Rethinking the Way of Doing Business: A Reframe of Management Structures for Developing Corporate Sustainability

Abstract

1. Introduction

2. Theoretical Background on Corporate Sustainability Management

3. Research Method

3.1. Delineating Research Theme and Objective

3.2. Planning Methodological Procedures

3.3. Systematic Search for Scientific Papers

3.4. Collecting and Analyzing Data

3.5. Trustworthiness Evaluation

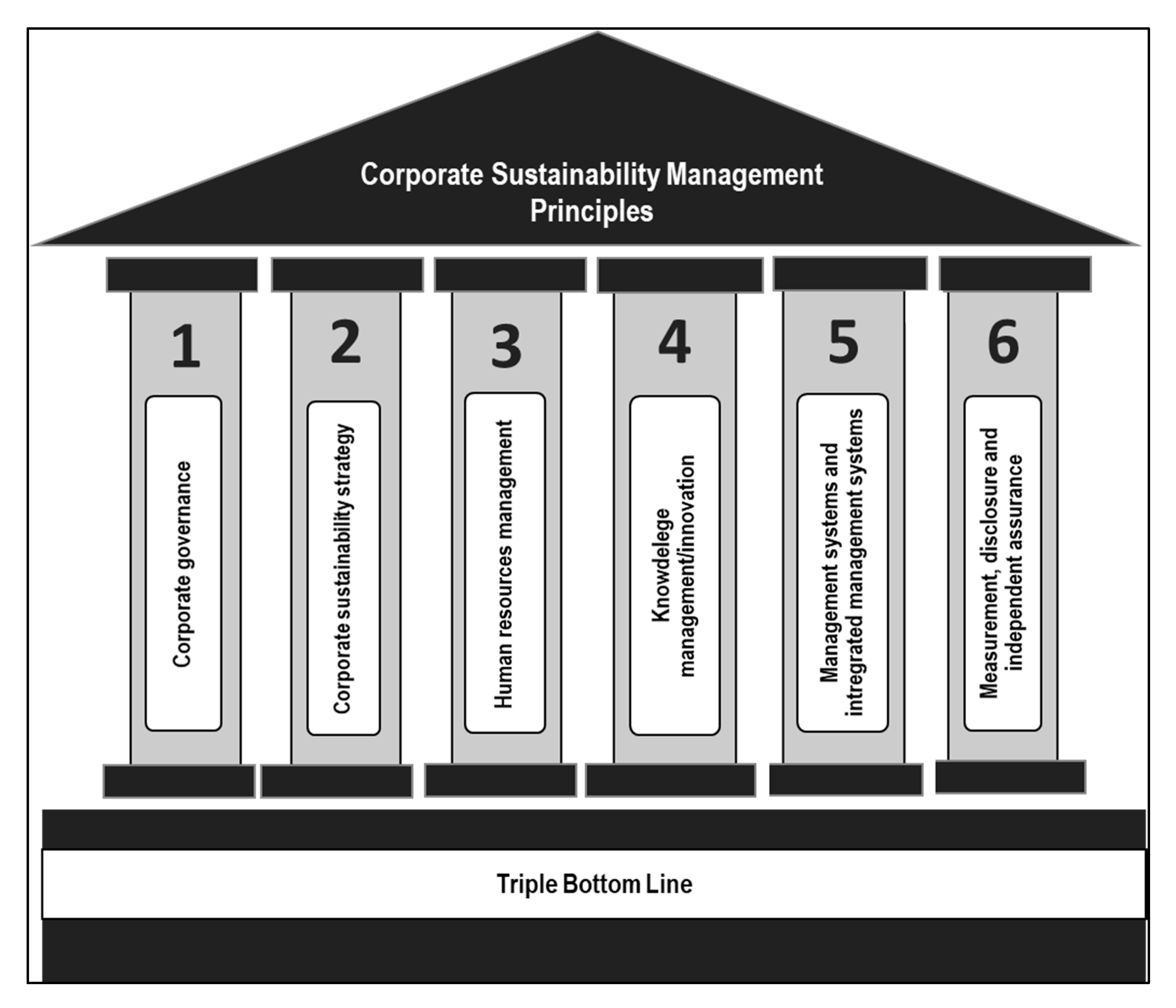

4. Results

4.1. Sustainable Corporate Governance

4.2. Corporate Sustainability Strategy

4.3. Sustainable Management of Human Resources

4.4. Sustainable Knowledge and Innovation Management

4.5. Measurement, Disclosure, and Independent Assurance of Corporate Sustainability

4.6. Sustainable Management Systems and Integrated Management Systems

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| Nº | Title | Author(s)/Year | Journal/ISSN | Times Cited (Scopus March 2018) |

|---|---|---|---|---|

| 1 | Corporate Social Responsibility and Corporate Sustainability Separate Pasts, Common Futures | Montiel (2008) | Organization & Environment/1086-0266 | 166 |

| 2 | Corporate Sustainability and Innovation in SMEs: Evidence of Themes and Activities in Practice | Bos-Brouwers (2010) | Business Strategy and the Environment/1099-0836 | 157 |

| 3 | Corporate sustainability and organizational culture | Linnenluecke and Griffiths (2010) | Journal of World Business/1090-9516 | 156 |

| 4 | Business Cases for Sustainability: The Role of Business Model Innovation for Corporate Sustainability | Schaltegger, Lüdecke-Freund and Hansen (2012) | International Journal of Innovation and Sustainable Development/1740-8830 | 152 |

| 5 | Corporate Sustainability Strategies: Sustainability Profiles and Maturity Levels | Baumgartner and Ebner (2010) | Sustainable Development/1099-1719 | 146 |

| 6 | W(h)ither Ecology? The Triple Bottom Line, the Global Reporting Initiative, and Corporate Sustainability Reporting | Milne and Gray (2013) | Journal of Business Ethics/0167-4544 | 128 |

| 7 | An analysis of indicators disclosed in corporate sustainability reports | Roca and Searcy (2012) | Journal of Cleaner Production/0959-6526 | 126 |

| 8 | Planetary Boundaries: Ecological Foundations for Corporate Sustainability | Whiteman, Walker and Perego (2013) | Journal of Management Studies/1467-6486 | 117 |

| 9 | The Impact of Corporate Sustainability on Organizational Processes and Performance | Eccles, Ioannou and Serafeim (2014) | Management Science/0025-1909 | 103 |

| 10 | Corporate Sustainability Reporting: A Study in Disingenuity? | Aras and Crowther (2009) | Journal of Business Ethics/0167-4544 | 102 |

| 11 | Is Corporate Sustainability a Value Increasing Strategy for Business? | Lo and Sheu (2007) | Corporate Governance An International Review/0964-8410 | 96 |

| 12 | Governance and sustainability: An investigation into the relationship between corporate governance and corporate sustainability | Aras and Crowther (2008) | Management Decision/0025-1747 | 93 |

| 13 | Corporate Sustainability Performance Measurement Systems:A Review and Research Agenda | Searcy (2012) | Journal of Business Ethics/0167-4544 | 91 |

| 14 | Corporate Sustainability Performance and Idiosyncratic Risk: A Global Perspective | Lee (2009) | The Financial Review/1540-6288 | 89 |

