Media and Institutional Investors Focus on the Impact on Corporate Sustainability Performance

Abstract

1. Introduction

2. Literature Review

2.1. A Review of Relevant Research on Media Attention

2.2. A Summary of Relevant Research on Institutional Investors’ Shareholdings

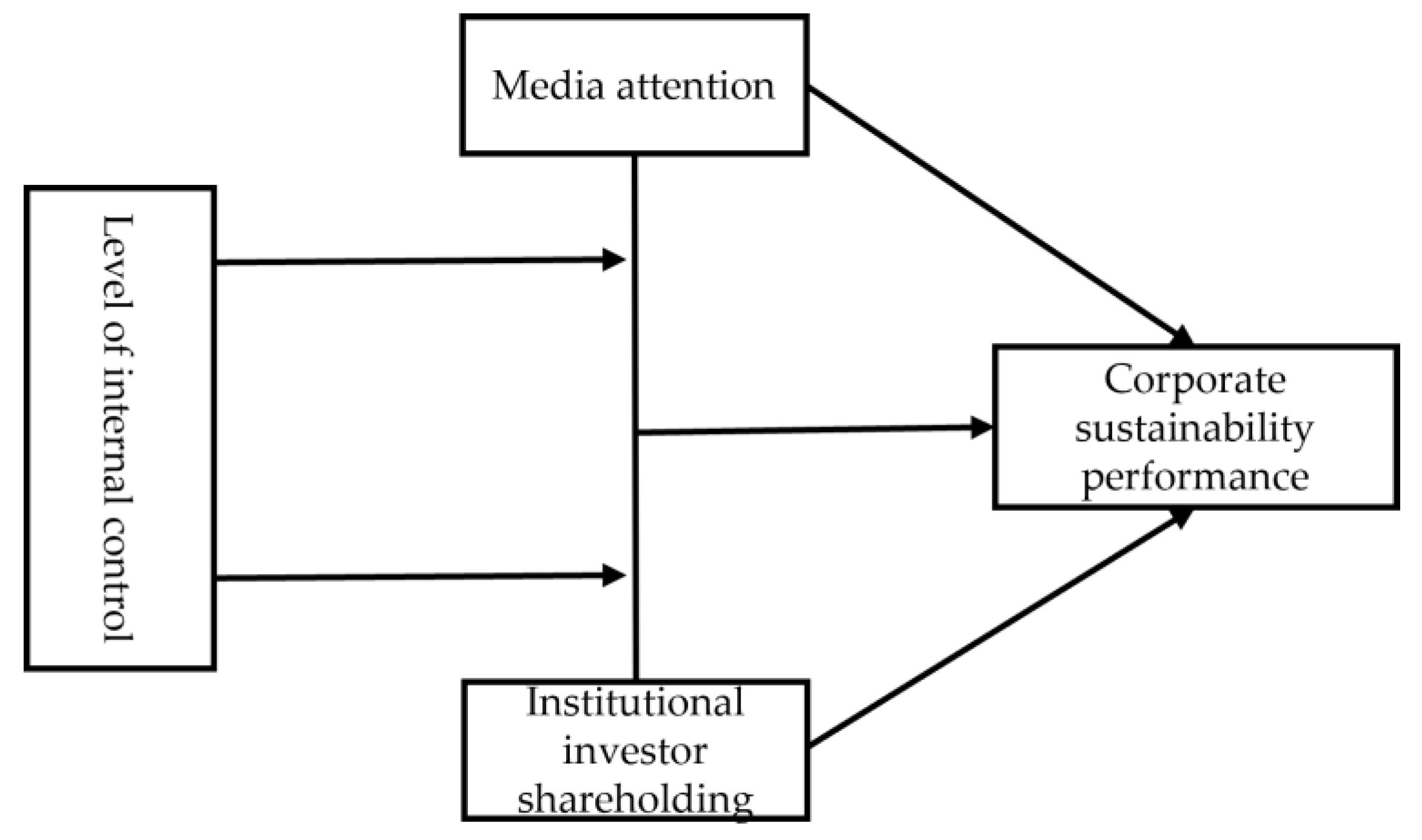

3. Theoretical Analysis and Research Hypotheses

3.1. Media Attention, Institutional Investor Shareholding, and Corporate Sustainability Performance

3.2. The Adjustment Effect of the Level of Internal Control of the Enterprise

4. Research Design

4.1. Sample Selection and Data Sources

4.2. Variable Selection

4.2.1. Explained Variable

4.2.2. Explanatory Variables

4.2.3. Adjustment Variables

4.2.4. Control Variables

4.3. Model Construction

5. Empirical Analysis and Discussion

5.1. Descriptive Statistics

5.2. Correlation Analysis

5.3. Analysis of Regression Results

5.4. Robustness Test

5.4.1. Endogenous Test

5.4.2. Robustness Check

6. Research Conclusions and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Dyck, A.; Volchkova, N.; Zingales, L. The corporate governance role of the media: Evidence from russia. J. Finance 2008, 63, 1093–1135. [Google Scholar] [CrossRef]

- Yang, D.G.; Chen, H.W.; Liu, Q.L. Media pressure and corporate innovation. Econ. Res. 2017, 52, 125–139. [Google Scholar]

- Zeng, W.; Liu, Z.J.; Zhang, Z. A study on media attention, internal control effectiveness and corporate performance volatility. J. Cent. South Univ. Soc. Sci. Ed. 2016, 22, 116–122. [Google Scholar]

- Bushee, B.J. The influence of institutional investors on myopic r&d investment behavior. Account. Rev. 1998, 73, 305–333. [Google Scholar]

- Korczak, P.; Tavakkol, A. Institutional investors and the information content of earnings announcements: The case of Poland. Econ. Syst. 2004, 28, 193–208. [Google Scholar] [CrossRef][Green Version]

- Hu, Q.Y. The correlation between environmental performance and financial performance of listed companies. China Popul. Resour. Environ. 2012, 22, 23–32. [Google Scholar]

- Li, W.J.; Lu, X.Y. Do institutional investors care about the environmental performance of firms?—Empirical evidence from listed companies in China’s heavily polluting industries. Financ. Res. 2015, 12, 97–112. [Google Scholar]

