Spatial Heterogeneity Effects of Green Finance on Absolute and Relative Poverty

Taiwan Research Institute, Xiamen University, Xiamen 361005, China

*

Author to whom correspondence should be addressed.

Sustainability 2023, 15(7), 6206; https://doi.org/10.3390/su15076206

Submission received: 1 March 2023

/

Revised: 27 March 2023

/

Accepted: 30 March 2023

/

Published: 4 April 2023

Abstract

:In light of the growing emphasis on sustainable development, financial poverty alleviation has become an increasingly important strategy. This study explores whether green finance, a new financial tool aimed at achieving sustainable development, can effectively reduce poverty. Using data from 25 provinces in China between 2004 and 2019, the study builds the China Green Financial Development Index, using the improved entropy power method, and uses a spatial econometric model to analyze the linear and non-linear impact of green finance on absolute and relatively poor poverty. The results demonstrate that green finance has a positive impact on poverty reduction, with a more significant impact on rural poverty reduction than urban poverty reduction. Interestingly, non-linear results reveal that the impact of green finance on rural poverty alleviation has gradually weakened, while the impact on urban poverty alleviation has gradually increased. Moreover, the introduction of technological progress as an intermediary variable has revealed an intermediary effect between green finance and poverty reduction. Overall, this study contributes to our understanding of the link between green finance and poverty and suggests a new approach to poverty alleviation.

1. Introduction

As society progresses and develops, social contradictions are constantly changing, but world poverty has always been a major issue. To improve the lives of people, the government and scholars began to pay attention to the role of financial development in poverty alleviation. Studies have found that financial development can promote economic development, so people began to study the relationship between financial development and poverty. As China’s economy shifts from high-speed development to high-quality development, the impact of green finance on poverty should be considered from the perspective of sustainable economic development. Despite not having developed a green finance index system from the national level, many developing countries have prioritized green finance development as a core strategy of national development. For example, the fourteenth five-year period is the critical period and window period for carbon peak. The Central Committee of the Communist Party of China and the State Council have entrusted the financial system with the glorious mission and important task of supporting green, low-carbon, and high-quality development in the financial sector in the new period and new stage. The financial sector should focus on carbon peak and carbon neutrality, plan of green finance, and give priority to the three supporting functions of finance (Zhao, 2022) [1].

As the largest developing country, poverty and relative poverty have always been an important problem restricting China’s development. In order to better solve the problem of poverty and relative poverty, we must deeply understand the causes of poverty and relative poverty. Since China’s reform and opening up, the Chinese economy has experienced rapid development, but there has been a wider income gap for urban people and rural people, due to the dual economic structure of urban and rural areas. This phenomenon is mainly driven by urban and rural development patterns; the developmental pattern mainly makes the rural develop by small-scale peasant economy, unable to realize the rapid development of economy. In conclusion, the gap between urban and rural income continues to widen. Starting from the urban-rural dual economic structure, using green finance to alleviate rural poverty, urban poverty, and relative poverty between cities, and rural areas from various aspects through a spatial econometric model, is discussed in this paper.

White (1996) first put forward the concept of environmental finance. By analyzing the role of corporate finance, he concluded that investment and financial institutions in solving environmental threats and environmental protection must be developed in a coordinated manner, and it is important to promote green finance, which is the embryonic form of green financing [2]. Scholten (2006) deeply studied the internal relationship between sustainable development and finance and proposed that green finance is to seek the optimal solution of environmental protection through a variety of financial tools [3]. Soundarrajan and Vivek (2016) studied the effectiveness of green finance in India’s industrial development. They found that green finance can be effectively applied to India’s industrial system, reduce environmental risks, and improve ecological integrity [4]. The study by Ngan (2018) identified and assessed the risk factors for slow growth in green economies in developing countries. As a result, financing risk is the main concern of the industry, followed by technology risk and supply chain risk [5]. Taghizadeh-Hesary and Yoshino (2020) found that investors can benefit from the spillover effect of green finance, using the relevant investment theory model by the use of related investment theoretical models, so as to expand the development level of green finance, reduce the risk of green finance, and improve the return rate of green energy [6]. Green finance policies are discussed by Yu et al. (2021) in relation to how they resolve financing constraints of firms for green innovation. Despite green finance policies’ ability to alleviate financing restraints on green innovation, generally, private enterprises are less likely to have access to green credits. In spite of this, these enterprises with severe financing constraints are relatively innovative [7].

The World Bank points out that the poor population’s average income is less than $100 by linking the poor with the gross national product. The main cause of poverty has been found to be urban and rural dual structures in a number of studies. The urban-rural dual structure is generally considered to be an economic structure in which urban economy and small-scale peasant production coexist. Urban economy is dominated by modern industry, while rural economy is dominated by small-scale peasantry, which leads to the transfer of the rural labor force to central cities and towns. This development model makes urban people richer and rural people poorer. The existence of the urban-rural dual structure requires that we should separate the rural and urban areas for discussion and put forward a more reasonable poverty reduction plan. This paper divides poverty into urban poverty and rural poverty, and this study examines how green finance can alleviate two types of poverty.

At present, there is little research on the effect of green finance on poverty alleviation, but there is more research on the effect of financial development. Financial development’s impact on scholars and poverty reduction are mainly divided into several representative views.

First, poverty alleviation is believed to be a result of financial development. Beck et al. (2007) investigated the relationship between finance, inequality, and poverty through empirical research [8]. Poor people’s income levels were improved by financial development and reduced the inequality of income to a certain extent. South Africa’s financial development, economic growth, and poverty reduction are examined by Odhiambo (2009) [9]. According to the study’s empirical findings, both financial development and economic growth are both responsible for poverty reduction in South Africa. AnneWelle–Strand (2010) compared several poverty eradication tools and found that microfinance can alleviate poverty more than social integration or institutional construction [10]. Inoue and Hamori (2011) investigated the impact of financial deepening on poverty reduction in India. In controlling international openness, the inflation rate, and economic growth, empirical results demonstrated that financial deepening significantly reduces poverty [11]. Abosedraet (2015) used data from 1975 to 2011 to analyze the relationship between Egyptian financial development and poverty reduction. He found that, if domestic credit to the private sector was used to indicate financial development, financial development could reduce poverty [12]. Park (2015) selected data from 37 Asian economies to test the impact of inclusive financial development on poverty and income inequality [13]. According to the results, inclusive financial development reduced poverty and narrowed the income gap. Li and Wang (2017) found that there are some limitations in the practice of financial poverty alleviation, but with the help of internet finance there can still be benefits from financial markets [14]. Raberto et al. (2016) found that there was a significant negative correlation between financial development and poverty through empirical research [15]. Meghana et al. (2020) found that the poverty rate has decreased due to financial deepening and that financial deepening will make rural areas migrate to the tertiary industry in urban areas, thus reducing the poverty level in rural areas [16]. David and Varaidzo (2020) found that financial inclusion is helpful to achieve seven of seventeen sustainable development items. Using simple linear regression, they found that the reduction of small-scale agricultural production is strongly influenced by financial inclusion. Therefore, the government of Zimbabwe must implement the financial inclusion policy in an all-round way to ensure the realization of the poverty reduction and poverty alleviation task [17]. Xiong (2022) investigated the relationship between digital inclusive finance and poverty reduction, using regional economic development as an intermediary variable. The study revealed a threshold effect of digital finance on poverty alleviation, where an increase in the threshold led to a gradual increase in the poverty reduction effect of digital inclusive finance [18]. Li (2022) focused on rural areas and explored the impact of inclusive finance on poverty reduction, using rural income as an intermediary variable. The study found that inclusive finance can promote people’s income in Xinjiang, reduce poverty at a deeper level, and increase farmers’ income [19]. Zhao (2022) and Yu (2021) analyzed the impact of digital inclusive finance on narrowing the urban-rural income gap using the intermediary effect model and the primary distribution theory. They found that digital inclusive finance has significant regional heterogeneity, but overall, it can effectively narrow the urban-rural income gap [20,21]. Finally, Song (2023) investigated the impact of digital finance on agricultural income from multiple perspectives using multiple intermediary effect models. The study revealed that digital finance can improve investment and land circulation to increase agricultural income but can also reduce labor force [22].