| 15 | The determinants of corporate sustainability performance | Artiach et al. (2010) | Accounting and Finance/1467-629X | 88 |

| 16 | The role of corporate sustainability performance for economic performance: A firm-level analysis of moderation effects | Wagner (2010) | Ecological Economics/0921-8009 | 79 |

| 17 | Cognitive frames in corporate sustainability: managerial sensemaking with paradoxical and business case frames | Hahn et al. (2014) | Academy of Management Review/0363-7425 | 77 |

| 18 | Measuring corporate sustainability management: A data envelopment analysis approach | Lee and Saen (2012) | International Journal of Production Economics/0925-5273 | 71 |

| 19 | Subcultures and Sustainability Practices: the Impact on Understanding Corporate Sustainability | Linnenluecke, Russell and Griffiths (2009) | Business Strategy and the Environment | 70 |

| 20 | A holistic perspective on corporate sustainability drivers | Lozano (2015) | Corporate Social Responsibility and Environmental Management | 66 |

| 21 | Defining and Measuring Corporate Sustainability: Are We There Yet? | Montiel and Delgado-Ceballos (2014) | Organization & Environment/1099-0836 | 60 |

| 22 | Tensions in Corporate Sustainability: Towards an Integrative Framework | Hahn et al. (2015) | Journal of Business Ethics/0167-4544 | 57 |

| 23 | Beyond the Bounded Instrumentality in Current Corporate Sustainability Research: Toward an Inclusive Notion of Profitability | Hahn and Figge (2011) | Journal of Business Ethics/0167-4544 | 57 |

| 24 | Conceptualising future change in corporate sustainability reporting | Adams and Whelan (2009) | Auditing & Accountability Journal/0951-3574 | 57 |

| 25 | What does GRI-Reporting tell us about Corporate Sustainability? | Isaksson and Steimle (2009) | The TQM Journal/1754-2731 | 56 |

| 26 | The Relationship Between Sustainable Supply Chain Management, Stakeholder Pressure and Corporate Sustainability Performance | Wolf (2014) | Journal of Business Ethics/0167-4544 | 55 |

| 27 | Corporate sustainability: an integrative definition and framework to evaluate corporate practice and guide academic research | Amini and Bienstock (2014) | Journal of Cleaner Production | 54 |

| 28 | Instrumental and Integrative Logics in Business Sustainability | Gao and Bansal (2013) | Journal of Business Ethics/0167-4544 | 50 |

| 29 | Corporate sustainability performance and firm performance research: Literature review and future research agenda | Goyal, Rahman ad Kazmi (2013) | Management Decision/0025-1747 | 49 |

| 30 | Managing Corporate Sustainability and CSR: A Conceptual Framework Combining Values, Strategies and Instruments Contributing to Sustainable Development | Baumgartner (2014) | Corporate Social Responsibility and Environmental Management/1535-3966 | 48 |

Appendix B

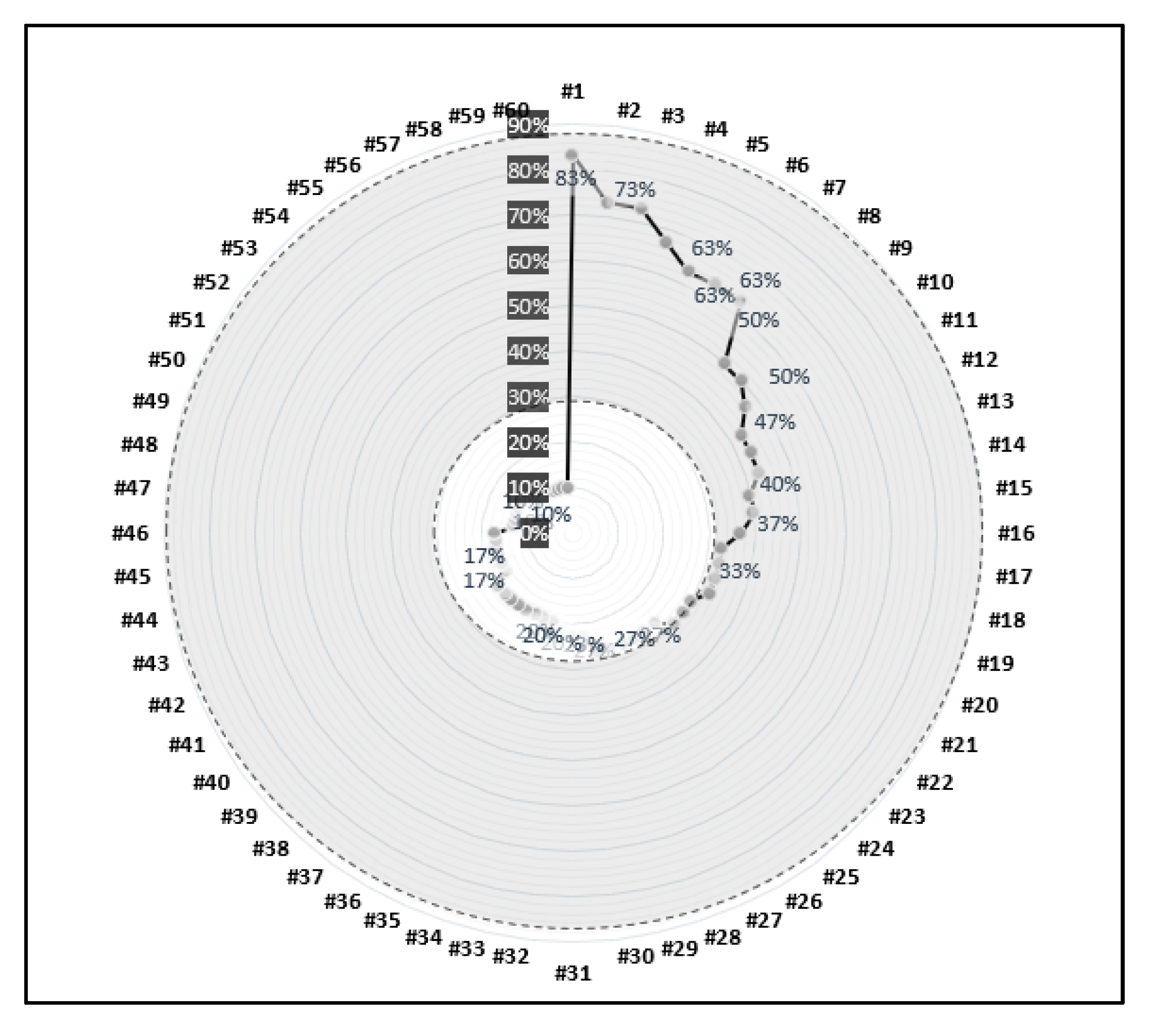

| # | CS Elements | Most Cited Articles #1–10 | Most Cited Articles #11–20 | Most Cited Articles #21–30 | Total % | |||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| #1 | #2 | #3 | #4 | #5 | #6 | #7 | #8 | #9 | #10 | #11 | #12 | #13 | #14 | #15 | #16 | #17 | #18 | #19 | #20 | #21 | #22 | #23 | #24 | #25 | #26 | #27 | #28 | #29 | #30 | |||

