Positioning in the Global Value Chain as a Sustainable Strategy: A Case Study in a Mature Industry

Abstract

:1. Introduction

1.1. Introduction Objectives

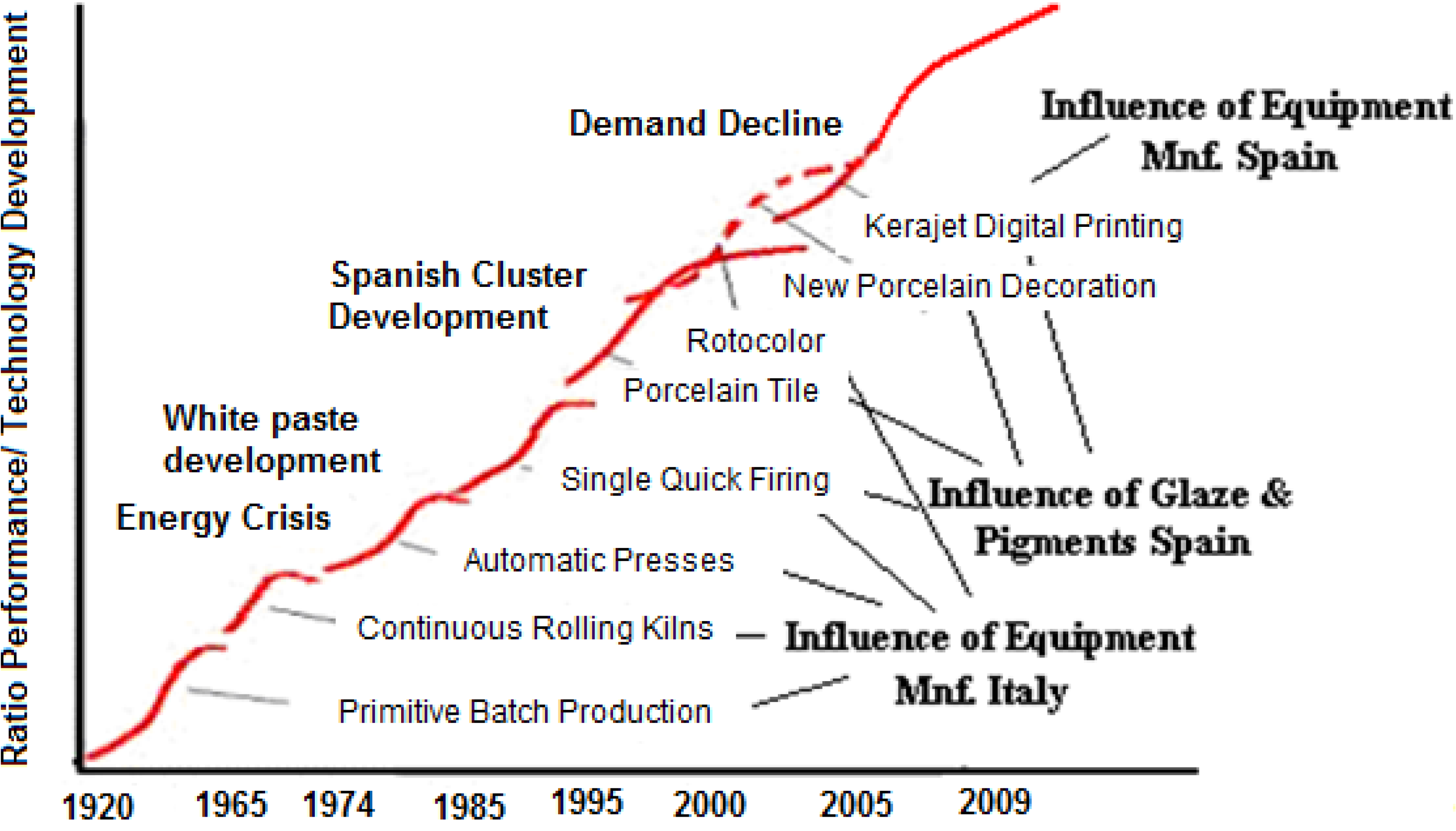

1.2. Context of Innovation System within a Cluster Context

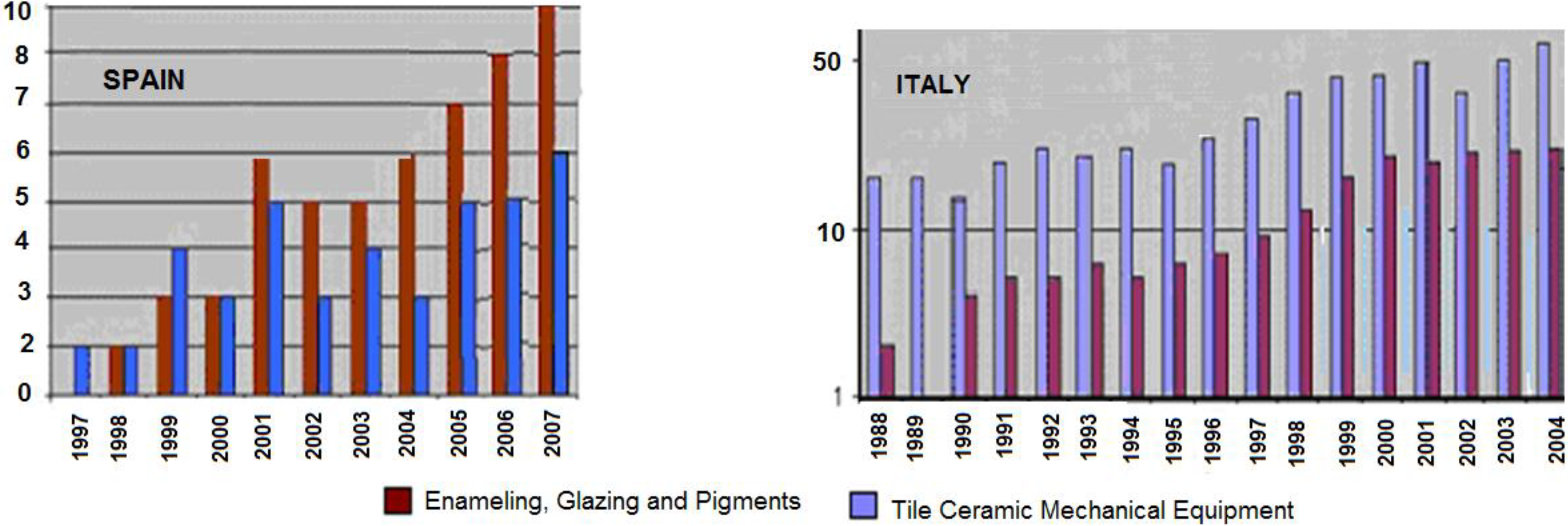

2. The Spanish Ceramic Tile Innovation System

2.1. Innovation Systems and Innovation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | 2007 (m.2Mill.) | 2008 (Sq.m.Mill.) | 2009 (Sq.m.Mill.) | 2010 (Sq.m.Mill.) | 2011 (Sq.m.Mill.) | % on 2011 world production | % var. 11/10 |

|---|---|---|---|---|---|---|---|

| China | 3200 | 3400 | 3600 | 4200 | 4800 | 45.7 | 14.3 |

| Brazil | 637 | 713 | 715 | 753 | 844 | 8.0 | 12.1 |

| India | 385 | 390 | 490 | 550 | 617 | 5.9 | 12.2 |

| Iran | 250 | 320 | 350 | 400 | 475 | 4.5 | 18.8 |

| Italy | 559 | 513 | 368 | 387 | 400 | 3.8 | 3.2 |

| Spain | 585 | 495 | 324 | 366 | 392 | 3.7 | 7.1 |

| Vietnam | 254 | 270 | 295 | 375 | 380 | 3.6 | 1.3 |

| Indonesia | 235 | 276 | 278 | 287 | 317 | 3.0 | 10.6 |

| Turkey | 260 | 225 | 205 | 245 | 260 | 2.5 | 6.1 |

| Mexico | 215 | 223 | 204 | 210 | 219 | 2.1 | 4.3 |

| Egypt | 140 | 160 | 200 | 220 | 175 | 1.7 | −20.5 |

| Thailand | 130 | 130 | 128 | 132 | 149 | 1.4 | 12.9 |

2.2. Characteristics of the Spanish Ceramic Tile Innovation System

| Interviews and Secondary Data | Castellon |

|---|---|

| Cluster paradigm * | Production focus; starting to change to a more sophisticated business chain |

