What Motivates Speculators to Speculate?

Abstract

:1. Introduction

2. Theoretical Frame and Conceptual Clarification

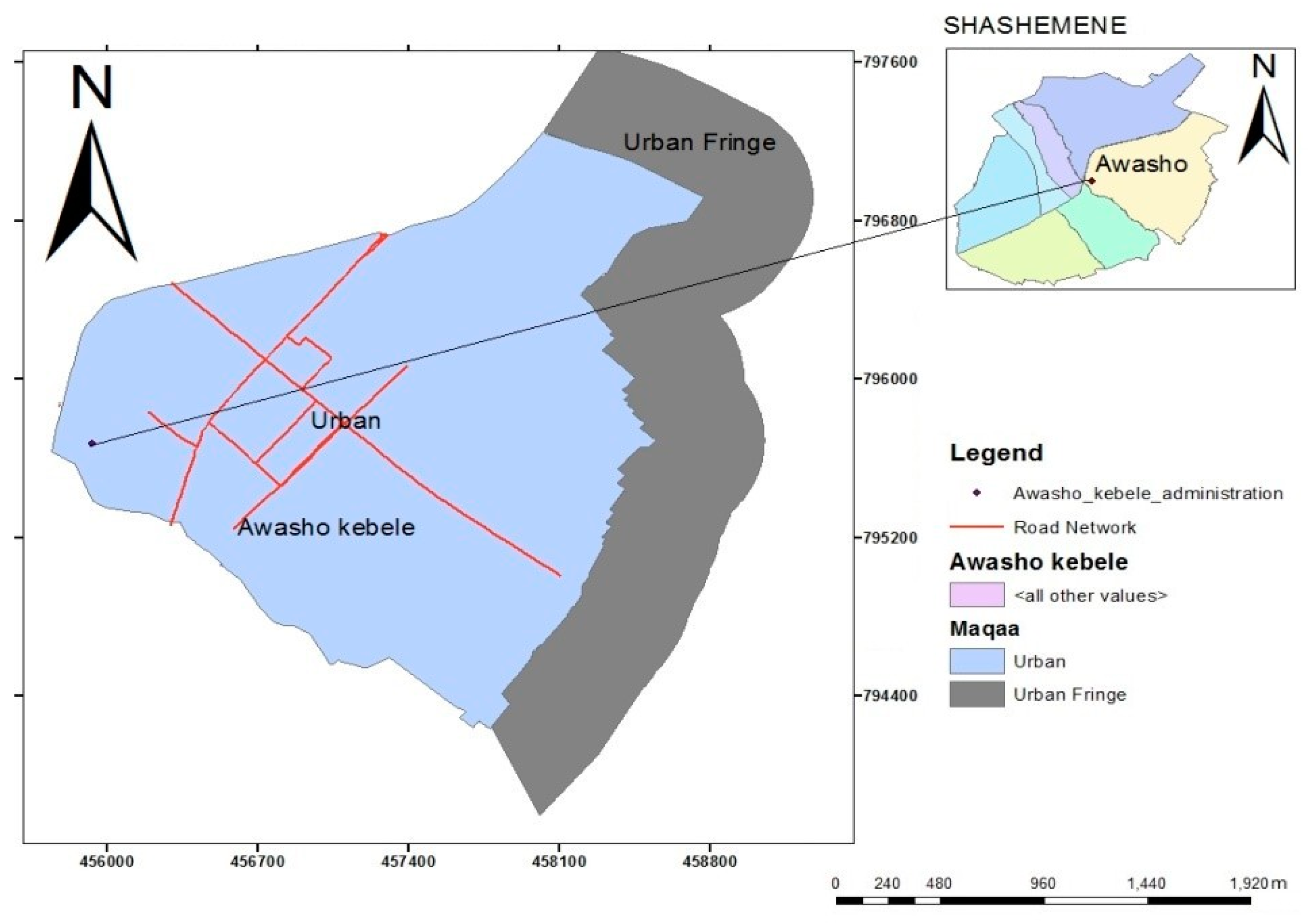

3. Methodology

4. Results and Discussion

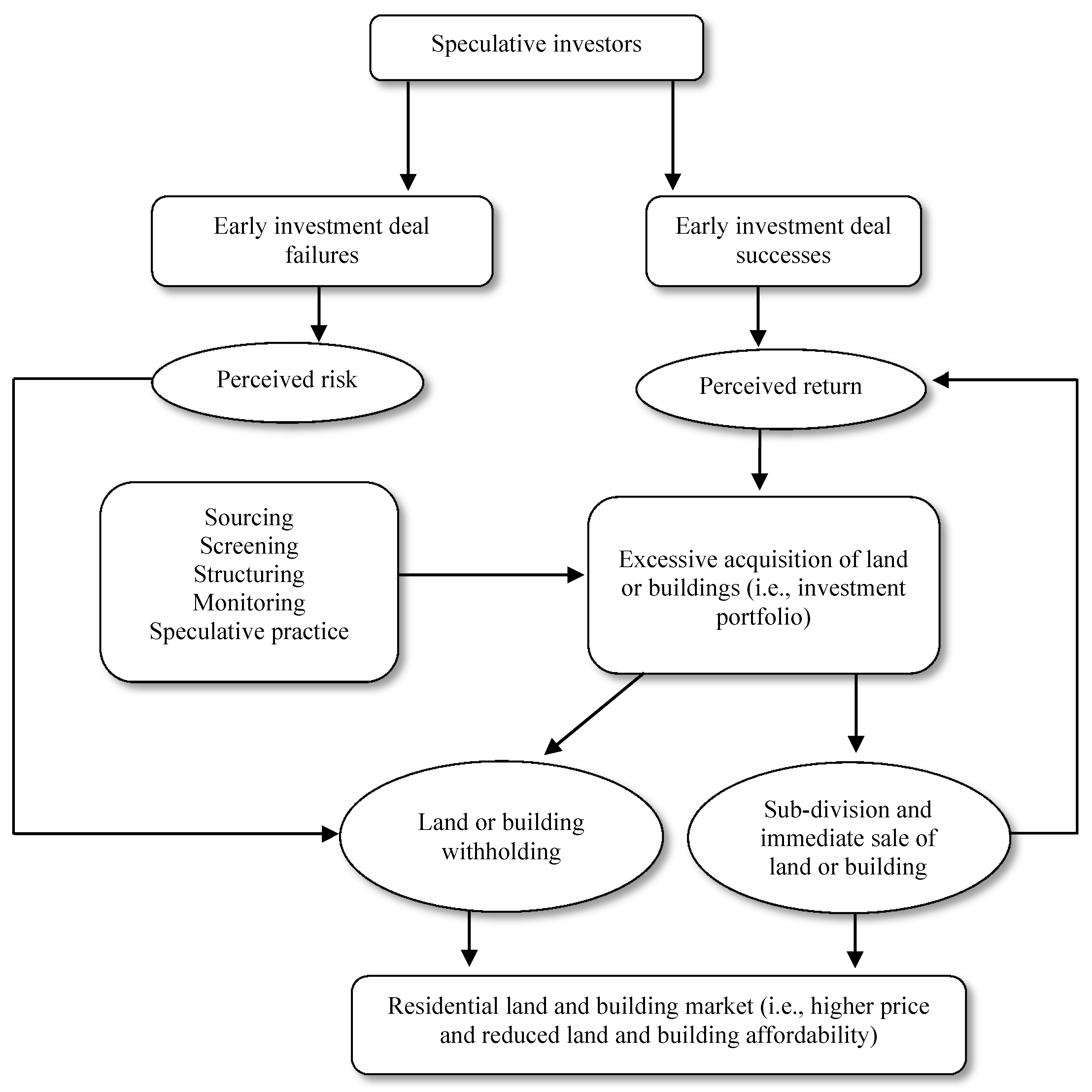

4.1. Factors Motivating Land Speculators

4.2. Prominent Characteristics of Land Acquisition

4.3. Range of Time between Actual Land Acquisition and Development by Speculators

4.4. Factors Responsible for Speculative Land Acquisition

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Dimuna, K.O. Enhancing Land Acquisition for Individual Housing Development in Nigeria: A Case Study of Benin Metropolis Edo State, Nigeria. Int. J. Res. Innov. Appl. Sci. 2016, 1, 1–9. [Google Scholar]

- Nwoko, K.C. Land ownership versus development in the era of globalisation: A trajectory of conflict and wealth accumulation in Southern Nigeria. J. Afr. Transform. 2016, 1, 77–94. [Google Scholar]

- Chang, V.; Newman, R.; Walters, R.J.; Wills, G.B. Review of economic bubbles. Int. J. Inf. Manag. 2016, 36, 497–506. [Google Scholar] [CrossRef]