| 1 | Cooperative relationship with stakeholders | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 83% | |||||

| 2 | Corporate sustainability performance measurement system | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 73% | ||||||||

| 3 | Factory inspections and audits | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 73% | ||||||||

| 4 | HR programs | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 67% | ||||||||||

| 5 | Top management support | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 63% | |||||||||||||

| 6 | Eco-efficiency-oriented measures | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 63% | |||||||||||

| 7 | Long-term orientation | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 63% | |||||||||||

| 8 | Corporate sustainability report | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 50% | ||||||||||||||

| 9 | Risk management | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 50% | ||||||||||||||

| 10 | Business adjustment, improvement or redesign | x | x | x | x | x | x | x | x | x | x | x | x | x | x | 47% | ||||||||||||||||

| 11 | Integration and balance of social, environmental, and business activities and responsibilities | x | x | x | x | x | x | x | x | x | x | x | x | x | 43% | |||||||||||||||||

| 12 | Sustainability-oriented organizational culture | x | x | x | x | x | x | x | x | x | x | x | x | x | 43% | |||||||||||||||||

| 13 | Product design aimed to innovation on environmental performance | x | x | x | x | x | x | x | x | x | x | x | x | x | 43% | |||||||||||||||||

| 14 | Health and safety initiatives | x | x | x | x | x | x | x | x | x | x | x | x | 40% | ||||||||||||||||||

| 15 | Codes of conduct/corporate governance/ethics | x | x | x | x | x | x | x | x | x | x | x | x | 40% | ||||||||||||||||||

| 16 | Legal compliance with regulation | x | x | x | x | x | x | x | x | x | x | x | 37% | |||||||||||||||||||

| 17 | Become an organizational changing agent | x | x | x | x | x | x | x | x | x | x | 33% | ||||||||||||||||||||

| 18 | Consideration of sustainability issues in purchase | x | x | x | x | x | x | x | x | x | 33% | |||||||||||||||||||||

| 19 | Promotion of flexibility, learn and, if necessary, change in processes | x | x | x | x | x | x | x | x | x | 33% | |||||||||||||||||||||

| 20 | Transparency in management | x | x | x | x | x | x | x | x | x | x | 33% | ||||||||||||||||||||

| 21 | Managerial best practices to promote sustainable supply chain management | x | x | x | x | x | x | x | x | x | 30% | |||||||||||||||||||||

| 22 | Philanthropic responsibilities | x | x | x | x | x | x | x | x | x | 30% | |||||||||||||||||||||

| 23 | Evaluation of sustainability business effect | x | x | x | x | x | x | x | x | x | 30% | |||||||||||||||||||||

| 24 | Energy and water saving projects | x | x | x | x | x | x | x | x | x | 27% | |||||||||||||||||||||

| 25 | Sustainability indices and guidelines | x | x | x | x | x | x | x | x | 27% | ||||||||||||||||||||||

| 26 | Minority and diversity programs | x | x | x | x | x | x | x | x | 27% | ||||||||||||||||||||||

| 27 | Evaluation of company’s reputation and brand value | x | x | x | x | x | x | x | x | 27% | ||||||||||||||||||||||

| 28 | R&D with multidisciplinary innovation project teams | x | x | x | x | x | x | x | x | x | x | x | x | x | 27% | |||||||||||||||||

| 29 | Co-development with business partners (e.g., suppliers, R&D institutions, universities) | x | x | x | x | x | x | x | x | 27% | ||||||||||||||||||||||

| 30 | Integration of CS with management systems and/or integrated management systems | x | x | x | x | x | x | x | 23% | |||||||||||||||||||||||

| 31 | Voluntary environmental restoration | x | x | x | x | x | x | x | 23% | |||||||||||||||||||||||

| 32 | Standards of corporate governance, compliance, ethics | x | x | x | x | x | x | x | 23% | |||||||||||||||||||||||

| 33 | Reduction of likelihood of environmental accidents | x | x | x | x | x | x | 20% | ||||||||||||||||||||||||

| 34 | Employee well-being initiatives | x | x | x | x | x | x | 20% | ||||||||||||||||||||||||

| 35 | Environmentally and socially superior products and services | x | x | x | x | x | x | 20% | ||||||||||||||||||||||||

| 36 | Multidisciplinary innovation meetings | x | x | x | x | x | x | 20% | ||||||||||||||||||||||||

| 37 | Innovation discussion panel with customers | x | x | x | x | x | x | 20% | ||||||||||||||||||||||||

| 38 | Strategic partnerships to overcome market barriers and promote new products and services | x | x | x | x | x | x | 20% | ||||||||||||||||||||||||

| 39 | Fluid information exchange | x | x | x | x | x | x | 20% | ||||||||||||||||||||||||

| 40 | Publicate a corporate sustainability policy | x | x | x | x | x | x | 20% | ||||||||||||||||||||||||

| 41 | Reduction of operations in environmentally sensitive locations | x | x | x | x | x | 17% | |||||||||||||||||||||||||

| 42 | Handling of toxic waste, effluents, used products from customers, plastic residues, paper and others | x | x | x | x | x | x | x | 17% | |||||||||||||||||||||||

| 43 | Development of employee eco-initiatives | x | x | x | x | x | 17% | |||||||||||||||||||||||||

| 44 | Occupational Health and Safety and Human Rights standards | x | x | x | x | x | 17% | |||||||||||||||||||||||||

| 45 | Products and services with lower energy or maintenance costs for customers | x | x | x | x | x | 17% | |||||||||||||||||||||||||

| 46 | Stakeholders’ ideals and needs | x | x | x | x | x | x | x | x | 17% | ||||||||||||||||||||||

| 47 | Teamwork and employee empowerment | x | x | x | x | 13% | ||||||||||||||||||||||||||

| 48 | Planning market entry or development | x | x | x | x | 13% | ||||||||||||||||||||||||||

| 49 | Use of waste for revenue and re-usable packages to delivery materials | x | x | x | x | 13% | ||||||||||||||||||||||||||

| 50 | Process improvements | x | x | x | x | 13% | ||||||||||||||||||||||||||

| 51 | Open dialogue across management levels and functions | x | x | x | x | 13% | ||||||||||||||||||||||||||

| 52 | Sustainability management system | x | x | x | 10% | |||||||||||||||||||||||||||

| 53 | Geographical and marketing segmentation | x | x | x | 10% | |||||||||||||||||||||||||||

| 54 | Integration of ecosystem stewardship into natural resource management practices | x | x | x | 10% | |||||||||||||||||||||||||||

| 55 | Recruitment of local employees | x | x | x | 10% | |||||||||||||||||||||||||||

| 56 | Promotion and sponsorship of projects geared toward sustainable development | x | x | x | 10% | |||||||||||||||||||||||||||

| 57 | Analysis of the impact of each stakeholder | x | x | x | x | 10% | ||||||||||||||||||||||||||

| 58 | Inspiration from networks, conferences | x | x | x | x | 10% | ||||||||||||||||||||||||||

| 59 | Incentives and reward systems | x | x | x | 10% | |||||||||||||||||||||||||||

| 60 | Ethical commitments regarding 2nd and 3rd world countries | x | x | x | 10% | |||||||||||||||||||||||||||