Second, financial development has a negative effect on poverty alleviation. Ravallion (1997, 2001) found that finance can alleviate poverty to some extent, but the inequality caused by finance also makes the poverty level deeper [23]. According to Maurer and Ha (2007), financial development can contribute to economic growth, but economic development often flows to high-income groups, and low-income people cannot get more funds, which will eventually widen the income gap and deepen the poverty level [24].

Third, it is unclear how financial development affects poverty alleviation. Greenwood and Jovanovic (1990) proposed that, when poor people have a low income at the beginning of their lives, they will not be able to obtain the financial services they want, so poverty cannot be effectively solved; when the initial income of poor people is very high, it will be easy for people to obtain financial services, and the poverty level will be reduced. Financial development has a complex impact on poverty alleviation, which is shown in the Kuznets curve, namely, the influence of financial development on income reduction shows a downward U-shaped trend [25]. Financial development and poverty in developing countries were examined by Perez-Moreno (2011). No Granger causality between poverty and financial development was demonstrated by the analysis [26].

Green finance has the potential to promote sustainable development and innovation in enterprises, leading to economic growth and poverty reduction. Recent studies by Ji (2020), Yang (2022), and Li (2022) indicated that enterprises with strong green social responsibility enjoy lower financing costs and are encouraged to undertake more social responsibilities, thereby promoting the common development of both enterprises and society [27,28,29]. Cao’s (2021) analysis of corporate credit policy revealed that green credit can increase long-term bank credit and reduce the risk of polluting corporate risk mismatch [30]. Dong (2022) suggested that listed companies should promote green innovation and enterprise transformation, as green finance can reduce long-term debt ratios and foster high-quality development [31]. Xiang (2022) and Li (2022) found that external financing favors green innovation, and government subsidies can increase corporate development subsidies to a certain extent, while green finance promotes green innovation through debt financing and equity financing [32,33]. Meanwhile, Chai (2022) and Peng (2022) discovered that green credit plays an important role in corporate financing for heavily polluting enterprises, helping them obtain more funds to support their upgrading and transformation [34,35]. Lai’s (2022) study on the impact of green credit on new energy companies found that it not only reduces financing costs, but also directly increases corporate value, with a long-term sustainability effect [36]. As a result, more scholars have begun to explore the impact of green credit on financing efficiency, revealing that, while the overall financing efficiency of Chinese enterprises has been restricted, the improvement of the green financial environment has led to significant enhancements (Yu, 2022; Li, 2022; Ming, 2022) [37,38,39].

Lili Jiang et al. (2020) assessed poverty alleviation through green finance and found that green finance is helpful for poverty alleviation, but there is room for improvement. Firstly, the method of year-by-year construction is adopted in the construction of the green finance index. As a result, green finance development index comparisons cannot be done in time. Secondly, in the empirical study, poverty is measured by per capita consumption expenditure, but it is not intuitive to use this index as the proxy variable of poverty. Thirdly, the spatial effect of poverty is not considered in this paper. Fourthly, the article does not consider the urban-rural dual structure of poverty in China [40].

Compared with the existing research, improvements are made in the following areas in this paper: (1) the linear and nonlinear relationship between green finance and relative and absolute poverty is studied from multiple perspectives; (2) using the number of urban and rural poor people in China as the proxy variable of poverty, which can more directly reflect the poverty level in China and can also further analyze the impact of green finance on poverty alleviation under the dual structure of urban and rural areas; (3) previous studies have primarily focused on linear studies, but this paper aims to expand the analysis by introducing a semi-parametric spatial lag model to study the dynamic change process of green finance poverty reduction from a nonlinear perspective. This approach provides a foundation for more nuanced and quantitative studies of the impact of green finance on poverty reduction; (4) in addition, this paper also introduces scientific and technological progress as an intermediary variable to further clarify the impact mechanism of green finance on poverty reduction. This allows for a deeper exploration of the complex relationship between green finance, technological progress, and poverty reduction, and provides theoretical support for subsequent analysis.

2. Theoretical Analysis

2.1. Theoretical Analysis of Poverty

In green finance, the ecological environment is protected, while economic development is promoted and quality economic development is achieved. Through financial innovation, green finance invests in environmental protection, energy conservation, and clean energy projects, while achieving the goals of economic development and environmental protection. The only way to achieve high-quality economic development is through green finance. The year 2021 is the first year for China to fully lift itself out of poverty. Due to the impact of COVID-19, China’s economic growth lacks momentum. In order to prevent the return to poverty and achieve rapid economic development, people began to discuss whether green finance can alleviate poverty and relative poverty in urban and rural areas. From a macro point of view, the essence of finance is to optimize its own interests as much as possible. In the market, financial companies often ignore the social costs, caused by doing so in pursuit of higher profits. Green finance has reduced the number of enterprises with high pollution and energy consumption, put the economy on a path of sustainable development, promoted high-quality economic development, and put forward a new method for effectively alleviating poverty and relative poverty. As seen from a micro perspective, green finance has given help and inspiration to rural areas. Modern financial tools and green sustainable development theory are combined to provide new development opportunities for poor people. Whether individuals can obtain high-quality financial services from the development of green finance mainly depends on three aspects: first, whether to provide innovative products. Since people in different regions of China have different needs, personalized financial products should be provided according to different needs of people; second, the promotion of financial products. As a result of China’s short development period for green finance, many areas, especially remote areas, cannot enjoy the help brought by green finance; third, whether residents have enough knowledge to obtain the financial products they want. Lusardi and Mitchell (2011) pointed out that education has a certain relationship with financial literacy. Low-income families have relatively low educational attainment and usually have low financial literacy. Families with high incomes typically have higher levels of education and financial literacy. Such a huge difference in financial literacy will lead to an obvious “knowledge gap”, which will further aggravate relative poverty [41].

Green finance is grounded in the principles of sustainable development theory, which aims to achieve poverty reduction. Sustainable development theory emphasizes the importance of long-term, stable economic development, while also emphasizing social and environmental harmony. Green finance serves as a crucial tool to achieve sustainable development by promoting the growth of green industries, such as renewable energy use, energy efficiency improvement, and sustainable agriculture development. Green finance creates new employment opportunities, increases income, and improves living standards, thereby reducing poverty. Furthermore, it helps to mitigate the negative impact of climate change and environmental degradation, which disproportionately affects the poor. Therefore, the theoretical basis of green finance poverty reduction is rooted in sustainable development principles that emphasize the significance of balanced economic growth, social welfare, and environmental protection.

Due to a lack of innovative financial products, this paper points out that some low-income families cannot get personalized financial products; financial products cannot be promoted in remote areas due to remote areas and lack of professional talents. The educational level of some low-income families is lower than that of rich families, and there is a “knowledge gap” phenomenon, which results in low-income families being unable to enjoy the benefits brought by green finance. With the development of green finance, financial enterprises are constantly seeking innovation and launching new financial products, effectively alleviating the problem of non-responsive financial products in remote areas. To a large extent, staff training and promotion correspond. Meanwhile, as education levels continue to improve, the financial literacy of residents in remote areas has been greatly improved.

