The Impact Mechanism of Green Credit Policy on the Sustainability Performance of Heavily Polluting Enterprises—Based on the Perspectives of Technological Innovation Level and Credit Resource Allocation

, , and

, , and

Abstract

:1. Introduction

2. Theoretical Analysis and Hypothesis Formulation

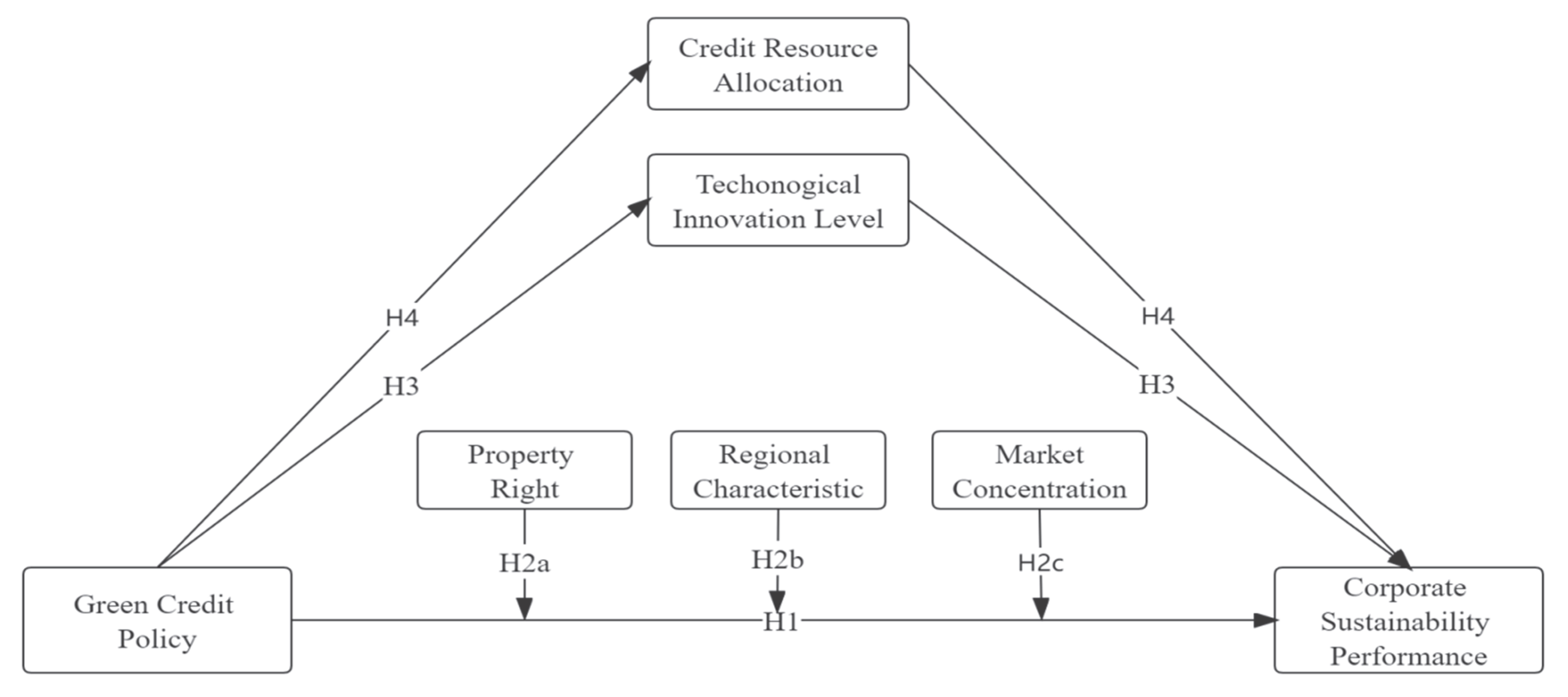

2.1. The Relationship between GCP and CSP

2.2. Heterogeneity in the Relationship between GCP and CSP

2.3. The Relationship between GCP, TIL and CSP

2.4. The Relationship between GCP, CRA and CSP

3. Materials and Method

3.1. Sample Selection and Data Sources

3.2. Variable Identification and Sample Description

3.2.1. Dependent Variables

3.2.2. Independent Variables

3.2.3. Mediating Variables

3.2.4. Control Variables

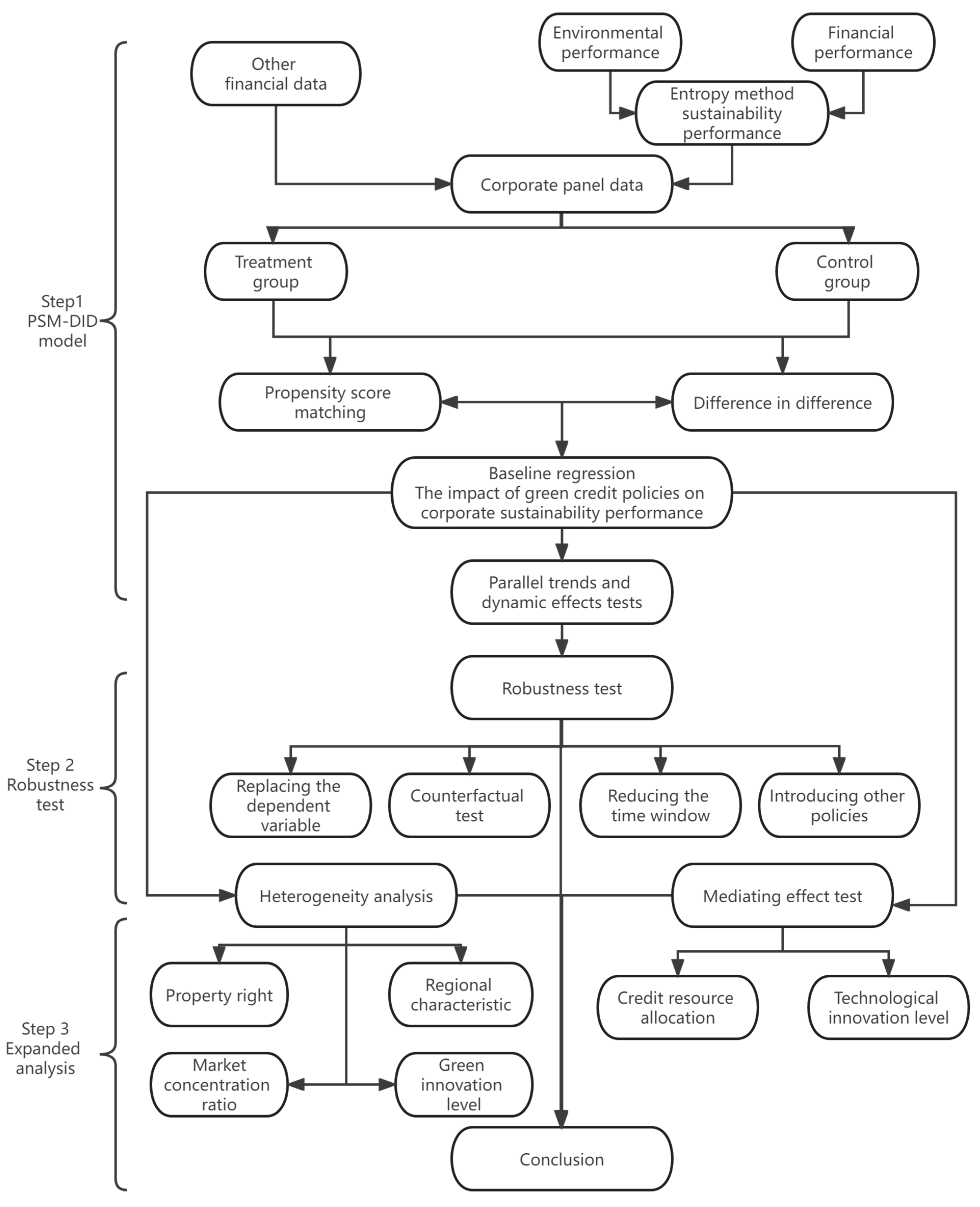

3.3. Research Method

4. Results

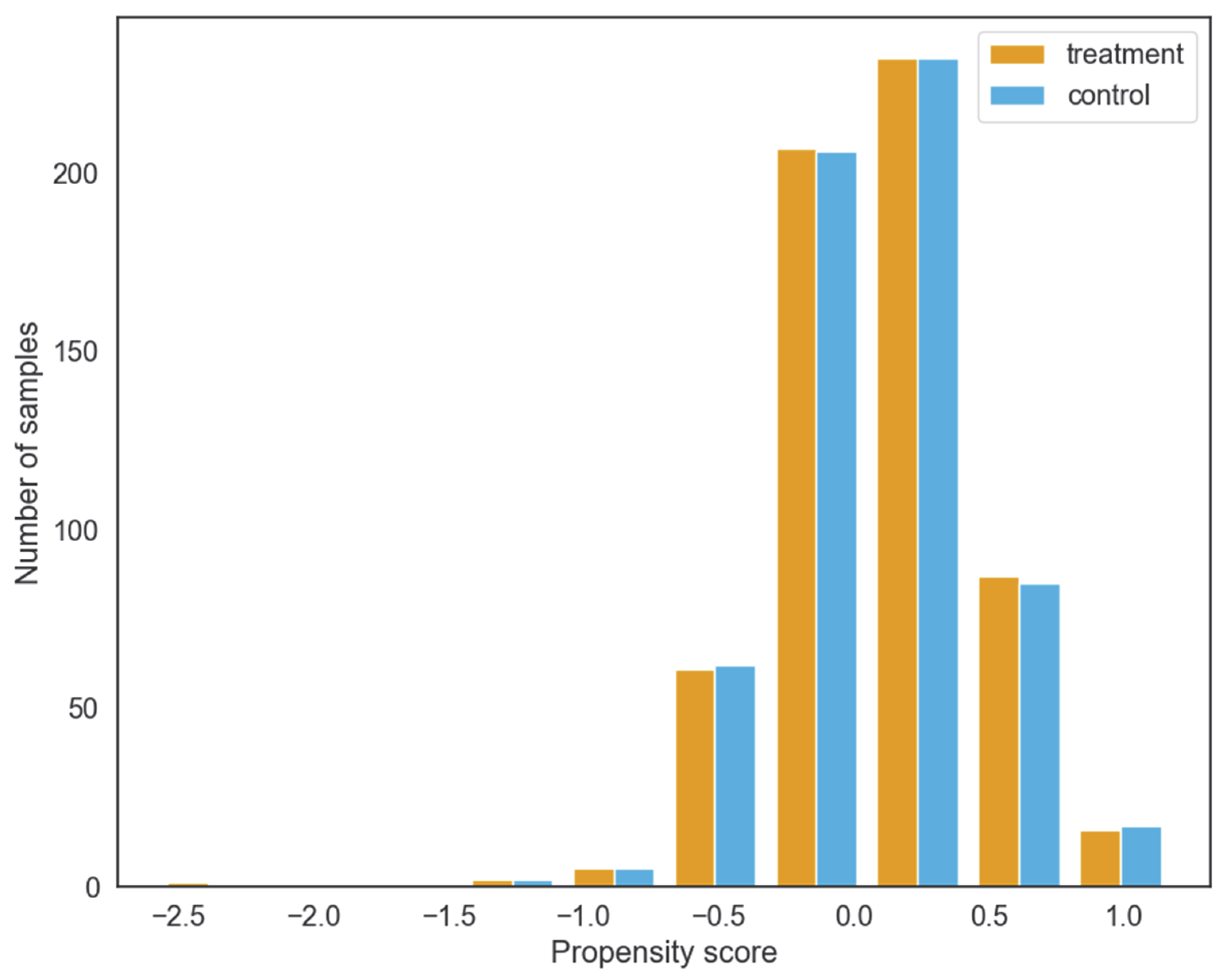

4.1. Propensity Score Matching and Analysis of Causal Effects

