Internationalization and Performance of Vietnamese Manufacturing Firms: Does Organizational Slack Matter?

School of Business, International University-Vietnam National University, Ho Chi Minh City 700000, Vietnam

*

Author to whom correspondence should be addressed.

Adm. Sci. 2018, 8(4), 64; https://doi.org/10.3390/admsci8040064

Submission received: 1 October 2018

/

Revised: 18 October 2018

/

Accepted: 22 October 2018

/

Published: 25 October 2018

Abstract

:This paper aims to investigate the three-stage theory of international expansion in the long run from the perspective of firm behavior. Although this topic has been mostly explored using data from developed countries, this paper aims to fill the research gap in an emerging market by using an extensive unbalanced panel data of 12,704 unlisted Vietnam manufacturing enterprises from the General Statistics Office during 2007 to 2012. The findings illustrated a significant S-shaped relationship between internationalization and performance. Notably, the results depict significantly moderating effects of both high-discretion slacks and low-discretion slacks on the internationalization–performance relationship across three stages of global expansion as an enterprise enhances this relationship in the first and third stage although this worsens it in the middle stage. The empirical results suggest that firms should determine the optimum level of internationalization and slacks in addition to balancing their costs with their real gains.

1. Introduction

The world has witnessed a spectacular change in which firms from developing countries have played an essential role in the global market (Chittoor 2009). In order to obtain access to new markets and maintain long-term profitability, firms have been motivated to implement a global expansion strategy. However, local firms are also confronted with the costs of the internationalization process, such as barriers to entry, high transaction cost, market volatility, and cultural diversity (Marano et al. 2016; Tsai 2014). Besides, small and medium enterprises, in comparison with larger firms, experience several disadvantages in terms of strategic resources and internal capabilities to ensure success in the internationalization process. In the research field, the findings on whether the increasing internationalization intensity will improve firm performance are very controversial and even raise more questions than answers. The differences among the empirical results of studies on the internationalization–performance relationship have been illustrated in several meta-analyses, which have found positive and negative linear relationships as well as combinations of linear relationships, such as U-shaped, inverted U-shaped, and S-shaped (Cardinal et al. 2011; Marano et al. 2016).

As an internalization strategy requires funds to launch and sustain implementation, the concept of organizational slacks has been created, which refers to the availability of financial resources used for implementing internal and external changes (Bourgeois 1981). Once the firms possess a high level of organizational slacks, they are more willing to invest in new chances, handle uncertainties, and sustain their competitiveness (Lin and Liu 2012; Lin et al. 2011; Tan 2003; Joensuu-Salo et al. 2018). However, Tan (2003) also considers slack as “inefficiency” as it has high opportunity costs and forces a company to break its formal discipline to pursue high-variance profits.

In addition, the issue is mostly supported by data from the developed world rather than emerging economies (Chittoor 2009). In recent years, the Vietnamese government has consistently updated policy and amended laws with respect to international practices to create more favorable conditions for newly Vietnamese internationalized firms (IFs) to go global and attract inward foreign capital. Besides, Vietnamese enterprises are also constantly changing their business strategies and practices to be in line with their international integration in a global competitive environment. However, there are still only a limited number of studies that have focused on the internationalization performance of Vietnamese enterprises. Therefore, from the perspective of firm behavior, this study aims to explore the global expansion–performance relationship and how the availability of organizational slacks influences this relationship in the context of an emerging economy, such as in Vietnam.

The paper is continued by investigating the relevant literature on the relationship between internationalization and firm performance, the importance of slack resources, and empirical evidences for these relationships. Then, we discuss the methodology such as data, model estimation, and variable measures employed to address the research questions. We next report the empirical results for model estimation. Finally, the paper ends with the conclusion, overall discussions, recommendations, and limitations.

2. Literature Review

2.1. Theoretical Review

2.1.1. Concept of Internationalization

Internationalization is defined as a multistage process in which the firms make the incremental efforts to strengthen their market involvement and gradually obtain commitments from foreign consumers (Johanson and Vahlne 1977). There are two incremental channels for the internationalization process of the firms (Contractor et al. 2003; Johanson and Vahlne 1977; Westhead et al. 2001). The first channel involves internationalization enabling the products and services of the firms to penetrate foreign markets by starting to export to an individual foreign country or establish export channels. The second channel involves new internationalized firms (Ifs) that are beginning to expand their operations abroad, such as developing sale subsidiaries and outsourcing their production to the favorable locations in the host countries (Westhead et al. 2001). However, export activities are the main focus of most IFs from developing countries to address the problem of an insufficient domestic market because they offer the best option to develop the market nature and size with the smallest associated cost (Contractor et al. 2003; Hutchinson et al. 2007).

Regardless of which internationalization strategies that the firms choose to implement, it is widely accepted that they always start with developing the market knowledge and exploration (Contractor et al. 2003). After this, the firms will make decisions about whether they should export or not. It is undeniable that an increase in market knowledge will not only stimulate or discourage firms’ decisions to internationalize but also is the key in determining the success of almost all IFs once they decide to participate in the global market (Chen and Hsu 2010). Indeed, the internationalization process is often implemented incrementally along with the increasing market knowledge. By learning the characteristics, tastes, and cultures as well as attaining useful information about the aimed foreign markets, the firm can enable their products and services to meet a wide range of standardized requirements and accumulate international experiences for further expansions (Oeconomica 2014).

2.1.2. The Degree of Internationalization and Firm Performance

The question of whether the higher degree of internationalization will lead to a higher level of firm performance is still a very controversial issue. This research field has even generated more questions than answers after many decades of studies (Glaum and Oesterle 2007). Notably, determining the mechanisms behind how the IFs gradually get involved in the global market is very attractive for the international business community. The previous empirical studies have created a fundamental springboard for further studies with many established theoretical frameworks. There are people on both sides who have arguments either for or against the impact of internationalization.