2.2. Indicators for Measuring China’s Green Finance Development

2.3. Models and Variables

2.3.1. Models

The spatial measurement method is used to study the impact of green finance and poverty because it takes into account the geographical location and spatial interdependence of regions. Poverty is not a localized problem and can be affected by neighboring regions. Therefore, it is important to consider the interdependence and spillover effects of different regions in poverty reduction policies. The spatial measurement method allows researchers to analyze the linear and non-linear relationships between green finance and poverty at different spatial levels, including national, regional, and local levels. This method provides a comprehensive understanding of the spatial distribution of poverty and the effectiveness of green finance in different regions, which can help policymakers design targeted poverty reduction policies based on regional characteristics. Overall, the spatial measurement method is a useful tool for understanding the complex relationship between green finance and poverty in a spatially explicit manner. The spatial econometric model is constructed as follows:

where s the individual effect, is the time effect, is the spatial regression coefficient, is the spatial autocorrelation coefficient, is the regression coefficient, is the spatial weight matrix, represents the green financial development index at time t, is the error term, and represents poverty level.

The semi-parametric spatial lag model is shown as follows:

where is nonparametric part.

This article aims to examine the impact of green finance on both absolute and relative poverty. To achieve this goal, the study utilizes technological progress (TPS) as an intermediary variable to establish a relationship between green finance and poverty.

2.3.2. Variables

The following variables in Table 2 are selected.

3. Empirical Analysis

3.1. Data Selection and Processing

To build China’s green finance development index, this paper selects index data from 2004 to 2019. The data are processed as follows: (1) an empirical analysis is conducted on 25 provinces and municipalities in China. Hong Kong, Macao, Taiwan, Tibet, Xinjiang, Ningxia, Guangxi, Inner Mongolia, Hainan, and other regions are excluded due to lack of data. (2) For some missing values in the data, the data in this paper are supplemented using linear interpolation. (3) In this paper, the number of urban minimum security population and rural minimum security population are used as the proxy variables of poverty reduction effect in China’s urban and rural areas. The fewer the minimum security population, the better the poverty reduction effect. (4) Chinese provinces’ statistical yearbooks and their annual financial operation reports provide the data.

3.2. Empirical Results of Green Finance Development Index

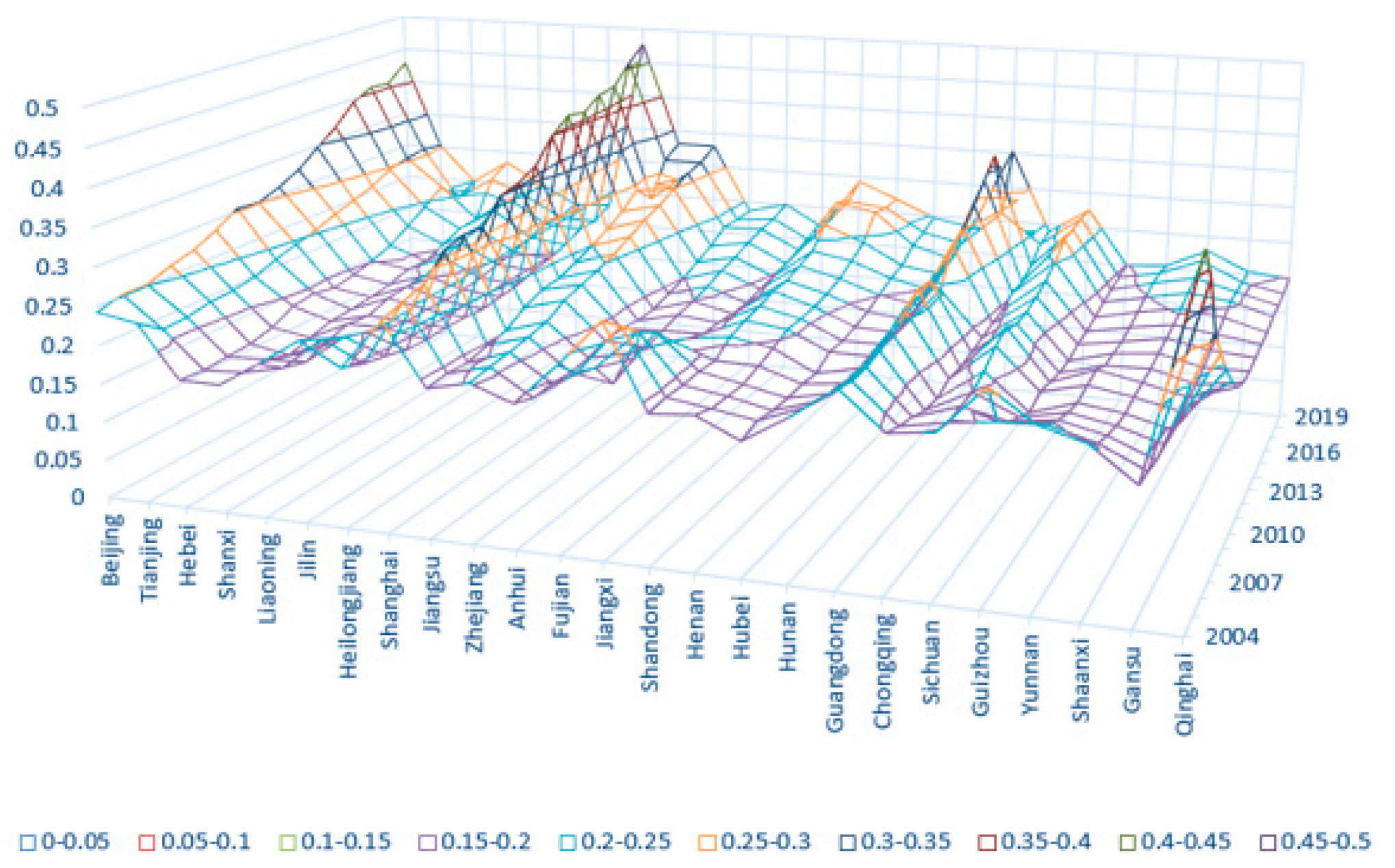

Through the improved entropy weight method (Li, 2022) [43], China’s green finance development level can be calculated for all provinces. From Table 3 and Figure 1, we can clearly see that, on the whole, China’s green finance development index is increasing every year, and there are certain differences in the development level of green finance in various regions of China. The initial development level of green finance in Shanghai, Beijing, Guangdong, Jiangsu, and Zhejiang is relatively high, and it shows an increasing trend year by year, while it is relatively low and slow in Qinghai, Guizhou, Yunnan, Gansu, and Jiangsu provinces.

To better understand the green finance development index, we will classify the green finance development index of 25 provinces by region. In order to find the level of green finance development in each region, we have divided it into four main regions, which are the eastern region, the central region, the western region, and the northeast region, as shown in Figure 2, Figure 3, Figure 4 and Figure 5.

From these figures, the western region has the highest level of green finance development in 2004, which is mainly due to the large number of nature reserves, low pollution level, and high forest coverage in the western region. However, green finance’s development level declined after 2004 and gradually increased around 2010. This trend also exists in the northeast and central regions, mainly because the rapid economic development has increased the pollution and damage to the environment. As China’s economy grows and environmental protection increases, the development level of green finance in these areas is gradually increasing. It is noteworthy that the eastern region has a relatively high level of financial development and has been showing an increasing trend. By 2019, in comparison to the other three regions, green finance has a much higher development level.

3.3. Empirical Results

3.3.1. Test and Analysis of Spatial Autocorrelation

This paper tests the spatial correlation of the green finance development index of 25 provinces in China through the selected 0–1 weight matrix and analyzes whether there is spatial dependence. Here, we selected the global Moran’s index and local Moran’s scatter diagram for analysis.

