Reinsurance treaties are undertaken to reduce risk, but there is a cost attached. In the present section we employ a dividend discount model to determine the available means by which the company is able to pay for reinsurance without reducing the firm’s value, and how this affects risk as measured by the standard deviation of the company value.

5.1. Reinsurance Premium and Dividend Adjustment

We assume the company’s current value is given by its future potential dividend stream, discounted to present value. Let

ρ be the time value of money and assume that dividends are paid at constant rate

d until the cedant’s default, if this occurs. Then the claim surplus process in (

1) must be modified to reflect the dividend payment:

The insurance company will require a specified safety loading

θ to be in effect after the dividend is paid, so the net profit condition (

2) is modified to

In (

18),

Y does not depend directly on

c and

d, only on

through the value of

θ. Since our main interest is in the cost of reinsurance, we will take

c and

d as given. In practice their values will be dependent on policyholders’ willingness to pay and the choice of safety loading

θ. Note also that the values of

c in (

1) and (

18) must differ if

and the same safety loading is used in both cases.

The ruin time of the company is now given by

, for an initial capital level

, and the cumulative dividend income by

The company is subsequently valued at

Now suppose a reinsurance scheme is incorporated, for which the cedant pays the reinsurer a premium which is constant in time at rate

r. As a result of the consequent change in risk profile of the insurer, policyholders may be willing to pay an increased premium

, while shareholders will accept a reduced dividend

. The reinsured claim surplus process is then given by

where the nondecreasing process

R represents the reduction in claims due to reinsurance. This is given by (

4) in the case of an EOL treaty, and by (

5) for the LCR treaty. The reinsured claim surplus process has ruin time

, and the dividend income Equation (

20) and the valuation Equation (

21) are then modified by replacing

d and

with

and

respectively. Thus

Since the aim of reinsurance is to prevent, or at least delay ruin, it is natural to require that

for all

. For the LCR and EOL reinsurance schemes, this can only be guaranteed if

, and so we make this assumption. Thus for a given new premium rate

and dividend rate

, the largest reinsurance premium the cedant would consider paying is

. When this condition holds, (

22) becomes

which does not depend on

or on

, and the valuation Equation (

23) becomes

where

does not depend on

or on

. In particular, reducing

reduces

.

Adopting a “utility indifference” rationale ([

13,

14]) whereby the reinsurance contract is beneficial for the cedant if its utility with reinsurance exceeds that without, and “utility” is taken to be the net present value of dividend income received, acceptable reinsurance contracts must satisfy

. So to find the maximal reinsurance premium

that the cedant is willing to pay for a reinsurance treaty

R, we should maximize

over all

for which

.

Since

is increasing in

, it follows immediately from (

21) and (

25) that the maximizing value of

is given by

and the corresponding maximal reinsurance premium by

One interesting aspect of (

27) is that the factor

depends on

u and

θ only, and not on

d, and so represents the proportion of the dividend that may be used to pay the reinsurance premium for a given safety loading. Thus if the reinsurer demands a premium which does not exceed

, then, without reducing the value of the firm, the premium can be paid for entirely with a reduction in dividend. However if the insurance premium is in excess of

, then the insurance company will be forced to turn to policyholders to pay part of the cost if a reduction in the value of the firm is to be avoided.

The calculation of

and

amounts to the evaluation of the Laplace transforms of

and

, where

represents the ruin time under whichever type of reinsurance is being considered. For LCR,

, and for EOL,

as specified in

Section 4.1 and

Section 4.2. Currently there are no known theoretical results for the Laplace transform of

, and it would be of interest and useful to derive them

2.

