1. Introduction

Sugarcane is produced in more than 100 countries [

1] and, in some of them, it has been produced for centuries. In many of these countries, it has fostered agroindustrial development, through the production of sugar for domestic and international markets. In some developing regions, sugarcane became an important source of income, foreign exchange savings, and a propeller to rural development and food sovereignty [

2].

The expansion of the sugar industry, however, particularly over the 20th century, occurred under uneven conditions, especially as to the adoption of technology on both agricultural and industrial stages. Such inequalities favored production instability and erratic international prices, which are exacerbated by climate conditions (disturbing yield levels) and the institutional environment that affects policies at different scales, from regional to global [

3].

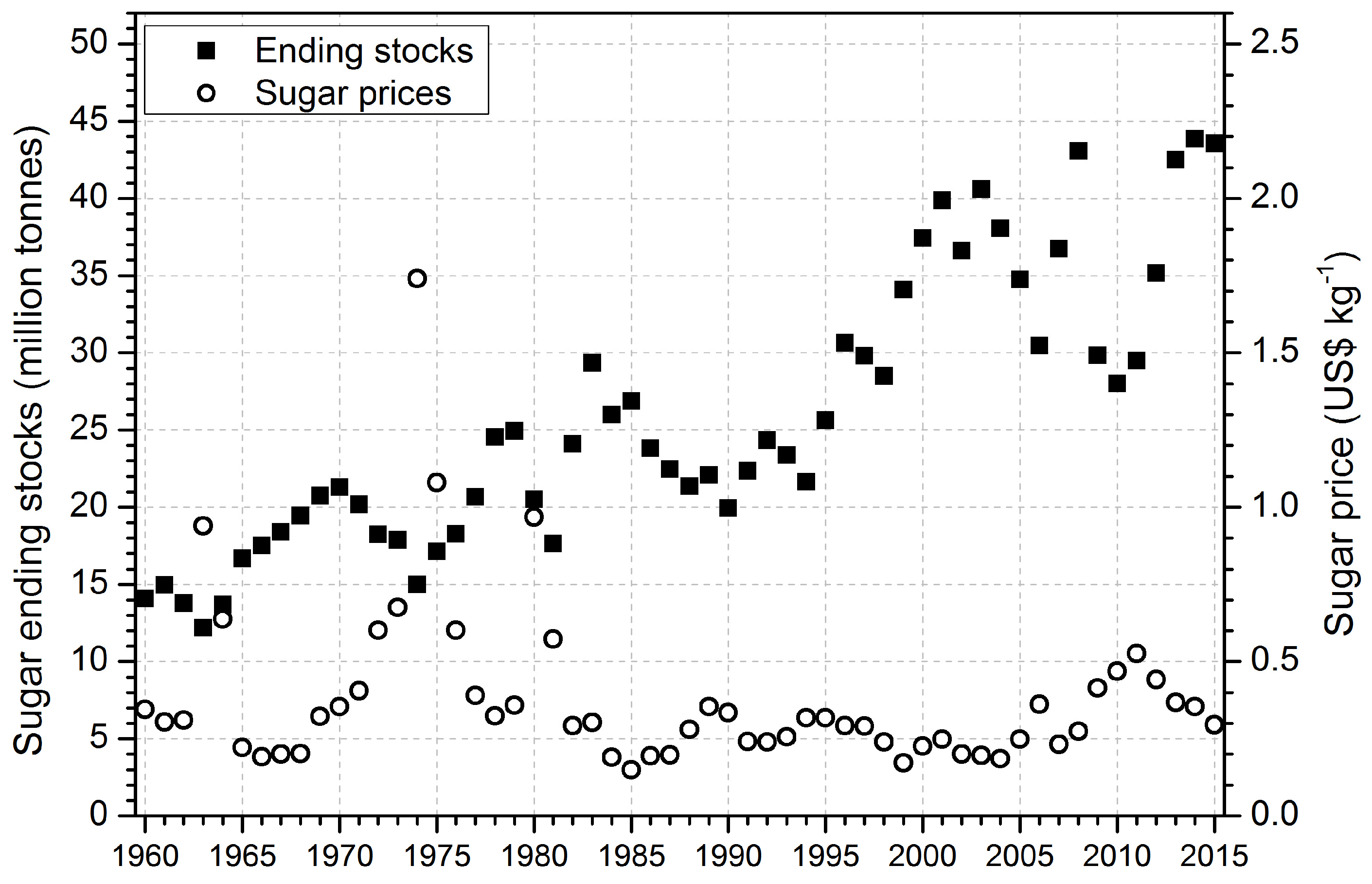

The instability of the sugar market peaked from 1950s to 1970s, when it was not rare to observe prices triple and then reach historic low levels within the same decade (

Figure 1). Since then, the sugar market has been relatively stable, mainly due to the consolidation of near future supply and demand assessments, which allowed producers to take action in the case of expected surpluses or deficits. Moreover, the number of sugar producing countries has increased, thus expanding the world capability (flexibility) to respond swiftly to market demands [

2] and reduced the impacts of regional adverse weather conditions.

In spite of relative stability, sugar prices reached record low levels from 2011 to 2015, coupled with record high sugar stocks (

Figure 1). Small sugar producers, limited in scale and product alternatives, are particularly sensitive and less resilient to market price volatility. Moreover, these countries are increasingly constrained by the high competition from large foreign exporters, such as Brazil and Thailand that together account for 60% of the international sugar market [

4].

The ACP (Africa, Caribbean and Pacific group of States) countries account for a large number of small sugar producers (e.g., Mozambique). For these countries, sugar exports depend on international accords to shield producers from the open sugar market through a combination of quota system, reference and minimum prices. The EU, one of the world’s largest importers of sugar and a key partner for ACP members, has been actively reforming its sugar import/export policy, with the end of the quota and minimum price agreements programed to September 2017. The fall of the European sugar regime is likely to exert a downward pressure on international sugar prices, thus squeezing margins and pushing out less competitive producers [