- Gao, J.; Kong, D.M.; Wang, R.M. Social well-being, media attention and corporate social responsibility. Zhejiang Soc. Sci. 2016, 9, 79–89 + 126 + 158. [Google Scholar]

- He, D.; Tang, T.; Chen, X.H. Institutional environment, institutional investors’ shareholding and corporate social responsibility. Invest. Res. 2018, 37, 122–146. [Google Scholar]

- Chen, C.-W.; Pantzalis, C.; Park, J.C. Press coverage and stock price deviation from fundamental value. J. Financ. Res. 2013, 36, 175–214. [Google Scholar] [CrossRef]

- Bushee, B.J.; Core, J.E.; Guay, W.; Hamm, S.J.W. The role of the business press as an information intermediary. J. Account. Res. 2010, 48, 1–19. [Google Scholar] [CrossRef]

- Reverte, C. Determinants of corporate social responsibility disclosure ratings by spanish listed firms. J. Bus. Ethics 2009, 88, 351–366. [Google Scholar] [CrossRef]

- Luo, D.L.; Chen, Q.; Shi, X.J. Media coverage, shareholder network relationships and firm performance. Invest. Res. 2022, 41, 85–106. [Google Scholar]

- Yuan, Y.H.; Xiong, X.H. A study on the relationship between esg performance and corporate performance of listed companies: The moderating effect of media attention. Jiangxi Soc. Sci. 2021, 41, 68–77. [Google Scholar]

- Tao, W.J.; Jin, Z.M. A study on the relationship between corporate social responsibility disclosure, media attention and corporate financial performance. J. Manag. 2012, 9, 1225–1232. [Google Scholar]

- Byun, S.; Oh, J.-M. Doing well by looking good: The causal impact of media coverage of corporate social responsibility on firm value. SSRN Electron. J. 2012. [Google Scholar] [CrossRef]

- Ying, Q.W.; Zhou, K.G.; Chen, S.S. Media attention and stock investment returns in the Chinese capital market—Risk compensation or attention drive? Secur. Mark. Her. 2015, 5, 33–42. [Google Scholar]

- Kang, J.J.; Wang, M.; Fan, Y.J. Media coverage, accounting robustness and the risk of stock price collapse. J. Nanjing Audit Univ. 2021, 18, 32–41. [Google Scholar]

- Song, J.; Zhang, J.M.; Li, H.Y. Can media coverage alleviate corporate financing constraints? Based on the perspective of commercial credit financing. J. Beijing Univ. Technol. Bus. Soc. Sci. Ed. 2019, 34, 60–73. [Google Scholar]