In general the Laplace transforms need to be approximated by some means. We did this by using the simulations to directly estimate

for large

T, and then observing that

This applies equally well to

. As a check on this, and to decide on the number of simulations needed for sufficient accuracy, we also used Proposition

A1 in the

Appendix, which shows that

where

and

is an independent exponential random variable with mean

. The right hand side of (

30) can be estimated by simulating the paths of

Y. (

30) also holds if

Y and

are replaced by

and

, so the Laplace transform of

can be estimated by the same means. Then

and

can be evaluated by

and

5.2. Choice of Parameters

Below we report on simulations for some of the derived quantities in the present section. We want to give reasonably realistic simulation scenarios, so we have to make a credible choice of parameter values. There seems to be little guidance in the literature for doing this. In the end, the values we decided on are loosely based on some given in [

21,

22] together with some pragmatic considerations.

To start with, the initial reserve level u is only determined up to a scale constant. It can be thought of as units of $10 k, or $1 m, etc., as convenient. The mean claim size µis then to be taken relative to u.

The time unit we set to be 0.01 years = 3.65 days, so values of

100, 500, 1000, as designated in

Section 3.3 and in the finite horizon scenarios considered in

Section 5.5, correspond to 1 year, 5 years, 10 years. The time value of money is set at

. Taken together with the time unit specified, this corresponds to a discount rate of

p.a. To approximate the infinite time horizon we take

in (

29) so that the error of the asymptotic approximation to (

30) is bounded by

.

Safety loadings are taken to be

, 0.025, 0.05, 0.075, 0.1. The expected claim size

and claims rate of

are again as designated in

Section 3.3. Thus claims accumulate on average an amount of 2 units per unit time length. This again is taken relative to

u. The rate of premium inflow

c and the dividend rate

d need not be specified because as shown in

Section 5.1, only the difference

is relevant for the computations in the present section, and this is fixed by our choice of

θ,

λ and µ.

How to decide on the value of

L for the EOL reinsurance is also problematic. Again we could find little guidance in the literature

3. We want to maintain comparability between the LCR and EOL schemes as far as possible. The values of

L used in

Table 4,

Table 5 and

Table 6 (finite horizon cases) were chosen so that the expected claim surpluses were equal at the specified expiration time

T of the reinsurance treaties. These were found by solving (

17). For the infinite time horizon problem, choosing

L by first solving (

17) and then letting

, would render EOL reinsurance equivalent to no reinsurance, as

when

. Hence in order to maintain comparability with LCR, for the simulations in the next section we chose

L as a percentile of the claim distribution in such a way that the proportion of the dividend available to support the reinsurance premium was approximately the same between the EOL and LCR schemes.

