Exploring the Link between Academic Dishonesty and Economic Delinquency: A Partial Least Squares Path Modeling Approach

,

,

Abstract

:1. Introduction

2. Literature Review

3. Materials and Methods

4. Results

5. Discussion

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- LaDuke, R.D. Academic Dishonesty Today, Unethical Practices Tomorrow? J. Prof. Nurs. 2013, 29, 402–406. [Google Scholar] [CrossRef] [PubMed]

- Nonis, S.; Swift, C.O. An Examination of the Relationship Between Academic Dishonesty and Workplace Dishonesty: A Multicampus Investigation. J. Educ. Bus. 2001, 77, 69–77. [Google Scholar] [CrossRef]

- Lucas, G.M.; Friedrich, J. Individual Differences in Workplace Deviance and Integrity as Predictors of Academic Dishonesty. Ethics Behav. 2005, 15, 15–35. [Google Scholar] [CrossRef]

- Chen, Y.-J.; Tang, T.L.-P. Attitude Toward and Propensity to Engage in Unethical Behavior: Measurement Invariance across Major among University Students. J. Bus. Ethics 2006, 69, 77–93. [Google Scholar] [CrossRef]

- Mazar, N.; Ariely, D. Dishonesty in everyday life and its policy implications. J. Public Policy Mark. 2006, 25, 117–126. [Google Scholar] [CrossRef] [Green Version]

- Harper, M.G. High tech cheating. Nurse Educ. Pract. 2006, 6, 364–371. [Google Scholar] [CrossRef]

- Schmelkin, L.P.; Gilbert, K.; Spencer, K.J.; Pincus, H.S.; Silva, R. A Multidimensional Scaling of College Students’ Perceptions of Academic Dishonesty. J. High. Educ. 2008, 79, 587–607. [Google Scholar] [CrossRef]

- Brown, D.L. Cheating Must Be Okay—Everybody Does It! Nurse Educ. 2002, 27, 6. [Google Scholar] [CrossRef]

- Faucher, D.; Caves, S. Academic dishonesty: Innovative cheating techniques and the detection and prevention of them. Teach. Learn. Nurs. 2009, 4, 37–41. [Google Scholar] [CrossRef]

- Gaberson, K.B. Academic Dishonesty Among Nursing Students. Nurs. Forum 1997, 32, 14–20. [Google Scholar] [CrossRef]

- Carpenter, D.D.; Harding, T.S.; Finelli, C.J.; Passow, H.J. Does academic dishonesty relate to unethical behavior in professional practice? An exploratory study. Sci. Eng. Ethics 2004, 10, 311–324. [Google Scholar] [CrossRef] [PubMed]

- Li-Ping Tang, T.; Chen, Y.-J.; Sutarso, T. Bad apples in bad (business) barrels: The love of money, Machiavellianism, risk tolerance, and unethical behavior. Manag. Decis. 2008, 46, 243–263. [Google Scholar] [CrossRef]

- Sheard, J.; Markham, S.; Dick, M. Investigating Differences in Cheating Behaviours of IT Undergraduate and Graduate Students: The maturity and motivation factors. High. Educ. Res. Dev. 2003, 22, 91–108. [Google Scholar] [CrossRef]

- Gerlach, P. The games economists play: Why economics students behave more selfishly than other students. PLoS ONE 2017, 12, e0183814. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Harris, J.R. A Comparison of the Ethical Values of Business Faculty and Students: How Different Are They? Bus. Prof. Ethics J. 1988, 7, 27–49. [Google Scholar] [CrossRef]

- Wood, J.A.; Longenecker, J.G.; McKinney, J.A.; Moore, C.W. Ethical attitudes of students and business professionals: A study of moral reasoning. J. Bus. Ethics 1988, 7, 249–257. [Google Scholar] [CrossRef]

- Bacon, A.M.; McDaid, C.; Williams, N.; Corr, P.J. What motivates academic dishonesty in students? A reinforcement sensitivity theory explanation. Br. J. Educ. Psychol. 2019. [Google Scholar] [CrossRef]

- Błachnio, A. Don’t cheat, be happy. Self-control, self-beliefs, and satisfaction with life in academic honesty: A cross-sectional study in Poland. Scand. J. Psychol. 2019, 60, 261–266. [Google Scholar] [CrossRef]