| Competitive advantages * | Glazing material suppliers leading the world industry; effective institutions; high know-how and tacit knowledge; efficient production process; clay in the area; collective efficiency |

| Ceramic tile active workers | 26,100 |

| Ceramic tile firms | 265; 73% less than 100 workers |

| Ceramic tile turnover | 3448 M Euros |

| Exports | 55% |

| Export average price | 5.77 Euros/m2 |

| Glazing firms | 26 |

| Glazing firms turnover | 835.9 M euros |

| Glazing firms workers | 3487 |

| Ceramic Equipment firms | 41 |

| Ceramic Equipment workers | 1250 |

| Ceramic Equipment turnover | 520 M euros |

| American segments covered | Followers, medium and low segments covered |

| European segments covered | Leading Portugal, U.K. and Ireland. Followers in other markets. Medium and low segments covered |

| Other institutions | Chambers of Commerce and other institutions |

| R&D personnel in Institutions ** | 56 full time (ITC) |

| R&D institutes budget from projects ** | Around 3,635,000 Euros |

3. The Value Chain Approach

3.1. Theoretical Approach

| Types | Definition | Characteristics |

|---|---|---|

| Market | Firms deal with each other mainly in “arms-length” exchange transactions | Many customers/many suppliers Repeat transactions possible, but information flows are limited No technical assistance |

| Balanced network | Firms form networks in which no one firm or group of firms exercises undue control over the others. Firms prefer to deal with other members of their networks. | The supplier has various customers If the supplier has few customers, the customer has few suppliers Intense information flow in both directions Both sides have capabilities that are hard to substitute. Commitment to solve problems through negotiation rather than threat or exit |

| Directed network | Firms form networks that tend to be controlled by certain lead firms. The lead firms specify what is to be produced by whom, and they monitor the performance of the producing firms. | The main customer takes at least 50% of the output The customer defines the product (design and technical specification) Monitoring of supplier performance by the customer The supplier’s exit options are more restricted than the customer’s The customer provides technical assistance The customer knows more about the supplier’s costs and capabilities than the supplier knows about the customer’s |

| Hierarchy | Firms are vertically integrated, so that they can directly control all or most of the activities of the chain | Vertical integration of several chain stages within the firm Supplying establishment owned by customer or vice versa Very limited autonomy to take decisions at the local level Having to consult with or obtain permission from the “headquarters” |