References

- Bocken, N.M.P.; Short, S.W.; Rana, P.; Evans, S. A literature and practice review to develop sustainable business model archetypes. J. Clean. Prod. 2014, 65, 42–56. [Google Scholar] [CrossRef]

- Adams, R.; Jeanrenaud, S.; Bessant, J.; Denyer, D.; Overy, P. Sustainability-oriented Innovation: A Systematic Review. Int. J. Manag. Rev. 2016, 18, 180–205. [Google Scholar] [CrossRef]

- Joyce, A.; Paquin, R.L. The triple layered business model canvas: A tool to design more sustainable business models. J. Clean. Prod. 2016, 135, 1474–1486. [Google Scholar] [CrossRef]

- Baumgartner, R.J.; Ebner, D. Corporate Sustainability Strategies: Sustainability Profi les and Maturity Levels. Sustain. Dev. Sust. Dev. 2010, 18, 76–89. [Google Scholar] [CrossRef]

- Milne, M.J.; Gray, R. W(h)ither Ecology? The Triple Bottom Line, the Global Reporting Initiative, and Corporate Sustainability Reporting. J. Bus. Ethics 2013, 118, 13–29. [Google Scholar] [CrossRef]

- Holton, I.; Glass, J.; Price, A.D.F. Managing for sustainability: Findings from four company case studies in the UK precast concrete industry. J. Clean. Prod. 2010, 18, 152–160. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C. Towards a standardised management system for corporate sustainable development. TQM J. 2014, 26, 411–430. [Google Scholar] [CrossRef]

- Mura, M.; Longo, M.; Micheli, P.; Bolzani, D. The Evolution of Sustainability Measurement Research. Int. J. Manag. Rev. 2018, 20, 661–695. [Google Scholar] [CrossRef]

- UNEP-FI Sustainability Metrics: Translation and Impact on Property Investment and Management. Available online: www.unepfi.org. (accessed on 1 August 2016).

- Savino, M.M.; Mazza, A. Toward environmental and quality sustainability: An integrated approach for continuous improvement. IEEE Trans. Eng. Manag. 2014, 61, 171–181. [Google Scholar] [CrossRef]

- United Nations Global Compact What’s the Commitment? 2019. Available online: https://www.unglobalcompact.org/participation/join/commitment (accessed on 1 September 2019).

- Roca, L.C.; Searcy, C. An analysis of indicators disclosed in corporate sustainability reports. J. Clean. Prod. 2012, 20, 103–118. [Google Scholar] [CrossRef]

- Siew, R.Y.J. A review of corporate sustainability reporting tools (SRTs). J. Environ. Manag. 2015, 164, 180–195. [Google Scholar] [CrossRef] [PubMed]

- Moldavska, A.; Welo, T. The concept of sustainable manufacturing and its definitions: A content-analysis based literature review. J. Clean. Prod. 2017, 166, 744–755. [Google Scholar] [CrossRef]

- Steurer, R.; Langer, M.E. Corporations, Stakeholders and Sustainable Development I: A Theoretical Exploration of Business – Society Relations. J. Bus. Ethics 2005, 61, 263–281. [Google Scholar] [CrossRef]

- Adams, W.M. The Future of Sustainability: Re-thinking Environment and Development in the Twenty-first Century; Report of the IUCN Renowned Thinkers Meeting; World Conservation Union: Gland, Switzerland, 2006; Volume 29, pp. 1–18. [Google Scholar]

- Salzmann, O.; Ionescu-Somers, A.M.; Steger, U. The business case for corporate sustainability: Literature review and research options. Eur. Manag. J. 2005, 23, 27–36. [Google Scholar] [CrossRef]

- Gao, J.; Bansal, P. Instrumental and Integrative Logics in Business Sustainability. J. Bus. Ethics 2013, 112, 241–255. [Google Scholar] [CrossRef]

- Lozano, R. A holistic perspective on corporate sustainability drivers. Corp. Soc. Responsib. Environ. Manag. 2015, 22, 32–44. [Google Scholar] [CrossRef]

- Feil, A.A.; de Quevedo, D.M.; Schreiber, D. An analysis of the sustainability index of micro- and small-sized furniture industries. Clean Technol. Environ. Policy 2017, 19, 1883–1896. [Google Scholar] [CrossRef]

- Montiel, I.; Delgado-Ceballos, J. Defining and Measuring Corporate Sustainability. Organ. Environ. 2014, 27, 113–139. [Google Scholar] [CrossRef]

- Lloret, A. Modeling corporate sustainability strategy. J. Bus. Res. 2016, 69, 418–425. [Google Scholar] [CrossRef]

- Hammer, J.; Pivo, G. The Triple Bottom Line and Sustainable Economic Development Theory and Practice. Econ. Dev. Q. 2017, 31, 25–36. [Google Scholar] [CrossRef]

- Gimenez, C.; Sierra, V.; Rodon, J. Sustainable operations: Their impact on the triple bottom line. Int. J. Prod. Econ. 2012, 140, 149–159. [Google Scholar] [CrossRef]

- Kurdve, M.; Shahbazi, S.; Wendin, M.; Bengtsson, C. Waste flow mapping to improve sustainability of waste management: A case study approach. J. Clean. Prod. 2015, 98, 304–315. [Google Scholar] [CrossRef]

- Gilinsky, A.; Sandra, J.; Thomas, K.N.; Cristina, S.A.; Alessio, S.; Augusti, C.; Gilinsky, A.; Sandra, J.; Thomas, K.N.; Cristina, S.A.; et al. Perceived efficacy of sustainability strategies in the US, Italian, and Spanish wine industries. Int. J. Wine Bus. Res. 2015, 3, 164–181. [Google Scholar] [CrossRef]

- Epstein, M.J.; Roy, M.J. Sustainability in Action: Identifying and Measuring the Key Performance Drivers. Long Range Plan. 2001, 34, 585–604. [Google Scholar] [CrossRef]

- Székely, F.; Knirsch, M. Responsible leadership and corporate social responsibility: Metrics for sustainable performance. Eur. Manag. J. 2005, 23, 628–647. [Google Scholar] [CrossRef]

- Nawaz, W.; Koç, M. Exploring Organizational Sustainability: Themes, Functional Areas, and Best Practices. Sustainability 2019, 11, 4307. [Google Scholar] [CrossRef]

- Gonzalez-Perez, M.A.; Leonard, L. The Global Compact: Corporate sustainability in the Post 2015 world. Adv. Sustain. Environ. Justice 2015, 17, 1–19. [Google Scholar]

- Hahn, T.; Pinkse, J.; Preuss, L.; Figge, F. Tensions in Corporate Sustainability: Towards an Integrative Framework. J. Bus. Ethics 2015, 127, 297–316. [Google Scholar] [CrossRef]

- Linnenluecke, M.K.; Griffiths, A. Corporate sustainability and organizational culture. J. World Bus. 2010, 45, 357–366. [Google Scholar] [CrossRef]