Internationalization is considered to be an auspicious driver for expanding the growth of firms and enhancing their competitive advantage (Hutchinson et al. 2007). Moreover, firms are more likely to internationalize under the circumstances of an insufficient domestic market. The global integration process can help them to expand their market size without the need for costly expenditures. It also results in many advantages, such as economies of scale, the applicable practice of price discrimination strategy, and access to cheaper resources (Contractor et al. 2003; Lin et al. 2009, 2011). On the other hand, many people argue that internationalization triggers negative impacts on firm performance. There are many disadvantages that the IFs must face once becoming global, such as fierce competition, high transaction costs, market volatility, and cultural diversity (Eriksson et al. 2014). Up to this point, it is argued that the market size of IFs may double, triple, or even grow exponentially. However, the increasing number of worldwide competitors as well as an extensive range of adjusted standards and restrictions may trigger a real burden rather than a good chance for IFs in the short-term (Bobillo et al. 2010).

Providing a more comprehensive view, Contractor et al. (2003) fully described the internationalization process with a new three-stage theory of internationalization, including three separating stages with different impacts on performance.

The first stage occurs when the new internationalized firm starts to experience the familiar foreign markets by exploring their specific characteristics, such as cultures, languages, habits, tastes, etc., before exporting their products and services to those markets. It is undeniable that during this stage, the firms are confronted with many legal and market barriers as well as payments for learning costs to obtain entry and market information (Eriksson et al. 2014; Johanson and Vahlne 1977). These costs are known as “the liability of foreignness” (Contractor et al. 2003). Moreover, it seems to be very risky for firms due to the high level of uncertainties and insufficient economies of scale at this initial stage (Westhead et al. 2001). However, Johanson and Vahlne (1977) emphasized that firms are willing to spend their budget in this stage to acquire market knowledge and international experience in order to integrate and successfully increase foreign commitments. Therefore, at the early stage, internationalization may negatively affect firm performance. Nevertheless, this effect may vary among firms depending on financial capacity, human capital, management know-how, and the flexibility of each enterprise when joining in the global market (Chen et al. 2016; Chiao et al. 2006; Dutta et al. 2016).

In the second stage or the mid-stage, it is believed that IFs will obtain initial gains from the internationalization process. Once the IFs successfully move to the second stage, they gradually absorb the increasing gains from global expansion. The learning cost is now offset by greater revenues. At the mid-stage, they now obtain adequate market knowledge and know how to implement their exporting strategies more efficiently. Up to this point, most of the firms reach the economies of scale and can apply a price discrimination strategy to different markets (Hutchinson et al. 2007). After initial success, the firms will be more ambitious to move to further steps of internationalization process. Commonly, they expand their operation abroad at an accelerated rate because they now have access to cheaper local resources such as material inputs and labor (Chittoor 2009; Singla and George 2013; Zhou 2018). It is obvious that internationalization offers a good chance to seek new potential markets and expand growth. Thus, in stage 2, internationalization is believed to lead to higher firm performance.

In the third stage or “beyond an optimal threshold” stage, it is supposed that not all expansion at this stage is beneficial because the firms may lose their control over a too-broad system over many countries and regions. This may impose a cost burden on firms rather than providing a new opportunity (Hutchinson et al. 2007; Lu and Beamish 2006). Once the firms reach the optimal level of internationalization process, any more international expansion appears to not be efficient in terms of opportunity cost. It is undeniable that the firms in the previous stages aimed to expand to the profitably familiar markets with the convenient conditions of geographical distance, customers’ tastes and resources (García-García et al. 2017). Dutta et al. (2016) believe that the more the markets diversifies, the more international involvement the firms can achieve while Assaf et al. (2012) argues that the governance and transaction costs become too high along with the market diversification. Moreover, the firms are forced to pay for timely information as a good way to sustain their competition in different foreign markets. In addition, the operation in many countries with diversified cultures is a costly and complex process. Therefore, in stage 3, the firm performance is assumed to be diminished when international expansion goes beyond the optimal level.

Based on the mentioned theories, a domestic firm can decide to internalize because this process may bring them many significant advantages and especially help them to overcome the insufficient local market. Being global is the best way to sustain the growth of a firm and enhance performance at lower costs in the long run. However, these benefits may be overwhelmed by a wide range of barriers and costs, such as learning costs, transaction, and governance costs, as the internationalization degree becomes higher and higher. Thus, the first hypothesis is provided below.

Hypothesis 1.

Internationalization has an S-shaped relationship with Vietnam manufacturing firms’ performance.

An S-shaped relationship means that the performance decreases in the early stage, increases until the optimal point, and declines in the later stage under the incremental degree of internationalization process.

2.1.3. Organizational Slacks

The slack resource is defined as a strategic tool that is used to deal with the firms’ uncertainties (Bourgeois 1981). Besides, the antecedents of organizational slacks have highlighted that the slacks originate from the surplus of financial resources out of the needed amount of resources to produce a given output (Bourgeois 2016). Bourgeois (1981) also emphasized that actual or potential resources are considered as slacks when they are intended to relieve internal and external pressures during the firm’s operations. This concept is very operational because it not only indicates the objective of slack expenditures but also illustrates how they are allocated among the organization resources. Specifically, slacks can be used to adapt to sudden change in the internal or external environment, such as meeting urgent situations or investing in new opportunities and challenges, including expanding to a new market.

Bourgeois (1981) discussed the four key roles of slacks thoughtfully as the best way to explain why he considered organizational slacks to be a miracle for successfully initiating and contributing to the internationalization process and firm performance. The slacks are firstly considered as a buffer to experiment the potential alternatives and effectively motivate the labor force within the organization, such as providing income and bonuses to retain and encourage the organizational actors’ contributions (Lin et al. 2011). Secondly, the slacks serve is considered to be an effective tool for dealing with a firm’s contradictions. For instance, the sufficient slacks help organizations to facilitate the making-decision process by offering more choices to reach the common goal. Thirdly, Bourgeois (1981) also mentioned that the firms with abundant slacks have more capacity and incentives to conduct Research and Development (R&D) activities in addition to investing in the updated techniques and technology towards sustaining a competitive advantage. Finally, from the perspective of external changes, organizational slacks act as the facilitators to turn strategic plans into reality (Brida et al. 2016; Yoon et al. 2018).

It is unquestionable that this surplus amount allows firms to implement the external strategic changes, such as launching new products, starting new ventures, entering new markets, and providing funds for innovations. Based on their flexibility for use and where they come from, organizational slacks are divided into two types, which are namely the high-discretion slack and low-discretion slack (Daniel et al. 2004).