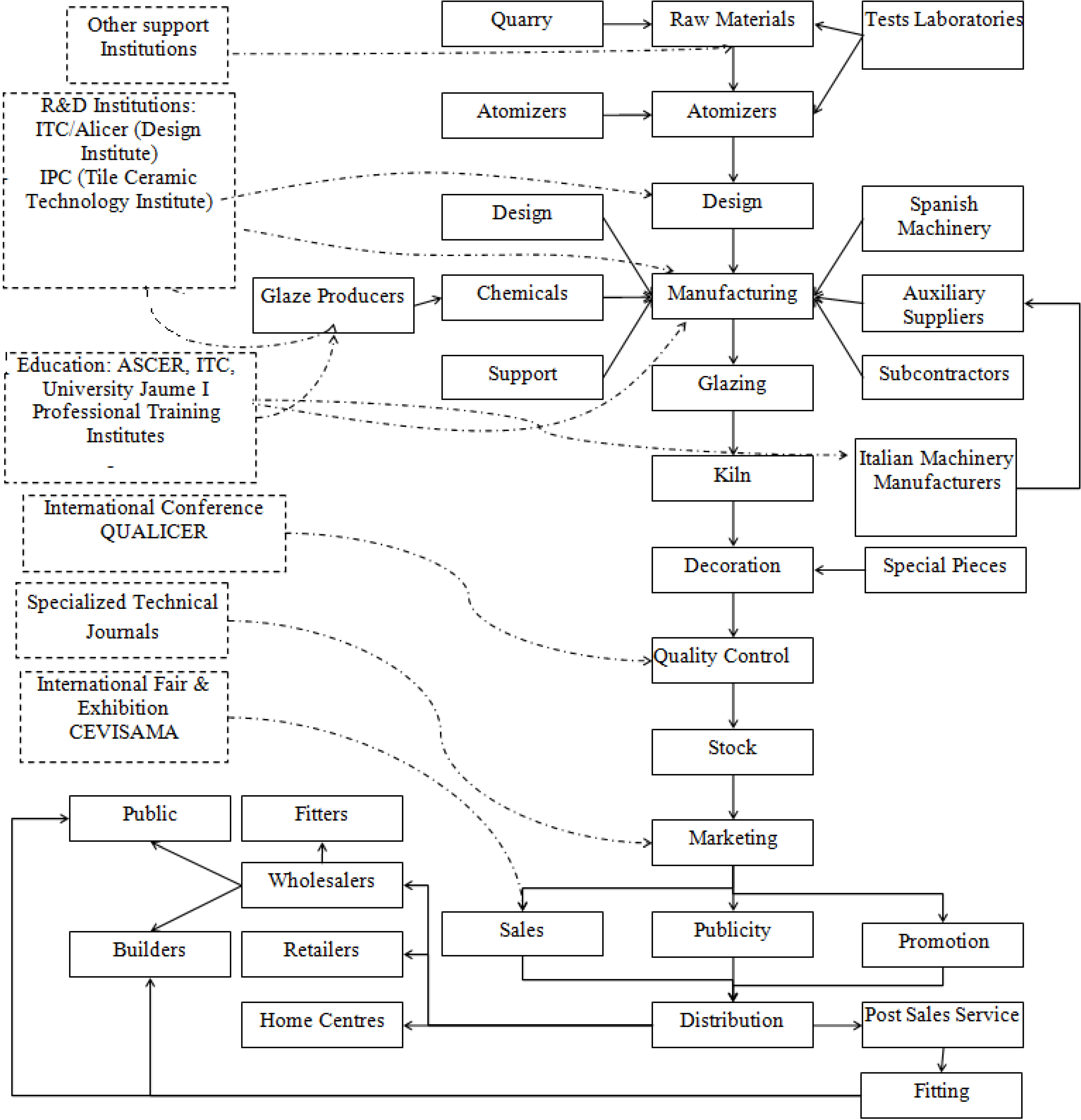

3.2. The Agents and Actors in the Value Chain

3.3. Governance Measurement Indicators

| Indicators | Source of Data | Type |

|---|---|---|

| Share of chain sales | Balance sheets | Quantitative |

| Share of chain value added | Firm-level interviews, performance data | Quantitative, Qualitative |

| Share of chain profits | Balance sheets | Quantitative |

| Rate of profit | Balance sheets | Quantitative |

| Share of chain buying power | Firm-level interviews | Quantitative, Qualitative |

| Control over a key technology (e.g., drive-train in autos) and holder of distinctive competence | Firm level interviews, patent registration | Quantitative Qualitative |

| Holder of chain “market identity” (e.g., brand name) | Firm-level interviews; studies of market share of brands in final markets | Qualitative |