- Eccles, R.G.; Ioannou, I.; Serafeim, G. The Impact of Corporate Sustainability on Organizational Processes and Performance. Manag. Sci. 2014, 60, 2835–2857. [Google Scholar] [CrossRef]

- Hahn, R. Standardizing Social Responsibility? New Perspectives on Guidance Documents and Management System Standards for Suistanable Development. Trans. Eng. Manag. 2012, 59, 4. [Google Scholar] [CrossRef]

- Baumgartner, R.J. Managing corporate sustainability and CSR: A conceptual framework combining values, strategies and instruments contributing to sustainable development. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 258–271. [Google Scholar] [CrossRef]

- Engert, S.; Rauter, R.; Baumgartner, R.J. Exploring the integration of corporate sustainability into strategic management: A literature review. J. Clean. Prod. 2016, 112, 2833–2850. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Bernardo, M.; Oliveira, O.J. Guiding principles of integrated management systems: Towards unifying a starting point for researchers and practitioners. J. Clean. Prod. 2018, 210, 977–993. [Google Scholar] [CrossRef]

- Petros Sebhatu, S.; Enquist, B. ISO 14001 as a driving force for sustainable development and value creation. TQM Mag. 2007, 19, 468–482. [Google Scholar] [CrossRef]

- Grimm, J.H.; Hofstetter, J.S.; Sarkis, J. Exploring sub-suppliers’ compliance with corporate sustainability standards. J. Clean. Prod. 2016, 112, 1971–1984. [Google Scholar] [CrossRef]

- Lozano, R.; Huisingh, D. Inter-linking issues and dimensions in sustainability reporting. J. Clean. Prod. 2011, 19, 99–107. [Google Scholar] [CrossRef]

- Asif, M.; De Bruijn, E.J.; Fisscher, O.A.M.; Searcy, C.; Steenhuis, H.-J. Process embedded design of integrated management systems. Int. J. Qual. Reliab. Manag. 2009, 26, 261–282. [Google Scholar] [CrossRef]

- Montiel, I. Corporate Social Responsibility and Corporate Sustainability: Separate Pasts, Common Futures. Organ. Environ. 2008, 21, 245–269. [Google Scholar]

- van Marrewijk, M. Concepts and definitions of CSR and corporate sustainability: Between agency and communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Bansal, P. Evolving sustainably: A longitudinal study of corporate sustainable development. Strateg. Manag. J. 2005, 26, 197–218. [Google Scholar] [CrossRef]

- WCED Report of the World Commission on Environment and Development: Our Common Future (The Brundtland Report). Med. Confl. Surviv. 1987, 4, 300.

- Baumgartner, R.J.; Rauter, R. Strategic perspectives of corporate sustainability management to develop a sustainable organization. J. Clean. Prod. 2017, 140, 81–92. [Google Scholar] [CrossRef]

- Isil, O.; Hernke, M.T. The Triple Bottom Line: A Critical Review from a Transdisciplinary Perspective. Bus. Strateg. Environ. 2017, 26, 1235–1251. [Google Scholar] [CrossRef]

- Broman, G.I.; Robèrt, K.-H. A Framework for Strategic Sustainable Development. J. Clean. Prod. 2017, 140, 1–15. [Google Scholar] [CrossRef]

- Pádua, S.I.D.; Jabbour, C.J.C. Promotion and evolution of sustainability performance measurement systems from a perspective of business process management: From a literature review to a pentagonal proposal. Bus. Process Manag. J. 2015, 21, 403–418. [Google Scholar] [CrossRef]

- Saratun, M. Performance management to enhance employee engagement for corporate sustainability. Asia-Pac. J. Bus. Adm. 2016, 8, 84–102. [Google Scholar] [CrossRef]

- Grewatsch, S.; Kleindienst, I. When Does It Pay to be Good? Moderators and Mediators in the Corporate Sustainability–Corporate Financial Performance Relationship: A Critical Review; Springer: Dordrecht, The Netherlands, 2017; Volume 145, ISBN 01674544. [Google Scholar]

- Büyüközkan, G.; Karabulut, Y. Sustainability performance evaluation: Literature review and future directions. J. Environ. Manag. 2018, 217, 253–267. [Google Scholar] [CrossRef]

- Kühnen, M.; Hahn, R. Systemic social performance measurement: Systematic literature review and explanations on the academic status quo from a product life-cycle perspective. J. Clean. Prod. 2018, 205, 690–705. [Google Scholar] [CrossRef]

- Morioka, S.N.; Bolis, I.; Carvalho, M.M.D. From an ideal dream towards reality analysis: Proposing Sustainable Value Exchange Matrix (SVEM) from systematic literature review on sustainable business models and face validation. J. Clean. Prod. 2018, 178, 76–88. [Google Scholar] [CrossRef]

- Amui, L.B.L.; Jabbour, C.J.C.; de Sousa Jabbour, A.B.L.; Kannan, D. Sustainability as a dynamic organizational capability: A systematic review and a future agenda toward a sustainable transition. J. Clean. Prod. 2017, 142, 308–322. [Google Scholar] [CrossRef]

- De Stefano, F.; Bagdadli, S.; Camuffo, A. The HR role in corporate social responsibility and sustainability: A boundary-shifting literature review. Hum. Resour. Manag. 2018, 57, 549–566. [Google Scholar] [CrossRef]

- Lüdeke-Freund, F.; Carroux, S.; Joyce, A.; Massa, L.; Breuer, H. The sustainable business model pattern taxonomy—45 patterns to support sustainability-oriented business model innovation. Sustain. Prod. Consum. 2018, 15, 145–162. [Google Scholar] [CrossRef]

- Chandan, H.C. Creating alignment between corporate sustainability and Global Compact initiatives. Adv. Sustain. Environ. Justice 2015, 16, 37–59. [Google Scholar]

- Zsóka, Á.; Vajkai, É. Corporate sustainability reporting: Scrutinising the requirements of comparability, transparency and reflection of sustainability performance. Soc. Econ. 2018, 40, 19–44. [Google Scholar] [CrossRef]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Identification and prioritization of corporate sustainability practices using analytical hierarchy process. J. Model. Manag. 2015, 10, 23–49. [Google Scholar] [CrossRef]

- Martinez, F. A Three-Dimensional Conceptual Framework of Corporate Water Responsibility. Organ. Environ. 2015, 28, 137–159. [Google Scholar] [CrossRef]

- Siano, A.; Piciocchi, P.; Vollero, A.; Volpe, M.D.; Palazzo, M.; Conte, F.; De Luca, D.; Amabile, S. Developing a Framework for Measuring Effectiveness of Sustainability Communications through Corporate Websites. Procedia Manuf. 2015, 3, 3615–3620. [Google Scholar] [CrossRef]

- Siano, A.; Conte, F.; Amabile, S.; Vollero, A.; Piciocchi, P. Communicating sustainability: An operational model for evaluating corporate websites. Sustainability 2016, 8, 950. [Google Scholar] [CrossRef]

- Morioka, S.N.; Carvalho, M.M. Measuring sustainability in practice: Exploring the inclusion of sustainability into corporate performance systems in Brazilian case studies. J. Clean. Prod. 2016, 136, 123–133. [Google Scholar] [CrossRef]