Based on Moran’s index of green finance development, Table 4 shows the statistical test results for each province of China. In the first four years, Moran’s index is not significant. Since 2008, it has gradually become significant and shows spatial dependence. Through the previous research on spatial metrology, we can find that most years can still be calculated by using spatial metrology.

With the help of Moran’s I scatter map, the spatial correlation of each year can be analyzed and explored. Figure 6 and Figure 7 illustrate that the vast majority of provinces in 2008 and 2019 are in the first and third quadrants, which shows that there is a positive spatial correlation between the development of green finance in most provinces of China over the past two years. The positive correlation occurs because green finance develops in each province and spills over spatially, and the provinces with a high level of green finance development appear to aggregate, and it is the same for the provinces with low levels—that is, the trend of high-level agglomeration and low-level agglomeration. Some provinces are in the second or fourth quadrant, which indicates that these provinces in China have a negative correlation with the development level of green finance. This negative correlation indicates that these provinces suffer from negative spatial spillovers due to a low level of green finance development. Provinces with a high level of green finance development and provinces with a low level of green finance development gather together, which shows a trend of high–low aggregation and low–high aggregation.

3.3.2. Spatial Econometric Regression Results

In the theoretical analysis part of this paper, we introduce the commonly used spatial econometric models, but which of the above models should be chosen needs to be tested. First of all, we used the LM test to judge which model should be used. The SDM model should be considered if both models prove to be suitable. Meanwhile, a Wald test and likelihood ratio test (LR) are required to test the model. Once a model has been determined, to determine whether a fixed effect or random effect model should be used, the Hausmann test must be performed. A joint significance test is also required for spatial econometrics. To determine whether to use an individual fixed effect model or a time fixed effect model, the joint significance test is used. Its original hypothesis is to choose individual fixed effect/time fixed effect (Ind/time). If the results significantly reject the original hypothesis, we choose the double fixed effect (both) model. This paper will select the logarithm of the minimum security number of people in urban and rural areas as the explained variable to study. Here are the specific empirical results.

From Table 5 and Table 6, LM-lag in rural and urban areas passed the test of 10% significance level, but LM-err failed the test of 10% significance level, suggesting that simultaneous existence of spatial lag and spatial error models is possible. The subsequent LR test and Wald test confirmed that the spatial Durbin model cannot degenerate into spatial error model and spatial lag model. Thus, we chose the spatial Dubin model. Lm-err in urban relative poverty to rural passed the test of 10% significance level, but LM-lag failed the test of 10% significance level, suggesting that simultaneous existence of spatial lag and spatial error models is possible. The subsequent LR test and Wald test confirmed that neither the spatial Durbin model nor the spatial lag model can degenerate. Thus, we chose the spatial Dubin model. Meanwhile, it can also be found that all Hausmann tests are significant at 1%. Therefore, there is no systematic difference between fixed effects and random effects, contrary to the original hypothesis, and the fixed effect model should be constructed. Finally, the results of Table 7 show that they are significant at 0.1%. Therefore, we refused to use an individual fixed effect model and time fixed effect model and chose the double fixed effect model. The regression results are shown in Table 8.

Through the results of spatial econometric regression, we can get the following conclusions:

- (1)

- Spatial econometric regression confirms the conclusion that green finance is conducive to targeted poverty alleviation. According to the results in Table 9, for urban areas, when a 1% increase occurs in green finance development, the poverty level will decrease by 0.339% with a 10% significance level; for rural areas, when a 1% increase occurs in green finance development, the poverty level will decrease by 0.749% with a 1% significance level. At the same time, green finance is more conducive to alleviating rural poverty.

- (2)

- Interestingly, we can also see from the table that green finance affects both urban and rural poverty in a negative way. If green finance increases by 1%, the relative poverty of urban and rural areas will increase by 0.097%. In other words, the development of green finance will increase the poverty gap between rural and urban areas. There may be a reason that the financial and economic development of cities is much faster than that of rural areas, and the utilization efficiency of policies and resources is much higher than that of rural areas. With China’s vigorous support for green finance, cities are the first to gain the dividend of green finance development, while rural areas are unable to respond to the call of policies the first time due to various reasons, which leads to the slow development of green finance and, finally, exacerbates the relative poverty between urban and rural areas.

From Table 9, the indirect effect and total effect of the green finance development level on urban poverty alleviation are significant at a 1% level, while the direct effect is significant at a 10% level. Green finance has a significant spillover effect in China’s provinces. The development of green finance can effectively alleviate the level of urban poverty and play a positive role in alleviating poverty in surrounding provinces.

We also found that the green financial development level of rural poverty directly slows the effect on the 1% significance level, indirect effect in the 10% significance level, and the total effect on the 5% significance level. The green financial development of China’s provinces experiences significant spillover effects; green finance can not only reduce the development of rural poverty levels, but it can also have a positive spillover effect on surrounding provinces.

Meanwhile, in urban and rural areas, relative poverty is significant at the level of 5% in terms of direct effect, indirect effect, and total effect. Therefore, China’s provinces are spatially affected by green finance. However, it is worth noting that the direct effect is negative, while the indirect effect and total effect are positive, indicating that the effects of green finance on itself and surrounding provinces are inconsistent. From the overall effect, green finance development will increase the poverty level between urban and rural areas.

3.3.3. Semi-Parametric Spatial Econometric Regression Results

Figure 8 and Table 10 show the partial derivative of urban green finance development against the poverty level, from which we can see the path of urban poverty change caused by green finance development, which, in general, fluctuates up and down around the horizontal axis. When green finance is at the 0–32 level of development, green finance can effectively promote the reduction of the poverty level in urban areas. When green finance is at the 32–38 level of development, green finance will aggravate the poverty of the city.

Figure 9 shows the partial derivative diagram of rural green finance development on the poverty level, from which we can see the path of urban poverty change, caused by green finance development, showing an inverted “U” shaped trend on the whole. When green finance is 0–10 and 23–38, green finance can effectively promote the level of rural and urban poverty; when green finance is 10–23, green finance will increase the level of rural poverty. The main reason may be that China’s early development model, which relied heavily on polluting and energy-intensive enterprises, boosted incomes, especially in rural areas. Therefore, poverty in rural areas is negatively correlated with the development of green finance. However, with economic growth and policy support, people pursue high-quality economic development, and green finance has optimized and improved the economic quality of rural residents to a certain extent. Therefore, it finally shows a decreasing trend.

Figure 10 shows the partial derivative of green finance on rural and urban relative poverty. As shown in the figure, green finance will cause the change of rural and urban relative poverty in an inverted “U” shape. The level of green financial development is 0–4, and the development of green finance will increase the relative poverty of urban and rural areas. When the financial development level is 4–4.7, it is possible to alleviate the relative poverty between urban and rural areas through green finance, and as green finance develops, the reduction rate of relative poverty between urban and rural areas is greatly accelerated.

3.4. Mediating Effect

This article aims to investigate the relationship between green finance and poverty by utilizing technological progress as a mediator variable. The study employs bootstrap statistics to conduct a secondary test to verify the robustness of the mediation effect test results. The findings presented in Table 11, Table 12 and Table 13 indicate that both technological progress and green finance can effectively reduce poverty levels. The results of the bootstrap test reveal that the 95% confidence interval does not include 0, indicating that technological progress mediates the relationship between green finance and poverty. Moreover, the results suggest that green finance primarily relies on technological progress to achieve poverty reduction. Green finance facilitates technological progress by improving the market competition environment, promoting knowledge spillovers, and facilitating enterprise transformation and upgrading. As a specialized financial product, green finance can channel funds to specific enterprises, improving their financing efficiency, increasing their financing scale, and accelerating their development. These outcomes ultimately contribute to increased household income and reduced poverty. Therefore, green finance can effectively reduce absolute and relative poverty levels while promoting enterprise progress and development, thereby contributing to sustainable development.

