy for Chinese government to develop public housing PPP project [25]. Yuan et al. (2018) established a conceptual model of operation performance indicator for PRH delivery by PPP [8].

2.2. Investment Valuation Methods of PPP Project

Investment valuation of a PPP project is conventionally done using traditional tools based on Discounted Cash Flow (DCF) analysis and utilizing indicators such as Net Present Value (NPV) and Internal Rate of Return (IRR). These tools are based on the assumption of reversible investments, certain evolution of future cash flows, passive management, and so on [26]. Looking at investment in a static way, these methods are limited in the investment valuation of a long-term project [27]. The disadvantages of these traditional tools have been increasingly recognized [28,29,30]. By contrast, ROA is accepted as a theoretically superior tool compared to traditional approaches when irreversibility, uncertainty, and managerial flexibility come into play [31,32,33]. It can help capture optimal investment timing according to changes caused by uncertainties [34,35].

Since a PPP project has the nature of numerous uncertainties, long payback period, and large amount of investment [12], the impact associated with such high uncertainties on future cash flows cannot be ignored. Traditional investment philosophy holds that high uncertainty is likely to cause investment losses to a large extent which somewhat ignores the investor’s ability to recognize and utilize opportunities for value added of the project [36]. In the viewpoint of real option, the greater the project uncertainty, the greater the potential opportunity value of the project [37,38]. If the managerial flexibility can be fully used, higher value can be created. Real option theory provides an innovative decision-making concept and analytical thinking for high-risk investment projects under an uncertain environment. It has become a new topic in the investment valuation of PPP projects [39].

2.3. Real Option Theory and Its Application

The real option theory was first put forward by Myers [40]. Real option is a right rather than an obligation for the holder to take a share affecting a real asset at a fixed cost during a specific time [28]. Real option theory acknowledges managerial flexibility and strategic adaptability to adjust an investment project under future uncertainties to maintain or enhance its profitability [41]. Generally, real option can be classified into six different types, including deferral option, growth option, expansion option, contraction option, switch option, and abandonment option [42,43]. Deferral option refers to the right to postpone investment until necessary information for decision-making is acquired [28]. Growth option refers to the right to take advantage of new investment opportunities in the future after a successful initial investment [44]. Expansion option or contraction option allows the investor to expand or scale back the project respectively [41]. Switch option refers to the right to switch the investment to an alternative usage and adjust the inputs or outputs to maximize the project value according to the change of external environment [45]. Abandonment option implies to stop or sell the project to avoid further losses [41].

Many scholars have applied the real option theory to real estate investment field. Among them, Titman (1985) first introduced real option theory into the real estate field and used ROA to the valuation of undeveloped land [46]. Baldi (2013) applied ROA to the investment estimation for a new and multi-purpose building in Roma [47]. Čirjevskis and Tatevosjans (2015) empirically examined ROA application in real estate market [48]. Mintah et al. (2018) valued the option embedded in residential projects by using ROA and compared with the results from traditional DCF method [49]. This theory has even been applied to the PRH investment field by very few scholars. For instance, Li et al. (2014) established a real option based valuation model for a privately owned PRH project [9]. Li et al. (2016) assessed the investment value of a privately owned PRH project with multiple options [50].

Recently, real option theory has been widely applied to the PPP field as well. For example, Liu et al. (2014) constructed a valuation model for the guarantee of restrictive competition in PPP projects using ROA [51]. Xiong and Zhang (2016) regarded the renegotiations in PPP projects as real options, and built a real option based model to solve the value of renegotiation [52]. Using real option theory, Liu et al. (2017) studied the pricing mechanisms for early termination of a PPP project under two scenarios of excessively low or excessively high cash flows [53]. Ma et al. (2018) analyzed the distribution of option value in a PPP project by utilizing game theory combined with risk sharing [54].

By reviewing the literature, it can be concluded that PPP has been widely seen as a strategy to provide affordable housing and ROA is considered to be more proper for the investment valuation of PPP project. The research of real option theory in the domain of real estate and PPP project has accumulated rich achievements, while very few researchers have applied it to the field of PRH projects. Stage differences in the life cycle of the PRH project are not considered in the existing literature on the application of ROA in the PRH project. Current research on the application of real option theory is mainly for general PPP projects where differences of specific PPP projects are not well considered. Based on these discoveries, introducing ROA into the investment valuation of the PRH PPP project in China is of great significance but yet to gain attention. In this paper, we address this knowledge gap by establishing an investment valuation model of a PRH PPP project from a real option perspective. According to the stage characteristics of the PRH PPP project, the model is divided into two stages and three types of options are identified so that decision flexibility at each stage can be reflected. The two-stage compound option model will be elaborated in the next section.

3. Investment Valuation Model of a PRH PPP Project

In this section, the investment valuation model of a PRH PPP project for private sector is established from a real option perspective. The main structure of this section is designed as follows:

- (1)

- Option pricing model selection for a PRH PPP project. This subsection describes and compares two fundamental option pricing models in the real option theory, and then the binomial model is selected for the valuation model construction of a PRH PPP project. Considering the representativeness of the model, other derivative option pricing models are not included for selection.

- (2)

- Real option identification during the concession period of a PRH PPP project. In this subsection, the concession period of the PRH PPP project is divided into two stages. Then, the types of real options contained in the two stages are identified according to the stage characteristics of the PRH PPP project. In this way, the stage differences during the concession period of the PRH PPP project are considered.

- (3)

- Investment value composition of a PRH PPP project. This subsection explains the composition of the investment value of the PRH PPP project by adopting the concept of Expanded NPV. It means that from the real option perspective, the investment value is made up of the static NPV (SNPV) and the real option value (ROV). The solving formula of SNPV is shown in this part.

- (4)

- Real option pricing model of a PRH PPP project. Based on the first two subsections, a two-stage compound option pricing model of the PRH PPP project is established for solving the option value in this part. Then, the investment value of the PRH PPP project can be estimated according to this part combined with the third subsection.

3.1. Option Pricing Model Selection for a PRH PPP Project

The first task of the investment valuation of a PRH PPP project is to select a proper option pricing model for real option analysis. In the real option theory, there are two classical option pricing models, namely the Black–Scholes (B-S) model [55] and the binomial model [56]. Among these two models, the B-S model allows deducing option price by using a partial differential equation, while it can only model one or at most two correlated uncertainties, causing it difficult to apply in real life projects [26]. Furthermore, the B-S model simply values European-style options that can only be exercised at the time when the options expire, i.e., at a specified date. It cannot estimate American-style options where decisions can be taken at any time during the life-cycle of the project. As to the PRH PPP project with long cooperation period, options in it can be exercised at any time before expiration, provided that it can create added value for the project. Hence, it is not proper to apply the B-S model to value the PRH PPP project.

