Are Green Taxes a Good Way to Help Solve State Budget Deficits?

Department of Economics, University of Connecticut, Box U-63, Storrs, CT 06269, USA

*

Author to whom correspondence should be addressed.

Sustainability 2012, 4(6), 1329-1353; https://doi.org/10.3390/su4061329

Submission received: 8 May 2012

/

Revised: 31 May 2012

/

Accepted: 7 June 2012

/

Published: 18 June 2012

(This article belongs to the Special Issue Environmental and Resource Economics)

Abstract

:States are increasingly turning to environmental taxes as a means of raising revenue. These taxes are often thought to generate a double dividend: an environmental dividend stemming from the environmental improvement, and an economic dividend resulting from use of the revenue from environmental taxes to reduce other distortionary taxes (e.g., income or sales taxes). We review the economic literature on the double-dividend hypothesis, and show explicitly that the conditions under which the second dividend exists are less likely to hold when the amount of revenue that would be raised by an optimal environmental tax is small relative to the tax revenue from other taxes. We then present estimates of the potential revenue that could be raised from two environmental taxes in Connecticut. The results suggest that, because of their small tax base, environmental taxes are likely to have limited potential to raise revenue to finance state government budget deficits and/or reduce other distortionary taxes. Overall, environmental taxes could still generate significant gains for society if they lead to significant improvements in environmental quality. However, without more evidence of the existence of a double dividend, states should not try to justify these taxes on the basis of raising revenue more efficiently.

1. Introduction

Many states in the U.S. currently face significant budget deficits and are looking for ways to raise revenue to help close budget gaps. For example, the FY 2012 projected budget deficit for the State of Connecticut was $3.2 billion [1]. In an effort to reduce the projected deficit and ultimately balance its budget, the state recently raised existing tax rates and added some new taxes [2]. The primary source of additional revenue was increased income taxes and sales/use taxes.

While income and sales taxes are the primary fiscal instruments used by states to raise revenue, during the past two decades or so, there has been an increasing interest in using environmental taxes as a source of revenue to help reduce budget deficits. Environmental taxes have long been advocated by economists as a means of internalizing pollution externalities, i.e., forcing private parties to pay for the environmental impacts of their decisions, thereby discouraging behavior that is harmful to the environment. While more common in Europe (e.g., Ekins [3], Sterner and Köhlin [4]), environmental taxes have not historically been used to address environmental concerns in the U.S.. However, concerns about budget deficits, at both the federal and state levels, have increased the interest in using environmental taxes for another reason, namely, to raise tax revenue. For example, Oates [5] argued that a national tax on sulfur and nitrogen oxide emissions could be considered as a revenue-raising tool to help reduce the federal budget deficit. More recently, when discussing the potential use of a carbon tax, William Nordhaus [6] states: “Simply put, there is no better fiscal instrument to employ at this time, in this country, and given the fiscal constraints faced by the U.S.”. Similar arguments have been made at the state level. For example, in 2011 Texas considered imposing a state gas guzzler tax to raise revenue and to help address its multibillion-dollar budget shortfall. Under this proposal, a $100 surcharge would be imposed on sales of all new cars (including light trucks and SUVs) not meeting federal fuel economy standards [7]. Similarly, while the initial purpose of Maryland’s “flush tax” was to raise revenue to fund restoration efforts for the Chesapeake Bay [8], lawmakers recently considered increasing the annual tax from $30 to $54 per household to help raise revenue to balance the state’s budget deficit [9].

These proposals raise the following question: what role could/should environmental taxes play as a source of revenue to help reduce government budget deficits? The answer to this question needs to address the two dimensions of environmental taxes noted above: (1) their ability to discourage polluting behavior, and (2) their ability to raise tax revenue. Regarding this second dimension, the question is whether environmental taxes are a “good” or a “better” way to raise tax revenue than other traditional sources, such as income or sales taxes. In other words, if the need to raise (additional) revenue is taken as a premise, the question is whether raising the required revenue using environmental taxes leads to a better outcome for society as a whole than raising that same amount of revenue using a different tax mix.

There is a large literature within economics relating to the above question (see discussion below). It seeks to evaluate the argument that environmental taxes generate a “double dividend” by simultaneously internalizing pollution externalities, thereby improving environmental quality, and raising revenue, thereby allowing reductions in, for example, income and sales taxes, which are known to discourage productive activities. While the first dividend is strongly supported by the theoretical and empirical literature, the second dividend is more contentious.

The purpose of this paper is to draw on the double dividend literature to shed some light on whether states should seek to reduce budget deficits using environmental taxes. After reviewing the double dividend literature, we present a stylized economic model that provides an explicit formulation of the double dividend hypothesis and illustrates the critical role that the magnitude of the tax base plays in determining if it holds. The basic conclusion is that, although environmental taxes are efficient instruments for improving environmental quality, they are not necessarily a better way to raise revenue than other types of taxes (e.g., income tax and sales tax), due at least in part to their relatively small tax base. We then present an example from the State of Connecticut that estimates the tax revenue that might be raised from a state-level carbon tax or gas-guzzler tax and compare this with the revenue raised from the state’s income and sales taxes. This comparison highlights the relative magnitudes of the tax bases, and suggests that, because the environmental tax base is relatively small, environmental taxes may not be an efficient means of raising tax revenue to reduce state budget deficits. This does not imply that states like Connecticut should not advocate use of environmental taxes. Rather, it suggests that such advocacy should be based on the potential for these taxes to improve environmental quality rather than on claims that they will raise the needed revenue more efficiently than other taxes. The former argument rests on solid ground, while the latter is much more tenuous.

The rest of this paper is organized as follows. Section 2 briefly reviews some of the economic literature on environmental taxes and the double dividend. Drawing on that literature, in Section 3 we present a basic model of the double dividend hypothesis, decomposing the effect of an environmental tax. We then define the optimal tax rate based on that model and demonstrate the role of the relative size of the tax bases and the corresponding tax revenues. In Section 4 we present estimates of the potential for raising revenue in Connecticut through a carbon tax or a gas guzzler tax, and highlight the relative tax bases. The final section summarizes our conclusions.

2. Economic Literature on Externalities and the “Double Dividend”

2.1. Internalizing Externalities

In terms of economic efficiency, the best tax system is the one that allows the greatest net benefits for society as a whole, or, analogously, the system that allows a given amount of revenue to be raised at the lowest possible cost to society. While individuals think of the cost of a tax in terms of how much it will cost them (directly and indirectly), economists define the losses or economic cost of a tax in terms of the “deadweight loss” that it generates [10]. In the context of taxes on beneficial activities, the deadweight loss refers to the foregone net benefit to society that results from the tax or, equivalently, the amount by which the losses to consumers and producers in the market exceed the tax revenue that is collected. Intuitively, taxes cause a deadweight loss because they reduce productive activities such as sales or labor supply, implying that some activities that would benefit both consumers and producers do not occur.

Taxes on socially beneficial activities generate deadweight losses because they discourage activities that improve overall welfare. In contrast, environmental taxes on pollution activities could be welfare-improving, because they discourage activities that are harmful and generate negative externalities. An externality exists when an individual or a firm does not consider the full social costs (or benefits) of its activities when making decisions about those activities (see Baumol and Oates [11]). Pollution is a classic example. When firms such as electric utilities produce electricity from fossil fuels, they consider the costs of the labor, capital, and fuel that are required for that production, but with fuel prices determined solely by the market, they do not consider the environmental costs that society bears as a result of, for example, the associated emissions of carbon dioxide. Therefore, the costs they face are less than the true social costs of those activities, creating an incentive for the firm to use more fossil fuel than would be warranted based on a broader, social comparison of benefits and costs. The same is true for individuals when they purchase gasoline, if the price of gasoline is less than its full social cost. Similarly, when individuals use disposable rather than reusable bags at grocery stores or other retail establishments, they consider the convenience of that use but not its impact on the environment, since the latter is borne more broadly by society rather than directly by the individual making the use decision. An optimally-designed pollution tax (often referred to as a “Pigouvian” tax) can help correct these types of externalities. By setting the tax rate equal to the gap between the social and private marginal costs, an environmental tax would provide an incentive for polluters to adjust their behavior to a socially desirable level.

