A Strategic Roadmap for the Wine Sector in the Setúbal Peninsula

Instituto Politécnico de Setúbal, School of Business and Administration, IPS Campus, Estefanilha, 2910-761 Setúbal, Portugal

*

Author to whom correspondence should be addressed.

Adm. Sci. 2024, 14(4), 77; https://doi.org/10.3390/admsci14040077

Submission received: 20 January 2024

/

Revised: 6 March 2024

/

Accepted: 11 April 2024

/

Published: 19 April 2024

(This article belongs to the Special Issue Innovation and Internationalization in Wine Sector)

Abstract

:The wine sector contributes significantly to economic, environmental and social development. In Portugal, the Setúbal Peninsula is one of the fourteen wine regions. Operated by numerous local businesses in a rural area, the wine industry generates enhanced value and provides jobs in the region. The main purpose of this research is to study the wine sector in the Setúbal Peninsula, Portugal, in the context of the COVID-19 pandemic and propose a roadmap, which includes strategic mitigation options regarding the impacts of the crisis. This study is based on qualitative data collected through in-depth interviews and focus group interviews. The results show that the wine sector presents a tendency toward concentration with the emergence of producers with scale and notoriety at a national level who, due to the greater dynamism of their activity, have sought international markets of great dimension and with a purchasing power, which values quality products. Finally, a business model is proposed, where companies are advised to offer competitive value propositions, which capitalize on the uniqueness of national grape varieties and traditional production processes in order to offer high-quality products at competitive prices on the global market.

1. Introduction

The wine market is composed of all alcoholic beverages based on fermented grapes and is categorized into segments, including still, sparkling and fortified wine (Statista Market Forecast 2022). European Union (EU) Regulation No. 1308/2013 establishes the definition of wine as a product derived exclusively from the complete or partial alcoholic fermentation of fresh grapes, with or without crushing, or from grape must (European Parliament and Council 2013). On a global scale, the wine market constitutes the smallest segment within the broader alcoholic drinks industry (Statista Market Forecast 2022).

Given its reliance on agricultural products, the wine market is notably influenced by the quality of each year’s harvest. The industry’s dynamics are shaped by various factors, such as weather conditions, soil characteristics, geological features and manufacturing technologies (Commité Européen des Enterprises Vins 2021). Consequently, the market exhibits considerable diversity in terms of offerings and prices, reflecting the unique qualities and individuality of each wine bottle.

In Europe, wine production commands widespread recognition and appreciation, particularly for its top quality in the intense international competition. Statistics reveal that half of the wine produced in EU countries is consumed domestically, with a quarter being transported to other member states. The remaining portion is exported, consistently showing growth in both volume and value, as reported by the European Commission (2022). In terms of production, Spain, France and Italy emerge as the primary contributors in the European region, followed closely by Germany and Portugal (Directorate-General for Agriculture and Rural Development 2022).

The wine sector in Europe plays a multifaceted role, contributing significantly to economic, environmental and social development. Operated by numerous local businesses in rural areas, the wine industry generates enhanced value, providing jobs for millions of people. Due to their specialized nature, these jobs often offer better compensation than other agricultural occupations (Commité Européen des Enterprises Vins 2021). Beyond agriculture, the socioeconomic impact extends to other sectors, directly or indirectly supporting activities such as the oak industry, glass manufacturing and cork production (Commité Européen des Enterprises Vins 2021).

Furthermore, the wine sector contributes to the tourism industry, known as wine tourism. This economic activity involves visits to vineyards and wineries and the organization of wine festivals and shows, all aimed at providing an authentic experience of grape wine tasting and showcasing the region’s unique attributes (Hall and Sharples 2008).

Presently, wine production substantially contributes to the overall agricultural output in Europe, constituting more than 5% of the gross output value generated by the European Union’s agricultural industry (Eurostat 2021). Italy, Spain and France emerged as the leading wine producers within the EU in 2019.

The wine industry is predominantly driven by family businesses and cooperatives, categorizing them as small and medium-sized enterprises (SMEs) (Ferrer et al. 2022). While the fundamental principles of viticulture and wine production are universally applicable, the natural, economic, social and technological conditions vary significantly among individual producers across countries and even within regions of the same country (Christ and Burritt 2013). This diversity is closely tied to the impact of non-technical barriers on the sustainability performance of certain SME wineries, necessitating improvements or solutions. One such barrier is the insufficient transfer of knowledge regarding sustainable agri-food practices to producers (Flores 2018). Despite efforts made by vinicultural organizations to adopt more environmentally friendly practices, (Carroquino et al. 2020; Schimmenti et al. 2016) observed that wineries primarily engage in sustainable initiatives due to ethical and environmental considerations, with economic motives being of lesser significance.

1.1. The COVID-19 Pandemic’s Impact on the Wine Industry and Consumer Behavior

In numerous industries, both the supply and demand dynamics experienced significant disruptions due to government policies implemented to combat the COVID-19 pandemic. However, certain products, such as wine, were relatively insulated from major interruptions owing to their long-term storability and the exemptions granted regarding labor movements. Nonetheless, the pandemic did exert its effects on income levels and consumer habits, with wine consumption bearing the impact of containment measures. This was particularly evident through the closure of restaurants and bars, restrictions on celebrations and a substantial decline in international travel (Wittwer and Anderson 2021).

A substantial body of academic literature has delved into the analysis of how COVID-19 and related government policies have influenced wine consumption habits and purchasing patterns. Various studies (Wittwer and Anderson 2021; Compés et al. 2022; Dubois et al. 2021; Miftari et al. 2021; Rebelo et al. 2021; Duarte Alonso et al. 2022) have scrutinized these impacts. Additionally, significant attention has been directed toward assessing the repercussions of the pandemic on wine tourism (Eastham 2022; Fountain et al. 2022). To a somewhat lesser extent, the focus has extended to examining the effects on wine producers (Niklas et al. 2022; Wittwer and Anderson 2021).

The substantial repercussions of the COVID-19 pandemic on the wine industry in 2020 manifested in a notable 14% decline in global sales (Lu 2020; Wittwer and Anderson 2021). This downturn was further compounded by the disruption of traditional distribution channels (Coyne 2020) and the indirect impact on other sectors associated with the wine industry (Almeida et al. 2022). Noteworthy transformations emerged in response to the pandemic, including the emergence of new digital distribution channels (Coyne 2020; Jorge et al. 2020) and a shift toward more socially conscious, sustainable and hybrid business models. These transitions were often facilitated by government subsidies and support from industry associations (DeYoung 2020). Additionally, novel digital experiences within the sector gained prominence (Carmer et al. 2020). Collectively, these changes have had discernible impact on the financial performance of companies operating within the wine sector.

In the European Union (EU), the region housing the majority of Old World wine-producing nations, the European Commission (EC) forecasted as early as the spring of 2020 that containment measures would result in an 8% reduction in wine consumption compared to the previous five-year average. This projection is considered an uptick in retail sales (European Commission 2020). Nevertheless, the shifts in consumption patterns are likely to differ among countries. (Niklas et al. 2022) conducted analyses on surveys gathered from wineries across various nations, leading to the observation that Old World countries, particularly those labeled as “historic countries” (France, Italy and Spain), face a more substantial impact from COVID-19 in terms of international market access. The authors posit that this is attributed to the relatively greater significance of exports for the business models adopted in these countries. Specifically, “historic countries” contend with intricate supply chains involving longer distances from wine producers to consumers. (Ugaglia 2019) elucidates that the Old World’s wine industry exhibits high diversity, encompassing actors such as cooperatives, merchants and wholesalers. This diversity results in longer chains, as opposed to the New World, and excessive fragmentation, which hinders the emergence of large companies capable of competitive volume-based operations.

Wittwer and Anderson (2021) delved into the repercussions of the COVID-19 pandemic on worldwide wine markets. Their findings highlighted detrimental impacts on both international trade and domestic sales. The imposition of social distancing measures and self-isolation protocols led to temporary shifts away from on-premise sales, closing restaurants, bars and clubs. Additionally, the substantial decline in international travel and tourism further exacerbated the challenges faced by the industry. While this situation adversely affected global wine sales, there was a partial offset through increased off-premise and direct e-commerce sales. The study emphasized that the recovery of markets from the impacts of COVID-19 might extend over several years. Notably, the premium sparkling wines category bore the brunt of the damage, although all segments of wine quality experienced some level of impact. Small premium producers and independent retailers were particularly hard-hit, contrasting with larger scale producers of lower quality wines typically found in supermarkets. Their 2021 forecasts indicate that wine-exporting countries are poised to experience greater losses due to the decrease in prices for their exported products.

Conversely, the importing countries stand to benefit from buying wines at reduced prices. With the contemporary shift toward online structures influencing various aspects of daily life, from routine shopping to professional engagements and collaborative agreements, markets have adapted to align with customers’ evolving demands. In the European wine market, the primary opportunity for stakeholders lies in introducing innovative solutions capable of securing market share and averting economic stagnation or decline (Fortune Business Insights n.d.). Notably, social distancing measures and the imposed lockdowns have constrained the traditional tools of wineries used to attract clients, such as wine tasting and cellar door sale (Bruwer et al. 2013).