- Luo, J.H. The impact of media coverage on the cost of equity and the cost of debt and its differences—Empirical evidence from Chinese listed companies. Invest. Res. 2012, 31, 95–112. [Google Scholar]

- Porter, M.E.; Kramer, M.R. Strategy and society: The link between competitive advantage and corporate social responsibility. Harv. Bus. Rev. 2006, 84, 78–92, 163. [Google Scholar] [PubMed]

- Brammer, S.; Pavelin, S. Voluntary Social Disclosure by Large UK Companies. Bus. Ethics Eur. Rev. 2004, 13, 86–99. [Google Scholar] [CrossRef]

- Tang, Z.; Tang, J. Can the media discipline chinese firms’ pollution behaviors? The mediating effects of the public and government. J. Manag. 2016, 42, 1700–1722. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D. Media legitimacy and corporate environmental communication. Account. Organ. Soc. 2009, 34, 1–27. [Google Scholar] [CrossRef]

- Chen, J.P.; Li, Y.P. A study on the relationship between environmental performance and financial performance from the perspective of media attention—Empirical evidence based on Chinese listed companies. Financ. Account. Newsl. 2014, 68, 106–108. [Google Scholar]

- Xu, L.P.; Chen, L.; Zhang, S.X.; Liu, N. Corporate top environmental tone, media attention and environmental performance. East China Econ. Manag. 2018, 32, 114–123. [Google Scholar]

- Frankel, R.; Kothari, S.P.; Weber, J. Determinants of the informativeness of analyst research. J. Account. Econ. 2006, 41, 29–54. [Google Scholar] [CrossRef]

- Beyer, A.; Cohen, D.A.; Lys, T.Z.; Walther, B.R. The financial reporting environment: Review of the recent literature. J. Account. Econ. 2010, 50, 296–343. [Google Scholar] [CrossRef]

- Cheng, X.; Yang, Z.J.; Wan, X.Y. Institutional investors, information transparency and stock price volatility. Invest. Res. 2018, 37, 55–77. [Google Scholar]

- Liu, J.H.; Chen, X.D.; Zhang, F.F.; Xie, J.Z. Institutional investors, volatility and stock returns—An empirical study based on Shanghai and Shenzhen a-share stock markets. Macroecon. Res. 2013, 6, 45–56 + 99. [Google Scholar]

- Ward, C.; Yin, C.; Zeng, Y. Institutional investor monitoring motivation and the marginal value of cash. J. Corp. Financ. 2018, 48, 49–75. [Google Scholar] [CrossRef]

- Clay, D.G. Institutional Ownership and Firm Value; S & P Global Market Intelligence Research Paper Series; S & P Global: Arlington, VA, USA, 2002. [Google Scholar]

- Shi, M.J.; Tong, W.H. Do institutional investors enhance firm value?—Empirical evidence from the post-share reform period. Financ. Res. 2009, 10, 150–161. [Google Scholar]

- Zhao, Y.H.; Guo, M.L. Research on the impact of institutional investors’ shareholding on firm value—An empirical study based on the perspective of institutional investors’ heterogeneity. Price Theory Pract. 2019, 22, 88–91. [Google Scholar]

- David, P.; Kochhar, R. Barriers to effective corporate governance by institutional investors: Implications for theory and practice. Eur. Manag. J. 1996, 14, 457–466. [Google Scholar] [CrossRef]

- Khan, R.; Dharwadkar, R.; Brandes, P. Institutional ownership and ceo compensation: A longitudinal examination. J. Bus. Res. 2005, 58, 1078–1088. [Google Scholar] [CrossRef]

- Oh, W.-Y.; Chang, Y.; Martynov, A. The effect of ownership structure on corporate social responsibility: Empirical evidence from korea. J. Bus. Ethics 2011, 104, 283–297. [Google Scholar] [CrossRef]

- Bae, B.; Sami, H. The effect of potential environmental liabilities on earnings response coefficients. J. Account. Audit. Finance 2005, 20, 43–70. [Google Scholar] [CrossRef]

- Kacperczyk, M.T.; Hong, H.G. The price of sin: The effects of social norms on markets. J. Financ. Econ. 2006, 93, 15–36. [Google Scholar] [CrossRef]