- Fida, R.; Tramontano, C.; Paciello, M.; Ghezzi, V.; Barbaranelli, C. Understanding the Interplay Among Regulatory Self-Efficacy, Moral Disengagement, and Academic Cheating Behaviour During Vocational Education: A Three-Wave Study. J. Bus. Ethics 2018, 153, 725–740. [Google Scholar] [CrossRef]

- Keener, T.A.; Galvez Peralta, M.; Smith, M.; Swager, L.; Ingles, J.; Wen, S.; Barbier, M. Student and faculty perceptions: Appropriate consequences of lapses in academic integrity in health sciences education. BMC Med. Educ. 2019, 19, 209. [Google Scholar] [CrossRef] [Green Version]

- Blankenship, K.L.; Whitley, B.E. Relation of General Deviance to Academic Dishonesty. Ethics Behav. 2000, 10, 1–12. [Google Scholar] [CrossRef]

- Fass, R. Cheating and plagiarism. Ethics High. Educ. 1990. Available online: https://eric.ed.gov/?id=ED324727 (accessed on 12 November 2019).

- Walsh, K. Understanding Taxpayer Behaviour—New Opportunities for Tax Administration. Econ. Soc. Rev. 2012, 43, 451–475. [Google Scholar]

- Lim, V.K.G.; Teo, T.S.H. Sex, money and financial hardship: An empirical study of attitudes towards money among undergraduates in Singapore. J. Econ. Psychol. 1997, 18, 369–386. [Google Scholar] [CrossRef]

- Yamauchi, K.T.; Templer, D.J. The Development of a Money Attitude Scale. J. Personal. Assess. 1982, 46, 522–528. [Google Scholar] [CrossRef] [PubMed]

- Fox, S.; Spector, P.E.; Miles, D. Counterproductive Work Behavior (CWB) in Response to Job Stressors and Organizational Justice: Some Mediator and Moderator Tests for Autonomy and Emotions. J. Vocat. Behav. 2001, 59, 291–309. [Google Scholar] [CrossRef]

- Caruso, E.M.; Vohs, K.D.; Baxter, B.; Waytz, A. Mere exposure to money increases endorsement of free-market systems and social inequality. J. Exp. Psychol. Gen. 2013, 142, 301–306. [Google Scholar] [CrossRef] [Green Version]

- Phau, I.; Woo, C. Understanding compulsive buying tendencies among young Australians: The roles of money attitude and credit card usage. Mark. Intell. Plan. 2008, 26, 441–458. [Google Scholar] [CrossRef] [Green Version]

- McHoskey, J.W. Factor structure of the protestant work ethic scale. Personal. Individ. Differ. 1994, 17, 49–52. [Google Scholar] [CrossRef]

- Mudrack, P.E. Protestant work-ethic dimensions and work orientations. Personal. Individ. Differ. 1997, 23, 217–225. [Google Scholar] [CrossRef]

- Mirels, H.L.; Garrett, J.B. The Protestant Ethic as a personality variable. J. Consult. Clin. Psychol. 1971, 36, 40–44. [Google Scholar] [CrossRef]

- Hassall, S.L.; Muller, J.J.; Hassall, E.J. Comparing the Protestant work ethic in the employed and unemployed in Australia. J. Econ. Psychol. 2005, 26, 327–341. [Google Scholar] [CrossRef]

- Amos, C.; Zhang, L.; Read, D. Hardworking as a Heuristic for Moral Character: Why We Attribute Moral Values to Those Who Work Hard and Its Implications. J. Bus. Ethics 2019, 158, 1047–1062. [Google Scholar] [CrossRef]

- Murdock, T.B.; Stephens, J.M. 10—Is Cheating Wrong? Students’ Reasoning about Academic Dishonesty. In Psychology Academic Cheating; Anderman, E.M., Murdock, T.B., Eds.; Academic Press: Burlington, ON, Canada, 2007; pp. 229–251. ISBN 978-0-12-372541-7. [Google Scholar]

- Jensen, L.A.; Arnett, J.J.; Feldman, S.S.; Cauffman, E. It’s Wrong, But Everybody Does It: Academic Dishonesty among High School and College Students. Contemp. Educ. Psychol. 2002, 27, 209–228. [Google Scholar] [CrossRef]

- Ciarrochi, J.; Heaven, P.C.; Davies, F. The impact of hope, self-esteem, and attributional style on adolescents’ school grades and emotional well-being: A longitudinal study. J. Res. Personal. 2007, 41, 1161–1178. [Google Scholar] [CrossRef]