4.2. Baseline Regression Results

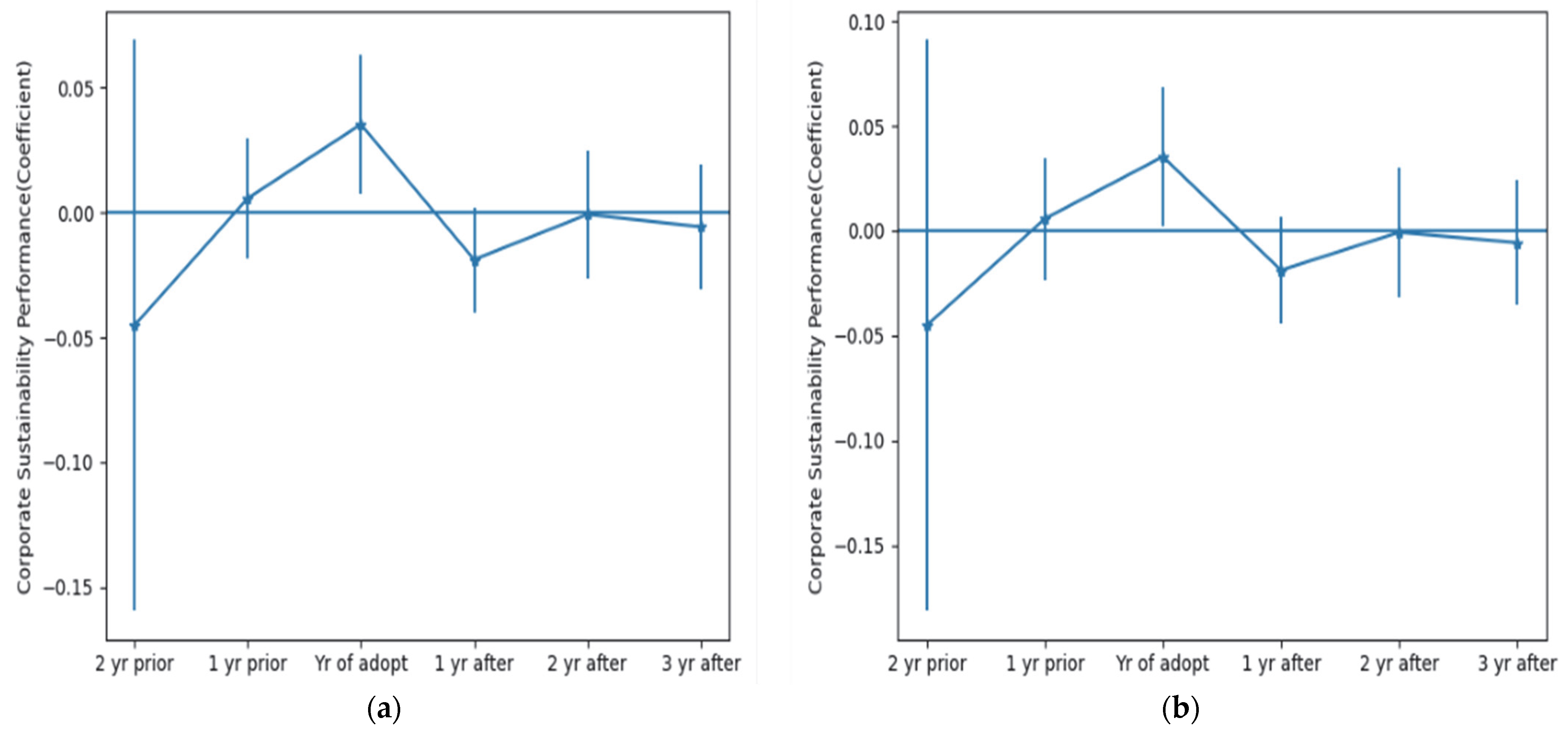

4.3. Analysis of Parallel Trends and Dynamic Effects

4.4. Robustness Test

5. Expanded Research

5.1. Heterogeneity Test

5.2. Analysis of Mediating Effects

6. Discussion

7. Conclusions

7.1. Conclusions and Implications

7.2. Limitations and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Classification | Industries |

|---|---|

| Treatment group | Wine, beverage and refined tea manufacturing; textile industry; textile clothing and apparel industry; leather, fur, feather and feather products and footwear industry; paper and paper products industry; printing and recording media reproduction industry; petroleum processing, coking and nuclear fuel processing industry; chemical raw materials and chemical products manufacturing industry; pharmaceutical manufacturing industry; chemical fiber manufacturing industry; rubber and plastic products industry; non-metallic mineral products industry; ferrous metal smelting and calendering processing industry; non-ferrous metal smelting and rolling processing industry; metal products industry |

| Control group | Agriculture and food processing industry; food manufacturing industry; tobacco manufacturing industry; wood processing and wood, bamboo, rattan, palm and grass products industry; furniture manufacturing industry; cultural, educational, industrial, aesthetic, sporting and recreational goods manufacturing industry; general equipment manufacturing industry; special equipment manufacturing industry; automobile manufacturing industry; railway, ship, aerospace and other transportation equipment manufacturing industry; electrical machinery and equipment manufacturing industry; computer, communication and other electronic equipment manufacturing; instrumentation manufacturing; other manufacturing; comprehensive utilization of waste resources manufacturing; machinery and equipment repair manufacturing |

