Risk-Constrained Stochastic Scheduling of a Grid-Connected Hybrid Microgrid with Variable Wind Power Generation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

- A risk-constrained stochastic decision-making model is developed for optimal scheduling of a grid-connected microgrid considering the uncertainties of wind power generation, EVs and load demand as well as DA prices.

- A risk component is introduced into the scheduling problem of the microgrid to estimate profit of the operator. The influences of risk-based decision-making are investigated on the optimal scheduling results of microgrid in different levels of wind power penetration.

- A sensitivity analysis is performed to evaluate the effect of wind power penetration and the risk-aversion parameter on the cost of generation, profit and CVaR as well as trading power with the main grid.

2. Problem Description and Formulation

2.1. Problem Description

2.2. Market-Based DR Modeling

2.3. EVs Participation in DR Programs

2.4. Uncertainty Characterization

2.5. Objective Function

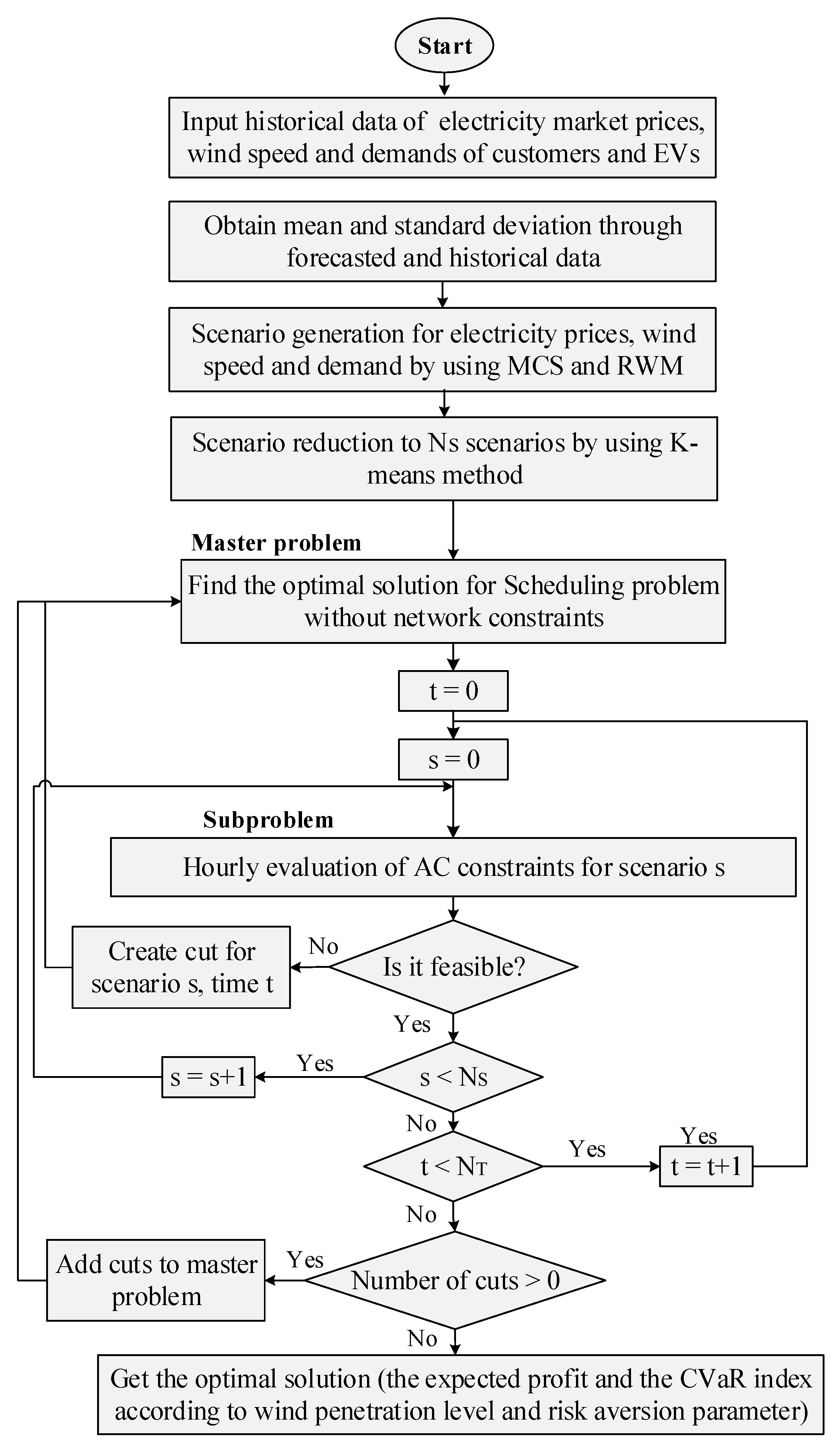

2.6. Solution Methodology

3. Simulation and Numerical Results

3.1. Case Study

3.2. Numerical Results

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

Nomenclature

| Sets and Indices | |

| (.),t,s | At time t in scenario s. |

| , | Minimum and maximum amount of a variable. |

| t, s, i, w | Indices of time, scenario, dispatchable generation units and wind turbines. |

| j, e | Indices of customers’ and EVs’ demand. |

| b, n, r | Indices of system buses. |

| , , | Set of dispatchable units, loads and wind turbines. |

| , | Set of scenarios and time slots. |

| Parameters and Constants | |

| () | Demand of customers and EVs before participation in DR programs (kW). |

| Forecasted price of day-ahead market. | |

| B | Risk-aversion parameter. |