As a solution for addressing American-style options, the binomial model can evaluate the value in executing an option before expiration. It has been regarded as the most generic, intuitive, and flexible approach in valuing real options [57]. Studies on computational efficiency have suggested a preference for the binomial approach in the value estimation of long-term American-style options [31]. Compared with the B-S model, the binomial model is more applicable for complicated types of real options and can better reveal the economic intuition underlying the decision-making process [58]. In the PRH PPP project, the private sector actually has different types of American-style options in different stages of the project. Therefore, the binomial model is selected for the investment evaluation of a PRH PPP project herein.

3.2. Real Option Identification during the Concession Period of a PRH PPP Project

Another important process of the investment analysis is to identify the types of options contained in different stages of the concession period of a PRH PPP project. In Section 2.3, we have mentioned six typical types of real option. Among these options, the growth option is usually embedded in the newly developed industries, such as R&D and high tech projects with multiple generations of products [59]; while the switch option is a right for the investor to change the input materials or output products, generally appearing in the industries with high substitutability for inputs and outputs such as flex-fuel vehicles [41]. In this case, the studied PPP project has been already determined to provide PRH, and other types of products are beyond the scope of this paper. Thus, the growth option and switch option are not considered herein.

According to the operation process of PPP project, the life-cycle of a PRH PPP project can be divided into four stages [60]: (1) approval and bidding stage; (2) construction stage; (3) operation stage; (4) post transfer stage. The approval and bidding stage involves the tasks of feasibility study, tendering and bidding and concession negotiation, etc., which are almost all government-led. When it arrives at the post transfer stage, the investor has to transfer the project to the government free of charge. Thus, only the construction stage and operation stage are included in the concession period when the private sector is given the privilege granting it investment flexibility to some extent [60].

In the construction stage, the main work is carried out by the private investor, including contract negotiation, project financing, construction, etc. At this stage, when facing uncertainties, it is often necessary for the investor to make a systematic evaluation of the project and decide whether construction should be carried out immediately. When the macro environment or technical condition of the project is not ideal, the investor can adopt the strategy of delaying and wait for the investment condition to be improved in the contract duration, so he has a deferral option at this stage. When the implementation of the project is difficult to continue due to extreme deterioration of funds or problems in financing, the investor can also execute an abandonment option returning the project to the government to obtain a certain amount of residual compensation.

In the operation stage, the private sector reclaims investment costs and obtains benefits by operating and maintaining the project [61]. Due to the social welfare nature and huge demand of PRH, the construction of PRH has obvious purpose of public interests. Besides this, thanks to the product nature of PRH, earlier operation can recover more costs. Therefore, we do not consider the deferral option here. When the market condition is not ideal, it is usually difficult for the investor to find other operators to reduce the operation scale by partial transferring or leasing the project. In response to this situation, the government usually gives the investor a guaranteed return negotiated in the concession agreement. Hence, the contraction option is ignored herein. When the future demand of PRH is increasing, the investor is usually encouraged to expand the project scale within the scope of the concession agreement to settle more medium–low income people and obtain more income at the same time, so the expansion option is considered at this stage. In addition, the investor can execute an abandonment option transferring the project to the government when unable to maintain the project operation.

In summary, the types of real options considered in this paper during the concession period are as follows: (1) abandonment option and deferral option in the construction stage; and (2) expansion option and abandonment option in the operation stage.

3.3. Investment Value Composition of a PRH PPP Project

As mentioned above, the traditional NPV approach has defects in considering uncertainty and management flexibility. Nevertheless, as one of the most widely used pricing methods, the NPV approach has some irreplaceable advantages in reflecting the static value of the project. ROA is considered to be a further inheritance and development rather than total negation of traditional tools [37]. Trigeorgis (2005) proposed the concept of Expanded NPV (ENPV), which organically combines the NPV approach and ROA [45]. Based on this concept, the investment value of the project is the sum of the static NPV and the real option value:

Expanded NPV (ENPV) = Static NPV (SNPV) + Real Option Value (ROV)

In this formula, ENPV is equivalent to the investment value of the project with flexibility, SNPV means the value of the project without flexibility, and ROV can be seen as the value of managerial flexibility. In the light of this formula, the uncertainties and flexibility contained in the investment are considered. The concept of ENPV has been widely used in real option analysis recently [37,58,62,63]. Accordingly, we adopt this formula in this paper to value the PRH PPP project. That is to say, from the real option perspective, the investment value of a PRH PPP project is composed of two parts: SNPV and ROV. SNPV can be calculated by Formula (2) where t is the time of the cash flow, ic is the discount rate, and CIt and COt are cash inflow and cash outflow at time t, respectively. The calculation model of ROV will be established in the next section.

3.4. Real Option Pricing Model of a PRH PPP Project

3.4.1. Binomial Option Pricing Model

In Section 3.1, we selected the binomial model for the investment valuation of the PRH PPP project. The binomial model is a discrete numerical option pricing approach based on scenario analysis and an n-steps binomial tree for calculating ROV [58]. In this model, there are five main variables affecting the pricing of real options: (1) underlying asset value of the project S; (2) execute price of real options X; (3) maturity time of real options T; (4) risk-free interest rate r; (5) volatility associated with the underlying asset σ.

- (a)

- calculation of the binomial lattice of the underlying asset value;

- (b)

- calculation of real options valuation lattice via recursive backward induction.