References

- Sznajderska, A.; Kapuściński, M. Macroeconomic spillover effects of the Chinese economy. Rev. Int. Econ. 2020, 28, 992–1019. [Google Scholar] [CrossRef] [PubMed]

- Sharma, G.; Verma, M.; Shahbaz, M.; Gupta, M.; Chopra, R. Transitioning green finance from theory to practice for renewable energy development. Renew. Energy 2022, 195, 554–565. [Google Scholar] [CrossRef]

- Cheng, Q.; Lai, X.; Liu, Y.; Yang, Z.; Liu, J. The influence of green credit on China’s industrial structure upgrade: Evidence from industrial sector panel data exploration. Environ. Sci. Pollut. Res. 2021, 29, 22439–22453. [Google Scholar] [CrossRef] [PubMed]

- Zhao, X.; Chen, H. Research on influencing factors and transmission mechanisms of green credit risk. Environ. Sci. Pollut. Res. 2022, 22, 22041. [Google Scholar] [CrossRef] [PubMed]

- Andreoni, V. Environmental taxes: Drivers behind the revenue collected. J. Clean. Prod. 2019, 221, 17–26. [Google Scholar] [CrossRef]

- Khan, M.; Riaz, H.; Ahmed, M.; Saeed, A. Does green finance really deliver what is expected? An empirical perspective. Borsa Istanb. Rev. 2022, 22, 586–593. [Google Scholar] [CrossRef]

- Su, C.W.; Li, W.; Umar, M.; Lobonţ, O.R. Can green credit reduce the emissions of pollutants? Econ. Anal. Policy 2022, 74, 205–219. [Google Scholar] [CrossRef]

- Zhang, A.; Deng, R.; Wu, Y. Does the green credit policy reduce the carbon emission intensity of heavily polluting industries? -Evidence from China’s industrial sectors. J. Environ. Manag. 2022, 311, 114815. [Google Scholar] [CrossRef]

- Taghizadeh-Hesary, F.; Yoshino, N. The way to induce private participation in green finance and investment. Financ. Res. Lett. 2019, 31, 98–103. [Google Scholar] [CrossRef]

- Yang, X.; He, L.; Zhong, Z.; Wang, D. How does China’s green institutional environment affect renewable energy investments? The nonlinear perspective. Sci. Total Environ. 2020, 727, 138689. [Google Scholar] [CrossRef]

- Chen, C.; Zhang, Y.; Bai, Y.; Li, W. The impact of green credit on economic growth—The mediating effect of environment on labor supply. PLoS ONE 2021, 16, e0257612. [Google Scholar] [CrossRef]

- Zubair, M.D.; Alexander, S.D. Green Finance for Sustainable Development in Pakistan. IPRI J. 2019, 19, 1–34. [Google Scholar] [CrossRef]

- Alqudah, A.; Hamdan, A.; Alokaily, M.; Alhaddad, L. The impact of green lending on credit risk: Evidence from UAE’s banks. Environ. Sci. Pollut. Res. 2022, 21, 18224. [Google Scholar] [CrossRef]

- Lin, B.; Bai, R. Machine learning approaches for explaining determinants of the debt financing in heavy-polluting enterprises. Financ. Res. Lett. 2022, 44, 102094. [Google Scholar] [CrossRef]

- Zhang, Z.; Duan, H.; Shan, S.; Liu, Q.; Geng, W. The Impact of Green Credit on the Green Innovation Level of Heavy-Polluting Enterprises—Evidence from China. Int. J. Environ. Res. Public Health 2022, 19, 650. [Google Scholar] [CrossRef]

- Zhang, W.; Liu, Y.; Zhang, F.; Dou, H. Green Credit Policy and Corporate Stock Price Crash Risk: Evidence From China. Front. Psychol. 2022, 13, 891284. [Google Scholar] [CrossRef]

- Xing, C.; Zhang, Y.; Wang, Y. Do banks value green management in China? the perspective of the Green Credit Policy. Financ. Res. Lett. 2020, 35, 101601. [Google Scholar] [CrossRef]

- Zhang, J.; Luo, Y.; Ding, X. Can green credit policy improve the overseas investment efficiency of enterprises in China? J. Clean. Prod. 2022, 340, 130785. [Google Scholar] [CrossRef]

- Ronaldo, R.; Suryanto, T. Green finance and sustainability development goals in Indonesian Fund Village. Resour. Policy 2022, 78, 102839. [Google Scholar] [CrossRef]

- He, L.; Wu, C.; Yang, X.; Liu, J. Corporate social responsibility, green credit, and corporate performance: An empirical analysis based on the mining, power, and steel industries of China. Nat. Hazards 2018, 95, 73–89. [Google Scholar] [CrossRef]

- Silva, G.; Styles, C.; Lages, L. Breakthrough innovation in international business: The impact of tech-innovation and market-innovation on performance. Int. Bus. Rev. 2017, 26, 391–404. [Google Scholar] [CrossRef]

