An Empirical Study of User Adoption of Cryptocurrency Using Blockchain Technology: Analysing Role of Success Factors like Technology Awareness and Financial Literacy

Abstract

:1. Introduction

2. Literature Review

2.1. Blockchain Technology

2.2. The Unified Theory of Acceptance and Use of Technology 2

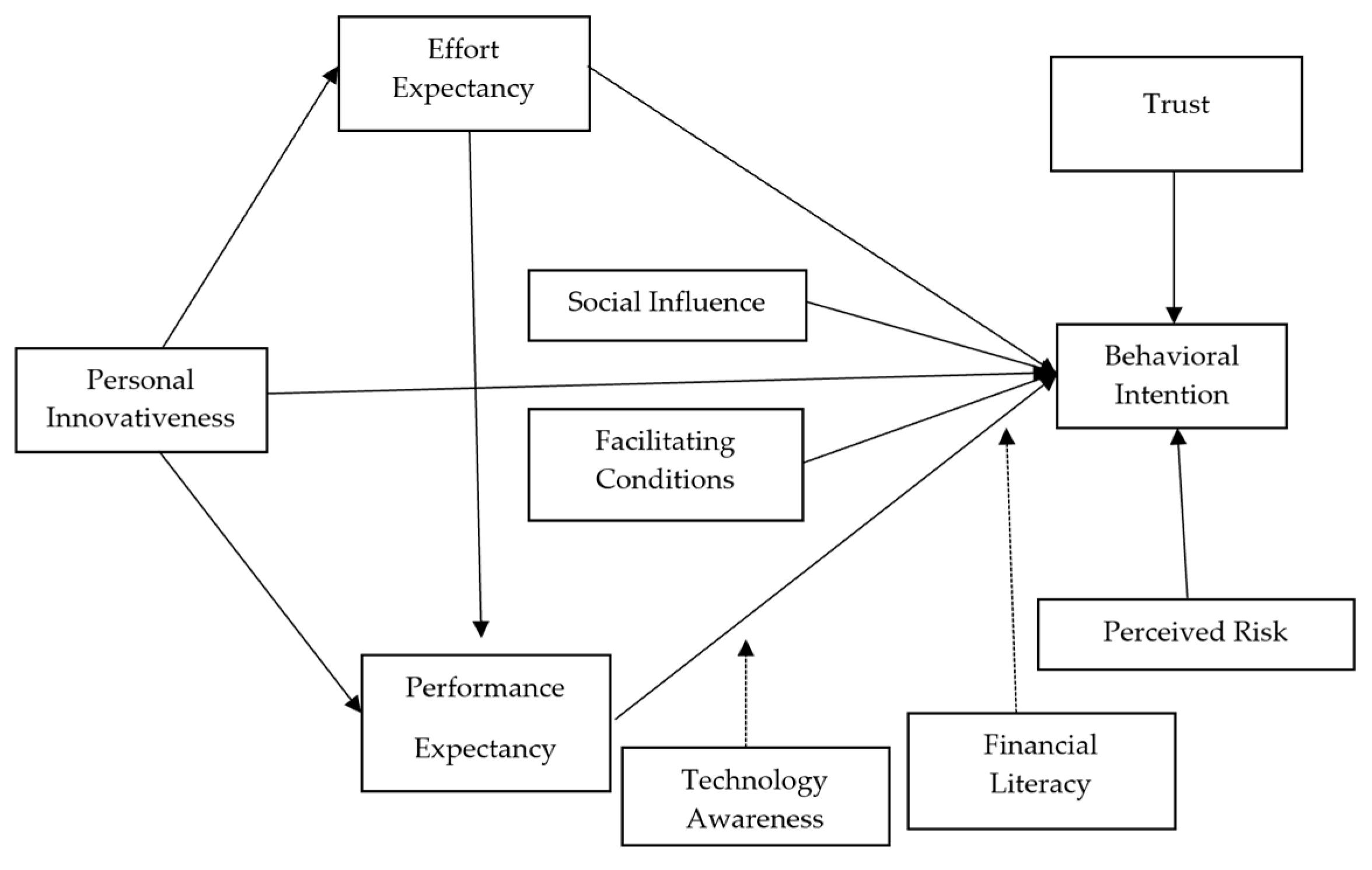

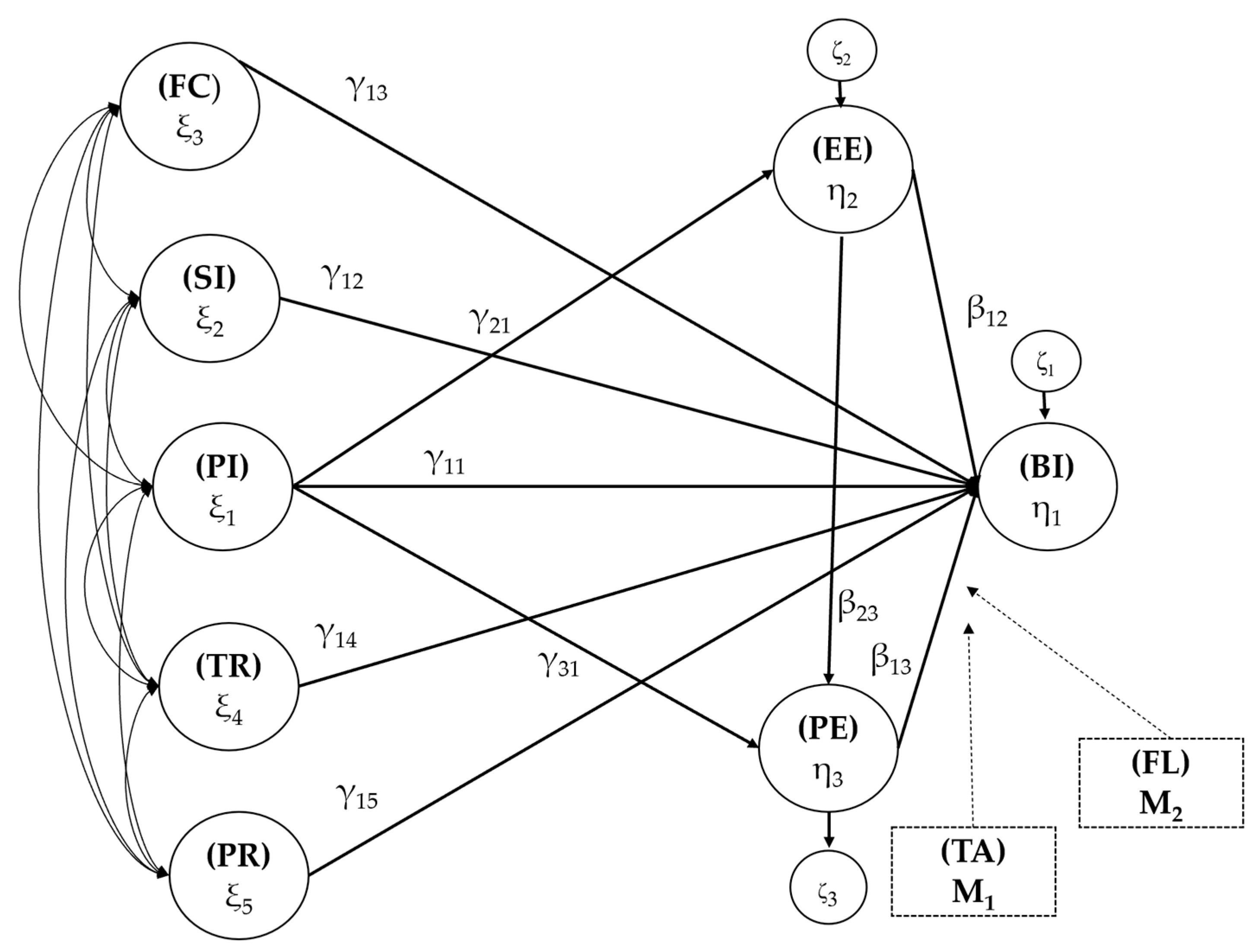

3. Hypotheses Development and Conceptual Model

3.1. Personal Innovativeness

3.2. Performance Expectancy and Effort Expectancy

3.3. Social Influence

3.4. Facilitating Conditions

3.5. Trust

3.6. Perceived Risk

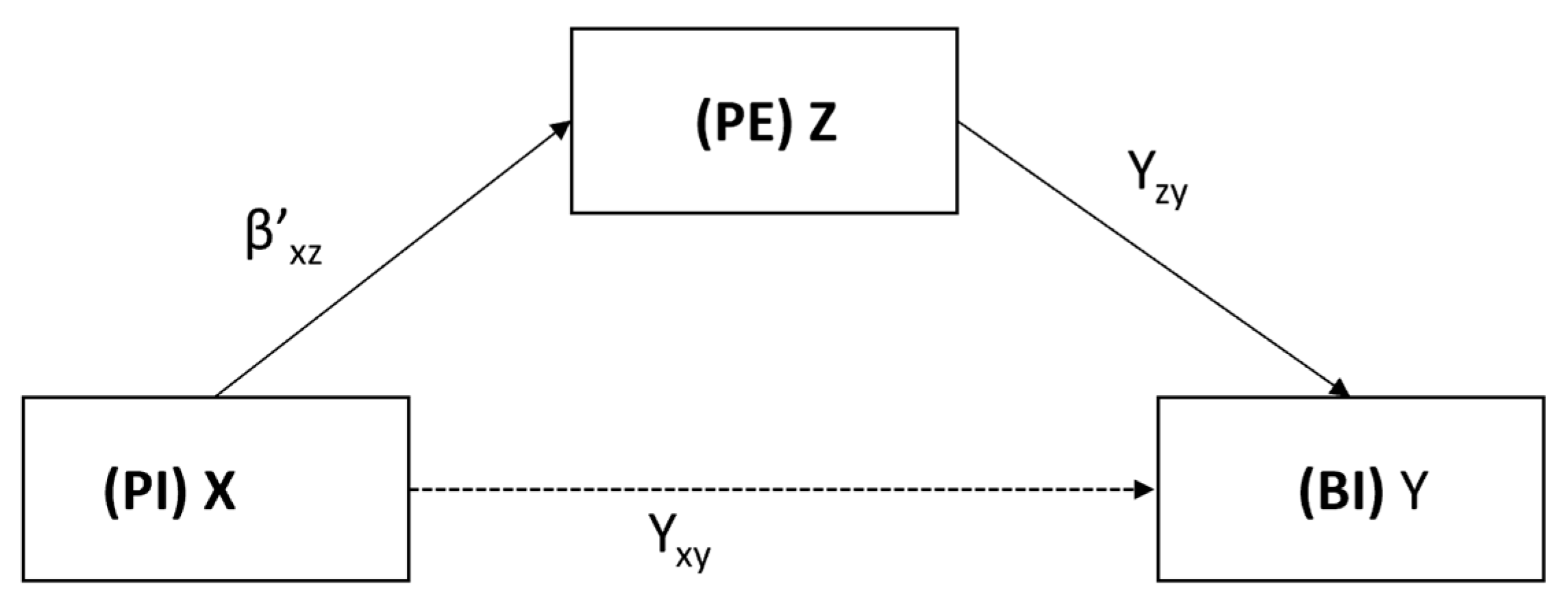

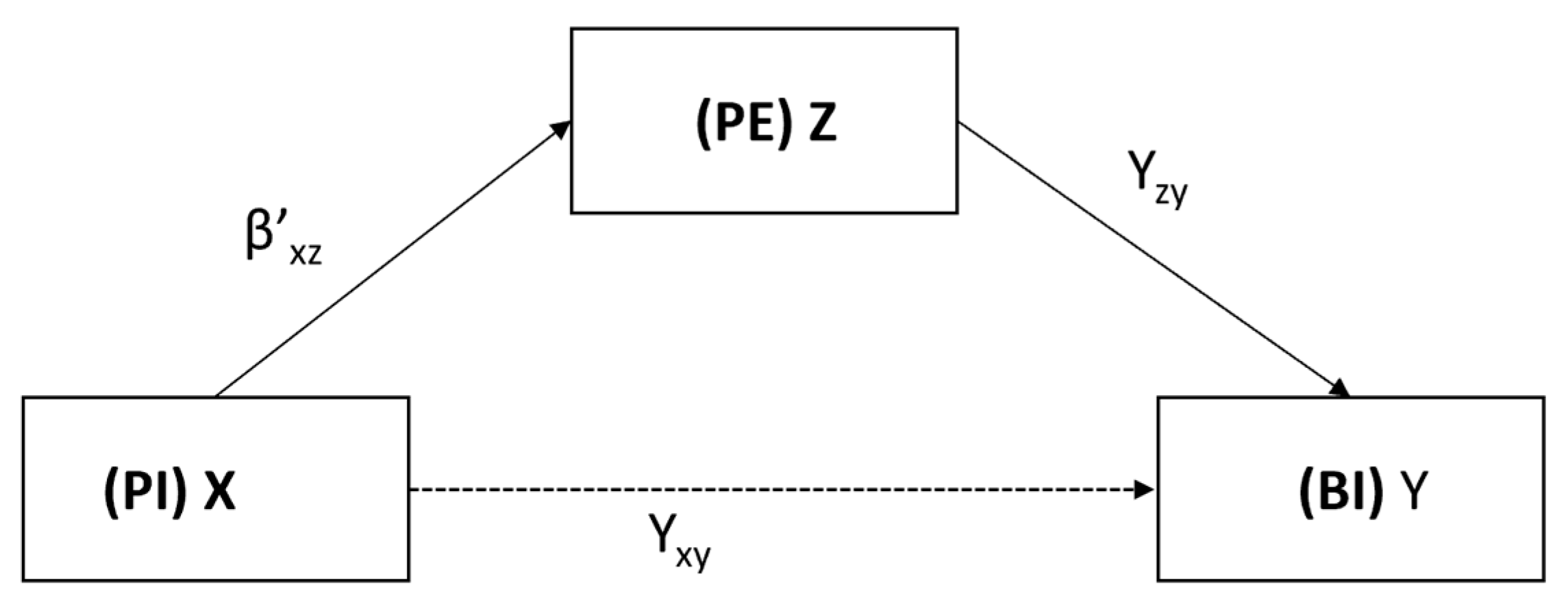

3.7. The Mediating Role of Performance Expectancy

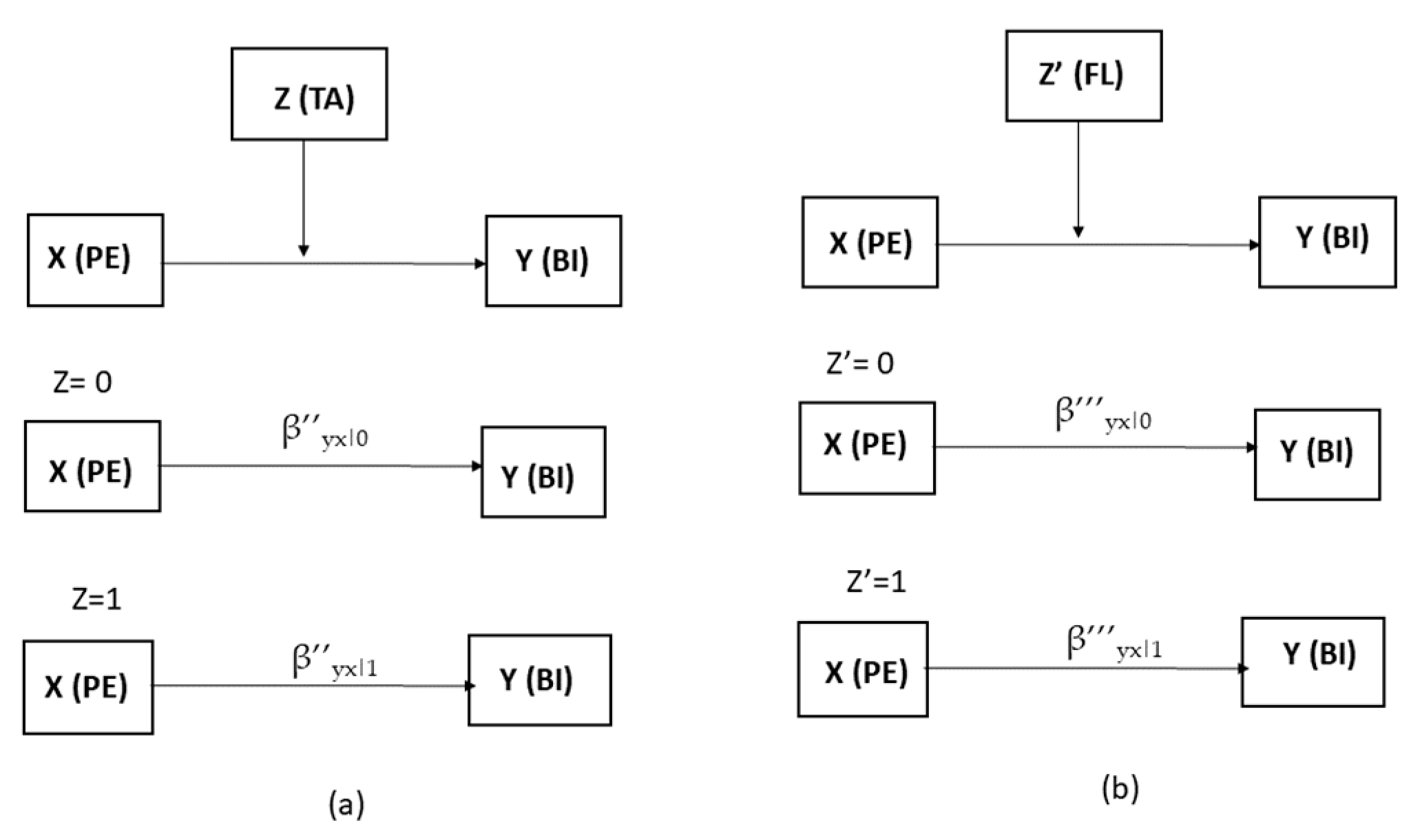

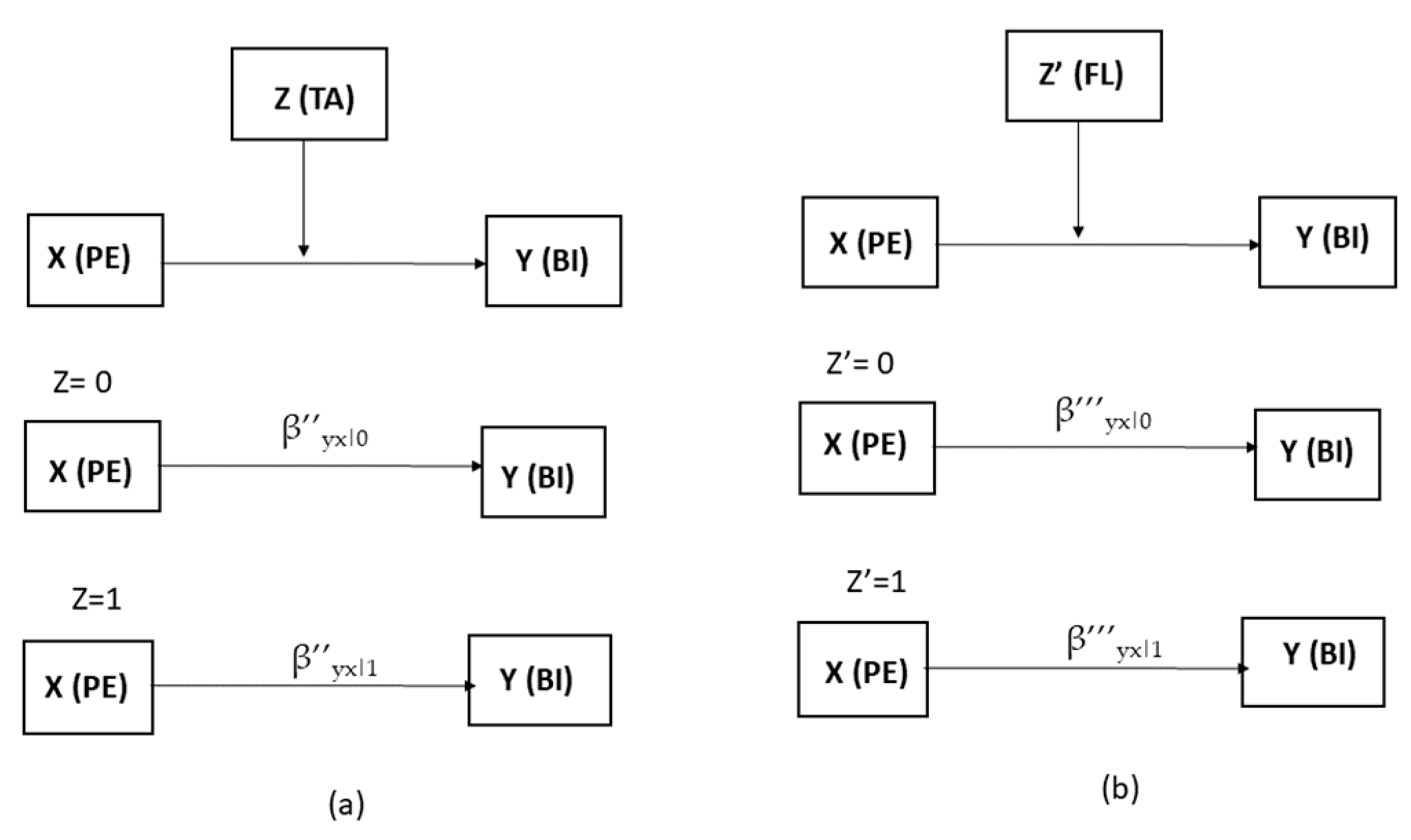

3.8. The Moderating Role of Technology Awareness

3.9. The Moderating Role of Subjective Financial Literacy

4. Methodology

5. Data Analysis and Results

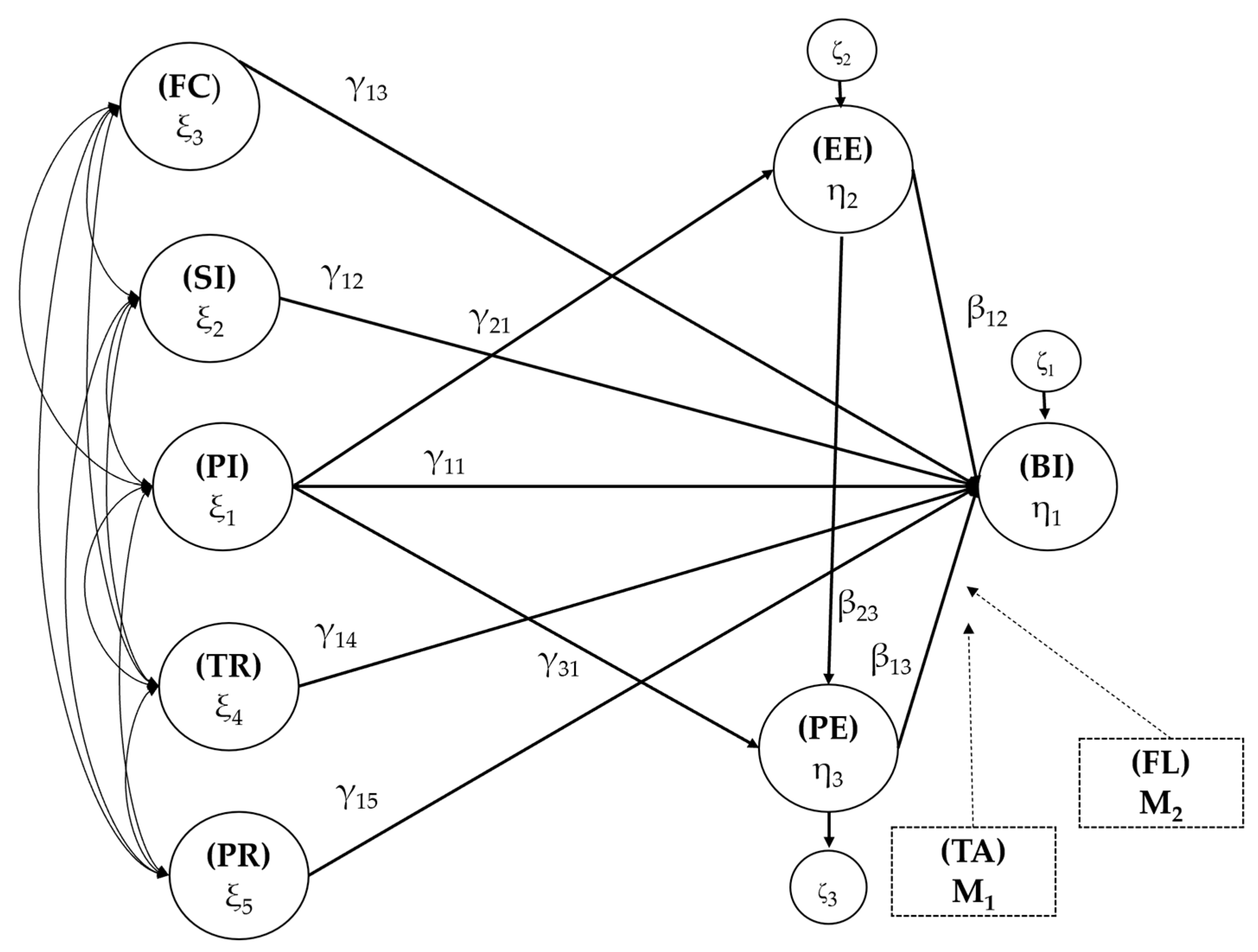

5.1. Structural Equation Modeling

5.2. Non-Response and Common Method Bias

5.3. Reliability and Validity

5.4. Model Fit

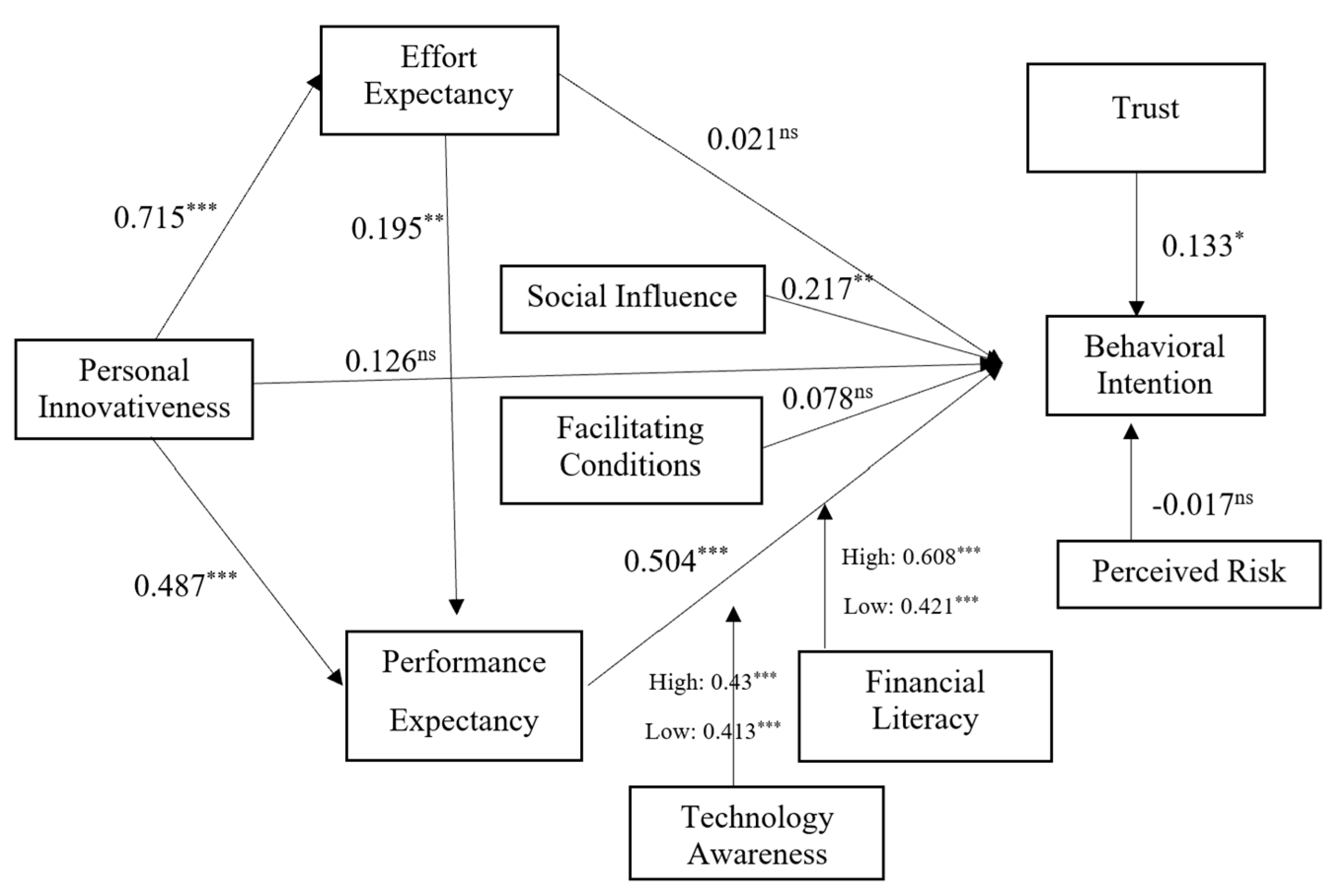

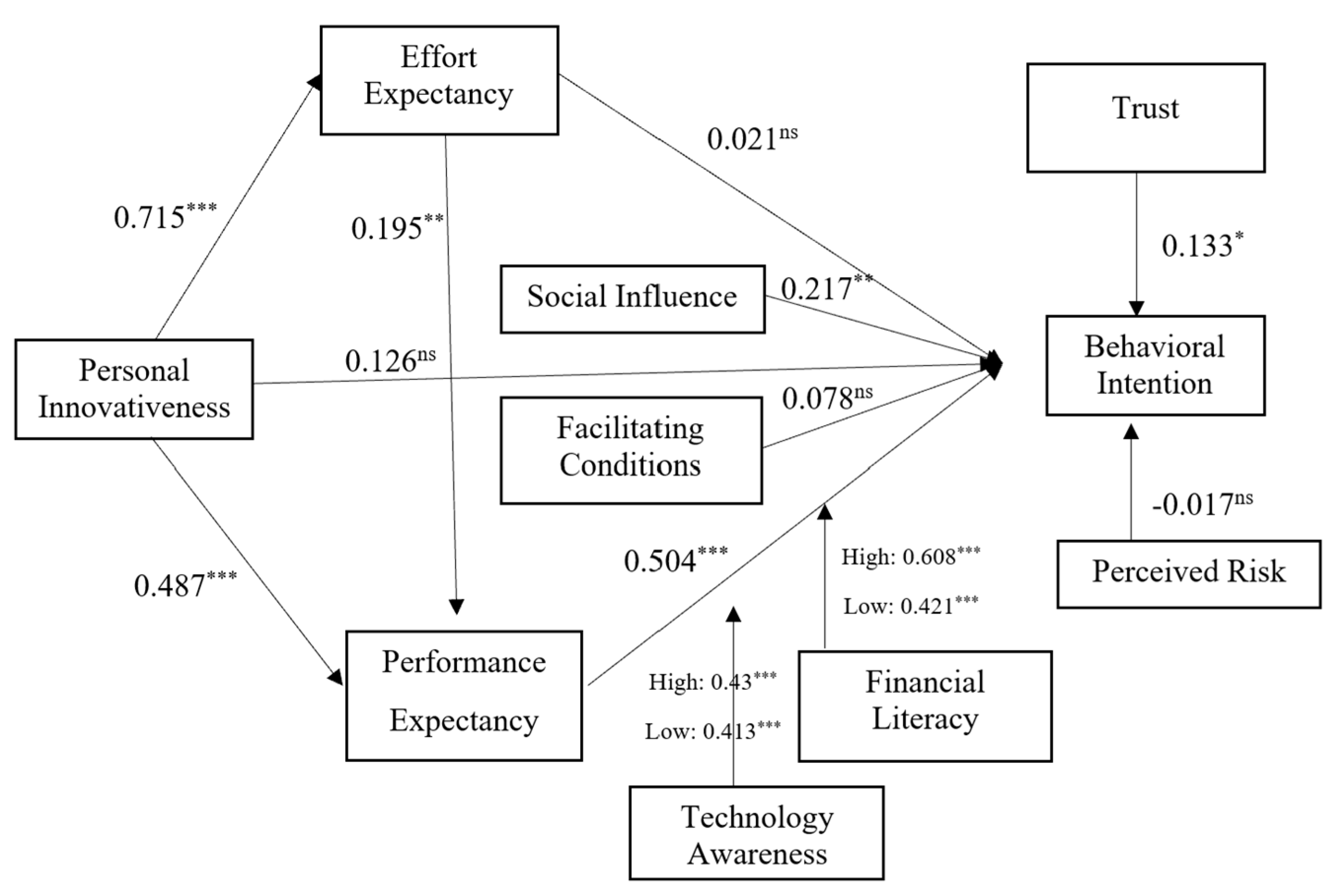

5.5. Hypothesis Testing Results

6. Discussion

7. Implications