- Mullen, S.P.; Gothe, N.P.; McAuley, E. Evaluation of the factor structure of the Rosenberg Self-Esteem Scale in older adults. Personal. Individ. Differ. 2013, 54, 153–157. [Google Scholar] [CrossRef] [Green Version]

- Rosenberg, M. Society and the Adolescent Self-Image; Princeton University Press: Princeton, NJ, USA, 2015; ISBN 978-1-4008-7613-6. [Google Scholar]

- Fox, S.; Spector, P.E. A model of work frustration–aggression. J. Organ. Behav. 1999, 20, 915–931. [Google Scholar] [CrossRef]

- Schwarzer, R.; Jerusalem, M. The general self-efficacy scale (GSE). Anxiety Stress Coping 2010, 12, 329–345. [Google Scholar]

- Luszczynska, A.; Scholz, U.; Schwarzer, R. The General Self-Efficacy Scale: Multicultural Validation Studies. J. Psychol. 2005, 139, 439–457. [Google Scholar] [CrossRef] [Green Version]

- Reiss, M.C.; Mitra, K. The Effects of Individual Difference Factors on the Acceptability of Ethical and Unethical Workplace Behaviors. J. Bus. Ethics 1998, 17, 1581–1593. [Google Scholar] [CrossRef]

- Scholz, U.; Doña, B.G.; Sud, S.; Schwarzer, R. Is general self-efficacy a universal construct? Psychometric findings from 25 countries. Eur. J. Psychol. Assess. 2002, 18, 242. [Google Scholar] [CrossRef]

- Hoon, L.S.; Lim, V.K.G. Attitudes towards money and—for Asian management style following the economic crisis. J. Manag. Psychol. 2001, 16, 159–173. [Google Scholar] [CrossRef]

- Chitchai, N.; Senasu, K.; Sakworawich, A. The moderating effect of love of money on relationship between socioeconomic status and happiness. Kasetsart J. Soc. Sci. 2018. [Google Scholar] [CrossRef]

- Vohs, K.D. Money priming can change people’s thoughts, feelings, motivations, and behaviors: An update on 10 years of experiments. J. Exp. Psychol. Gen. 2015, 144, e86–e93. [Google Scholar] [CrossRef] [PubMed]

- Mitchell, M.S.; Baer, M.D.; Ambrose, M.L.; Folger, R.; Palmer, N.F. Cheating under pressure: A self-protection model of workplace cheating behavior. J. Appl. Psychol. 2018, 103, 54–73. [Google Scholar] [CrossRef]

- Kouchaki, M.; Smith-Crowe, K.; Brief, A.P.; Sousa, C. Seeing green: Mere exposure to money triggers a business decision frame and unethical outcomes. Organ. Behav. Hum. Decis. Process. 2013, 121, 53–61. [Google Scholar] [CrossRef]

- Piff, P.K. Wealth and the Inflated Self: Class, Entitlement, and Narcissism. Personal. Soc. Psychol. Bull. 2014, 40, 34–43. [Google Scholar] [CrossRef] [Green Version]

- Durvasula, S.; Lysonski, S. Money, money, money—How do attitudes toward money impact vanity and materialism?—The case of young Chinese consumers. J. Consum. Mark. 2010, 27, 169–179. [Google Scholar] [CrossRef] [Green Version]

- Roberts, J.A.; Jones, E. Money Attitudes, Credit Card Use, and Compulsive Buying among American College Students. J. Consum. Aff. 2001, 35, 213–240. [Google Scholar] [CrossRef]

- Roberts, J.A.; Sepulveda, M.C.J. Demographics and money attitudes: A test of Yamauchi and Templers (1982) money attitude scale in Mexico. Personal. Individ. Differ. 1999, 27, 19–35. [Google Scholar] [CrossRef]

- Wernimont, P.F.; Fitzpatrick, S. The meaning of money. J. Appl. Psychol. 1972, 56, 218–226. [Google Scholar] [CrossRef]

- Roberts, J.A.; Sepulveda, M.C.J. Money Attitudes and Compulsive Buying. J. Int. Consum. Mark. 1999, 11, 53–74. [Google Scholar] [CrossRef]