Wine tourism, considered an integral facet of the agricultural sector, holds significance in the overall wine industry (Fuentes-Fernández et al. 2022; Aleffi et al. 2020). According to (Getz et al. 1999), wine tourism involves travel, which is drawn to wineries and wine regions, encompassing visits to wine cellars and participation in festivals. However, this activity, typically concentrated in areas with a high population density, experienced notable repercussions due to the measures implemented during the COVID-19 pandemic, limiting it to individual wine tourism and excluding mass events (Bibicioiu and Creţu 2013).

Furthermore, the pandemic substantially impacted winegrowers who offered food or accommodation services and supplied restaurants and hotels with a significant portion of their produce, as noted in (Profi Press n.d.). This led some winemakers to explore new distribution channels for their products, while others were compelled to re-evaluate their business strategies, with closures or partial shutdowns becoming a necessity for some establishments. To adapt to the challenging circumstances, winemakers engaged in underselling practices, employing special offers or reducing prices (Profi Press n.d.).

The study presented by (Compés et al. 2022) analyzed consumer behavior regarding wine purchases in the unprecedented context of the COVID-19 pandemic. The findings indicated a shift in alcohol consumption habits influenced by the pandemic. Generally, consumers curtailed their spending on wine during the restrictions, driven by uncertainties about their future income. The heightened concerns about economic stability prompted consumers to prioritize purchasing staple foods over wine. Additionally, insights from (Rebelo et al. 2021) revealed divergent reasons for wine consumption during the restrictions between Spaniards and Portuguese. In Spain, the fear of isolation emerged as a pivotal factor contributing to an increased frequency of wine consumption, while in Portugal, concerns about the economic crisis acted as a psychological driver of higher frequency of wine consumption.

1.2. Setúbal Peninsula Wine Region

The Setúbal Peninsula covers an area of 1421 km2 and is one of Portugal’s fourteen wine regions. The growing quality of the region’s wines was decisive in the recognition of the denomination of origin (DO) “Setúbal” and “Palmela” and the geographical identification (IG) Setúbal Peninsula. The sector is characterized by a large number of micro, small and medium-sized companies supplying different destination markets.

Despite the investments made in the sector, the “Vitiviniculture Sectorial Diagnosis” report (Ministério da Agricultura 2007) identified some vulnerabilities regarding the dynamic factors of competitiveness, namely in management, innovation, promotion and commercialization. Therefore, it is a sector with a set of vulnerabilities intensified by the crisis caused by COVID-19, and it reveals some lack of preparation on the part of entrepreneurs and their businesses (micro and small).

Thus, although the possibility of internationalization today represents a real opportunity for companies to approach new markets with competitive attractiveness, there is a need to enhance key management areas. The emphasis on international markets requires marketing strategies, which are effective in giving visibility and notoriety to national brands in light of intense international competition, reinforcing the relationship between the quality of Portuguese wines and their competitive sales prices in comparison to most traditional wine-producing countries (e.g., France and Italy). Simultaneously, the distribution and logistics strategies contribute toward the cost-effective transportation of the products, reducing the associated cost per bottle of wine and ensuring the mentioned competitiveness of the sales prices presented to the international market (Francisco Avillez 2014; Kshetri 2018).

Therefore, the relevance of this study is justified by the importance of the sector nationwide, the relevance of the wine-growing region of the Setúbal Peninsula and the characteristics of the sector’s business environment.

As a starting point, a diagnosis of the wine sector in the Setúbal Peninsula was performed in the context of the pandemic to understand the difficulties producers and companies face in maintaining and recuperating their businesses.

In addition, empirical research was performed with producers and sector specialists, which contributes to scientific evidence of strategic options for the rehabilitation and development of wine companies in the Setúbal Peninsula.

2. Methodology

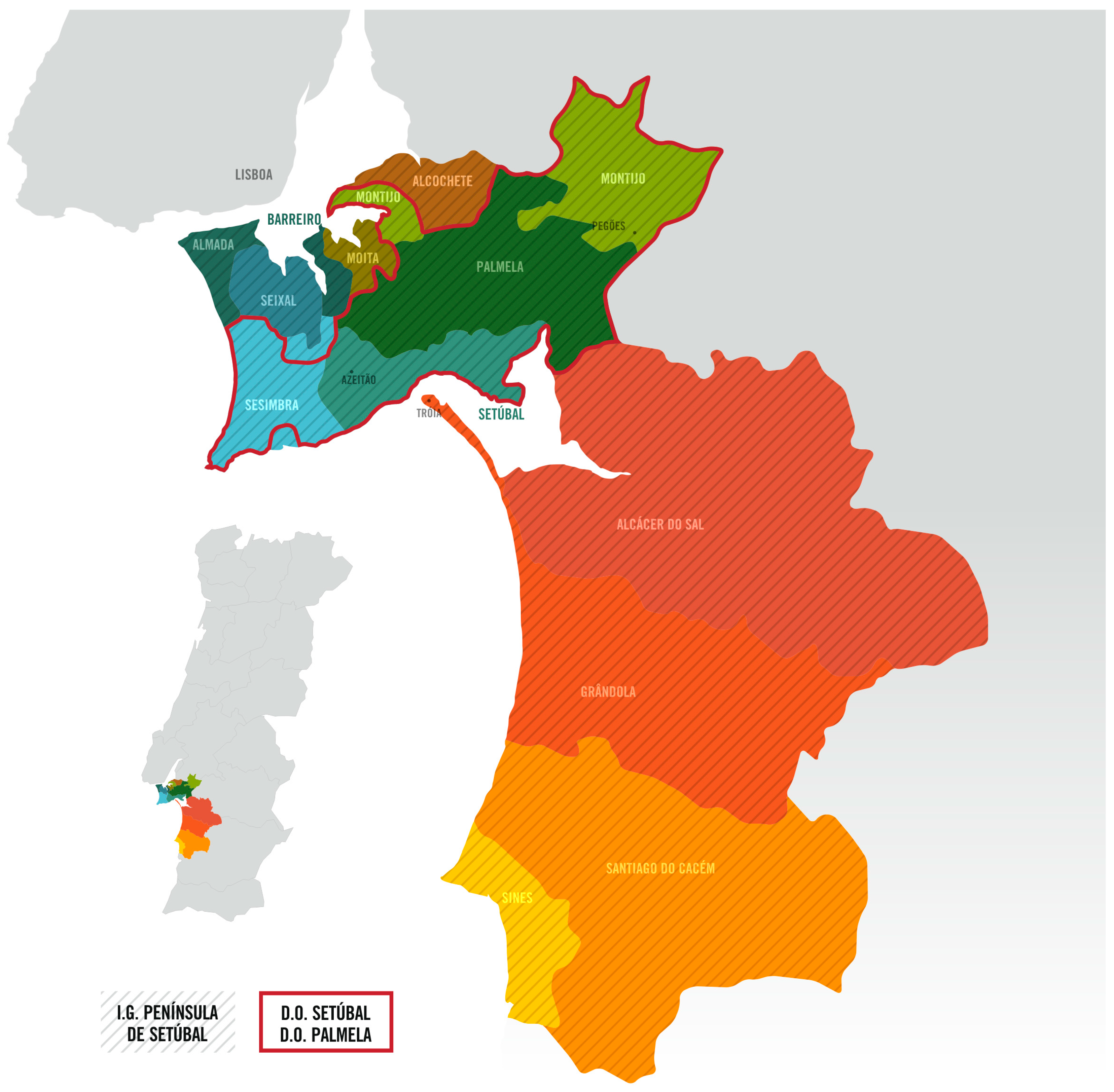

The paper aims to analyze the wine sector in the Setúbal Peninsula (Figure 1), Portugal, in the context of the pandemic and propose a roadmap, which includes strategic mitigation options regarding the impacts of the crisis. In line with this, the analysis is based on qualitative data collected through in-depth interviews (IDIs) with twelve producers (representing 50% of the total turnover of producers in this region) and focus group interviews (FGIs) with five experts in the sector (interprofessional organization, consultant regional commission, public organization for wine promotion). Below, in Table 1, we present a brief characterization as well as a map of the region where these producers are located.

Both data collection techniques allowed for the triangulation of data. Qualitative research allows for interaction with the research subject, which is—in the perspective of (R. Yin 2011)—adequate for studying the wine sector in the Setúbal Peninsula. A particular methodology of this type of research is the case study because it enables the “investigation of a contemporary phenomenon in its real context, especially when the boundaries between phenomenon and context are not clearly defined” (R. K. Yin 2003, p. 13).

The application of IDI involves one interviewer and one interviewee (Patton 2015). IDIs were applied to collect information concerning generic competitiveness conditions, critical success factors and critical competitiveness areas (important information for building the strategic roadmap), as well as to support possible business development guidelines. FGIs were applied to confirm the information provided by producers through a moderation of interactions between the experts interviewed (David Silverman n.d.).

Data collection from IDIs and FGIs took place between November 2021 and March 2022.