7.1. Theoretical Implications

7.2. Managerial Implications

8. Conclusions

9. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Constructs | Item Code |

|---|---|

| Performance expectancy (PE) | |

| Using cryptocurrencies will increase opportunities to achieve important goals for me. | PE1 |

| Using cryptocurrencies would increase my work productivity (accepting payments from peers/clients in cryptocurrencies is easier as no 3rd party like banks are involved) | PE2 |

| Using cryptocurrencies will increase my standard of living. | PE3 |

| Using cryptocurrencies would enable me to perform my payments more quickly. | PE4 |

| Effort expectancy (EE) | |

| It will be easy for me to learn how to use cryptocurrencies. | EE1 |

| Using cryptocurrencies will be clear and understandable for me. | EE2 |

| It will be easy for me to become an expert in the use of cryptocurrencies. | EE3 |

| Personal innovativeness (PI) | |

| I heard about new information technology. I would look for ways to experiment with it. | PI1 |

| Among my peers, I am the first one to try out new information technologies | PI2 |

| I like to experiment with new technologies | PI3 |

| Trust (TR) | |

| I trust Cryptocurrencies to be reliable. | TR1 |

| I trust Cryptocurrencies to be secure. | TR2 |

| I believe Cryptocurrencies are trustworthy. | TR3 |

| I trust Cryptocurrencies. | TR4 |

| Perceived risk (PR) | |

| Using cryptocurrency is risky. | PR1 |

| There is too much uncertainty associated with the use of cryptocurrencies | PR2 |

| Compared with other currencies or investments, cryptocurrencies are riskier. | PR3 |

| Facilitating conditions (FC) | |

| I have the necessary resources to use cryptocurrencies. | FC1 |

| I have the necessary knowledge to use cryptocurrencies | FC2 |

| I can get help if I have difficulty using cryptocurrencies | FC3 |

| Social influence (SI) | |

| People (family, friends) who are important to me think that I should use cryptocurrency. | SI1 |

| People who influence my behaviour think that I should use cryptocurrency | SI2 |

| People whose opinions that I value would like that I use cryptocurrency. | SI3 |

| Financial literacy (FL) | |

| I rate my overall financial knowledge on a scale of 1 to 7 as | FL1 |

| I feel I have a high capacity to deal with financial matters | FL2 |

| I have a good level of financial knowledge | FL3 |

| Technology awareness (TA) | |

| I follow news and development about cryptocurrencies | TA1 |

| I seek advice on blogs, social media or about cryptocurrency products or services. | TA2 |