6,

7,

8].

African countries in particular are very dependent on the European sugar regime [

7]. Despite being a net importer of sugar, in the 2014/2015 season the continent exported 2.4 Mt of sugar, most of all directed to the EU. This is a relatively small amount compared to the globally traded sugar in the same period (i.e., 64 Mt) [

9]. Yet for countries such as Mozambique, Zambia, Sudan, Malawi and Madagascar, the international sugar market represent an important source of foreign exchange savings, employment and rural infrastructural development [

6,

9,

10].

The looming reforms in the EU sugar regime have a special impact in Mozambique, where the sugar industry is a leading sector in the generation of jobs and engagement of smallholder farmers in outgrower schemes [

11,

12]. Although previous assessments have indicated a way forward to sugar mills and policies in Mozambique [

12], there is a general absence of more quantitative studies that combine sugar and bioenergy production.

In this paper, our aim is to explore alternatives for the sugar-based industry of Mozambique exploring key conditions to kick-off bioenergy production that includes comparing the current, business as usual (BAU) scenario, vis-à-vis alternatives and its consequences in terms of agroindustrial adaptation and required investment cost. The country features as a typical sugar producer in the ACP region, with standard technologies to crop and process sugarcane to obtain sugar, molasses and bagasse as outputs. Moreover, sugar mills in Mozambique have been significantly dependent on the EU market for their exports, as 70% of the Mozambican sugar production, channels to the European market [

4]. Our approach simulates the potential for bioenergy (i.e., electricity and ethanol) in addition to sugar, at an existing sugar mill in southern Mozambique, and estimates the investments required in each alternative. Furthermore, we also highlight some of the key institutional enabling conditions, such as regulatory frameworks, to kick-off bioenergy production.

