How Do Firms Promote Green Innovation through International Mergers and Acquisitions: The Moderating Role of Green Image and Green Subsidy

Abstract

:1. Introduction

2. Theory and Hypotheses

2.1. The Driver of Green Innovation

2.2. The Nature of Exploratory and Exploitative International M&As

2.3. Impacts of Exploratory and Exploitative International M&As on Green Innovation Performance

2.3.1. Exploratory International M&As and Green Innovation Performance

2.3.2. Exploitative International M&As and Green Innovation Performance

2.4. Strategic and Environmental Contingencies of Exploratory and Exploitative International M&As

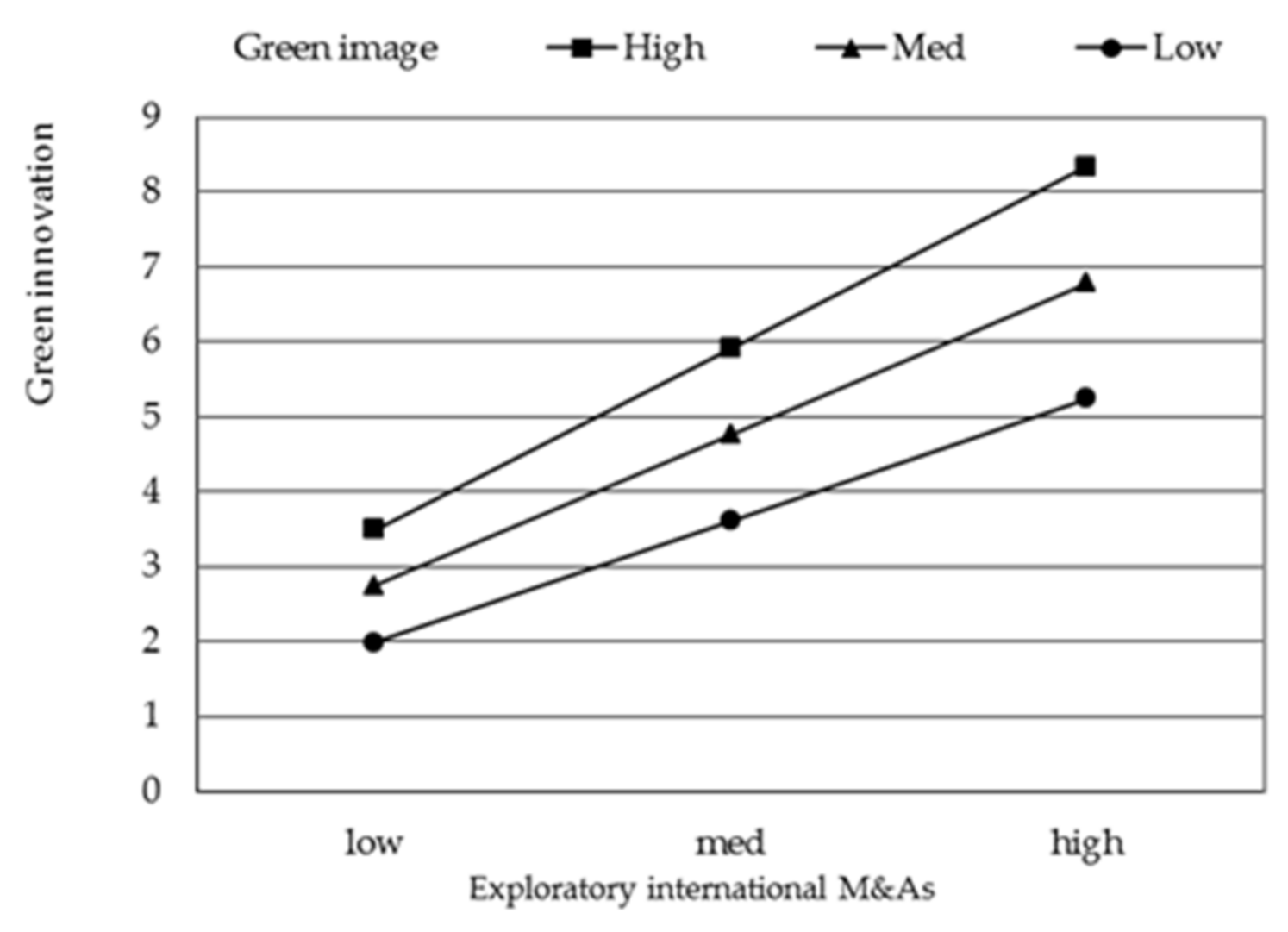

2.4.1. Strategic Fit: Exploratory International M&As, Exploitative International M&As and Green Image

2.4.2. Environmental Fit: Exploratory International M&As, Exploitative International M&As and Green Subsidy

3. Methodology

3.1. Sample and Data Collection

3.2. Measures

3.2.1. Dependent Variable

3.2.2. Independent Variables

3.2.3. Moderating Variables

3.2.4. Control Variables

4. Analysis and Results

4.1. Validity of Variable Scales

4.2. Descriptive Statistics

4.3. Tests of Hypotheses

4.4. Supplementary Analyses

5. Discussion

5.1. Main Findings

5.2. Theoretical and Managerial Implications

5.3. Limitations and Future Research Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Berrone, P.; Fosfuri, A.; Gelabert, L.; Gomez-Mejia, L.R. Necessity as the mother of ‘green’ inventions: Institutional pressures and environmental innovations. Strateg. Manag. J. 2013, 34, 891–909. [Google Scholar] [CrossRef]

- Cuerva, M.C.; Triguero-Cano, Á.; Córcoles, D. Drivers of green and non-green innovation: Empirical evidence in Low-Tech SMEs. J. Clean. Prod. 2014, 68, 104–113. [Google Scholar] [CrossRef]

- Xie, X.; Huo, J.; Zou, H. Green process innovation, green product innovation, and corporate financial performance: A content analysis method. J. Bus. Res. 2019, 101, 697–706. [Google Scholar] [CrossRef]