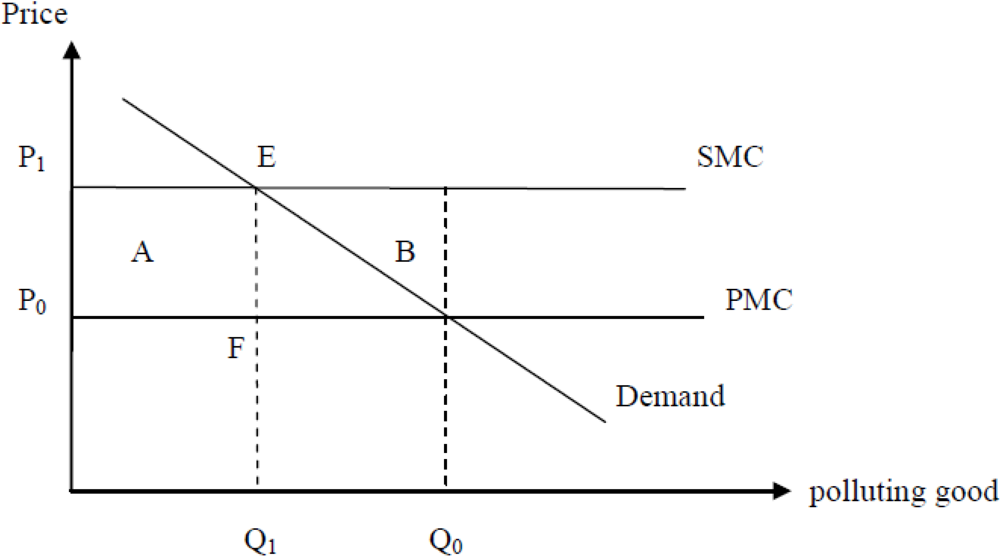

Figure 1 illustrates this result. Without an environmental tax, the equilibrium quantity of the polluting good would be Q0, where the private marginal cost curve (PMC) intersects the demand (which reflect the social marginal benefit of consuming the good). This exceeds the efficient level Q1, which is the quantity at which the social marginal cost curve (SMC) intersects with the demand curve. This generates a deadweight loss for the economy, given by the triangle area B. If an environmental tax is imposed with a tax rate equal to (P1− P0) (i.e., the distance between E and F), the new equilibrium would be at the quantity Q1. Thus, the environmental tax would internalize the negative externality and increase the welfare of the economy by area B (see, for example, Fullerton et al. [12]). The revenue generated by the tax in this case is the rectangle area A.

Figure 1.

Effect of a tax on a polluting good.

Historically, the literature on environmental taxes assumed that the revenue was returned to the economy in a lump-sum fashion, in order to avoid any other distortions [13]. However, as noted above, concerns about budget deficits and distortions created by taxes on productive activities led to suggestions that environmental taxes be used in place of other taxes to raise revenue, thereby generating a possible double dividend. Several European countries have undertaken this type of “green tax reform” (albeit primarily in response to environmental rather than budget concerns) [3,14]. In the following section, we briefly review both the theoretical and empirical literature on the double dividend. Since this literature is voluminous, this review is not meant to be exhaustive. Rather, it is intended to indicate the nature of the debate about the double dividend hypothesis. More comprehensive reviews are provided by, for example, Bosquet [14], Ekins and Barker [15], Fullerton et al. [12], Goulder [16], and Shackleton et al. [17].

2.2. The Double Dividend from Environmental Taxes

The idea of the double dividend was first introduced by Tullock [18], who argued that, in addition to addressing the problem of an externality, a Pigouvian tax would also generate revenue that could be used to reduce other distortionary taxes, thereby improving the efficiency of the whole tax system. Pearce [19] was the first to use the term “double dividend” to refer to this possibility. The figure above can be used to illustrate the potential for a double dividend. First, a tax on the polluting good would reduce pollution (the first dividend) and eliminate the deadweight loss from over-production of the polluting good, thereby increasing welfare by area B in Figure 1. Second, if the revenue collected from the environmental tax (area A in Figure 1) is used to reduce the tax on labor income, it could further help reduce the deadweight loss from the income tax, which would reduce the inefficiency of the tax system (the second dividend).

Goulder [16] gives a more comprehensive survey of the double dividend hypothesis. He distinguishes among three forms of the hypothesis. The weak form states that using the revenues from the environmental tax to reduce other distortionary taxes could achieve a lower efficiency cost relative to the case in which the revenue from the environmental tax is simply returned in a lump-sum fashion. The intermediate form states that there exists at least one kind of distortionary tax such that the revenue-neutral substitution of the environmental tax for this tax leads to a zero or negative gross cost. The strong form states that swaps of environmental taxes for any typical distortionary tax result in a zero or negative gross cost. Roughly, the last two forms can be classified as the strong version that implies that environmental taxes will generate environmental benefits at a zero or negative cost to the economy. While the weak form has generally been supported by both theoretical and empirical work, the strong version is questioned in many studies [20,21,22,23].

An important theoretical study on the strong version of the double dividend hypothesis is Bovenberg and de Mooij [20]. They construct a general equilibrium model with a polluting (dirty) commodity in which the only distortionary tax is on labor. They consider the effects of using the revenues from levying a tax on the dirty consumption good to reduce the marginal tax rate on labor income. They find that the strong form of the double dividend only holds when the uncompensated wage elasticity of labor supply is negative, which contradicts the results from most empirical work on labor supply, such as Hausman [24]. The reason why the strong version does not hold is that the environmental tax would interact with the pre-existing taxes (i.e., tax on labor income). The environmental tax increases the cost of production and leads to a general increase in commodity prices, which decreases the real wage and discourages labor supply. If this “interaction effect” is greater than the “revenue recycling effect”, then Bovenberg and de Mooij [20] conclude that “environmental taxes typically exacerbate, rather than alleviate, preexisting tax distortions—even if revenues are employed to cut preexisting distortionary taxes” (p. 1085). In this case, the revenue-recycling effect does not fully offset the negative effect of the environmental tax on employment even when the revenue is used to reduce the tax rate on labor income. The decomposition of the revenue-recycling effect and the interaction (or interdependency) effect was first introduced by Parry [22]. Earlier literature, such as Nordhaus [25], focused on the revenue-recycling effect and ignored the interaction effect.

The theoretical literature exemplified by the above studies concludes that a strong double dividend is possible but not guaranteed, and in general depends on existing tax rates and elasticities, among other things. For example, Goulder [21] finds that the costs of carbon taxes rely heavily on the initial tax rate of the pre-existing distortionary tax; the higher the existing tax rate, the higher would be the cost of the introduction of a carbon tax. Subsequent literature has shown the importance of other factors as well. Bento and Jacobsen [26] examine the double dividend hypothesis in a context where a fixed factor (e.g., coal) is an input into production of the taxed good and find that in this case the strong form of the hypothesis is more likely to hold than when all inputs are variable. Importantly, they find that a potential tradeoff can exist between the magnitudes of the first and second dividends, i.e., conditions that are likely to increase the second dividend will also reduce the first dividend. Intuitively, the second dividend is increased when the degree of pass-through of the environmental tax to product prices is low, but this condition also implies that the reduction in the output of the polluting product is small. Bayindir-Upmann [27] also finds evidence of such a tradeoff, due at least in part to imperfect competition in input and output markets.

The above discussion focuses on the theoretical literature on the double dividend. There have also been a number of empirical studies in the literature, as well as several meta-analyses (see, e.g., Anger et al. [28] and Patuelli et al. [29]). These studies differ in a number of ways. For example, some measure the second dividend based on employment effects, while others measure impacts on gross domestic product (GDP) or welfare. In addition, the studies use a variety of modeling approaches and methodologies. For example, Goulder [21] and Jorgenson-Wilcoxen [30] use intertemporal computable general equilibrium (CGE) models, while the DRI and LINK models used by Shackleton et al. [31] are macroeconometric models. Macroeconometric models have advantages in analyzing the short-term effects of exogenous shocks, while CGE models are better for describing responses in the long run. Shah and Larsen [32] use a partial equilibrium model to test the double dividend hypothesis in both developed and developing countries. Goulder [21] and Jorgenson-Wilcoxen [30] use equivalent variations to measure welfare changes, while the DRI and LINK models [17,31] use the percentage change in consumption and Shah and Larsen [32] use compensating variations.