- Fornell, C.; Bookstein, F.L. Two Structural Equation Models: LISREL and PLS Applied to Consumer Exit-Voice Theory. J. Mark. Res. 1982, 19, 440–452. [Google Scholar] [CrossRef] [Green Version]

- Joreskog, K.G.; Wold, H. The ML and PLS techniques for modeling with latent variables: Historical and comparative aspects. In Systems under Indirect Observation: Part I.; Joreskog, K.G., Wold, H., Eds.; North–Holland: Amsterdam, The Netherland, 1982; pp. 263–270. [Google Scholar]

- Nunnally, J.C.; Bernstein, I.H. Psychometric Theory, 3rd ed.; McGraw-Hill: New York, NY, USA, 1994; ISBN 978-0-07-047849-7. [Google Scholar]

- Fornell, C.; Larcker, D.F. Evaluating structural equation models with unobservable variables and measurement error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Kennedy, P. A Guide to Econometrics, 6st ed.; Wiley-Blackwell: Malden, MA, USA, 2008; ISBN 978-1-4051-8257-7. [Google Scholar]

- Hu, L.; Bentler, P.M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Struct. Equ. Model. Multidiscip. J. 1999, 6, 1–55. [Google Scholar] [CrossRef]

- Cohen, J. Statistical Power Analysis for the Behavioral Sciences, 2nd ed.; Routledge: Hillsdale, MI, USA, 1988; ISBN 978-0-8058-0283-2. [Google Scholar]

- Mirshekary, S.; Lawrence, A.D.K. Academic and Business Ethical Misconduct and Cultural Values: A Cross National Comparison. J. Acad. Ethics 2009, 7, 141–157. [Google Scholar] [CrossRef]

{kind=link}

| Items [23] | Dimension | |

|---|---|---|

| ATT1 | To claim credits or tax/payment reliefs that you are not entitled to | Tax Evasion and Social Insurance Fraud Acceptance (TESIFA) |

| ATT2 | To deliberately not pay the taxes you are supposed to pay | |

| ATT3 | To deliberately claim state social benefits that you are not entitled to | |

| ATT4 | To knowingly buy counterfeit goods (e.g., clothing, handbags) | Piracy Acceptance (PA) |

| ATT5 | To knowingly buy pirated goods (e.g., books, CDs, DVDs) | |

| ATT6 | To use a computer software without having a valid license for it | |

| Items from the Protestant Ethic Scale [31] | ||

|---|---|---|

| Item | Latent Variable | Manifest Variable |

| WORK1 | Hard Work as the Path to Achievement (HAWPACH) [30] | Any person who is able and willing to work hard has a good chance of succeeding |

| WORK2 | If one works hard enough they are likely to make a good life for themselves | |

| WORK3 | Valuing leisure time (VLT) [30] | People should have more leisure time to spend in relaxation |

| WORK4 | Life would be more meaningful if we had more leisure time | |

| Self-Esteem Scale [36] | Latent Variables—Feelings | ||

|---|---|---|---|

| EST1 | On the whole, I am satisfied with myself. | Positive | |

| EST2 | At times I think I am no good at all. | Negative | |

| EST3 | I feel that I have a number of good qualities. | Positive | |

| EST4 | I am able to do things as well as most other people. | Positive | |

| EST5 | I feel I do not have much to be proud of. | Negative | |

| EST6 | I certainly feel useless at times. | Negative | |

| EST7 | I feel that I’m a person of worth, at least on an equal plane with others. | Positive | |

| EST8 | I wish I could have more respect for myself. | Negative | |

| EST9 | All in all, I am inclined to feel that I am a failure. | Negative | |

| EST10 | I take a positive attitude toward myself. | Positive | |

| Item | Latent Variable | Manifest Variable |

|---|---|---|

| PFM1 | Preoccupation with money [44] | Compared to people I know, I believe I think about money more than they do. |

| PFM2 | I often fantasize about money and what I can do with it. | |

| PFM3 | Most of my friends have more money than I do. | |

| PFM4 | Money is the most important thing in my life. |

| Latent Structure | Observed Variables |

|---|---|

| NEF | Negative feelings. Part of the self-esteem scale, the items capture negative feelings toward oneself: EST2, EST5, EST6, EST8, EST9 |

| POF | Positive feelings. Part of the self-esteem scale, the items capture positive feelings toward oneself: EST1, EST3, EST4, EST7, EST10 |

| HAWPACH | Hard work as the path to achievement. Hard work provides ground for success in life: WORK1, WORK2 |