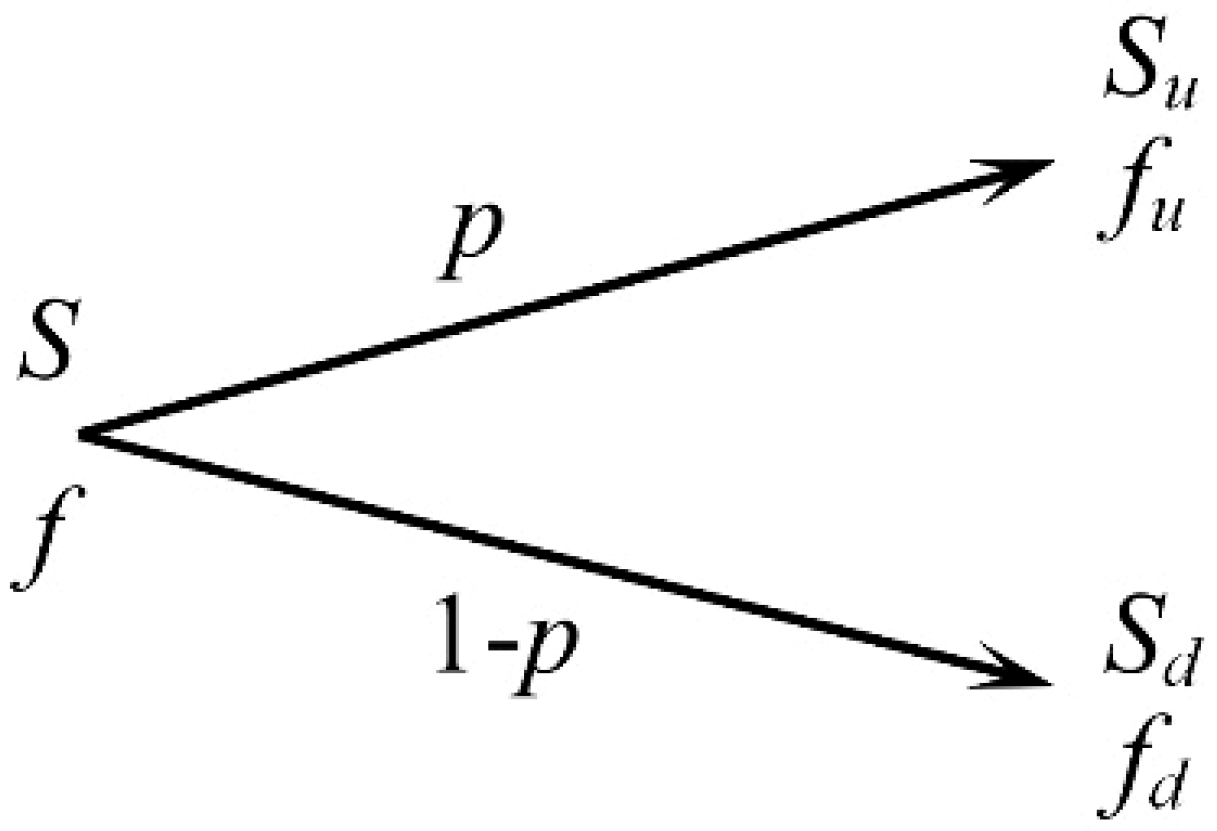

In the first step, we establish the binomial tree of the underlying asset value (see Figure 1) and proceed from the initial node (S00) on the very left side of the binomial tree. The binomial tree can be divided into a number of single-period binomial trees. In the single-period binomial tree (see Figure 2), it can be assumed that there are only two cases where the underlying asset value goes up and down when the time interval (t) is short enough [50]. Let the underlying asset value of the initial node of the single-period binomial tree is S, and the corresponding option value is f. The underlying asset values after going up and going down are Su and Sd respectively, and the corresponding option values are fu and fd. p and 1-p denote the probabilities for value going up and going down respectively. u and d are rising and decreasing factors (u > 1, d < 1). When the volatility σ and time interval t are known, u and d can be calculated as follows:

Then Su and Sd can be calculated:

As long as the initial value of the underlying asset S00 is known, we can extend the single binomial tree to the multi-stage binomial tree model, and the underlying asset value in each tree node Snj can be calculated.

The second step is to create the binomial tree of the ROV (see Figure 3). According to a certain decision rule of value maximization and possible state values of the underlying asset, ROV at each final node of the binomial tree, i.e., fnj (j = 0, 1, …, n + 1), can be obtained. The decision rule of value maximization is based on a maximization function works by comparing every possible scenario in the option exercise period, which will be mentioned in the next section. In this step, the probabilities for the value to increase or decrease (p and 1-p) can be computed by a risk-neutral measure:

It is worth pointing out that, in the general binomial tree model for option analysis, there is another variable called the continuous dividend payout δ which also affects the parameter p [58]. Considering its tiny impact, it is often not considered by scholars applying the binomial model [28,30,33,58]. It is considered reasonable to price European and American options [31]. Thus, δ is not included in Formula (7).

After obtaining the value of p, ROV at each intermediate node can be calculated from the option values of the latter two nodes according to the formula as follows:

By backward-recursion from the final nodes and according to Formula (8), ROV at the initial node of the binomial tree (i.e., f00) can be obtained, which is considered to be the ROV of the project.

3.4.2. Binomial Tree Model of a PRH PPP Project

In this part, the aforementioned binomial tree model is used here for the investment valuation of a PRH PPP project. To establish an n-steps binomial tree for solving the ROV of a PRH PPP project, it is necessary to divide the concession period into n periods. It is set that the validity period of the compound options (i.e., concession period) is T, then the duration of each period of the binomial tree is t = T/n. We construct a two-stage binomial tree model for a PRH PPP project here (see Figure 4).

In this model, the investor has two choices at each node: holding option or executing option. If the investor executes an option, he can obtain the option exercise value. The exercise value of the abandonment option, deferral option, and expansion option at each node can be marked as fnjAbandon, fnjDefer and fnjExpand here. The solving of the exercise value of each type of real option will be described in Section 3.4.3. If the investor gives up executing options (i.e., holding options) at the intermediate nodes of the model, he still holds the option value (known as the continuation value, marked as fnjContinue) which can be calculated by Formulas (7) and (8); while at the terminal nodes of the model, since all the options expire, fnjContinue = 0. According to the decision rule of value maximization, the ROV of each nodes of the binomial tree can be obtained: fnj = max (fnjAbandon, fnjDefer, fnjContinue, 0) in the construction stage; fnj = max (fnjAbandon, fnjExpand, fnjContinue, 0) in the operation stage.

According to the corresponding option value at each node and the decision rule of value maximization, by backward-recursion from the final nodes of the tree, we can get the ROV at the initial node of the binomial tree (f00), that is the ROV of the PRH PPP project created by managerial flexibility.

3.4.3. Exercise Value of Real Options

(1) Exercise value of abandonment option

When the investor cannot continue the project, he can choose to execute an abandonment option, like at the nodes f12, f23, and f45 in Figure 4. The abandonment option is a put option, whose execute price at each node (marked as XnjAbandon) is the liquidation value of the project. If the investor chooses to abandon the project, he can get the liquidation value as compensation, which is set to be measured by k (i.e., compensation factor, k < 1) times of the actual cumulative investment cost at each node (marked as Cnj), that is to say, it can be measured:

The exercise value of abandonment option can be obtained as follows:

(2) Exercise value of deferral option

In the construction stage, when facing strong uncertainties or poor investment environment, the investor can execute a deferral option instead of immediately carrying out the construction, like at the nodes f12 and f22 in Figure 4. According to China’s relevant law of real estate management, the developer needs to begin construction within one year after obtaining the land use right; otherwise, land idle fees will be levied. On this basis, the maturity time of deferral option is set as one year herein. The deferral option is a call option whose execute price at each node (marked as XnjDefer) is the sum of the present value of the cash outflow after one-year postponement from each node, that is:

The exercise value of deferral option can be obtained as follows:

(3) Exercise value of expansion option

In the operation stage, when the investment return is promising, the investor can execute an expansion option, like at the nodes f31, f41, and f42 in Figure 4. The expansion option is a call option whose execute price is the additional investment cost for scale expansion (marked as CnjExpand). Set x is the expansion coefficient, then the execute price of the expansion option can be measured:

The exercise value of expansion option can be obtained as follows:

4. Hypothetical Example

4.1. Project Profile

To verify the effectiveness of the proposed model, a hypothetical case study was conducted choosing a typical PRH PPP project. It is worth pointing out that using hypothetical examples is a standard process in the real option related literature [9,50,64,65,66]. Chongqing is one of the cities whose PRH coverage is the largest and the development of PRH is the most mature in China. We selected the “Muer Airport Paradise” PRH project, located in Yubei District, Chongqing, as a case to carry out the investment value analysis. The project is a modern community with 80 high-rise buildings containing about 29 thousand suites of PRH. PPP is adopted in this project, that is, the government provides some designated land and funds for the construction of PRH, while the private sector obtains the construction and management right of the project via bidding competition. The project has been successfully completed, hence the case study is a hypothetical example designed on the basis of some real data of the project, assuming that the project has just started.