| I discuss with friends and people around me about cryptocurrencies. | TA3 |

| I read about Cryptocurrency usage in newsletters or articles. | TA4 |

| I hear about cryptocurrency on TV, podcasts or the radio. | TA5 |

| Behavioural intention (BI) | |

| I intend to periodically use cryptocurrency. | BI1 |

| I want to use the services where can pay by cryptocurrency. | BI2 |

| I want to use cryptocurrency to pay for my use. | BI3 |

| Awareness test | |

| I have never heard of any digital currencies like cryptocurrencies | |

| I know basic details about cryptocurrencies | |

| I know what to do with cryptocurrencies | |

| I am aware of and know how to use cryptocurrencies |

References

- Nofer, M.; Gomber, P.; Hinz, O.; Schiereck, D. Blockchain. Bus. Inf. Syst. Eng. 2017, 59, 183–187. [Google Scholar] [CrossRef]

- Du, M.; Ma, X.; Zhang, Z.; Wang, X.; Chen, Q. A Review on Consensus Algorithm of Blockchain. In Proceedings of the 2017 IEEE International Conference on Systems, Man, and Cybernetics (SMC), Banff, AB, Canada, 5–8 October 2017; ISBN 978-1-5386-1645-1. [Google Scholar]

- Norton, B.; Kaduthanum, A. Moving toward a Cashless Society with Crypto Payments. Available online: https://www.tcs.com/what-we-do/industries/banking/white-paper/crypto-payments-currency-future (accessed on 20 April 2023).

