1. Introduction

The steel industry has never fully recovered from the 2008 global economic crisis. Existing industry practices such as continuous investments in old and new facilities has equated to a global oversupply of steel. Furthermore, high-quality Ni has all but been exhausted worldwide. As a result, the price of Nickel (Ni) is the lowest it has been within the last decade. Many smelters have responded by using low-priced and low-quality raw materials in their production [

1]. While this solution has kept Ni smelters in business, using low-grade Ni ore often increases costs due to ore deterioration. The Ni smelting industry is currently at a risk of global failure [

1]. Failure within in this industry would have significant global impacts as steel, and therefore Ni, is arguably the “building blocks” of industrial progress. To avoid stressing the global steel industry, there is a need to improve the profitability of the Ni smelting industry. This paper proposes an optimum pricing index model to apply to the purchasing of raw Ni materials with the concept of the raw material (feedstock) supplier and smelter sharing in the risks of worsening Ni ore compositions.

The pricing model presented introduces a risk sharing model for deteriorating raw material caused by resource exhaustion, non-existent in literature. While this study is focused on Ni and stainless-steel manufacturing, it could feasibly be used for any raw material of declining quality. This paper begins with brief descriptions of the Ni smelting process, manufacturing process, organizational structures, and an overall analysis of the Ni market to educate the reader on the background of the problem. The existing relevant literature is then presented to support this paper’s added value to the general body of knowledge. Finally, the proposed model is presented, and its efficacy supported through a life cycle cost analysis.

1.1. Extraction, Smelting, and Manufacturing Process

The most common smelting Ni process is pyrometallurgical. This process is used to smelt a high-quality nickel ore consisting of saprorite. The process is as follows:

Drying: Remove the moisture from the saprorite.

Calcine/Reduction: Partially restore the nickel oxide through mixing with the restoring agent.

Smelting: Produce Ni and Fe through this restoration process.

Refining: Perform a final refining process to remove sulfur, phosphorus, carbon, etc. The FeNi is transformed into an ingot or a granule as FeNi or matte [

2].

The Ni extracted in this process comes from the oxidation of either the limonite or saprorite ore. Limonite contains 0.8–1.5% Ni, 40–50% Iron (Fe), and approximately 50–60% other gangue components. Alternatively, saprorite has 1.8–3.0% Ni, 10–25% Fe, and a mixed layer in which limonite and saprorite coexist. Processing ores with a high nickel content is more economically viable. However, even when using the same limonite and saprorite ore, Ni and Fe content can vary widely impacting the manufacturing cost accordingly [

3]. The feedstock’s selling price is generally priced at the net Ni weight. Fewer impurities, such as carbon, sulfur, and phosphorus, also increase the pricing. The smelting of Ni typically falls into two categories, high-power and low-power Ni ratio, which results in a high-grade and low-grade manufacturing. It is generally considered to be profitable for the high-power ratio if the Ni content of the ore is 2.1% or more and 1.7% Ni content for the low-power ratio. Although high-grade Ni ores ensure sustainable profits, smelters are often unable to acquire them due to worldwide scarcity [

4].

The Ni and Fe content also impact the manufacturing costs. A decrease in Ni content can lead to low productivity and low quality of Ni in the final product, stainless steel. This results in a profit decrease as consumers desire high-quality Ni to minimize their risk of product failure. It also impacts productivity, as stainless steel manufacturers experience a decrease of about 6000 tons/year when the Ni content in the ore decreases from 2.0% to 1.5%. Alternatively, an increase of Fe in the ores leads to a higher manufacturing cost. One study found that an increase in Fe content of 10% reduced the manufacturers profit approximately 2% [

2].