Given the differences in methodologies, assumptions, and measures, it is not surprising that the empirical evidence regarding the existence of a strong double dividend is mixed. Studies focusing on Europe tend to find a positive second dividend when using employment effects as the benchmark, and modest positive or negative effects on output (e.g., Bosquet [14], Ekins and Barker [15], Ekins et al. [33], Lutz and Meyer [34], Moe [35] and Patuelli et al. [29]). However, in an analysis of taxes in the United Kingdom, Schöb [36] finds that the strong form of the double dividend hypothesis fails.

In contrast to the European studies, despite differences in methodology, most empirical studies of the U.S. have found that, when the revenue from environmental taxes is used to reduce pre-existing taxes, the gross cost of the tax system increases, i.e., the strong form of the double dividend hypothesis does not hold. For example, Goulder [37] finds that welfare is reduced by 0.48% when the environmental tax is used to reduce the corporate income tax and by 0.53% when used to reduce the personal income tax. In a review of empirical studies based on the five models mentioned above, Goulder [16] finds that a tax swap results in a welfare loss for all models except the Jorgenson-Wilcoxen model.

While most of the empirical literature does not find support for the strong form of the double dividend hypothesis, there are some exceptions. For instance, as noted above, the results from the Jorgenson-Wilcoxen model [30] support the strong version in some cases, which leads them to conclude that “using the revenue to reduce a distortionary tax would lower the net cost of a carbon tax by removing inefficiency elsewhere in the economy” (p. 20). They find that there is a 1.7% loss of GDP under a lump-sum transfer, a 0.7% loss by using the revenue to cut labor taxes, and a 1.1% gain by cutting capital taxes (p. 22 Table 5). Goulder [16] suggests that the negative gross cost in the case of a reduction in capital taxes stems from the assumptions about capital embodied in the Jorgenson-Wilcoxen model. It assumes perfect mobility and rapid adjustment of capital, which would explain why the gross costs are negative when the environmental tax revenue is used to reduce the capital tax, while there are positive gross costs when the revenue is used to reduce the labor tax [16]. Ekins and Barker [15] suggest that the different results for Europe and the U.S. might be due, at least in part, to lower unemployment and labor taxes in the U.S..

There are only a handful of empirical studies on the weak form of the double dividend hypothesis, but they generally support this hypothesis (which is supported by theory as well). For example, Goulder [37] found that the economic cost of environmental taxes would be about 35% higher if the revenues are returned in a lump-sum fashion rather than used to reduce other distortionary taxes. Similarly, Bovenberg and Goulder [38] found that the welfare costs would be two to three times larger for a lump-sum swap than for a replacement of other distortionary taxes. These conclusions are consistent with other results (e.g., Parry [22]) that show that policies that yield the same level of pollution control but do not raise revenue (such as grandfathered permits, which have a similar impact to taxes with lump sum redistribution) result in significantly higher costs than revenue-raising taxes where the revenues are used to reduce distortionary taxes.

Both the theoretical and empirical literature suggests that one reason environmental taxes are not good revenue-raising devices is their small tax base. If the revenue from environmental taxes were enough to finance the entire government budget, then all distortionary taxes could be abandoned and we could have both the improvement of the environment and an efficient revenue-raising system. In such an ideal case, environmental taxes would generate a strong double dividend. However, in reality, the tax base of environmental taxes is usually too small and the revenue from them is not enough to fund all public spending, implying the need for other taxes. When the tax base on the environmental tax is small relative to the tax base on, for example, labor income, then in a revenue-neutral swap the magnitude of the increase in the environmental tax would have to be much larger than the magnitude of the reduction in the labor tax simply because of the difference in tax bases. This has implications for the efficiency impacts of such a swap. In general, as a means of raising revenue, a tax that relies on a narrower tax base is less efficient than one that relies on a broader base [20]. For example, Goulder [21] notes that one reason a revenue-neutral swap of a carbon tax for a reduction in the income tax leads to a less efficient tax system is that the tax base of the carbon tax is narrower than the tax base for the income tax. The simulation results from Goulder [37] also show the importance of the breadth of the tax base. Moreover, Bovenberg and de Mooij [20] point out that introduction of an environmental tax would induce consumers to substitute from the taxed dirty commodities to untaxed cleaner goods, which erodes the tax base of the environmental tax, making it even smaller.

The above discussion focuses on the use of environmental taxes that raise revenue. Note that tradable permits that are auctioned rather than distributed free of charge could also address environmental externalities and raise revenue (see Fullerton et al. [12]). However, although taxes and permits can yield identical resource allocations under some conditions, more generally the effects of these and other policy instruments (such as freely allocated tradable permits or emissions standards) depend on a number of factors, including market structures, the extent and nature of uncertainty, and the degree of irreversibility of investments in abatement technologies (see, for example, Agliardi and Sereno [39], Coria [40], Montero [41,42] and Van Soest [43]).

3. Basic Model for Double Dividend of Environmental Taxes and the Effect of Tax Bases

3.1. Decomposition of the Effects of Environmental Taxes

Here we present an analytical model based on the frameworks of Bovenberg and de Mooij [20] and Parry et al.[44] to illustrate the basic results of the double dividend literature formally. We then further exploit this model to show the effect of the small tax base on the efficiency of raising revenue using environmental taxes.

We assume there is a linear technology for the production of three goods: a clean good (C), a dirty good (D) and a public good (G). The only input is labor and the market is assumed to be perfectly competitive. As in Bovenberg and de Mooij [20], we normalize units so that the rates of transformation between these three produced commodities (and hence their marginal costs) are unity, and we assume that the environmental tax is imposed on a final dirty good, rather than on intermediate inputs. The main difference between our model and the Bovenberg and de Mooij [20] model is the format of the labor input. They assume that production satisfies ![Sustainability 04 01329 i002]() , where the labor productivity

, where the labor productivity ![Sustainability 04 01329 i003]() is constant. Based on their assumption that

is constant. Based on their assumption that ![Sustainability 04 01329 i003]() is constant through time, we further modify the model such that the labor productivity is normalized to unity. Thus, we write the production possibilities as:

is constant through time, we further modify the model such that the labor productivity is normalized to unity. Thus, we write the production possibilities as:

, where the labor productivity

, where the labor productivity  is constant. Based on their assumption that is constant through time, we further modify the model such that the labor productivity is normalized to unity. Thus, we write the production possibilities as:

is constant. Based on their assumption that is constant through time, we further modify the model such that the labor productivity is normalized to unity. Thus, we write the production possibilities as: (1)

(1)where ![Sustainability 04 01329 i005]() in Equation (1) can be viewed as the efficiency units of labor. The purpose of this modification is just to simplify the calculations below and represent the results in a more succinct way. It does not affect the basic conclusions.

in Equation (1) can be viewed as the efficiency units of labor. The purpose of this modification is just to simplify the calculations below and represent the results in a more succinct way. It does not affect the basic conclusions.

in Equation (1) can be viewed as the efficiency units of labor. The purpose of this modification is just to simplify the calculations below and represent the results in a more succinct way. It does not affect the basic conclusions.

in Equation (1) can be viewed as the efficiency units of labor. The purpose of this modification is just to simplify the calculations below and represent the results in a more succinct way. It does not affect the basic conclusions.The government provides the public good G. To finance its expenditure on a given amount of G, the government imposes taxes on labor income and consumption of dirty goods. The rates for the labor income tax and pollution tax are ![Sustainability 04 01329 i006]() and

and ![Sustainability 04 01329 i007]() , respectively. The government’s budget constraint is thus given by:

, respectively. The government’s budget constraint is thus given by:

and

and  , respectively. The government’s budget constraint is thus given by:

, respectively. The government’s budget constraint is thus given by: (2)

(2)The representative consumer gets utility from consumption of the clean good, the dirty good and the public good. He also gets utility from leisure ( ![Sustainability 04 01329 i009]() ). The time endowment is