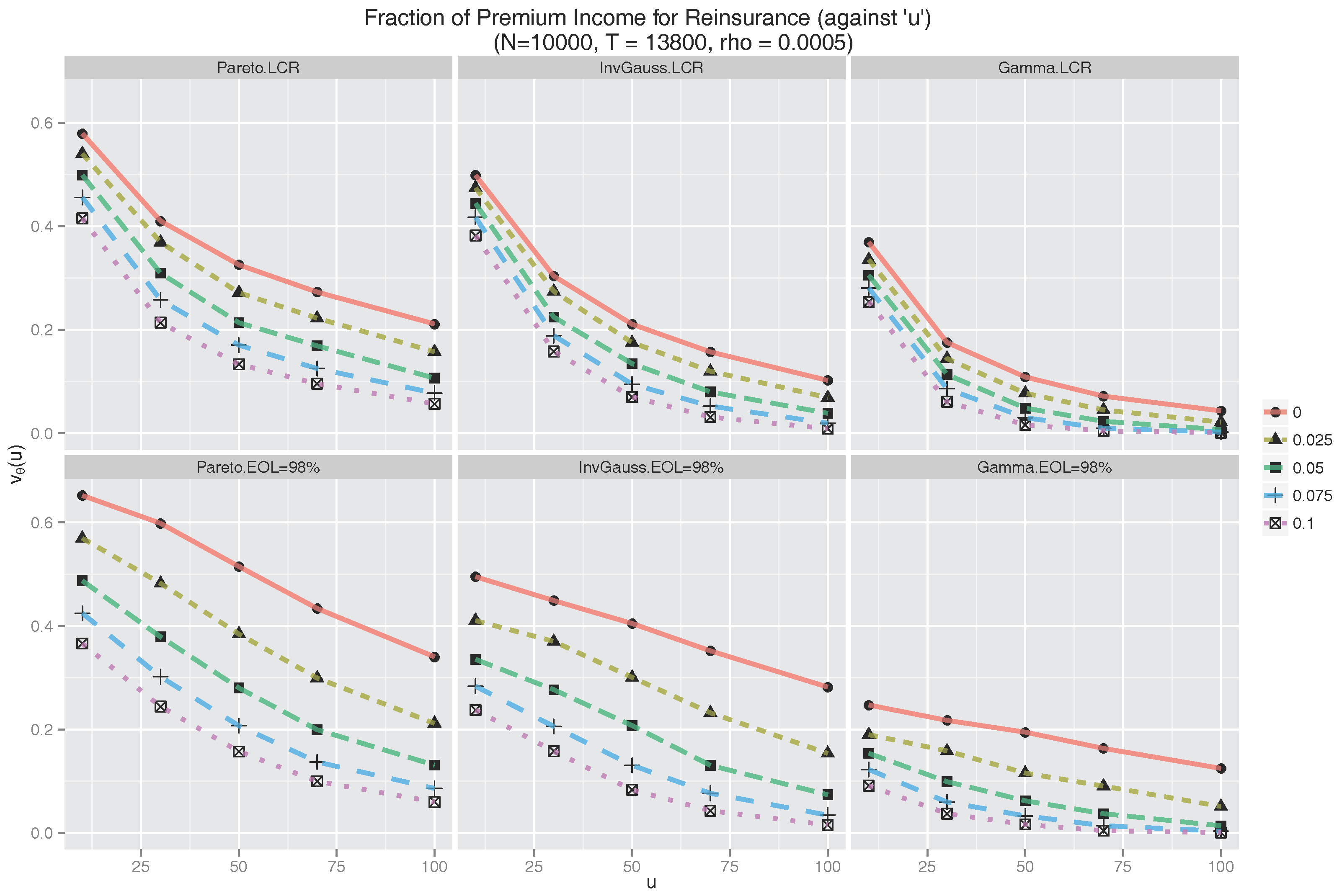

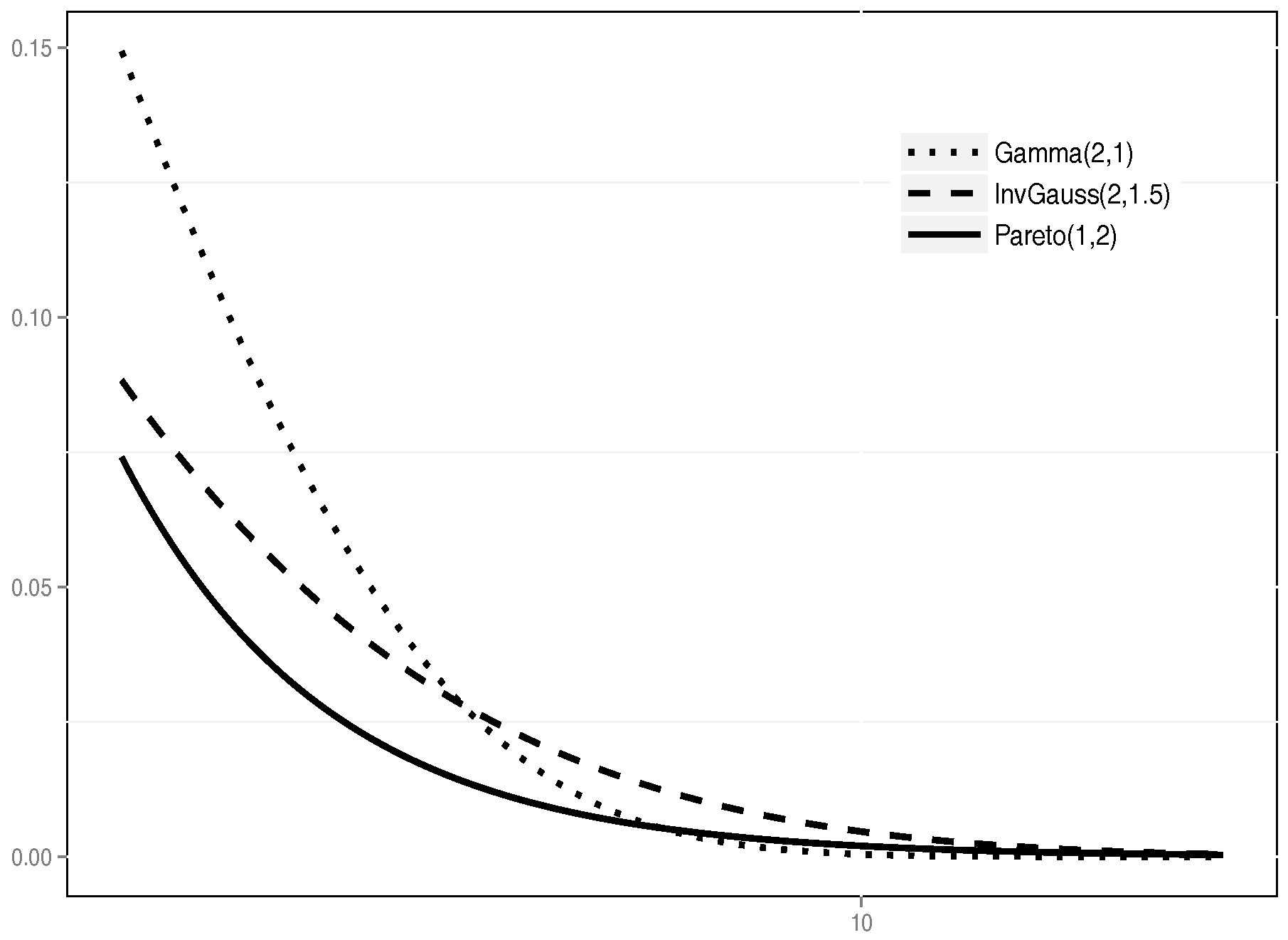

5.3. Proportion of Dividend Paid for Reinsurance

Figure 6 exhibits the graph of

(see (

32)) for each of the LCR and EOL treaties under each of the three claims distributions. For the EOL treaty,

L is taken as the 98th percentile of the claims distribution. This percentile was chosen after some experimentation to give similar values for

in the LCR and EOL cases.

In both the LCR and EOL frameworks, we observe from

Figure 6 that

varies noticeably across

u levels and distributions. As the reserve level increases from

to

, the proportion of the dividend the company is willing to pay for reinsurance drops significantly, for each value of

θ. The rate of decrease is larger for smaller values of

u for LCR but rather uniform across

u values for EOL. As the safety loading increases, the insurance company is only willing to apportion a smaller part of the dividend toward reinsurance.

It is interesting to note that is bounded by in all settings, indicating that the cedant is unwilling to pay more than of the dividend to reinsurance despite the high risk of ruin in cases when θ is low and u is low (e.g., and ). In this high risk region, ruin, though being likely (certain when ), will, with sufficient frequency, occur far enough into the future that the dividend stream lost due to ruin is negligible. Hence the cedant finds it unneccesary to dedicate more than 65% of dividend to reinsurance.

Since we have adopted a “utility indifference” rationale in calculating the premium, the expected values of the company, with and without reinsurance, are forced to be equal. This can also be readily checked: from (

21), (

23) and (

31), we have

5.4. Standard Deviation of Dividend Income

In this section we compare the two reinsurance treaties, and the case with no reinsurance, with respect to the standard deviation of the dividend income. This will provide insight into the stabilising effect, or otherwise, of the reinsurance, which is a primary concern of the cedant company.