- Nenavath, S. Impact of fintech and green finance on environmental quality protection in India: By applying the semi-parametric difference-in-differences (SDID). Renew. Energy 2022, 193, 913–919. [Google Scholar] [CrossRef]

- Kang, H.; Jung, S.Y.; Lee, H. The impact of Green Credit Policy on manufacturers’ efforts to reduce suppliers’ pollution. J. Clean. Prod. 2020, 248, 119271. [Google Scholar] [CrossRef]

- Tian, C.; Li, X.; Xiao, L.; Zhu, B. Exploring the impact of green credit policy on green transformation of heavy polluting industries. J. Clean. Prod. 2022, 335, 130257. [Google Scholar] [CrossRef]

- Liu, C.J.; Zhang, S.H.; Li, X. Has Green Credit Policy Boosted Green Total Factor Productivity in China’s Heavily Polluting Industries? Stud. Int. Financ. 2022, 4, 3–11. [Google Scholar] [CrossRef]

- Si, L.J.; Cao, H.Y. Does Green Credit Policies Improve Corporate Environmental Social Responsibility —The Perspective of External Constraints and Internal Concerns. China Ind. Econ. 2022, 4, 137–155. [Google Scholar] [CrossRef]

- Zou, W.; Wang, W.X. Can Green Credit Policy Improve Carbon Emission Efficiency?—An inquiry from the perspective of technology progress and factor structure. J. Xiangtan Univ. (Philos. Soc. Sci.) 2022, 46, 60–66. [Google Scholar] [CrossRef]

- Jiang, Y.; Qin, S.; Xu, Y. Impact of green credit policy on sustainability performance of high-pollution enterprises. Environ. Sci. Pollut. Res. 2022, 29, 79199–79213. [Google Scholar] [CrossRef]

- Aller, C.; Jesus, H.M.; Javier, O. The Effect of Financial Development on Energy Intensity in China. Energy J. 2018, 39, 25–38. [Google Scholar] [CrossRef]

- Zhang, K.; Zhou, X. Is Promoting Green Finance in Line with the Long-Term Market Mechanism? The Perspective of Chinese Commercial Banks. Mathematics 2022, 10, 1374. [Google Scholar] [CrossRef]

- Xi, B.; Wang, Y.; Yang, M. Green credit, green reputation, and corporate financial performance: Evidence from China. Environ. Sci. Pollut. Res. 2021, 29, 2401–2419. [Google Scholar] [CrossRef] [PubMed]

- Zhang, K.; Li, Y.; Qi, Y.; Shao, S. Can green credit policy improve environmental quality? Evidence from China. J. Environ. Manag. 2021, 298, 113445. [Google Scholar] [CrossRef] [PubMed]

- Zhao, S.; Wang, H.; Li, W. Allocation of Credit Resources and “Borrow to Lend” Activities: Evidence From Chinese-Listed Companies. Front. Psychol. 2022, 13, 856056. [Google Scholar] [CrossRef] [PubMed]

- Zheng, H.; He, Y. How do the China Pollution Discharge Fee Policy and the Environmental Protection Tax Law affect firm performance during the transitional period? Environ. Sci. Pollut. Res. 2022, 29, 44541–44557. [Google Scholar] [CrossRef]

- Zhou, G.; Liu, C.; Luo, S. Resource Allocation Effect of Green Credit Policy: Based on DID Model. Mathematics 2021, 9, 159. [Google Scholar] [CrossRef]

- Li, X.; Lu, Y. How green credit policy shapes financial performance: Evidence from Chinese listed construction energy-saving enterprise. Front. Environ. Sci. 2022, 10, 1004247. [Google Scholar] [CrossRef]

- Wen, H.; Lee, C.C.; Zhou, F. Green credit policy, credit allocation efficiency and upgrade of energy-intensive enterprises. Energy Economics 2021, 94, 105099. [Google Scholar] [CrossRef]

- Lin, X.M.; Guan, S. Does Environmental Regulation Promote the Transformation and Upgrading of Industrial Structure: Based on Strategic Interaction of Local Government Environmental Regulation. South China J. Econ. 2020, 11, 99–115. [Google Scholar] [CrossRef]

- Cao, Y.Q.; Zhang, C.Y.; Yang, X. Green effects and impact mechanisms of green credit policies—Evidence based on green patent data of Chinese listed companies. Financ. Forum 2021, 26, 7–17. [Google Scholar] [CrossRef]

- Yang, N.; Liu, Q.; Wang, X. How does industrial coagglomeration affect regional green innovation? Evidence from Chinese cities. Technol. Anal. Strateg. Manag. 2022, 1, 2026139. [Google Scholar] [CrossRef]

- Ge, T.; Cai, X.; Song, X. How does renewable energy technology innovation affect the upgrading of industrial structure? The moderating effect of green finance. Renew. Energy 2022, 197, 1106–1114. [Google Scholar] [CrossRef]

- Kvalseth, T. Measurement of market (industry) concentration based on value validity. PLoS ONE 2022, 17, e0264613. [Google Scholar] [CrossRef] [PubMed]

- Li, S.; Zhang, W.; Zhao, J. Does green credit policy promote the green innovation efficiency of heavy polluting industries?—Empirical evidence from China’s industries. Environ. Sci. Pollut. Res. 2022, 29, 46721–46736. [Google Scholar] [CrossRef] [PubMed]

- Hong, M.; Li, Z.; Drakeford, B. Do the Green Credit Guidelines Affect Corporate Green Technology Innovation? Empirical Research from China. Int. J. Environ. Res. Public Health 2021, 18, 1682. [Google Scholar] [CrossRef] [PubMed]