). The time endowment is ![Sustainability 04 01329 i010]() . The utility function of the representative consumer is given by

. The utility function of the representative consumer is given by

). The time endowment is

). The time endowment is  . The utility function of the representative consumer is given by

. The utility function of the representative consumer is given by (3)

(3)where ![Sustainability 04 01329 i012]() is quasi-concave and continuous. The separability assumption embodied in Equation (3) simplifies the analysis but is not essential for the basic results. Environmental quality is a decreasing function of the aggregate consumption of the dirty good.

is quasi-concave and continuous. The separability assumption embodied in Equation (3) simplifies the analysis but is not essential for the basic results. Environmental quality is a decreasing function of the aggregate consumption of the dirty good. ![Sustainability 04 01329 i013]() represents the disutility from pollution, where

represents the disutility from pollution, where ![Sustainability 04 01329 i014]() . Note that when the consumer make decisions, he takes

. Note that when the consumer make decisions, he takes ![Sustainability 04 01329 i015]() in the disutility part as exogenously given, as he does not consider the negative external effect of his dirty consumption on the quality of the environment. Under the perfect competition assumption, the equilibrium wage rate equals the marginal product of labor and thus it is also equal to one. In addition, the prices of the commodities equal their marginal costs, which are normalized to unity, as noted above. Thus, the budget constraint of the consumer is given by

in the disutility part as exogenously given, as he does not consider the negative external effect of his dirty consumption on the quality of the environment. Under the perfect competition assumption, the equilibrium wage rate equals the marginal product of labor and thus it is also equal to one. In addition, the prices of the commodities equal their marginal costs, which are normalized to unity, as noted above. Thus, the budget constraint of the consumer is given by

is quasi-concave and continuous. The separability assumption embodied in Equation (3) simplifies the analysis but is not essential for the basic results. Environmental quality is a decreasing function of the aggregate consumption of the dirty good.

is quasi-concave and continuous. The separability assumption embodied in Equation (3) simplifies the analysis but is not essential for the basic results. Environmental quality is a decreasing function of the aggregate consumption of the dirty good.  represents the disutility from pollution, where

represents the disutility from pollution, where  . Note that when the consumer make decisions, he takes

. Note that when the consumer make decisions, he takes  in the disutility part as exogenously given, as he does not consider the negative external effect of his dirty consumption on the quality of the environment. Under the perfect competition assumption, the equilibrium wage rate equals the marginal product of labor and thus it is also equal to one. In addition, the prices of the commodities equal their marginal costs, which are normalized to unity, as noted above. Thus, the budget constraint of the consumer is given by

in the disutility part as exogenously given, as he does not consider the negative external effect of his dirty consumption on the quality of the environment. Under the perfect competition assumption, the equilibrium wage rate equals the marginal product of labor and thus it is also equal to one. In addition, the prices of the commodities equal their marginal costs, which are normalized to unity, as noted above. Thus, the budget constraint of the consumer is given by (4)

(4)Next we derive the three separate parts of the effect of the environmental tax, following the procedure by Parry et al.[44]. From the consumer’s problem, we can derive the uncompensated demand functions:

and

and  (5)

(5)Substituting these into the utility function Equation (3) yields the indirect utility function:

(6)

(6)Roy’s identity then implies:

and

and  (7)

(7)where ![Sustainability 04 01329 i023]() is the marginal utility of income.

is the marginal utility of income.

is the marginal utility of income.

is the marginal utility of income.Differentiating Equation (2) with respect to ![Sustainability 04 01329 i007]() and setting the resulting expression equal to zero (since the change in the environmental tax is assumed to be revenue-neutral) yields:

and setting the resulting expression equal to zero (since the change in the environmental tax is assumed to be revenue-neutral) yields:

and setting the resulting expression equal to zero (since the change in the environmental tax is assumed to be revenue-neutral) yields: (8)

(8)where

(9)

(9)Using Equation (8), we can obtain the effect of a change in the environmental tax on the labor income tax rate as:

(10)

(10)Next, we define:

(11)

(11)to be the partial equilibrium marginal excess burden of the labor income tax, or the additional efficiency cost of marginal revenue from the labor tax, as defined in Parry et al.[44]. The denominator is the marginal revenue from the labor tax ( ![Sustainability 04 01329 i028]() ). The numerator is the loss of welfare (or the increase in the efficiency cost) from the marginal increase in the labor income tax rate (tax rate times the marginal reduction in labor supply). Most empirical studies of labor supply find that the uncompensated elasticity is positive, e.g., Hausman [24], implying that the numerator is positive in general. Assuming the labor tax rate is not high enough to be on the downward-sloping part of its Laffer curve, the denominator is positive. While

). The numerator is the loss of welfare (or the increase in the efficiency cost) from the marginal increase in the labor income tax rate (tax rate times the marginal reduction in labor supply). Most empirical studies of labor supply find that the uncompensated elasticity is positive, e.g., Hausman [24], implying that the numerator is positive in general. Assuming the labor tax rate is not high enough to be on the downward-sloping part of its Laffer curve, the denominator is positive. While ![Sustainability 04 01329 i029]() is generally positive, we cannot determine whether it is bigger or smaller than one, which depends on the magnitude of the elasticity of the labor supply.

is generally positive, we cannot determine whether it is bigger or smaller than one, which depends on the magnitude of the elasticity of the labor supply.

). The numerator is the loss of welfare (or the increase in the efficiency cost) from the marginal increase in the labor income tax rate (tax rate times the marginal reduction in labor supply). Most empirical studies of labor supply find that the uncompensated elasticity is positive, e.g., Hausman [24], implying that the numerator is positive in general. Assuming the labor tax rate is not high enough to be on the downward-sloping part of its Laffer curve, the denominator is positive. While

). The numerator is the loss of welfare (or the increase in the efficiency cost) from the marginal increase in the labor income tax rate (tax rate times the marginal reduction in labor supply). Most empirical studies of labor supply find that the uncompensated elasticity is positive, e.g., Hausman [24], implying that the numerator is positive in general. Assuming the labor tax rate is not high enough to be on the downward-sloping part of its Laffer curve, the denominator is positive. While  is generally positive, we cannot determine whether it is bigger or smaller than one, which depends on the magnitude of the elasticity of the labor supply.

is generally positive, we cannot determine whether it is bigger or smaller than one, which depends on the magnitude of the elasticity of the labor supply.By differentiating the indirect utility function in Equation (6), we can find the welfare effect of a change in the environmental tax rate:

(12)

(12)Substituting Equations (7), (10), and (11) into Equation (12) gives:

(13)

(13)This result is parallel to equation (II.13) in Parry et al.[44]. Based on their argument, the welfare effect of a change in the environmental tax can be divided into three parts. Part I is the environmental gain from correcting the negative externality. It equals the difference between the demand price for the dirty good ![Sustainability 04 01329 i032]() and its marginal social cost

and its marginal social cost ![Sustainability 04 01329 i033]() , multiplied by the reduction in dirty goods consumption. Part II is the “revenue recycling effect”. When the total revenue from the environmental tax (

, multiplied by the reduction in dirty goods consumption. Part II is the “revenue recycling effect”. When the total revenue from the environmental tax ( ![Sustainability 04 01329 i034]() ) is used to reduce the distortionary tax on labor income, the total reduction in the efficiency cost is the change in total revenue from the environmental tax times the marginal excess burden (or marginal efficiency cost) of one additional dollar of revenue from the labor income tax. The remaining part III is the “tax interaction effect” (or interdependency effect). It contains two terms. The first term,

) is used to reduce the distortionary tax on labor income, the total reduction in the efficiency cost is the change in total revenue from the environmental tax times the marginal excess burden (or marginal efficiency cost) of one additional dollar of revenue from the labor income tax. The remaining part III is the “tax interaction effect” (or interdependency effect). It contains two terms. The first term, ![Sustainability 04 01329 i035]() , shows the negative effect of the environmental tax on labor supply. The environmental tax increases the cost of production and leads to general increase in the goods prices, which reduces the real wage and discourages labor supply. The second term