| VLT | Valuing leisure time. Appreciation for leisure time: WORK3, WORK4 |

| ACADISH | Academic dishonesty. Motivators for academic cheating: DIS1, DIS2 |

| SELFEFF | Self-efficacy. The level of self-efficacy: SELFEFF1–SELFEFF10 |

| PFM | Preoccupation with money. Importance of money and fantasies around them: MON1, MON2, MON3, MON4 |

| TESIFA | Tax evasion and social insurance fraud acceptance. The level of acceptance of active rule bending: ATT1, ATT2, ATT3 |

| PA | Piracy acceptance. The level of piracy acceptance: ATT4, ATT5, ATT6 |

| Variable | Abbreviation | Composite Reliability (Dillon Goldstein rho) | Cronbach’s Alpha | Average Variance Extracted (AVE) |

|---|---|---|---|---|

| Negative feelings | NEF | 0.889 | 0.833 | 0.668 |

| Positive feelings | POF | 0.897 | 0.827 | 0.743 |

| Valuing leisure time | VLT | 0.867 | 0.692 | 0.765 |

| Hard Work as the Path to Achievement | HAWPACH | 0.873 | 0.710 | 0.775 |

| Self-efficacy | SELFEFF | 0.936 | 0.923 | 0,621 |

| Preoccupation with money | PFM | 0.828 | 0.583 | 0.706 |

| Academic Dishonesty | ACADISH | 0.955 | 0.906 | 0.914 |

| Tax Evasion and Social Insurance Fraud | TESIFA | 0.883 | 0.824 | 0.654 |

| Piracy acceptance | PA | 0.851 | 0.736 | 0.656 |

| Variable | NEF | POF | VLT | HAWPACH | SELFEFF | PFM | ACADISH | TESIFA | PA |

|---|---|---|---|---|---|---|---|---|---|

| NEF | 0.817 | 0.593 | −0.028 | 0.163 | 0.395 | −0.114 | −0.130 | −0.272 | −0.195 |

| POF | 0.862 | 0.081 | 0.288 | 0.583 | 0.030 | −0.021 | −0.096 | −0.073 | |

| VLT | 0.874 | 0.145 | 0.127 | 0.136 | 0.084 | 0.049 | 0.143 | ||

| HAWPACH | 0.881 | 0.347 | 0.031 | −0.087 | −0.197 | −0.193 | |||

| SELFEFF | 0.788 | 0.112 | −0.049 | −0.224 | −0.073 | ||||

| PFM | 0.840 | 0.249 | 0.190 | 0.275 | |||||

| ACADISH | 0.956 | 0.392 | 0.475 | ||||||

| TESIFA | 0.809 | − | |||||||