- Hemanand, D.; Mishra, N.; Premalatha, G.; Mavaluru, D.; Vajpayee, A.; Kushwaha, S.; Sahile, K. Applications of Intelligent Model to Analyze the Green Finance for Environmental Development in the Context of Artificial Intelligence. Comput. Intell. Neurosci. 2022, 22, 2977824. [Google Scholar] [CrossRef]

- He, L.; Gan, S.; Zhong, T. The impact of green credit policy on firms’ green strategy choices: Green innovation or green-washing? Environ. Sci. Pollut. Res. 2022, 29, 73307. [Google Scholar] [CrossRef]

- Zhang, S.; Wu, Z.; Wang, Y.; Hao, Y. Fostering green development with green finance: An empirical study on the environmental effect of green credit policy in China. J. Environ. Manag. 2021, 296, 113159. [Google Scholar] [CrossRef]

- Wang, Y.; Lei, X.; Long, R.; Zhao, J. Green Credit, Financial Constraint, and Capital Investment: Evidence from China’s Energy-intensive Enterprises. Environ. Manag. 2020, 66, 1059–1071. [Google Scholar] [CrossRef]

- Yang, Y.C.; Niu, X.T. The Impact of the New Environmental Protection Law on the Efficiency of Listed Companies in China’s Heavy Pollution Industry: Based on Perspective of “Porter’s Hypothesis”. Manag. Rev. 2021, 33, 55–69. [Google Scholar] [CrossRef]

- Liu, X.G.; Shao, R.X. Environmental Protection Tax, Technological Innovation and Corporate Financial Performance — A Study Based on the Difference-in-Differences Method. J. Ind. Technol. Econ. 2021, 40, 24–30. [Google Scholar]

- Alexopoulos, I.; Kounetas, K.; Tzelepis, D. Environmental and financial performance. Is there a win-win or a win-loss situation? Evidence from the Greek manufacturing. J. Clean. Prod. 2018, 197, 1275–1283. [Google Scholar] [CrossRef]

- Kline, A.; Luo, Y. PsmPy: A Package for Retrospective Cohort Matching in Python. In Proceedings of the 2022 44th Annual International Conference of the IEEE Engineering in Medicine & Biology Society (EMBC), Glasgow, Scotland, UK, 11–15 July 2022. [Google Scholar] [CrossRef]

- Olmuş, H.; Beşpınar, E.; Nazman, E. Performance evaluation of some propensity score matching methods by using binary logistic regression model. Commun. Stat. Simul. Comput. 2019, 51, 1647–1660. [Google Scholar] [CrossRef]

- Cohen, J. A power primer. Psychol. Bull. 1992, 112, 155–159. [Google Scholar] [CrossRef] [PubMed]

- Du, M.; Chai, S.; Wei, W.; Wang, S.; Li, Z. Will environmental information disclosure affect bank credit decisions and corporate debt financing costs? evidence from China’s heavily polluting industries. Environ. Sci. Pollut. Res. 2022, 29, 47661–47672. [Google Scholar] [CrossRef] [PubMed]

- Peng, B.; Yan, W.; Elahi, E.; Wan, A. Does the green credit policy affect the scale of corporate debt financing? evidence from listed companies in Heavy Pollution Industries in China. Environ. Sci. Pollut. Res. 2021, 29, 755–767. [Google Scholar] [CrossRef]

- Chen, R. The effects of green credit policy on the formation of zombie firms: Evidence from Chinese listed firms. Environ. Sci. Pollut. Res. 2022, 29, 80669–80682. [Google Scholar] [CrossRef]

- Igartua, J.; Hayes, A. Mediation, Moderation, and Conditional Process Analysis: Concepts, Computations, and Some Common Confusions. Span. J. Psychol. 2021, 24, E49. [Google Scholar] [CrossRef]

- Ren, X.; Shao, Q.; Zhong, R. Nexus between Green Finance, non-fossil energy use, and carbon intensity: Empirical evidence from China based on a vector error correction model. J. Clean. Prod. 2020, 277, 122844. [Google Scholar] [CrossRef]

- Zhang, B.; Yang, Y.; Bi, J. Tracking the implementation of Green Credit policy in China: Top-down perspective and bottom-up reform. J. Environ. Manag. 2011, 92, 1321–1327. [Google Scholar] [CrossRef]

- Wang, M.; Liao, G.; Li, Y. The relationship between environmental regulation, pollution and corporate environmental responsibility. Int. J. Environ. Res. Public Health 2021, 18, 8018. [Google Scholar] [CrossRef]

- Ding, X.; Ye, L.; Yang, Y.; Efimova, O.; Steblyanskaya, A.; Zhang, J. The Impact Mechanism of Environmental Information Disclosure on Corporate Sustainability Performance—Micro-Evidence from China. Sustainability 2022, 14, 12366. [Google Scholar] [CrossRef]

- Contreras, G.; Bos, J.; Kleimeier, S. Self-regulation in sustainable finance: The adoption of the Equator Principles. World Dev. 2019, 122, 306–324. [Google Scholar] [CrossRef]

- Ali, H.; Danish, R.; Asrar-ul-Haq, M. How corporate social responsibility boosts firm financial performance: The mediating role of corporate image and customer satisfaction. Corp. Soc. Responsib. Environ. Manag. 2019, 27, 166–177. [Google Scholar] [CrossRef]

- Steblyanskaya, A.; Ai, M.; Denisov, A.; Efimova, O.; Rybachuk, M. Carbon dioxide emissions reduction efficiency and growth potential: Case of China. PSU Res. Rev. 2022, 2, 66. [Google Scholar] [CrossRef]