2. Materials and Methods

There are several ways to initiate ethanol and electricity production based on sugarcane in sugar producing countries. The different projects may be grouped into greenfield and brownfield initiatives:

Greenfield projects: starting from scratch with state of the art technology for ethanol and electricity production. Although this arrangement has the advantage to make the most efficient use of the available cane, it also requires relatively high investments together with agricultural expansion (i.e., new areas for sugarcane). While the former demands large sums of capital immobilization, the latter is a socially sensitive issue;

Brownfield projects: construction of an ethanol distillery annexed to an existing sugar mill. The new installation uses molasses as feedstock for ethanol production, thus allowing a swift start of biofuel production, with relatively low investment costs. Furthermore, in this arrangement, there is no immediate need to expand sugarcane area and sugar output may remain unaffected. In this type of project, the ratio of sugar/ethanol may also vary by reducing the molasses exhaustion, diverting part of the cane juice to the distillery, and/or increasing the production of sugarcane up to the mill processing capacity.

Several countries have successfully promoted brownfield projects, such as Brazil, Colombia, Guatemala, Thailand and Mauritius. Moreover, there are several lessons that can be learnt from them, including the impacts on cane payment system, technology selected for fermenting, distilling, and energy system upgrades–such as bagasse fired high pressure steam boilers and turbine generators, with reduction in process steam consumption.

Because brownfield projects are often the entry strategy for bioenergy production in sugarcane producing regions, we, therefore, selected this model as the most realistic to explore ethanol and electricity production in Mozambique. The sugar sector in Mozambique consists of four mills, two in the southern province of Maputo (Maragra and Xinavane), and two in the central province of Sofala (Mafambisse and Marromeu) (

Figure 2). According to the last sugar balance report, the national production of sugar amounted to 383 thousand tons out of 46 thousand hectares of sugarcane (

Table 1).

The mills in Mozambique are significantly different in sizes and performance, especially in the agricultural phase (cane yields;

Table 1), which is closely related to management and technology adoption (e.g., irrigation). Xinavane stands out with the largest area under cultivation, as well as better productivity indicators in terms of sugar and sugarcane yields (

Table 1). Furthermore, Xinavane has, by far, the largest area of sugarcane under smallholders’ arrangements. The South African agroindustrial group behind Xinavane management, estimates that in 2016 smallholders will account for 28% of the supplied cane, in an area of roughly 5.5 thousand hectares. Integrating smallholder farmers to sugarcane production is at the core of many development initiatives fostered by significant flows of international funding, particularly from the EU. The close ties between Xinavane and local communities raised international interest in the potential of sugarcane projects to stimulate rural development. Moreover, it also serves as a platform to explore whether technological innovation could promote beneficial spillovers towards rural areas. For electricity and ethanol, a desirable outcome is wider access to modern energy sources, therefore, helping to curb energy poverty, a known cause of underdevelopment in sub-Saharan Africa. Although this is a likely consequence of bioenergy production from sugarcane mills, particularly in developing regions, socioeconomic aspects of ethanol and electricity production are not the main target of this paper.

Scenarios and Technical Coefficients

To explore the potential for bioenergy production in Mozambique we compared the BAU scenario with alternative scenarios, which embodied technological innovations through retrofitting an existing sugar mill (i.e., brownfield project). The key parameters for a greenfield project (new industrial plant) are also presented as a comparative reference to brownfield scenarios. BAU scenario represents the common sugarcane production model in which sugar is the major product, with molasses as byproduct, and electricity cogeneration aims at self-sufficiency (no surpluses). We constructed the alternative scenarios, starting from the BAU, in two main stages. First, an annexed distillery is erected, thus adding ethanol production from molasses, as a coproduct from the sugar production. Second, an efficient high-pressure steam boiler powered by bagasse and turbine generator are introduced, allowing the mill to increase electricity output without changing cane input. The information required for this study derives from the BAU scenario and simulation of an alternative, with incremental production of bioenergy (i.e., ethanol and electricity). We assembled this information from field data collection and literature review, including a database of performance parameters and investment costs developed by the Brazilian Bioethanol Science and Technology Laboratory (CTBE) as part of the Sugarcane Virtual Biorefinery simulation package [

14].