4.2. Basic Data

We assume that the “Muer Airport Paradise” PRH project was launched in early 2018, and private enterprise A was determined as the investor. The duration of the approval and bidding stage is one year, while that of the construction stage and operation stage is two years and 20 years respectively. Main building indicators and financial indicators are extracted from the feasibility study of this project and shown in Table 1 and Table 2. In Table 1, residential area represents the building area of PRH, while commercial area means the building area for commercial use. In Table 2, special financial funds are provided by the government as an incentive for the project, while enterprise capital contribution means the capital provided by enterprise A directly. The rest of investment is financed through bank loans. As the result of policy incentives, the financing interest rate is 4.41%. The repayment is made over the first 10 years of the operation stage according to the average capital plus interest method which means that the repayment of the loan capital and interest is at an equal amount per year within the repayment period. The construction stage is from early 2019 to the end of 2020. The investment volume is assumed to be equal in each year of this stage which can be calculated as 2908.4346 million CNY respectively in 2019 and 2020. The capital provided by enterprise A directly in each year of this stage is 290.8435 million CNY, which accounts for 10% of the investment volume. The operation stage is from early 2021 to the end of 2040 when the investor needs to repay 365.9398 million CNY of the capital and interest to the bank in each year of the first 10 years. Note that, according to the average capital plus interest method, the repayment amount per year can be deduced: . In this equation, A is the total amount of the loan; β is the financing interest rate; m is the repayment period (unit: year). The amount of 365.9398 million CNY is calculated by this equation. The deduction process of this equation can be found at the website: https://www.cnblogs.com/hanganglin/p/6777838.html.

4.3. Cash Flow Analysis of the Project

4.3.1. Analysis of Cash Inflow

The cash inflow of this project is mainly composed of the rental income of PRH, commercial facilities, and parking spaces during the operation stage. We assume that on the basis of market survey and comprehensive analysis, some related data are predicted as follows.

The operation stage is divided into five phases with a unit of four years. Taking into account the changes in the market, the rental prices of PRH, commercial facilities and parking spaces are adjusted every phase. In the first four years of the operation stage, the rental price of PRH is 11 CNY/m2/month, and then increases 6% every four years, i.e., Pn = (1+6%) Pn-4 (Pn is the rental price of PRH in the nth year of the operation stage). The rental rate of PRH is predicted as 70% and 80% at the first two phases, 90% at the two intermediate phases, and 100% at the last phase.

The rental price of commercial facilities in the first phase is 600 CNY/m2/year, and then increases 12% every four years, i.e., P′n = (1+12%) P′n-4 (P′n is the rental price of commercial facilities in the nth year of the operation stage). The rental rate of commercial facilities is expected to be 60% and 80% in the first two phases, and reach 100% in the last three phases.

Another part of cash inflow is the rental income of 5606 parking spaces. The rental price of each parking space is 2400 CNY/year, and equivalently increases 400 CNY/year each four years, i.e., P″n = P″n-4 + 400 (P″n is the rental price of each parking space in the nth year of the operation stage). The rental rates in the first 10 years are predicted to be 50%, 55%, 60%, 65%, 70%, 75%, 80%, 85%, 90%, 95%, and 100% in the last 10 years. The predicted rental rate of PRH, commercial facilities, and parking spaces in each year of the operation stage is shown in Table 3.

4.3.2. Analysis of Cash Outflow

The cash outflow of this project consists of two parts: (1) capital provided by enterprise A directly in the construction stage; (2) operation costs and loan repayment in the operation stage. Tax expenditure is not considered here because tax needs not to be paid when renting PRH and related facilities. The operation cost of a construction project is mainly composed of maintenance cost, insurance cost, management cost, and sales cost. The property management fees coming from the tenants are used to maintain the project operation, so the maintenance cost is not included in the operation cost. In this case, all income comes from rental rather than sales, thus the sales cost is also not considered. The insurance cost here refers to the expense for insurance during the operation stage and is estimated according to 0.1% of the total investment and paid annually. The management cost is the expense for management in the renting process of PRH and related supporting facilities and is estimated at 0.5% of the annual income of the project.

4.3.3. Net Cash Flow of the Project

Based on the analysis above, the net cash flow of enterprise A during the concession period of the project can be obtained as shown in Table 4. It should be noted that in the hypothetical example, although some assumptions seem to be unrealistic and simplified, they will not invalidate the investment analysis because the main objective of this section is to show the advantage of ROA in excavating the potential value of the project. Furthermore, since necessary data on the future of the project is unavailable, significant improvement of this aspect is difficult to make. Actually, investment valuation is never an exact science [28], so these drawbacks may be disregarded in this paper. The next section will present the application of ROA in the investment valuation of the project based on the analysis above.

4.4. Investment Valuation of the Project

4.4.1. Static Investment Value of the Project

The static investment value of the “Muer Airport Paradise” PRH project can be calculated according to Formula (2) and net cash flow of each year. In the feasibility study of this project based on comprehensive analysis, the benchmark discount rate (ic) is determined as 8%. By substituting the cash flow data of each year and ic into Formula (2), we can get the net present value of the project at early 2019, i.e., SNPV = 14.2412 million CNY.

4.4.2. Real Option Value of the Project

Before estimating the ROV of the project, there are several variables needed to be determined. One important variable is the volatility associated with the underlying asset σ. PRH is a new type of affordable housing in China which lacks special rent related statistical data. However, PRH rent is positively relative to the selling price of commodity houses (PRH rent is generally determined to be 30–70% of the rent of the private commodity houses nearby), hence σ can be represented by the volatility of the selling price of commodity houses [9]. Just like Li (2014), we selected the volatility of the commodity housing prices in recent 10 years in Chongqing as σ of this project [9]. Based on the process of estimating volatility described by Zhang et al. (2014) [33], σ of this project is calculated as 12.8%.

The concession period lasts 22 years from early 2019 to the end of 2040, so we construct a 22-step binomial tree where each step is regulated as every one year. Taking the beginning of each year as a time node, the binomial tree has 23 time nodes, i.e., 2019, 2020, …, 2041. The initial value of the underlying asset S00 can be calculated as the present value of the expected earnings (i.e., cash inflow) of the project, i.e., million CNY. According to Formulas (3) and (4), we can obtain the value of u and d: u = 1.137, d = 0.880. S00 is substituted to Formulas (5) and (6) and the underlying asset value of each node Snj can be obtained. We then can get the binomial tree of the underlying asset value of this project as shown in Figure 5.