The main question areas in both IDIs and FGIs revolved around several key topics:

- -

- How companies responded in terms of business models to recent challenges, particularly those stemming from the pandemic situation;

- -

- Identification of business-critical success factors;

- -

- Analysis of the main characteristics and resources of Portuguese competitors;

- -

- Identification of priority products and markets for Portuguese competitors;

- -

- Exploration of competitive advantages for development, considering the resources and characteristics of Portuguese competitors.

The average duration of a focus group interview was 1 h and 30 min, while individual interviews with producers had an average duration of 1 h.

The chosen topics allowed for addressing all the mentioned subjects in both the focus groups and individual interviews. Each of the questions addressed different aspects related to competitor analysis and adapting business models to current circumstances, including challenges caused by the pandemic. By covering a variety of topics, the interviewers ensured a comprehensive understanding of participants’ responses and perceptions regarding the market and Portuguese competitors.

The study’s results are eminently descriptive elements, showing what the researchers were able to collect, analyze, develop and interpret.

In conclusion, it should be noted that due to the complexity and peculiarity of the case study, the final objective is to distinguish—in a meticulous and detailed way—the case itself and not its generalization (Stake 2010).

3. Strategic Roadmap for the Wine Sector in Setúbal Peninsula

3.1. Generic Competitiveness Conditions and Critical Success Factors

Based on analysis of the information collected from producers in the wine sector and confirmed via interviews with sector experts, one can identify a set of generic conditions affecting the competitiveness of these companies.

The climate of uncertainty caused by the pandemic and the war situation in Europe has fostered an inflationary pressure on production factors (particularly energy), which may lead to higher prices and a negative impact on demand. However, the experts interviewed in the focus group highlighted the importance of the diversity of national grape varieties and the ancestral know-how of the Portuguese wine sector, associating these factors with the investment made in recent years in innovative technologies and processes in order to contribute to mitigation of these risks and strengthen the “Wines of Portugal” brand.

Concerning international competitors, the producers referred to being characterized by their brand image in the market due to their historical notoriety as exporting countries and by the scale operations of their companies, which allows them to offer wines at higher prices and a high efficiency of transport and logistics operations.

On the other hand, the experts mentioned that national players are currently witnessing an incremental development of process technologies (aimed at streamlining and modernizing the production equipment to reduce costs and environmental impacts and to increase the productive flexibility of vineyards) and product technologies (aimed at developing new types of wines, taking advantage of traditional practices, the multiplicity of grape varieties and new market needs).

Such concerns of national companies, identified by the panel of experts, also aim to respond to environmental problems related to climate change, which may eventually be overcome with new technological processes.

Simultaneously, the producers highlighted that with market development and the diversification of the available offer, there is a greater demand for quality, which is evaluated regarding the prices offered by international competitors. Such market evolution has contributed to a gradual increase in production and exports, which presents an opportunity for approaching larger international markets and the potential for greater growth. Although small-sized companies constitute the national wine sector, they have a relevant degree of singularity in light of the different grape varieties used and the specific work processes developed, which increase the differentiation of the products they offer. Moreover, in response to the potential market growth, Portuguese companies have explored and developed different partnerships, which have favored a reduction in transportation and logistics costs and entrance into international markets.

In this context, the experts believe, there is currently a wide range of national wine varieties and possibilities of combinations or blends, which enhances the influence on aspects related to the quality and uniqueness of Portuguese wines, which continue to offer competitive prices compared to their direct competitors. Therefore, this contributes to a more significant presence of Portuguese brands in international markets, highlighting the importance of creating trust-based relationships with key partners and customers in foreign markets to ensure the operations’ sustainability. As such, the producers and experts referred to the importance of presence in international events and actions to promote the offer of Portuguese players among the international markets.

As said before, the strategic factors of competitiveness involve the analysis and reflection on the exogenous factors for the sector and the companies (which regulate their development) and the endogenous factors for the sector and the companies themselves.

Thus, based on the conditioning factors mentioned above by the producers and experts, the following strategic factors for the players’ competitiveness can be considered:

- -

- The greatest possible control or decrease in dependence on upstream activities (suppliers of raw materials and energy);

- -

- Use of less energy-consuming equipment;

- -

- Use of environmental control systems to adapt to environmental restrictions;

- -

- Product development (current or new), if a strategy of product extension is adopted (extending to possible entry into the most sophisticated international markets and the new segments associated with innovative products);

- -

- Reinforcing product quality and certification, which implies equipping the company with the necessary technical and technological competence (human resources and equipment);

- -

- Use of direct commercialization channels with adequate capacity for communication, customer service, response and technical assistance, which are associated with efficient logistics procedures encompassing the offer of different producers, increase the scale of operations and reduce transportation costs per traded bottle.

Based on the interviews conducted with the producers and the information collected from focus groups with the experts, and considering that the critical success factors result from the intersection between the key purchasing factors and the competition factors, here is a synthesis of some factors related to the main clients—current or potential—of the wine sector identified by the agents involved in the two activities. Generically speaking, and taking into consideration the two main commercialization channels—restaurants and distribution—and the international markets, the following may be considered as the key purchasing factors:

- -

- Price: This is crucial, especially for higher volume and less sophisticated products and in markets with lower added value;

- -

- Image: Company and product visibility and notoriety can condition consumer choice due to greater brand recognition and possible national and international awards;

- -

- Quality: The most sophisticated markets want unique wines with unique characteristics. The remaining segments seek wines, which optimize the relationship between price and perceived quality;

- -

- Response capacity: In international markets and distribution, the scale of operations is essential, since it is important to respond not only in terms of quality but also in terms of quantity to cope with the higher volume of operations;

- -

- Relationship: The ability to respond to the evolution in market needs through a constant adaptation of supply to demand is also a factor highly valued by international markets and more sophisticated customer segments.

Regarding competition factors, the following were also identified by the agents involved in the two activities (interviews with the producers and focus groups with the experts):

- -

- Process efficiency: To reduce the pressure on prices, companies seek to reduce their logistics costs and increase vineyard productivity through new processes in order to increase the scale of their production with the same resources;

- -

- Marketing communication: Attending international events to promote Portuguese wines to the final customers, obtaining awards and developing an attractive product image associated with its uniqueness and the characteristics of the markets are essential to give visibility and notoriety to Portuguese wines;

- -

- Technological innovation: Acquiring more advanced equipment and technology has enabled the consolidation of working procedures and contributed to greater activity, productivity and greater responsiveness, both in terms of the scale of operation and in terms of deadlines;

- -

- Product innovation: The sector’s traditional and unique practices, along with the diversity of grape varieties in the national territory, contribute to constant innovation of the wines produced and to providing access to more sophisticated markets, which are less sensitive to price through a relevant degree of differentiation compared to the main international competitors;

- -

- Market adequacy: Building sustainable partnership relations with the destination markets contributes to establishing trustful relationships and a better knowledge of the clients’ needs, increasing the cost of switching to possible alternative suppliers.

Therefore, the following critical success factors can be identified, as shown in Table 2.

3.2. Critical Competitiveness Areas

Considering the critical success factors identified and the potential growth scenario for several international markets, it can be inferred that there are development conditions for competitors, which may contribute to the creation of competitive advantages over direct competition.

According to the interviews and the experts in the focus group, once the domain of the specific technologies associated with the processes and products is assured as an indispensable condition to remain in or enter the market at the demand production level, it will be necessary to guarantee the conditions for obtaining a minimum of competitiveness. This entails producing wines with the differentiation, deadlines and prices according to market expectations, as well as marketing communication and a client service level, which guarantees the creation of sustainable commercial relationships with the business partners.

The following are some factors identified by the producers and experts, which can contribute to managing the level of differentiation, the deadlines, the prices, the marketing communication and the client service, and as a consequence, the level of competitiveness of Portuguese players in the wine sector.

Obtaining competitive prices involves the minimization of production costs, which, among others, can be obtained through the following:

- -

- The systematic search for better suppliers in terms of price and quality, possibly raising the opportunity to create central purchases to increase the negotiating power with the main material suppliers (such as glass, cardboard, labeling, etc.);

- -

- Use of less energy-consuming equipment;

- -

- Adequacy of installed capacity for the expected production volumes, avoiding, as much as possible, surpluses or under-capacity situations;

- -

- Establishing partnerships and business associations in order to reduce the costs of raw material acquisition and distribution of the final products in the destination markets;

- -

- Good planning, which allows the maximum use of existing resources (facilities, equipment and workforce), avoiding inactivity;

- -

- Correct placement of the installations and equipment in order to avoid unnecessary transportation of materials and components;

- -

- Good stock management (raw materials, components, work in progress and finished products) to avoid excesses (fixed assets costing money) or production disruptions due to lack of material.

The compliance and deadline reduction involve

- -

- Good planning and programming of the productive activity, which will contribute not only to better use of the resources but also to meeting deadlines and, through monitoring and control actions, to making possible adjustments;

- -

- Flexible production processes, which allow—at reduced costs—production changes and/or changes in production volumes.