, shows the negative effect of the environmental tax on labor supply. The environmental tax increases the cost of production and leads to general increase in the goods prices, which reduces the real wage and discourages labor supply. The second term ![Sustainability 04 01329 i036]() is the marginal efficiency cost of labor tax revenue times the reduction of labor tax revenue. These two terms imply that when there are pre-existing distortions in the tax system, the interaction between environmental taxes and labor income taxes is another source of additional excess burden, i.e., the environmental tax tends to exacerbate pre-existing tax distortions.

is the marginal efficiency cost of labor tax revenue times the reduction of labor tax revenue. These two terms imply that when there are pre-existing distortions in the tax system, the interaction between environmental taxes and labor income taxes is another source of additional excess burden, i.e., the environmental tax tends to exacerbate pre-existing tax distortions.

and its marginal social cost

and its marginal social cost  , multiplied by the reduction in dirty goods consumption. Part II is the “revenue recycling effect”. When the total revenue from the environmental tax (

, multiplied by the reduction in dirty goods consumption. Part II is the “revenue recycling effect”. When the total revenue from the environmental tax (  ) is used to reduce the distortionary tax on labor income, the total reduction in the efficiency cost is the change in total revenue from the environmental tax times the marginal excess burden (or marginal efficiency cost) of one additional dollar of revenue from the labor income tax. The remaining part III is the “tax interaction effect” (or interdependency effect). It contains two terms. The first term,

) is used to reduce the distortionary tax on labor income, the total reduction in the efficiency cost is the change in total revenue from the environmental tax times the marginal excess burden (or marginal efficiency cost) of one additional dollar of revenue from the labor income tax. The remaining part III is the “tax interaction effect” (or interdependency effect). It contains two terms. The first term,  , shows the negative effect of the environmental tax on labor supply. The environmental tax increases the cost of production and leads to general increase in the goods prices, which reduces the real wage and discourages labor supply. The second term

, shows the negative effect of the environmental tax on labor supply. The environmental tax increases the cost of production and leads to general increase in the goods prices, which reduces the real wage and discourages labor supply. The second term  is the marginal efficiency cost of labor tax revenue times the reduction of labor tax revenue. These two terms imply that when there are pre-existing distortions in the tax system, the interaction between environmental taxes and labor income taxes is another source of additional excess burden, i.e., the environmental tax tends to exacerbate pre-existing tax distortions.

is the marginal efficiency cost of labor tax revenue times the reduction of labor tax revenue. These two terms imply that when there are pre-existing distortions in the tax system, the interaction between environmental taxes and labor income taxes is another source of additional excess burden, i.e., the environmental tax tends to exacerbate pre-existing tax distortions.3.2. Optimal Level of Environmental Tax

In the previous section, we presented some basic results from the literature regarding the multiple effects of environmental taxes based on the models from Bovenberg and de Mooij [20] and Parry et al.[44]. In the following two sections, we further explore the impact of environmental taxes based on the above model. In this subsection, we derive the optimal level of the tax in this model and compare it with the Pigovian tax rate. In the following subsection, we then study the effect of the tax base on the potential for a double dividend to exist.

Consider Equation (13) evaluated at an initial tax rate of zero:

(14)

(14)This reflects the impact of introducing a relatively small environmental tax into an economy where previously all revenue was raised by an income tax. The first part in Equation (14) is positive and represents the environmental gain by reducing the consumption of the dirty goods. The second term is also positive. However, the third term is negative, because the “interaction effect” discourages the labor supply, i.e., ![Sustainability 04 01329 i038]() is negative. In general, the sum of the first two terms can be expected to dominate the last term when

is negative. In general, the sum of the first two terms can be expected to dominate the last term when ![Sustainability 04 01329 i007]() is very small (e.g., when

is very small (e.g., when ![Sustainability 04 01329 i039]() ), implying that the total welfare gain is positive, i.e., a marginal increase in the environmental tax from zero is welfare improving.

), implying that the total welfare gain is positive, i.e., a marginal increase in the environmental tax from zero is welfare improving.

is negative. In general, the sum of the first two terms can be expected to dominate the last term when is very small (e.g., when

is negative. In general, the sum of the first two terms can be expected to dominate the last term when is very small (e.g., when  ), implying that the total welfare gain is positive, i.e., a marginal increase in the environmental tax from zero is welfare improving.

), implying that the total welfare gain is positive, i.e., a marginal increase in the environmental tax from zero is welfare improving.As the tax rate increases, though, the signs and relative magnitudes of these three parts will change. When ![Sustainability 04 01329 i007]() becomes large enough, the consumption of dirty goods will be reduced below the efficient level, implying that a further marginal increase in

becomes large enough, the consumption of dirty goods will be reduced below the efficient level, implying that a further marginal increase in ![Sustainability 04 01329 i007]() would reduce total welfare, i.e., term I in Equation (13) would become negative. Moreover, if the tax rate

would reduce total welfare, i.e., term I in Equation (13) would become negative. Moreover, if the tax rate ![Sustainability 04 01329 i007]() is sufficiently large, it will lie on the downward-sloping part of the Laffer curve of the environmental tax. In this case, an increase in the tax rate

is sufficiently large, it will lie on the downward-sloping part of the Laffer curve of the environmental tax. In this case, an increase in the tax rate ![Sustainability 04 01329 i007]() would reduce the total revenue from the environmental tax, thereby making the revenue-recycling effect (term II) negative. Since the third term is always negative, when the tax rate is already large enough, a marginal increase in

would reduce the total revenue from the environmental tax, thereby making the revenue-recycling effect (term II) negative. Since the third term is always negative, when the tax rate is already large enough, a marginal increase in ![Sustainability 04 01329 i007]() will unambiguously reduce total welfare.

will unambiguously reduce total welfare.

becomes large enough, the consumption of dirty goods will be reduced below the efficient level, implying that a further marginal increase in would reduce total welfare, i.e., term I in Equation (13) would become negative. Moreover, if the tax rate is sufficiently large, it will lie on the downward-sloping part of the Laffer curve of the environmental tax. In this case, an increase in the tax rate would reduce the total revenue from the environmental tax, thereby making the revenue-recycling effect (term II) negative. Since the third term is always negative, when the tax rate is already large enough, a marginal increase in will unambiguously reduce total welfare.We can see that as the environmental tax rate increases from zero to a sufficiently high level, welfare at first increases and then decreases, implying that there is an optimal tax rate at which welfare reaches a maximum. This optimal tax rate is implicitly defined by setting Equation (13) equal to zero, which is the first order condition for the optimal tax. This defines the following implicit relationship between the two tax rates (see Appendix A):

(15)

(15)where ![Sustainability 04 01329 i041]() and

and ![Sustainability 04 01329 i042]() are the corresponding tax rates on labor income and dirty commodity, respectively, that would be optimal if the only objective were to raise revenue, i.e., in the absence of the pollution externality. Substituting the government budget constraint (Equation (2)) into Equation (15) and solving for the optimal tax rate for the dirty good yields:

are the corresponding tax rates on labor income and dirty commodity, respectively, that would be optimal if the only objective were to raise revenue, i.e., in the absence of the pollution externality. Substituting the government budget constraint (Equation (2)) into Equation (15) and solving for the optimal tax rate for the dirty good yields:

and

and  are the corresponding tax rates on labor income and dirty commodity, respectively, that would be optimal if the only objective were to raise revenue, i.e., in the absence of the pollution externality. Substituting the government budget constraint (Equation (2)) into Equation (15) and solving for the optimal tax rate for the dirty good yields:

are the corresponding tax rates on labor income and dirty commodity, respectively, that would be optimal if the only objective were to raise revenue, i.e., in the absence of the pollution externality. Substituting the government budget constraint (Equation (2)) into Equation (15) and solving for the optimal tax rate for the dirty good yields: (16)

(16)Note that, when there is no need for the government to levy other distortionary taxes to finance its expenditure, the optimal environmental tax will just be the Pigovian tax, which is equal to the marginal environmental damage (MED). This can be seen by setting ![Sustainability 04 01329 i044]() equal to zero in Equation (15), which implies that in this case:

equal to zero in Equation (15), which implies that in this case:

equal to zero in Equation (15), which implies that in this case:

equal to zero in Equation (15), which implies that in this case: (17)

(17)More generally, though, whether the optimal tax on the dirty good should be higher or lower than the first–best Pigovian tax depends on the relative magnitudes of the revenue recycling and interaction effects when the tax is set at the Pigovian level. If at this tax rate the revenue recycling effect is larger than the negative interaction effect, the optimal environmental tax would lie above the Pigovian tax, implying that a double dividend exists, i.e., that society would realize a gain in total welfare from raising the environmental tax and reducing the labor income tax. However, if at that level the interaction effect of the environmental tax with the preexisting distortionary tax is larger than the revenue recycling effect, the optimal environmental tax would lie below the Pigovian tax level [20,22,36]. In this case, the second dividend does not exist, implying that increasing the environmental tax is not a preferred way of raising revenue.