3.5. Robustness Test

In this paper, weight matrix changes are used to test robustness and research uses the geographical distance matrix (latitude and longitude) instead of the 0–1 matrix. The results of changing the weight matrix are shown in Table 14. It can be seen from the results that green finance development can reduce the poverty level of urban and rural areas, as well as the poverty gap between urban and rural areas, both of which are significant at a 1% level. Numerically, transforming the spatial weight matrix produces similar results to leaving it unchanged, with only a small range of numerical changes. In this paper, robust spatial measurement results are presented.

4. Conclusions and Policy Analysis

The improved entropy weight method is used in this paper to calculate green finance development levels in Chinese provinces and finds that China’s green finance development level by province is generally showing an upward trend. Through the spatial econometric model, the paper discusses whether there are positive and negative spatial spillovers among provinces. At the same time, the semi parametric spatial lag model is used to describe the partial derivative of green finance to poverty and the path map of green finance to poverty change. From the results of spatial measurement, rural and urban poverty are negatively impacted by the development of green finance, and the effect of green finance on the poverty alleviation of urban areas is better than that of rural ones. Meanwhile, at the beginning of the development of green finance, green finance will aggravate the relative poverty of urban and rural areas, but with the continuous increase of green finance, green finance will alleviate the relative poverty of urban and rural areas to a certain extent. In conclusion, this study revealed that scientific and technological progress plays an intermediary role in the relationship between green finance and poverty reduction. Compared to previous research, this study takes a more comprehensive approach to poverty reduction by examining multiple poverty indices, including absolute poverty (both urban and rural) and relative poverty, to analyze the impact of green finance on poverty from various angles. Additionally, this study takes into account regional linkages and employs a spatial measurement model to more accurately measure the relationship between green finance and poverty. The non-linear results provide valuable insights into the dynamic changes of green finance and poverty. Moreover, this study extends the existing literature by introducing scientific and technological progress as an intermediary variable, aiming to uncover the underlying mechanism linking green finance and poverty reduction. Overall, these methodological and conceptual contributions enhance our understanding of the complex relationship between green finance and poverty reduction.

This study has significant policy implications for poverty alleviation. Policymakers need to expand their vision when developing poverty reduction policies, consider the sustainable development goals, and encourage the development of green finance by creating a supportive regulatory environment. The government should implement policies to ensure adequate financing for enterprises, improve financing efficiency, and promote technological innovation. It is also important to strengthen international cooperation to ensure sufficient green financial funds and to promote economic development to increase people’s income. To achieve the goal of poverty reduction, policymakers should prioritize improving the access of low-income families, small enterprises, and marginalized communities to green finance, broaden the scope of green finance, and achieve a common reduction of relative and absolute poverty. Additionally, policymakers should focus on investing in green industries to create more job opportunities and income for residents in low-income regions, which would promote high-speed and sustainable economic development. These policy recommendations can effectively use green finance to reduce poverty levels and promote sustainable development. Decision-makers should take these suggestions into account when developing policies to ensure that green finance is utilized to its fullest potential in poverty alleviation efforts.

This article provides valuable insights into the relationship between green finance and poverty. However, it is important to acknowledge some of the limitations of this study. Firstly, the construction of green finance indicators used in this study is not yet comprehensive enough due to data limitations. Although indicators from three dimensions were used, there is still room for improvement. Therefore, future research should aim to improve the accuracy of China’s green finance index by incorporating more comprehensive and reliable indicators. Secondly, the mechanism by which green finance affects poverty reduction should be further explored. Although the study finds that technological progress is one pathway through which green finance can reduce poverty, there are other complex pathways that need to be further examined. Therefore, future research should explore additional impact pathways to better understand the relationship between green finance and poverty. To address these limitations, future research should aim to improve the accuracy and comprehensiveness of green finance indicators and explore additional pathways through which green finance can reduce poverty. By doing so, we can gain a deeper understanding of the relationship between green finance and poverty reduction and develop more effective policies to promote sustainable development and poverty reduction.

Author Contributions

Y.T.: field sampling, designing lab protocol, improving paper quality, and revision; H.W.: conceptualization, methodology, and writing original draft. Z.L.: improving paper quality. All authors have read and agreed to the published version of the manuscript.

Funding

This paper is supported of Yonghong Tang by a major project of Fujian Social Science Fund “Research on the Function of the Integrated Development Demonstration Zone Across the Taiwan Straits” (No.: FJ2021Z023). This paper is also supported of Yonghong Tang by the Fundamental Research Funds for the Central Universities “Study on a New Road for Integrated Development Across the Taiwan Straits” (No.: 2072021088).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Research data can be obtained from the corresponding author through email.

Acknowledgments

The authors extend their sincere appreciation to the Researchers.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Zhao, W. China’s goal of achieving carbon neutrality before 2060: Experts explain how. Natl. Sci. Rev. 2022, 8, nwac115. [Google Scholar] [CrossRef] [PubMed]

- White, M.A. Environmental finance: Value and risk in an age of ecology. Bus. Strategy Environ. 1996, 5, 198–206. [Google Scholar] [CrossRef]

- Scholtens, B. Finance as a Driver of Corporate Social Responsibility. J. Bus. Ethic 2006, 68, 19–33. [Google Scholar] [CrossRef]

- Soundarrajan, P.; Vivek, N. Green finance for sustainable green economic growth in India. Agric. Econ. 2016, 62, 35–44. [Google Scholar] [CrossRef] [Green Version]

- Ngan, S.L.; Promentilla, M.A.B.; Yatim, P.; Lam, H.L. A Novel Risk Assessment Model for Green Finance: The Case of Malaysian Oil Palm Biomass Industry. Process. Integr. Optim. Sustain. 2018, 3, 75–88. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, F.; Rasoulinezhad, E.; Yoshino, N.; Chang, Y.; Morgan, P.J. The energy–pollution–health nexus: A panel data analysis of low- and middle-income asian countries. Singap. Econ. Rev. 2020, 66, 435–455. [Google Scholar] [CrossRef]

- Yu, C.-H.; Wu, X.; Zhang, D.; Chen, S.; Zhao, J. Demand for green finance: Resolving financing constraints on green innovation in China. Energy Policy 2021, 153, 112255. [Google Scholar] [CrossRef]

- Beck, T.; Demirgüç-Kunt, A.; Levine, R. Finance, inequality and the poor. J. Econ. Growth 2007, 12, 27–49. [Google Scholar] [CrossRef]

- Odhiambo, N.M. Finance-growth-poverty nexus in South Africa: A dynamic causality linkage. J. Socio Econ. 2009, 38, 320–325. [Google Scholar] [CrossRef]

- Welle-Strand, A.; Kjøllesdal, K.; Sitter, N. Assessing microfinance: The bosnia and herzegovina case. Manag. Glob. Transit. 2010, 8, 145–166. [Google Scholar]

- Inoue, T.; Hamori, S. How has financial deepening affected poverty reduction in India? Empirical analysis using state-level panel data. Appl. Financ. Econ. 2011, 22, 395–408. [Google Scholar] [CrossRef] [Green Version]

- Abosedra, S.; Shahbaz, M.; Nawaz, K. Modeling Causality Between Financial Deepening and Poverty Reduction in Egypt. Soc. Indic. Res. 2015, 126, 955–969. [Google Scholar] [CrossRef]

- Park, C.Y. Financial Inclusion, Poverty, and Income Inequality in Developing Asia. Soc. Sci. Electron. Publ. 2015, 20, 419–435. [Google Scholar] [CrossRef] [Green Version]

- Li, Y.; Wang, C. Risk identification, future value and credit capitalization: Research on the theory and policy of poverty alleviation by Internet finance. China Finance Econ. Rev. 2017, 5, 1. [Google Scholar] [CrossRef] [Green Version]