- Makkonen, T.; Williams, A.M. Border region studies: The structure of an ‘offbeat’ field of regional studies. Reg. Stud. Reg. Sci. 2016, 3, 355–367. [Google Scholar] [CrossRef] [Green Version]

- Scott, J.W.; Sohn, C. Place-making and the bordering of urban space: Interpreting the emergence of new neighbourhoods in Berlin and Budapest. Eur. Urban Reg. Stud. 2018, 096977641876457. [Google Scholar] [CrossRef]

- Molotch, H. The City as a Growth Machine: Toward a Political Economy of Place. Am. J. Sociol. 1976, 82, 309–332. [Google Scholar] [CrossRef]

- Siegel, J.J. What Is an Asset Price Bubble? An Operational Definition. Eur. Financ. Manag. 2003, 9, 11–24. [Google Scholar] [CrossRef]

- Kittrell, K. Impacts of Vacant Land Values. Transp. Res. Rec. J. Transp. Res. Board 2012, 2276, 138–145. [Google Scholar] [CrossRef]

- Mohamed, R. The Psychology of Residential Developers. J. Plan. Educ. Res. 2006, 26, 28–37. [Google Scholar] [CrossRef]

- Fauser, M. The Emergence of Urban Border Spaces in Europe. J. Borderl. Stud. 2017, 34, 605–622. [Google Scholar] [CrossRef]

- Joshua, P.B.; Glanda, G.G.; Ilesanmi, F.A. The Effects of Land Speculation on Urban Planning and Development in Bajabure Area, Girei Local Government, Adamawa State. J. Environ. Earth Sci. 2016, 6, 128–133. [Google Scholar]

- Gemeda, B.S.; Abebe, B.G.; Cirella, G.T. The Role of Land Speculators around the Urban Edge of Shashemene City, Ethiopia. Eur. J. Sustain. Dev. Res. 2019, 4, em0108. [Google Scholar] [CrossRef] [Green Version]

- Golland, A.; Boelhouwer, P. Speculative housing supply land and housing, markets: A comparison. J. Prop. Res. 2002, 19, 231–251. [Google Scholar] [CrossRef]

- Wang, X.L.; Hua, S. Influence Factors of Chinese Real Estate. Appl. Mech. Mater. 2013, 405–408, 3391–3395. [Google Scholar] [CrossRef]

- Westerink, J.; Haase, D.; Bauer, A.; Ravetz, J.; Jarrige, F.; Aalbers, C.B.E.M. Dealing with Sustainability Trade-Offs of the Compact City in Peri-Urban Planning Across European City Regions. Eur. Plan. Stud. 2013, 21, 473–497. [Google Scholar] [CrossRef]

- World Bank. Urbanization beyond Municipal Boundaries; The World Bank: Washington, DC, USA, 2013; ISBN 978-0-8213-9840-1. [Google Scholar]

- Ambaye, D.W. Land Rights and Expropriation in Ethiopia. Ph.D. Thesis, School of Architecture and the Built Environment, Royal Institute of Technology, Stockholm, Sweden, 2013. [Google Scholar]

- NechaSungena, T.; Serbeh-Yiadom, K.; Asfaw, M. Towards an Efficient Implementation of the Land Lease Policy of Ethiopia: A case-study of Hawassa. Dev. Ctry. Stud. 2014, 4, 155–166. [Google Scholar]

- Abdo, M. Legislative Protection of Property Rights in Ethiopia: An Overview. Mizan Law Rev. 2014, 7, 165. [Google Scholar] [CrossRef] [Green Version]

- Barbier, E.B.; Hochard, J.P. Does Land Degradation Increase Poverty in Developing Countries? PLoS ONE 2016, 11, e0152973. [Google Scholar] [CrossRef] [Green Version]

- Unruh, J.D. Land Tenure and the “Evidence Landscape” in Developing Countries. Ann. Assoc. Am. Geogr. 2006, 96, 754–772. [Google Scholar] [CrossRef]

- Diergarten, Y. Indigenous or Out of Scope? Large-scale Land Acquisitions in Developing Countries, International Human Rights Law and the Current Deficiencies in Land Rights Protection. Hum. Rights Law Rev. 2019, 19, 37–52. [Google Scholar] [CrossRef]

- Business Dictionary Online Business Dictionary. Available online: http://www.businessdictionary.com/ (accessed on 20 June 2019).