The high-discretion slack represents the financial resources, which are quite liquid, such as cash and receivables; a higher level of high-discretion slack means that a firm can provide a greater level of flexibility to cash flow with rapid liquidity. It is worth noting that the higher level of high-discretion slack will provide available resources to enable top managers to internalize. Besides, it provides a good fund to deal with uncertainties and obtain market knowledge during the internationalization process. Therefore, we have created the second hypothesis as below.

Hypothesis 2.

Higher level of high discretion slack enhances the relationship between internationalization and performance.

A low-discretion slack implies more nonliquid resources, such as debt and unused fixed assets. A higher level of low-discretion slack means that the firm has more potential slacks and greater borrowing power to have access to funds from the financial market. Similar to high-discretion slacks, a higher level of low-discretion slacks is also a good signal for firms to internalize. Hence, the third hypothesis is described as below.

Hypothesis 3.

Higher level of low discretion slack enhances the relationship between internationalization and performance.

2.2. Empirical Review

The studies on global expansion have used various methodologies, variables, measurements, and have found the controversial results. Furthermore, they mainly focus on the common questions whether internationalization stimulates or discourages the performances of IFs. However, this appears to raise even more questions because these studies did not take account into the existence of moderating effects which can have both direct and indirect influences on DOI and firm performance.

Recently, several studies have used various moderating factors as an effective tool to fully investigate this relationship from different perspectives. For instance, they have investigated internal and external competitive advantages (Bobillo et al. 2010), organizational slacks, and attainment discrepancy from the perspective of firm behavior (Lin et al. 2011).

Bobillo et al. (2010) found an S-shaped relationship between the international diversification and firm performance under the moderating effects of internal and external capabilities. The Worldscope database provides more than 1500 manufacturing firms’ financial statements from 1991 to 2001 in five various EU countries to form a panel data of more than 15,000 observations. DOI (measured as the ratio of foreign sale to total sale) and other control variables, such as size (measured by the taking the logarithm of total employees), and ownership (measured by insiders’ shareholdings) were added in the regression model. Moreover, the study attempted to capture the effects of internationalization on performance across three different stages using the following quadratic and cubic regression models.

ROAit = β0 + β1DOIit + β2DOIit2 + β3DOIit3 + β4SIZEit + β5OWNERSHIPit + ηi + εit

In their conclusion, Bobillo et al. (2010) found that firm performance varies in different directions as the internationalization degree moves upward. The initially negative impact on performance may be caused by higher transaction costs, greater burden from more complicated governance structure, as well as the urgent demand to adopt market knowledge and technology. However, the downward or upward trends of performance toward DOI also depend on internal and external factors at both the firm level and country level. In the implications, they believed that the firm could only succeed in their internationalization strategy once they are able to take advantage of their capabilities, which are in favor of the country’s institutional factors, such as the financial system and labor market.

Pangarkar (2008) measured the effects of degree of internationalization on the performance of listed SMEs in Singapore in 2004 using the OLS method. He used the lagged value of the internationalization degree in 2013 as a predictor to explain the firm performance that was determined in 2004. The degree of internationalization is primarily determined by the sale expansion over the foreign market, which is measured as the ratio of the foreign sale to total sale. The sample included 94 completed questionnaires that followed the Likert scale and was obtained in the mid-2005. The control variables, such as firm size, capabilities, and host market attractiveness, are added to the regression equation as follows

PERFORMANCEt = β0 + β1DOIi,t−1 + β2SIZEit + β3CAPABILITIES + β4HOST_MARKET_ATTRACTIVENESS + εit

Finally, he found a positive linear relationship between DOI and firm performance. The study also discovered that Singapore firms have more incentives to get involved in international markets due to insufficient local markets. However, the problem is how they can cooperate with each other to conquer their common barriers and develop their capabilities (Pangarkar 2008).

From the perspective of firm behavior, Lin et al. (2011) conducted the fixed effect analysis on the sample of 179 high-tech listed firms in Taiwan for the period of 2000 to 2005. They primarily focused on the moderating effects of organizational slacks and attainment discrepancy. Furthermore, they added firm size, firm age, insider shareholding, diversifications, and R&D intensity as the control variables.

Firm performance = β0 + β1Internationalization + β2firm_size + β3firm_age + β4Insider_Shareholding + β5Diversification + β6R&D_ratio + β7High_discretion_slack + β8Low_discretion_slack + β9Attainment_discrepancy + β10High_discretion_slack × Internationalization + β11Low_discretion_slack × Internationalization + ε

Furthermore, they found that internationalization negatively affects the firm performance while a significant S-shaped relationship was not found. More importantly, the effect of internationalization on performance is enhanced for the firms with a higher level of both types of organizational slacks.

Positioning slacks as a strategic resource for internationalization process, Tan (2003) conducted the empirical studies on the longitudinal data set of more than 17,000 large and medium state-owned enterprises in China from 1995 to 1996 to investigate the contribution of slacks on IF’s performance. In order to test the causal relationship between slack and internationalization performance, he applied the lagged model in which lagged ROA is used as predictor. By reviewing many previous researches on how to classify the types of slacks depending on the research purposes, capital depreciation funds and retained earnings were selected to reflex two major sources of slacks among Chinese internationalizing firms. The performance was measured by ROA, which is also the performance proxy in the study of Lin et al. (2011). Besides, firm size and firm age were also added as control variables. Finally, he found that firm performance is improved by higher level slacks. In order to explain for this, he discussed that once IFs possess abundant slacks, they are more willing to invest on higher-risk markets which are expected to bring higher returns. Moreover, by higher level of slack resources, they also have more capability to manage the risks and maintain their competitiveness in the long-run survival.

To further complicate the issue, Daniel et al. (2004) conducted the meta-analysis on 80 samples from 66 studies from 1991 to 2000. From these previous empirical studies, slacks were differently classified, but the most common classification of slacks includes available, recoverable, and potential slacks. In addition, there are many controversies on whether we should consider slacks as a resource—a positive impact on performance or inefficiency of resource allocation and a negative impact on performance (Glaum and Oesterle 2007). The recent finding is that different types of slacks have various impacts on performance. By calculating the mean correlation and variance of the combined studies, Daniel et al. (2004) used them for testing the relationship between slack and internationalization performance. In their findings, Daniel et al. (2004) emphasized the contribution of organizational slacks on firm performance by dealing with both internal and external obstacles.