- Raberto, M.; Ozel, B.; Ponta, L.; Teglio, A.; Cincotti, S. From financial instability to green finance: The role of banking and credit market regulation in the Eurace model. J. Evol. Econ. 2018, 29, 429–465. [Google Scholar] [CrossRef] [Green Version]

- Ayyagari, M.; Beck, T.; Hoseini, M. Finance, law and poverty: Evidence from India. J. Corp. Financ. 2020, 60, 101515. [Google Scholar] [CrossRef]

- Mhlanga, D.; Denhere, V. Determinants of Financial Inclusion in Southern Africa. Stud. Univ. Babes Bolyai Oeconomica 2020, 65, 39–52. [Google Scholar] [CrossRef]

- Xiong, M.; Li, W.; Teo, B.S.X.; Othman, J. Can China’s Digital Inclusive Finance Alleviate Rural Poverty? An Empirical Analysis from the Perspective of Regional Economic Development and an Income Gap. Sustainability 2022, 14, 16984. [Google Scholar] [CrossRef]

- Li, Z.; Tuerxun, M.; Cao, J.; Fan, M.; Yang, C. Does inclusive finance improve income: A study in rural areas. AIMS Math. 2022, 7, 20909–20929. [Google Scholar] [CrossRef]

- Zhao, H.; Zheng, X.; Yang, L. Does Digital Inclusive Finance Narrow the Urban-Rural Income Gap through Primary Distribution and Redistribution? Sustainability 2022, 14, 2120. [Google Scholar] [CrossRef]

- Yu, N.; Wang, Y. Can Digital Inclusive Finance Narrow the Chinese Urban–Rural Income Gap? The Perspective of the Regional Urban–Rural Income Structure. Sustainability 2021, 13, 6427. [Google Scholar] [CrossRef]

- Song, K.; Tang, Y.; Zang, D.; Guo, H.; Kong, W. Does Digital Finance Increase Relatively Large-Scale Farmers’ Agricultural Income through the Allocation of Production Factors? Evidence from China. Agriculture 2022, 12, 1915. [Google Scholar] [CrossRef]

- Ravallion, M.; Wodon, Q. Poor Areas, or Only Poor People? J. Reg. Sci. 1999, 39, 689–711. [Google Scholar] [CrossRef] [Green Version]

- Maurer, N.; Haber, S. Related Lending and Economic Performance: Evidence from Mexico. J. Econ. Hist. 2007, 67, 551–581. [Google Scholar] [CrossRef] [Green Version]

- Greenwood, J.; Jovanovic, B. Financial Development, Growth, and the Distribution of Income. J. Political Econ. 1990, 98, 1076–1107. [Google Scholar] [CrossRef] [Green Version]

- Perez-Moreno, S. Financial development and poverty in developing countries: A causal analysis. Empir. Econ. 2010, 41, 57–80. [Google Scholar] [CrossRef]

- Ji, D.; Liu, Y.; Zhang, L.; An, J.; Sun, W. Green Social Responsibility and Company Financing Cost-Based on Empirical Studies of Listed Companies in China. Sustainability 2020, 12, 6238. [Google Scholar] [CrossRef]

- Yang, S.; Zhang, H.; Zhang, Q.; Liu, T. Peer effects of enterprise green financing behavior: Evidence from China. Front. Environ. Sci. 2022, 10, 132458. [Google Scholar] [CrossRef]

- Li, X.; Yang, Y. Does Green Finance Contribute to Corporate Technological Innovation? The Moderating Role of Corporate Social Responsibility. Sustainability 2022, 14, 5648. [Google Scholar] [CrossRef]

- Cao, Y.; Zhang, Y.; Yang, L.; Li, R.; Crabbe, M. Green Credit Policy and Maturity Mismatch Risk in Polluting and Non-Polluting Companies. Sustainability 2021, 13, 3615. [Google Scholar] [CrossRef]

- Dong, Z.; Xu, H.; Zhang, Z.; Lyu, Y.; Lu, Y.; Duan, H. Whether Green Finance Improves Green Innovation of Listed Companies—Evidence from China. Int. J. Environ. Res. Public Health 2022, 19, 10882. [Google Scholar] [CrossRef]

- Xiang, X.; Liu, C.; Yang, M. Who is financing corporate green innovation? Int. Rev. Econ. Financ. 2022, 78, 321–337. [Google Scholar] [CrossRef]

- Li, W.; Cui, G.; Zheng, M. Does green credit policy affect corporate debt financing? Evidence from China. Environ. Sci. Pollut. Res. 2021, 29, 5162–5171. [Google Scholar] [CrossRef]

- Chai, S.; Zhang, K.; Wei, W.; Ma, W.; Abedin, M.Z. The impact of green credit policy on enterprises’ financing behavior: Evidence from Chinese heavily-polluting listed companies. J. Clean. Prod. 2022, 363, 132458. [Google Scholar] [CrossRef]

- Peng, B.; Yan, W.; Elahi, E.; Wan, A. Does the green credit policy affect the scale of corporate debt financing? Evidence from listed companies in heavy pollution industries in China. Environ. Sci. Pollut. Res. 2021, 29, 755–767. [Google Scholar] [CrossRef]

- Lai, X.; Yue, S.; Chen, H. Can green credit increase firm value? Evidence from Chinese listed new energy companies. Environ. Sci. Pollut. Res. 2021, 29, 18702–18720. [Google Scholar] [CrossRef]

- Yu, Y.; Yan, Y.; Shen, P.; Li, Y.; Ni, T. Green Financing Efficiency and Influencing Factors of Chinese Listed Construction Companies against the Background of Carbon Neutralization: A Study Based on Three-Stage DEA and System GMM. Axioms 2022, 11, 467. [Google Scholar] [CrossRef]

- Li, X.; Shao, X.; Chang, T.; Albu, L.L. Does digital finance promote the green innovation of China’s listed companies? Energy Econ. 2022, 114, 106254. [Google Scholar] [CrossRef]

- Zhang, M.; Zhang, X.; Song, Y.; Zhu, J. Exploring the impact of green credit policies on corporate financing costs based on the data of Chinese A-share listed companies from 2008 to 2019. J. Clean. Prod. 2022, 375, 134012. [Google Scholar] [CrossRef]

- Jiang, L.; Wang, H.; Tong, A.; Hu, Z.; Duan, H.; Zhang, X.; Wang, Y. The Measurement of Green Finance Development Index and Its Poverty Reduction Effect: Dynamic Panel Analysis Based on Improved Entropy Method. Discret. Dyn. Nat. Soc. 2020, 2020, 8851684. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Financial Literacy Around the World: An Overview. J. Pension Econ. Financ. 2011, 10, 497–508. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Wang, H.; Jiang, L.; Duan, H.; Wang, Y.; Jiang, Y.; Lin, X. The Impact of Green Finance Development on China’s Energy Structure Optimization. Discret. Dyn. Nat. Soc. 2021, 2021, 2633021. [Google Scholar] [CrossRef]

- Li, W.; Lin, X.; Wang, H.; Wang, S. High-quality economic development, green credit and carbon emissions. Front. Environ. Sci. 2022, 10, 1653. [Google Scholar] [CrossRef]

Figure 1.

Green finance development in China.

Figure 2.

Green finance development in eastern regions.

Figure 3.

Green finance development in central regions.

Figure 4.

Green finance development in western regions.

Figure 5.

Green finance development in northeast regions.

Figure 6.

Moran’s I scatter plot of GFI in 2008.

Figure 7.

Moran’s I scatter plot of GFI in 2019.

Figure 8.

Partial map of urban green finance development on poverty.

Figure 9.