- Wang, Z.; Kleiner, G.; Bragina, Z.; Denisov, A.; Steblyanskaya, A. Russian and Chinese Natural Gas Industries: Perspectives on Sustainable Growth. Int. J. Public Adm. 2019, 42, 1381–1394. [Google Scholar] [CrossRef]

- Hadlock, C.; Pierce, J. New Evidence on Measuring Financial Constraints: Moving Beyond the KZ Index. Rev. Financ. Stud. 2010, 23, 1909–1940. [Google Scholar] [CrossRef]

| Variable Category | Specific Indicators | Signs | Variable Description | Data Sources | Mean | Min | Max |

|---|---|---|---|---|---|---|---|

| Dependent variables | Financial performance | Roe | Ratio of net profit to equity | CNRDS Database Hexun.com Database | 0.038 | −7.220 | 0.823 |

| Environmental performance | Ep | Corporate environmental responsibility score | 5.648 | 0.000 | 30.000 | ||

| Sustainability performance | Csp | Entropy of return on equity and environmental performance | 0.193 | 0.000 | 0.901 | ||

| Independent variables | Target of policy implementation | Treated | High polluters as 1, otherwise as 0 | Wind Database | 0.499 | 0.000 | 1.000 |

| Time of policy implementation | Post | After policy implementation as 1, otherwise as 0 | 0.667 | 0.000 | 1.000 | ||

| Net effect of policy implementation | Treated × Post | Policy target × time of policy implementation | 0.338 | 0.000 | 1.000 | ||

| Mediator | Total level of debt financing | Adf | Long- and short-term bank loans as a percentage of total assets | 0.262 | 0.001 | 0.689 | |

| Level of long-term debt financing | Ldf | Long-term bank loans as a percentage of total assets | 0.088 | 0.000 | 0.479 | ||

| Level of technological innovation | Rd | Investment in research and development as a percentage of operating revenue | 0.019 | 0.000 | 0.122 | ||

| Control variables | Corporate size | Size | Natural logarithm of total assets | CSMAR Database | 22.992 | 20.088 | 26.961 |

| Leverage ratio | Lev | Ratio of liabilities to assets | 0.595 | 0.193 | 1.050 | ||

| Corporate growth | Growth | Operating revenue growth rate | 0.217 | −1.463 | 6.217 | ||

| Type of shareholding | State | State-owned enterprises as 1, otherwise as 0 | 0.685 | 0.000 | 1.000 | ||

| Ratio of independent directors | Idr | Ratio of independent directors to total board members | 0.377 | 0.200 | 0.667 | ||

| Financial background of directors | Fbd | Financial background as 1, otherwise as 0 | 0.663 | 0.000 | 1.000 | ||

| Economic development level | Gdp | Natural logarithm of gross regional product | NBS Database | 4.320 | 3.059 | 4.874 | |

| Market development level | Mai | Market index | CMI Database | 8.178 | 3.359 | 11.113 |

| Variables | Unmatched Cohort | Matched Cohort | ||||||

|---|---|---|---|---|---|---|---|---|

| Mean | t-Test | Mean | t-Test | |||||

| Treated (n = 611) | Controls (n = 613) | t-Value | p-Value | Treated (n = 610) | Controls (n = 154) | t-Value | p-Value | |

| Size | 22.829 | 23.156 | 4.675 | <0.001 *** | 23.155 | 23.136 | 0.185 | 0.853 |