Lin et al. (2011) attempted to discover the moderating role of organizational slacks on a firm’s internationalization performance. Under the perspective of firm behavior, the research defined slack resources based on the flexibility for use and used the financial indicators to estimate. The proxies for these two types of slacks—high-discretion slack and low-discretion slack are calculated as current assets to current liabilities ratio and equity to debt ratio, respectively. This work appeared to be the extended work of their study in 2009 when they had already researched how organizational slacks affect the degree of internationalization for the same sample and the same defined types of organizational slacks. Using the general linear squares (GLS) random-effect model, Lin et al. (2009) found a U-shaped relationship between high-discretion slack and DOI while low-discretion slacks play as a facilitator for firms to internalize all of the time. However, Lin et al. (2011) not only considered organizational slacks as their direct contributions to firm performance or DOI, but also their moderating effect on enhancing the relationship between internationalization degree and firm performance. Also, a wide range of control variables were added to the model such as firm size, firm age, insider shareholding, degree of diversification, and R&D intensity.

The finding reinforced for the theory of Bourgeois (1981) that the abundant resources of slacks in both kinds of high-discretion and low-discretion will encourage the top management to launch new chances, specifically to enter new foreign markets. Moreover, the organizational slack is also one of important sources of the performance improvement due to its capability to support the firm overcome the bad times as well as the uncertainties during international expansion process.

3. Methodology

3.1. Data

The study uses the panel data of 12,704 Vietnamese manufacturing enterprises surveyed by the General Statistics Office from 2007 to 2012. This survey has been conducted each year to collect the data from all existing firms and agencies. After filtering all missing information and outliers, we formed an unbalanced panel data of 58,332 observations used for data analysis. The observations of unlisted firms provide adequate cross-sectional data from various industries, including food processing, textiles & garments, stationery, construction materials, high-tech, water, and electricity supply. The investigated enterprise data in 2011 and 2012 recorded each indicator twice per year; once at the beginning of the year (1/1) and another at the end of the year (31/12). In this case, the study used the last indicators (31/12) for estimations. Moreover, the data for export volume was not available during the period of 2007 to 2010, so it is relatively estimated by dividing the export-tax expenses for export tax.

Moreover, the study only uses the data of the Vietnam manufacturing firms as the initial research objective. Thus, the 100% foreign-invested companies and cooperatives (lhdn = 12 and lhdn = 6, respectively) were excluded from the testing model. In addition, in order to obtain the sample from the whole population, the appropriate Vietnamese manufacturing firms were filtered carefully. The manufacturing firms with the “nganh_kd” or 2-digit industry code from 10* to 33* are kept for the testing model. Then, the filtered data is removed for detected duplicates based on id (madn + macs + nganh_kd + year) and year basis. The outliers are also eliminated to improve the reliability of the coefficients. The panel data is initially balanced in term of id and years. However, after removing duplicates and eliminating outliers, the processed data becomes unbalanced in term of year.

3.2. Model Estimation

The sample was drawn from the population of more than 300,000 Vietnamese firms each year. Then, the repeated manufacturing firms were filtered and appended to form a panel data for a six-year period from 2007 to 2012. Stoker et al. (2005) described that panel data contains the cross-sectional indicators of the same individual or entity, such as country, region, firm, consumer, etc., which are observed repeatedly over time. The panel data may be balanced—each repeated individual or entity has the same periods of time—or unbalanced, each repeated individual or entity has different periods of time.

In their analysis Greene (2003) pointed out several reasons to explain why the panel data (longitudinal data) is popularly chosen for the testing model and suggested several methods of panel model estimation. Firstly, the panel data allows the researchers to observe the firms’ behaviors and trends across years. Secondly, by combining the time-series with cross-sectional observations, panel data contains more useful information and more variability to eliminate the collinearity between variables; at the same time generates many degrees of freedom and enhances the reliability of estimation. Thirdly, by studying the repeated cross-sectional firm observations, the panel data is more appropriate to see how firms’ cross-sectional indicators vary year by year. Finally, panel data can discover and measure effectively the unobserved impacts that cross-sectional or time-series data cannot.

In order to test the three main hypotheses, the study conducted the two most popular models for testing panel data including fixed effect model and random effect model. In addition, the quadratic and cubic forms of DOI are added to capture the curvilinear effect of DOI on performance across three different phases as the first hypothesis (Lin and Liu 2012; Lin et al. 2009, 2011). Since there is the indication and strong evidences of a curvilinear relationship between DOI and performance from both the theory (Contractor et al. 2003) and the previous empirical studies (Bobillo et al. 2010; Contractor et al. 2007; Lin et al. 2011; Tsai 2014), it is assumed that a linear relationship between internationalization and firm performance cannot fully explained in the case of Vietnam’s IFs. Furthermore, the study aims to test the S-shaped theory of (Contractor et al. 2003). Therefore, it is quite reasonable to include both the quadratic and cubic form of DOI to satisfy those concerns.

Equations for linear and curvilinear relationships:

| Y’ = a + b1X1 | Linear (Straight line) |

| Y’ = a + b1X1 + b2X12 | Quadratic (U-shaped) |

| Y’ = a + b1X1 + b2X12+ b3 X13 | Cubic (S-shaped) |

Furthermore, the study primarily focuses on investigating the moderating effect of high-discretion slack and low discretion slack on the relationship between internationalization and performance. In other words, a third variable (Z) representing firm-specific advantages, such as slacks, is considered as a moderating variable as it simultaneously has relevant relationships with both the dependent variable (firm performance) and an explanatory variable (internationalization) (Chiao et al. 2006). More important, as Z can affect the effect of X on Y, an improving or discouraging effect of X on Y is dependent on the level of Z.

In this way, the most two common models estimating panel data are considered (Lin et al. 2011). Fixed effect model assumes that there are the possible correlations between time-invariant differences across entities and the explanatory variables. According to Greene (2003) and Stoker et al. (2005), fixed effect model (FEM) can control and separate the effects of these differences from the predictors to help us estimate the net effects on the explanatory variables on dependent variable. However, FEM also reveals the limitation as it cannot measure time-invariant factors, such as gender, race, etc., as it absorbs the dummies variables on the intercept. Another limitation is that there are many variables generated in the model which may lead to lower degree of freedom and higher possibility of multicollinearity in the model. On the other hand, the random effect model assumes random variations across entities and that there is no correlation between these variations and the explanatory variables. The random effect model, in contrast to the FEM, can measure the influence of unchanged-over-time variables; however, it fails to control the bias of omitted variables. Since we have detected there is the existence of omitted variables, so the fixed effect model is the best choice to control for this bias.