- Park, R.E.; Burgess, E.W.; McKenzie, R.D. The City; University of Chicago Press: Chicago, IL, USA, 1925; ISBN 0226646114. [Google Scholar]

- Adams, J.S.; Hoyt, H. 1939: The structure and growth of residential neighborhoods in American cities. Washington, DC: Federal Housing Administration. Prog. Hum. Geogr. 2005, 29, 321–325. [Google Scholar] [CrossRef]

- Alonso, W. The Historic and the Structural Theories of Urban Form: Their Implications for Urban Renewal. Land Econ. 1964, 40, 227. [Google Scholar] [CrossRef]

- Burgess, E.W. The Growth of the City: An Introduction to a Research Project. In Urban Ecology; Springer: Boston, MA, USA, 2008; pp. 71–78. [Google Scholar]

- Motoro, P. A Comparative Analysis of Residential Property Rental Markets in Informal Settlements and Formal Areas of Lae and Port Moresby. Master’s Thesis, Addis Ababa University, Addis Ababa, Ethiopia, 2016. [Google Scholar]

- Hoyt, H. One Hundred Years of Land Values in Chicago: The Relationship of the Growth of Chicago to the Rise of Its Land Values, 1830–1933; Beard Books: Washington, DC, USA, 2000; ISBN 9781587980169. [Google Scholar]

- Perman, R.; Perman, R. Natural Resource and Environmental Economics; Pearson Addison Wesley: Harlow, UK, 2011; ISBN 0321417534. [Google Scholar]

- Valliere, D.; Peterson, R. Venture Capitalist Behaviours: Frameworks for Future Research. Ventur. Cap. 2005, 7, 167–183. [Google Scholar] [CrossRef]

- Oduwaye, L. Challenges of Sustainable Physical Planning and Development in Metropolitan Lagos. J. Sustain. Dev. 2009, 2, 159. [Google Scholar] [CrossRef] [Green Version]

- Osabuohien, E.S. Large-scale agricultural land investments and local institutions in Africa: The Nigerian case. Land Use Policy 2014, 39, 155–165. [Google Scholar] [CrossRef]

- Ariyo, J.A.; Ogbonna, D.O. The effects of land speculation on agricultural production among peasants in Kachia local government area of Kaduna State, Nigeria. Appl. Geogr. 1992, 12, 31–46. [Google Scholar] [CrossRef]

- Cotula, L. The international political economy of the global land rush: A critical appraisal of trends, scale, geography and drivers. J. Peasant Stud. 2012, 39, 649–680. [Google Scholar] [CrossRef]

- Nesheim, I.; Verburg, R.; Abdeladhim, M.A.; Bursztyn, M.; Chen, L.; Cissé, Y.; Feng, S.; Gicheru, P.; Jochen König, H.; Novira, N.; et al. Causal chains, policy trade offs and sustainability: Analysing land (mis)use in seven countries in the South. Land Use Policy 2014, 37, 60–70. [Google Scholar] [CrossRef]

- Sharmina, M.; Hoolohan, C.; Bows-Larkin, A.; Burgess, P.J.; Colwill, J.; Gilbert, P.; Howard, D.; Knox, J.; Anderson, K. A nexus perspective on competing land demands: Wider lessons from a UK policy case study. Environ. Sci. Policy 2016, 59, 74–84. [Google Scholar] [CrossRef] [Green Version]

- Brown, H.G. Wealth and Want: Speculation. Available online: http://www.wealthandwant.com/themes/Speculation.html (accessed on 18 June 2019).

- Sinclair, U. Wealth and Want: Speculation. Available online: http://www.wealthandwant.com/docs/Sinclair_CoLS.html (accessed on 18 June 2019).

- Malpezzi, S.; Wachter, S.M. The Role of Speculation in Real Estate Cycles. J. Real Estate Lit. 2005, 13, 143–164. [Google Scholar] [CrossRef] [Green Version]

- Messerli, P.; Giger, M.; Dwyer, M.B.; Breu, T.; Eckert, S. The geography of large-scale land acquisitions: Analysing socio-ecological patterns of target contexts in the global South. Appl. Geogr. 2014, 53, 449–459. [Google Scholar] [CrossRef]

- Colin, J.-P. Securing rural land transactions in Africa. An Ivorian perspective. Land Use Policy 2013, 31, 430–440. [Google Scholar] [CrossRef]

- Hurni, H.; Berhe, W.A.; Chadhokar, P.; Daniel, D.; Gete, Z.; Grunder, M.; Kassaye, G. Soil and Water Conservation in Ethiopia: Guidelines for Development Agents; Centre for Development and Environment (CDE), University of Bern, with Bern Open Publishing (BOP): Bern, Switzerland, 2016; ISBN 9783906813134. [Google Scholar]