To calculate the standard deviation of the dividend income, observe that

while for the reinsured portfolio, by (

26),

where

is the coefficient of variation of

and

is the coefficient of variation of

. Observe that the change in standard deviation is by a factor

which, as for

, depends on

u and

θ but not on

d. Values of

are summarised in

Figure 7, which shows a clear reduction in the standard deviation of the dividend income received, compared with the case of no reinsurance, across all distributions, reserve levels and safety loadings, for both LCR and EOL. The reduction is most significant under the Pareto claim distribution, lessening as the tail of the claim distribution becomes lighter.

As the safety loading θ increases, in almost all cases, the amount of variance reduction increases. However, looking across u levels, two clearly different trends emerge for LCR and EOL reinsurances. In the EOL setting, decreases across all scenarios. In contrast, for LCR, increases initially except for larger values θ in the Pareto case. Interestingly, small values of u exhibit the least variance reduction for EOL across all distributions, but, outside of the Pareto case, the most variance reduction for LCR, for the chosen parameters.

Overall, it may be adjudged that reinsurance has a non-trivial stabilising effect on the value of the company, particularly for heavier tailed claims distributions.

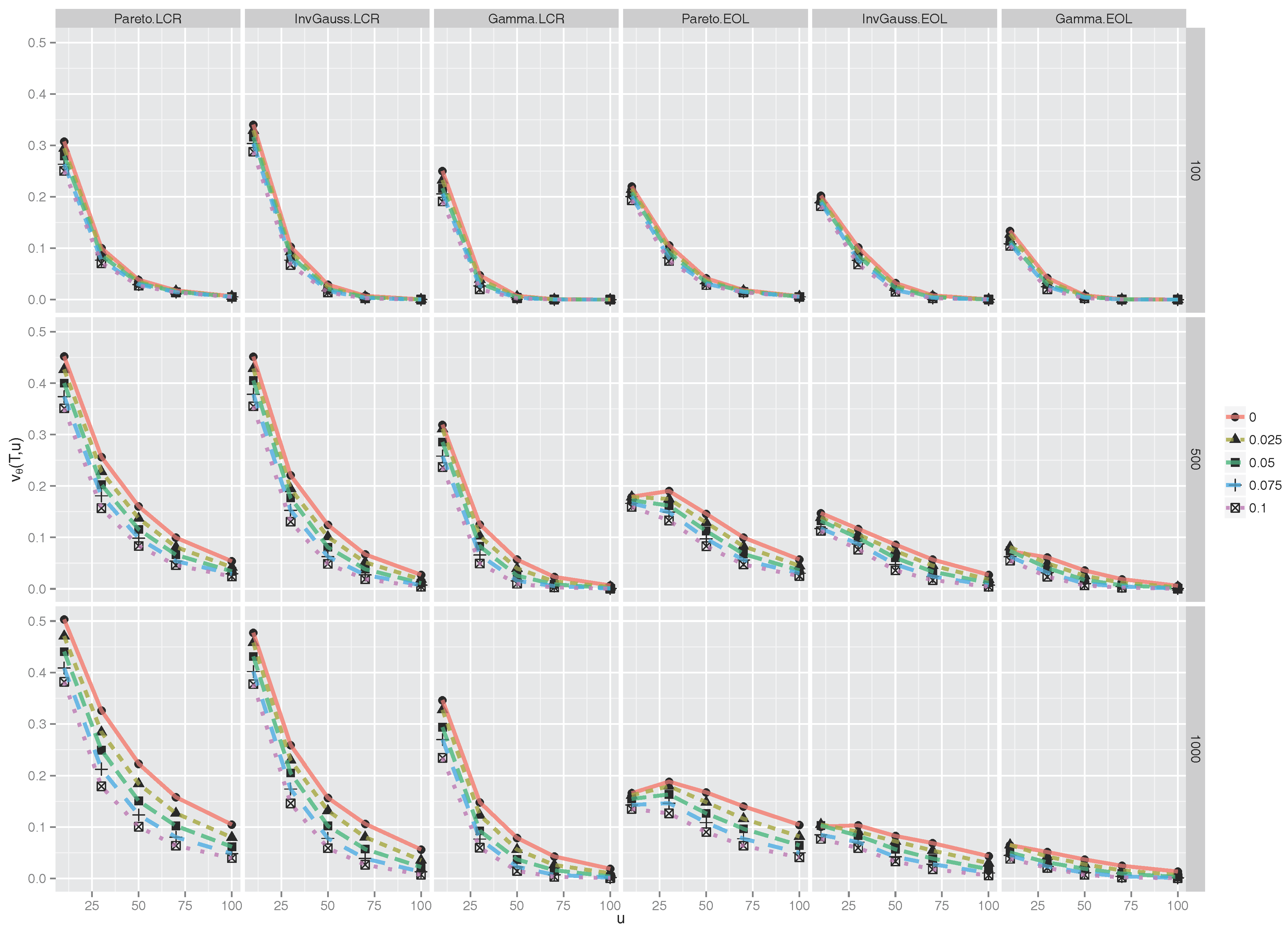

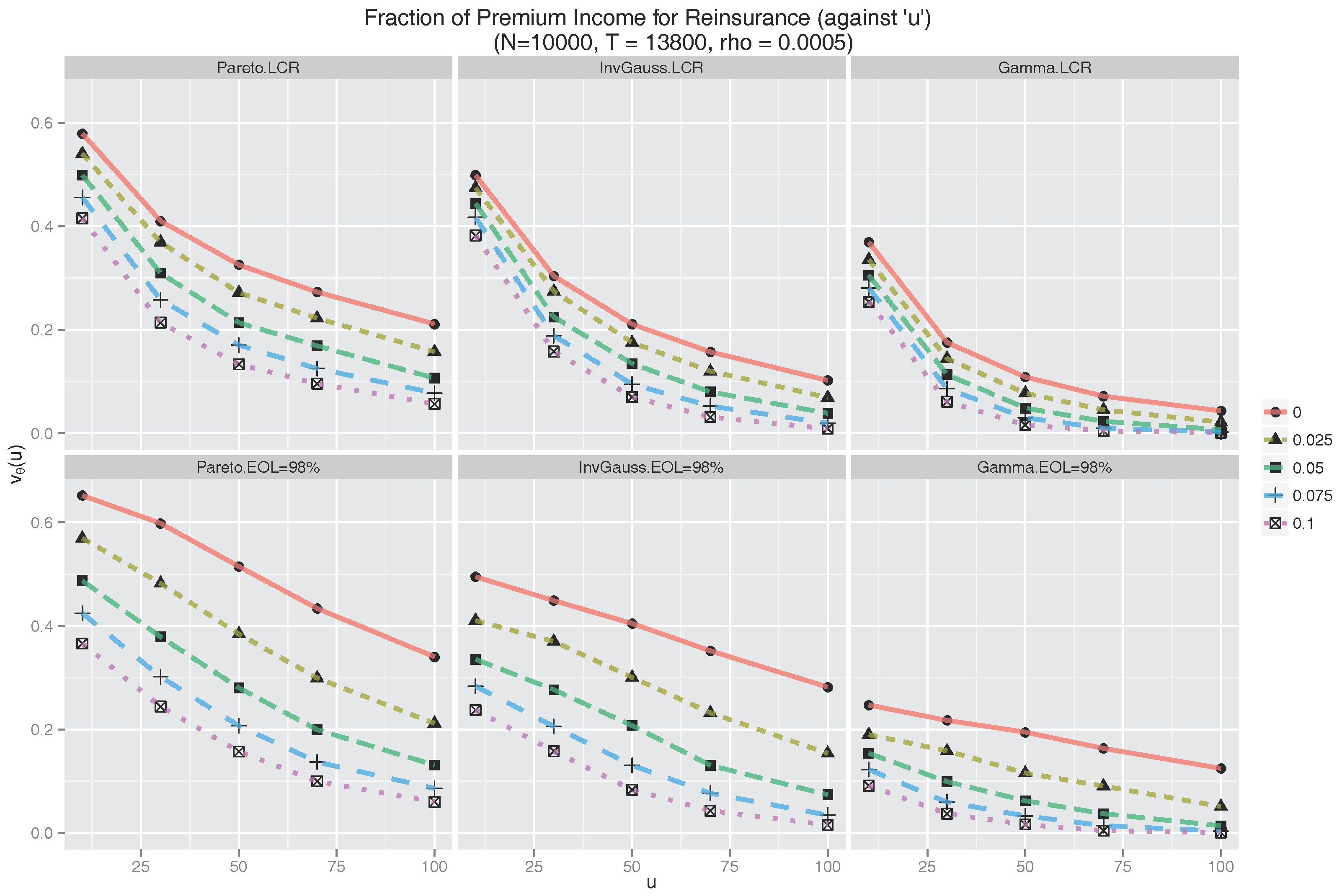

5.5. Dividend Adjustment and Reinsurance Premium, Finite Horizon