Nevertheless, the Hausman test is also reported to ensure whether the fixed effect model or random effect model is more appropriate. The Hausman test raises the null hypothesis that the estimations of the fixed effect model and random effect model are indifferent. Because p-value is less than 0.05, the null hypothesis is rejected and a FEM is recommended for testing the Vietnamese enterprise panel data from 2007 to 2012. Besides, the OLS model is also tested and followed by a series tests VIF test for multicollinearity, Ramsey RESET test for omitted variables, White’s test for heteroskedasticity, and Wooldridge test for autocorrelation. Then, any problem found is corrected immediately to improve the reliability of the regression coefficients.

3.3. Regression Equation

The study applies the fixed effect model to analyze the data set according to the suggestions of the Hausman test. Series tests of omitted variables, multicollinearity and heteroskedasticity are also applied to eliminate bias estimations.

ROAit = β0 + β1INTit + β2INTit2 + β2INTit3 + β4HSit + β5LSit + β6INTit × HSit + β7INTit × LSit + β8INTit2 × HSit + β9INTit2 × LSit + β10INTit3 × HSit + β11INTit3 × LSit + β12firm_sizeit + β13privatet + β14sharet + β15industry_riskt + εit + µi

3.4. Variable Measures

3.4.1. Dependent Variables

The firm performance is measured by return on assets (ROA), which is a very popular proxy for performance in many empirical studies (Lin et al. 2011). Although it is a single measure, Chen et al. (2016) emphasized that ROA is a very appropriate indicator to show the efficiency of the internationalization strategy and contributes to the economies of scope and scale.

3.4.2. Independent Variables

Internationalization (INT) is measured by the ratio of foreign sales to total sales in many previous empirical studies (Bobillo et al. 2010; Tsai 2014). Besides, the quadratic and cubic form of internationalization [INT2 and INT3] are calculated to absorb the degree of internationalization in the second and third stage when the internationalization process incrementally expands in terms of scale and revenues (Marano et al. 2016).

3.4.3. Moderating Variables

Lin et al. (2011) measured the high-discretion slack (HS) as the ratio of current assets to current liabilities and low-discretion slacks (LS) as the equity to debt ratio. This study adopts these proxies to estimate the moderating effects. They are available in the dataset and also reflect the idle firm resources, which are different from the necessary operation resources (Lin and Liu 2012).

3.4.4. Control Variables

Firm size is considered to be a common indicator, which is significantly associated with firm performance. The logarithm of sales is widely used as the measure for firm size because it reflects the level of the firm’s inputs and capability (Chen et al. 2016; Tsai 2014). Lin et al. (2011) found a significant impact of ownership identity on firm performance. Thus, three common ownership identities of joint stock (share), private, and state enterprises will serve as the control dummy variables added to the model. Moreover, the industrial risk is added and measured by the residual revenue of firms (Marano et al. 2016).

4. Empirical Results

Table 1 illustrates the descriptive statistic numbers of the variables, such as the mean, standard deviation, and the correlation between variables. Table 1 also shows the significant correlations between all variables. Specifically, the degree of internationalization at three levels (DOI, DOI2, and DOI3) was found to be negatively correlated with firm performance at −0.0514, −0.0534, and −0.0519, respectively. Besides, the high-discretion slack was found to be negatively correlated with firm performance (β = −0.1575) at a level of confidence of 95%, while low discretion slack was positively correlated with performance at p-value < 0.1. The largest positive correlation coefficients obviously belong to the two pairs of DOI & DOI_highslack and DOI & DOI_lowslack as their moderating components multiplied each other. Specifically, the findings proved no multicollinearity between the predictors, except for the accepted collinearity between DOI, DOI2, and DOI3, since all of the correlation coefficients between variables are less than 0.8.

Table 2 indicates the regression results using the fixed-effect model. By using the “robust” option, the heteroscedasticity is constrained. The results have illustrated that there is a significant S-shaped linkage between the internationalization and firm performance as the performance will initially decrease (β1 = −0.408, p < 0.01), increase considerably (β2 = 0.724, p < 0.01), and reduce again (β3 = −0.442, p < 0.01) with a higher level of internationalization. Interestingly, the moderating effects of high and low discretion slack on the internationalization–performance relationship are significantly positive, except for during the middle stage due to the control effects of firm size, product diversity, industrial risk, and ownership identity. It is worth noting that the estimate of firm size confirmed the findings of many previous studies as the firm scale is the main determinant factor of firm performance in the international market. Besides, share ownership has a statistically positive relationship with firm performance. Meanwhile, the other two ownership types (private and state) have no impact on firm performance.