- Amel-Zadeh, A.; Serafeim, G. Why and how investors use esg information: Evidence from a global survey. Financ. Anal. J. 2018, 74, 103–187. [Google Scholar] [CrossRef]

- Zhang, R.; Guan, K.L. Executive embezzlement-based job crimes, institutional investors and market reactions—Empirical evidence from Chinese listed companies. Account. Res. 2017, 12, 52–58 + 97. [Google Scholar]

- Zhao, Y.; Shen, H.T.; Zhou, Y.K. Environmental information asymmetry, institutional investors’ field research and corporate environmental governance. Stat. Res. 2019, 36, 104–118. [Google Scholar]

- Wang, H.M.; Lv, X.J.; Lin, W.F. The impact of foreign equity participation and executive and institutional shareholding on corporate social responsibility: An empirical study based on Chinese a-share listed companies. Account. Res. 2014, 8, 81–87 + 97. [Google Scholar]

- Guan, J.; Que, Y. Research on the relationship between performance feedback, institutional investors’ shareholding and corporate environmental performance. J. Cent. South Univ. Soc. Sci. Ed. 2020, 26, 124–138. [Google Scholar]

- Xu, N.; Yan, M.Z. Research on the impact of media attention and corporate social responsibility on corporate performance. Hubei Soc. Sci. 2013, 7, 82–85. [Google Scholar]

- Huang, H. Negative media coverage, market reaction and corporate performance. China Soft Sci. 2013, 8, 104–116. [Google Scholar]

- Chen, Z.J.; Min, Y.J. Family control and corporate social responsibility: An explanation based on socio-emotional wealth theory. Econ. Manag. 2015, 37, 42–50. [Google Scholar]

- Jiang, G.S.; Lu, J.C.; Li, W.A. Do Green Investors Make a Difference?—An empirical study of corporate participation in green governance. Financ. Res. 2021, 5, 117–134. [Google Scholar]

- Chen, Z.J.; Dong, M.T.; Ma, P.C.; Min, Y.J. The Interaction between Media and Institutional Investors’ Concerns on Internal Control: Empirical Data from State-owned Enterprises. Financ. Trade Res. 2020, 31, 99–110. [Google Scholar]

- Xie, X.M.; Zhu, Q.W. How to solve the problem of “harmonious coexistence” in corporate green innovation practices? Manag. World 2021, 37, 128–149 + 129. [Google Scholar]

- Xi, L.S.; Zhao, H. Executive dual environmental perceptions, green innovation and corporate sustainability performance. Econ. Manag. 2022, 44, 139–158. [Google Scholar]

- Wang, J.X.; Liao, Z.C. Media attention and high-quality development of state-owned enterprises: A path analysis based on internal control. J. Jishou Univ. Soc. Sci. Ed. 2022, 43, 55–64. [Google Scholar]

- Wang, H.F.; Wang, X.Y.; Wang, M.T.; Zhang, X.Y. Institutional investors’ shareholding, dual innovation and firm value—An analysis based on the perspective of optimizing business environment. Price Theory Pract. 2021, 417, 114–117 + 198. [Google Scholar]

- Wang, Y.; Guo, Z.G. Institutional investors’ shareholding and total factor productivity of firms: Effective or ineffective monitoring. J. Shanxi Univ. Financ. Econ. 2021, 43, 113–126. [Google Scholar]

{kind=link}

| Variable Category | Variable Name | Variable Name | Variable Definitions |

|---|---|---|---|

| Explained variable | Sustainability Performance | Sustain | According to the return on total assets (ROA) of the company and the social and environmental responsibility score of Hexun.com, it is calculated using the entropy weight method. |

| Explanatory variables | Media attention | Media | Add 1 to the number of newspapers and Internet business information reports to get the logarithmic value |

| Institutional investor shareholding | Inst | Institutional investors’ share of total equity | |

| Moderator | Level of internal control | IC | Add one to the internal control index provided by Dibo Company to get the logarithmic value |

| Control variables | Company Size | Size | Natural logarithm of annual total assets |

| Assets and liabilities | Lev | Annual Total Liabilities/Annual Total Assets | |

| Business growth | Growth | Operating income for the current year/operating income for the previous year−1 | |

| Number of directors | Board | The natural logarithm of the number of directors | |

| Proportion of independent directors | Indep | Number of independent directors/directors | |

| Two jobs in one | Dual | 1 if the chairman and manager are the same person, 0 otherwise | |