- Nolte, K. Large-scale agricultural investments under poor land governance in Zambia. Land Use Policy 2014, 38, 698–706. [Google Scholar] [CrossRef]

- Petrick, M.; Wandel, J.; Karsten, K. Rediscovering the Virgin Lands: Agricultural Investment and Rural Livelihoods in a Eurasian Frontier Area. World Dev. 2013, 43, 164–179. [Google Scholar] [CrossRef] [Green Version]

- Andreasson, P.; Bekiros, S.; Nguyen, D.K.; Uddin, G.S. Impact of speculation and economic uncertainty on commodity markets. Int. Rev. Financ. Anal. 2016, 43, 115–127. [Google Scholar] [CrossRef]

- Ermolieva, T.; Havlík, P.; Ermoliev, Y.; Mosnier, A.; Obersteiner, M.; Leclère, D.; Khabarov, N.; Valin, H.; Reuter, W. Integrated Management of Land Use Systems under Systemic Risks and Security Targets: A Stochastic Global Biosphere Management Model. J. Agric. Econ. 2016, 67, 584–601. [Google Scholar] [CrossRef] [Green Version]

- Brunnermeier, M.K.; Cheridito, P.; Brunnermeier, M.K.; Cheridito, P. Measuring and Allocating Systemic Risk. Risks 2019, 7, 46. [Google Scholar] [CrossRef] [Green Version]

- Singh, G. Is India Hedged Against Systemic Risk? An Attempt at an Answer. Rev. Mark. Integr. 2013, 5, 83–129. [Google Scholar] [CrossRef]

- Huang, X.; Vodenska, I.; Havlin, S.; Stanley, H.E. Cascading failures in bi-partite graphs: Model for systemic risk propagation. Sci. Rep. 2013, 3, 1219. [Google Scholar] [CrossRef] [Green Version]

- Knittel, C.; Pindyck, R. The Simple Economics of Commodity Price Speculation; The MIT Press: Cambridge, MA, USA, 2013. [Google Scholar]

- Triantafyllopoulos, N. On the origins of tourist urbanisation in Greece: Land speculation and property market (in)efficiency. Land Use Policy 2017, 68, 15–27. [Google Scholar] [CrossRef]

- Maruani, T.; Amit-Cohen, I. Open space planning models: A review of approaches and methods. Landsc. Urban Plan. 2007, 81, 1–13. [Google Scholar] [CrossRef]

- Jonas, A.E.G.; Wilson, D. The Urban Growth Machine: Critical Perspectives Two Decades Later; SUNY Press: Albany, NY, USA, 1999; pp. 1–312. [Google Scholar]

- Logan, J.R.; Molotch, H.L. Urban Fortunes: The Political Economy of Place; University of California Press: Berkeley, CA, USA, 1987; ISBN 0520063414. [Google Scholar]

- Wetzstein, S. The global urban housing affordability crisis. Urban Stud. 2017, 54, 3159–3177. [Google Scholar] [CrossRef]

- Paczoski, A.; Abebe, S.T.; Cirella, G.T. Debt and Deficit Growth Rate Reporting for Post-Communist European Union Member States. Soc. Sci. 2019, 8, 173. [Google Scholar] [CrossRef] [Green Version]

- Paczoski, A. Różnice kulturowe wobec wzrostu gospodarczego: Ze szczególnym uwzględnieniem przykładów państw UE (Translated from Polish: “Cultural differences and economic growth: With emphasized examples from the EU”). Polityka Gospod. 2014, 22, 91–118. [Google Scholar]

- Atkinson, R. Limited exposure: Social concealment, mobility and engagement with public space by the super-rich in London. Environ. Plan. A Econ. Sp. 2016, 48, 1302–1317. [Google Scholar] [CrossRef] [Green Version]

- Hay, I. Geographies of the Super-Rich; Edward Elgar: Cheltenham, UK, 2013; ISBN 0857935682. [Google Scholar]

- Hay, I.; Muller, S. ‘That Tiny, Stratospheric Apex That Owns Most of the World’-Exploring Geographies of the Super-Rich. Geogr. Res. 2012, 50, 75–88. [Google Scholar] [CrossRef]

- Lee, K.N.H. Residential property price-stock price nexus in Hong Kong: New evidence from ARDL bounds test. Int. J. Hous. Mark. Anal. 2017, 10, 204–220. [Google Scholar] [CrossRef]

