1. Introduction

Corporate social responsibility (CSR) has become a fast-growing essential requirement for a long-lasting enterprise in the recent decade. Consumers and governmental organizations have an increasing demand for CSR programs, nowadays. CSR is the allusion of firm behavior and one of the major issues in the business environment. It deals with a firm’s relationship toward stakeholders and the increasingly recognized moral implications in investments [

1]. In addition, preservation of the environment, social participation, and good governance in business operations and reciprocity with their stakeholders are the basis of firms’ citizenship and voluntary initiatives [

2,

3]. The significant effect of CSR on financial performance has an overriding relevance on businesses, society, and nation-building [

4].

Based on the landscape of literature on CSR, related issues and phenomenon have been discussed in general context. The investigation of this matter is relevant to the increasing recognition of CSR performance in a specific industry [

5]. There are few studies which contemplate the analysis of CSR into sustainability and the cognizance of this strategy in a specific sector, with firms as the evaluating unit [

6]. For instance, there is an increasing awareness from consumers and other stakeholders of firms from food industry regarding their purchasing power on reducing the demand for goods perceived as sustainable over non-sustainable [

5]. In addition, Cuganesan et al. [

5] mentioned that governments around the world are taking initiatives and actions in promoting CSR. This study extends the arguments of how CSR performance differs across industries to how it might differ within industries.

Firms from food industry have started to notice complexities in sustainability in terms of social, environmental, and economic aspects [

6]. The perception and criticism of consumers regarding insufficient CSR programs can be destructive to a company [

7]. In addition, the integration of supply chain accountability into CSR causes challenging issues in the management of socially responsible programs [

7]. Rana et al. [

6] mentioned that an unlimited case of issues such as labor practices and relationship between firms and community are accompanied by opportunities for a better standard of living through increased access to knowledge and technology. In addition, Rana et al. [

6] alluded that the concern on community relations is escalated in the food industry of developing economies. The rising importance and relevance of such issues in the progression of the industry landscape, has become a key factor in business growth and strategy [

6].

Value creation is the main concern in the effective utilization of the resources of a company, aligned from formulation of strategic programs and policies. Intellectual capital (IC) exists in all organizations as a stock of knowledge-based resources which an organization potentially can use in its value creation process [

8]. Ethiraj, Kale, Krishnan, and Singh [

9] and Haas and Hansen [

10] mentioned that IC is an essential intangible requirement in the formation of corporate value. However, the increasing recognition of CSR programs with strong emphasis on social and environmental concerns to the conduct of business operations, for the purpose of solving issues in society [

11], creates a huge debate and comprises the management of stakeholder relationships [

12]. CSR can be associated as a strategic program of firms when it supports core business activities in promoting effectiveness and efficiency of firms to achieve its goal and generate substantial business-related benefits [

13]. In fact, the relevance of CSR has attracted the attention of academics, practitioners, and policy makers [

14].

Most of the prior studies reveal that CSR is a definitive factor of financial performance. Other facets of this phenomenon have been uncertain [

15]. Moreover, prior research projects reveal that IC increases the value of the company and generates profitability [

16,

17]. The uncertainty in the past literature offers a great chance to examine the phenomenon with comprehensive reflections and estimates. We conjecture that the cognizance of the phenomenon is relevant and useful in promoting IC and CSR activities among business firms. Following the proposition of Razafindrambinina and Kariodimedjo [

18], we contemplate that investigating corporate financial performance in an empirical study would deliver a better cognizance in a correlative study of CSR. Hence, we propose that a major issue in the pervasiveness of IC is its impact on CSR and this relationship is mediated by corporate financial performance.

To address these important issues, we developed an empirical study to fill the gaps in the literature. This study aims to investigate the phenomenon through the mediating role of corporate financial performance in the relationship between IC and CSR. CSR is a factor in improving IC which leads to better financial performance [

4]. We conjecture that the effective and efficient utilization of IC would cause profitability advantage and CSR performance, eventually. We examine the phenomenon in the context of firms from the food industry in Asia. Food industry has substantial visibility to the public and plays a large role in daily human life and the economy. This industry also contends many CSR challenges such as food safety, obesity, abuse of alcohol, and packaging management [

5]. The Center for Livable Future [

19] mentioned that food sustainability-related issues are a concern for American voters. In the USA and Europe, food citizenship is a common concept [

20]. Morin [

20] added that expectations of the majority of Asian consumers are changing. Asia is mostly composed of developing countries. Recently, lawmakers, businesses, and mass media are attentive to the issues of poor labor practices and working conditions in developing economies [

21]. For instance, the cost reduction of materials and processes by transferring the production to developing countries, increases the problem of food safety [

22]. In addition, Perkowski [

22] mentioned that the profitability of firms from developing countries is associated with the low cost of production but it affects the environment due to carbon footprint caused by logistic complexities.

