2.4.2. BMI, MACS and SIO: The Links

It is apparent to note that using a sustainable orientation and BMI individually does not necessarily warrant effective positive changes in corporate performance [

1,

2,

12]. This is because important aspects of the innovation process itself, such as commercialization, are deemed to be in constant need of proper management [

12], meaning that commercialization is the last pivotal step in innovation that can prove to be ineffective if it is not properly managed. Thus, the benefits of a sustainable orientation for the entire production process can be exploited by having effective managerial tools. Most importantly, the organization must possess a better understanding of these aspects, implications, and benefits of a sustainable orientation [

43]. Moreover, there are also suggestions that reveal that an understanding of a sustainable orientation is necessary in order to have a better understanding of the competitive environment [

11].

Looking at the above discussions, it is therefore imperative that organizational strategies must be realigned to encompass marketing and innovation capabilities. This establishes an important synergy between MACS and a sustainable orientation [

18,

20]. Based on the sustainable orientation point of view, MACS help to provide insights into key issues that need to be addressed as well as into the current position of the firm. Additionally, the use of MACS is regarded as a position to strongly reveal the dominant stakeholders of a company and their related needs [

19]. Either way, there is possible mediating role of MACS in the relationship between BMI and sustainable orientation.

Meanwhile, BMI and sustainable orientation make it feasible for firms to adopt and implement the required differentiation strategy. This is important because it helps the firm to devote attention towards special product characteristics that are essential to customers. However, the successful implementation of this strategy requires a proper understanding of the competitive situation so as to convince customers of the benefits of the sustainably reoriented product features [

11]. It is believed that a lot of customers and retailers are presently in need of more details regarding sustainably reoriented products [

16]. This is important because it causes firms to acquire important feedback about important product features in a timely manner [

11]. Thus, the introduction of new products is strongly determined by the firm’s market orientation. Benchmarking can thus be used to reinforce the effective use of market orientation to support the introduction of new products by drawing lessons from other successful companies [

41]. In doing so, firms can gain a better understanding of the demanded products and services and how they contribute towards enhancing customer value. That is, MACS use budgets and cost accounting strategies to reinforce the effectiveness of differentiation strategies [

41]. However, there are arguments that contend that MACS cannot be tailor-made to match diverse and complex business environments [

11]. As a result, the following hypotheses are formulated.