The BAU scenario reflects data collected during two field trips to Mozambique in 2014 and 2015. In the first trip, we visited a sugarcane mill in southern Mozambique. This was a rather exploratory assessment, important to gain essential knowledge about the flow of activities, efficiencies, scale and timing for sugarcane management and sugar production. In the second one, to the same region, we examined the relationship between the sugarcane industry and local communities, as well as the opportunities for wider modern energy access, through bioenergy production, in Mozambique. We conducted interviews guided by a semi-structured questionnaire with scientists from the Technical University of Mozambique and Eduardo Mondlane University, non-governmental organizations (i.e., Kulima and Gwevhane), agricultural organizations (Cepagri) and the private sector (Greenlight). Additional information came from consultation with Brazilian sugarcane mills and companies to complement and validate some of the technical coefficients, especially those on electricity cogeneration and ethanol production.

The alternative scenarios are the following:

Ethanol-1 scenario: accounts for the construction of a molasses-based ethanol distillery annexed to the sugar mill.

Ethanol-2 scenario: accounts for an expansion of Ethanol-1 scenario to process 50% of the sugarcane juice plus molasses to ethanol fuel. In this scenario, there is a reduction of 50% in sugar production compared to Ethanol-1.

Ethanol/EE scenario: this scenario accounts for the installation of a full retrofitted energy system (boilers, steam generators, electrification of mechanical drives and reduction of process steam consumption) in addition to the molasses-based ethanol scenario (i.e., Ethanol-1). It also considers unburned cane harvest and the collection of 50% of cane straw to supplement bagasse in power generation. The focus of the Ethanol/EE scenario is to produce electricity surpluses while maintaining sugar production at BAU levels.

Greenfield scenario: a brand new ethanol distillery built to optimize energy production (i.e., ethanol and electricity), but with no sugar production.

Table 2 summarizes the information used in our simulation. We selected Xinavane as our benchmark sugarcane mill for the BAU scenario, while the alternative scenarios reflect a balance between literature information, expert consultation and field data.

Our simulations assumed that the existing boilers and turbine generators have spare capacity to provide the necessary steam and electricity to run the annexed distillery. Investments necessary to connect the mill to the power grid were not included in the analysis, as well as acquisition of harvesters and other equipment necessary to switch from burned cane to unburned cane harvesting, along with straw collection and processing equipment. Besides, investment cost for the Greenfield scenario, which serves as a reference for the other scenarios, is restricted to the industrial facilities, thus not including land ownership arrangements, cane cultivation and management. These values were based primarily on the Brazilian experience and reflect the technical coefficients built-in the Sugarcane Virtual Biorefinery simulation package [

14]. The main coeffients used are shown in

Table 3.

Other assumptions to the parameterization of the model:

Bagasse production: 297 kg per ton of cane (moisture 50%; cane fiber 14.1%).

Cane quality: sucrose 14% and reducing sugars 0.6% based on clean stalks, 5% vegetal impurities.

Ethanol production from molasses with 42.1% total sugars as sucrose and 90% fermentation efficiency, with a yield of 260 liters of ethanol per ton. With 40 kg of molasses per ton of cane results in around 10 L of ethanol per ton of cane.

Molasses composition range (%) [

15]: total solids 76–83; sucrose 30–36; fructose + glucose 11–15.

3. Results and Discussion

Table 4 summarizes the key results from our simulations. The alternative of annexing an ethanol distillery to the existing mill and using the molasses as the only feedstock, i.e., Ethanol-1, is promising. With an investment of US$ 4.4 million, which is relatively small compared to other scenarios, particularly the greenfield project (

Table 4), 16 million liters of ethanol can be produced, which is sufficient to blend roughly 3% ethanol in all gasoline consumed in Mozambique [

16] and, at the same time, maintain sugar production unaltered.