| Per unit confidence level. | |

| Electricity price ($/kWh). | |

| () | Bid of up (down)-spinning reserve submitted by unit i ($/kWh). |

| () | Bid of up (down)-spinning reserve submitted by loads ($/kWh). |

| () | Bid of up (down)-spinning reserve submitted by the main grid ($/kWh). |

| Bid of non-spinning reserve submitted by unit i in period t ($/kWh). | |

| () | Self-elasticity (cross-elasticity) of loads. |

| Probability of scenario s. | |

| Energy capacity of EVs (kWh). | |

| Coefficient of EVs’ charge efficiency. | |

| Variables | |

| () | Demand of customers (EVs) (kW). |

| Scheduled power of dispatchable unit i (kW). | |

| Output power of wind turbine w (kW). | |

| () | Up-spinning reserve deployed by dispatchable unit i (loads). |

| () | Down-spinning reserve deployed by dispatchable unit i (loads). |

| () | Up (down)-spinning reserve deployed by main grid (kW). |

| Non-spinning reserve deployed by dispatchable unit i. | |

| Mandatory load shedding (kW). | |

| Exchanged power between microgrid and the main grid (kW). | |

| SUi, SDi | Start-up/shut-down costs of dispatchable unit i. |

| URi, DRi | Ramp-up/down rates of dispatchable unit i. |

| UTi, DTi | Minimum up/down times of dispatchable unit i. |

| Commitment status of dispatchable unit i, {0, 1}. | |

| , | Start-up and shut-down indicators of dispatchable unit i, {0, 1}. |

References

- Rashidizadeh-Kermani, H.; Vahedipour-Dahraie, M.; Shafie-khah, M.; Catalão, J.P.S. A Bi-level risk-constrained offering strategy of a wind power producer considering demand side resources. Int. J. Electr. Power Energy Syst. 2019, 104, 562–574. [Google Scholar] [CrossRef]

- Sáiz-Marín, E.; Lobato, E.; Egido, I. New challenges to wind energy voltage control. Survey of recent practice and literature review. IET Renew. Power Gener. 2018, 12, 267–278. [Google Scholar] [CrossRef]