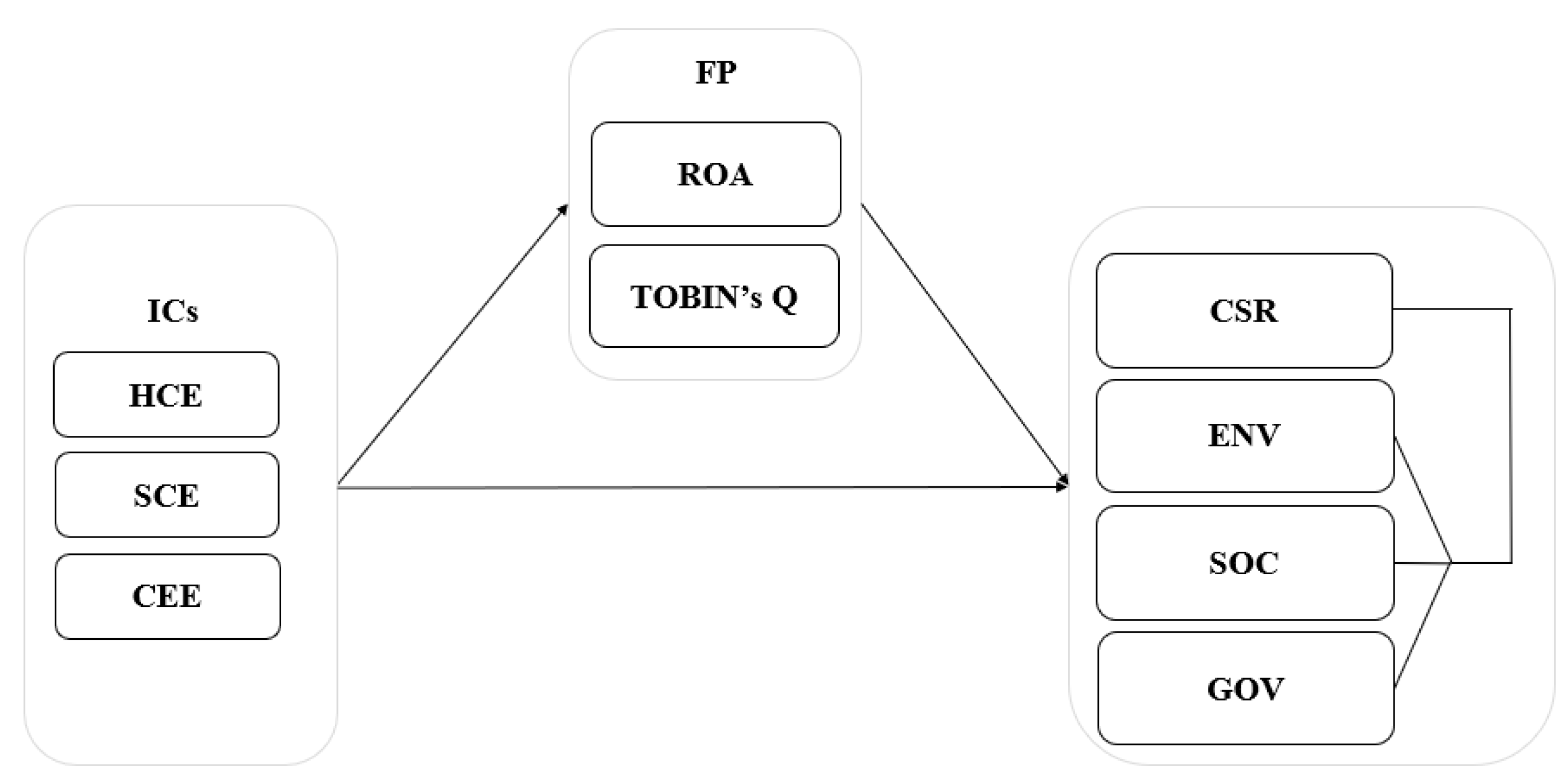

Our main analysis focuses on the effects of IC components (ICs) such as human capital efficiency (HCE), structural capital efficiency (SCE), and capital employed efficiency (CEE) on the composite ratings of CSR. We also reflect on three pillars of CSR namely: environmental, social, and corporate governance to disaggregate the effects of the combined CSR scores. Moreover, this study contemplates the mediating effects of return on assets (ROA) and Tobin’s Q as proxies of corporate financial performance. This research article endows to the body of knowledge of firms’ efficiency and strategic approaches for the formation of value to firms from the food industry. We conduct an extensive knowledge generation in the literature on the relationships between IC and corporate social responsibility of firms from food industry, an industry currently facing sustainability challenges. Our evidence provides enlightenment to this industry about the beneficial roles of IC in implementing corporate social responsibility activities. Lastly, our empirical findings serve as a guide to the management of firms from food industry in utilizing resources through IC investments and promoting CSR programs which create value for the business and stakeholders.

The remainder of the paper is organized as follows:

Section 2 briefly discusses and reviews the empirical literature regarding IC, financial performance, and CSR. It also presents the formulated hypotheses of the study.

Section 3 expounds the methodology applied in this study.

Section 4 presents the empirical results and discussions. Lastly,

Section 5 concludes the paper and recommends further studies.

4. Results and Discussions

Table 1 presents the descriptive statistics and the correlation coefficients between all of the variables utilized in this study.

Table 1 shows that CSR has a mean value of 47.62 based on the Thomson Reuters ESG database. The components of CSR show that SOC has the highest mean value of 56.04 while GOV has the lowest mean value of 33.40. Return on assets (ROA) shows a mean value of 6.35, which indicates that most of the firms from the food industry in Asia have an efficient utilization of assets to generate earnings. Tobin’s Q shows a mean value of 1.52 × 10

−3, indicating that capital of firms from food industry is valued by the stock market less than its replacement cost. ICs such as HCE show a highest mean value of 11.23. CSR is significantly and positively related to its components.

We conducted a separate regression for each component to identify the individual effect of ICs on each CSR pillar. CEE is significantly and positively related to CSR, implying that as the level of CEE increases, the value of CSR also increases. In addition, RDI, ROA, and Tobin’s Q are positively and significantly related to CSR. SCE has a positive and significant relation on ENV and SOC while CEE has a positive and significant relation on ENV and SOC. However, HCE is significantly and positively related to GOV, implying that as the human capital efficiency of firms increases, its corporate governance improves.