- Ioannides, Y.M.; Rosenthal, S.S.; Ioannides, Y.; Rosenthal, S. Estimating the Consumption and Investment Demands for Housing and Their Effect on Housing Tenure Status. Rev. Econ. Stat. 1994, 76, 127–141. [Google Scholar] [CrossRef]

- Fernandez, R.; Hofman, A.; Aalbers, M.B. London and New York as a safe deposit box for the transnational wealth elite. Environ. Plan. A Econ. Sp. 2016, 48, 2443–2461. [Google Scholar] [CrossRef]

- Ho, H.K.; Atkinson, R. Looking for big ‘fry’: The motives and methods of middle-class international property investors. Urban Stud. 2018, 55, 2040–2056. [Google Scholar] [CrossRef] [Green Version]

- Knight Frank International Residential Investment in London: International Project Marketing 2013. Available online: https://content.knightfrank.com/research/503/documents/en/2013-1217.pdf (accessed on 10 December 2019).

- Zheng, S. Record Complaints as Overseas Sales Sting Hong Kong Investors. Available online: https://www.scmp.com/news/hong-kong/economy/article/2065077/record-complaints-overseas-sales-sting-hong-kong-investors (accessed on 15 December 2019).

- Census and Statistics Department Mid-Year Population for 2018. Available online: https://www.info.gov.hk/gia/general/201808/14/P2018081400417.htm (accessed on 10 December 2019).

- Bangura, M.; Lee, C.L. The differential geography of housing affordability in Sydney: A disaggregated approach. Aust. Geogr. 2019, 50, 295–313. [Google Scholar] [CrossRef]

- Lee, C.L. An examination of the risk-return relation in the Australian housing market. Int. J. Hous. Mark. Anal. 2017, 10, 431–449. [Google Scholar] [CrossRef]

- Lee, M.-T.; Lee, C.L.; Lee, M.-L.; Liao, C.-Y. Price linkages between Australian housing and stock markets. Int. J. Hous. Mark. Anal. 2017, 10, 305–323. [Google Scholar] [CrossRef]

- Revington, N.; Townsend, C. Market Rental Housing Affordability and Rapid Transit Catchments: Application of a New Measure in Canada. Hous. Policy Debate 2016, 26, 864–886. [Google Scholar] [CrossRef]

- Fleming, T.; Damon, W.; Collins, A.B.; Czechaczek, S.; Boyd, J.; McNeil, R. Housing in crisis: A qualitative study of the socio-legal contexts of residential evictions in Vancouver’s Downtown Eastside. Int. J. Drug Policy 2019, 71, 169–177. [Google Scholar] [CrossRef]

- Rogers, D.; Koh, S.Y. The globalisation of real estate: The politics and practice of foreign real estate investment. Int. J. Hous. Policy 2017, 17, 1–14. [Google Scholar] [CrossRef]

- Joseph, L.; Belisle, P. Bayesian Sample Size Determination for Case-Control Studies When Exposure May be Misclassified. Am. J. Epidemiol. 2013, 178, 1673–1679. [Google Scholar] [CrossRef] [Green Version]

- Krejcie, R.V.; Morgan, D.W. Determining Sample Size for Research Activities. Educ. Psychol. Meas. 1970, 30, 607–610. [Google Scholar] [CrossRef]

- Bekiros, S.; Nguyen, D.K.; Sandoval Junior, L.; Salah Uddin, G. Information Diffusion, Cluster formation and Entropy-based Network Dynamics in Equity and Commodity Markets. Eur. J. Oper. Res. 2015, 256, 945–961. [Google Scholar] [CrossRef] [Green Version]

- Harremoës, P.; Topsøe, F. Maximum Entropy Fundamentals. Entropy 2001, 3, 191–226. [Google Scholar] [CrossRef]

- Zhang, Y.-C. Toward a Theory of Marginally Efficient Markets. Phys. A Stat. Mech. Its Appl. 1999, 269, 30–44. [Google Scholar] [CrossRef] [Green Version]

- Mercer. Western European Cities–Top Quality of Living Ranking; Mercer: London, UK, 2016. [Google Scholar]

- Swierenga, R.P. Land Speculation and Its Impact on American Economic Growth and Welfare: A Historiographical Review. West. Hist. Q. 1977, 8, 283. [Google Scholar] [CrossRef]