Obtaining differentiation involves

- -

- The creation of unique wines through the use of traditional production techniques, the properties of national grape varieties, and the climatic and natural conditions of the territory;

- -

- Quality procedures (control, prevention, inspection, etc.), which enable obtaining improved quality standards and, essentially, a reduction in costs due to non-conformities;

- -

- Equipment and technological processes adjusted to the type of production, which avoid deficiencies and consequently lower the costs of waste and/or corrections;

- -

- Suitable product design for the characteristics of its use;

- -

- The use of materials and components of adequate quality to avoid deficiencies in the manufactured products.

Concerning marketing communication, it can be assured through different aspects, which may contribute to greater institutional and product visibility and notoriety, highlighting, among others, the following actions:

- -

- Development of marketing tools in the various languages of the main export markets, which enhance the image of the company and the products produced and are aligned with the company’s commercial strategy;

- -

- Establishment of wine clubs for top-quality products, contributing to institutional notoriety;

- -

- Website development to promote the company and its products to markets and international customers, which are not geographically close;

- -

- Participating in competitions for prizes, which value and highlight the quality of the wines;

- -

- Achieving increasingly better grades in specialized wine magazines (e.g., Wine Spectator, The Wine Advocate, Wine Enthusiast) and prizes in leading international wine competitions;

- -

- Participation in fairs and events promoted by sector associations in order to boost relationships with partners and business in international markets;

- -

- Promoting meetings and visits of potential business partners, contributing to the development of close and trust-based relationships;

- -

- Establishing communication channels, which allow constant monitoring of customer needs, fostering a relational marketing strategy with the creation of communities with consumers and customer relationship management (CRM) with the main customers.

Finally, good service provision includes

- -

- An adequate marketing and distribution structure close to the customers;

- -

- A technical staff conveniently prepared for the detection and solution of customer problems;

- -

- The ability to create a product range suited to customers’ changing needs over time.

Section 4 also originates from the insights gathered during the focus groups with experts, which were based on the following questions:

- -

- What internationalization opportunities might be seized most easily?

- -

- What lessons can we learn from the pandemic, and what are the main challenges and opportunities emerging and their impact on business models and internal resources?

- -

- Is innovation important in achieving competitive advantages in terms of products and processes?

- -

- Given the technological innovations resulting from the pandemic and the new emerging markets, will e-commerce have greater relevance in the business models of Portuguese companies?

- -

- How are companies addressing and planning for the long term to ensure the sustainability of the activity and the environment?

Section 5, on the other hand, incorporates the proposed business model resulting from insights gathered both from the focus groups with experts and individual interviews with producers.

In summary, while Section 4 stems from the findings and discussions in the focus groups with experts, Section 5 integrates the insights obtained from both the focus groups with experts and individual interviews with producers. These sections reflect a synthesis of the data collected and the discussions held during the research process.

4. Possible Business Development Guidelines

4.1. Products and Markets

One of the first decisions to be made when developing a business is to determine which products to sell (whether to manufacture in-house or to trade) and in which market segments. It is therefore a commercial vision (Freire 1998).

According to the segmentation used in the wine sector (for example, see the “Vitiviniculture Sectorial Diagnosis” report), the Table 3 shows a possible product–market matrix summary.

Regarding the national market, analyzing the statistics in Table 4 with the weight of the marketing channels, it can be seen that although distribution has increased its importance in terms of volume, restaurants still represent about 50% of the market value.

Simultaneously, the following Table 5 shows that the sales of certified wines had a very positive progression in recent years (from 2016 to 2021, an increase of more than 5% was noted, even accounting for the constraints in recent years associated with COVID-19), currently representing about 50% of the total market. Non-certified wines had a negative trend, with sales decreasing by about 10% from 2016 to 2021.

Unlike in some New World countries, such as Brazil, where the online wine market already has a significant weight in sales thanks to companies such as Wine.com or Evino. In Portugal, its weight is still quite small due to dispersion and accessibility of this product category through other off-trade distribution channels. During the pandemic, and due to the closure of on-trade channels (i.e., restaurants), online sales channels were very dynamic. At the same time, in order to reach consumers locked down at home, many wineries, including those in the Setúbal Peninsula, began to create an e-commerce section on their websites (e.g., Adega Cooperativa de Palmela).

Similarly, sales in the winery shop have always represented an important part of winery sales, particularly for small producers, who find it more difficult to supply the large distribution chains. This is also the case in the Setúbal Peninsula region, and even during the distribution challenges imposed by the lockdown, small producers, such as Quinta do Alcube, began organizing direct deliveries to their private customers.

The average price per liter of certified wine in Portugal in 2021 was EUR 4.93, up 3.6% from 2016, as can be seen in Table 6. The main region in terms of consumption in Portugal—the Alentejo region—had a much higher average price of EUR 5.30 thanks to a great appreciation since 2016 in the restaurant channel and particularly in distribution.

The growth in volume in the Setúbal Peninsula region compared to other regions was due to this perception of wines with a great price/quality ratio, which—in 2021—stood at EUR 3.58 per liter.

Regarding the international market, there has been a positive evolution in exports in recent years, especially in certified wines and countries outside the European Union. Table 7 shows that exports of certified wines increased by 17.4% from 2015 to 2021, with a remarkable growth of 27.5% in markets outside the European Union, currently representing a market share of 54% of total national exports.

Analyzing Portuguese wine exports by continent of destination, as shown in Table 8, it can be seen that markets such as America and non-community Europe represent significant business opportunities for Portuguese producers, with growth since 2015 of 82.5% and 260%, respectively.

In conclusion, concerning the product and market strategy, there seems to be evidence that the focus should be on the production of certified wines, which are increasingly valued by the different commercialization channels in the national market.

Regarding the international market, taking into consideration the diversity of grape varieties, which exist in the territory, the strong tradition of the sector with the application of traditional production techniques and the qualification of national human resources, there also seem to be opportunities to diversify the destination markets. This can be achieved through the progressive production of new certified wines with unique characteristics contributing to greater differentiation of the “Wines of Portugal” brand vis-a-vis the major global competitors. This vision was shared by the producers interviewed and the experts participating in the focus group.

4.2. Types of Competitive Advantage

Once the business development strategy is defined, the strategic positioning has to be determined; that is, the type of competitive advantage has to be determined (price or differentiation) Figure 2.

To compete with a cost advantage, it will be necessary to (Porter 1985)

- Seek to achieve economies of scale and experience, which requires a greater effort to obtain market share;

- Have strict cost control in terms of suppliers, efficient use of equipment, employees and stocks;

- Strive for maximum product standardization;

- Implement process simplification.

To compete with an advantage in terms of differentiation, one must (Porter 1985)

- Possess and master the technologies, especially those associated with product development;

- Meet the delivery deadlines better than the competition;

- Make a permanent effort in promotion and publicity, aiming above all to create good notoriety and/or brand image.

Thus, bearing in mind that Portuguese players are small compared to the main international competitors, and that it is therefore challenging to achieve the economies of scale, which would allow them to compete based on the price factor, the strategic positioning to be adopted should involve the development of unique skills, which contribute to the development of an offer based on the uniqueness and sophistication of the product. This strategy should be appropriately supported by investments in marketing communication, which project the brands onto major international markets.

Notice that positioning based on differentiation does not imply that companies do not also pursue cost efficiencies in their operational processes. This fact is even more relevant considering that Portuguese production factors are cheaper than those of other international competitors, such as Spain, Italy and France, which also contributes to the creation of comparative advantages in terms of costs, which may reduce the impact of the smaller scale of the activity.

Such competitive advantages are aligned with the suggestion to develop the product–market matrix defined in the previous section and shared by the producers and experts in the activities they participate in.

5. Development of a Business Model

Several approaches have been designed to identify sets of elements, blocks, areas or components, which any business model must consider. (Johnson et al. 2008) defined a set of four blocks. (Teece 2010) defined six essential elements to build a business model. (Wikström et al. 2010) addressed five sets of elements. (Osterwalder and Pigneur 2010) developed a model based on four blocks and nine components.

This study analyzes the business model for the wine sector in the Setúbal Peninsula according to Osterwalder and Pigneur’s model. According to these authors, this tool allows for the description, visualization, evaluation and alteration of existing business models or the creation of new models under a common and easily understandable language. The model is composed of nine basic components divided into four blocks: customers (value proposition), value offering (customer segment, channels and relationships), infrastructure (key resources, key activities and main partnerships) and financial viability (cost structure and revenue sources). Table 9 presents the nine components of this model in greater detail.

In fact, concerning the wine sector, there is a need for particular attention to be paid to the companies’ business models, which means the logic of the organization of the sector and its ability to create value sustainably.

The wine sector in the Setúbal Peninsula—considering the information gathered from regional stakeholders (producers and experts)—shows a trend toward concentration, with the emergence of producers on a national scale and with notoriety. As a result of the greater dynamism of their activity, they have sought large international markets with purchasing power, which value quality products. This trend is proven by the statistics available on the website of the Instituto da Vinha e do Vinho (Vineyard and Wine Institute), showing that the region is one of the three with the lowest number of producers. Thus, with regard to the business model, in general terms, and considering the business development strategies suggested in the previous sections, the companies’ value propositions should seek competitive positions, which capitalize on the uniqueness of the national grape varieties and traditional production processes and which contribute to the supply of high-quality products at competitive prices to the global market (as a consequence of cheaper production factors compared to major international competitors and increasingly efficient logistical processes).