We performed regression analysis to examine the mediating effect of corporate financial performance on the relationship between ICs and CSR and its pillars.

Table 2 shows the regression results of the mediating effect of corporate financial performance on the relationship between ICs and CSR. Model 1 of

Table 2 shows that CEE has a positive and significant effect on CSR with β = 0.19 at

p < 0.01. This finding supports H1a which states that ICs (CEE) have a positive relationship with CSR. Our findings about the effect of CEE on CSR of firms from the food industry are similar to the result of firms from banking industry from the study of Musibah and Alfattani [

26].

Model 2 presents the relationship between the components of IC and financial performance (ROA and Tobin’s Q).

Table 2 shows CEE has a positive and significant effect on corporate financial performance represented by ROA and Tobin’s Q with β = 0.44 at

p < 0.01 and β = 0.29 at

p < 0.01, respectively. In addition, SCE has a positive and significant effect on Tobin’s Q with β = 0.41 at

p < 0.01. These findings are consistent with H2 which states that there is a positive relationship between ICs and financial performance (ROA and Tobin’s Q). However, HCE has a negative and significant relationship with ROA and Tobin’s Q at β = −0.30 at

p < 0.05 and β = 0.46 at

p < 0.01, respectively. These findings are inconsistent with H2. Model 3 presents the relationship between the firms’ financial performance (ROA and Tobin’s Q) and CSR.

Table 2 shows that Tobin’s Q has a negative and significant effect on CSR with β = −0.18 at

p < 0.01. In addition, ROA has insignificant impact on CSR. These outcomes do not support H3a which states that the higher the financial performance, the higher the CSR will be.

Model 4 presents the results of the mediating effect of corporate financial performance on the relationship between ICs and CSR. Model 4 of

Table 2 shows that CEE has a positive and significant effect on CSR with β = 0.21 at

p < 0.01. ROA shows an insignificant effect on CSR. Hence, ROA has no mediating effect on the relationship between ICs and CSR, inconsistent with H4a. Moreover, Model 4 of

Table 2 shows that CEE has a positive and significant effect on CSR with β = 0.28 at

p < 0.01. Tobin’s Q has a negative and significant effect on CSR with β = −0.29 at

p < 0.01. Hence, Tobin’s Q partially mediates the relationship between ICs and CSR, consistent with H4a

. This result provides evidence that financial performance in terms of the combination of accounting and market-based measures has an arbitrary impact on the relationship between the components of IC and CSR, a result conforming to the findings of Musibah and Alfattani [

26]. However, HCE and SCE have an insignificant effect on CSR. Hence, Tobin’s Q has no mediating effect on the relationship between these ICs and CSR.