1.2. Organization of Project Based Company and Ore Procurement

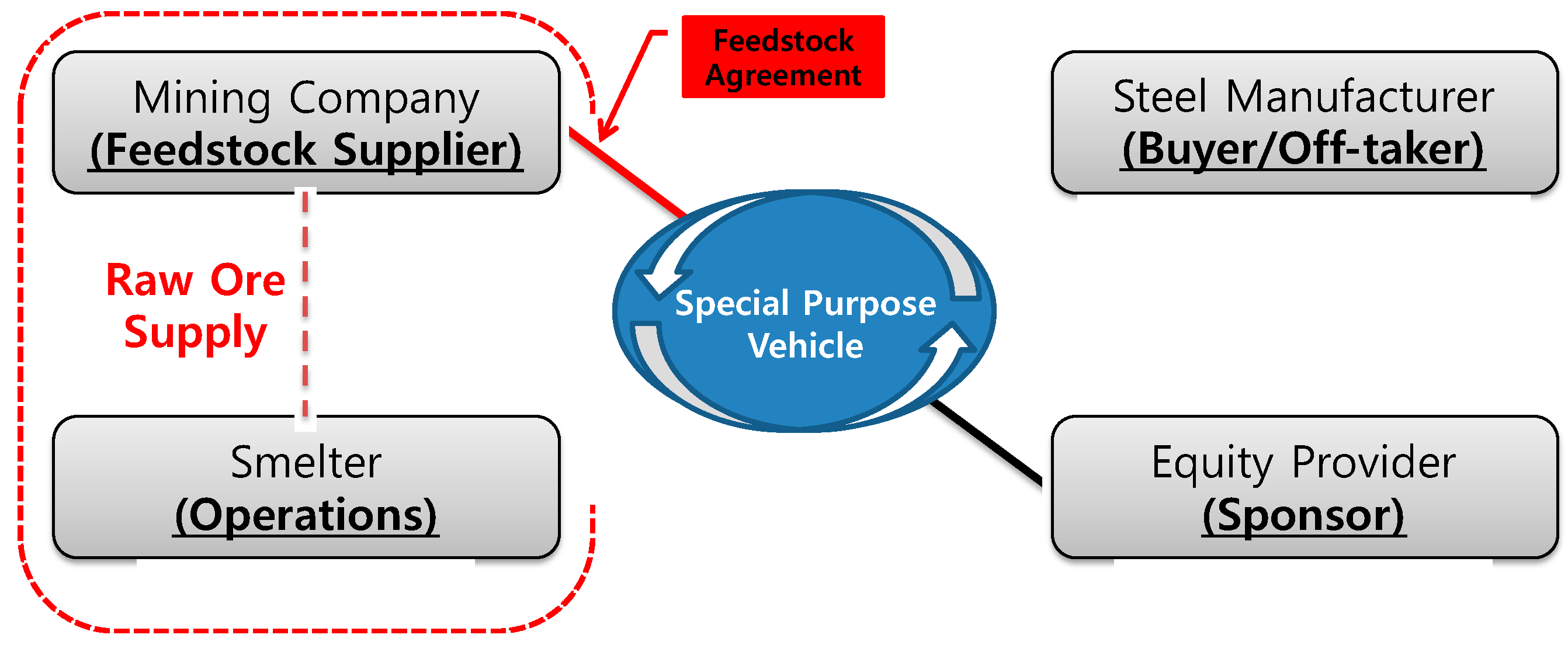

Due to the enormity of required investment, most Ni smelting operations require a special purpose company (SPC). The SPC is a legal entity encompassing a combination of organizations involved in the manufacturing of Ni who share all risks and project profitability. For this paper, the SPC consists of an equity provider, mining company, smelter, and steel manufacturer. Of the many agreements required to create this arrangement is the procurement of raw materials for stainless steel manufacturing. This is the focus of this paper and is also known as the feedstock agreement.

Figure 1 displays the SPC used for this paper, specifically identifying the feed stock supply agreement.

At the inception of the project, the feedstock agreement is executed, ensuring a stable supply of mined ores throughout the duration of the project. Theoretically any losses due to low-grade ores is borne by all organizations. However, often, the SPC contract does not provide for fluctuations in the ore Fe and Ni content which becomes the smelting company’s responsibility [

5]. Often, a set Ni ore price is determined for the duration of the project based on a bilateral negotiation executed at the start of the project. The price calculation considers the supply period, quantity, and market price without a global standard. The supply period, quantity and price of the ore, ore supply rate, and quotation are specified within the feedstock supply agreement. An “as-is” practice is the most common practice for calculating the Ni purchasing price, with the following formula [

5]:

where

Equation (1) uses a constant price ratio is a poor practice due to both the potential for variation in the ore’s Ni content and price within the current market [

5]. Equation (1) also does not consider the Fe content which has a negative impact on the manufacturing price. With these inadequacies of the current process, this paper suggests an alternative solution: sharing the smelter’s profitability fluctuation risk depending on the changes in the Ni and Fe content.

2. Literature Review

Within Ni smelting literature, most studies focus on improving Ni smelting profitability through process efficiencies. For example, Oxley [

4] proposed pre-processing ores used for Ni smelting to produce high quality raw materials. They performed a net present value (NPV) analysis for the quantitative impact on manufacturing costs. The results of pre-processing ores included a reduction in cost per ton of Ni production, reduced energy consumption, and increase in Ni grade [

4]. The studies of Pournaderi [

6] and Li et al. [

7] on Ni smelting are used to support this paper’s development of associated manufacturing costs. Pournaderi [

6] studied the impact composition and yield of metals change according to the reduction conditions of Laterite Ni ore. Li et al. [

7] studied the Rotary Kiln-Electric Furnace method applied to Laterite Ni. In this method, the reduction characteristics change depending on the conditions of reducing material, temperature, and time [

7]. As stated, studies on improving the Ni smelting efficiencies are vast and the above are just the most relevant examples. While these are valid measures to increase profitability, they do not aid smelters in reducing the risk of ore price/quality volatility.