3.3. The Effect of the Relative Size of Tax Bases and the Corresponding Tax Revenues

As mentioned above, one reason that environmental taxes may not be good revenue-raising devices is due to their small tax bases. If the revenue from environmental taxes is enough to finance the government’s expenditure, there is no need to collect other distortionary taxes and the government faces the “first-best case” in which it only needs to set the environmental tax rate equal to the Pigovian tax level. However, in reality, the bases of environmental taxes are likely to be too small to finance the total expenditure of the government, and thus the government faces a more complicated second-best case, in which it needs to take into account the interaction effect of the environmental tax with other distortionary taxes. Moreover, the relatively small bases and thus the tax revenues of environmental taxes compared with other typical distortionary taxes also have a significant influence on the relative magnitudes of the revenue-recycling effect and interaction effect, and thus the net change in total welfare resulting from an environmental tax.

To see this, it can be shown that the revenue recycling effect (part II in Equation (13)) can be written as:

(18)

(18)The first term in the bracket is the partial effect of the tax rate ![Sustainability 04 01329 i047]() on the total revenue from taxation of the dirty good. The second term shows the feedback effect of the corresponding change in

on the total revenue from taxation of the dirty good. The second term shows the feedback effect of the corresponding change in ![Sustainability 04 01329 i048]() on the consumption of the dirty good. It implies that the reduction in

on the consumption of the dirty good. It implies that the reduction in ![Sustainability 04 01329 i048]() (due to the introduction of the environmental tax) makes the opportunity cost of leisure increase; consumers will thus decrease their demand for leisure and increase their demand for the dirty good. According to Parry [22], this feedback effect is relatively small as long as the percentage change in

(due to the introduction of the environmental tax) makes the opportunity cost of leisure increase; consumers will thus decrease their demand for leisure and increase their demand for the dirty good. According to Parry [22], this feedback effect is relatively small as long as the percentage change in ![Sustainability 04 01329 i048]() is small and can thus be ignored. Equation (10) implies that the change in

is small and can thus be ignored. Equation (10) implies that the change in ![Sustainability 04 01329 i048]() is small when the tax base of the dirty good is relatively small, and thus the proportionate change in

is small when the tax base of the dirty good is relatively small, and thus the proportionate change in ![Sustainability 04 01329 i048]() is small. Following the argument by Parry [22], we also ignore this feedback effect here and in addition treat

is small. Following the argument by Parry [22], we also ignore this feedback effect here and in addition treat ![Sustainability 04 01329 i049]() as a constant. Then Equation (18) can be simplified as:

as a constant. Then Equation (18) can be simplified as:

on the total revenue from taxation of the dirty good. The second term shows the feedback effect of the corresponding change in

on the total revenue from taxation of the dirty good. The second term shows the feedback effect of the corresponding change in  on the consumption of the dirty good. It implies that the reduction in (due to the introduction of the environmental tax) makes the opportunity cost of leisure increase; consumers will thus decrease their demand for leisure and increase their demand for the dirty good. According to Parry [22], this feedback effect is relatively small as long as the percentage change in is small and can thus be ignored. Equation (10) implies that the change in is small when the tax base of the dirty good is relatively small, and thus the proportionate change in is small. Following the argument by Parry [22], we also ignore this feedback effect here and in addition treat

on the consumption of the dirty good. It implies that the reduction in (due to the introduction of the environmental tax) makes the opportunity cost of leisure increase; consumers will thus decrease their demand for leisure and increase their demand for the dirty good. According to Parry [22], this feedback effect is relatively small as long as the percentage change in is small and can thus be ignored. Equation (10) implies that the change in is small when the tax base of the dirty good is relatively small, and thus the proportionate change in is small. Following the argument by Parry [22], we also ignore this feedback effect here and in addition treat  as a constant. Then Equation (18) can be simplified as:

as a constant. Then Equation (18) can be simplified as: (19)

(19)where ![Sustainability 04 01329 i051]() is the uncompensated elasticity of demand for the dirty good with respect to the tax rates

is the uncompensated elasticity of demand for the dirty good with respect to the tax rates ![Sustainability 04 01329 i007]() .

.

is the uncompensated elasticity of demand for the dirty good with respect to the tax rates .

is the uncompensated elasticity of demand for the dirty good with respect to the tax rates .Similarly, we can write the interaction effect as:

(20)

(20)where ![Sustainability 04 01329 i053]() and

and ![Sustainability 04 01329 i054]() are the uncompensated elasticities of labor supply with respect to the tax rates

are the uncompensated elasticities of labor supply with respect to the tax rates ![Sustainability 04 01329 i006]() and

and ![Sustainability 04 01329 i007]() , respectively.

, respectively.

and

and  are the uncompensated elasticities of labor supply with respect to the tax rates and , respectively.

are the uncompensated elasticities of labor supply with respect to the tax rates and , respectively.From Equations (19) and (20), we can write the ratio of the absolute values of RE and IE as:

(21)

(21)Equation (21) reveals the effect of the small environmental tax base and corresponding tax revenues. Assuming the elasticities are constant, then the ratio of RE and IE depends on ratio of the revenue that would be generated by the two taxes, which in turn depend on both the tax rates and the tax bases. The smaller is the environmental tax revenue relative to the labor income revenue (i.e., the smaller is the ratio ![Sustainability 04 01329 i056]() ), the smaller

), the smaller ![Sustainability 04 01329 i057]() will be, i.e., the more likely it will be that the revenue recycling effect RE is less than the interaction effect IE, implying that a double dividend does not exist.

will be, i.e., the more likely it will be that the revenue recycling effect RE is less than the interaction effect IE, implying that a double dividend does not exist.

), the smaller

), the smaller  will be, i.e., the more likely it will be that the revenue recycling effect RE is less than the interaction effect IE, implying that a double dividend does not exist.

will be, i.e., the more likely it will be that the revenue recycling effect RE is less than the interaction effect IE, implying that a double dividend does not exist.4. Using Environmental Taxes to Raise Revenue: The Case of Connecticut

The above discussion suggests that the existence of a strong double dividend is not guaranteed, and, all else equal, it is less likely to occur when the environmental tax base is small, implying a limited potential for environmental taxes to replace other distortionary taxes. To illustrate the disparity between environmental and other tax bases and shed some light on whether it would be reasonable to expect a double dividend from state-level environmental taxes, we consider the revenue-raising potential of environmental taxes in the State of Connecticut. For illustrative purposes, we focus on two specific types of taxes that have been proposed or used in other jurisdictions: a carbon tax and a gas-guzzler tax. We estimate the potential revenues from these two taxes in Connecticut and compare the magnitude of revenues from these two environmental taxes with those of the income taxes and sales/use taxes, the two distortionary taxes that comprise the primary source of revenue for Connecticut and other states. We recognize that this information alone does not allow a determination of whether or not a double dividend would result from raising revenue through environmental taxes rather than increases in these other taxes. Such a determination would require an estimate of all of the factors that influence the relative magnitudes of the revenue-recycling and interaction effects (see Equation (21)), including relevant (disaggregated) elasticities, which could be derived from a state-level general equilibrium model. Nonetheless, even in the absence of a full detailed state-level analysis, examining the revenue-raising potential of environmental taxes can provide information about one important factor influencing whether an environmental tax swap would likely generate a double dividend.