While it may be useful for planning and evaluation purposes to consider infinite horizon results, in practice a reinsurance treaty is not taken over an infinite time horizon, nor are dividends paid at a constant rate forever. Thus it is also prudent to value the company over a finite time horizon. In this case we should take into account both the value of the dividends paid,

, up to the expiration time

T of the reinsurance treaty, and also the value of the (liquidated) portfolio,

, at time

T. Thus, we replace (

21) for the uninsured process with

Similarly, for the reinsured process, (

23) is replaced by

By analogy with the infinite horizon case, we now wish to find the maximal reinsurance premium the cedant is willing to pay subject to

a.s,

and

4.

Applying the same logic as in

Section 5.1, we find that

is given by (

24) and does not depend on

. Since

for all

, the condition

is automatically satisfied. Thus, arguing as before, the maximizing dividend rate

and the corresponding maximal reinsurance premium

(now both depending on

T and

u) are found by equating

and

in (

35) and (

36). Setting

(where the second equality in (

37) follows from (

A1) in the

Appendix), we find that

Observe that , and, as in the infinite horizon case, depends on u and θ but not on d. Thus, again, only a fixed proportion of the dividend is available to pay for reinsurance if the value of the firm is not to be reduced.

We simulated

with the parameters kept the same as in

Table 1,

Table 2 and

Table 3 for LCR reinsurance and

Table 4,

Table 5 and

Table 6 for EOL reinsurance. As mentioned previously, this is done to maintain comparability between the two reinsurance schemes. In particular