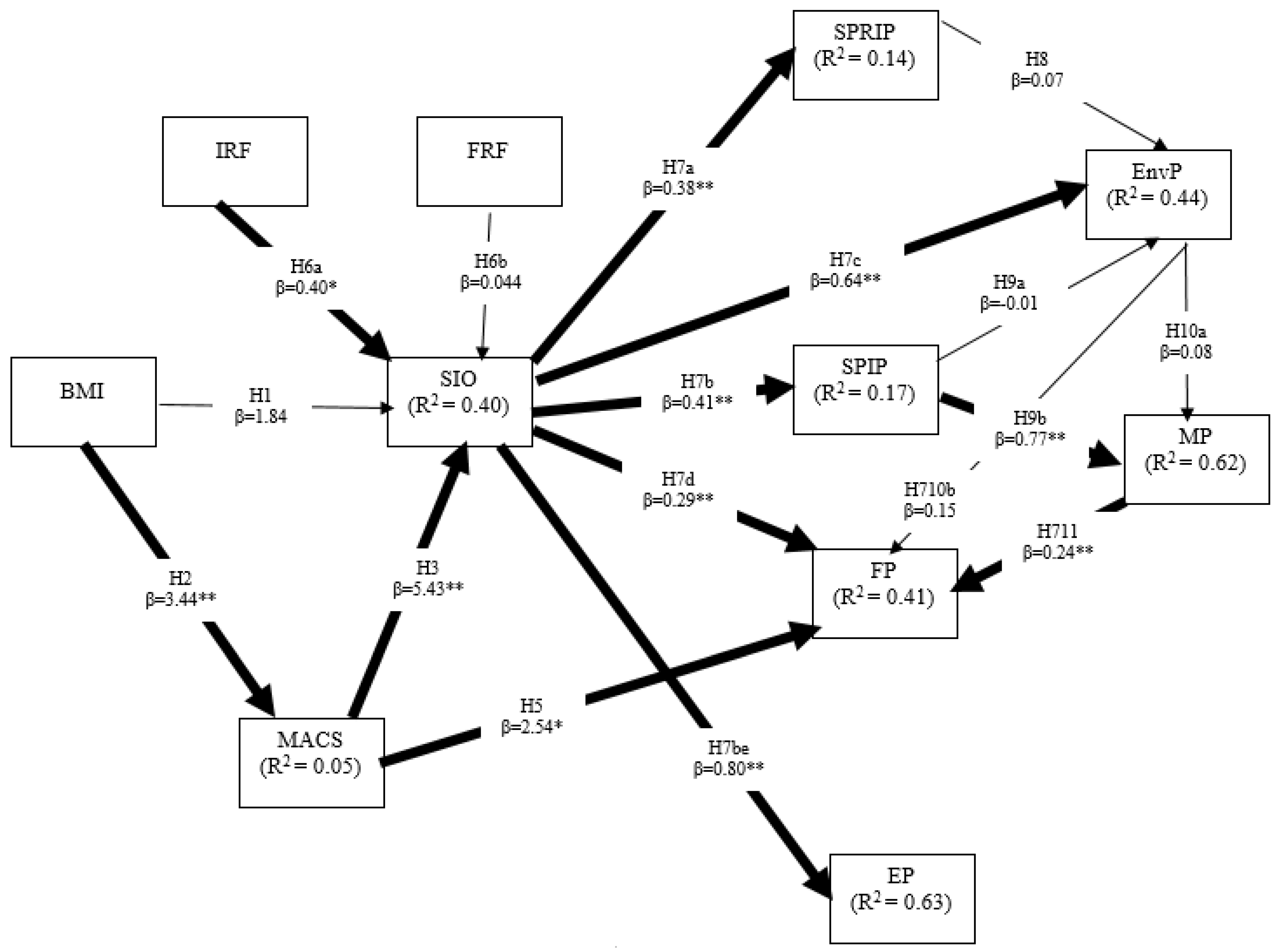

Hypothesis 2 (H2): A positive relationship exists between BMI and MACS.

Hypothesis 3 (H3): A positive relationship exists between MACS and SIO.

Hypothesis 4 (H4): MACS mediate the relationship between BMI and SIO.

Hypothesis 5 (H5): MACS positively influence financial performance.

2.4.3. Sustainable Innovation Orientation: Drivers and Outcomes

Even though sustainable innovation is still new and has not yet been exhaustively and empirically explored, Maletic et al. [

11] opined that it is a significant force that will drive change in business and society at large. Meanwhile, the factor that drives SIO still remains empirically unexplored. Some studies opined that SIO is being driven by internal resources [

8,

16,

46]. The study of Varadarajau [

14] highlights size, globalization, and reputation and slack as the firm-related factors that drive SIO. The study opined that more institutional pressure, especially from the stakeholders, will be on a large firm than the relatively smaller firms. This view corroborates the study of Haanaes et al. [

47], which found that a larger percentage of big firms tend to embrace sustainability than smaller firms. As for globalization, Varadarajau [

14] posited that global firms are often challenged with different institutional pressure urging them to show how committed they are to the sustainability of the environment where they operate.

Firm reputation was described by Brown et al. [

48] as the “set of corporate associations that individuals outside an organization believe are central, ensuring and distinctive to the organization”. It was argued in the study of Varadajau [

14] that reputation management by firms and the protection of their brand are among the factors underlying the “corporate social responsibility” (CSR) of firm activities. Hannaes et al. [

48] noted that firms with a favorable reputation in terms of sustainability are at advantage of receiving other benefits, such as the penetration of a new market, as well as attracting and retaining the best brains. Organizational slack is the fourth indicator of firm-related factors identified by Varadarajau [

14]. It was described by Bourgeouis [

49] (p. 30) as “that cushion of actual or potential resources which allows an organization to adapt successfully to internal pressures for adjustment or to external pressures for change”. Some previous studies have examined the role of slack in relation to sustainable innovations [

14]. Their studies suggest that while the slack allows managers to market their green market, the benefits do not seem to be immediate. Drawing from the literature, it shows there is a possible relationship between the firm-related factors and the firm’s sustainable innovation orientation [

14].

Moreover, the relative environmental impact of industry, the sustainability initiatives of firms in upstream supplies industries and downstream customer industries, and the size of the end user customer base are grouped and theorized as the industry-specific factors that drive SIO. Though each of the factors has been examined individually by previous authors, for instance, the relationship between the relative environmental impact of an industry and sustainable innovation [

16,

47,

50] and sustainability initiatives of firms in upstream supplies industries and downstream customer industries [

50]., the firm and industry-related factors are only theorized by Varadarajau [

14], and no empirical study has been conducted yet. It is on these grounds that we are proposing two factors as the drivers for SIO.