| Ownership concentration | Top1 | Number of shares held by the largest shareholder/total number of shares | |

| Equity balance | Balance | The sum of the shareholding ratio of the second to five largest shareholders/the shareholding ratio of the first largest shareholder |

| Variable | Obs | Mean | Std. Dev. | Min | Max |

|---|---|---|---|---|---|

| Sustain | 9117 | 0.524 | 0.518 | 0.0130 | 0.851 |

| Media | 9119 | 4.389 | 1.212 | 0 | 8.04 |

| Inst | 9119 | 0.520 | 0.197 | 0 | 0.987 |

| IC | 9023 | 6.5 | 0.15 | 2.194 | 6.903 |

| Size | 9119 | 22.723 | 1.39 | 18.833 | 28.636 |

| Lev | 9119 | 0.492 | 0.194 | 0.022 | 1.352 |

| Growth | 9119 | 0.447 | 19.888 | −0.953 | 1878.372 |

| Board | 9106 | 2.176 | 0.2 | 1.386 | 2.996 |

| Indep | 9106 | 0.372 | 0.057 | 0.125 | 0.8 |

| Dual | 8945 | 0.153 | 0.36 | 0 | 1 |

| Top 1 | 9119 | 0.356 | 0.156 | 0.034 | 0.9 |

| Balance | 9119 | 0.576 | 0.567 | 0.004 | 3.731 |

| Sustain | Media | Inst | Inc | Size | Lev | Growth | Board | Indep | Dual | Top 1 | Balance | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Sustain | 1.000 *** | |||||||||||

| media | 0.057 *** | 1.000 *** | ||||||||||

| inst | 0.167 *** | 0.064 *** | 1.000 *** | |||||||||

| inc | 0.309 *** | 0.061 *** | 0.193 *** | 1.000 *** | ||||||||

| Size | −0.002 | 0.225 *** | 0.432 *** | 0.205 *** | 1.000 *** | |||||||

| Lev | −0.337 *** | 0.142 *** | 0.148 *** | 0.041 *** | 0.464 *** | 1.000 *** | ||||||

| Growth | −0.001 | 0.013 | 0.032 *** | 0.020 * | 0.037 *** | 0.025 ** | 1.000 *** | |||||

| Board | 0.014 | 0.030 *** | 0.199 *** | 0.075 *** | 0.223 *** | 0.093 *** | 0.027 ** | 1.000 *** | ||||

| Indep | −0.031 *** | 0.033 *** | −0.031 *** | 0.021 ** | 0.085 *** | 0.041 *** | −0.008 | −0.418 *** | 1.000 *** | |||

| Dual | 0.015 | 0.035 *** | −0.182 *** | −0.043 *** | −0.064 *** | −0.047 *** | 0.024 ** | −0.160 *** | 0.084 *** | 1.000 *** | ||

| Top 1 | 0.080 *** | −0.037 *** | 0.634 *** | 0.121 *** | 0.233 *** | 0.100 *** | −0.001 | 0.052 *** | 0.043 *** | −0.132 *** | 1.000 *** | |

| Balance | 0.018 * | 0.079 *** | −0.107 *** | −0.022 ** | 0.032 *** | −0.044 *** | 0.027 ** | 0.053 *** | −0.051 *** | 0.082 *** | −0.643 *** | 1.000 *** |