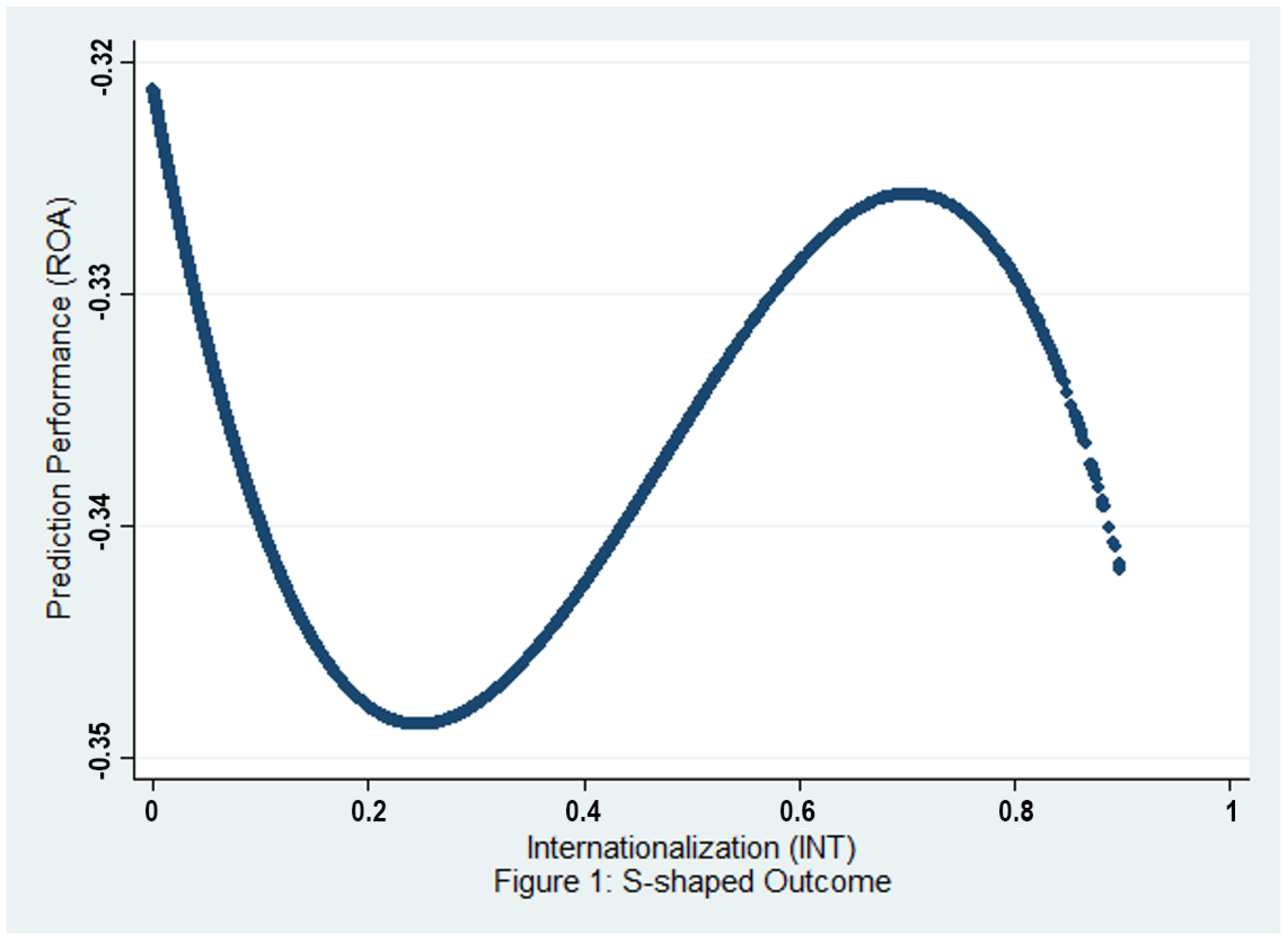

Figure 1 illustrates the prediction results of the regression model. It has revealed that the performance has an S-shaped relationship with the internationalization process of Vietnamese enterprises from 2007 to 2012. At the first stage, when the degree of global expansion is less than 22 percent, firm performance sharply decreases. The second stage is between 22 percent and 70 percent when the performance witnesses a significant rise. The third stage occurs when the degree of internationalization exceeds 70 percent, firm performance is again in a downward trend. Similar to previous studies, this result confirms the three-stage theory (S-shaped) of Contractor et al. (2003) and is consistent with the findings of Lin et al. (2011). This outcome sheds new light on an international strategy of manufacturing firms in Vietnam. This implies that managers should know how to overcome the challenges and explore more opportunities for each stage.

5. Conclusions and Discussions

5.1. Main Findings and Discussions

The finding of an S-shaped relationship between the internationalization and performance is consistent with the three-stage theory of (Contractor et al. 2003). During the first stage, it is undeniable that the firms must not only be confronted by many legal and market barriers but also compensate for learning costs to obtain the entry and market information. During the second stage, it is believed that IFs achieve initial gains from the internationalization process. The greater revenues now offset the learning cost. During the third stage, not all expansion is currently beneficial since the firms could lose their control over a too-broad system over many countries and regions. It may impose a cost burden on firms instead of providing a new opportunity.

Another finding is the importance of organizational slacks in moderating the relationship between the internationalization and firm performance during the first and third stage of internationalization process. Both the high discretion slack and low discretion slack are the strategic tool to relieve the internal pressures and facilitate the implementation of the external challenges and opportunities during these two stages (Lin et al. 2011). However, during the second stage, the presence of slack causes internationalization. Although slacks can play an essential role in buffering the internationalization, its success can be ruined by risky investments and high opportunity costs. Moreover, some new ventures or innovative projects using slacks may only pay off in the unpredictable long run independently of the current financial situation (Tan 2003). Therefore, the IFs should allocate their slack resources thoughtfully and efficiently to eliminate the risks of this uncommitted resource.

5.2. Recommendations

The empirical results suggest two recommendations regarding a managerial perspective. The first recommendation is determining the appropriate level of internationalization for the firm. The assumption of “the more international integration, the more benefits” is no longer valid in the case of Vietnamese manufacturing firms. Once the firm decides to go global, they should invest in planning a thoughtful internationalization strategy regarding which markets that they plan to expand into along with the development of their market knowledge. In this way, the firms should consider starting their new ventures in the similar foreign markets. For example, Vietnamese IFs should initially exploit the familiar markets, such as ASEAN and Asian countries with similar incomes and tastes, rather than expending huge effort to enter high-income markets that are too different, such as those of the European Union or the United States.

The firms must be patient until their capabilities are strong enough to expand to the high-risk markets. After that, the firm should also consider which level of expansion is optimal for sustaining the benefits of internationalization and orienting the whole company to follow the right vision. Secondly, as organizational slacks play a very important role in buffering the success of the internationalization process within an organization, the IFs should absorb the benefits of this strategic tool by allocating their slack resources effectively and efficiently. In this way, the slacks should be spent to facilitate and deal with the uncertainties during the internationalization process, such as adoption fees of information, market knowledge, and higher transaction and governance costs. Specifically, the firm can directly manage their high discretion slack by a healthy practice of current assets and current liabilities. For low-discretion slack, due to its nature of inflexibility, the manager should distribute this kind of organizational resource for very selective uses, for example, skilled labor retainment, technology investment, and capacity building.

5.3. Limitations

The limited access to sufficient secondary data has imposed several limitations on sampling and estimations. First, the sample failed to estimate the effects of the interesting control variables added, such as the ICT use, learning capacity, and R&D intensity, due to insufficient observations. It is obvious that these control variables were found to have significant impact on performance as determined in previous empirical studies and can also contribute to the control problem of omitted variables. Secondly, the use of the single index to measure the degree of internationalization may not be adequate in absorbing the specific attributes of internationalization. The most common composite index of internationalization includes three dimensions: (1) internationalization performance (calculated as the ratio of foreign sale to total sale), (2) internationalization structure (calculated as the ratio of foreign assets to total assets), and (3) internationalization geographic dispersion (measured as the number of countries that the firm has subsidiaries).