| PA | 0.810 |

| Variable | NEF | POF | VLT | HAWPACH | SELFEFF | PFM | ACADISH | TESIFA | PA |

|---|---|---|---|---|---|---|---|---|---|

| EST2 | 0.854 | −0.034 | −0.059 | −0.044 | −0.005 | −0.032 | −0.010 | 0.066 | 0.008 |

| EST5 | 0.722 | 0.016 | 0.049 | 0.041 | −0.021 | −0.055 | 0.039 | −0.008 | −0.037 |

| EST6 | 0.851 | −0.119 | 0.032 | 0.028 | 0.024 | 0.046 | −0.016 | 0.063 | 0.075 |

| EST9 | 0.835 | 0.142 | −0.015 | −0.019 | −0.002 | 0.034 | −0.006 | −0.125 | −0.053 |

| EST1 | −0.099 | 0.865 | −0.009 | −0.005 | −0.008 | −0.037 | 0.000 | 0.034 | 0.002 |

| EST7 | 0.033 | 0.856 | 0.027 | −0.003 | −0.037 | 0.061 | 0.021 | −0.052 | 0.045 |

| EST10 | 0.066 | 0.866 | −0.017 | 0.007 | 0.044 | −0.023 | −0.021 | 0.017 | −0.047 |

| WORK3 | 0.009 | −0.035 | 0.874 | 0.049 | 0.009 | −0.102 | −0.009 | 0.016 | 0.003 |

| WORK4 | −0.009 | 0.035 | 0.874 | −0.049 | −0.009 | 0.102 | 0.009 | −0.016 | −0.003 |

| WORK1 | 0.006 | 0.026 | −0.011 | 0.881 | 0.016 | 0.055 | 0.013 | −0.032 | 0.001 |

| WORK2 | −0.006 | −0.026 | 0.011 | 0.881 | −0.016 | −0.055 | −0.013 | 0.032 | −0.001 |

| SELFEFF1 | −0.064 | 0.042 | 0.022 | 0.066 | 0.827 | −0.012 | 0.018 | −0.067 | 0.067 |

| SELFEFF4 | 0.038 | 0.070 | −0.004 | −0.039 | 0.859 | −0.053 | 0.050 | 0.020 | −0.006 |

| SELFEFF5 | 0.013 | 0.085 | −0.019 | −0.093 | 0.805 | 0.116 | 0.034 | 0.009 | −0.003 |

| SELFEFF6 | −0.037 | 0.014 | −0.000 | 0.162 | 0.788 | 0.029 | −0.024 | −0.034 | −0.032 |

| SELFEFF7 | 0.099 | −0.077 | 0.005 | −0.061 | 0.708 | −0.123 | −0.104 | 0.081 | −0.095 |

| SELFEFF8 | −0.009 | −0.015 | 0.032 | −0.044 | 0.837 | −0.066 | −0.042 | −0.059 | −0.005 |

| SELFEFF9 | −0.059 | −0.060 | 0.012 | −0.025 | 0.724 | 0.028 | −0.009 | −0.085 | 0.037 |

| SELFEFF10 | −0.003 | 0.009 | −0.038 | −0.032 | 0.832 | 0.033 | 0.004 | 0.042 | −0.016 |