| (1) | (2) | (3) | (4) | (5) | |

|---|---|---|---|---|---|

| Sustain | Sustain | Sustain | Sustain | Sustain | |

| Media | 0.002 *** | 0.004 *** | 0.108 *** | ||

| (4.77) | (4.10) | (3.11) | |||

| Inst | 0.048 *** | 0.068 *** | 1.094 *** | ||

| (9.69) | (6.98) | (3.36) | |||

| −0.005 ** | −0.225 *** | ||||

| (−2.47) | (−3.46) | ||||

| IC | 0.131 *** | ||||

| (4.93) | |||||

| −0.016 *** | |||||

| (−2.96) | |||||

| −0.159 *** | |||||

| (−3.17) | |||||

| 0.034 *** | |||||

| (3.38) | |||||

| Size | 0.012 *** | 0.012 *** | 0.010 *** | 0.010 *** | 0.008 *** |

| (12.95) | (12.70) | (10.57) | (10.16) | (8.25) | |

| Lev | −0.113 *** | −0.113 *** | −0.109 *** | −0.109 *** | −0.098 *** |

| (−28.81) | (−28.86) | (−27.95) | (−27.99) | (−25.85) | |

| Growth | 0.000 | 0.000 | 0.000 | 0.000 | −0.000 |

| (0.39) | (0.33) | (0.14) | (0.24) | (−0.28) | |

| Board | −0.003 | −0.002 | −0.003 | −0.002 | −0.003 |

| (−0.68) | (−0.55) | (−0.79) | (−0.63) | (−0.88) | |

| Indep | 0.001 | 0.000 | 0.001 | 0.000 | 0.000 |

| (0.08) | (0.04) | (0.09) | (0.02) | (0.01) | |

| Dual | −0.001 | −0.001 | −0.001 | −0.001 | −0.001 |

| (−0.95) | (−0.97) | (−0.93) | (−0.92) | (−0.48) | |

| Top1 | 0.034 *** | 0.034 *** | −0.012 | −0.012 | −0.014 * |

| (5.11) | (5.09) | (−1.52) | (−1.45) | (−1.75) | |

| Dturn | 0.000 | −0.001 | 0.001 | −0.001 | −0.001 |

| (0.33) | (−0.53) | (0.56) | (−0.49) | (−1.11) | |

| Balance | 0.004 *** | 0.004 ** | −0.005 *** | −0.005 *** | −0.005 *** |

| (2.69) | (2.54) | (−2.79) | (−2.89) | (−3.18) | |

| _cons | 0.306 *** | 0.301 *** | 0.348 *** | 0.336 *** | −0.470 *** |

| (11.23) | (11.06) | (12.69) | (12.22) | (−2.71) | |

| Year | Yes | ||||

| Industry | Yes | ||||

| Adj R2 | 0.044 | 0.047 | 0.055 | 0.058 | 0.111 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| First | Second | First | Second | |

| Media | Sustain | Inst | Sustain | |

| M-Media | 0.926 *** | |||

| (13.78) | ||||

| M-Inst | 0.441 *** | |||

| (5.87) | ||||

| Media | 0.005 ** | |||

| (2.01) | ||||

| Inst | 0.241 *** | |||

| (3.94) | ||||

| Constant | −5.303 *** | 0.415 *** | −0.967 *** | 0.588 *** |

| (−14.22) | (42.04) | (−20.25) | (12.48) | |

| Controls | Yes | |||

| Year | Yes | |||

| Industry | Yes | |||

| Adj R2 | 0.28 | 0.63 | ||

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Sustain | Sustain | Sustain | Sustain | Sustain | Sustain | |

| Media_w | 0.002 *** | |||||

| (4.75) | ||||||

| Inst_w | 0.049 *** | |||||

| (9.68) | ||||||

| L.Media | 0.004 *** | |||||

| (2.80) | ||||||

| L.Inst | 0.006 *** | |||||

| (6.23) | ||||||

| Media | 0.001 ** | |||||

| (2.19) | ||||||

| Inst | 0.031 *** | |||||

| (6.17) | ||||||

| TobinQ | 0.006 *** | 0.006 *** | ||||

| (16.23) | (15.11) | |||||

| _cons | 0.301 *** | 0.348 *** | 0.303 *** | 0.335 *** | 0.223 *** | 0.257 *** |

| (11.06) | (12.68) | (11.05) | (12.14) | (8.10) | (9.19) | |

| Year | Yes | |||||

| Industry | Yes | |||||

| Adj R2 | 0.047 | 0.055 | 0.043 | 0.049 | 0.075 | 0.079 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, C.; Wang, X. Media and Institutional Investors Focus on the Impact on Corporate Sustainability Performance. Sustainability 2022, 14, 13878. https://doi.org/10.3390/su142113878

Liu C, Wang X. Media and Institutional Investors Focus on the Impact on Corporate Sustainability Performance. Sustainability. 2022; 14(21):13878. https://doi.org/10.3390/su142113878

Chicago/Turabian StyleLiu, Chuanzhe, and Xu Wang. 2022. "Media and Institutional Investors Focus on the Impact on Corporate Sustainability Performance" Sustainability 14, no. 21: 13878. https://doi.org/10.3390/su142113878

APA StyleLiu, C., & Wang, X. (2022). Media and Institutional Investors Focus on the Impact on Corporate Sustainability Performance. Sustainability, 14(21), 13878. https://doi.org/10.3390/su142113878