- Vahedipour-Dahraie, M.; Najafi, H.R.; Anvari-Moghaddam, A.; Guerrero, J.M. Security-constrained unit commitment in AC microgrids considering stochastic price-based demand response and renewable generation. Int. Trans. Electr. Energy Syst. 2018, 28, e2596. [Google Scholar] [CrossRef]

- Vahedipour-Dahraie, M.; Najafi, H.R.; Anvari-Moghaddam, A.; Guerrero, J.M. Study of the effect of time-based rate demand response programs on stochastic DA energy and reserve scheduling in islanded residential microgrids. Appl. Sci. 2017, 7, 378. [Google Scholar] [CrossRef]

- Anvari-Moghaddam, A.; Guerrero, J.M.; Vasquez, J.C.; Monsef, H. Efficient energy management for a grid-tied residential microgrid. IET Gener. Trans. Distrib. 2017, 11, 2752–2761. [Google Scholar] [CrossRef]

- Rashidizadeh-Kermani, H.; Vahedipour-Dahraie, M.; Najafi, H.R.; Anvari-Moghaddam, A.; Guerrero, J.M. A stochastic Bi-level scheduling approach for participation of EV aggregators in competitive electricity markets. Appl. Sci. 2017, 7, 1100. [Google Scholar] [CrossRef]

- Rashidizadeh-Kermani, H.; Najafi, H.R.; Anvari-Moghaddam, A.; Guerrero, J.M. Optimal decision-making strategy of an electric vehicle aggregator in short-term electricity markets. Energies 2018, 11, 2413. [Google Scholar] [CrossRef]

- Waqquas, A.; Zhang, C.; Pinson, P. An integrated multiperiod OPF model with demand response and renewable generation uncertainty. IEEE Trans. Smart Grid 2016, 7, 1495–1503. [Google Scholar]

- Yang, S.; Zeng, D.; Ding, H.; Yao, J.; Wang, K.; Li, Y. Stochastic security-constrained economic dispatch for random responsive price-elastic load and wind power. IET Renew. Power Gener. 2016, 10, 936–943. [Google Scholar] [CrossRef]

- Wanga, D.; Qiub, J.; Reedman, L.; Meng, K.; Lai, L.L. Two-stage energy management for networked microgrids with high renewable penetration. Appl. Energy 2018, 226, 39–48. [Google Scholar] [CrossRef]

- Lahon, R.; Gupta, G.C. Risk-based coalition of cooperative microgrids in electricity market environment. IET Gener. Transm. Distrib. 2018, 12, 3230–3241. [Google Scholar] [CrossRef]

- Rodrigues, T.; Ramírez, P.J.; Strbac, G. Risk-averse bidding of energy and spinning reserve by wind farms with on-site energy storage. IET Renew. Power Gener. 2018, 12, 165–173. [Google Scholar] [CrossRef]

- Mohammad, N.; Mishra, Y. Coordination of wind generation and demand response to minimise operation cost in day-ahead electricity markets using bi-level optimization framework. IET Gener. Transm. Distrib. 2018, 12, 3793–3802. [Google Scholar] [CrossRef]

- Paterakis, N.G.; de la Nieta, A.A.S.; Bakirtzis, A.G. Effect of risk aversion on reserve procurement with flexible demand side resources from the ISO point of view. IEEE Trans. Sustain. Energy 2017, 8, 1040–1050. [Google Scholar] [CrossRef]

- Vahedipour-Dahraie, M.; Najafi, H.R.; Anvari-Moghaddam, A.; Guerrero, J.M. Stochastic security and risk-constrained scheduling for an autonomous microgrid with demand response and renewable energy resources. IET Renew. Power Gener. 2017, 11, 1812–1821. [Google Scholar] [CrossRef]

- Vahedipour-Dahraie, M.; Anvari-Moghaddam, A.; Guerrero, J.M. Evaluation of reliability in risk-constrained scheduling of autonomous microgrids with demand response and renewable resources. IET Renew. Power Gener. 2018, 12, 657–667. [Google Scholar] [CrossRef]