4.1. Carbon Tax

There have been numerous calls for imposing a comprehensive federal carbon tax as a means of reducing emissions of carbon dioxide and raising revenue, and several European countries have enacted some form of carbon tax at the national level (e.g., Moe, [35], Sterner and Köhlin [4]). However, to date no such tax has been enacted in the U.S. [45]. Similarly, there are currently no U.S. states that have enacted a state-level carbon tax per se. However, there are examples of taxes that mimic a carbon tax imposed on specific products or sectors. For example, gasoline is subject to excise taxes at both the federal and state levels, and raising revenue through an increase in gasoline taxes would effectively be equivalent to imposition of a carbon tax on gasoline. The federal excise tax on gasoline is 18.4 cents per gallon, and in 2011 state excise taxes on gasoline range from a low of 4 cents per gallon in Florida to a high of 37.5 cents per gallon in Washington [46]. While designed primarily as revenue raising devices, these taxes also serve to internalize at least part of the externalities associated with gasoline consumption, including emissions of carbon. Parry and Small [47] estimate that the optimal gasoline tax for the U.S. (the tax that balances internalizing the associated externalities and the need to raise revenue) is $1.01 per gallon, which is more than double the average tax in the U.S.. Of course, gasoline taxes do not address carbon emissions from other sources, such as electricity generation. An ideal (comprehensive) carbon tax would apply to fossil fuel consumption in all sectors (residential, commercial, industrial, transportation and electric power).

There are some examples of state-level or local taxes that have some characteristics of a carbon tax, such as the “Climate Action Plan Tax” imposed in the City of Boulder, Colorado, which is imposed on electricity use and paid by end users of electricity. The tax generated about $1.8 million in 2010 [48]. Another example is a fee imposed on emissions of greenhouse gases (not limited to carbon dioxide) and paid by industrial facilities and businesses in the Bay Area Air Quality Management District in San Francisco. It is estimated to generate $1.3 million annually [49]. Montgomery County in Maryland also charges $5 per ton on any stationary source within the county that emits more than a million tons of carbon dioxide annually. The county expects to collect $10 million to $15 million each year from the tax [50].

In addition, as noted above, a cap-and-trade permit program where the permits are initially auctioned rather than distributed free of charge mimics (in terms of short-run incentives and revenue generation) the effects of a tax. An example is the Regional Greenhouse Gas Initiative (RGGI), which is a regional carbon cap-and-trade system covering several eastern U.S. states, including Connecticut, which auctions nearly all permits [51]. Since the first auction in September 2008, Connecticut has raised over $56 million through the RGGI auctions, [52], which has been used primarily to promote energy conservation [53]. Similar initiatives are underway in other regions (see e.g., [54]).

Because of the potential interest in pricing carbon, we estimate the potential revenue of a carbon tax in the State of Connecticut. We consider a tax of $50/metric ton of carbon (or equivalently $13.6/metric ton of carbon dioxide), which is imposed on the carbon content of all fossil fuels (coal, oil and natural gas) consumed within Connecticut, or, equivalently, on carbon dioxide emissions from fossil fuel consumption. Connecticut had a total of 38.1 million metric tons of CO2 emissions in 2008. Of this, 11.29% was from coal, 65.35% from petroleum products, and 23.36% from natural gas. Based on the carbon content of fuel sources, a $50 carbon tax would be equivalent to the following increases in fuel prices: $26/short ton for coal, $5.85/barrel for crude oil and $0.68/mcf for natural gas [55]. If fully passed on to consumers, the price increase for crude oil would increase the price of gasoline by about 12 cents per gallon.

The potential revenue from a carbon tax on all sectors (including residential, commercial, industrial, transportation and electric power sectors) can be estimated using the share of carbon dioxide emissions from each type of fuel and the total estimated carbon dioxide emissions in Connecticut in 2010. Imposition of the tax can be expected to reduce consumption of fossil fuels, thereby reducing the tax base. Since state-level estimates of this response are not available, we use the elasticity estimates from Metcalf [56], which are based on a comprehensive analysis by Bovenberg and Goulder [57] (see Metcalf [56] footnote 14). From these, we estimate that consumption of coal, crude oil and natural gas would be reduced by 13.9%, 0.76% and 1%, respectively. Because the reduction that would be induced by the tax is uncertain, we estimate the revenue of such carbon tax with and without this behavioral response. The estimated revenue is summarized in Table 1.

{kind=link}

| Fuel types | CO2 emission (%) | Increase in fuel price | Tax revenue (million dollars) | |

|---|---|---|---|---|

| Without behavioral response | With behavioral response | |||

| Coal | 11.29 | $26/short ton | 56.2 | 48.4 |

| Crude oil | 65.35 | $5.85/barrel | 325.3 | 322.8 |

| Natural gas | 23.36 | $0.68/mcf | 116.3 | 115.2 |

| Total | 497.8 | 486.4 | ||

Data source: from the calculation by the authors (see [55] for details).

4.2. Gas-Guzzler Taxes

While no states have to date enacted a state-level “gas-guzzler” tax, the Energy Tax Act of 1978 imposed a federal tax on sales of cars that fail to meet certain fuel economy levels (the current minimum level is 22.5 miles per gallon) [58]. The tax is paid by the manufacturer or importer of the car, not directly by the purchaser. The tax applies only to cars, and does not apply to sales of minivans, sport utility vehicles, and pick-up trucks, which constituted a relatively small fraction of the overall passenger vehicles at the time the tax was enacted [58]. The tax is graduated, starting at $1,000 per vehicle for models that get between 21.5 and 22.5 miles per gallon (mpg) and increasing to $7,700 per vehicle for models that get less than 12.5 mpg. While the tax rates are substantial, the tax base is actually quite small, comprised primarily of sales of sports cars and high-end luxury vehicles made by manufacturers such as Lamborghini, Ferrari, Rolls-Royce and Bentley [59].

Several states have considered state-level gas-guzzler taxes, such as Maryland, Illinois, New Jersey and Texas. In addition, several states (including Connecticut) have considered “feebates”, which combine a tax on low efficiency vehicles with a subsidy for high efficiency vehicles [60]. However, to our knowledge no state-level gas-guzzler taxes or feebates currently exist. Nonetheless, given the state-level interest in this approach, we consider imposing a state-level gas-guzzler tax based on fuel economy and levied at the point of new car registration in Connecticut. We focus on a gas-guzzler tax rather than a feebate, since clearly the tax alone has a greater potential for raising revenue.

Since data on total car sales or new car registration numbers for Connecticut were not available, we estimate tax revenue by extrapolating from available data for the City of Hartford. The following table is a comparison of the distribution of car sales by mpg categories for the entire U.S. and for the City of Hartford.

The following table indicates that overall new cars sold to Hartford residents are more fuel efficient than the national average. There are at least two possible factors contributing to the difference. First, Hartford is an urban city in New England. Preferences in general, and environmental consciousness in particular, are likely to be different in Hartford than in the country as a whole. All else equal, increased environmental consciousness is likely to lead to the purchase of more fuel efficient cars. Second, the average income per capita in Hartford is lower than the national level (the average annual per capita income from 2005 to 2009 was $17,094 in Hartford, and $27,041 in U.S. [61].). The wealthier people are, the more they are likely to be willing and able to pay for large but fuel inefficient cars. These two effects could explain why Hartford residents on average purchase cars with greater fuel efficiency than the national average (Table 2). However, since per capita income in Hartford is below the state average ($36,468), it is possible that at the state level the distribution of sales would be more heavily weighted toward low efficiency vehicles than the Hartford distribution would suggest. Thus, using estimates based on the distribution data for Hartford may underestimate the potential revenue for Connecticut as a whole.

| Mpg | U.S. | Hartford |

|---|---|---|

| Less than 18 | 16.90% | 12.50% |

| 18 to 21 | 22.35% | 18.06% |

| 21 to 25 | 36.68% | 30.40% |

| Above 25 | 32.96% | 39.04% |

Data source: U.S. distribution is calculated based on data from EPA Fuel Economy Trends Database, and from Robert W. French, Jr., U.S. EPA Office of Transportation and Air Quality; Hartford distribution is calculated based on data from R.L. Polk (see [55] for details).