- Brones, F.A.; Carvalho, M.M.D.; Zancul, E.D.S. Reviews, action and learning on change management for ecodesign transition. J. Clean. Prod. 2017, 142, 8–22. [Google Scholar] [CrossRef]

- Vildåsen, S.S.; Keitsch, M.; Fet, A.M. Clarifying the Epistemology of Corporate Sustainability. Ecol. Econ. 2017, 138, 40–46. [Google Scholar] [CrossRef]

- Seele, P. Predictive Sustainability Control: A review assessing the potential to transfer big data driven ‘predictive policing’ to corporate sustainability management. J. Clean. Prod. 2017, 153, 673–686. [Google Scholar] [CrossRef]

- Caldera, H.T.S.; Desha, C.; Dawes, L. Exploring the role of lean thinking in sustainable business practice: A systematic literature review. J. Clean. Prod. 2018, 167, 1546–1565. [Google Scholar] [CrossRef]

- Muñoz-Torres, M.J.; Fernández-Izquierdo, M.; Rivera-Lirio, J.M.; Ferrero-Ferrero, I.; Escrig-Olmedo, E.; Gisbert-Navarro, J.V.; Marullo, M.C. An assessment tool to integrate sustainability principles into the global supply chain. Sustainability 2018, 10, 535. [Google Scholar]

- Fritz, M.M.C.; Schöggl, J.-P.; Baumgartner, R.J. Selected sustainability aspects for supply chain data exchange: Towards a supply chain-wide sustainability assessment. J. Clean. Prod. 2017, 141, 587–607. [Google Scholar] [CrossRef]

- Kang, S.-W.; Lee, K.-H. Mainstreaming corporate environmental strategy in management research. Benchmarking 2016, 23, 618–650. [Google Scholar] [CrossRef]

- Yutu, W.E.; Krisnawatia, A.D.A.; Yudokoa, G.; Banguna, R. Environmental performance towards sustainable development: A review of clean production policies in Indonesia. J. Eng. Appl. Sci. 2016, 11, 1699–1705. [Google Scholar]

- Bai, C.; Sarkis, J.; Dou, Y. Corporate sustainability development in China: Review and analysis. Ind. Manag. Data Syst. 2015, 115, 5–40. [Google Scholar] [CrossRef]

- El-Khalil, R.; El-Kassar, A.-N. Effects of corporate sustainability practices on performance: The case of the MENA region. Benchmarking 2018, 25, 1333–1349. [Google Scholar] [CrossRef]

- Seuring, S.; Gold, S. Conducting content-analysis based literature reviews in supply chain management. Supply Chain Manag. Int. J. 2012, 17, 544–555. [Google Scholar] [CrossRef]

- Bengtsson, M. How to plan and perform a qualitative study using content analysis. NursingPlus Open 2016, 2, 8–14. [Google Scholar] [CrossRef]

- Wallace, D.P.; Van Fleet, C.; Downs, L.J. The research core of the knowledge management literature. Int. J. Inf. Manag. 2011, 31, 14–20. [Google Scholar] [CrossRef]

- Xia, B.; Olanipekun, A.; Chen, Q.; Xie, L.; Liu, Y. Conceptualising the state of the art of corporate social responsibility (CSR) in the construction industry and its nexus to sustainable development. J. Clean. Prod. 2018, 195, 340–353. [Google Scholar] [CrossRef]

- Aghaei Chadegani, A.; Salehi, H.; Md Yunus, M.M.; Farhadi, H.; Fooladi, M.; Farhadi, M.; Ale Ebrahim, N. A comparison between two main academic literature collections: Web of science and scopus databases. Asian Soc. Sci. 2013, 9, 18–26. [Google Scholar] [CrossRef]

- Oliveira, O.J.; Silva, F.F.; Juliani, F.; Barbosa, L.C.F.M.; Nunhes, T.V. Bibliometric Method for Mapping the State-of-the-Art and Identifying Research Gaps and Trends in Literature: An Essential Instrument to Support the Development of Scientific Projects. In Scientometrics Recent Advances; IntechOpen: Rijeka, Croatia, 2019; p. 13. ISBN 978-1-78984-713-0. [Google Scholar]

- Elo, S.; Kääriäinen, M.; Kanste, O.; Pölkki, T.; Utriainen, K.; Kyngäs, H. Qualitative Content Analysis: A focus in trustworthiness. SAGE Open 2014, 4, 1–10. [Google Scholar] [CrossRef]

- Scott, J. Content Analysis. In The Sage Dictionary of Social Research Methods; Sage Publications: London, UK, 2006; pp. 79–249. [Google Scholar]

- Vaismoradi, M.; Turunen, H.; Bondas, T. Content analysis and thematic analysis: Implications for conducting a qualitative descriptive study. Nurs. Heal. Sci. 2013, 15, 398–405. [Google Scholar] [CrossRef]

- Aras, G.; Crowther, D. Governance and sustainability. Manag. Decis. 2008, 46, 433–448. [Google Scholar] [CrossRef]

- Miras-rodr, M.; Mart, D. Which Corporate Governance Mechanisms Drive CSR Disclosure Practices in Emerging Countries? Sustainability 2018, 11, 61. [Google Scholar] [CrossRef]

- Bos-brouwers, H.E.J. Corporate sustainability and innovation in SMEs: Evidence of themes and activities in practice. Bus. Strateg. Environ. 2009, 19, 417–435. [Google Scholar] [CrossRef]

- Taliento, M.; Favino, C.; Netti, A. Impact of environmental, social, and governance information on economic performance: Evidence of a corporate “sustainability advantage” from Europe. Sustainability 2019, 11, 1738. [Google Scholar] [CrossRef]

- Wahba, H.; Elsayed, K. The mediating effect of financial performance on the relationship between social responsibility and ownership structure. Future Bus. J. 2015, 1, 1–12. [Google Scholar] [CrossRef]

- Abatecola, G.; Cristofaro, M. Ingredients of sustainable CEO behaviour: Theory and practice. Sustainability 2019, 11, 1950. [Google Scholar] [CrossRef]

- Ben-hassoun, A.; Aloui, C.; Ben-nasr, H. Research in International Business and Finance Demand for audit quality in newly privatized fi rms in MENA region: Role of internal corporate governance mechanisms audit. Res. Int. Bus. Financ. 2018, 45, 334–348. [Google Scholar]

- Antolín-López, R.; Delgado-Ceballos, J.; Montiel, I. Deconstructing corporate sustainability: A comparison of different stakeholder metrics. J. Clean. Prod. 2014, 136, 5–17. [Google Scholar]

- Adams, C.A.; Whelan, G. Conceptualising future change in corporate sustainability reporting. Account. Audit. Account. J. 2009, 22, 118–143. [Google Scholar] [CrossRef]

- Isaksson, R.; Steimle, U. What does GRI-Reporting tell us about Corporate Sustainability? Definitions for sustainable development and sustainability. TQM J. 2009, 21, 168–181. [Google Scholar] [CrossRef]