The investor has a one-year deferral option at the first two time nodes (i.e., 2019 and 2020). The execute price of deferral option (i.e., XnjDefer) at each time node can be obtained based on Formula (11) and the cash outflow values in Table 3: X2019Defer = 2686.2950 million CNY; X2020Defer = 2610.3551 million CNY. Then, based on Formula (12), the execute value of deferral option at each node fnjDefer can be obtained.

In this project, we assume that the investment scale is allowed to expand by 50% according to the concession agreement, i.e., the expansion coefficient x = 0.5, and the compensation factor is assumed to be k = 0.6. So, according to Formulas (9), (10), (13), and (14), the execute value of abandonment option and expansion option at each node fnjAbandon and fnjExpand can be obtained.

The risk-free interest rate r is usually based on the yield of the government’s debt [9]. The annual interest rate of China’s five-year period national debt announced in 2018 is chosen as the risk-free interest rate of this project, that is, r = 4.17%.

According to Formula (7), we can get p = 0.6326. Based on the solving rules of ROV mentioned before, the binomial tree of the real option value of the studied project can be created as shown in Figure 6. The ROV of the initial node of the model (i.e., f00) can be considered as the ROV contained in the “Muer Airport Paradise” PRH project, that is to say, ROV = f00 = 464.6439 million CNY.

4.4.3. Investment Valuation of the Project

As mentioned in Section 3.3, according to the real option viewpoint, the investment value with flexibility is equivalent to ENPV. Thus, the investment value (IV) of the studied project can be evaluated by Formula (15) as:

5. Discussion

Through a case study, it has been tested that the presented model in this paper is applicable to estimate the investment value with flexibility and find out optimal investment strategy portfolio for value added of the project. By comparing the results of traditional NPV method and ROA, it can be seen that the project contains great potential value. Traditional NPV method neglects ROV of the project resulting in a serious underestimation of the investment value. In the studied project, the capital contribution of private sector is 581.6869 million CNY, while of which NPV accounts for only 2.45%, which is clearly not attractive to the private sector. From the NPV result, the investment on a PRH PPP project seems to be in a “high risk and low returns” situation causing investors apprehension about their investment prospect. The real option model proposed in this paper looks at project in a dynamic perspective, and can fully excavate the potential value brought by future uncertainties and management flexibility. From the real option perspective, the estimated investment value of the studied project is 478.8851 million CNY, accounting for 82.33% of the capital contribution of the private sector. The ROV is 464.6439 million CNY, which reflects the value of managerial flexibility. From this result, it can be found that the investment returns have been greatly improved, proving the revenue risk can be reduced by adapting to the uncertainties through flexible strategies. Of course, this requires that the investor should fully analyze the market environment to get up-to-date, comprehensive, and realistic information. For the private sector, compared with the traditional NPV method, ROA provides a strategic thinking to excavate the value of flexible decision including abandonment, delay, and expansion of the project, which helps to improve the profit. For the government, it can greatly improve the enthusiasm and confidence of private sectors to participate in the development of PRH, thereby easing the pressure on government funds and improving the supply and operation efficiency and financial sustainability of PRH.

6. Conclusions and Limitations

Taking raising social capital for PRH in China as the start point, this paper studied the investment valuation for private sector on a PRH PPP project. Given the superiority of ROA in considering uncertainty and flexibility and the lack of its applications in the field of PRH project, this paper established an investment valuation model of PRH PPP project from a real option perspective. For the private sector, three types of options were identified during the concession period. On this basis, a two-stage binomial tree model was then constructed for estimating the investment value. To test the practical application value of the model, a hypothetical case study was conducted by choosing a typical PRH PPP project in Chongqing. The result shows that flexible strategy greatly increases the investment value by adapting to the uncertainties of the project.

The investment valuation model proposed in this paper opens up windows of opportunity that address the needs for estimating the economic feasibility of investment characterized by high risk, long-term horizons, strong uncertainties, and managerial flexibility, which is suitable for a PRH PPP project. Application of phased compound option for the investment on a PRH PPP project reinforces the originality of this paper. For the potential private investors of a PRH PPP project, it illuminates the black box of real option analytics and provides a dynamic decision thinking. The model equips the private sector with a framework of reference to excavate the opportunity value associated with uncertainties via flexible and reasonable strategies, which is of great significance to improve their investment returns. Thereby it helps to attract more private capital into the supply system of PRH in China and alleviate the financial pressure of the government, which is conductive to improving the supply efficiency and sustainability of the PRH project.

Nevertheless, much work still remains to be done in future research due to some limitations here. First, σ of the studied project is replaced by the volatility of commodity housing prices in the last 10 years which may deviate from the actual volatility of the project and have a certain impact of the investment value estimation. Therefore, it is necessary to further explore the scientific determination of model parameters. Second, some simplified assumptions are carried out, while the actual situation may be much more complicated. These analyses need to be further improved in future research as well. Third, three types of options are identified in the proposed model, while in reality, there may be more other types of options contained in a PRH PPP project. For example, the private sector is usually provided a minimum return guarantee in a PRH PPP project, which can be considered as one special kind of option (i.e., guarantee option). Exploring the impact of the guarantee option on the project value might add objectivity to the findings as another fertile ground for future studies.

Author Contributions

J.S. and K.D. conceived and designed the study; K.D. completed the paper in English and revised it critically for important intellectual content; S.W. gave many good research advices and revised the manuscript; R.Z. provided the relevant literature review and made a comprehensive English revision.

Funding

This research received no external funding.

Acknowledgments

We would like to thank the Editor and the anonymous reviewers for their helpful suggestions and comments.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Gan, X.; Zuo, J.; Wu, P.; Wang, J.; Chang, R.; Wen, T. How affordable housing becomes more sustainable? A stakeholder study. J. Clean. Prod. 2017, 162, 427–437. [Google Scholar] [CrossRef]

- Du, J.; Yang, Y.; Li, D.; Zuo, J. Do investment and improvement demand outweigh basic consumption demand in housing market? Evidence from small cities in Jiangsu, China. Habitat Int. 2017, 66, 24–31. [Google Scholar] [CrossRef]

- Gan, X.; Zuo, J.; Chang, R.; Li, D.; Zillante, G. Exploring the determinants of migrant workers’ housing tenure choice towards public rental housing: A case study in Chongqing, China. Habitat Int. 2016, 58, 118–126. [Google Scholar] [CrossRef]

- Zhu, L.; Zhao, X.; Chua, D.K.H. Agent-based debt terms’ bargaining model to improve negotiation inefficiency in PPP projects. J. Comput. Civ. Eng. 2016, 30, 1–11. [Google Scholar] [CrossRef]

- Song, J.; Li, Y.; Feng, Z.; Wang, H. Cluster Analysis of the Intellectual Structure of PPP Research. J. Manag. Eng. 2019, 35, 04018053. [Google Scholar] [CrossRef]

- Hussain, S.; Siemiatycki, M. Rethinking the role of private capital in infrastructure PPPs: The experience of Ontario, Canada. Public Manag. Rev. 2018, 20, 1122–1144. [Google Scholar] [CrossRef]