| Lev | 0.577 | 0.613 | 4.531 | <0.001 *** | 0.613 | 0.599 | 1.009 | 0.313 |

| Growth | 0.332 | 0.102 | −2.116 | 0.034 ** | 0.103 | 0.116 | −0.327 | 0.743 |

| State | 0.647 | 0.697 | 0.884 | 0.376 | 0.697 | 0.682 | 0.358 | 0.720 |

| Idr | 0.126 | 0.144 | 0.044 | 0.964 | 0.377 | 0.376 | 0.236 | 0.813 |

| Fbd | 0.684 | 0.643 | −1.492 | 0.135 | 0.644 | 0.643 | 0.032 | 0.974 |

| Gdp | 4.333 | 4.307 | −1.415 | 0.157 | 4.308 | 4.260 | 1.642 | 0.101 |

| Mai | 8.350 | 8.006 | −3.149 | 0.001 *** | 8.013 | 7.786 | 1.354 | 0.176 |

| Effect | Est. | S.e. | z | p > |z| | [95% Conf. int.] | |

|---|---|---|---|---|---|---|

| ATE | 0.049 | 0.012 | 3.976 | 0.000 *** | 0.025 | 0.073 |

| ATC | 0.054 | 0.012 | 4.517 | 0.000 *** | 0.031 | 0.078 |

| ATT | 0.048 | 0.012 | 3.381 | 0.000 *** | 0.023 | 0.072 |

| Dep. Variable | Model (1) | Model (2) | Model (3) |

|---|---|---|---|

| Csp | |||

| 0.021 ** | 0.043 *** | ||

| (2.12) | (2.64) | ||

| Size | −0.007 | −0.011 | |

| (−0.31) | (−0.46) | ||

| Lev | −0.042 | −0.050 | |

| (−0.62) | (−0.75) | ||

| Growth | 0.008 | 0.006 | |

| (0.64) | (0.47) | ||

| State | 0.118 ** | 0.121 ** | |

| (2.41) | (2.48) | ||

| Idr | 0.099 | 0.094 | |

| (0.70) | (0.67) | ||

| Fbd | 0.026 * | 0.024 * | |

| (1.78) | (1.66) | ||

| Gdp | 0.134 | −0.054 | |

| (1.33) | (−0.44) | ||

| Mai | 0.014 | −0.011 | |

| (−0.88) | (−0.75) | ||

| Intercept | 0.583 *** | 0.018 | 1.044 * |

| (84.89) | (0.43) | (1.93) | |

| Effects | Time | Time | Time |

| Entity | Entity | Entity | |

| No. Observations | 764 | 764 | 764 |

| R-Squared | 0.008 | 0.020 | 0.032 |

| Dep. Variable | Model (1) | Model (2) | Model (3) | Model (4) |

|---|---|---|---|---|

| Csp_new | Csp | Csp | Csp | |

| −0.012 | ||||

| (−0.17) | ||||

| 0.042 *** | 0.066 *** | 0.043 *** | ||

| (2.65) | (2.87) | (2.62) | ||

| 0.002 | ||||

| (0.12) | ||||

| Control variables | Yes | Yes | Yes | Yes |

| Intercept | 1.032 * | 0.193 | 3.614 ** | 1.063 * |

| (1.94) | (0.44) | (2.32) | (1.88) | |

| Effects | Time | Time | Time | Time |

| Entity | Entity | Entity | Entity | |

| No. Observations | 764 | 764 | 376 | 764 |

| R-Squared | 0.034 | 0.020 | 0.069 | 0.032 |

| Classifications | Property Rights Nature | Regional Characteristics | Concentration Ratio | Green Innovation Level | ||||

|---|---|---|---|---|---|---|---|---|

| SOEs | Non-SOEs | East | Non-East | Low | High | Low | High | |

| Dep. Variable | Csp | |||||||

| 0.017 | 0.062 *** | 0.053 ** | 0.029 | 0.071 ** | 0.030 | 0.050 | 0.045 ** | |

| (0.57) | (3.18) | (2.52) | (1.127) | (2.33) | (1.50) | (1.39) | (2.36) | |

| Control variables | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Intercept | 0.327 | 1.388 *** | 0.987 | 1.234 | 2.382 ** | 0.616 | 1.175 | 1.338 ** |

| (0.32) | (2.11) | (1.52) | (1.20) | (2.05) | (0.97) | (0.92) | (2.11) | |

| Effects | Time | Time | Time | Time | Time | Time | Time | Time |

| Entity | Entity | Entity | Entity | Entity | Entity | Entity | Entity | |

| Observations | 530 | 234 | 462 | 302 | 245 | 519 | 540 | 224 |

| R-squared | 0.033 | 0.093 | 0.057 | 0.034 | 0.111 | 0.026 | 0.004 | 0.044 |

| Dep. Variable | Model (1) | Model (2) | Model (3) | Model (4) | Model (5) | Model (6) |

|---|---|---|---|---|---|---|

| Rd | Csp | Adf | Csp | Ldf | Csp | |

| 7.195 | 0.051 *** | 0.005 | 0.043 *** | −0.006 | 0.043 *** | |

| (9.23) | (2.92) | (0.56) | (2.63) | (−0.78) | (2.64) | |

| Adf | 0.010 | |||||

| (0.13) | ||||||

| Ldf | 0.023 | |||||

| (0.24) | ||||||

| Rd | −0.001 | |||||

| (−1.26) | ||||||

| Control variables | Yes | Yes | Yes | Yes | Yes | Yes |

| Intercept | −27.283 | 1.013 * | 0.779 *** | 1.036 * | 0.581 ** | 1.031 * |

| (−1.09) | (1.88) | (2.81) | (1.90) | (2.43) | (1.90) | |

| Effects | Time | Time | Time | Time | Time | Time |

| Entity | Entity | Entity | Entity | Entity | Entity | |

| No. Observations | 764 | 764 | 764 | 764 | 764 | 764 |

| R-Squared | 0.383 | 0.034 | 0.294 | 0.032 | 0.133 | 0.032 |

| Bootstrap test | is not significant, so Bootstrap test is necessary | are not significant, so Bootstrap test is necessary | are not significant, so Bootstrap test is necessary | |||

| 95% Confidence intervals | [−0.0176, −0.0014] | [0.0011, 0.0109] | [−0.0047, −0.0000] | |||

| Mediation effect | Significant | Significant | Significant | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ding, X.; Jing, R.; Wu, K.; Petrovskaya, M.V.; Li, Z.; Steblyanskaya, A.; Ye, L.; Wang, X.; Makarov, V.M. The Impact Mechanism of Green Credit Policy on the Sustainability Performance of Heavily Polluting Enterprises—Based on the Perspectives of Technological Innovation Level and Credit Resource Allocation. Int. J. Environ. Res. Public Health 2022, 19, 14518. https://doi.org/10.3390/ijerph192114518

Ding X, Jing R, Wu K, Petrovskaya MV, Li Z, Steblyanskaya A, Ye L, Wang X, Makarov VM. The Impact Mechanism of Green Credit Policy on the Sustainability Performance of Heavily Polluting Enterprises—Based on the Perspectives of Technological Innovation Level and Credit Resource Allocation. International Journal of Environmental Research and Public Health. 2022; 19(21):14518. https://doi.org/10.3390/ijerph192114518

Chicago/Turabian StyleDing, Xiaowei, Ruxu Jing, Kaikun Wu, Maria V. Petrovskaya, Zhikun Li, Alina Steblyanskaya, Lyu Ye, Xiaotong Wang, and Vasiliy M. Makarov. 2022. "The Impact Mechanism of Green Credit Policy on the Sustainability Performance of Heavily Polluting Enterprises—Based on the Perspectives of Technological Innovation Level and Credit Resource Allocation" International Journal of Environmental Research and Public Health 19, no. 21: 14518. https://doi.org/10.3390/ijerph192114518