- Albort-Morant, G.; Leal-Millan, A.; Cepeda-Carrion, G. The antecedents of green innovation performance: A model of learning and capabilities. J. Bus. Res. 2016, 69, 4912–4917. [Google Scholar] [CrossRef]

- Kesidou, E.; Demirel, P. On the drivers of eco-innovations: Empirical evidence from the UK. Res. Policy 2012, 41, 862–870. [Google Scholar] [CrossRef]

- Ghisetti, C.; Marzucchi, A.; Montresor, S. The open eco-innovation mode. An empirical investigation of eleven European countries. Res. Policy 2015, 44, 1080–1093. [Google Scholar] [CrossRef]

- Horbach, J.; Rammer, C.; Rennings, K. Determinants of eco-innovations by type of environmental impactdthe role of regulatory push/pull, technology push and market pull. Ecol. Econ. 2012, 78, 112–122. [Google Scholar] [CrossRef] [Green Version]

- Marchi, V.D. Environmental innovation and R&D cooperation: Empirical evidence from Spanish manufacturing firms. Res. Policy 2012, 41, 614–623. [Google Scholar] [CrossRef]

- Wu, H.; Chen, J. International ambidexterity in firms’ innovation of multinational enterprises from emerging economies: An investigation of TMT attributes. Balt. J. Manag. 2020, 15, 431–451. [Google Scholar] [CrossRef]

- Makino, S.; Lau, C.-M.; Yeh, R.-S. Asset-exploitation versus asset-seeking: Implications for location choice of foreign direct investment from newly industrialized economies. J. Int. Bus. Stud. 2002, 33, 403–421. [Google Scholar] [CrossRef]

- Prange, C.; Verdier, S. Dynamic capabilities, internationalization process and performance. J. World Bus. 2011, 46, 126–133. [Google Scholar] [CrossRef]

- Bandeira-de-Mello, R.; Fleury, M.T.L.; Aveline, C.E.S.; Gama, M.A.B. Unpacking the ambidexterity implementation process in the internationalization of emerging market multinationals. J. Bus. Res. 2016, 69, 2005–2017. [Google Scholar] [CrossRef]