- Lee, K.; Farzipoor, R. Measuring corporate sustainability management: A data envelopment analysis approach. Int. J. Prod. Econ. 2012, 140, 219–226. [Google Scholar] [CrossRef]

- Crowther, D. Corporate Sustainability Reporting: A Study in Disingenuity? Güler Aras. J. Bus. Ethics 2009, 87, 279–288. [Google Scholar]

- Goyal, P.; Rahman, Z.; Kazmi, A.A. Corporate sustainability performance and firm performance research. Manag. Decis. 2013, 51, 361–379. [Google Scholar] [CrossRef]

- Schaltegger, S.; Freund, F.L.; Hansen, E.G. Business cases for sustainability: The role of business model innovation for corporate sustainability. Int. J. Innov. Sustain. Dev. 2012, 6, 95. [Google Scholar] [CrossRef]

- Lee, D.; Faff, R. Corporate sustainability performance and idiosyncratic risk: A global perspective. Financ. Rev. 2009, 44, 213–237. [Google Scholar] [CrossRef]

- Renwick, D.W.S.; Redman, T.; Maguire, S. Green Human Resource Management: A Review and Research Agenda*. Int. J. Manag. Rev. 2013, 15, 1–14. [Google Scholar] [CrossRef]

- Kantabutra, S. Achieving Corporate Sustainability: Toward a Practical Theory. Sustainability 2019, 11, 4155. [Google Scholar] [CrossRef]

- Lo, S.-F.; Sheu, H.-J. Is Corporate Sustainability a Value- Increasing Strategy for Business? Corp. Gov. Int. Rev. 2007, 15, 345–359. [Google Scholar] [CrossRef]

- Carrion, R.D.; Fernandez, P.M.R. Developing a sustainable HRM system from a contextual perspective. Corp. Soc. Responsib. Envirionmental Manag. 2018, 25, 1143–1153. [Google Scholar]

- Linnenluecke, M.K.; Russell, S.V.; Griffiths, A. Subcultures and sustainability practices: The impact on understanding corporate sustainability. Bus. Strateg. Environ. 2009, 18, 432–452. [Google Scholar] [CrossRef]

- Gismera, E.; Fernández, J.L.; Labrador, J.; Gismera, L. Suffering at Work: A Challenge for Corporate Sustainability in the Spanish Context. Sustainability 2019, 11, 4152. [Google Scholar] [CrossRef]

- Li, Y.; Tarafdar, M.; Rao, S.S. Collaborative knowledge management practices Theoretical development. Int. J. Oper. Prod. Manag. 2012, 32, 398–422. [Google Scholar] [CrossRef]

- Zeng, J.; Anh Phan, C.; Matsui, Y.; Anh, C.; Matsui, Y. The impact of hard and soft quality management on quality and innovation performance: An empirical study. Int. J. Prod. Econ. 2014, 162, 216–226. [Google Scholar] [CrossRef]

- Scharf, E.R.; Sierra, E.J.S. Knowledge management and the perceived value: A sustainable competitive strategy for the knowledge era. J. Inf. Syst. Technol. Manag. 2008, 5, 87–108. [Google Scholar]

- Mahendrawathi, E.R. Knowledge management support for enterprise resource planning implementation. Procedia Comput. Sci. 2015, 72, 613–621. [Google Scholar] [CrossRef]

- Tyagi, S.; Cai, X.; Yang, K.; Chambers, T. Lean tools and methods to support efficient knowledge creation. Int. J. Inf. Manag. 2015, 35, 204–214. [Google Scholar] [CrossRef]

- Artiach, T.; Lee, D.; Nelson, D.; Walker, J. The determinants of corporate sustainability performance. Account. Financ. 2010, 50, 31–51. [Google Scholar] [CrossRef]

- Searcy, C. Corporate Sustainability Performance Measurement Systems: A Review and Research Agenda. J. Bus. Ethics 2012, 107, 239–253. [Google Scholar] [CrossRef]

- Wolf, J. The Relationship Between Sustainable Supply Chain Management, Stakeholder Pressure and Corporate Sustainability Performance. J. Bus. Ethics 2014, 119, 317–328. [Google Scholar] [CrossRef]

- Asif, M.; Searcy, C.; Zutshi, A.; Fisscher, O.A.M. An integrated management systems approach to corporate social responsibility. J. Clean. Prod. 2013, 56, 7–17. [Google Scholar] [CrossRef]

- Maas, K. Integrating corporate sustainability assessment, management accounting, control, and reporting. J. Clean. Prod. 2016, 136, 237–248. [Google Scholar] [CrossRef]

- Boiral, O.; Henri, J.-F. Is Sustainability Performance Comparable? A Study of GRI Reports of Mining Organizations. Bus. Soc. 2017, 56, 283–317. [Google Scholar] [CrossRef]

- Wasara, T.M.; Ganda, F. The Relationship between Corporate Sustainability Disclosure and Firm Financial Performance in Johannesburg Stock Exchange (JSE) Listed Mining Companies. Sustainability 2019, 11, 4496. [Google Scholar] [CrossRef]

- Nawaz, W.; Koç, M. Development of a systematic framework for sustainability management of organizations. J. Clean. Prod. 2018, 171, 1255–1274. [Google Scholar] [CrossRef]

- Jorgensen, T.H. Towards more sustainable management systems: Through life cycle management and integration. J. Clean. Prod. 2008, 16, 1071–1080. [Google Scholar] [CrossRef]

- Qi, G.; Zeng, S.; Yin, H.; Lin, H. ISO and OHSAS certifications How stakeholders affect corporate decisions. Manag. Decis. 2013, 51, 1983–2005. [Google Scholar] [CrossRef]

- Rybski, C.; Jochem, R.; Homma, L. Empirical study on status of preparation for ISO 9001:2015. Total Qual. Manag. Bus. Excell. 2017, 28, 1076–1089. [Google Scholar] [CrossRef]

- Fonseca, L.M. Exploratory Research of ISO 14001: 2015 Transition among Portuguese Organizations. Sustainability 2018, 10, 781. [Google Scholar] [CrossRef]

- Klute-Wenig, S.; Refflinghaus, R. Integrating sustainability aspects into an integrated management system. TQM J. 2015, 27, 303–315. [Google Scholar] [CrossRef]

- Ranängen, H.; Cöster, M.; Isaksson, R. From Global Goals and Planetary Boundaries to Public Governance—A Framework for Prioritizing Organizational Sustainability Activities. Sustainability 2018, 10, 2741. [Google Scholar]

- de Oliveira Neves, F.; Salgado, E.G.; Beijo, L.A. Analysis of the Environmental Management System based on ISO 14001 on the American continent. J. Environ. Manag. 2017, 199, 251–262. [Google Scholar] [CrossRef]

- Maletic, M.; Podpečan, M.; Maletic, D. ISO 14001 in a corporate sustainability context: A multiple case study approach. Manag. Environ. Qual. Int. J. 2015, 26, 872–890. [Google Scholar] [CrossRef]

- Karapetrovic, S.; Casadesús, M. Implementing environmental with other standardized management systems: Scope, sequence, time and integration. J. Clean. Prod. 2009, 17, 533–540. [Google Scholar] [CrossRef]