Table 3 shows the regression results of the mediating effect of corporate financial performance on the relationship between ICs and the environmental pillar of CSR. Model 1 of

Table 3 shows that CEE has a positive and significant effect on ENV with β = 0.13 at

p < 0.10. This finding supports H1b which states that ICs (CEE) have a positive relationship with ENV. Our findings about the effect of CEE on ENV of firms from the food industry indicate that a higher capital-employed efficiency of firms from the food industry is an advantage to conduct socially responsible activities for the environment. In addition, we postulate that the other intellectual components are not relevant to environmental CSR but have significance on the other CSR pillars.

Model 2 presents the relationship between the components of IC and financial performance (ROA and Tobin’s Q).

Table 3 shows CEE has a positive and significant effect on corporate financial performance represented by ROA and Tobin’s Q with β = 0.44 at

p < 0.01 and β = 0.29 at

p < 0.01, respectively. In addition, SCE has a positive and significant effect on Tobin’s Q with β = 0.41 at

p < 0.01. These findings are consistent with H2 which states that there is a positive relationship between ICs and financial performance (ROA and Tobin’s Q). However, HCE has a negative and significant relationship with ROA and Tobin’s Q at β = −0.30 at

p < 0.05 and β = 0.46 at

p < 0.01, respectively. These findings are inconsistent with H2. Model 3 presents the relationship between the firms’ financial performance (ROA and Tobin’s Q) and ENV.

Table 3 shows that Tobin’s Q has a negative and significant effect on ENV with β = −0.14 at

p < 0.10. In addition, ROA has an insignificant impact on ENV. These outcomes do not support H3b which states that the higher the financial performance, the higher ENV will be.

Model 4 presents the results of the mediating effect of corporate financial performance on the relationship between ICs and ENV. Model 4 of

Table 3 shows that CEE has a positive and significant effect on ENV with β = 0.15 at

p < 0.10. ROA shows an insignificant effect on ENV. Hence, ROA has no mediating effect on the relationship between ICs and ENV, inconsistent with H4b. Moreover, Model 4 of

Table 3 shows that CEE has a positive and significant effect on ENV with β = 0.20 at

p < 0.01. Tobin’s Q has a negative and significant effect on ENV with β = −0.22 at

p < 0.01. Hence, Tobin’s Q partially mediates the relationship between ICs and ENV, consistent with H4b

. This result provides evidence that financial performance in terms of the combination of accounting and market-based measures has an arbitrary impact on the relationship between the components of IC and ENV. However, HCE and SCE have an insignificant effect on ENV. Hence, Tobin’s Q has no mediating effect on the relationship between these ICs and ENV.

Table 4 shows the regression results of the mediating effect of corporate financial performance on the relationship between ICs and the social pillar of CSR. Model 1 of

Table 4 shows that CEE has a positive and significant effect on SOC with β = 0.25 at

p < 0.01. This evidence supports H1c which states that there is a positive relationship ICs and SOC. HCE has negative and significant effect on SOC with β = −0.36 at

p < 0.05, inconsistent with H1c. However, SCE has an insignificant effect on SOC. We conjecture that a higher capital-employed efficiency is an advantage to conduct socially responsible activities in firms from the food industry for the community, employees, and other related social aspects. In addition, we infer that the SCE is not relevant while HCE has an inverse impact on the social pillar of CSR. The social pillar is composed of workforce, human rights, community, and product responsibility categories. Human capital is embodied in employees and includes their expertise, experience, skills, and motivation [

34]. The structural capital component of IC is focused on building infrastructure needed by human capital to create value. Hence, there is a trade-off between HCE, SCE, and SOC.

Model 2 presents the relationship between the components of IC and financial performance (ROA and Tobin’s Q).