- Rennings, K. Redefining innovation eco-innovation research and the contribution from ecological economics. Ecol. Econ. 2000, 32, 319–332. [Google Scholar] [CrossRef]

- Kemp, R. Eco-innovation: Definition, measurement and open research issues. Econ. Politics 2010, 27, 397–420. [Google Scholar] [CrossRef] [Green Version]

- Peng, Y.S.; Lin, S.S. Local responsiveness pressure, subsidiary resources, green management adoption and subsidiary’s performance: Evidence from Taiwanese manufactures. J. Bus. Ethics 2008, 79, 199–212. [Google Scholar] [CrossRef]

- Lin, R.J.; Tan, K.H.; Geng, Y. Market demand, green product innovation, and firm performance: Evidence from Vietnam motorcycle industry. J. Clean. Prod. 2013, 40, 101–107. [Google Scholar] [CrossRef]

- De Marchi, V.; Grandinetti, R. Knowledge strategies for environmental innovations: The case of Italian manufacturing firms. J. Knowl. Manag. 2013, 17, 569–582. [Google Scholar] [CrossRef]

- Carrillo-Hermosilla, J.; Rio, P.; Konnola, T. Diversity of eco-innovations: Reflections from selected case studies. J. Clean. Prod. 2010, 18, 1073–1083. [Google Scholar] [CrossRef]

- Dunning, J.H. International Production and the Multinational Enterprises; Allen and Unwin: London, UK, 1981. [Google Scholar]

- Hsu, C.-W.; Lien, Y.-C.; Chen, H. International ambidexterity and firm performance in small emerging economies. J. World. Bus. 2013, 48, 58–67. [Google Scholar] [CrossRef]

- Martineaua, C.; Pastoriza, D. International involvement of established SMEs: A systematic review of antecedents, outcomes and moderators. Int. Bus. Rev. 2016, 25, 458–470. [Google Scholar] [CrossRef]

- Hitt, M.A.; Ireland, R.D.; Harrison, J.S.; Hoskisson, R.E. Effects of acquisitions on R&D inputs and outputs. Acad. Manag. J. 1991, 34, 693–706. [Google Scholar] [CrossRef]

- Vermeulen, F.; Barkema, H. Learning through acquisitions. Acad. Manag. J. 2001, 44, 457–476. [Google Scholar] [CrossRef]

- Hitt, M.A.; Hoskisson, R.E.; Johnson, R.A.; Moesel, D.D. The market for corporate control and firm innovation. Acad. Manag. J. 1996, 39, 1084–1119. [Google Scholar] [CrossRef]

- Healy, P.M.; Palepu, K.G.; Ruback, R.S. Does corporate performance improve after mergers? J. Financ. Econ. 1992, 31, 135–175. [Google Scholar] [CrossRef] [Green Version]

- Ahuja, G.; Riitta, K. Technological acquisitions and the innovation performance of acquiring firms: A longitudinal study. Strateg. Manag. J. 2001, 22, 197–220. [Google Scholar] [CrossRef]

- March, J. Exploration and exploitation in organizational learning. Organ. Sci. 1991, 2, 71–87. [Google Scholar] [CrossRef]

- Levinthal, D.A.; March, J.G. The myopia of learning. Strat. Manag. J. 1993, 14, 95–113. [Google Scholar] [CrossRef]

- Katila, R.; Ahuja, G. Something old, something new: A longitudinal study of search behavior and new product introduction. Acad. Manag. J. 2002, 45, 1183–1194. [Google Scholar] [CrossRef]

- Cainelli, G.; de Marchi, V.; Grandinetti, R. Does the development of environmental innovation require different resources? Evidence from Spanish manufacturing firms. J. Clean. Prod. 2015, 94, 211–220. [Google Scholar] [CrossRef]