- Silvestre, H.C.; Marques, R.C.; Gomes, R.C. Joined-up Government of utilities: A meta-review on a public–public partnership and inter-municipal cooperation in the water and wastewater industries. Public Manag. Rev. 2018, 20, 607–631. [Google Scholar] [CrossRef]

- Yuan, J.; Li, W.; Zheng, X.; Skibniewski, M.J. Improving operation performance of public rental housing delivery by PPPs in China. J. Manag. Eng. 2018, 34, 1–17. [Google Scholar] [CrossRef]

- Li, D.; Chen, H.; Hui, E.C.; Xiao, C.; Cui, Q.; Li, Q. A real option-based valuation model for privately-owned public rental housing projects in China. Habitat Int. 2014, 43, 125–132. [Google Scholar] [CrossRef]

- Vecchi, V.; Hellowell, M.; Longo, F. Are Italian healthcare organizations paying too much for their public–private partnerships? Public Money Manag. 2010, 30, 125–132. [Google Scholar] [CrossRef]

- Vasudevan, V.; Prakash, P.; Sahu, B. Options Framework and Valuation of Highway Infrastructure under Real and Financial Uncertainties. J. Infrastruct. Syst. 2018, 24, 1–9. [Google Scholar] [CrossRef]

- Wang, H.; Xiong, W.; Wu, G.; Zhu, D. Public–private partnership in Public Administration discipline: A literature review. Public Manag. Rev. 2018, 20, 293–316. [Google Scholar] [CrossRef]

- Xiong, W.; Zhao, X.; Yuan, J.F.; Luo, S. Ex post risk management in public private partnerships infrastructure projects. Proj. Manag. J. 2017, 48, 76–89. [Google Scholar] [CrossRef]

- Yuan, J.; Li, W.; Guo, J.; Zhao, X.; Skibniewski, M.J. Social risk factors of transportation PPP projects in China: A sustainable development perspective. Int. J. Environ. Res. Public Health 2018, 15, 1323. [Google Scholar] [CrossRef] [PubMed]

- Wang, X.; Du, L. Study on carbon capture and storage (CCS) investment decision-making based on real options for China’s coal-fired power plants. J. Clean. Prod. 2016, 112, 4123–4131. [Google Scholar] [CrossRef]

- Abdul-Aziz, A.R.; Jahn Kassim, P.S. Objectives, success and failure factors of housing public-private partnerships in Malaysia. Habitat Int. 2011, 35, 150–157. [Google Scholar] [CrossRef]

- Xiong, W.; Zhao, X.; Wang, H. Information asymmetry in renegotiation of public–private partnership projects. J. Comput. Civ. Eng. 2018, 32, 04018028. [Google Scholar] [CrossRef]

- Blessing, A. Public, private, or in-between? The legitimacy of social enterprises in the housing market. Voluntas 2013, 26, 198–221. [Google Scholar] [CrossRef]

- Vale, L.J.; Freemark, Y. From public housing to public-private housing: 75 years of american social experimentation. J. Am. Plan. Assoc. 2012, 78, 379–402. [Google Scholar] [CrossRef]

- Lima, V. Social housing under the Workers’ Party government: An analysis of the private sector in Brazil. Third World Q. 2017, 6597, 1–16. [Google Scholar] [CrossRef]

- Kwofie, T.E.; Afram, S.; Botchway, E. A critical success model for PPP public housing delivery in Ghana. Built Environ. Proj. Asset Manag. 2016, 6, 58–73. [Google Scholar] [CrossRef]

- Guarini, M.R.; Battisti, F. A Model to Assess the Feasibility of Public–Private Partnership for Social Housing. Buildings 2017, 7, 44. [Google Scholar] [CrossRef]

- Sani, M.; Sani, A.; Ahmed, U.S. Exploring Factors Affecting Implementation of Public Private Partnership Housing Projects in Bauchi State, Nigeria. Path Sci. 2018, 4, 7001–7005. [Google Scholar] [CrossRef]

- Bockman, J. Removing the public from public housing: Public–private redevelopment of the Ellen Wilson Dwellings in Washington, DC. J. Urban. Aff. 2018, 2166, 1–21. [Google Scholar] [CrossRef]

- Yuan, J.; Guang, M.; Wang, X.; Li, Q.; Skibniewski, M.J. Quantitative SWOT analysis of public housing delivery by public–private partnerships in China based on the perspective of the public sector. J. Manag. Eng. 2012, 28, 407–420. [Google Scholar] [CrossRef]

- Schachter, J.A.; Mancarella, P. A critical review of Real Options thinking for valuing investment flexibility in Smart Grids and low carbon energy systems. Renew. Sustain. Energy Rev. 2016, 56, 261–271. [Google Scholar] [CrossRef]

- Odetayo, B.; MacCormack, J.; Rosehart, W.D.; Zareipour, H. A real option assessment of flexibilities in the integrated planning of natural gas distribution network and distributed natural gas-fired power generations. Energy 2018, 143, 257–272. [Google Scholar] [CrossRef]

- Santos, L.; Soares, I.; Mendes, C.; Ferreira, P. Real Options versus Traditional Methods to assess Renewable Energy Projects. Renew. Energy 2014, 68, 588–594. [Google Scholar] [CrossRef]

- Ban, L.; Misawa, T.; Miyahara, Y. Valuation of Hong Kong REIT based on risk sensitive value measure method. Int. J. Real Opt. Strateg. 2016, 4, 1–33. [Google Scholar] [CrossRef]

- Kim, K.; Park, H.; Kim, H. Real options analysis for renewable energy investment decisions in developing countries. Renew. Sustain. Energy Rev. 2017, 75, 918–926. [Google Scholar] [CrossRef]

- Yao, H.; Pretorius, F. Demand uncertainty, development timing and leasehold land valuation: Empirical testing of real options in residential real estate development. Real Estate Econ. 2014, 42, 829–868. [Google Scholar] [CrossRef]

- Moon, Y.; Baran, M. Economic analysis of a residential PV system from the timing perspective: A real option model. Renew. Energy 2018, 125, 783–795. [Google Scholar] [CrossRef]

- Zhang, M.; Zhou, D.; Zhou, P. A real option model for renewable energy policy evaluation with application to solar PV power generation in China. Renew. Sustain. Energy Rev. 2014, 40, 944–955. [Google Scholar] [CrossRef]

- Haque, M.A.; Topal, E.; Lilford, E. A numerical study for a mining project using real options valuation under commodity price uncertainty. Resour. Policy 2014, 39, 115–123. [Google Scholar] [CrossRef]

- Inthavongsa, I.; Drebenstedt, C.; Bongaerts, J.; Sontamino, P. Real options decision framework: Strategic operating policies for open pit mine planning. Resour. Policy 2016, 47, 142–153. [Google Scholar] [CrossRef]