One method of mitigating price volatility risk existent in the literature is to perform future to predict pricing fluctuations. Wårell [

8], Pustov et al. [

9], Morandi et al. [

10], Labson [

11], and Sverdrup and Ragnarsdottir [

12] are all examples of attempted to predict the future costs of material ores based on different identified variables. Both Wårell and Marandi et al. identified the main factors indicating future of material ore pricing [

8,

10]. Pustov et al. [

9] used a marginal cost approach and incentive pricing, supplemented with a Monte-Carlo simulation, to present confidence intervals of future material ore pricings. Labson [

11] developed an econometric trade model that evaluates the dynamics of the world steel market, forecasting future market demands. Sverdrup and Ragnarsdottir [

12] combined mining, ore grade changes, trade markets, price mechanisms, supply and demand, estimates of stock-in-use, waste, and recycling into a comprehensive model which also forecasted future market demands through 2080. Their findings emphasize the importance of recycling and metal conversation to secure long-term sustainable supply chains [

12]. While the resultant models from these research endeavors could be integrated into feedstock agreements, they are highly complex in execution, require data that SPCs may not have access to, and have a wide range of accuracy. Another strategy to mitigate price fluctuations in research is flexible operating strategy to mitigate Ni ore price uncertainties (e.g., [

13,

14,

15,

16,

17]). The strategic flexibility to expand, contract, defer, or abandon production has historically been one of the more popular ways to mitigate market demand and price fluctuations [

13]. While valid, there are many reasons companies may not have flexible operations (e.g., labor availability, market demands, finance terms, and contractual agreements).

Alternative to reacting to the market, Liu et al. [

18], Deng et al. [

19], Ma [

20], Sukagawa [

21], and Wårell [

22] studied alternative solutions to reducing the erratic pricing trends of commodities. Liu et al. [

18] found using price reforms to artificially increase commodity pricing had disastrous impacts to the downstream organizations. Deng et al. [

19] studied the feasibility and related efficiency of a national commodity pricing mechanism, finding current methods of Chinese pricing to be inadequate, largely due to the long duration between adjustment periods. In response to these fluctuating pricing, many organizations have begun to rely on the concept of “spot iron ore pricing”. Ma [

20] examined the variables that impact iron ore spot prices within the global market and what factors minimize its volatility. Sukagawa [

21] presented the evolution of past and current iron ore negotiation practices, ending with this concept. Wårell [

22] found that market pricing is actually more volatile after the introduction of spot market.

The above solutions could be considered to be a part of a larger research topic, supply chain management. Supply chain management is a collection of approaches used to efficiently integrate suppliers, manufacturers, storage facilities, and vendors to minimize systemwide costs [

23]. Researchers have suggested the use of a price cap for material contracts [

24]; a supply chain that is as lean as possible [

25], agile in its ability to fluctuate with minimal impacts to cost [

26], and a combination of the two [

27]; and managerial methods to predict and manage the supply chain risks of a turbulent market [

28,

29,

30]. Most relevant to this research is the proposed use of option pricing [

31] and flexible and risk-sharing supply contracts [

32] under uncertainty. Burnetas and Ritchken [

31] proposed the use of an option contract when there are fluctuations in the profitability of the supply chain [

31]. The publication presents a model which predicts the conditions under which the options can be used. Li and Kouvelis [

32] presented a flexible, risk-sharing option for general supply contracts. Within their solution are contracts which promote flexible time, unit quantities, and purchasing pricing given the status of selected variables. The lattermost is the goal of the Ni smelting fluctuating price ratio solution, described below.

Finally, the literature has also previously assessed the life-cycle profitability of different supply chains. Within power generation literature, Hong and Lee [

33] used a life-cycle approach with Monte-Carlo to perform an economic analysis of a steam-cycle optimization model. Kannan et al. [

34] performed a life cycle cost analysis (LCCA) on the fiscal viability of electricity generation from a typical oil-fired steam turbine plant in Singapore. Kannan et al. [

35] performed a life cycle assessment of solar PV systems in Singapore. Life-cycle analysis have also been performed to assess the profitability of metal recover chains. Xu et al. [

36] presented a model to predict the resiliency of a supply chain based on random supply disruptions. Kibira and Jain [

37] assessed the profitability of recycling vehicle parts including the financial, environmental, social, and manufacturing domains. Wang et al. [

38] presented a quick and effective model to aid manufacturers in maximizing profitability through recycling, reusing, and remanufacturing electrical and electronic equipment. Rosa and Terzi [

39] reviewed 35 studies that focus on decision-support methods for the profitability of metal recovery chains. However, most of these studies focus on the recovery of machinery and none discuss new or recovered steel or Ni supply chains, or how the pricing negotiations are managed.