- Li, C.R.; Chu, C.P.; Lin, C.J. The contingent value of exploratory and exploitative learning for new product development performance. Ind. Mark. Manag. 2010, 39, 1186–1197. [Google Scholar] [CrossRef]

- Mihalache, O.R.; Jansen, J.J.J.P.; Van Den Bosch, F.A.J.; Volberda, H.W. Offshoring and firm innovation: The moderating role of top management team attributes. Strateg. Manag. J. 2012, 33, 1480–1498. [Google Scholar] [CrossRef]

- Lee, K.H.; Min, B. Green R&D for eco-innovation and its impact on carbon emissions and firm performance. J. Clean. Prod. 2015, 108, 534–542. [Google Scholar] [CrossRef] [Green Version]

- Scott, W.R. Organizations: Rational, Natural, and Open Systems, 3rd ed.; Prentice Hall: Englewood Cliffs, NJ, USA, 1992. [Google Scholar]

- Venkatraman, N. The concept of fit in strategy research: Toward verbal and statistical correspondence. Acad. Manag. Rev. 1989, 14, 423–444. [Google Scholar] [CrossRef]

- Amores-Salvado, J.; Castro, M.D.; Navas-Lopez, J.E. Green corporate image: Moderating the connection between environmental product innovation and firm performance. J. Clean. Prod. 2014, 83, 356–365. [Google Scholar] [CrossRef]

- Chen, Y.S. The drivers of green brand equity: Green brand image, green satisfaction, and green trust. J. Bus. Ethics 2010, 93, 307–319. [Google Scholar] [CrossRef]

- Xie, X.; Huo, J.; Qi, G.; Zhu, K.X. Green process innovation and financial performance in emerging economies: Moderating effects of absorptive capacity and green subsidies. IEEE Trans. Eng. Manag. 2016, 63, 101–112. [Google Scholar] [CrossRef]

- Chen, Y.S.; Lai, S.B.; Wen, C.T. The influence of green innovation performance on corporate advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Chen, Y.-S. The driver of green innovation and green image—Green core competence. J. Bus. Ethics 2008, 81, 531–543. [Google Scholar] [CrossRef]

- Cui, L.; Meyer, K.E.; Hu, H.W. What drives firms’ intent to seek strategic assets by foreign direct investment? A study of emerging economy firms. J. World Bus. 2014, 49, 488–501. [Google Scholar] [CrossRef]

- Luo, Y. Capability exploitation and building in a foreign market: Implications for multinational enterprises. Organ. Sci. 2002, 13, 48–63. [Google Scholar] [CrossRef]

- Wu, H.; Liu, Y. Balancing local and international knowledge search for internationalization of emerging economy multinationals: Evidence from China. Chin. Manag. Stud. 2018, 12, 701–719. [Google Scholar] [CrossRef]

- Wu, H.; Chen, J.; Liu, Y. The impact of OFDI on firm innovation in an emerging country. Int. J. Technol. Manag. 2017, 74, 167–184. [Google Scholar] [CrossRef]

- Filatotchev, I.; Liu, X.; Buck, T.; Wright, M. The export orientation and export performance of high-technology SMEs in emerging markets: The effects of knowledge transfer by returnee entrepreneurs. J. Int. Bus. Stud. 2009, 40, 1005–1021. [Google Scholar] [CrossRef]

- Lu, Y.; Zhou, L.; Bruton, G.; Li, W. Capabilities as a mediator linking resources and the international performance of entrepreneurial firms in an emerging economy. J. Int. Bus. Stud. 2010, 41, 419–436. [Google Scholar] [CrossRef]

- Li, H.; Zhang, Y. The role of managers’ political networking and functional experience in new venture performance: Evidence from China’s transition economy. Strateg. Manag. J. 2007, 28, 791–804. [Google Scholar] [CrossRef]

- Hoskisson, R.E.; Hitt, M.A.; Johnson, R.A.; Grossman, W. Conflicting voices: The effects of institutional ownership heterogeneity and internal governance on corporate innovation strategies. Acad. Manag. J. 2002, 45, 697–716. [Google Scholar] [CrossRef]