Using the total new car sales data for Hartford [62] from 2003 to 2009, coupled with information on sales per capita estimated from the Hartford data, we estimate the new car registrations/sales by mpg for Connecticut in 2010. These estimates are shown in Table 3.

| Mpg | Estimated Total Sales |

|---|---|

| Less than 18 | 32551 |

| 18 to 21 | 47003 |

| 21 to 25 | 79143 |

| More than 25 | 101621 |

As noted previously, currently only a few cars are subject to the federal gas-guzzler tax and the tax does not apply to SUVs, minivans and light trucks. We assume that, if a state-level gas guzzler tax were imposed, it would be levied on all passenger vehicles, including SUVs, minivans and light trucks, with low fuel economy. For illustrative purposes, we estimate the tax revenue from three alternative gas-guzzler taxes, as shown in the following table:

| Mpg | Tax 1 | Tax 2 | Tax 3 |

|---|---|---|---|

| Less than 18 | $100 | $100 | $2500 |

| 18 to 21 | $100 | $100 | $1500 |

| 21 to 25 | 0 | $100 | $500 |

| More than 25 | 0 | 0 | 0 |

| Estimated revenue (million dollars) | 7.96 | 15.87 | 191.45 |

Under Tax 1, registration of new vehicles with fuel economy below 21 mpg would be subject a $100 guzzler surcharge. This is similar to the gas-guzzler tax proposed in Maryland, which would have imposed a $100 surcharge on purchases of vehicles with fuel efficiency below 21 mpg [63]. In addition, the threshold for imposition of the tax (21 mpg) is similar to the threshold at which the federal gas-guzzler tax is imposed (22.5 mpg). Based on the sales estimates in Table 2, the estimated potential revenue for this tax policy is about $7.96 million per year. This assumes that the tax would not induce a significant change in purchasing behavior, given that the tax is small relative to the price of vehicles.

Under Tax 2, vehicles with fuel economy below 25 mpg would be subject a $100 surcharge. Thus, in contrast to Tax 1, under this proposal vehicles with mpg between 21 and 25 would also be subject to the surcharge. This is similar to the proposal in Texas, under which a $100 surcharge would be levied on the sales of new cars that do not meet the federal CAFE standards [7]. Including vehicles with mpg between 21 and 25 would nearly double the estimated revenue that the tax would raise, increasing it from $7.96 million to $15.87 million per year.

Finally, we consider a much larger, graduated tax, Tax 3. Tax 3 would impose a tax of $2500 on new vehicles with fuel economy below 18 mpg; $1500 on new vehicles with fuel economy between 18 and 21 mpg; and $500 on new vehicles with fuel economy between 21 and 25 mpg. Vehicles above 25 mpg would not be subject to the tax. While much larger than the surcharges proposed in Maryland or Texas, the magnitudes of taxes under Tax 3 are comparable to the federal gas-guzzler tax, which ranges from $1,000 to $7,700 but is currently only imposed on a small subset of luxury cars [58]. If the taxes do not change purchase behavior, the estimated potential revenue is about $191.45 million per year for Tax 3. However, while the tax rates under Tax 1 and Tax 2 are low, the tax rates under Tax 3 are sufficiently large that they might be expected to induce changes in purchase behavior. Depending on the extent of this response, the tax revenue would be reduced correspondingly.

Note that, to the extent that consumers buy more fuel efficient vehicles as a result of a gas-guzzler tax, there could be a “rebound effect” on gasoline consumption. The term “rebound effect” refers to the fact that improvements in fuel economy reduce the cost of driving, which can induce individuals to drive more, thereby offsetting some of the reduction in gasoline use that would result solely from improved fuel economy. While estimates of the magnitude of the rebound effect differ (see Sorrell et al. [64]), this phenomenon suggests that increasing the tax on gasoline would be a more effective means of reducing gasoline use than imposing a gas-guzzler tax.

4.3. Comparison of Environmental and Other Taxes

In this part, we compare the relative magnitude of the estimated revenue from the proposed environmental taxes with other tax revenues, to see the potential for using the revenue from environmental taxes to reduce some pre-existing distortionary taxes. We focus on two taxes: the personal income tax and the sales/use tax. The revenues from the different taxes are summarized in Table 5:

Table 5.

Comparison between the revenues from environmental taxes and typical taxes in Connecticut in 2010 (million dollars).

| Tax | Tax Revenue |

|---|---|

| Personal income tax | 6,585.85 |

| Sales and use taxes | 3,205.43 |

| Carbon tax (without behavioral response) | 497.8 |

| Carbon tax (with behavioral response) | 486.4 |

| Gas-guzzler: Tax 1 | 8.0 |

| Gas-guzzler: Tax 2 | 15.9 |

| Gas-guzzler: Tax 3 | 191.5 |

Table 5 shows that the estimated revenues from the two proposed environmental taxes are much lower than the revenues from income tax and sales tax. The revenues from a carbon tax without considering the behavioral response are only about 7.6% of income tax revenue and 15.5% of sales and use tax revenue. Factoring in consumers’ behavioral response, the tax revenue would be even less (about 7.4% of the income tax revenue and 15.2% of sales and use tax revenue). Among the three gas-guzzler taxes, even the largest one (Tax 3) would likely generate an amount of tax revenue that is negligible compared with the revenue from other taxes (2.9% of the income tax revenue and 5.97% of the sales and use tax revenue).

The above estimates suggest that imposition of environmental taxes such as a carbon tax or a gas-guzzler tax would allow for only small decreases in the state income or sales/use taxes, because of the large disparity in the tax bases. In addition, a tax imposed in Connecticut but not in neighboring states, all else equal, would generate a larger deadweight loss than a regional or federal tax since consumers or producers can avoid the tax by buying or producing in neighboring states. Thus, although imposition of these environmental taxes could be effective in reducing pollution and hence generate the first dividend, i.e., an improvement in environmental quality, both the general literature on the double dividend discussed above and the estimates of their revenue-raising potential provided here cast doubt on the conjecture that they would also yield a second dividend, i.e., a more efficient tax system.

5. Conclusions

Environmental taxes are effective policy instruments for correcting negative externalities. They can improve environmental quality and lead to overall gains for society as a whole by reducing excessive polluting activities. Environmental taxes are often thought to generate a double dividend: an environmental dividend stemming from the environmental improvement, and an economic dividend resulting from the use of the revenue from environmental taxes to reduce other distortionary taxes, such as taxes on income, sales or capital. The double-dividend hypothesis generally takes one of two forms. The weak form states that using the revenues from the environmental tax to reduce other distortionary taxes could achieve a lower efficiency cost relative to the case in which the revenue is returned in a lump-sum fashion. This form is widely supported, both theoretically and empirically. It implies that environmental policy instruments that raise revenue, such as taxes (or auctioned permits), can yield greater benefits than non-revenue-raising policies (such as standards) if the revenue is used to reduce other distortionary taxes. It provides a basis for arguing for one type of environmental policy over another.

In contrast, the strong form of the double dividend hypothesis states that the tax swap would actually lead to a zero or negative gross cost, i.e., that the gain from reducing other distortionary taxes would lead to a more efficient (i.e., less costly) tax system overall. If true, it would argue for one type of revenue-raising approach (through environmental taxes) over another (distortionary taxes), even if the former yielded no environmental gains. However, this strong form is questioned by many economists. Although the revenue from the environmental tax could be used to reduce other distortionary taxes, the environmental tax would interact with these other taxes (e.g. the tax on labor income). If the “interaction effect” is greater than the “revenue recycling effect”, then environmental taxes may exacerbate pre-existing tax distortions and lead to a positive gross efficiency cost. When the interaction effect is larger than the revenue recycling effect, the optimal environmental tax is less than what would be optimal in the absence of the desire to raise revenue, i.e., the Pigovian tax. In this case, a second dividend does not exist, since the environmental tax is not a good revenue-raising tool. This is more likely to be true when the amount of revenue that would be raised by an optimal environmental tax is small relative to the tax revenue from other, distortionary taxes, which is likely to be true for most environmental taxes.