4. Research Methodology

5. Analysis of Results

5.1. Governance Relationships among the Analyzed Actors: Qualitative Results

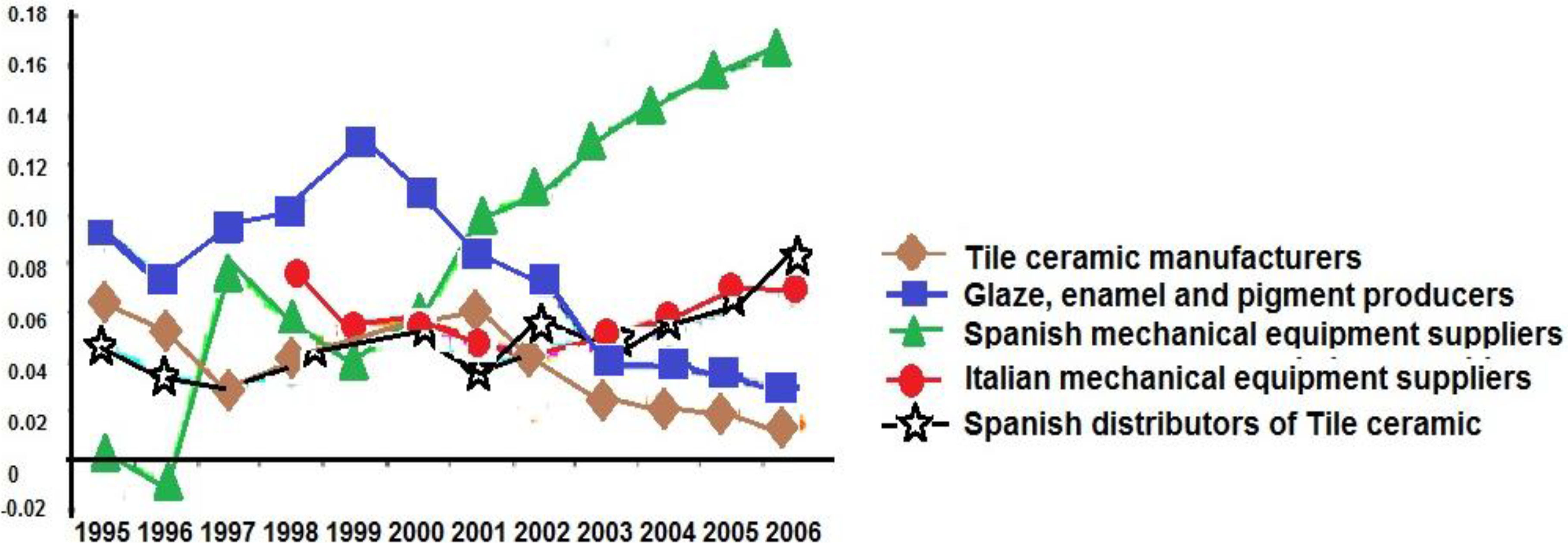

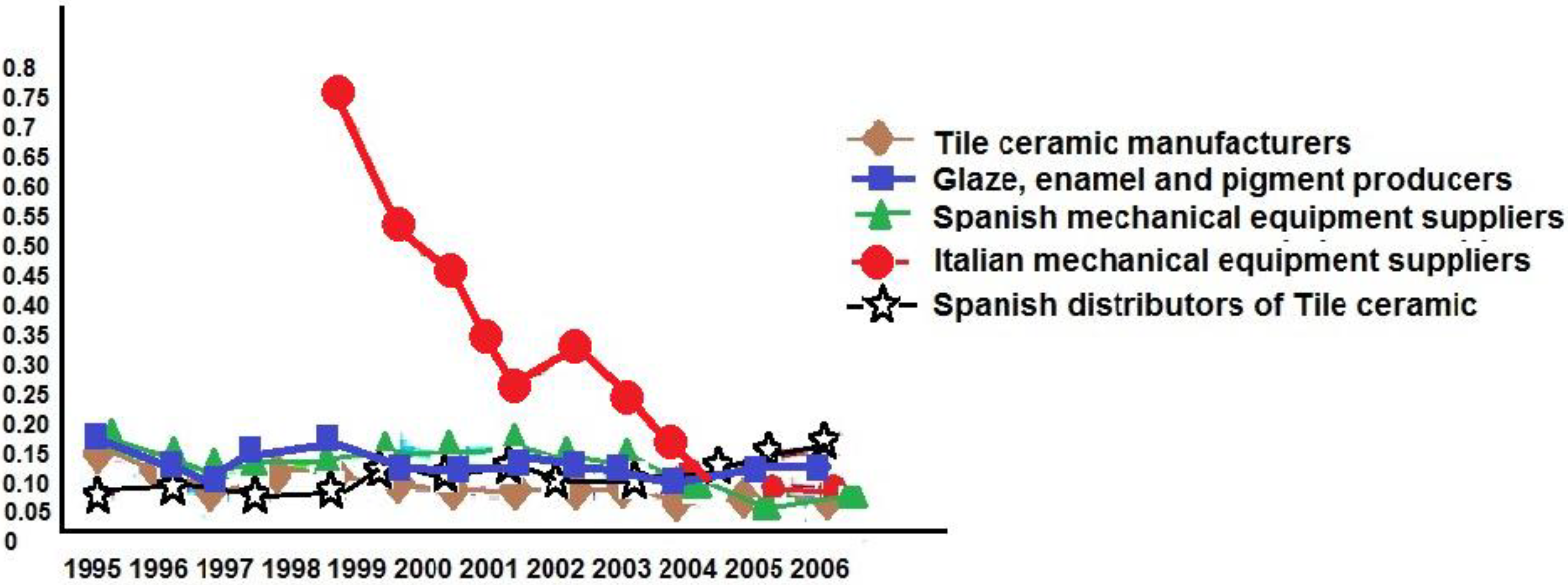

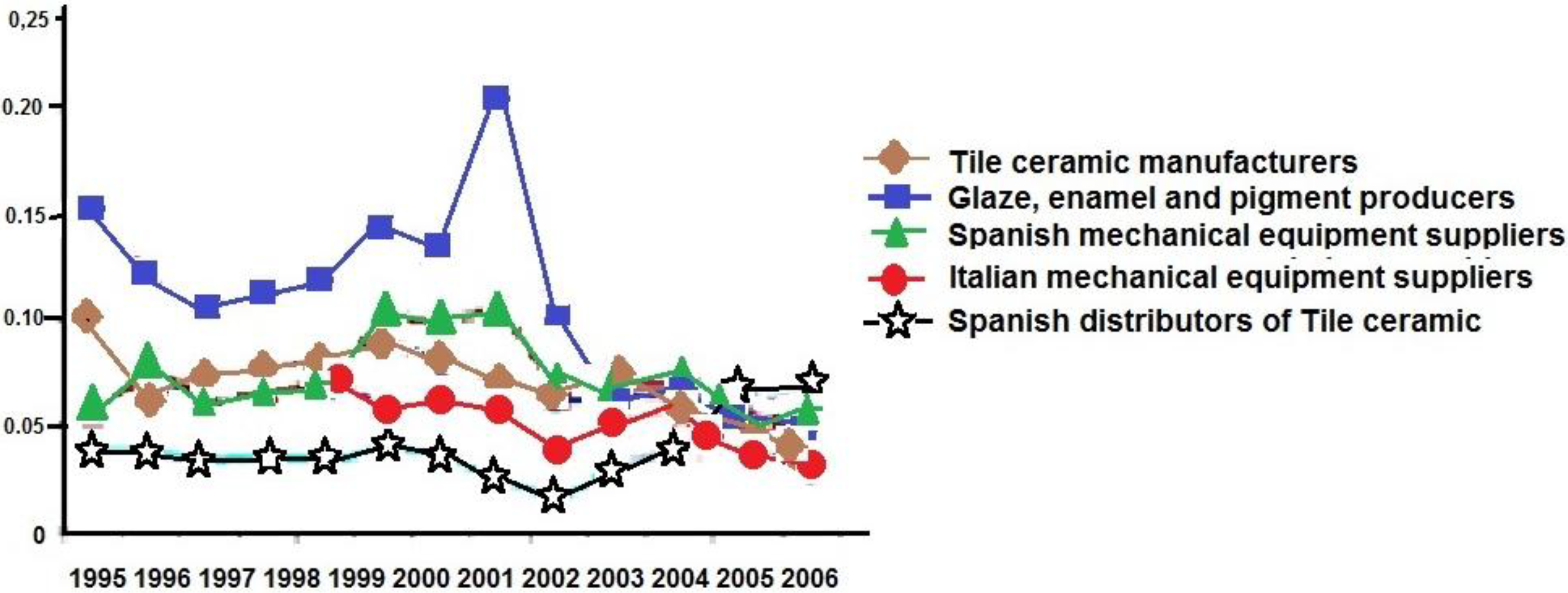

5.2. Governance Relationships among the Analyzed actors: Quantitative Results

| Ratio | Abbreviation |

|---|---|

| Return on Assets | ROA |

| Earnings before interest, taxes, depreciation and amortization (EBITDA) on sales | EBITDA |

| Operating profit on assets | OPA |

6. Conclusions

Author Contributions

Conflicts of interest

References

- Porter, M.E. Clusters and the New Economics of Competition. Harv. Bus. Rev. 1998, 76, 77–90. [Google Scholar]