Partial map of urban green finance development on poverty.

Figure 10.

Partial plot of the impact of urban green finance development on relative poverty.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Indicator system of China’s green finance development level.

| Dimension | Basic Indicator | Attribute | Calculation Method |

|---|---|---|---|

| Economic Dimension | Unemployment rate | − | Unemployment/(Unemployment + employees) |

| Per capita gross regional product | + | Gross regional product/regional population | |

| Per capita disposable income | + | Regional total disposable income/regional population | |

| Environmental Dimensions | Wastewater discharge per unit of financial resources | − | Wastewater discharge/(Deposit + Loan) |

| Sulfur dioxide emissions per unit of financial resources | − | SO2 emissions/(Deposit + Loan) | |

| Solid waste output per unit of financial resources | − | Solid waste output/(Deposit + Loan) | |

| Energy consumption per unit of financial resources | − | Energy consumption/(Deposit + Loan) | |

| Coverage rate of nature reserves under unit of financial resources | + | Area of Natural Reserve/(deposit + loan) | |

| Forest coverage per unit financial resources | + | Forest coverage/(deposit + loan) | |

| Financial Dimension | Number of banking institutions per area | + | Number of banking institutions/regional area |

| Number of banking employees per area | + | Number of banking employees/regional area | |

| Average number of banking institutions per resident | + | Number of banking institutions/number of regions | |

| Average number of banking employees of residents | + | Number of banking practitioners/regional population | |

| Bank deposit | + | Deposit balance of financial institutions/GDP | |

| Bank loans | + | Loan balance of financial institutions/GDP | |

| Insurance density | + | Premium income/number of people | |

| Insurance depth | + | Premium income/GDP |

Table 2.

Definition of main variables.

| Variable | Variable Name | Variable Meaning | Variable Method |

|---|---|---|---|

| Explained variable | UPI | Poverty level | Logarithm of urban minimum security number |

| RPI | Poverty level | logarithm of rural minimum security number | |

| LPK | Poverty level | logarithm of urban minimum security number/Logarithm of rural minimum security number | |

| Explanatory variable | GFI | Green financial development level | Green finance development index |

| Intermediary variable | TPS | Technical progress | Number of patent licenses per capita |

| Control variable | CPI | Inflation level | Consumer price level |

| LROAD | Infrastructure construction | Logarithm of highway mileage | |

| LGV | Level of government intervention in economy | Logarithm of government expenditure | |

| LOPRN | Economic openness | Logarithm of total import and export | |

| LEDU | Education | Logarithm of the average number of students enrolled in higher education institutions per 100,000 people | |

| LASSET | Level of financial asset development | Logarithm of total assets of financial institutions |

Table 3.

Green finance development index of China’s provinces from 2004 to 2019.

| Province | 2004 | … | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|---|---|---|

| Beijing | 0.243 | … | 0.348 | 0.368 | 0.396 | 0.409 | 0.406 | 0.429 |

| Tianjin | 0.234 | … | 0.274 | 0.284 | 0.297 | 0.304 | 0.307 | 0.303 |

| Hebei | 0.166 | … | 0.211 | 0.228 | 0.245 | 0.264 | 0.236 | 0.25 |

| Shanxi | 0.166 | … | 0.193 | 0.205 | 0.216 | 0.219 | 0.268 | 0.284 |

| Liaoning | 0.199 | … | 0.224 | 0.234 | 0.247 | 0.253 | 0.247 | 0.254 |

| Jilin | 0.233 | … | 0.197 | 0.202 | 0.212 | 0.219 | 0.218 | 0.226 |

| Heilongjiang | 0.204 | … | 0.192 | 0.198 | 0.205 | 0.217 | 0.217 | 0.23 |

| Shanghai | 0.268 | … | 0.418 | 0.414 | 0.429 | 0.433 | 0.458 | 0.477 |

| Jiangsu | 0.19 | … | 0.261 | 0.275 | 0.295 | 0.27 | 0.317 | 0.331 |

| Zhejiang | 0.202 | … | 0.279 | 0.288 | 0.3 | 0.311 | 0.317 | 0.331 |

| Anhui | 0.183 | … | 0.2 | 0.211 | 0.221 | 0.236 | 0.236 | 0.237 |

| Fujian | 0.235 | … | 0.216 | 0.222 | 0.23 | 0.238 | 0.241 | 0.251 |

| Jiangxi | 0.188 | … | 0.195 | 0.199 | 0.205 | 0.212 | 0.213 | 0.221 |

| Shandong | 0.188 | … | 0.232 | 0.24 | 0.265 | 0.285 | 0.275 | 0.294 |

| Henan | 0.202 | … | 0.219 | 0.23 | 0.244 | 0.275 | 0.27 | 0.271 |

| Hubei | 0.241 | … | 0.201 | 0.211 | 0.216 | 0.232 | 0.238 | 0.248 |

| Hunan | 0.195 | … | 0.191 | 0.199 | 0.208 | 0.216 | 0.227 | 0.238 |

| Guangdong | 0.202 | … | 0.302 | 0.321 | 0.344 | 0.367 | 0.275 | 0.353 |

| Chongqing | 0.26 | … | 0.195 | 0.205 | 0.206 | 0.216 | 0.234 | 0.24 |

| Sichuan | 0.202 | … | 0.24 | 0.252 | 0.27 | 0.272 | 0.276 | 0.276 |

| Guizhou | 0.26 | … | 0.176 | 0.181 | 0.187 | 0.194 | 0.196 | 0.2 |

| Yunnan | 0.223 | … | 0.187 | 0.194 | 0.2 | 0.206 | 0.206 | 0.205 |

| Shanxi | 0.208 | … | 0.195 | 0.203 | 0.21 | 0.217 | 0.229 | 0.23 |

| Gansu | 0.167 | … | 0.187 | 0.196 | 0.204 | 0.203 | 0.203 | 0.205 |

| Qinghai | 0.432 | … | 0.18 | 0.181 | 0.188 | 0.189 | 0.192 | 0.199 |

Table 4.

Results of Moran’s test of green finance in China.

| Year | Moran’s I | Z | p |

|---|---|---|---|

| 2004 | −0.102 | −0.508 | 0.306 |

| 2005 | −0.080 | −0.314 | 0.377 |

| 2006 | −0.023 | 0.134 | 0.447 |

| 2007 | 0.031 | 0.523 | 0.300 |

| 2008 | 0.133 | 1.309 | 0.095 |

| 2009 | 0.184 | 1.667 | 0.048 |

| 2010 | 0.186 | 1.703 | 0.044 |

| 2011 | 0.234 | 2.067 | 0.019 |

| 2012 | 0.291 | 2.534 | 0.006 |

| 2013 | 0.258 | 2.267 | 0.012 |

| 2014 | 0.266 | 2.319 | 0.010 |

| 2015 | 0.268 | 2.268 | 0.012 |

| 2016 | 0.267 | 2.227 | 0.013 |

| 2017 | 0.220 | 1.872 | 0.031 |

| 2018 | 0.319 | 2.691 | 0.004 |

| 2019 | 0.277 | 2.327 | 0.010 |

Table 5.

LM Test.

| Statistic | Prob. | ||

|---|---|---|---|

| Urban | LM-lag | 4.455 | 0.035 |

| LM-err | 0.329 | 0.566 | |

| Rural | LM-lag | 37.686 | ≤0.001 |

| LM-err | 0.161 | 0.688 | |

| Urban relative poverty to Rural | LM-lag | 1.711 | 0.191 |

| LM-err | 252.510 | 0.000 | |

Table 6.