Author Contributions

H.T.N.H. developed conceptualization, wrote methodology, drafted first version, and revised the final one. P.V.N. collected data, conducted data analysis, provided initial discussions and checked the final version. K.T.T. conducted the research design and provided a significant interpretation of the empirical results and the recommendations.

Funding

This research is funded by Vietnam National University Ho Chi Minh City (VNU-HCMC) under grant number C2016-28-06.

Acknowledgments

We thank Hoa D.X. Trieu for her excellent technical and administrative support.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Assaf, A. George, Alexander Josiassen, Brian T. Ratchford, and Carlos Pestana Barros. 2012. Internationalization and Performance of Retail Firms: A Bayesian Dynamic Model. Journal of Retailing 88: 191–205. [Google Scholar] [CrossRef]

- Bobillo, Alfredo M., Felix López-Iturriaga, and Fernando Tejerina-Gaite. 2010. Firm performance and international diversification: The internal and external competitive advantages. International Business Review 19: 607–18. [Google Scholar] [CrossRef]

- Bourgeois, L. Jay, III. 1981. On the measurement of organizational slack. Academy of Management Review 6: 29–39. [Google Scholar] [CrossRef]

- Bourgeois, L. Jay, III. 2016. The Measurement of Organizational Knowledge Sharing. Academy of Management 6: 29–39. [Google Scholar]

- Brida, Juan Gabriel, Oana Driha, Ana B. Ramón-Rodriguez, and Maria Jesus Such-Devesa. 2016. The inverted-U relationship between the degree of internationalization and the performance: The case of Spanish hotel chains. Tourism Management Perspectives 17: 72–81. [Google Scholar] [CrossRef]

- Cardinal, Laura B., C. Chet Miller, and Leslie E. Palich. 2011. Breaking the cycle of iteration: Forensic failures of international diversification. Global Strategy Journal 1: 175–86. [Google Scholar] [CrossRef]

- Chen, Homin, and Chia-Wen Hsu. 2010. Internationalization, resource allocation and firm performance. Industrial Marketing Management 39: 1103–10. [Google Scholar] [CrossRef]

- Chen, Hsiang-Lan, Wen-Tsung Hsu, and Chiao-Yi Chang. 2016. Independent directors’ human and social capital, firm internationalization and performance implications: An integrated agency-resource dependence view. International Business Review 25: 859–71. [Google Scholar] [CrossRef]

- Chiao, Yu-Ching, Kuo-Pin Yang, and Chwo-Ming Joseph Yu. 2006. Performance, internationalization, and firm-specific advantages of SMES in a newly-industrialized economy. Small Business Economics 26: 475–92. [Google Scholar] [CrossRef]

- Chittoor, Raveendra. 2009. Internationalization of emerging economy firms-need for new theorizing. Indian Journal of Industrial Relations 45: 27–40. [Google Scholar]

- Contractor, Farok J., Sumit K. Kundu, and Chin-Chun Hsu. 2003. A three-stage theory of international expansion: The link between multinationality and performance in the service sector. Journal of International Business Studies 34: 5–18. [Google Scholar] [CrossRef]

- Contractor, Farok J., Vikas Kumar, and Sumit K. Kundu. 2007. Nature of the relationship between international expansion and performance: The case of emerging market firms. Journal of World Business 42: 401–17. [Google Scholar] [CrossRef]

- Daniel, Francis, Franz T. Lohrke, Charles J. Fornaciari, and R. Andrew Turner Jr. 2004. Slack resources and firm performance: A meta-analysis. Journal of Business Research 57: 565–74. [Google Scholar] [CrossRef]

- Dutta, Dev K., Shavin Malhotra, and PengCheng Zhu. 2016. Internationalization process, impact of slack resources, and role of the CEO: The duality of structure and agency in evolution of cross-border acquisition decisions. Journal of World Business 51: 212–25. [Google Scholar] [CrossRef]

- Eriksson, Kent, Jan Johanson, Anders Majkgård, and D. Deo Sharma. 2014. Experiential components knowledge and cost in the internationalization process. Journal of International Business Studies 28: 337–60. [Google Scholar] [CrossRef]

- García-García, Raquel, Esteban García-Canal, and Mauro F. Guillén. 2017. Rapid internationalization and long-term performance: The knowledge link. Journal of World Business 52: 97–110. [Google Scholar] [CrossRef] [Green Version]

- Glaum, Martin, and Michael-Jörg Oesterle. 2007. Introduction: 40 Years of Research on Internationalization and Firm Performance: More Questions than Answers? MIR: Management International Review 47: 307–17. [Google Scholar]

- Greene, William H. 2003. Models for Panel Data. In Econometric Analysis. Edited by Rod Banister and P. J. Boardman. Upper Saddle River: Prentice Hall, p. 283. [Google Scholar]

- Hutchinson, Karise, Nicholas Alexander, Barry Quinn, and Anne Marie Doherty. 2007. Internationalization Motives and Facilitating Factors: Qualitative Evidence from Smaller Specialist Retailers. Journal of International Marketing 15: 96–122. [Google Scholar] [CrossRef]

- Joensuu-Salo, Sanna, Kirsti Sorama, Anmari Viljamaa, and Elina Varamäki. 2018. Firm Performance among Internationalized SMEs: The Interplay of Market Orientation, Marketing Capability and Digitalization. Administrative Sciences 8: 31. [Google Scholar] [CrossRef]

- Johanson, Jan, and Jan-Erik Vahlne. 1977. The Internationalization Process of the Firm—A Model of Knowledge Development and Increasing Foreign Market Commitments. Journal of International Business Studies 8: 23–32. [Google Scholar] [CrossRef] [Green Version]

- Lin, Wen-Ting, and Yunshi Liu. 2012. Successor characteristics, organisational slack, and change in the degree of firm internationalisation. International Business Review 21: 89–101. [Google Scholar] [CrossRef]