- OECD. National Innovation Sysstems. Organization for Economic Development: Paris, France, 1997. [Google Scholar]

- Freeman, C. Technology and Economic Performance: Lessons from Japan; Pinter: London, 1987. [Google Scholar]

- Cooke, P.; Gomez-Uranga, M.; Etxebarria, G. Regional innovation systems: Institutional and organisational dimensions. Res. Policy. 1997, 26, 475–491. [Google Scholar] [CrossRef]

- Camagni, R. Towards a Concept of Territorial Capital. In Modelling Regional Scenarios for the Enlarged Europe; Capello, R., Camagni, R., Chizzolini, B., Fratesi, U., Eds.; Springer: Berlin, Germany, 2008. [Google Scholar]

- Johannisson, B.; Ramírez-Pasillas, M.; Karlsson, G. The institucional embeddedness of local inter-firm networks: A leverage for business creation. Entrep. Reg. Dev. 2002, 14, 297–315. [Google Scholar] [CrossRef]

- Schumpeter, J. The Theory of Economic Development: An Inquiry into Profits, Capital, Credit, Interest and the Business Cycle; Harvard University Press: Cambridge, MA, USA, 1911; (1934 translation, Cambridge). [Google Scholar]

- Patel, P.; Pavitt, K. The Nature and Economic Importance of National Innovation System. Sci. Technol. Ind. Rev. 1994, 14, 125–138. [Google Scholar]

- Freeman, C. The Economics of Industrial Innovation; Penguin Books, Ltd.: London, UK, 1974; pp. 197–198. [Google Scholar]

- Freeman, C. Innovation and growth. In The Handbook of Industrial Innovation; Dogson, M., Rothwell, R., Eds.; Edward Elgar: Aldershot, UK, 1994. [Google Scholar]

- Albors, J. Study and diagnosis on the industry of machinery for the ceramic tile industry. In Técnica Cerámica; Anual Report: Barcelona, Spain, 2000. (In Spanish) [Google Scholar]

- Albors, J. Networking and technology transfer in the Spanish ceramic tiles cluster: Its role in the sector competitiveness. J. Technol. Transf. 2002, 27, 263–273. [Google Scholar]

- Hervas-Oliver, J.L.; Albors-Garigos, J.; Dalmau Porta, J.I. External ties and the reduction of knowledge asymmetries among clusters within global value chains: The case of the ceramic tile district of Castellon. Eur. Plan. Stud. 2008, 16, 507–520. [Google Scholar] [CrossRef]

- Pavitt, K. Sectoral patterns of technical change: Towards a taxonomy and a theory. Res. Policy. 1984, 13, 343–373. [Google Scholar] [CrossRef]

- Albors-Garrigos, J.; Hervas-Oliver, J.L. Adoption of Contingent Technology Production Strategies in Mature Industries: An Empirical Study. In Proceedings of the IBIMA Conference, Marraketch, 11 November 2009.

- Ascer. Asociación Española de Fabricantes de Azulejos y Pavimentos Cerámicos. Available online: http://www.ASCER.es (accessed on 15 November 2013).

- Infotile. International online directory of ceramic tile, stone and allied products and manufacturers. Available online: http://www.Infotile.com (accessed on 20 October 2013).