- Clawson, M. Urban Sprawl and Speculation in Suburban Land. In A Geography of Urban Places; Putnam, R.G., Taylor, F.J., Kettle, P.K., Eds.; Routledge: London, UK, 1970; pp. 329–342. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Land Bought (m2) | Location | Year Purchased | Year Developed | † Price per m2 | Document Title When Purchased | Status | Vacant Period (Years) |

|---|---|---|---|---|---|---|---|

| 160 | Awasho | 1997 | not developed | 2000 | illegal receipt | Vacant | 23 |

| 220 | Awasho | 1998 | not developed | 1400 | illegal receipt | Vacant | 22 |

| 320 | Awasho | 2000 | not developed | 1000 | illegal receipt | Vacant | 19 |

| 350 | Awasho | 2001 | not developed | 2500 | illegal receipt | Underutilized | 18 |

| 200 | Awasho | 2004 | not developed | 4000 | illegal receipt | Vacant | 16 |

| 6900 | Awasho | 2015 | not developed | 5000 | legal receipt | Vacant | 5 |

| 350 | Alelu | 2001 | not developed | 4000 | family receipt | Vacant | 19 |

| 250 | Alelu | 2005 | not developed | 3500 | illegal receipt | Vacant | 15 |

| 140 | Alelu | 2013 | not developed | 2500 | legal receipt | Vacant | 7 |

| 500 | Arada | 1997 | not developed | 3500 | illegal receipt | Vacant | 23 |

| 450 | Arada | 1995 | 2013 | 4500 | illegal receipt | developed | 19 |

| 400 | Bulchana | 1991 | not developed | 875 | family receipt | Underutilized | 29 |

| 320 | Bulchana | 1998 | 2016 | 3500 | illegal receipt | Developed | 19 |

| 140 | Dida Boke | 1997 | 2005 | 4500 | illegal receipt | Developed | 9 |

| 250 | Dida Boke | 2000 | 2014 | 3500 | illegal receipt | Developed | 15 |

| 250 | Dida Boke | 2004 | not developed | 980 | legal receipt | Vacant | 16 |

| 200 | Kuyera | 2011 | not developed | 1050 | legal receipt | Vacant | 9 |

| † Variable | Comp1 | Comp2 | Comp 3 | Comp 4 | Comp 5 | Comp 6 | Comp 7 | Unexplained |