Nevertheless, the viability of ethanol production relies on the opportunity cost for molasses. In recent years, molasses has become a valuable coproduct in the international market, particularly as animal feed. Despite some volatility, molasses price and export quantities have soared over the last decade (

Figure 3). Therefore, diverting molasses to ethanol production is only feasible if domestic prices are attractive for sugarcane mills, while sufficiently cheaper than gasoline, thus not affecting consumers of fuel (i.e., blended gasoline). Alternatively, proper government policies, such as blending mandates, may reduce molasses opportunity cost to guarantee a market share for ethanol in the national fuel pool.

Assuming molasses at US$ 100 per ton, a reference value for the period between 2009 and 2013 (

Figure 3), and pump gasoline prices in Mozambique (i.e., US$ 0.98 per liter (

http://pt.globalpetrolprices.com/Mozambique/gasoline_prices/) in May 2016) the economic feasibility of molasses ethanol may be within reach. Molasses is the main byproduct of sugar mills. Productivity (kg per ton of cane) is quite variable, depending on the quality of sugarcane, the efficiency of the juice treatment and, mainly, the efficiency of the crystallization process. The quantity produced is usually in the range of 30–45 kg per ton of cane. Fermentable sugars (i.e., sucrose, fructose and glucose) content allows the production of ethanol, usually between 240 and 280 liters per ton of molasses [

15]. Assuming a yield of 260 liters of ethanol per ton of molasses and the price of molasses at US$ 100 per ton, the feedstock cost of ethanol would be US$ 0.38 L

−1. Parity between ethanol and gasoline, based on the energy content, is achieved at an ethanol price of US$ 0.65 L

−1. The difference between these two values (i.e., US$ 0.27 L

−1) is the economic gap to cover molasses to ethanol processing costs, distribution and dispensing the biofuel and profit margins for producers and distributors. Although this is relatively comparable to wholesale and retail prices for ethanol in Brazil [

18], the right price for ethanol in Mozambique remains out of the scope of this article, as it requires an in depth study based on the local conditions. Yet it is likely that price alone will not trigger biofuel development, which requires long-term incentives, such as mandatory blending policies, to boost confidence among investors.

Intermediate scenarios, such as Ethanol-2 increases progressively the ethanol production by using part of the sugarcane juice (50% in the simulated scenario) together with final molasses. The spare capacity created in the sugar factory in this process provides flexibility in the ethanol/sugar production ratio, thus optimizing the mill income based on the sugar and, eventually, ethanol market fluctuations. In this scenario, investment cost increases if compared to Ethanol-1, but remain relatively low in comparison with the other scenarios (

Table 4). Nevertheless, Ethanol-2 significantly increases ethanol production thus allowing a blend of about 12% across the country (12% ethanol and 88% gasoline). Moreover, ethanol may be a way to promote foreign savings, since today 100% of the gasoline consumed in Mozambique is imported [

16].

Besides, ethanol and sugar mills have a large potential for electricity (co)generation. This potential is particularly enhanced if part of the cane straw is collected and used, together with bagasse, in modern industrial settings [

19]. As such, sugar mills may help to alleviate the current energy gap that exists in sub-Saharan Africa [

20]. In Mozambique, for instance, only 20% of the population have access to electricity [

21]. However, upgrading the mill energy system requires a much larger investment than for molasses-based ethanol scenarios. Investment costs are as low as US$ 4.4 million for the annexed distillery using molasses only, growing to US$ 55 million (Ethanol/EE), and may reach US$ 141 million in a greenfield scenario in which 100% of the cane is diverted to bioenergy (

Table 4). For the Ethanol/EE scenario, some 80% of this investment costs refer to the boiler, steam generator and auxiliary systems. Yet, the 90 GWh/year surplus electricity generated by the Ethanol/EE scenario represents approximately 1% of the country’s electricity consumption [

22]. In the greenfield scenario, surplus electricity production is tripled to achieve 296 GWh·year

−1 as a consequence of a more efficient energy system and, mainly, to the use of 50% of the sugarcane straw to supplement bagasse (

Table 3).