In terms of customer segments, the product and market strategy, as mentioned before, should aim to diversify into new markets and penetrate segments with greater purchasing power, where uniqueness is valued and customers are not as price-sensitive. Therefore, there should be a tendency to expand the offer matrix to new markets based on competitive advantages grounded in product differentiation.

To reach the new markets, companies should pursue marketing channels (traders and sales representatives), which enable access to the premium segments (in the more unique wines) and mass consumption segments, such as large distribution chains for the less noble wines. Such channels are also fundamental for developing market relationships through the introduction of the national companies’ offers, through communication tools or by organizing tasting events, which contribute to the visibility and notoriety of the offers. Simultaneously, companies should also be firmly committed to participating in the main sector fairs and international competitions to establish direct contact with the final customers and develop closer relationships tailored to market needs.

Thus, revenues should come primarily from higher margins—arising from higher prices associated with the uniqueness of the products—but also from the larger scale of operations, which allows reaching larger markets.

Regarding their internal infrastructure, companies should, over time, try to incorporate into their work procedures the production, vineyard treatment and harvesting equipment, which is innovative and energy-efficient, in line with the best operational practices of the leading international competitors, combining tradition and innovation. Additionally, these material resources should be accompanied by the continuous hiring of qualified human resources with strong sector experience. This union of resources may contribute to companies in the region becoming a benchmark for the Portuguese wine sector. Concerning the key business activities, of note is the step related to vineyard treatment and maintenance processes, which contributes to increasing the vineyard’s longevity and productivity. This way, the periodic production capacity is increased, mitigating the impact of the smaller size of national properties compared to the competition in other larger markets. Finally, concerning partnerships, emphasis should be placed on the need to establish relationships with associations of regional producers, thus allowing the inclusion of the offer of different producers in the logistics operations associated with international markets, contributing to the lower cost per each bottle exported and to more competitive sales prices in comparison with external competitors.

Table 10 contains a summary with the suggested business model to be adopted by most companies in the Setúbal Peninsula.

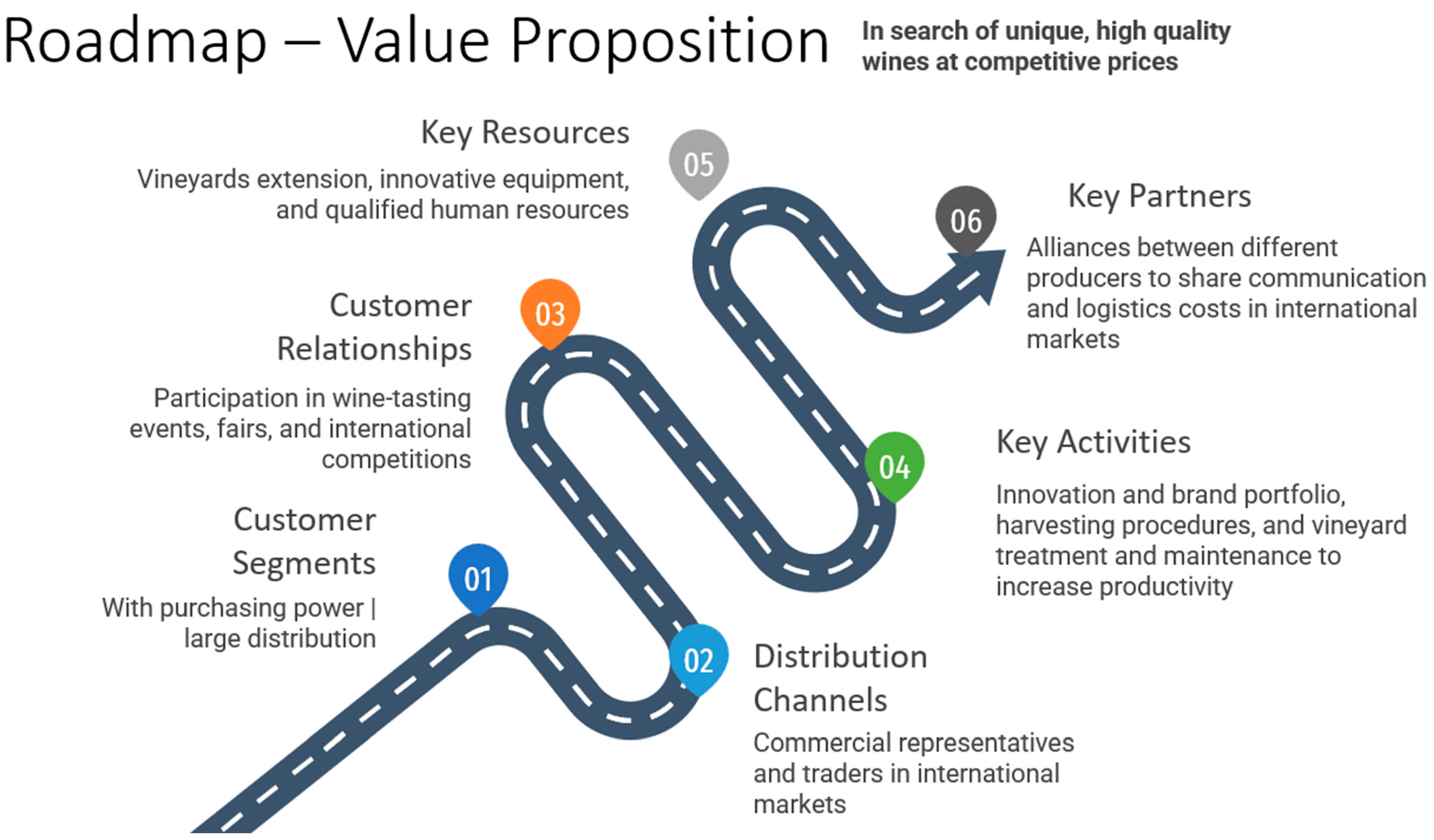

Figure 3 intends to highlight the path to be taken by companies in the wine sector in the Setúbal Peninsula to ensure sustained success over the coming years.

6. Conclusions

This research aimed to suggest a set of strategic development options for companies in the wine industry in the Setúbal Peninsula.

Thus, in the literature review, a reflection was put forward on some concepts and theories associated with strategic formulation. It encompassed issues such as the critical success factors of industries and the possible strategic alternatives regarding the definition of products and market segments to be targeted and the definition of competitive advantages (Kshetri 2018; Ansoff 1984; Porter 1980).

Regarding the empirical study, through interviews with the panels of experts, the critical success factors and strategic alternatives were identified for the development of companies in the wine industry in the Setúbal Peninsula, characterized by the definition of strategic positions favoring the penetration of high-value-added market segments, with special emphasis on international ones. An opportunity was also found for the implementation of combined strategies, which would provide high levels of differentiation associated with the unique potential of traditional knowledge and the diversity of grape varieties in the national territory and process efficiencies related to the implementation of the best technologies in different stages of the value chain of the farming and production activities. Finally, based on the proposed strategic alternatives, a suggested business model to be implemented was also described, which aligns the companies’ operating characteristics with the market segments and commercialization channels appropriate to the defined value proposition associated with the offer of unique, quality Portuguese wines at competitive prices.

Author Contributions

Conceptualization, T.C., N.T. and P.M.; formal analysis T.C., N.T.; investigation, T.C., N.T.; Writing-original draft, T.C.; Methodology, M.C., R.G., S.N.; Resources, T.C., M.C., R.G., S.N.; Data curation T.C., M.C., R.G., S.N.; Writing—review & editing, P.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research was financially supported by Instituto Politécnico de Setúbal.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are contained within the article.

Acknowledgments

The authors would like to thank the comments and suggestions from reviewers that contributed to improving this paper.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Aleffi, Chiara, Sabrina Tomasi, Concetta Ferrara, Cristina Santini, Gigliola Paviotti, Federica Baldoni, and Alessio Cavicchi. 2020. Universities and Wineries: Supporting Sustainable Development in Disadvantaged Rural Areas. Agriculture 10: 378. [Google Scholar] [CrossRef]

- Almeida, Sofia, Susana Mesquita, and Inês Carvalho. 2022. The COVID-19 impacts on the hospitality industry highlights from experts in portugal. Tourism and Hospitality Management 28. [Google Scholar] [CrossRef]

- Ansoff, H. Igor. 1984. Implanting Strategic Management. New York: Prentice Hall. [Google Scholar]

- Bibicioiu, Sorin, and Romeo Cătălin Creţu. 2013. Enotourism: A Niche Tendency within the Tourism Market. Scientific Papers Series Management, Economic Engineering in Agriculture and Rural Development 13. [Google Scholar]

- Bruwer, Johan, Michael Coode, Anthony Saliba, and Frikkie Herbst. 2013. Wine Tourism Experience Effects of the Tasting Room on Consumer Brand Loyalty. Tourism Analysis 18: 399–414. [Google Scholar] [CrossRef]

- Carmer, Adam, Natalia Velikova, Jean Hertzman, Christine Bergman, Michael Wray, and Taricia LaPrevotte Pippert. 2020. An Inquiry Into the Pedagogy of the Sensory Perception Tasting Component of Wine Courses in the Time of COVID-19. Wine Business Journal 4: 96–115. [Google Scholar] [CrossRef]

- Carroquino, Javier, Nieves Garcia-Casarejos, and Pilar Gargallo. 2020. Classification of Spanish Wineries According to Their Adoption of Measures against Climate Change. Journal of Cleaner Production 244: 118874. [Google Scholar] [CrossRef]

- Christ, Katherine L., and Roger L. Burritt. 2013. Critical Environmental Concerns in Wine Production: An Integrative Review. Journal of Cleaner Production 53: 232–42. [Google Scholar] [CrossRef]

- Commité Européen des Enterprises Vins. 2021. EU Wine Sector-CEEV. Available online: https://www.ceev.eu/about-the-eu-wine-sector/ (accessed on 27 February 2024).