Furthermore, collaboration between a firm and external parties has been identified by some authors to be beneficial to the innovation process [

16,

50]. Ayuso et al. [

51] stressed that the achievement of SIO is driven my firms-related factors (such as balancing stakeholder interests and internally integrating their knowledge). This implies that the ability to use and share information with the stakeholder so as to capitalize on their knowledge could possibly help the organization in adapting to the external environmental changes in order to gain a competitive advantage in the market where they operate [

14].Meanwhile, Jorna [

52] observed that there is a challenge in measuring the significance of firm-related factors as a driver for SIO, as the study found that SIO is not only driven by firm-related factors but also by their interactions with the firm’s “internal and external stakeholders”. Therefore, it is imperative to have a better understanding of the determinants of SIO. In view of these, we propose the following hypothesis:

Hypothesis 6n (H6): Sustainable innovation orientation is positively influenced by (a) industry-related factors and (b) firm-related factors.

In reference to the resource-based view (RBV) [

54] and the extension (organizational capabilities) by Amit and Schoemaker [

55], both theories lend credence to the positive relationship between SIO and product and process innovation performance. Varadarajau [

15] corroborated the argument and posited that a high level of SIO over a certain period of time could lead to the company accumulating resources, and, more importantly, the capacity that is significant for the development and implementation of superior “sustainable process innovations and product innovations”. Moreover, it is expected that significant sustainable product innovation performance and sustainable process innovation would influence environmental performance. In the study of Kuckertz and Wagner [

56], it was argued that the achievement of a competitive advantage that is sustainable by an organization should encourage a firm to transform environmental concern into opportunities. This, they stressed, can only be achieved when the firm shares their internal environmental capabilities with the stakeholders. This, in turn, will lead to the firm achieving a competitive advantage that will be sustainable in the market where they operate.

Meanwhile, the literature on the relationship between SIO and financial performance suggests a positive relationship in the long term [

12,

15,

47]. An observation was made by Berrone and Gomez-Mejia [

57] that the relationship between environmental innovation and financial performance might not be linear, which implies that achieving acceptable environmental performance could take more time than expected, thereby increasing outcome uncertainty. Madsen and Rodgers [

58] therefore observed that while it is possible for a company to gather benefits that could be “reputational insurance, leniency from regulators, and decreased risk of public activism from their CRS activities”, there is a possibility for the cost of CRS to outweigh the benefits over a short period of time. However, positive outcomes are noted in the expected value of financial performance in the long run. The issue of financial performance and sustainable innovation was also investigated by Barnett and Salomon [

59]. The study observed that despite numerous studies on the relationship, the results were mixed. For instance, Luo and Bhattacharya [

60] investigated the relationship between CRS and financial performance, and the study found that positive, non-significant, or negative returns from CSR is possible under different environments. On the part of Chatterji, Levine, and Toffel [

61], it was stated that in case the CRS metrics are noisy indicators that are correct for CRS operations, a small correlation as an outcome could understate the link between expected CSR and financial performance. However, in a situation where bogus metrics are presented to the stakeholders, the possibility of achieving a positive correlation is high, with the attendant consequence being the overstating of the relationship between the expected CRS and financial performance.

In reference to the resource-based view (RBV) [

53] and the extension (organizational capabilities) by Amit and Schoemaker [

54], both theories lend credence to the positive relationship between SIO and product and process innovation performance. Varadarajau [

15] corroborated the argument and posited that a high level of SIO over a certain period of time could lead to the company accumulating resources, and, more importantly, the capacity that is significant for the development and implementation of superior “sustainable process innovations and product innovations”. Moreover, it is expected that significant sustainable product innovation performance and sustainable process innovation would influence environmental performance. In the study of Kuckertz and Wagner [

55], it was argued that the achievement of a competitive advantage that is sustainable by an organization should encourage a firm to transform environmental concern into opportunities. This, they stressed, can only be achieved when the firm shares their internal environmental capabilities with the stakeholders. This, in turn, will lead to the firm achieving a competitive advantage that will be sustainable in the market where they operate.