- Pellegrino, R.; Vajdic, N.; Carbonara, N. Real option theory for risk mitigation in transport PPPs. Built Environ. Proj. Asset Manag. 2013, 3, 199–213. [Google Scholar] [CrossRef]

- Tang, B.J.; Zhou, H.L.; Chen, H.; Wang, K.; Cao, H. Investment opportunity in China’s overseas oil project: An empirical analysis based on real option approach. Energy Policy 2017, 105, 17–26. [Google Scholar] [CrossRef]

- Fonseca, M.N.; Pamplona, E.D.O.; Valerio, V.E.D.M.; Aquila, G.; Rocha, L.C.S.; Junior, P.R. Oil price volatility: A real option valuation approach in an African oil field. J. Pet. Sci. Eng. 2017, 150, 297–304. [Google Scholar] [CrossRef]

- Song, J.; Zhang, H.; Dong, W. A review of emerging trends in global PPP research: Analysis and visualization. Scientometrics 2016, 107, 1111–1147. [Google Scholar] [CrossRef]

- Myers, S.C. The determinants of corporate borrowing. J. Financ. Econ. 1977, 5, 229–263. [Google Scholar] [CrossRef]

- Kozlova, M. Real option valuation in renewable energy literature: Research focus, trends and design. Renew. Sustain. Energy Rev. 2017, 80, 180–196. [Google Scholar] [CrossRef]

- Trigeorgis, L. The Nature of Option Interactions and the Valuation of Investments with Multiple Real Options. J. Financ. Quant. Anal. 1993, 28, 1–20. [Google Scholar] [CrossRef]

- Trigeorgis, L.; Reuer, J.J. Real options theory in strategic management. Strateg. Manag. J. 2017, 38, 42–63. [Google Scholar] [CrossRef]

- Kulatilaka, N.; Perotti, E.C. Strategic Growth Options. Manag. Sci. 1998, 44, 1021–1031. [Google Scholar] [CrossRef] [Green Version]

- Trigeorgis, L. Making Use of Real Options Simple: An Overview and Applications in Flexible/Modular Decision Making. Eng. Econ. 2005, 50, 25–53. [Google Scholar] [CrossRef]

- Titman, B.S. Urban Land Prices Under Uncertainty. Am. Econ. Rev. 1985, 75, 505–514. [Google Scholar]

- Baldi, F. Valuing a greenfield real estate property development project: A real options approach. J. Eur. Real Estate Res. 2013, 6, 186–217. [Google Scholar] [CrossRef]

- Čirjevskis, A.; Tatevosjans, E. Empirical Testing of Real Option in the Real Estate Market. Procedia Econ. Financ. 2015, 24, 50–59. [Google Scholar] [CrossRef] [Green Version]

- Mintah, K.; Higgins, D.; Callanan, J.; Wakefield, R. Staging option application to residential development: Real options approach. Int. J. Hous. Mark. Anal. 2018, 11, 101–116. [Google Scholar] [CrossRef]

- Li, D.; Guo, K.; You, J.; Hui, E.C. Assessing investment value of privately-owned public rental housing projects with multiple options. Habitat Int. 2016, 53, 8–17. [Google Scholar] [CrossRef]

- Liu, J.; Yu, X.; Cheah, C.Y.J. Evaluation of restrictive competition in PPP projects using real option approach. Int. J. Proj. Manag. 2014, 32, 473–481. [Google Scholar] [CrossRef]

- Xiong, W.; Zhang, X. The Real Option Value of Renegotiation in Public–Private Partnerships. J. Constr. Eng. Manag. 2016, 142, 1–11. [Google Scholar] [CrossRef]

- Liu, J.; Gao, R.; Cheah, C.Y.J. Pricing Mechanism of Early Termination of PPP Projects Based on Real Option Theory. J. Manag. Eng. 2017, 33, 04017035. [Google Scholar] [CrossRef]

- Ma, G.; Du, Q.; Wang, K. A concession period and price determination model for PPP projects: Based on real options and risk allocation. Sustainability 2018, 10, 706. [Google Scholar] [CrossRef]

- Black, F.; Scholes, M. The Pricing of Options and Corporate Liabilities. J. Polit. Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Cox, J.C.; Ross, S.A.; Rubinstein, M. Option pricing: A simplified approach. J. Financ. Econ. 1979, 7, 229–263. [Google Scholar] [CrossRef]

- Gilbert, E. Investment Basics XLIX. An introduction to real options. Investig. Anal. J. 2005, 33, 49–52. [Google Scholar] [CrossRef]

- Loncar, D.; Milovanovic, I.; Rakic, B.; Radjenovic, T. Compound real options valuation of renewable energy projects: The case of a wind farm in Serbia. Renew. Sustain. Energy Rev. 2017, 75, 354–367. [Google Scholar] [CrossRef]

- Fernandes, B.; Cunha, J.; Ferreira, P. The use of real options approach in energy sector investments. Renew. Sustain. Energy Rev. 2011, 15, 4491–4497. [Google Scholar] [CrossRef] [Green Version]

- Shen, L.Y.; Li, H.; Li, Q.M. Alternative Concession Model for Build Operate Transfer Contract Projects. J. Constr. Eng. Manag. 2002, 128, 326–330. [Google Scholar] [CrossRef]

- Hwang, B.; Zhao, X.; Gay, M.J.S. Public private partnership projects in Singapore: Factors, critical risks and preferred risk allocation from the perspective of contractors. Int. J. Proj. Manag. 2013, 31, 424–433. [Google Scholar] [CrossRef]

- Hu, Q.; Zhang, A. Real option analysis of aircraft acquisition: A case study. J. Air Transp. Manag. 2015, 46, 19–29. [Google Scholar] [CrossRef]

- Ha, N.T.; Fujiwara, T. Real Option Approach on Infrastructure Investment in Vietnam: Focused on Smart City Project. Glob. J. Flex. Syst. Manag. 2015, 16, 331–345. [Google Scholar] [CrossRef]

- Kokkaew, N.; Chiara, N. A modeling government revenue guarantees in privately built transportation projects: A risk-adjusted approach. Transport 2013, 28, 186–192. [Google Scholar] [CrossRef]

- Almassi, A.; McCabe, B.; Thompson, M. Real options–based approach for valuation of government guarantees in Public–Private Partnerships. J. Infrastruct. Syst. 2013, 19, 196–204. [Google Scholar] [CrossRef]

- Buyukyoran, F.; Gundes, S. Optimized real options-based approach for government guarantees in PPP toll road projects. Constr. Manag. Econ. 2018, 36, 203–216. [Google Scholar] [CrossRef]

Figure 1.

Binomial tree of the underlying asset value.

Figure 2.

Single period of binomial tree.

Figure 3.

Binomial tree of the real option value.

Figure 4.

Two-stage binomial tree model for a public rental housing (PRH) public–private partnership (PPP) project.

Figure 4.

Two-stage binomial tree model for a public rental housing (PRH) public–private partnership (PPP) project.

Figure 5.

Binomial tree of the underlying asset value of the studied project.