- Compés, Raúl, Samuel Faria, Tânia Gonçalves, João Rebelo, Vicente Pinilla, and Katrin Simon Elorz. 2022. The Shock of Lockdown on the Spending on Wine in the Iberian Market: The Effects of Procurement and Consumption Patterns. British Food Journal 124: 1622–40. [Google Scholar] [CrossRef]

- Coyne, Matthew. 2020. Three Sticks Wines: Digital Marketing, Branding, and Hospitality During a Crisis. Wine Business Journal 4: 27–51. [Google Scholar] [CrossRef]

- DeYoung, Hannah. 2020. Napa Green: Funding Nonprofit Social Ventures in Crisis. Wine Business Journal. [Google Scholar] [CrossRef]

- Directorate-General for Agriculture and Rural Development. 2022. Agri-Wine Prices. Available online: https://agridata.ec.europa.eu/extensions/DashboardWine/WinePrice.html (accessed on 27 February 2024).

- Duarte Alonso, Abel, Alessandro Bressan, Oanh Thi Kim Vu, Lan Thi Ha Do, Roberta Garibaldi, and Andrea Pozzi. 2022. How Consumers Relate to Wine during COVID-19—A Comparative, Two Nation Study. International Journal of Wine Business Research 34: 590–607. [Google Scholar] [CrossRef]

- Dubois, Magalie, Lara Agnoli, Jean Marie Cardebat, Raúl Compés, Benoit Faye, Bernd Frick, Davide Gaeta, Eric Giraud-Héraud, Eric Le Fur, Livat Florine, and et al. 2021. Did Wine Consumption Change during the Covid-19 Lockdown in France, Italy, Spain, and Portugal? Journal of Wine Economics 16: 131–68. [Google Scholar] [CrossRef]

- Eastham, Jane. 2022. Post-Covid-19 Developments in the Wine Tourism Sector. In Routledge Handbook of Wine Tourism. London: Routledge. [Google Scholar] [CrossRef]

- European Commission. 2022. Agri-Food Data Portal—Agricultural Markets. Available online: https://agridata.ec.europa.eu/extensions/DataPortal/wine.html (accessed on 27 February 2024).

- European Commission, DG Agriculture, and Rural Development. 2020. Short Term Outlook for EU Agricultural Markets in 2020: Spring 2020. Luxembourg: European Commission. [Google Scholar]

- European Parliament and Council. 2013. Regulation (EU) No 1308/2013 of the European Parliament and of the Council of 17 December 2013. Available online: https://eurlex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32013R1308 (accessed on 27 February 2024).

- Eurostat. 2021. Key Figures on the European Food Chain—2021 Edition. Statistical Books. Available online: https://ec.europa.eu/eurostat/web/products-key-figures/-/ks-fk-21-001 (accessed on 27 February 2024).

- Ferrer, Juan R., María Carmen García-Cortijo, Vicente Pinilla, and Juan Sebastián Castillo-Valero. 2022. The Business Model and Sustainability in the Spanish Wine Sector. Journal of Cleaner Production 330: 129810. [Google Scholar] [CrossRef]

- Flores, Shana Sabbado. 2018. What Is Sustainability in the Wine World? A Cross-Country Analysis of Wine Sustainability Frameworks. Journal of Cleaner Production 172: 2301–12. [Google Scholar] [CrossRef]

- Fortune Business Insights. n.d. Wine Market Size, Share, Analysis and Industry Trends. Available online: https://www.fortunebusinessinsights.com/wine-market-102836 (accessed on 19 January 2024).

- Fountain, Joanna, Rory Hill, and Nicholas Cradock-Henry. 2022. Wine Tourism and the Global Pandemic Realizing Opportunities for New Wine Markets and Experiences. In Routledge Handbook of Wine Tourism. London: Routledge. [Google Scholar] [CrossRef]

- Francisco Avillez. 2014. A Agricultura Portuguesa - Caminhos Para Um Crescimento Sustentaável. AGRO.GES. Available online: https://www.agroges.pt/a-agricultura-portuguesa-caminhos-para-um-crescimento-sustentavel/ (accessed on 27 February 2024).

- Freire, Adriano. 1998. Estratégia—Sucesso Em Portugal. Lisboa: Verbo. [Google Scholar]

- Fuentes-Fernández, Rosana, Javier Martínez-Falcó, Eduardo Sánchez-García, and Bartolomé Marco-Lajara. 2022. Does Ecological Agriculture Moderate the Relationship between Wine Tourism and Economic Performance? A Structural Equation Analysis Applied to the Ribera Del Duero Wine Context. Agriculture 12: 2143. [Google Scholar] [CrossRef]

- Getz, Donald, Ross Dowling, Jack Carlsen, and Donald Anderson. 1999. Critical Success Factors for Wine Tourism. International Journal of Wine Marketing 11: 20–43. [Google Scholar] [CrossRef]

- Hall, C. Michael, and Liz Sharples. 2008. Food and Wine Festivals and Events Around the World: Development, Management and Markets. London: Routledge. [Google Scholar] [CrossRef]

- Johnson, Mark W., Clayton M. Christensen, and Henning Kagermann. 2008. Reinventing Your Business Model. Harvard Business Review 86: 50–59. [Google Scholar]

- Jorge, Oriol, Adria Pons, Josep Rius, Carla Vintró, Jordi Mateo, and Jordi Vilaplana. 2020. Increasing Online Shop Revenues with Web Scraping: A Case Study for the Wine Sector. British Food Journal 122: 3383–401. [Google Scholar] [CrossRef]

- Kshetri, Nir. 2018. 1 Blockchain’s Roles in Meeting Key Supply Chain Management Objectives. International Journal of Information Management 39: 80–89. [Google Scholar] [CrossRef]

- Lu, Y. 2020. Wine Report 2020, Statista Consumer Market Outlook-Segment Report. Available online: https://www.statista.com/study/48818/wine-report/ (accessed on 27 February 2024).

- Miftari, Iliriana, Marija Cerjak, Marina Tomić Maksan, Drini Imami, and Vlora Prenaj. 2021. Consumer Ethnocentrism and Preference for Domestic Wine in Times of Covid-19. Studies in Agricultural Economics 123: 103–13. [Google Scholar] [CrossRef]

- Ministério da Agricultura, do Desenvolvimento Rural e das Pescas (MADRP). 2007. Olivicultura—Diagnóstico Sectorial. Lisbon: Gabinete de Planeamento e Políticas. [Google Scholar]

- Niklas, Britta, Jean Marie Cardebat, Robin M. Back, Davide Gaeta, Vicente Pinilla, João Rebelo, Roberto Jara-Rojas, and Guenter Schamel. 2022. Wine Industry Perceptions and Reactions to the COVID-19 Crisis in the Old and New Worlds: Do BusinessModels Make a Difference? Agribusiness 38: 810–31. [Google Scholar] [CrossRef] [PubMed]

- Osterwalder, Alexander, and Yves Pigneur. 2010. Business Model Generation: A Handbook for Visionaries, Game Changers, and Challengers. In A Handbook for Visionaries, Game Changers, and Challengers. Hoboken: John Wiley & Sons. [Google Scholar] [CrossRef]

- Patton, Michael Quinn. 2015. Qualitative Research and Evaluation Methods, 4th ed. London: Sage Publications. [Google Scholar]

- Porter, Michael E. 1980. Competitive Strategy: Techniques for Analyzing Industries and Competitors. Boston: Faculty & Research, Harvard Business School. [Google Scholar]

- Porter, Michael E. 1985. Competitive Advantage: Creating and Sustaining Superior Performance. New York City: The Free Press. [Google Scholar]

- Profi Press. n.d. The Pandemic Has Significantly Disrupted the Wine Market. Available online: https://zemedelec.cz/pandemievyrazne-narusila-trh-s-vinem/ (accessed on 19 January 2024).