Table 4 shows CEE has a positive and significant effect on corporate financial performance represented by ROA and Tobin’s Q with β = 0.44 at

p < 0.01 and β = 0.29 at

p < 0.01, respectively. In addition, SCE has a positive and significant effect on Tobin’s Q with β = 0.41 at

p < 0.01. These findings are consistent with H2 which states that there is a positive relationship between ICs and financial performance (ROA and Tobin’s Q). However, HCE has negative and significant relationship with ROA and Tobin’s Q at β = −0.30 at

p < 0.05 and β = 0.46 at

p < 0.01, respectively. These findings are inconsistent with H2. Model 3 presents the relationship between firms’ financial performance (ROA and Tobin’s Q) and ENV. This outcome does not support H3c which states that the higher the financial performance, the higher the SOC will be.

Table 4 shows that ROA has a positive and significant effect on SOC with β = 0.14 at

p < 0.10. In addition, Tobin’s Q has an insignificant impact on SOC.

Model 4 presents the results of the mediating effect of corporate financial performance on the relationship between ICs and SOC. Model 4 of

Table 4 shows that CEE has a positive and significant effect on SOC with β = 0.24 at

p < 0.01. HCE has a negative and significant effect on SOC with β = −0.35 at

p < 0.10. However, SCE has an insignificant effect on SOC. ROA has an insignificant effect on SOC. Hence, ROA has no mediating effect on the relationship between ICs and SOC, inconsistent with our hypothesis. This finding provides evidence that financial performance in terms of the accounting measure has no arbitrary impact on the relationship between the ICs and SOC activities of firms from the food industry. Moreover, Model 4 of

Table 4 shows that SCE and CEE have positive and significant effects on SOC with β = 0.41 at

p < 0.05 and β = 0.31 at

p < 0.01, respectively. HCE has a negative and significant effect on SOC with β = −0.45 at

p < 0.05. Tobin’s Q shows a negative and significant effect on SOC with β = −0.20 at

p < 0.05. Hence, Tobin’s Q has a partially mediating effect on the relationship between ICs and the social pillar of CSR, consistent with the hypothesis of the study. These findings provide evidence that financial performance in terms of the combination of accounting and market-based measure has an arbitrary impact on the relationship between ICs and SOC.

Table 5 shows the regression results of the mediating effect of corporate financial performance on the relationship between ICs and the governance pillar of CSR. Model 1 of

Table 5 shows that HCE, SCE, and CEE have an insignificant effect on GOV. These findings are not parallel to H1d which states that a positive relationship between ICs and GOV exists on firms from the food industry in Asia. We infer that the ICs are not relevant to the governance pillar of CSR. The governance pillar is consisted of categories such as management, shareholders, and CSR strategies.

Model 2 presents the relationship between the components of IC and financial performance (ROA and Tobin’s Q).

Table 5 shows CEE has a positive and significant effect on corporate financial performance represented by ROA and Tobin’s Q with β = 0.44 at

p < 0.01 and β = 0.29 at

p < 0.01, respectively. In addition, SCE has a positive and significant effect on Tobin’s Q with β = 0.41 at

p < 0.01. These findings are consistent with H2 which states that there is a positive relationship between ICs and financial performance (ROA and Tobin’s Q). However, HCE has a negative and significant relationship with ROA and Tobin’s Q at β = −0.30 at

p < 0.05 and β = 0.46 at

p < 0.01, respectively. These findings are inconsistent with H2. Model 3 presents the relationship between firms’ financial performance (ROA and Tobin’s Q) and ENV.

Table 5 shows that Tobin’s Q has a negative and significant effect on GOV with β = −0.25 at

p < 0.01. In addition, ROA has an insignificant impact on SOC. These outcomes do not support H3d which states that the higher the financial performance, the higher the GOV will be.

Model 4 presents the results of the mediating effect of corporate financial performance on the relationship between ICs and GOV. Model 4 of

Table 5 shows that CEE has positive and significant effect on GOV with β = 0.13 at

p < 0.05. HCE and SCE have an insignificant effect on GOV. ROA shows a negative and significant effect on GOV with β = −0.13 at

p < 0.05. Moreover, Model 4 of

Table 5 shows that CEE has a positive and significant effect on GOV with β = 0.16 at

p < 0.01. HCE and SCE have an insignificant effect on GOV. Tobin’s Q shows a negative and significant effect on GOV with β = −0.31 at

p < 0.01. Hence, ROA and Tobin’s Q partially mediate the relationship between ICs and SOC, consistent with the hypothesis of the study. These findings provide evidence that financial performance in terms of the accounting measure and the combination of accounting and market-based measures have an arbitrary impact on the relationship between the ICs and SOC. However, HCE and SCE have an insignificant effect on GOV. Hence, financial performance has no mediating effect on the relationship between these ICs and GOV. The hypotheses results are presented in

Table 6.