L is not the 98-th percentile, as in the infinite horizon case, but is chosen according to (

17). The results are summarized in

Figure 8, which displays several interesting features.

For both types of reinsurance, the value of

is slightly higher for a Pareto claim distribution than for an Inverse Gaussian, which is greater again than for a Gamma claim distribution. This is consistent with the results for the ruin times in

Table 1,

Table 2,

Table 3,

Table 4,

Table 5 and

Table 6. It is notable that for

,

, regardless of

θ and the claim distribution, the cedant is essentially unwilling to commit any of the dividend payment to reinsurance. Observe also that when the ruin probabilities under LCR and EOL are comparable in

Table 1,

Table 2,

Table 3,

Table 4,

Table 5 and

Table 6, the values of

are also comparable, whereas when the ruin probability under LCR is smaller than under EOL, for example when

across all distributions, the cedant is able to contribute a larger portion of the dividend to reinsurance for LCR than EOL.

Considered as a function of

u,

is decreasing and apparently convex in the case of the LCR treaty across all values of

θ and

T and all distributions, and this is also true for the EOL treaty in the

case. For larger

T,

is neither decreasing nor convex for EOL. Indeed for small

u,

is seen to be increasing. As a function of

T, for fixed

θ and

u,

is increasing for the LCR treaty. For the EOL treaty this is not the case since, for example,

is decreasing for

. Finally, for fixed

T and

u, the influence of the safety loading

θ is much less pronounced than in

Figure 6.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}