LR test, Wald test, and Hausman test.

| LR Test | Wald Test | Hausman Test | |||

|---|---|---|---|---|---|

| SAR | SEM | ||||

| Urban | Statistic | 20.830 | 21.140 | 21.690 | 129.940 |

| Prob. | 0.004 | 0.003 | 0.002 | 0.000 | |

| Rural | Statistic | 13.650 | 13.040 | 13.310 | 67.400 |

| Prob. | 0.057 | 0.071 | 0.064 | 0.000 | |

| Urban relative poverty to Rural | Statistic | 34.820 | 36.620 | 38.340 | 226.920 |

| Prob. | 0.000 | 0.000 | 0.000 | 0.000 | |

Table 7.

Joint significance test (rural).

| LR chi2 | Prob. | ||

|---|---|---|---|

| Urban | Time | 774.770 | ≤0.001 |

| Ind | 59.440 | ≤0.001 | |

| Rural | Time | 317.520 | ≤0.001 |

| Ind | 36.950 | ≤0.001 | |

| Urban relative poverty to Rural | Time | 621.280 | ≤0.001 |

| Ind | 0.000 | ≤0.001 |

Table 8.

Spatial measurement results of green finance for poverty reduction.

| Urban | Rural | Urban Relative Poverty to Rural | |

|---|---|---|---|

| GFI | −0.339 * | −0.749 *** | −0.097 *** |

| CPI | −0.001 | −0.030 *** | 0.002 |

| LROAD | −0.176 * | −0.033 | 0.035 * |

| LGV | 0.888 ** | −0.001 | −0.038 *** |

| LOPRN | −0.057 | −0.100 *** | −0.015 * |

| LEDU | −0.085 | 0.475 *** | 0.013 |

| LASSET | 0.046 | −0.064 | 0.009 |

| R2 | 0.342 | 0.249 | 0.428 |

t statistics in parentheses * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 9.

Direct effect, indirect effect, and total effect of spatial Durbin model.

| Urban | Rural | Urban Relative Poverty to Rural | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variables | Direct Effect | Indirect Effect | Total Effect | Direct Effect | Indirect Effect | Total Effect | Direct Effect | Indirect Effect | Total Effect |

| GFI | −356 * | −1.308 *** | −1.665 *** | −0.892 *** | −1.587 * | −2.479 ** | −0.110 *** | 0.350 *** | −0.239 *** |

| CPI | −0.001 | 0.005 | 0.004 | −0.031 *** | 0.005 | −0.025 | 0.002 | 0.001 | 0.003 |

| LROAD | −0.169 | 0.002 | −0.166 | −0.022 | 0.003 | −0.019 | 0.034 * | 0.040 | 0.754 |

| LGV | 0.091 ** | −0.025 | 0.065 | 0.021 | 0.214 | 0.236 | −0.037 *** | −0.004 | −0.042 *** |

| LOPEN | −0.013 | −0.044 | −0.057 | −0.062 | 0.552 ** | 0.490 * | −0.016 * | 0.009 | −0.007 |

| LEDU | −0.081 | −0.070 | −0.151 | 0.403 ** | −0.887 | −0.484 | 0.014 | −0.003 | 0.010 |

| LASSET | 0.053 | 0.384 ** | 0.438 ** | −0.041 | 0.221 | 0.180 | 0.116 | −0.423 | −0.030 |

t statistics in parentheses * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 10.

Regression results of semi-parametric spatial lag model.

| Urban | Rural | Urban Relative Poverty to Rural | |

|---|---|---|---|

| GFI | Partial derivative figure | Partial derivative figure | Partial derivative figure |

| CPI | −0.004 *** | −0.030 *** | 0.030 |

| LROAD | 0.013 | 0.013 | 1.441 |

| LGV | −0.051 ** | −0.045 * | 0.410 |

| LOPRN | −0.051 | −0.045 | −1.314 |

| LEDU | −0.061 | −0.097 | −4.438 ** |

| LASSET | 0.083 ** | −0.083 ** | 1.277 |

t statistics in parentheses * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 11.

Intermediary effect model (rural).

| Variable | Model (4) | Model (5) | Model (6) |

|---|---|---|---|

| GFI | −1.906 *** (0.353) | 89 *** (7.521) | −1.060 *** (0.402) |

| TPS | −0.009 ** (0.002) | ||

| _coms | 4.624 *** (0.923) | −36.332 * (19.907) | 4.276 *** (0.909) |

| Bootstrap test (Indirect effect) | −0.791 *** (z = −4.258, p = 0.000) | ||

| Bootstrap test (Direct effect) | −0.791 *** (z = −2.877, p = 0.004) | ||

| [95%Conf.Interval] | (−1.179, −0.518) | ||

| R2 | 0.915 | 0.677 | 0.821 |

t statistics in parentheses * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 12.

Intermediary effect model (urban).

| Variable | Model (4) | Model (5) | Model (6) |

|---|---|---|---|

| GFI | −1.532 *** (0.198) | 89.363 *** (7.521) | −1.796 *** (0.223) |

| TPS | 0.003 ** (0.001) | ||

| _coms | 8.102 *** (0.547) | −36.332 * (19.907) | 8.624 *** (0.542) |

| Bootstrap test (Indirect effect) | −1.471 *** (z = −6.057, p = 0.000) | ||

| Bootstrap test (Direct effect) | 0.408 (z = 0.941, p = 0.346) | ||

| [95%Conf.Interval] | (−2.135, −1.081) | ||

| R2 | 0.600 | 0.6717 | 0.608 |

t statistics in parentheses * p < 0.1, ** p < 0.05, *** p < 0.01.

Table 13.

Intermediary effect model (relative poverty).

| Variable | Model (4) | Model (5) | Model (6) |

|---|---|---|---|

| GFI | −0.269 *** (0.058) | 144.428 *** (7.242) | −0.038 * (0.012) |

| TPS | −0.001 *** (0.003) | ||

| _coms | 1.020 *** (0.013) | −24.407 *** (1.881) | 0.978 *** (0.019) |

| Bootstrap test (Indirect effect) | −0.142 *** (z = −3.707, p = 0.000) | ||

| Bootstrap test (Direct effect) | 0.316 *** (z = 3.677, p = 0.000) | ||

| [95%Conf.Interval] | (−1.187, −0.536) | ||

| R2 | 0.423 | 0.677 | 0.421 |

t statistics in parentheses * p < 0.1, *** p < 0.01.

Table 14.

Spatial measurement results of green finance for poverty reduction.

| Urban | Rural | Urban Relative Poverty to Rural | |

|---|---|---|---|

| GFI | −0.580 *** | −1.137 *** | −0.117 ** |

| CPI | −0.002 | −0.041 *** | −0.007 *** |

| LROAD | −0.137 | −0.088 | 0.022 |

| LGV | 0.038 | −0.061 | −0.020 ** |

| LOPRN | −0.051 | −0.082 | −0.019 |

| LEDU | −0.075 | 0.666 *** | 0.137 *** |

| LASSET | 0.193 | −0.102 | −0.007 |

| R2 | 0.432 | 0.362 | 0.436 |

t statistics in parentheses ** p < 0.05, *** p < 0.01.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Tang, Y.; Wang, H.; Lin, Z. Spatial Heterogeneity Effects of Green Finance on Absolute and Relative Poverty. Sustainability 2023, 15, 6206. https://doi.org/10.3390/su15076206

AMA Style

Tang Y, Wang H, Lin Z. Spatial Heterogeneity Effects of Green Finance on Absolute and Relative Poverty. Sustainability. 2023; 15(7):6206. https://doi.org/10.3390/su15076206

Chicago/Turabian StyleTang, Yonghong, Hui Wang, and Zirong Lin. 2023. "Spatial Heterogeneity Effects of Green Finance on Absolute and Relative Poverty" Sustainability 15, no. 7: 6206. https://doi.org/10.3390/su15076206

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.