5. Conclusions

This study investigates the mediating effect of corporate financial performance on the relationship between ICs and CSR of firms the from food industry in Asia. We dwell on prior literature stating that IC and CSR are responsible in value formation for better financial performance. Hence, we proposed that a major issue in the pervasiveness of IC is its impact on CSR and the relationship is mediated by corporate financial performance. We conjecture that the cognizance of the phenomenon is relevant and useful in promoting IC and CSR activities among business firms from the food industry.

This article reveals that intellectual capital and CSR are strategies implemented by firms from the food industry in Asia since improvements in economic value are observed based on composite ratings. Our main findings show that a firm’s investment on capital-employed efficiency generates better composite CSR, ENV, and SOC ratings, which support proponents of the stakeholder theory and resource-based perspective. However, the investments of firms from the food industry in human capital generates lower SOC ratings. In addition, the structural capital efficiency has no significant implication with CSR and its dimensions. Our findings also reveal that a higher CEE generates a better financial performance, both ROA and Tobin’s Q. In addition, a higher SCE generates better financial outcome in terms of Tobin’s Q. However, a higher HCE reflects a lower financial performance both in ROA and Tobin’s Q. Human capital is an employee-related investment to enhance their capabilities and expertise while structural capital is focused on building infrastructure needed by human capital to create value. We conjecture that CEE and SCE are investments which are in line in making more profits for the company. On the other hand, HCE has an immediate effect as it increases costs which lessen the profitability and performance of the company. We infer that this effect can be seen in the long-run as IC components are interrelated in the creation of value for the company.

In terms of financial performance, Tobin’s Q reveals a consistently negative effect on CSR and its pillars while ROA has a favorable effect on SOC. Tobin’s Q is a combination of accounting and market-based estimates of financial performance. These negative effects are associated with the treatment of firms from the food industry as an additional cost due to different compliance and demands from stakeholders. We conjecture that in the long-run, firms from this industry will benefit from CSR initiatives. Lastly, this study asserts that financial performance thru Tobin’s Q partially mediates the relationship between CEE and CSR and its pillars. Moreover, it partially mediates the relationship between other ICs such as HCE, SCE, and SOC. ROA has no mediating effect on ICs and CSR and its pillars. However, it partially mediates the relationship between CEE and GOV.

This study makes a number of theoretical and practical contributions about the dynamics and evolution of IC, financial performance, and CSR. The present study provides findings which can be used in the cognizance of the phenomenon among corporate citizenship, knowledge-based resources, and value creation for sustainability of doing business in the food industry. Theoretically, we contemplate on an integrated model to explain how intellectual components affect CSR. We include firm financial performance as a mediator to the existing relationship in this important issue at a specific context. Hence, this article provides new empirical evidence from the inconclusive findings from prior literature.

This study also sheds greater light on the importance of IC and socially responsible activities to boost value formation in the food industry context. This industry has substantial visibility to the public and plays a large role in daily human life and the economy and contends with many CSR issues such as food safety, obesity, abuse of alcohol, and packaging management. We suggest that firms from the food industry reflect on these findings as ICs have varied effects on CSR and its pillars. Intangible resources and socially responsible activities should be reported properly to serve as a basis for proper evaluation of the company. Policy makers may reflect on the findings of this research based on the increasing efforts in encouraging CSR engagements in the food industry. A firm’s decision makers should contemplate the idea that CSR initiatives and IC improvements are investments which create a positive image and generate earnings in the long-run. We conjecture that acknowledging the essence of ethical practices with proper management of knowledge resources will lead to greater consumer demand and employee productivity, firm efficiency, and better corporate financial performance. We believe that the cognizance of the phenomenon regarding the investment of firms from the food industry in intellectual capital, compliance and recognition of CSR activities, and profitability and performance, are important issue to ensure food security.

This study examines a limited number of data of food industry firms from the countries available in Thomson Reuters ESG database. We propose that a greater number of representative firms from the food industry in most, if not all, countries in Asia be included for better cognizance of the phenomenon. Our results are subject to verification since the effect of IC and CSR and the mediating effect of financial performance is still inconclusive. Hence, we propose future studies to investigate the magnitude to which this result can be further generalized. Lastly, we suggest that new research examines the impact of the phenomenon in other contexts such as industry and country specifics and creates comparisons for a better understanding of the issue.

{kind=link}