- Lin, Wen-Ting, Kuei-Yang Cheng, and Yunshi Liu. 2009. Organizational slack and firm’s internationalization: A longitudinal study of high-technology firms. Journal of World Business 44: 397–406. [Google Scholar] [CrossRef]

- Lin, Wen-Ting, Yunshi Liu, and Kuei-Yang Cheng. 2011. The internationalization and performance of a firm: Moderating effect of a firm’s behavior. Journal of International Management 17: 83–95. [Google Scholar] [CrossRef]

- Lu, Jane W., and Paul W. Beamish. 2006. SME internationalization and performance: Growth vs. profitability. Journal of International Entrepreneurship 4: 27–48. [Google Scholar] [CrossRef]

- Marano, Valentina, Jean-Luc Arregle, Michael A. Hitt, Ettore Spadafora, and Marc van Essen. 2016. Home country institutions and the internationalization-performance relationship: A meta-analytic review. Journal of Management 42: 1075–110. [Google Scholar] [CrossRef]

- Oeconomica, Acta. 2014. Stages of internationalization: A contribution to the establishment of a theoretical framework. Akadémiai Kiadó 30: 13–30. [Google Scholar]

- Pangarkar, Nitin. 2008. Internationalization and performance of small- and medium-sized enterprises. Journal of World Business 43: 475–85. [Google Scholar] [CrossRef]

- Singla, Chitra, and Rejie George. 2013. Internationalization and performance: A contextual analysis of Indian firms. Journal of Business Research 66: 2500–6. [Google Scholar] [CrossRef]

- Stoker, Thomas, Ernst R. Berndt, Denny Ellerman, and Susanne Schennach. 2005. Panel Data Analysis. Journal of Econometrics 127: 131–64. [Google Scholar] [CrossRef]

- Tan, Justin. 2003. Curvilinear relationship between organizational slack and firm performance: Evidence from Chinese State enterprises. European Management Journal 21: 740–49. [Google Scholar] [CrossRef]

- Tsai, Huei-Ting. 2014. Moderators on international diversification of advanced emerging market firms. Journal of Business Research 67: 1243–48. [Google Scholar] [CrossRef]

- Westhead, Paul, Mike Wright, and Deniz Ucbasaran. 2001. The internationalization of new and small firms: A resource-based view. Journal of Business Venturing 16: 333–58. [Google Scholar] [CrossRef]

- Yoon, Junghyun, Ki Keun Kim, and Alisher Tohirovich Dedahanov. 2018. The role of international entrepreneurial orientation in successful internationalization from the network capability perspective. Sustainability 10: 1709. [Google Scholar] [CrossRef]

- Zhou, Chao. 2018. Internationalization and performance: Evidence from Chinese firms. Chinese Management Studies. [Google Scholar] [CrossRef]

Figure 1.

S-shaped relationship between internationalization and performance.

{kind=link}

Table 1.

Descriptive statistics.

| Mean | SD | ROA | DOI | Firm_Size | High_Slack | Low_Slack | DOI_Highslack | DOI_Lowslack | Joinstock | |

|---|---|---|---|---|---|---|---|---|---|---|

| ROA | 0.0096 | 0.0714 | 1.0000 | |||||||

| DOI | 0.0258 | 0.1057 | −0.0514 * | 1.0000 | ||||||

| Firm_size | 8.4111 | 2.5124 | 0.2220 * | 0.2989 * | 1.0000 | |||||

| High_slack | 1.6951 | 1.8701 | −0.1575 * | −0.1500 * | −0.6166 * | 1.0000 | ||||

| Low_slack | 0.7883 | 1.2615 | 0.0932 * | 0.0414 * | −0.0694 * | −0.0808 * | 1.0000 | |||

| DOI_highslack | 0.0142 | 0.0889 | −0.0309 * | 0.6315 * | 0.1498 * | −0.0357 * | 0.0332 * | 1.0000 | ||

| DOI_lowslack | 0.0259 | 0.1817 | 0.0436 * | 0.5812 * | 0.1614 * | −0.0853 * | 0.2383 * | 0.3894 * | 1.0000 | |

| Joint_stock | 0.1327 | 0.3392 | 0.0304 * | 0.2251 * | 0.3806 * | −0.1977 * | 0.0316 * | 0.1307 * | 0.1517 * | 1 |

* p < 0.10.

Table 2.

Estimated result by using fixed effect model.

| ROA | |

|---|---|

| Internationalization (INT) | −0.408 *** |

| (0.057) | |

| INT2 | 0.724 *** |

| (0.163) | |

| INT3 | −0.442 *** |

| (0.150) | |

| High-discretion slack (HS) | 0.001 ** |

| (0.001) | |

| Low-discretion slack (LS) | 0.007 *** |

| (0.001) | |

| INT × HS | 0.078 *** |

| (0.023) | |

| INT × LS | 0.106 *** |

| (0.032) | |

| INT2 × HS | −0.039 ** |

| (0.016) | |

| INT2 × LS | −0.076 *** |

| (0.025) | |

| INT3 × HS | 0.006 ** |

| (0.003) | |

| INT3 × LS | 0.013 *** |

| (0.005) | |

| Firm size | 0.036 *** |

| (0.002) | |

| Private | −0.002 |

| (0.009) | |

| Share | 0.016 * |

| (0.009) | |

| Industry risk | −0.000 * |

| (0.000) | |

| _cons | −0.325 *** |

| (0.023) | |

| N | 58,332 |

Standard errors in parentheses. * p < 0.10, ** p < 0.05, *** p < 0.01.

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Thi Ngoc Huynh, H.; V. Nguyen, P.; T. Tran, K. Internationalization and Performance of Vietnamese Manufacturing Firms: Does Organizational Slack Matter? Adm. Sci. 2018, 8, 64. https://doi.org/10.3390/admsci8040064

AMA Style

Thi Ngoc Huynh H, V. Nguyen P, T. Tran K. Internationalization and Performance of Vietnamese Manufacturing Firms: Does Organizational Slack Matter? Administrative Sciences. 2018; 8(4):64. https://doi.org/10.3390/admsci8040064

Chicago/Turabian StyleThi Ngoc Huynh, Hien, Phuong V. Nguyen, and Khoa T. Tran. 2018. "Internationalization and Performance of Vietnamese Manufacturing Firms: Does Organizational Slack Matter?" Administrative Sciences 8, no. 4: 64. https://doi.org/10.3390/admsci8040064

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.