- Rebelo, João, Raúl Compés, Samuel Faria, Tânia Gonçalves, Vicente Pinilla, and Katrin Simón-Elorz. 2021. Covid-19 Lockdown and Wine Consumption Frequency in Portugal and Spain. Spanish Journal of Agricultural Research 19: e0105R. [Google Scholar] [CrossRef]

- Schimmenti, Emanuele, Giuseppina Migliore, Caterina Patrizia Di Franco, and Valeria Borsellino. 2016. Is There Sustainable Entrepreneurship in the Wine Industry? Exploring Sicilian Wineries Participating in the SOStain Program. Wine Economics and Policy 5: 14–23. [Google Scholar] [CrossRef]

- Silverman, David. n.d. Doing Qualitative Research: A Practical Handbook, 3rd ed. New York: Sage Publications.

- Stake, Robert E. 2010. Qualitative Research: Studying How Things Work. In Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis. New York City: The Guilford Press, p. 53. [Google Scholar]

- Statista Market Forecast. 2022. Wine—Worldwide. Available online: https://www.statista.com/outlook/cmo/alcoholic-drinks/wine/worldwide (accessed on 27 February 2024).

- Teece, David J. 2010. Business Models, Business Strategy and Innovation. Long Range Planning 43: 172–94. [Google Scholar] [CrossRef]

- Ugaglia, Adeline Alonso. 2019. Introduction: The Diversity of Organizational Patterns in the Wine Industry. In The Palgrave Handbook of Wine Industry Economics. Berlin/Heidelberg: Springer. [Google Scholar] [CrossRef]

- Wikström, Kim, Karlos Artto, Jaakko Kujala, and Jonas Söderlund. 2010. Business Models in Project Business. International Journal of Project Management 28: 832–41. [Google Scholar] [CrossRef]

- Wittwer, Glyn, and Kym Anderson. 2021. Covid-19 and Global Beverage Markets: Implications for Wine. Journal of Wine Economics 16: 117–30. [Google Scholar] [CrossRef]

- Yin, Robert. 2011. Qualitative Research From Start To Finish. New York City: The Guilford Press. [Google Scholar]

- Yin, Robert K. 2003. Case Study Research and Applications: Design and Methods, 3rd ed. New York: SAGE Publications, Inc. [Google Scholar]

Figure 1.

Map of the Setúbal Peninsula. Source: https://www.thebft.co.uk/index.php/business-directory/item/setubal-peninsula-wines (accessed on 6 April 2024).

Figure 1.

Map of the Setúbal Peninsula. Source: https://www.thebft.co.uk/index.php/business-directory/item/setubal-peninsula-wines (accessed on 6 April 2024).

Figure 2.

Michael Porter’s generic strategies.

Figure 3.

Roadmap for the wine sector in the Setúbal Peninsula.

{kind=link}

{kind=link}

{kind=link}

Table 1.

Characterization of producers interviewed.

| Legal Structure of the Business | Number of Employees | In Operation Since (Year) | Business Model (Nationally) | Business Model (Internationally) | Age of the Main Manager |

|---|---|---|---|---|---|

| Private Limited Company | 30–49 | 1950 | Self-distribution | In-house export team | Between 41 and 65 years old |

| Private Limited Company | 5–9 | 2008 | Self-distribution | Both | Over 25 and under 41 years old |

| Private Limited Company | 15–29 | 1996 | Both | Both | Over 25 and under 41 years old |

| Limited Liability Cooperative | 76–100 | 1958 | Self-distribution | In-house export team | Between 41 and 65 years old |

| Private Limited Company | 10–14 | 2017 | Both | Both | Between 41 and 65 years old |

| Private Limited Company | 5–9 | 1992 | Using national distributors | Both | Between 41 and 65 years old |

| Cooperative | 50–75 | 1955 | Using national distributors | Both | Between 41 and 65 years old |

| Private Limited Company | 1–4 | 2011 | Both | In-house export team | Between 41 and 65 years old |

| Sole Proprietorship via Shares (LLC) | 5–9 | 1999 | Both | Both | Between 41 and 65 years old |

| Public Limited Company | 15–29 | 1964 | Both | Both | Between 41 and 65 years old |

| Private Limited Company | 10–14 | 2008 | Self-distribution | Both | Between 41 and 65 years old |

| Private Limited Company | 1–4 | 1997 | Both | Using trading companies | Agents or brokers |

Table 2.

Critical success factors.

| Key Buying Factors | Key Competition Factors | Critical Success Factors |

|---|---|---|

| Prices | Process Efficiency | Prices |

| Response Capacity | Technological Innovation | Process Innovation |

| Image | Marketing Communication | Marketing Communication |

| Quality | Product Innovation | Product Differentiation |

| Relationship | Market Adequacy | Service Level |

Table 3.

Product–market matrix.

| Wine Type | National Market | International Market | ||||

|---|---|---|---|---|---|---|

| Intra EU | Extra EU | |||||

| Restaurants | Distribution | Restaurants | Distribution | Restaurants | Distribution | |

| Certified | ||||||

| Non-Certified | ||||||

Table 4.

Evolution in still wine sales in the domestic market by distribution channel (as percentage).

Table 4.

Evolution in still wine sales in the domestic market by distribution channel (as percentage).

| January–March | Variation 1st Qtr. 21/22 | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2021 | 2022 | ||

| Volume Quota | |||||||||

| Restaurants | 29% | 30% | 31% | 32% | 20% | 17% | 6% | 26% | 20% |

| Distribution | 71% | 70% | 69% | 68% | 80% | 83% | 94% | 74% | −20% |

| Total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 0% |

| Value Quota | |||||||||

| Restaurants | 54% | 56% | 55% | 56% | 39% | 34% | 13% | 48% | 35% |

| Distribution | 46% | 44% | 45% | 44% | 61% | 66% | 87% | 52% | −35% |

| Total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 0% |

Source: IVV (2022).

Table 5.

Evolution in wine sales by region (liters).

| Region | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

|---|---|---|---|---|---|---|

| Certified wines (total) | 109,737,188 | 112,363,732 | 115,103,876 | 124,599,625 | 112,002,071 | 115,420,759 |

| Minho | 18,625,525 | 19,983,662 | 20,334,191 | 21,469,566 | 19,721,313 | 19,828,643 |

| Tras os montes | 539,211 | 687,664 | 429,621 | 392,807 | 274,448 | 283,167 |

| Douro | 11,753,648 | 13,623,943 | 13,143,932 | 12,900,583 | 12,304,512 | 13,632,325 |

| Beiras | 108,515 | 88,963 | 259,060 | 298,131 | 93,359 | 126,421 |

| Terras de cister | 33,870 | 27,242 | 23,820 | 29,584 | 54,417 | 31,020 |

| Beira atlantico | 1,062,653 | 762,668 | 1,066,136 | 883,932 | 522,329 | 376,644 |

| Terras do dão | 6,243,657 | 5,984,241 | 6,482,985 | 6,587,279 | 5,490,780 | 5,300,953 |

| Beira interior | 372,565 | 415,358 | 770,569 | 903,668 | 848,363 | 969,075 |

| Lisbon | 3,895,621 | 4,806,982 | 5,482,162 | 5,289,946 | 4,587,955 | 5,044,984 |

| Tejo | 4,845,416 | 5,201,550 | 5,167,240 | 10,234,310 | 8,944,478 | 8,605,083 |

| Setúbal peninsula | 14,042,265 | 14,810,295 | 17,624,800 | 20,081,558 | 20,605,445 | 21,792,324 |

| Alentejo | 47,928,070 | 45,576,684 | 43,835,850 | 45,113,270 | 38,329,383 | 39,213,524 |

| Algarve | 286,172 | 394,480 | 483,510 | 414,991 | 225,289 | 216,596 |

| Non-certified wines (total) | 147,163,289 | 155,031,652 | 148,990,336 | 153,690,291 | 138,726,043 | 133,221,786 |

| Imported | 3,046,159 | 3,186,089 | 4,597,781 | 8,165,902 | 8,380,755 | 9,317,916 |

| National | 144,117,130 | 151,845,563 | 144,392,555 | 145,524,389 | 130,345,288 | 123,903,870 |

| Wines sales (total) | 256,900,477 | 267,395,384 | 264,094,212 | 278,289,916 | 250,728,114 | 248,642,545 |

Table 6.

Average price in the main regions of Portugal by distribution channel (price per liter of certified wine).

Table 6.