- Adrian, T.; Mancini-Griffoli, T. Technology behind Crypto Can Also Improve Payments, Providing a Public Good; International Monetary Fund. Available online: https://www.imf.org/en/Blogs/Articles/2023/02/23/technology-behind-crypto-can-also-improve-payments-providing-a-public-good (accessed on 18 April 2023).

- Guo, Y.; Liang, C. Blockchain Application and Outlook in the Banking Industry. Financ. Innov. 2016, 2, 24. [Google Scholar] [CrossRef]

- Zhao, J.L.; Fan, S.; Yan, J. Overview of Business Innovations and Research Opportunities in Blockchain and Introduction to the Special Issue. Financ. Innov. 2016, 2, 28. [Google Scholar] [CrossRef]

- Nakamoto, S. Bitcoin: A Peer-to-Peer Electronic Cash System. Decentralized Bus. Rev. 2008, 21260. [Google Scholar]

- Nejad, M.G. Research on Financial Innovations: An Interdisciplinary Review. Int. J. Bank Mark. 2022, 40, 578–612. [Google Scholar] [CrossRef]

- Groß, J.; Sandner, P.G.; Klein, M.; Bank, D.; Gross, J.; Sandner, P. The Digital Euro and the Role of DLT for Central Bank Digital Currencies; Venture Capitalist Social Capital View Project Impact of Business Angels on Startup Success View Project May 2020; Frankfurt School Blockchain Center: Frankfurt, Germany, 2020. [Google Scholar]

- Visa Digital Currency: Visa’s Vision for Supporting the Future of Money. Available online: https://www.visa.es/dam/VCOM/regional/na/us/Solutions/documents/visa-digital-currency-overview.pdf (accessed on 17 May 2023).

- MIT Technology Review Insights Cryptocurrency Fuels New Business Opportunities. 2022. Available online: https://www.technologyreview.com/ (accessed on 15 March 2023).

- Chhangani, A. Snapshot: Which Countries Have Made the Most Progress on CBDCs So Far in 2023. Available online: https://www.atlanticcouncil.org/blogs/econographics/which-countries-have-made-the-most-progress-in-cbdcs-so-far-in-2023/ (accessed on 1 June 2023).

- Kosse, A.; Ilaria, M. Gaining Momentum—Results of the 2021 BIS Survey on Central Bank Digital Currencies. Available online: https://www.bis.org/publ/bppdf/bispap125.pdf (accessed on 15 March 2023).

- Berman, N. What Does the Cryptocurrency Decline Mean for Bitcoin Countries? Available online: https://www.cfr.org/in-brief/what-does-cryptocurrency-decline-mean-bitcoin-countries (accessed on 13 February 2023).

- BIS Digital Currencies. Available online: https://www.bis.org/cpmi/publ/d137.htm (accessed on 15 March 2023).

- Venter, H. Digital Currency—A Case for Standard Setting Activity; Australian Accounting Standards Board: Melbourne, Australia, 2016. [Google Scholar]

- Kim, J.J.; Radic, A.; Chua, B.L.; Koo, B.; Han, H. Digital Currency and Payment Innovation in the Hospitality and Tourism Industry. Int. J. Hosp. Manag. 2022, 107, 103314. [Google Scholar] [CrossRef]

- Salcedo, E.; Gupta, M. The Effects of Individual-Level Espoused National Cultural Values on the Willingness to Use Bitcoin-like Blockchain Currencies. Int. J. Inf. Manag. 2021, 60, 102388. [Google Scholar] [CrossRef]

- Solberg Söilen, K.; Benhayoun, L. Household Acceptance of Central Bank Digital Currency: The Role of Institutional Trust. Int. J. Bank Mark. 2022, 40, 172–196. [Google Scholar] [CrossRef]

- Molina-Collado, A.; Salgado-Sequeiros, J.; Gómez-Rico, M.; Aranda García, E.; De Maeyer, P. Key Themes in Consumer Financial Services Research from 2000 to 2020: A Bibliometric and Science Mapping Analysis. Int. J. Bank Mark. 2021, 39, 1446–1478. [Google Scholar] [CrossRef]

- Kim, M. A Psychological Approach to Bitcoin Usage Behavior in the Era of COVID-19: Focusing on the Role of Attitudes toward Money. J. Retail. Consum. Serv. 2021, 62, 102606. [Google Scholar] [CrossRef]

- Albayati, H.; Kim, S.K.; Rho, J.J. Accepting Financial Transactions Using Blockchain Technology and Cryptocurrency: A Customer Perspective Approach. Technol. Soc. 2020, 62, 101320. [Google Scholar] [CrossRef]

- Shahzad, F.; Xiu, G.Y.; Wang, J.; Shahbaz, M. An Empirical Investigation on the Adoption of Cryptocurrencies among the People of Mainland China. Technol. Soc. 2018, 55, 33–40. [Google Scholar] [CrossRef]

- Prados-Castillo, J.F.; Guaita Martínez, J.M.; Zielińska, A.; Gorgues Comas, D. A Review of Blockchain Technology Adoption in the Tourism Industry from a Sustainability Perspective. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 814–830. [Google Scholar] [CrossRef]

- Sohaib, O.; Hussain, W.; Asif, M.; Ahmad, M.; Mazzara, M. A PLS-SEM Neural Network Approach for Understanding Cryptocurrency Adoption. IEEE Access 2020, 8, 13138–13150. [Google Scholar] [CrossRef]

- Nazifi, A.; Murdy, S.; Marder, B.; Gäthke, J.; Shabani, B. A Bit(Coin) of Happiness after a Failure: An Empirical Examination of the Effectiveness of Cryptocurrencies as an Innovative Recovery Tool. J. Bus. Res. 2021, 124, 494–505. [Google Scholar] [CrossRef]

- Yoo, K.; Bae, K.; Park, E.; Yang, T. Understanding the Diffusion and Adoption of Bitcoin Transaction Services: The Integrated Approach. Telemat. Inform. 2020, 53, 101302. [Google Scholar] [CrossRef]

- Mattke, J.; Maier, C.; Reis, L.; Weitzel, T. Bitcoin Investment: A Mixed Methods Study of Investment Motivations. Eur. J. Inf. Syst. 2019, 30, 1–25. [Google Scholar] [CrossRef]

- Lee, D. Handbook of Digital Currency: Bitcoin, Innovation, Financial Instruments, and Big Data; Academic Press: Cambridge, MA, USA, 2015; ISBN 0-12-802351-1. [Google Scholar]

- Statista Cryptocurrencies—India. Available online: https://www.statista.com/outlook/dmo/fintech/digital-assets/cryptocurrencies/india (accessed on 25 April 2023).

- Despite Hurdles, Crypto Users in India Set to Reach 156 Million in 2023—Next Crypto Hub? 2023. Available online: https://www.cnbctv18.com/ (accessed on 1 May 2023).

- Tapscott, D.; Tapscott, A. Blockchain Revolution: How the Technology Behind; Penguin Publishing Group: New York, NY, USA.