- Guo, Y.; Wang, L.; Yang, Q. Do corporate environmental ethics influence firms’ green practice? The mediating role of green innovation and the moderating role of personal ties. J. Clean. Prod. 2020, 266, 1–10. [Google Scholar] [CrossRef]

- Min, Z.; Sawang, S.; Kivits, R.A. Proposing circular economy ecosystem for Chinese SMEs: A systematic review. Int. J. Environ. Res. Public Health 2021, 18, 2395. [Google Scholar] [CrossRef]

- Atuahene-Gima, K.; Murray, J.Y. Exploratory and exploitative learning in new product development: A social capital perspective on new technology ventures in China. J. Int. Mark. 2007, 15, 1–29. [Google Scholar] [CrossRef]

- Yalcinkaya, G.; Calantone, R.J.; Griffith, D.A. An examination of exploration and exploitation capabilities: Implications for product innovation and market performance. J. Int. Mark. 2007, 15, 63–93. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Constructs/Measurement Items | Standardized Loadings |

|---|---|

| Exploratory international M&As (Cronbach α = 0.963, AVE = 0.840) | |

| 1. Get high-level R&D and management talent through international M&As | 0.895 |

| 2. Seek technological and marketing resources for firm’s development | 0.897 |

| 3. Acquire the managerial know-how for further improvement | 0.907 |

| 4. Take advantage of advanced R&D infrastructure | 0.893 |

| 5. Obtain global business information and technology spillover | 0.988 |

| Exploitative international M&As (Cronbach α = 0.921, AVE = 0.700) | |

| 1. Leverage technological advantages in foreign markets | 0.848 |

| 2. Enter into foreign markets to expand the market space | 0.834 |

| 3. Intend to lower transportation cost by producing abroad | 0.850 |

| 4. Utilize cheap labor and raw material in foreign markets | 0.827 |

| 5. Expand into foreign markets to benefit from investment incentives | 0.825 |

| Green image (Cronbach α = 0.920, AVE = 0.794) | |

| 1. Firms have raised awareness about the environmental risks and impacts | 0.916 |

| 2. Firms have been regarded as the best benchmark of environmental management | 0.879 |

| 3. Firms have demonstrated the ability to reduce waste via corresponding environmental performance | 0.878 |

| Green subsidy (Cronbach α = 0.913, AVE = 0.779) | |

| 1. Firms have obtained a large amount of subsidies related to environmental protection | 0.886 |

| 2. The government gives a lot of subsidies for environmental protection | 0.895 |

| 3. The government’s environmental subsidies are encouraging for firms | 0.866 |

| Green innovation performance (Cronbach α = 0.985, AVE = 0.916) | |

| 1.The firm has used an environmentally friendly design and packaging for existing and new products | 0.954 |

| 2.The firm has reduced the consumption of energy, such as water, electricity, coal, or oil | 0.958 |

| 3.The firm has reduced the consumption of raw materials | 0.952 |

| 4.The firm has reduced the emission of hazardous substances or waste | 0.953 |

| 5.The firm has used raw materials to be easily recycled, reused and decomposed | 0.972 |

| 6.The firm has used clean technologies and environmental protection equipment to promote energy efficiency and pollution prevention | 0.952 |

| Max | Min | Mean | S. D | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1.Firm age | 42.000 | 2.000 | 15.80 | 8.246 | 1 | ||||||||

| 2.Firm size | 11.127 | 4.605 | 7.536 | 1.388 | 0.263 ** | 1 | |||||||

| 3.R&D intensity | 0.130 | 0.010 | 0.050 | 0.024 | 0.052 | 0.006 | 1 | ||||||

| 4.International experience | 30.000 | 3.000 | 6.970 | 3.730 | −0.036 | 0.021 | 0.457 ** | 1 | |||||

| 5.Green image | 6.670 | 1.330 | 4.756 | 1.232 | 0.001 | −0.163 * | 0.019 | −0.040 | 1 | ||||