Average price in the main regions of Portugal by distribution channel (price per liter of certified wine).

| Region/Distribution Channel | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | VAR% 2021/2016 |

|---|---|---|---|---|---|---|---|

| Minho | 4.43 | 4.68 | 4.79 | 4.86 | 4.21 | 4.24 | −4.2% |

| Restaurants | 8.34 | 8.39 | 8.77 | 8.86 | 8.71 | 8.71 | 4.4% |

| Distribution | 3.11 | 3.18 | 3.27 | 3.29 | 3.27 | 3.33 | 7.1% |

| Douro | 7.13 | 7.73 | 8.49 | 9.61 | 8.26 | 8.23 | 15.5% |

| Restaurants | 13.14 | 14.01 | 15.71 | 16.52 | 16.82 | 16.09 | 22.4% |

| Distribution | 4.61 | 4.76 | 5.22 | 5.88 | 5.93 | 6.19 | 34.4% |

| Terras do dão | 5.40 | 5.18 | 4.76 | 4.95 | 4.47 | 4.49 | −16.7% |

| Restaurants | 8.55 | 10.99 | 8.41 | 8.14 | 7.90 | 7.68 | −10.1% |

| Distribution | 3.09 | 3.06 | 3.16 | 3.35 | 3.52 | 3.72 | 20.2% |

| Lisbon | 4.29 | 4.33 | 4.59 | 4.44 | 3.94 | 4.51 | 5.1% |

| Restaurants | 8.62 | 9.23 | 10.04 | 9.73 | 11.96 | 11.14 | 29.4% |

| Distribution | 2.97 | 3.09 | 3.34 | 3.39 | 3.41 | 3.53 | 18.8% |

| Tejo | 3.76 | 3.77 | 3.75 | 3.23 | 3.08 | 3.11 | −17.1% |

| Restaurants | 6.51 | 6.19 | 5.86 | 4.65 | 5.05 | 5.21 | −20.0% |

| Distribution | 2.59 | 2.66 | 2.84 | 2.40 | 2.46 | 2.53 | −2.4% |

| Setúbal peninsula | 3.50 | 3.62 | 3.66 | 3.81 | 3.44 | 3.58 | 2.3% |

| Restaurants | 9.46 | 9.83 | 9.87 | 9.56 | 8.99 | 9.56 | 1.1% |

| Distribution | 2.71 | 2.86 | 2.99 | 3.00 | 3.03 | 3.20 | 18.4% |

| Alentejo | 4.72 | 5.27 | 5.85 | 6.02 | 5.22 | 5.30 | 12.3% |

| Restaurants | 10.44 | 10.89 | 11.56 | 11.39 | 11.55 | 11.89 | 14.0% |

| Distribution | 3.22 | 3.53 | 3.79 | 3.96 | 4.04 | 4.23 | 31.4% |

| Total | 4.76 | 5.14 | 5.42 | 5.49 | 4.80 | 4.93 | 3.6% |

| Restaurants | 9.85 | 10.41 | 10.81 | 10.40 | 10.47 | 10.65 | 8.2% |

| Distribution | 3.21 | 3.42 | 3.59 | 3.66 | 3.73 | 3.92 | 22.0% |

Table 7.

Exports by product type.

| Intra + Extra EU | HL | Variation 2021/2020 | ||||||

|---|---|---|---|---|---|---|---|---|

| January–December | ||||||||

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | ||

| Certified Wine | 928,490 | 981,167 | 1,105,731 | 1,118,730 | 1,155,086 | 1,351,796 | 1,429,605 | 5.8% |

| Wine with Denomination of Origin (DO) | 517,656 | 550,863 | 596,491 | 618,225 | 606,058 | 688,890 | 712,533 | 3.4% |

| Wine with Geographical Identification (IG) | 410,834 | 430,304 | 509,241 | 500,505 | 549,028 | 662,906 | 717,072 | 8.2% |

| Wine (ex-table) | 1,128,260 | 1,070,522 | 1,154,685 | 1,138,946 | 1,102,411 | 1,089,173 | 1,107,916 | 1.7% |

| Wine | 1,085,056 | 1,031,731 | 1,121,370 | 1,067,887 | 1,044,513 | 1,028,243 | 1,054,210 | 2.5% |

| Wine with Grape Variety Indication | 43,203 | 38,792 | 33,315 | 71,059 | 57,898 | 60,931 | 53,707 | −11.9% |

| Liqueur Wine with Protected Denomination of Origin (DOP)/Protected Geographical Identification (IGP) | 701,527 | 678,884 | 677,690 | 646,923 | 657,908 | 657,029 | 691,440 | 5.2% |

| Porto | 671,981 | 651,340 | 640,027 | 607,327 | 617,049 | 611,902 | 652,120 | 6.6% |

| Madeira | 24,294 | 21,521 | 28,246 | 28,135 | 27,052 | 23,827 | 25,885 | 8.6% |

| Others | 5252 | 6023 | 9417 | 11,461 | 13,807 | 21,300 | 13,434 | −36.9% |

| Liqueur Wine without DOP/IGP | 8583 | 9487 | 3120 | 3471 | 3011 | 2603 | 3921 | 50.7% |

| Sparkling Wines | 13,205 | 17,557 | 13,948 | 22,361 | 17,577 | 20,965 | 18,199 | −13.2% |

| Other Wines and Musts | 18,123 | 21,889 | 26,395 | 27,768 | 27,217 | 29,819 | 35,222 | 18.1% |

| Total | 2,798,189 | 2,779,505 | 2,981,569 | 2,958,198 | 2,963,210 | 3,151,384 | 3,286,303 | 4.3% |

| Total Intra EU | 1,402,522 | 1,646,785 | 1,678,630 | 1,687,863 | 1,567,970 | 1,411,747 | 1,506,129 | 6.7% |

| Total Extra EU | 1,395,667 | 1,132,719 | 1,302,940 | 1,270,335 | 1,395,240 | 1,739,637 | 1,780,173 | 2.3% |

Source: IVV (2022).

Table 8.

Exports per continent.

| Destination | HL | Variation 2021/2020 | ||||||

|---|---|---|---|---|---|---|---|---|

| January–December | ||||||||

| 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | ||

| Africa | 744,080 | 383,543 | 468,250 | 425,928 | 495,335 | 447,609 | 456,921 | 2.1% |

| America | 378,452 | 419,664 | 497,364 | 525,433 | 572,320 | 660,942 | 690,730 | 4.5% |

| Asia | 122,023 | 130,183 | 161,784 | 135,504 | 124,429 | 94,860 | 112,960 | 19.1% |

| European community | 1,402,522 | 1,646,785 | 1,678,630 | 1,687,863 | 1,567,970 | 1,411,747 | 1,506,129 | 6.7% |

| Non-community Europe | 139,362 | 184,952 | 159,232 | 165,944 | 182,494 | 516,242 | 502,602 | −2.6% |

| Oceania | 8759 | 10,928 | 11,873 | 13,726 | 16,706 | 18,701 | 15,096 | −19.3% |

| Other destinations | 2991 | 3450 | 4435 | 3800 | 3956 | 1283 | 1864 | 45.4% |

| Total | 2,798,189 | 2,779,505 | 2,981,569 | 2,958,198 | 2,963,210 | 3,151,384 | 3,286,303 | 4.3% |

Source: IVV (2022).

Table 9.

The nine components of the CANVAS business model.

| Block/Macro Area | Component | Synthetic Description |

|---|---|---|

| Offer (What?) | Value Proposition (VP) | Describes the set of products and services, which create value for a specific customer segment. |

| Client (Who?) | Customer Segments (CS) | Various groups of people or organizations, which a company aims to reach. |

| Channels (CN) | Describes how a company communicates and tries to influence its customer segments to deliver a value proposition. | |

| Customer Relationship (RC) | Describes the types of relationships a company establishes with specific customer segments. | |

| Infrastructure (How?) | Key Resources (KR) | Describes the most important assets for the functioning of the business model. |

| Key Activities (KA) | Describes the most important things a company must do to make its business model work. | |

| Key Partnerships (KP) | Describes the network of suppliers and partners, which make the business model work. | |

| Financial Viability (How much?) | Cost Structure (CS) | Describes all the resources involved in operating a business model, as well as their cost. |

| Income Flow (IF) | Represents the money, which a company generates from each customer segment. |

Source: Adapted from Osterwalder and Pigneur (2010).

Table 10.

Suggested business model.

| Block/Macro Area | Component | Main Characteristics |

|---|---|---|

| Offer (What?) | Value Proposition | Unique, high-quality wines at competitive prices. |

| Client (Who?) | Customer Segments | Final customers—consumers with purchasing power—large distribution. |

| Channels | Commercial representatives and traders in international markets. | |

| Customer Relationship | Participation in wine-tasting events, fairs and international competitions. | |

| Infrastructure (How?) | Key Resources | Vineyard extension, innovative equipment and qualified human resources. |

| Key Activities | Innovation and brand portfolio, harvesting procedures and vineyard treatment and maintenance to increase productivity. | |

| Key Partners | Alliances between different producers to share communication and logistics costs in international markets. | |

| Financial Viability (How much?) | Cost Structure | Vineyard treatment equipment and human resources. |

| Revenue Streams | The scale of operations and high margins based on higher selling prices related to the unique quality of the wines. |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Costa, T.; Teixeira, N.; Cravidão, M.; Galvão, R.; Nunes, S.; Mares, P. A Strategic Roadmap for the Wine Sector in the Setúbal Peninsula. Adm. Sci. 2024, 14, 77. https://doi.org/10.3390/admsci14040077

AMA Style

Costa T, Teixeira N, Cravidão M, Galvão R, Nunes S, Mares P. A Strategic Roadmap for the Wine Sector in the Setúbal Peninsula. Administrative Sciences. 2024; 14(4):77. https://doi.org/10.3390/admsci14040077

Chicago/Turabian StyleCosta, Teresa, Nuno Teixeira, Mário Cravidão, Rosa Galvão, Sandra Nunes, and Pedro Mares. 2024. "A Strategic Roadmap for the Wine Sector in the Setúbal Peninsula" Administrative Sciences 14, no. 4: 77. https://doi.org/10.3390/admsci14040077

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.