| MON1 | −0.045 | 0.056 | −0.071 | −0.062 | −0.010 | 0.840 | 0.013 | 0.006 | 0.039 |

| MON2 | 0.045 | −0.056 | 0.071 | 0.062 | 0.010 | 0.840 | 0.013 | −0.006 | −0.039 |

| DIS1 | −0.001 | 0.034 | 0.002 | 0.008 | −0.014 | 0.008 | 0.956 | 0.018 | −0.007 |

| DIS2 | 0.001 | −0.034 | −0.002 | −0.008 | 0.014 | −0.008 | 0.956 | −0.018 | 0.007 |

| ATT1 | 0.060 | −0.005 | 0.034 | −0.059 | 0.032 | 0.054 | 0.107 | 0.823 | − |

| ATT2 | −0.025 | −0.014 | −0.031 | 0.074 | 0.010 | −0.022 | −0.054 | 0.834 | − |

| ATT3 | −0.008 | 0.011 | 0.015 | 0.049 | 0.002 | 0.037 | 0.008 | 0.780 | − |

| ATT4 | 0.003 | −0.001 | 0.006 | −0.031 | 0.047 | −0.046 | 0.098 | − | 0.839 |

| ATT5 | −0.001 | −0.059 | 0.033 | −0.038 | −0.031 | 0.030 | −0/065 | − | 0.739 |

| ATT6 | −0.002 | 0.053 | −0.034 | 0.064 | −0.019 | 0.019 | −0.041 | − | 0.848 |

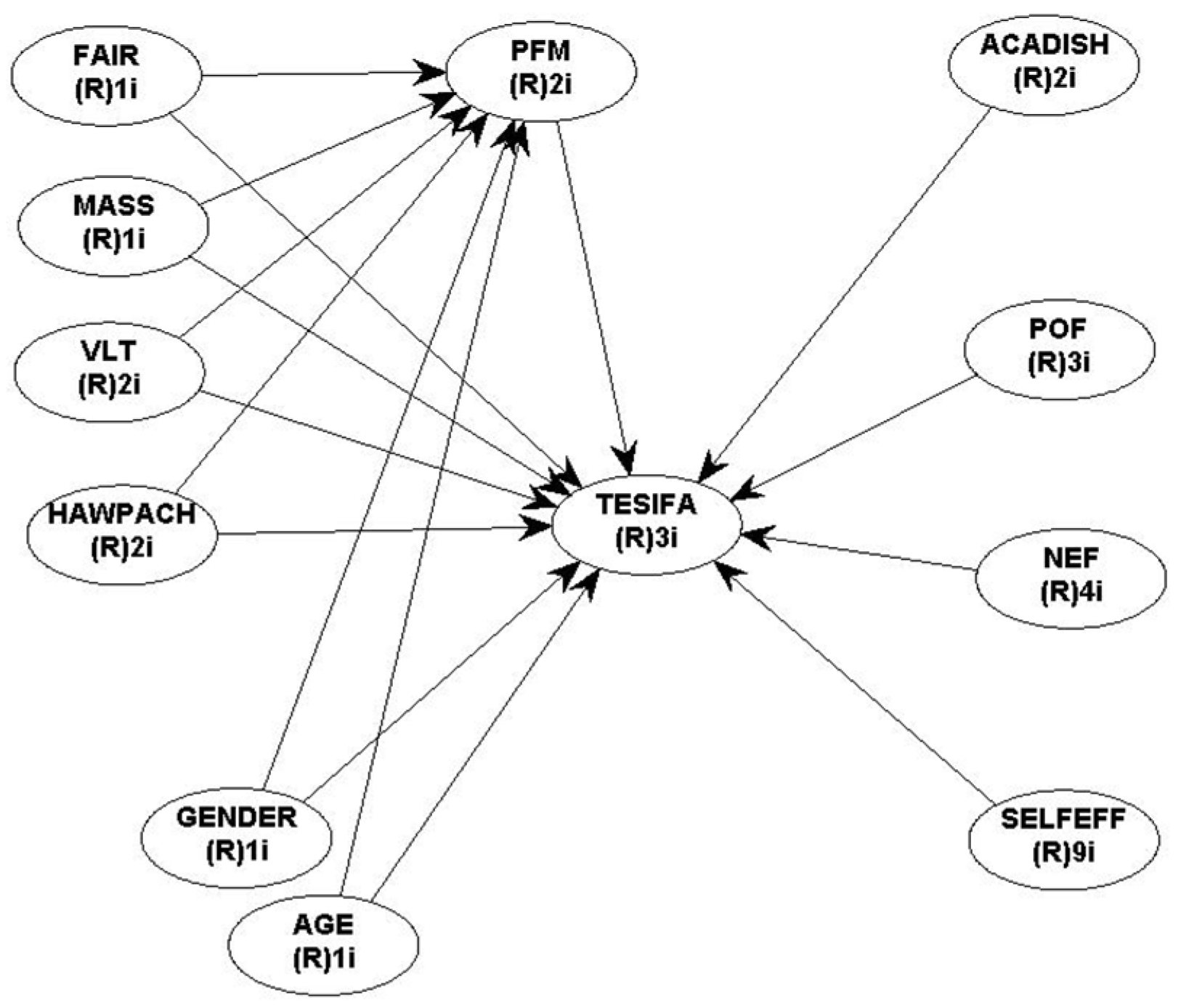

| Direct Effects | Indirect Effects | Direct Effect Sizes (f2) | Total Effects (Direct Effect + Indirect Effect via Preoccupation for Money) | |||

|---|---|---|---|---|---|---|

| Preoccupation for Money | TESIFA | TESIFA | Preoccupation for Money | TESIFA | PA | |

| Preoccupation with money | − | 0.100 * (0.011) | 0.022 | 0.100 * (0.011) | ||

| FAIR | 0.090 * (0.021) | 0.048 (0.137) | 0.009 (0.387) | 0.015 | 0.005 | 0.057. (0.097) |

| MASS | 0.353 *** (<0.001) | 0.093 * (0.017) | 0.035 (0.129) | 0.141 | 0.018 | 0.129 ** (0.002) |

| HAWPACH | 0.085 * (0.026) | −0.079 * (0.036) | 0.009 (0.392) | 0.007 | 0.006 | −0.071. (0.054) |

| VLT | 0.099 * (0.013) | 0.058 (0.096) | 0.010 (0.376) | 0.014 | 0.016 | 0.068. (0.063) |

| Gender Male Female | Reference −0.128 ** (0.002) | Reference −0.083 * (0.030) | Reference −0.013 (0.341) | 0.019 | 0.014 | Reference −0.096 * (0.015) |

| Age | 0.040 (0.181) | −0.105 ** (0.008) | 0.004 (0.449) | 0.003 | 0.015 | −0.101 * (0.011) |