- Beck, R.; Avital, M.; Rossi, M.; Thatcher, J.B. Blockchain Technology in Business and Information Systems Research. Bus. Inf. Syst. Eng. 2017, 59, 381–384. [Google Scholar] [CrossRef]

- Lewis, A. The Basics of Bitcoins and Blockchains: An Introduction to Cryptocurrencies and the Technology That Powers Them; Mango Media Inc.: Coral Gables, FL, USA, 2018; ISBN 1-63353-801-X. [Google Scholar]

- Underwood, S. Blockchain beyond Bitcoin. Commun. ACM 2016, 59, 15–17. [Google Scholar] [CrossRef]

- Pilkington, M. Blockchain Technology: Principles and Applications. In Research Handbook on Digital Transformations; Edward Elgar Publishing: Cheltenham, UK, 2016; pp. 225–253. [Google Scholar]

- Casino, F.; Dasaklis, T.K.; Patsakis, C. A Systematic Literature Review of Blockchain-Based Applications: Current Status, Classification and Open Issues. Telemat. Inform. 2019, 36, 55–81. [Google Scholar] [CrossRef]

- Slade, E.L.; Dwivedi, Y.K.; Piercy, N.C.; Williams, M.D. Modeling Consumers’ Adoption Intentions of Remote Mobile Payments in the United Kingdom: Extending UTAUT with Innovativeness, Risk, and Trust. Psychol. Mark. 2015, 32, 860–873. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User acceptance of information technology: Toward a unified view. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Venkatesh, V.; Thong, J.Y.L.; Xu, X. Consumer Acceptance and Use of Information Technology: Extending the Unified Theory of Acceptance and Use of Technology. MIS Q. Manag. Inf. Syst. 2012, 36, 157–178. [Google Scholar] [CrossRef]

- Oliveira, T.; Thomas, M.; Baptista, G.; Campos, F. Mobile Payment: Understanding the Determinants of Customer Adoption and Intention to Recommend the Technology. Comput. Hum. Behav. 2016, 61, 404–414. [Google Scholar] [CrossRef]

- Thakur, R.; Srivastava, M. Adoption Readiness, Personal Innovativeness, Perceived Risk and Usage Intention across Customer Groups for Mobile Payment Services in India. Internet Res. 2014, 24, 369–392. [Google Scholar] [CrossRef]

- Zhou, T.; Lu, Y.; Wang, B. Integrating TTF and UTAUT to Explain Mobile Banking User Adoption. Comput. Hum. Behav. 2010, 26, 760–767. [Google Scholar] [CrossRef]

- Baptista, G.; Oliveira, T. Understanding Mobile Banking: The Unified Theory of Acceptance and Use of Technology Combined with Cultural Moderators. Comput. Hum. Behav. 2015, 50, 418–430. [Google Scholar] [CrossRef]

- Kim, M.J.; Hall, C.M. What Drives Visitor Economy Crowdfunding? The Effect of Digital Storytelling on Unified Theory of Acceptance and Use of Technology. Tour. Manag. Perspect. 2020, 34, 100638. [Google Scholar] [CrossRef]

- Agarwal, R.; Prasad, J. A Conceptual and Operational Definition of Personal Innovativeness in the Domain of Information Technology. Inf. Syst. Res. 1998, 9, 204–215. [Google Scholar] [CrossRef]

- Gefen, D. E-Commerce: The Role of Familiarity and Trust. Omega 2000, 28, 725–737. [Google Scholar] [CrossRef]

- Dowling, G.R. Perceived Risk: The Concept and Its Measurement. Psychol. Mark. 1986, 3, 193–201. [Google Scholar] [CrossRef]

- Dinev, T.; Hu, Q. The Centrality of Awareness in the Formation of User Behavioral Intention toward Protective Information Technologies. J. Assoc. Inf. Syst. 2007, 8, 386–408. [Google Scholar] [CrossRef]

- Raddatz, N.; Coyne, J.; Menard, P.; Crossler, R.E. Becoming a Blockchain User: Understanding Consumers’ Benefits Realisation to Use Blockchain-Based Applications. Eur. J. Inf. Syst. 2021, 32, 287–314. [Google Scholar] [CrossRef]

- Hastings, J.S.; Madrian, B.C.; Skimmyhorn, W.L. Financial Literacy, Financial Education, and Economic Outcomes. Annu. Rev. Econ. 2013, 5, 347–373. [Google Scholar] [CrossRef]

- Esmaeilzadeh, P.; Subramanian, H.; Cousins, K. Individuals’ Cryptocurrency Adoption Individuals’ Cryptocurrency Adoption: A Proposed Moderated-Mediation Model. In Proceedings of the 25th Americas Conference on Information Systems, Cancún, Mexico, 15–17 August 2019. [Google Scholar]

- Arias-Oliva, M.; Pelegrín-Borondo, J.; Matías-Clavero, G. Variables Influencing Cryptocurrency Use: A Technology Acceptance Model in Spain. Front. Psychol. 2019, 10, 475. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations, 5th ed.; New York Free Press: Glencoe, IL, USA, 2003; ISBN 978-0-7432-5823-4. [Google Scholar]

- Lu, J.; Yao, J.E.; Yu, C.S. Personal Innovativeness, Social Influences and Adoption of Wireless Internet Services via Mobile Technology. J. Strateg. Inf. Syst. 2005, 14, 245–268. [Google Scholar] [CrossRef]

- Lin, Z.; Filieri, R. Airline Passengers’ Continuance Intention towards Online Check-in Services: The Role of Personal Innovativeness and Subjective Knowledge. Transp. Res. Part E Logist. Transp. Rev. 2015, 81, 158–168. [Google Scholar] [CrossRef]

- Twum, K.K.; Ofori, D.; Keney, G.; Korang-Yeboah, B. Using the UTAUT, Personal Innovativeness and Perceived Financial Cost to Examine Student’s Intention to Use E-Learning. J. Sci. Technol. Policy Manag. 2022, 13, 713–737. [Google Scholar] [CrossRef]

- Lee, Y.K.; Park, J.H.; Chung, N.; Blakeney, A. A Unified Perspective on the Factors Influencing Usage Intention toward Mobile Financial Services. J. Bus. Res. 2012, 65, 1590–1599. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. Manag. Inf. Syst. 1989, 13, 319–339. [Google Scholar] [CrossRef]

- Chan, R.; Troshani, I.; Rao Hill, S.; Hoffmann, A. Towards an Understanding of Consumers’ FinTech Adoption: The Case of Open Banking. Int. J. Bank Mark. 2022, 40, 886–917. [Google Scholar] [CrossRef]

- Sankaran, R.; Chakraborty, S. Factors Impacting Mobile Banking in India: Empirical Approach Extending UTAUT2 with Perceived Value and Trust. IIM Kozhikode Soc. Manag. Rev. 2022, 11, 7–24. [Google Scholar] [CrossRef]

- Sankaran, R.; Chakraborty, S. Why Customers Make Mobile Payments? Applying a Means-End Chain Approach. Mark. Intell. Plan. 2021, 39, 109–124. [Google Scholar] [CrossRef]

- Rahi, S.; Othman Mansour, M.M.; Alghizzawi, M.; Alnaser, F.M. Integration of UTAUT Model in Internet Banking Adoption Context: The Mediating Role of Performance Expectancy and Effort Expectancy. J. Res. Interact. Mark. 2019, 13, 411–435. [Google Scholar] [CrossRef]

- Alalwan, A.A.; Dwivedi, Y.K.; Rana, N.P. Factors Influencing Adoption of Mobile Banking by Jordanian Bank Customers: Extending UTAUT2 with Trust. Int. J. Inf. Manag. 2017, 37, 99–110. [Google Scholar] [CrossRef]

- Oliveira, T.; Faria, M.; Thomas, M.A.; Popovič, A. Extending the Understanding of Mobile Banking Adoption: When UTAUT Meets TTF and ITM. Int. J. Inf. Manag. 2014, 34, 689–703. [Google Scholar] [CrossRef]

- Jalan, A.; Matkovskyy, R.; Urquhart, A.; Yarovaya, L. The Role of Interpersonal Trust in Cryptocurrency Adoption. J. Int. Financ. Mark. Inst. Money 2023, 83, 101715. [Google Scholar] [CrossRef]

- Zarifis, A.; Cheng, X.; Dimitriou, S.; Efthymiou, L.; Zarifis, A.; Cheng, X.; Dimitriou, S.; Leonidas, E. Trust in Digital Currency Enabled Transactions Model; Association for Information Systems (AIS): Atlanta, Georgia, 2015. [Google Scholar]

- Marella, V.; Upreti, B.; Merikivi, J.; Tuunainen, V.K. Understanding the Creation of Trust in Cryptocurrencies: The Case of Bitcoin. Electron. Mark. 2020, 30, 259–271. [Google Scholar] [CrossRef]

- Gefen, D.; Karahanna, E.; Straub, D.W. Trust and TAM in Online Shopping: An Integrated Model. MIS Q. 2003, 27, 51–90. [Google Scholar] [CrossRef]

- Sankaran, R.; Chakraborty, S. Measuring Consumer Perception of Overall Brand Equity Drivers for M-Payments. Int. J. Bank Mark. 2023, 41, 130–157. [Google Scholar] [CrossRef]

- Kirton, M. Adaptors and Innovators: A Description and Measure. J. Appl. Psychol. 1976, 61, 622–629. [Google Scholar] [CrossRef]

- Mitchell, V. Understanding Consumers’ Behaviour: Can Perceived Risk Theory Help? Manag. Decis. 1992, 30, 26–31. [Google Scholar] [CrossRef]

- Yang, S.; Lu, Y.; Gupta, S.; Cao, Y.; Zhang, R. Mobile Payment Services Adoption across Time: An Empirical Study of the Effects of Behavioral Beliefs, Social Influences, and Personal Traits. Comput. Hum. Behav. 2012, 28, 129–142. [Google Scholar] [CrossRef]

- Balvers, R.J.; McDonald, B. Designing a Global Digital Currency. J. Int. Money Finance 2021, 111, 102317. [Google Scholar] [CrossRef]