Figure 6.

Binomial tree of the real option value of the studied project. Note: the nodes fijContinue, fijDefer, fijExpand, and fijAbandon mean respectively that holding the options, executing deferral option, executing expansion option, and executing abandonment option are the best choices at each node.

Figure 6.

Binomial tree of the real option value of the studied project. Note: the nodes fijContinue, fijDefer, fijExpand, and fijAbandon mean respectively that holding the options, executing deferral option, executing expansion option, and executing abandonment option are the best choices at each node.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Main building indicators of the studied project.

| Indicator | Value | Indicator | Value |

|---|---|---|---|

| Total land area (m2) | 481,128.65 | Residential area (m2) | 1,434,539 |

| Total construction area (m2) | 1,809,088 | Commercial area (m2) | 229,003 |

| PRH suites | 28,993 | Number of parking spaces | 5606 |

Table 2.

Main financial indicators of the studied project (unit: million CNY).

| Indicator | Value | Remark |

|---|---|---|

| Total investment | 5816.8692 | |

| Special financial funds | 2326.7477 | Accounting for 40% of total investment |

| Enterprise capital contribution | 581.6869 | Accounting for 10% of total investment |

| Bank loans | 2908.4346 | Accounting for 50% of total investment |

Table 3.

The predicted rental rate in each year.

| Year | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | |

| Items | |||||||||||

| PRH | 70% | 70% | 70% | 70% | 80% | 80% | 80% | 80% | 90% | 90% | |

| Commercial facilities | 60% | 60% | 60% | 60% | 80% | 80% | 80% | 80% | 100% | 100% | |

| Parking space | 50% | 55% | 60% | 65% | 70% | 75% | 80% | 85% | 90% | 95% | |

| Year | 2031 | 2032 | 2033 | 2034 | 2035 | 2036 | 2037 | 2038 | 2039 | 2040 | |

| Items | |||||||||||

| PRH | 90% | 90% | 90% | 90% | 90% | 90% | 100% | 100% | 100% | 100% | |

| Commercial facilities | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | |

| Parking space | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | |

Table 4.

Capital cash flow statement of the project (unit: million CNY).

| Year | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | |

| Items | |||||||||

| Rental income of PRH | 132.5514 | 132.5514 | 132.5514 | 132.5514 | 160.5766 | 160.5766 | |||

| Rental income of commercial facilities | 82.4411 | 82.4411 | 82.4411 | 82.4411 | 123.1120 | 123.1120 | |||

| Rental income of parking spaces | 6.7272 | 7.3999 | 8.0726 | 8.7454 | 10.9878 | 11.7726 | |||

| Cash inflow | 221.7197 | 222.3924 | 223.0651 | 223.7378 | 294.6763 | 295.4612 | |||

| Loan repayment | 365.9398 | 365.9398 | 365.9398 | 365.9398 | 365.9398 | 365.9398 | |||

| Insurance costs | 5.8169 | 5.8169 | 5.8169 | 5.8169 | 5.8169 | 5.8169 | |||

| Management costs | 1.1086 | 1.1120 | 1.1153 | 1.1187 | 1.4734 | 1.4773 | |||

| Cash outflow | 290.8435 | 290.8435 | 372.8653 | 372.8686 | 372.8720 | 372.8754 | 373.2301 | 373.2340 | |

| Net cash flow | −290.8435 | −290.8435 | −151.1456 | −150.4762 | −149.8069 | −149.1375 | −78.5537 | −77.7728 | |

| Year | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | |

| Items | |||||||||

| Rental income of PRH | 160.5766 | 160.5766 | 191.4875 | 191.4875 | 191.4875 | 191.4875 | 202.9768 | 202.9768 | |

| Rental income of commercial facilities | 123.1120 | 123.1120 | 172.3568 | 172.3568 | 172.3568 | 172.3568 | 193.0396 | 193.0396 | |

| Rental income of parking spaces | 12.5574 | 13.3423 | 16.1453 | 17.0422 | 17.9392 | 17.9392 | 20.1816 | 20.1816 | |

| Cash inflow | 296.2460 | 297.0309 | 379.9896 | 380.8866 | 381.7836 | 381.7836 | 416.1980 | 416.1980 | |

| Loan repayment | 365.9398 | 365.9398 | 365.9398 | 365.9398 | |||||

| Insurance costs | 5.8169 | 5.8169 | 5.8169 | 5.8169 | 5.8169 | 5.8169 | 5.8169 | 5.8169 | |

| Management costs | 1.4812 | 1.4852 | 1.8999 | 1.9044 | 1.9089 | 1.9089 | 2.0810 | 2.0810 | |

| Cash outflow | 373.2379 | 373.2418 | 373.6566 | 373.6611 | 7.7258 | 7.7258 | 7.8979 | 7.8979 | |

| Net cash flow | −76.9919 | −76.2110 | 6.3330 | 7.2255 | 374.0578 | 374.0578 | 408.3002 | 408.3002 | |

| Year | 2035 | 2036 | 2037 | 2038 | 2039 | 2040 | |||

| Items | |||||||||

| Rental income of PRH | 202.9768 | 202.9768 | 239.0616 | 239.0616 | 239.0616 | 239.0616 | |||

| Rental income of commercial facilities | 193.0396 | 193.0396 | 216.2044 | 216.2044 | 216.2044 | 216.2044 | |||

| Rental income of parking spaces | 20.1816 | 20.1816 | 22.4240 | 22.4240 | 22.4240 | 22.4240 | |||

| Cash inflow | 416.1980 | 416.1980 | 477.6900 | 477.6900 | 477.6900 | 477.6900 | |||

| Insurance costs | 5.8169 | 5.8169 | 5.8169 | 5.8169 | 5.8169 | 5.8169 | |||

| Management costs | 2.0810 | 2.0810 | 2.3884 | 2.3884 | 2.3884 | 2.3884 | |||

| Cash outflow | 7.8979 | 7.8979 | 8.2053 | 8.2053 | 8.2053 | 8.2053 | |||

| Net cash flow | 408.3002 | 408.3002 | 469.4846 | 469.4846 | 469.4846 | 469.4846 | |||

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Shi, J.; Duan, K.; Wen, S.; Zhang, R. Investment Valuation Model of Public Rental Housing PPP Project for Private Sector: A Real Option Perspective. Sustainability 2019, 11, 1857. https://doi.org/10.3390/su11071857

AMA Style

Shi J, Duan K, Wen S, Zhang R. Investment Valuation Model of Public Rental Housing PPP Project for Private Sector: A Real Option Perspective. Sustainability. 2019; 11(7):1857. https://doi.org/10.3390/su11071857

Chicago/Turabian StyleShi, Jiangang, Kaifeng Duan, Shiping Wen, and Rui Zhang. 2019. "Investment Valuation Model of Public Rental Housing PPP Project for Private Sector: A Real Option Perspective" Sustainability 11, no. 7: 1857. https://doi.org/10.3390/su11071857

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.