- Gianni, M.; Gotzamani, K.; Tsiotras, G. Multiple perspectives on integrated management systems and corporate sustainability performance. J. Clean. Prod. 2017, 168, 1297–1311. [Google Scholar] [CrossRef]

- Witjes, S.; Vermeulen, W.J.V.; Cramer, J.M. Exploring corporate sustainability integration into business activities. Experiences from 18 small and medium sized enterprises in the Netherlands. J. Clean. Prod. 2017, 153, 528–538. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Ferreira Motta, L.C.; de Oliveira, O.J. Evolution of integrated management systems research on the Journal of Cleaner Production: Identification of contributions and gaps in the literature. J. Clean. Prod. 2016, 139, 1234–1244. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Oliveira, O.J. Analysis of Integrated Management Systems research: Identifying core themes and trends for future studies. Total Qual. Manag. 2018, 1–23. [Google Scholar] [CrossRef]

| Research Topic | Author(s)/Year |

|---|---|

| Corporate sustainability performance | [49,50,51,52,53,54] |

| Corporate sustainability and strategic management | [36,55,56] |

| Sustainable business models | [54,57] |

| Corporate sustainability reporting | [13,30,58,59] |

| Corporate sustainability frameworks, tools, and practices | [60,61,62,63,64,65,66,67,68,69] |

| Sustainable supply chain | [70] |

| Environmental corporate sustainability | [71,72] |

| Adopting corporate sustainability in specific countries/regions | [73,74] |

| # | CS Elements ≥ 30% Freq. | # | 10% ≤ CS Elements < 30% Freq. | Pillars |

|---|---|---|---|---|

| 7 | Long-term orientation | 38 | Strategic partnerships to overcome market barriers and promote new products and services | Corporate sustainability strategy |

| 9 | Risk management | 48 | Planning market entry or development | |

| 10 | Business adjustment, improvement or redesign | 53 | Geographical and marketing segmentation | |

| 18 | Consideration of sustainability issues in purchase | |||

| 1 | Cooperative relationship with stakeholders | 27 | Evaluation of a company’s reputation and brand value | Corporate governance |

| 5 | Top management support | 40 | Publication of a corporate sustainability policy | |

| 15 | Codes of conduct/corporate governance/ethics | 56 | Promotion and sponsorship of projects geared toward sustainable development | |

| 16 | Legal compliance with regulation | 60 | Ethical commitments regarding 2nd and 3rd world countries | |

| 20 | Transparency in management | |||

| 22 | Philanthropic responsibilities | |||

| 4 | HR programs | 26 | Minority and diversity programs | Human resources management |

| 12 | Sustainability-oriented organizational culture | 36 | Multidisciplinary innovation meetings | |

| 43 | Development of employee eco-initiatives | |||

| 47 | Teamwork and employee empowerment | |||

| 55 | Recruitment of local employees | |||

| 59 | Incentives and reward systems | |||

| 6 | Eco-efficiency-oriented measures | 28 | R&D with multidisciplinary innovation project teams | Knowledge and innovation management |

| 13 | Product design aimed to innovation on environmental performance | 29 | Co-development with business partners (e.g., suppliers, R&D institutions, universities) | |

| 19 | Promotion of flexibility, learn and, if necessary, change in processes | 35 | Environmentally and socially superior products and services | |

| 37 | Innovation discussion panel with customers | |||

| 39 | Fluid information exchange | |||

| 45 | Products and services with lower energy or maintenance costs for customers | |||

| 49 | Use of waste for revenue and re-usable packages to delivery materials | |||

| 50 | Open dialogue across management levels and functions | |||

| 51 | Sustainability management system | |||

| 58 | Inspiration from networks, conferences | |||

| 3 | Factory inspections and audits | 25 | Sustainability indices and guidelines | Measurement, disclosure and independent assurance |

| 8 | Corporate sustainability report | 32 | Standards of corporate governance, compliance, ethics | |

| 23 | Evaluation of sustainability business effect | 57 | Analysis of the impact of each stakeholder | |

| 2 | Corporate sustainability performance measurement system | |||

| 11 | Integration and balance of social, environmental, and business activities and responsibilities | 24 | Energy and water-saving projects | Management systems and integrated management systems |

| 14 | Health and safety initiatives | 30 | Integration of CS with management systems and/or integrated management systems | |

| 21 | Managerial best practices to promote sustainable supply chain management | 31 | Voluntary environmental restoration | |

| 33 | Reduction of the likelihood of environmental accidents | |||

| 41 | Reduction of operations in environmentally sensitive locations | |||

| 42 | Handling of toxic waste, effluents, used products from customers, plastic residues, paper, and others | |||

| 44 | Occupational health and safety and human rights standards | |||

| 52 | Sustainability management system |

| TBL Focus Area(s) | Management Standard/Guideline/Regulation |

|---|---|

| Economic | - ISO 9001 Quality management system |

| - ISO 44001 Collaborative business relationship management systems | |

| - ISO 37001 Anti-bribery management system | |

| - ISO 22301 Business continuity management system | |

| Environmental | - ISO 14001 and EMAS—Environmental management system |

| - ISO/DIS 24526 Water efficiency management systems | |

| - ISO 50001 Energy management system | |

| - ISO 14064 Carbon management system | |

| Social | - ISO 45001 Occupational health and safety management system |

| - ISO 18788 Management system for private security operations | |

| - SA 8000 Social Accountability | |

| Economic, environmental and social | - ISO 19600 Compliance management system and AA1000AS Assurance standard |

| - ISO 28001 Security management system for the supply chain | |

| - ISO/IEC 27001 Information security management system and ISO/IEC 2000-1 Service management system | |

| - ISO 30401 Human resource management—Knowledge management systems | |

| - ISO 31000 Risk management system | |

| - ISO 26000 Guidance on social responsibility | |

| - British BSI PAS 99; Danish DS 8001; Spanish UNE 66177; Australia/New Zealand AS/NZS4581 Integrated management system | |

| - BS 8900 Managing sustainable development |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nunhes, T.V.; Bernardo, M.; Oliveira, O.J.d. Rethinking the Way of Doing Business: A Reframe of Management Structures for Developing Corporate Sustainability. Sustainability 2020, 12, 1177. https://doi.org/10.3390/su12031177

Nunhes TV, Bernardo M, Oliveira OJd. Rethinking the Way of Doing Business: A Reframe of Management Structures for Developing Corporate Sustainability. Sustainability. 2020; 12(3):1177. https://doi.org/10.3390/su12031177

Chicago/Turabian StyleNunhes, Thaís Vieira, Merce Bernardo, and Otávio José de Oliveira. 2020. "Rethinking the Way of Doing Business: A Reframe of Management Structures for Developing Corporate Sustainability" Sustainability 12, no. 3: 1177. https://doi.org/10.3390/su12031177

APA StyleNunhes, T. V., Bernardo, M., & Oliveira, O. J. d. (2020). Rethinking the Way of Doing Business: A Reframe of Management Structures for Developing Corporate Sustainability. Sustainability, 12(3), 1177. https://doi.org/10.3390/su12031177