|---|---|---|---|---|---|---|---|---|

| Q1 | −0.2115 | 0.6684 | −0.1562 | 0.1136 | −0.1684 | −0.6653 | 0.0144 | 0 |

| Q2 | −0.3811 | 0.0490 | 0.4494 | −0.1927 | 0.7660 | −0.1616 | 0.0190 | 0 |

| Q3 | −0.1903 | 0.1367 | 0.7892 | 0.2840 | −0.4580 | 0.1774 | 0.0201 | 0 |

| Q4 | −0.2884 | 0.5696 | −0.2687 | 0.0696 | 0.1431 | 0.7032 | 0.0192 | 0 |

| Q5 | 0.2873 | −0.0128 | −0.0217 | 0.8822 | 0.3697 | −0.0423 | −0.0089 | 0 |

| Q6 | 0.5470 | 0.3424 | 0.2116 | −0.2120 | 0.0973 | 0.0461 | −0.6984 | 0 |

| Q7 | 0.5607 | 0.3004 | 0.1827 | −0.2032 | 0.0918 | 0.0383 | 0.7147 | 0 |

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy | 0.60 | |

|---|---|---|

| Bartlett’s test of sphericity | approx. chi-square | 192.773 |

| - | df | 21 |

| - | sig | 0.000 |

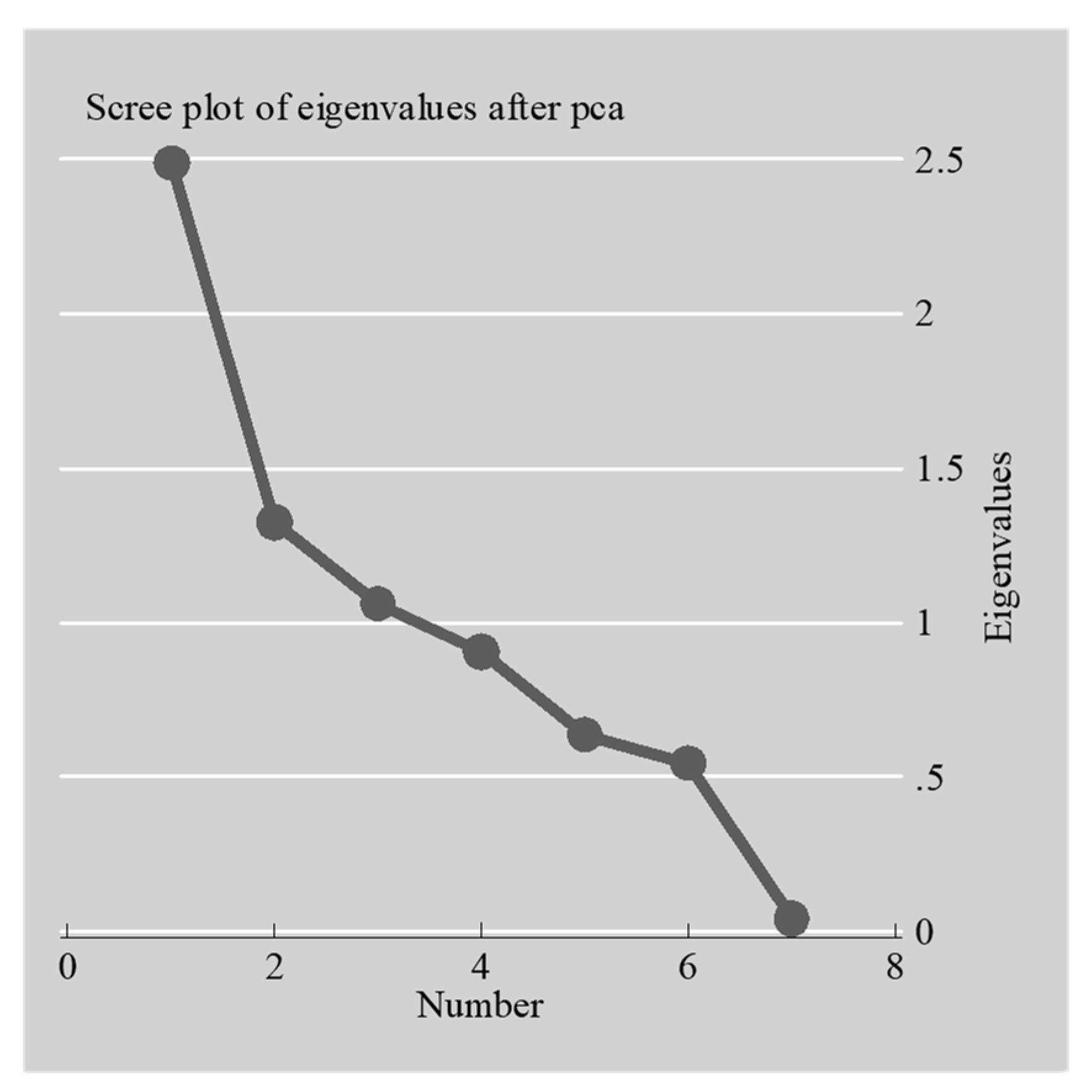

| Component | Initial Eigenvalues | Cumulative Percentage of Variance | |

|---|---|---|---|

| Total | Percent of Variance | ||

| 1 | 2.48345 | 35.48 | 35.48 |

| 2 | 1.32565 | 18.94 | 54.42 |

| 3 | 1.0619 | 15.17 | 69.59 |

| 4 | 0.907426 | 12.96 | 82.55 |

| 5 | 0.636939 | 9.10 | 91.65 |

| 6 | 0.544361 | 7.78 | 99.42 |

| 7 | 0.0402671 | 0.58 | 100.00 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gemeda, B.S.; Abebe, B.G.; Paczoski, A.; Xie, Y.; Cirella, G.T. What Motivates Speculators to Speculate? Entropy 2020, 22, 59. https://doi.org/10.3390/e22010059

Gemeda BS, Abebe BG, Paczoski A, Xie Y, Cirella GT. What Motivates Speculators to Speculate? Entropy. 2020; 22(1):59. https://doi.org/10.3390/e22010059

Chicago/Turabian StyleGemeda, Bedane S., Birhanu G. Abebe, Andrzej Paczoski, Yi Xie, and Giuseppe T. Cirella. 2020. "What Motivates Speculators to Speculate?" Entropy 22, no. 1: 59. https://doi.org/10.3390/e22010059

APA StyleGemeda, B. S., Abebe, B. G., Paczoski, A., Xie, Y., & Cirella, G. T. (2020). What Motivates Speculators to Speculate? Entropy, 22(1), 59. https://doi.org/10.3390/e22010059