| ACADISH | − | 0.296 *** (<0.001) | − | − | 0.119 | 0.296 *** (<0.001) |

| NEF | − | −0.164 *** (<0.001) | − | − | 0.047 | −0.164 *** (<0.001) |

| POF | − | −0.062. (0.081) | − | − | 0.008 | −0.062. (0.081) |

| SELFEFF | − | −0.191 *** (<0.001) | − | − | 0.048 | −0.191 *** (<0.001) |

| R2/ Adjusted R2 | 20%/19% | 31.8%/30.3% | − | − | − | − |

| Direct Effects | Indirect Effects | Direct Effect Sizes (f2) | Total Effects (Direct Effect + Indirect Effect via Preoccupation for Money) | |||

|---|---|---|---|---|---|---|

| Preoccupation for Money | PA | PA | Preoccupation for Money | PA | PA | |

| Preoccupation with money | − | 0.139 *** (<0.001) | − | 0.040 | 0.139 *** (<0.001) | |

| FAIR | 0.090 * (0.021) | 0.017 (0.354) | 0.012 (0.346) | 0.015 | 0.001 | 0.029 (0.255) |

| MASS | 0.353 *** (<0.001) | −0.015 (0.365) | 0.049. (0.058) | 0.141 | 0.003 | 0.034 (0.223) |

| HAWPACH | 0.085 * (0.026) | −0.110 ** (0.003) | 0.012 (0.353) | 0.007 | 0.021 | −0.099 * (0.013) |

| VLT | 0.099 * (0.013) | 0.122 ** (0.006) | 0.014 (0.331) | 0.014 | 0.022 | 0.136 *** (<0.001) |

| Gender Male Female | Reference −0.128 ** (0.002) | Reference −0.165 *** (<0.001) | Reference −0.018 (0.285) | 0.019 | 0.046 | Reference −0.183 *** (<0.001) |

| Age | 0.040 (0.181) | 0.131 ** (0.001) | 0.006 (0.429) | 0.003 | 0.023 | 0.137 *** (<0.001) |

| ACADISH | − | 0.376 *** (<0.001) | − | − | 0.180 | 0.376 *** (<0.001) |

| NEF | − | −0.088 * (0.023) | − | − | 0.017 | −0.088 * (0.023) |

| POF | − | 0.026 (0.276) | − | − | 0.003 | 0.026 (0.276) |

| SELFEFF | − | 0.002 (0.486) | − | − | 0.000 | 0.002 (0.486) |

| R2 /Adjusted R2 | 20%/19% | 34.5%/33% | − | − | − | − |

| Predictor | Preoccupation for Money | Direct Effects | Indirect Effects | Total Effects | |||

|---|---|---|---|---|---|---|---|

| TESIFA | PA | TESIFA | PA | TESIFA | PA | ||

| FAIR | + (*) | None | None | None | None | + (.) | None |

| MASS | + (***) | + (*) | None | None | + (.) | + (**) | None |

| HAWPACH | + (*) | − (*) | − (**) | None | None | − (.) | − (*) |

| VLT | + (*) | + (.) | + (***) | None | None | + (.) | + (***) |

| Gender Male Female | Reference − (***) | Reference − (*) | Reference − (***) | None | None | Reference − (*) | Reference − (***) |

| Age | None | − (**) | + (**) | None | None | − (*) | + (***) |

| Predictor | Tax Evasion and Security Insurance Fraud | Piracy Acceptance |

|---|---|---|

| PFM | + (*) | + (***) |

| ACADISH | + (***) | + (***) |

| NEF | − (***) | − (*) |

| POF | − (.) | None |

| SELFEFF | − (***) | None |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Druică, E.; Vâlsan, C.; Ianole-Călin, R.; Mihail-Papuc, R.; Munteanu, I. Exploring the Link between Academic Dishonesty and Economic Delinquency: A Partial Least Squares Path Modeling Approach. Mathematics 2019, 7, 1241. https://doi.org/10.3390/math7121241

Druică E, Vâlsan C, Ianole-Călin R, Mihail-Papuc R, Munteanu I. Exploring the Link between Academic Dishonesty and Economic Delinquency: A Partial Least Squares Path Modeling Approach. Mathematics. 2019; 7(12):1241. https://doi.org/10.3390/math7121241

Chicago/Turabian StyleDruică, Elena, Călin Vâlsan, Rodica Ianole-Călin, Răzvan Mihail-Papuc, and Irena Munteanu. 2019. "Exploring the Link between Academic Dishonesty and Economic Delinquency: A Partial Least Squares Path Modeling Approach" Mathematics 7, no. 12: 1241. https://doi.org/10.3390/math7121241