| 6.Green subsidy | 7.000 | 1.000 | 4.225 | 1.251 | 0.206 ** | −0.145 * | 0.019 | −0.004 | 0.082 | 1 | |||

| 7.Exploratory international M&As | 6.600 | 1.000 | 3.957 | 1.349 | −0.001 | 0.198 ** | 0.220 ** | 0.172 ** | 0.017 | −0.056 | 1 | ||

| 8.Exploitative international M&As | 6.800 | 1.400 | 4.601 | 1.059 | 0.059 | 0.134 * | 0.233 ** | 0.169 * | 0.268 ** | 0.212 ** | 0.179 ** | 1 | |

| 9.Green innovation performance | 6.833 | 1.167 | 3.925 | 1.659 | 0.045 | 0.214 ** | 0.308 ** | 0.203 ** | 0.128 | 0.146 * | 0.399 ** | 0.415 ** | 1 |

| Model 1 | Model 2 | Model 3 | Model 4 | Model 5 | |

|---|---|---|---|---|---|

| Industry dummy 1 (electronic information) | −0.022 | −0.045 | −0.063 | −0.085 | −0.095 |

| Industry dummy 2 (special equipment manufacturing) | 0.060 | −0.004 | −0.070 | −0.058 | −0.106 |

| Industry dummy 3 (transportation equipment manufacturing) | −0.002 | −0.054 | −0.075 | −0.102 | −0.114 |

| Industry dummy 4 (ordinary machinery manufacturing) | 0.048 | 0.015 | −0.011 | −0.013 | −0.032 |

| Industry dummy 5 (metal product) | 0.043 | 0.007 | −0.052 | −0.024 | −0.069 |

| Firm size | 0.300 *** | 0.177 ** | 0.165 ** | 0.164 ** | 0.158 ** |

| Firm age | −0.074 | −0.046 | −0.084 | −0.054 | −0.085 |

| R&D intensity | 0.272 *** | 0.177 ** | 0.152 * | 0.106 | 0.093 |

| International experience | 0.072 | 0.030 | 0.040 | 0.068 | 0.068 |

| Green image | 0.139 * | 0.054 | 0.004 | 0.029 | −0.009 |

| Green subsidy | 0.184 ** | 0.141 * | 0.139 * | 0.159 ** | 0.156 ** |

| Exploratory international M&As | 0.281 *** | 0.275 *** | 0.303 *** | 0.294 *** | |

| Exploitative international M&As | 0. 258 *** | 0.222 *** | 0. 238 *** | 0.214 *** | |

| Exploratory international M&As * Green image | 0.268 *** | 0.214 *** | |||

| Exploitative international M&As * Green image | −0.166 ** | −0.133 * | |||

| Exploratory international M&As * Green subsidy | 0.277 *** | 0.246 *** | |||

| Exploitative international M&As * Green subsidy | −0.169 ** | −0.131 * | |||

| R2 | 0.210 | 0.343 | 0.415 | 0.438 | 0.483 |

| F | 5.203 *** | 8.560 *** | 9.995 *** | 10.985 *** | 11.463 *** |

| Max VIF | 2.521 | 2.548 | 2.599 | 2.588 | 2.622 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Wu, H.; Qu, Y. How Do Firms Promote Green Innovation through International Mergers and Acquisitions: The Moderating Role of Green Image and Green Subsidy. Int. J. Environ. Res. Public Health 2021, 18, 7333. https://doi.org/10.3390/ijerph18147333

Wu H, Qu Y. How Do Firms Promote Green Innovation through International Mergers and Acquisitions: The Moderating Role of Green Image and Green Subsidy. International Journal of Environmental Research and Public Health. 2021; 18(14):7333. https://doi.org/10.3390/ijerph18147333

Chicago/Turabian StyleWu, Hang, and Yiying Qu. 2021. "How Do Firms Promote Green Innovation through International Mergers and Acquisitions: The Moderating Role of Green Image and Green Subsidy" International Journal of Environmental Research and Public Health 18, no. 14: 7333. https://doi.org/10.3390/ijerph18147333