To make these alternatives economically viable and risk manageable, adequate policy frameworks are necessary. As in many other countries, with active bioenergy programs, there is a need to implement blending mandates, attractive pricing system, power regulatory schemes and feed-in tariffs. Such arrangements may need temporary and/or permanent subsidies for the consolidation of the bioenergy market. In Mozambique, some of these initiatives are already in place. In late 2014, the country introduced a feed-in tariff for biomass electricity that ensures producers a price of about 0.1 US$ kWh

−1 [

23]. Mozambique also pioneered with the development of a sustainability framework for biofuels, particularly sugarcane ethanol [

24], with a complete set of criteria and indicators for promotion and development across the country. Yet, progress on biomass electricity as well as ethanol has been sluggish.

Missed opportunities apparently point to molasses-based ethanol (i.e., Ethanol-1 scenario), for which economic viability seems to be hanging in the lower branches. Moreover, ethanol, at 10% blending rate with gasoline, is a drop-in fuel, requiring no changes in the existing Otto-engines vehicles, nor in the storage and distribution systems. Therefore, enabling an immediate start of the ethanol use with minimum or no investment in infrastructure upgrading. After 10%, the introduction of pure ethanol (E100) or ambitious blends, such as E85, requires a separate infrastructure to store, distribute and dispense the biofuel, followed by strict regulation and control of fuel quality, besides engine adaptations.

As for the sale of renewable electricity from sugarcane mills, uncertainty still exists on whether the current feed-in tariff system provides sufficient economic incentives. Another hindering aspect is location. Rural areas often lack power lines, thus adding an important infrastructural hurdle for biomass electricity. Price competitive energy coupled with long-term contracts seems key to boost confidence and prop up regional investment.

4. Conclusions

Our assessment highlights the opportunities for ethanol production in Mozambique with relatively low investment cost and without disturbing sugar production (i.e., Ethanol-1 scenario). Ethanol production can also expand at the expense of sugar production (Ethanol-2 scenario), but with additional investments, thus allowing a flexible management between sugar/ethanol production guided by market opportunities. Surplus electricity could be also a viable alternative, but at a much larger investment cost.

A fundamental question for this study is whether bioenergy is a necessity or an opportunity for sugar mills in Mozambique. Our results indicate that there is a bit of both. This has a lot to do with diversification strategies, of course, away from sugar as a ‘winner’ product. Ethanol and electricity are must-look alternatives for sugar mills due to their wide and successful utilization in many countries, coupled with consolidated technological background. This is a pressing issue, particularly with negative prospects for Mozambique and other ACP countries after 2017, when the EU sugar regime reform ends. Opportunities, on the other hand, relate to a set of conditions necessary to foster business activity. In this respect, sugarcane ethanol has both an economic and infrastructural edge over electricity that requires larger investment capital. While researchers have highlighted the opportunities associated with sugarcane ethanol [

12], businesses such as large sugar producers in Southern Africa are keen to implement and expand their incipient ethanol production from sugarcane, insofar as policies and economic incentives allow [

25]. Currently, high molasses prices together with record low oil prices pose a challenge for ethanol production.

In spite of slow progress, prospects for sugarcane are positive. As a well-known crop, most of the available technologies and management are at reach for counties worldwide. Besides, late outcomes from COP21 also raise hopes for larger allocation of capital and research efforts on renewable sources of energy in developing regions. Tropical regions in particular can benefit from sugarcane high energy yields [

19,

26].

Finally, our simulations raise awareness to some alternatives for bioenergy production and business diversification in sugarcane mills. The analysis was inspired by a mill in southern Mozambique. However, we hope that our findings are also useful to other developing regions. A more extensive economic analysis underpinned by an in-depth local assessment is necessary to draft a detailed roadmap for policymakers and investors. Our approach offers a rather qualitative discussion, which is biased by the Brazilian experience, but informative in exploring opportunities for bioenergy and in paving the way for more detailed studies.

{kind=link}

{kind=link}

{kind=link}