- Lu, J. Are Personal Innovativeness and Social Influence Critical to Continue with Mobile Commerce? Internet Res. 2014, 24, 134–159. [Google Scholar] [CrossRef]

- Jackson, J.D.; Yi, M.Y.; Park, J.S. An Empirical Test of Three Mediation Models for the Relationship between Personal Innovativeness and User Acceptance of Technology. Inf. Manag. 2013, 50, 154–161. [Google Scholar] [CrossRef]

- Remund, D.L. Financial Literacy Explicated: The Case for a Clearer Definition in an Increasingly Complex Economy. J. Consum. Aff. 2010, 44, 276–295. [Google Scholar] [CrossRef]

- Gignac, G.E. The Association between Objective and Subjective Financial Literacy: Failure to Observe the Dunning-Kruger Effect. Personal. Individ. Differ. 2022, 184, 111224. [Google Scholar] [CrossRef]

- Munnukka, J.; Uusitalo, O.; Koivisto, V.-J. The Consequences of Perceived Risk and Objective Knowledge for Consumers’ Investment Behavior. J. Financ. Serv. Mark. 2017, 22, 150–160. [Google Scholar] [CrossRef]

- Nejad, M.G.; Javid, K. Subjective and Objective Financial Literacy, Opinion Leadership, and the Use of Retail Banking Services. Int. J. Bank Mark. 2018, 36, 784–804. [Google Scholar] [CrossRef]

- Nejad, M. Research on Financial Services Innovations: A Quantitative Review and Future Research Directions. Int. J. Bank Mark. 2016, 34, 1042–1068. [Google Scholar] [CrossRef]

- Gefen, D.; Straub, D.W. Consumer Trust in B2C E-Commerce and the Importance of Social Presence: Experiments in e-Products and e-Services. Omega 2004, 32, 407–424. [Google Scholar] [CrossRef]

- Faqih, K.M.S. An Empirical Analysis of Factors Predicting the Behavioral Intention to Adopt Internet Shopping Technology among Non-Shoppers in a Developing Country Context: Does Gender Matter? J. Retail. Consum. Serv. 2016, 30, 140–164. [Google Scholar] [CrossRef]

- Lusardi, A.; Mitchell, O.S. Baby Boomer Retirement Security: The Roles of Planning, Financial Literacy, and Housing Wealth. J. Monet. Econ. 2007, 54, 205–224. [Google Scholar] [CrossRef]

- Hair, J.; Black, W.; Babin, B.; Anderson, R. Multivariate Data Analysis, 7th ed.; Pearson Prentice Hall: Hoboken, NJ, USA, 2009. [Google Scholar]

- Grewal, R.; Cote, J.A.; Baumgartner, H. Multicollinearity and Measurement Error in Structural Equation Models: Implications for Theory Testing. Mark. Sci. 2004, 23, 519–529. [Google Scholar] [CrossRef]

- Cheung, G.W.; Lau, R.S. Testing Mediation and Suppression Effects of Latent Variables: Bootstrapping with Structural Equation Models. Organ. Res. Methods 2008, 11, 296–325. [Google Scholar] [CrossRef]

- Hoyle, R.H.; Smith, G.T. Formulating Clinical Research Hypotheses as Structural Equation Models: A Conceptual Overview. J. Consult. Clin. Psychol. 1994, 62, 429. [Google Scholar] [CrossRef] [PubMed]

- Astrachan, C.B.; Patel, V.K.; Wanzenried, G. A Comparative Study of CB-SEM and PLS-SEM for Theory Development in Family Firm Research. Innov. Establ. Res. Methods Fam. Bus. 2014, 5, 116–128. [Google Scholar] [CrossRef]

- Hair, J.; Celsi, M.; Money, A.; Samouel, P.; Page, M. Essentials of Business Research Methods; ME Sharpe, Inc.: New York, NY, USA, 2011. [Google Scholar]

- Yap, B.W.; Khong, K.W. Examining the Effects of Customer Service Management (CSM) on Perceived Business Performance via Structural Equation Modelling. Appl. Stoch. Models Bus. Ind. 2006, 22, 587–605. [Google Scholar] [CrossRef]

- Hair, J.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 3rd ed.; SAGE Publications: Thousand Oaks, CA, USA, 2021. [Google Scholar]

- Gunzler, D.; Chen, T.; Wu, P.; Zhang, H. Introduction to Mediation Analysis with Structural Equation Modeling. Shanghai Arch. Psychiatry 2013, 25, 390. [Google Scholar] [PubMed]

- Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 8th ed.; Cengage Learning, EMEA: Hampshire, UK, 2019; ISBN 978-1-4737-5654-0. [Google Scholar]

- Armstrong, J.S.; Overton, T.S. Estimating Nonresponse Bias in Mail Surveys. J. Mark. Res. 1977, 14, 396–402. [Google Scholar] [CrossRef]

- Podsakoff, P.M.; MacKenzie, S.B.; Lee, J.Y.; Podsakoff, N.P. Common Method Biases in Behavioral Research: A Critical Review of the Literature and Recommended Remedies. J. Appl. Psychol. 2003, 88, 879–903. [Google Scholar] [CrossRef]

- Ioannou, A.; Tussyadiah, I.; Lu, Y. Privacy Concerns and Disclosure of Biometric and Behavioral Data for Travel. Int. J. Inf. Manag. 2020, 54, 102122. [Google Scholar] [CrossRef]

- Serrano Archimi, C.; Reynaud, E.; Yasin, H.M.; Bhatti, Z.A. How Perceived Corporate Social Responsibility Affects Employee Cynicism: The Mediating Role of Organizational Trust. J. Bus. Ethics 2018, 151, 907–921. [Google Scholar] [CrossRef]

- MacKenzie, S.B.; Podsakoff, P.M. Common Method Bias in Marketing: Causes, Mechanisms, and Procedural Remedies. J. Retail. 2012, 88, 542–555. [Google Scholar] [CrossRef]

- Nunnally, J.C. An Overview of Psychological Measurement; Wolman, B.B., Ed.; Clinical Diagnosis of Mental Disorders; Springer: Boston, MA, USA; pp. 97–146.

- Fornell, C.; Larcker, D.F.; Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark. Res. 1981, 18, 39–50. [Google Scholar] [CrossRef]

- Byrne, B.M. Structural Equation Modeling with AMOS: Basic Concepts, Applications, and Programming; Routledge: London, UK, 2016; ISBN 1-315-75742-7. [Google Scholar]

- Zhao, X.; Lynch, J.G., Jr.; Chen, Q. Reconsidering Baron and Kenny: Myths and Truths about Mediation Analysis. J. Consum. Res. 2010, 37, 197–206. [Google Scholar] [CrossRef]

- Kalinić, Z.; Liébana-Cabanillas, F.J.; Muñoz-Leiva, F.; Marinković, V. The Moderating Impact of Gender on the Acceptance of Peer-to-Peer Mobile Payment Systems. Int. J. Bank Mark. 2020, 38, 138–158. [Google Scholar] [CrossRef]

- Lee, U.-K.; Kim, H. UTAUT in Metaverse: An “Ifland” Case. J. Theor. Appl. Electron. Commer. Res. 2022, 17, 613–635. [Google Scholar] [CrossRef]

| Authors | Focus of the Study | Theoretical Foundation |

|---|---|---|

| Salcedo and Gupta [18] | Examine the willingness to use blockchain currencies based on national cultural values. | Hofstede’s framework of national culture |

| Solberg Söilen et al. [19] | Examine household acceptance of CBDCs (central bank digital currencies) | UTAUT and institutional trust theory (ITT) |

| Kim [21] | Understand usage behaviour of Bitcoin in the Covid-19 era through a psychological approach. | Theory of Planned Behaviour (TPA) and money attitudes |

| Kim et al. [17] | Study CBDC as a payment method adoption in the tourism sector | Attention, Interest, Desire, and Action (AIDA) model |

| Esmaeilzadeh et al. [52] | Proposed a moderated-mediation model developed through qualitative research to study the adoption of cryptocurrency. | UTAUT and utility theory |

| Shahzad et al. [23] | Examine the adoption of cryptocurrencies by people in China | Technology Acceptance Model (TAM) extended with Awareness, Perceived Trustworthiness |

| Arias-Oliva et al. [53] | Understanding the variables impacting behavioural intention to use cryptocurrency in Spain | Extension of Technology Acceptance Model (TAM) with perceived risk and financial literacy |

| Albayati et al. [22] | Investigate consumer behaviour towards financial transactions based on blockchain technology and cryptocurrency. | Technology Acceptance Model (TAM) with external variables: design, experience, social influence, regulatory support and trust |

| Sohaib et al. [25] | Understanding cryptocurrency adoption combining technology readiness dimension and TAM using SEM and ANN | Technology Acceptance Model (TAM) with Technology Readiness (TR) |