- Albors-Garrigos, J.; Hervas-Oliver, J.L. The European tile ceramic industry in the XXI century. Challenges of the present decade. Bol. Soc. Esp. Cer. Vidrio 2006, 45, 13–21. [Google Scholar]

- Belussi, F.; de Propis, L. They are industrial districts, but not as we know them! In Handbook of Industry Studies and Economic Geography; Belussi, F., de Propris, L., Eds.; Edward Elgar: Chentelham, UK, 2014. [Google Scholar]

- Porter, M.E. Competitive Advantage: Creating and Sustaining Superior Performance. The Free Press: New York, NY, USA, 1985. [Google Scholar]

- Manual for Value Chain on Homeworkers in the Garment Industry. Available online: https://www.ids.ac.uk/idspublication/manual-for-value-chain-research-on-homeworkers-in-the-garment-industry (accessed on 17 June 2014).

- Humphrey, J.; Schmitz, H. Governance in global value chains. IDS Bulletin 2001, 32, 19–29. [Google Scholar] [CrossRef]

- Gereffi, G. A commodity chains framework for analysing global industries, in Institute of Development Studies, 1999, Background Notes for Workshop on Spreading the Gains from Globalisation. Available online: http://www.ids.ac.uk/ids/global/conf/wkscf.html (accessed on 21 October 2013).

- Kaplinsky, R.; Morris, M. A Handbook for Value Chain Research; International Development Research Centre (IRDC): Ottawa, Canada, 2001. [Google Scholar]

- Kaplinsky, R.; Readman, J. Integrating SMEs in Global Value Chains: Towards Partnership for Development; UNIDO: Vienna, Austria, 2001. [Google Scholar]

- Schmith, H. Does Local Co-operation Matter? Evidence from Industrial Clusters in South Asia and Latin America. Oxf. Dev. Stud. 2000, 28, 323–336. [Google Scholar] [CrossRef]

- Albors, J.; Marquez, P.B. Relationships manufacturer distributor as key competitive elements in the case of the spanish ceramic tile cluster. Empirical analysis of the moderating factors. Bol. Soc. Esp. Ceram. V 2008, 47, 339–344. [Google Scholar] [CrossRef]

- Meyer-Stamer, J.; Maggi, C.; Seibel, S. Improving upon Nature. Creating Competitive Advantage in Ceramic Tile Clusters in Italy, Spain, and Brazil; INEF Report 54; Institut für Entwicklung und Frieden: Duisburg, Germany, 2001. [Google Scholar]

- Foster, R. Innovation. In The Attackers Advantage; Mckinsey: New York, NY, USA, 1986. [Google Scholar]

- Albors-Garrigos, J.; Hervas-Oliver, J.L. Disruptive Technology in Mature Industries: Its Contribution to Industry Sustainability. In Proceedings of the PICMET’13: Technology Management in the IT-Driven Services (PICMET), San Jose, CA, USA, 28 July 2013–1 August 2013; pp. 585–596.

- EPO. European Patent Office. Available online: http://www.epo.org/searching/free/espacenet.html (accessed on 22 October 2013).

© 2014 by the authors; licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution license (http://creativecommons.org/licenses/by/3.0/).

Share and Cite

Albors-Garrigos, J.; De Miguel Molina, B.; De Miguel Molina, M. Positioning in the Global Value Chain as a Sustainable Strategy: A Case Study in a Mature Industry. Adm. Sci. 2014, 4, 155-172. https://doi.org/10.3390/admsci4020155

Albors-Garrigos J, De Miguel Molina B, De Miguel Molina M. Positioning in the Global Value Chain as a Sustainable Strategy: A Case Study in a Mature Industry. Administrative Sciences. 2014; 4(2):155-172. https://doi.org/10.3390/admsci4020155

Chicago/Turabian StyleAlbors-Garrigos, Jose, Blanca De Miguel Molina, and Maria De Miguel Molina. 2014. "Positioning in the Global Value Chain as a Sustainable Strategy: A Case Study in a Mature Industry" Administrative Sciences 4, no. 2: 155-172. https://doi.org/10.3390/admsci4020155

APA StyleAlbors-Garrigos, J., De Miguel Molina, B., & De Miguel Molina, M. (2014). Positioning in the Global Value Chain as a Sustainable Strategy: A Case Study in a Mature Industry. Administrative Sciences, 4(2), 155-172. https://doi.org/10.3390/admsci4020155