Meanwhile, the literature on the relationship between SIO and financial performance suggests a positive relationship in the long term [

11,

14,

46]. An observation was made by Berrone and Gomez-Mejia [

56] that the relationship between environmental innovation and financial performance might not be linear, which implies that achieving acceptable environmental performance could take more time than expected, thereby increasing outcome uncertainty. Madsen and Rodgers [

57] therefore observed that while it is possible for a company to gather benefits that could be “reputational insurance, leniency from regulators, and decreased risk of public activism from their CRS activities”, there is a possibility for the cost of CRS to outweigh the benefits over a short period of time. However, positive outcomes are noted in the expected value of financial performance in the long run. The issue of financial performance and sustainable innovation was also investigated by Barnett and Salomon [

58]. The study observed that despite numerous studies on the relationship, the results were mixed. For instance, Luo and Bhattacharya [

59] investigated the relationship between CRS and financial performance, and the study found that positive, non-significant, or negative returns from CSR is possible under different environments. On the part of Chatterji, Levine, and Toffel [

60], it was stated that in case the CRS metrics are noisy indicators that are correct for CRS operations, a small correlation as an outcome could understate the link between expected CSR and financial performance. However, in a situation where bogus metrics are presented to the stakeholders, the possibility of achieving a positive correlation is high, with the attendant consequence being the overstating of the relationship between the expected CRS and financial performance.

In reference to the relationship of the SIO to employee performance, some studies supported a positive relationship between SIO and employee performance [

11]. The study stressed that having a sense of belonging in a company that an employee works for is one of the social and psychological rewards that an employee expects from an organization [

47]. This is with the view that the feeling of being part of the firm will enhance the commitment of the employee, especially regarding a societal issue, such as environmental sustainability, through its SIO [

11].

In our study, drawing from the extant literature, we believe that if SIO is properly pursued by the manufacturing companies in UAE, the outcome from the SIO will influence sustainable process innovation performance, sustainable product innovation performance, environmental performance, financial performance, and employee performance. Thus, we propose the following hypothesis:

Hypothesis 7 (H7): Sustainable innovation orientation directly influences (a) sustainable process innovation performance, (b) sustainable product innovation performance, (c) environmental performance, (d) financial performance, and (e) employee performance.

Furthermore, it is expected that a firm will attract consumers that are environmentally conscious through SIO, will earn loyalty among green-conscious consumers, and will improve its reputation among a wider cross-section of society. On the other hand, in a market environment that is characterized by the growing of sustainability awareness among consumers in the stages of making decisions regarding brand choice where there is a high number of products, the consumers are likely to limit their set of considerations to the brands with a high sustainability rating. Although, the final decision could still be influenced by other factors, the inclusion or exclusion of which could be influenced by the sustainability attributes, the positive relationship between SIO and marketing performance is well-founded [

11,

14]. However, Claudy et al. [

61] studied the link between sustainable products and process innovations, and the consumer behaviors indicated that a wide gap exists between the consumer’s intention to purchase a green product and their actual behavior. For instance, their study shows that about 40% of the respondents were willing to purchase green product but only 4% actually did. A similar study by Luchs et al. [

62] submitted that for “strength-related” products, their attributes are valued, and the positive influence of sustainability characteristics on the consumer choice could be reduced and could sometimes result in consumers switching to other products, and this would negate the sustainability properties. The study then suggested that in such conditions, the company can reduce the potential negative influence of sustainability properties on the consumer choice by using “explicit cues” about the strength of the firm product.

Meanwhile, Olson [

63] was of the opinion that the general adoption of green products could possibly demand a “green tradeoff reduction and/or compensation for the tradeoff”, which would be possible by providing significant information on the merit of non-green properties in comparison to brown products, which are the alternatives. This view was in agreement with Kronrod, Grinstein, and Wathieu [

64], who observed that swaying customers to participates in eco-friendly activities poses a serious challenge as a result of the perception that most of the time, the beneficiaries are not the customers who participate in the eco-friendly behavior but that it is the other customers and society at large who benefits. It is on this note that we propose the following hypotheses:

Hypothesis 8 (H8): Sustainable process innovation performance directly influences environmental performance.

Hypothesis 9 (H9): Sustainable product innovation performance directly influences (a) environmental performance and (b) marketing performance.

Hypothesis 10 (H10): Environmental performance directly influences (a) marketing performance and (b) financial performance.

Hypothesis 11 (H11): Marketing performance directly influences financial performance.

{kind=link}

{kind=link}