5. Results and Discussions

Table 5 depicts the estimated ore purchasing cost and decrease in profit as the Ni% reduces from 2.0% to 1.5% in 0.1% intervals. As can be seen, when the ore content is reduced by 0.1%, the price of the ore will decrease by

$3.6 M USD/ton.

Using the price ratios for Model 2, defined in

Table 1,

Table 6 depicts the ore price, ore purchasing cost, and profit decrease. With a set price ratio, the purchase cost of ore is reduced as the Ni content within the ore is reduced due to a reduction in the “Net Ni Weight”. However, due to the reduction of quality of the ore, it can also be seen that the profit decreases significantly from 2.0% to 1.5% Ni. This reduction is caused by the increased production costs of poor-quality ores. With Model 1, this risk is transferred 100% to the manufacturer. Alternatively, with a fluctuating price ratio, the risk is shared between the supplier and manufacturer, as seen in the higher profits at 1.5% Ni content.

Although the increase in the Fe content in the ore is not a purchasing decision variable in feedstock agreement, it results in a decrease in profits. With the “as-is” scenario, the ore price remains unchanged as the Fe content increases. Using the price ratios defined in

Table 2,

Table 7 depicts the ore price, ore purchasing cost, and profit decrease.

By applying an ore purchase price patio that varies according to the Ni or Fe content, the manufacturer’s risk is mitigated. The above is an illustrative example of this. To validate this model’s risk sharing potential (in comparison to the existing model), a LCCA was performed. The LCCA was performed using the @Risk Monte Carlo software, with the calculations and assumptions outlined in Equations (10)–(14). The outputs are the smelter’s NPV, IRR, and PI when the model is and is not used. As can be seen in

Figure 8, using the model equates to an NPV average increase of 16 M USD. However, it should be noted that the results of using the model depict lower minimum and maximum profits.

Figure 9 depicts the IRR results, showing that using the model equates to an approximate increase to the internal rate of return of 5%.

Figure 10 depicts the PI results, showing an improved PI range of −0.9% to 13.3% in using the model compared to a −1.6% to 12.6% range without the model.

As can be seen in

Table 8, the NPV, IRR, and PI are all superior when the proposed model is used. According to the results of the probabilistic economic evaluation using @Risk, the probability of the NPV > 0 and IRR > 0 increases when a fluctuating price ratio model is used. Alternatively, the distribution range of the PI is also higher. The probabilistic model’s findings confirm that the proposed price index model equates to a reduction in the smelter’s ore quality fluctuation risk.

This model successfully mitigates the cited weaknesses of the existing long-term iron ore pricing model [

40,

41] used in contractual feedstock agreements between the material supplier and smelter. It also negates the need for complex iron ore pricing modeling [

10,

11,

12,

13,

14]. Although this model is presented for the Ni smelting process, the findings could theoretically be applied to any long-term procurement activities with variable quality and market conditions.

6. Conclusions

This paper presents a price index model to be applied to the long-term Ni ore feedstock agreements between manufacturers and smelters which considers the fluctuating ore quality and market conditions. Based on the LCCA, the authors found the “as-is” practice of using a constant price ratio to be unsuited to fluctuating and worsening ores (low-grade ores are low in Ni and high in Fe). The developed model increases the smelter’s likelihood of making a profit by 5% (NPV > 0, IRR > 0) with an approximate 15 M USD in savings.

Although the model represents an advance in the current state of practice, some limitations exist within this study. First, the actual purchase with the ore purchase index model of the dry Ni smelter was not applied. Second, only data for a dry Ni smelter were applied as operational information of the ore purchase index model. In the case of a feedstock supply agreement, it is usually difficult to confirm the condition of the ores at the initial stage of the project. It is also difficult to confirm the aforesaid with no quantitative operational data of the ore’s composition and impact on manufacturing cost. Furthermore, since the Ni smelting industry is private and competitive, there are few interactions between companies. There is little sharing of knowledge, know-how, and information disclosure of operational technologies. If data were acquired on the effect of ore ingredients on the manufacturing cost of Ni smelting from various smelters, future research could provide a more reliable ore purchase index model. Additional practical research with actual cases and operational information of the smelter companies are needed. To that point, the presented ore purchase index model is expected to be applied as a guideline for a new project in the future as conditions of renewal of the ore purchase contract for Company A. This real-life application of the proposed model will allow future case studies to see the efficacy of the proposed model in practice.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}