| Frequency | Percentage | |

|---|---|---|

| Age (in years) | ||

| 18–25 | 170 | 54.5% |

| 25–35 | 104 | 33.4% |

| 36–45 | 31 | 9.9% |

| Above 45 | 7 | 2.2% |

| Gender | ||

| Male | 228 | 73.1% |

| Female | 84 | 26.9% |

| Annual Income | ||

| Less than five lakhs | 177 | 56.7% |

| Between 6 and 15 lakhs | 89 | 28.5% |

| Between 15 and 25 lakhs | 24 | 7.7% |

| Between 25 and 40 lakhs | 9 | 2.9% |

| Above 40 lakhs | 13 | 4.2% |

| Highest Education | ||

| Graduate | 174 | 55.8% |

| Postgraduate | 125 | 40.1% |

| Doctorate | 13 | 4.1% |

| Total | 312 | 100 |

| Construct | Item Code | Mean | Std Deviation | FL | Alpha | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Performance Expectancy (PE) | 0.912 | ||||||||||||||

| PE1 | 4.125 | 1.77 | 0.852 | ||||||||||||

| PE2 | 3.923 | 1.80 | 0.794 | ||||||||||||

| PE3 | 3.971 | 1.80 | 0.873 | ||||||||||||

| PE4 | 3.888 | 1.71 | 0.889 | ||||||||||||

| Effort Expectancy (EE) | 0.899 | ||||||||||||||

| EE1 | 4.737 | 1.62 | 0.853 | ||||||||||||

| EE2 | 4.683 | 1.58 | 0.938 | ||||||||||||

| EE3 | 4.385 | 1.65 | 0.812 | ||||||||||||

| Personal Innovativeness (PI) | 0.856 | ||||||||||||||

| PI1 | 4.766 | 1.60 | 0.816 | ||||||||||||

| PI2 | 4.093 | 1.78 | 0.809 | ||||||||||||

| PI3 | 4.933 | 1.68 | 0.824 | ||||||||||||

| Trust (TR) | 0.955 | ||||||||||||||

| TR1 | 3.837 | 1.67 | 0.888 | ||||||||||||

| TR2 | 4.083 | 1.73 | 0.887 | ||||||||||||

| TR3 | 3.894 | 1.71 | 0.952 | ||||||||||||

| TR4 | 3.881 | 1.73 | 0.943 | ||||||||||||

| Perceived Risk (PR) | 0.863 | ||||||||||||||

| PR1 | 4.708 | 1.65 | 0.747 | ||||||||||||

| PR2 | 5.135 | 1.59 | 0.915 | ||||||||||||

| PR3 | 5.189 | 1.64 | 0.818 | ||||||||||||

| Facilitating Conditions (FC) | 0.837 | ||||||||||||||

| FC1 | 4.061 | 1.78 | 0.79 | ||||||||||||

| FC2 | 3.981 | 1.81 | 0.847 | ||||||||||||

| FC3 | 4.574 | 1.70 | 0.755 | ||||||||||||

| Social Influence (SI) | 0.918 | ||||||||||||||

| SI1 | 3.147 | 1.65 | 0.813 | ||||||||||||

| SI2 | 3.413 | 1.65 | 0.94 | ||||||||||||

| SI3 | 3.558 | 1.72 | 0.914 | ||||||||||||

| Financial Literacy (FL) | 0.835 | ||||||||||||||

| FL1 | 4.410 | 1.57 | 0.808 | ||||||||||||

| FL2 | 4.394 | 1.60 | 0.817 | ||||||||||||

| FL3 | 4.817 | 2.11 | 0.717 | ||||||||||||

| Technology Awareness (TA) | 0.908 | ||||||||||||||

| TA1 | 4.353 | 1.63 | 0.752 | ||||||||||||

| TA2 | 3.878 | 1.93 | 0.738 | ||||||||||||

| TA3 | 3.939 | 1.98 | 0.735 | ||||||||||||

| TA4 | 4.413 | 1.80 | 0.805 | ||||||||||||

| TA5 | 4.429 | 1.80 | 0.759 | ||||||||||||

| Behavioural Intention (BI) | 0.851 | ||||||||||||||

| BI1 | 3.849 | 1.60 | 0.918 | ||||||||||||

| BI2 | 4.045 | 1.62 | 0.914 | ||||||||||||

| BI3 | 4.077 | 1.74 | 0.799 | ||||||||||||

| Descriptive statistics and exploratory factor analysis results | |||||||||||||||

| AVE | CR | BI | EE | PE | SI | PR | TR | PI | FC | ||||||

| BI | 0.772 | 0.910 | 0.878 | ||||||||||||

| EE | 0.756 | 0.902 | 0.576 | 0.869 | |||||||||||

| PE | 0.727 | 0.914 | 0.816 | 0.531 | 0.852 | ||||||||||

| SI | 0.793 | 0.919 | 0.673 | 0.409 | 0.612 | 0.890 | |||||||||

| PR | 0.688 | 0.868 | 0.031 | 0.155 | 0.021 | 0.055 | 0.829 | ||||||||

| TR | 0.843 | 0.955 | 0.716 | 0.617 | 0.682 | 0.61 | −0.115 | 0.918 | |||||||

| PI | 0.666 | 0.955 | 0.602 | 0.619 | 0.543 | 0.057 | 0.178 | 0.565 | 0.816 | ||||||

| FC | 0.637 | 0.840 | 0.657 | 0.776 | 0.537 | 0.598 | 0.125 | 0.747 | 0.691 | 0.798 | |||||

| Discriminant validity results | |||||||||||||||

| Fit Indices | Values | Acceptable Thresholds |

|---|---|---|

| CMIN/df | 2.3 | ≤3 |

| RMSEA | 0.085 | 0.05–0.10 |

| CFI | 0.908 | >0.9 |

| GFI | 0.83 | >0.7 |

| NFI | 0.911 | 0–1 |

| Hypothesis | Relationship | Coefficient | p-Value | Result |

|---|---|---|---|---|

| H1a | Personal Innovativeness (PI)→ Behavioural Intention (BI) | 0.126 | 0.215 | Not Supported |

| H1b | Personal Innovativeness (PI)→Performance Expectancy (PE) | 0.487 | *** | Supported |

| H1c | Personal Innovativeness (PI)→ Effort Expectancy (EE) | 0.715 | *** | Supported |

| H2 | Performance Expectancy (PE)→ Behavioural Intention (BI) | 0.504 | *** | Supported |

| H3 | Effort Expectancy (EE) → Behavioural Intention (BI) | 0.021 | 0.724 | Not Supported |

| H4 | Effort Expectancy (EE) → Performance Expectancy (PE) | 0.195 | 0.024 ** | Supported |

| H5 | Social Influence (SI)→ Behavioural Intention (BI) | 0.217 | *** | Supported |

| H6 | Facilitating Conditions (FC)→ Behavioural Intention (BI) | 0.078 | 0.380 | Not Supported |

| H7 | Trust (TR)→ Behavioural Intention (BI) | 0.133 | 0.053 * | Supported |

| H8 | Perceived Risk (PR)→ Behavioural Intention (BI) | −0.017 | 0.692 | Not Supported |

| Hypothesis | Mediation Relationship | Indirect Effect | Direct Effect | Result |

|---|---|---|---|---|

| H9 | Personal Innovativeness (PI)→ Behavioural Intention (BI) via Performance Expectancy (PE) | 0.359 (p = 0.000) | 0.139 (p = 0.185) | Indirect only mediation |

| Effect | Moderator | High | Low | Δχ2 | Moderation | ||

|---|---|---|---|---|---|---|---|

| Performance Expectancy (PE)→ Behavioural Intention (BI) | Estimate | t-value | Estimate | t-value | |||

| Technology Awareness (TA) | 0.43 | 6.528 *** | 0.413 | 6.716 *** | 7.089 ** | Yes | |

| Financial Literacy (FL) | 0.608 | 7.244 *** | 0.421 | 6.905 *** | 38.222 *** | Yes | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kumari, V.; Bala, P.K.; Chakraborty, S. An Empirical Study of User Adoption of Cryptocurrency Using Blockchain Technology: Analysing Role of Success Factors like Technology Awareness and Financial Literacy. J. Theor. Appl. Electron. Commer. Res. 2023, 18, 1580-1600. https://doi.org/10.3390/jtaer18030080

Kumari V, Bala PK, Chakraborty S. An Empirical Study of User Adoption of Cryptocurrency Using Blockchain Technology: Analysing Role of Success Factors like Technology Awareness and Financial Literacy. Journal of Theoretical and Applied Electronic Commerce Research. 2023; 18(3):1580-1600. https://doi.org/10.3390/jtaer18030080

Chicago/Turabian StyleKumari, Vandana, Pradip Kumar Bala, and Shibashish Chakraborty. 2023. "An Empirical Study of User Adoption of Cryptocurrency Using Blockchain Technology: Analysing Role of Success Factors like Technology Awareness and Financial Literacy" Journal of Theoretical and Applied Electronic Commerce Research 18, no. 3: 1580-1600. https://doi.org/10.3390/jtaer18030080

APA StyleKumari, V., Bala, P. K., & Chakraborty, S. (2023). An Empirical Study of User Adoption of Cryptocurrency Using Blockchain Technology: Analysing Role of Success Factors like Technology Awareness and Financial Literacy. Journal of Theoretical and Applied Electronic Commerce Research, 18(3), 1580-1600. https://doi.org/10.3390/jtaer18030080