- Sharifi, R.; Anvari-Moghaddam, A.; Fathi, S.H. Economic demand response model in liberalized electricity markets with respect to flexibility of consumers. IET Gener. Trans. Distrib. 2017, 11, 4291–4298. [Google Scholar] [CrossRef]

- Sharifi, R.; Anvari-Moghaddam, A.; Fathi, S.H. Dynamic pricing: An efficient solution for true demand response enabling. J. Renew. Sustain. Energy 2017, 9, 065502. [Google Scholar] [CrossRef] [Green Version]

- Carrión, M.; Arroyo, J.M.; Conejo, A.J. A bilevel stochastic programming approach for retailer futures market trading. IEEE Trans. Power Syst. 2009, 24, 1446–1456. [Google Scholar] [CrossRef]

- Heydarian-Forushani, E.; Moghaddam, M.P.; Sheikh-El-Eslami, M.K.; Shafie-Khah, M. Risk-constrained offering strategy of wind power producers considering intraday demand response exchange. IEEE Trans. Sustain. Energy 2014, 5, 1036–1047. [Google Scholar] [CrossRef]

- Geramifar, H.; Shahabi, M.; Barforoshi, T. Coordination of energy storage systems and demand resources for optimal scheduling of microgrids under uncertainties. IET Renew. Power Gener. 2017, 11, 378–388. [Google Scholar] [CrossRef]

- Rashidizadeh-Kermani, H.; Vahedipour-Dahraie, M.; Anvari-Moghaddam, A.; Guerrero, J.M. Stochastic risk-constrained decision-making approach for a retailer in a competitive environment with flexible demand side resources. Int. Trans. Electr. Energy Syst. 2019, 29, e2719. [Google Scholar] [CrossRef]

- Arthur, D.; Vassilvitskii, S. K-means++: The advantages of careful seeding. In Proceedings of the 18th Annual ACM-SIAM Symposium Discrete Algorithms (SODA’07), New Orleans, LA, USA, 7–9 January 2007; pp. 1027–1035. [Google Scholar]

- Rezaei, N.; Kalantar, M. Economic–environmental hierarchical frequency management of a droop-controlled islanded microgrid. Energy Convers. Manag. 2014, 88, 498–515. [Google Scholar] [CrossRef]

- Relevant Information on the Market Pertaining to Nordpool. Available online: http://www.Nordpool.com (accessed on 5 September 2016).

- Rezaei, N.; Kalantar, M. Smart microgrid hierarchical frequency control ancillary service provision based on virtual inertia concept: An integrated demand response and droop controlled distributed generation framework. Energy Convers. Manag. 2015, 92, 287–301. [Google Scholar] [CrossRef]

- The General Algebraic Modeling System (GAMS) Software. Available online: http://www.gams.com (accessed on 15 September 2016).

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Vahedipour-Dahraie, M.; Rashidizadeh-Kermani, H.; Anvari-Moghaddam, A. Risk-Constrained Stochastic Scheduling of a Grid-Connected Hybrid Microgrid with Variable Wind Power Generation. Electronics 2019, 8, 577. https://doi.org/10.3390/electronics8050577

Vahedipour-Dahraie M, Rashidizadeh-Kermani H, Anvari-Moghaddam A. Risk-Constrained Stochastic Scheduling of a Grid-Connected Hybrid Microgrid with Variable Wind Power Generation. Electronics. 2019; 8(5):577. https://doi.org/10.3390/electronics8050577

Chicago/Turabian StyleVahedipour-Dahraie, Mostafa, Homa Rashidizadeh-Kermani, and Amjad Anvari-Moghaddam. 2019. "Risk-Constrained Stochastic Scheduling of a Grid-Connected Hybrid Microgrid with Variable Wind Power Generation" Electronics 8, no. 5: 577. https://doi.org/10.3390/electronics8050577