Risk Culture and the Role Model of the Honorable Merchant

Abstract

:1. Introduction: Risk Culture in an Organization versus Organizational Culture of Risk

Although there may be different understandings of the specific nature of culture [...] by using culture as a root metaphor, they are all influenced to consider organization as a particular form of human expression. […]A cultural analysis [of organizations] moves us in the direction of questioning taken-for-granted assumptions, raising issues of context and meaning, and bringing to the surface underlying values. […]Denhardt in “In the Shadow of Organization” (1981) noted that organization and administration studies tend to take as their task improving organizational efficiency rather than questioning the “ethic of organization”

2. Probability of Repeated Games versus Risk in Human Decision-Making

The Risk of losing any Sum is […] the product of the Sum adventured multiplied by the Probability of the Loss.

3. A Short History of Risk Culture

- ancient societies, in which each event was attributed to a “whim of the gods” (Bernstein 1996) by passive people with a predetermined fate

- honorable merchants as rational individual decision-makers with personal responsibility in long-term relationships starting with sea merchants in the Italian Renaissance

- illusion of control in modern society since the 20th century with the paradigm of a “clockwork economy”, in which human beings act as cogwheels without a face

- “Risicum” was used in the context of individual (commercial) conscious decision under uncertainty, but with the responsibility to accept or cover the (financial) consequences and damages

- “Periculum” or, respectively, “fortunam” were used for exogenous (natural) forces, which the merchant could not be aware of and with could be covered by a contract, i.e., something unrelated to the individual decision-making of a professional and experienced sea merchant

- When men are close to each other, they no longer decide randomly and independently of each other, they each reacts to the others

- … you regard men as infinitely selfish and infinitely farsighted. The first hypothesis may perhaps be admitted in a first approximation, the second may call for some reversion.

4. From “Normal Accidents” to “Normal Wrongdoing”

Shapira and Zingales (2017) pointed out several mechanisms for that case: path dependency and time lag (with C8 usage already from 1952, information of toxicity by 1984, and continuous use until 20002), broken regulatory framework (without consistency and low penalties), and information advantage or information asymmetry between the company and all other stakeholders. This may be one example only, but many others are well-known cases from Enron to Volkswagen to misconduct with mortgages et cetera. There is no obvious pattern to point to a certain industry or a certain type of management.DuPont, one of the most respectable US companies, caused environmental damage that ended up costing the company around a billion dollars.…rule out the possibilities that this bad outcome was due to ignorance, an unexpected realization, or a problem of bad governance. The documents rather suggest that the polluting was a rational decision: under reasonable probabilities of detection, …One common reason for the failures of deterrence mechanisms is that the company controls most of the information and its release. …From 1951 to 2000 DuPont received C8 from a supplier (the Minnesota Mining & Manufacturing Company, later renamed 3M). …By 1984 DuPont knew that C8 is toxic, …, and seeps into local drinking water supplies. The executives acknowledged that the legal and medical departments would recommend stopping the usage of C8 altogether. …Yet the business side ultimately overruled these recommendations and opted to continue (in fact, double) C8 emissions. …DuPont’s decision, it seems, was a case of “rational wrongdoing”: a decision that maximizes shareholder value ex ante, even though it is socially harmful. …Indeed, a critical mass of honest research and well-documented studies of C8 were generated in-house …These scientists seemingly tried to instill in DuPont a corporate culture of the highest standards in that regard, as is evident from the words of Bruch Karrh, DuPont’s medical director and vice president in the relevant time frame (since 1983) …One of the interesting aspects of the DuPont-C8 case is the “faceless crime” element. Even though the company suffered negative media coverage, none of its top managers were dragged through the mud. The lack of personal accountability …rational, “normal,” wrongdoing. C8 emissions and the suppression of information about it were not an evil plan or an accident. They were the natural course of action of a profit-maximizing company, which fully utilized the tools available under then-current laws.

5. A Self-Organized Lex Mercatoria for Risk?

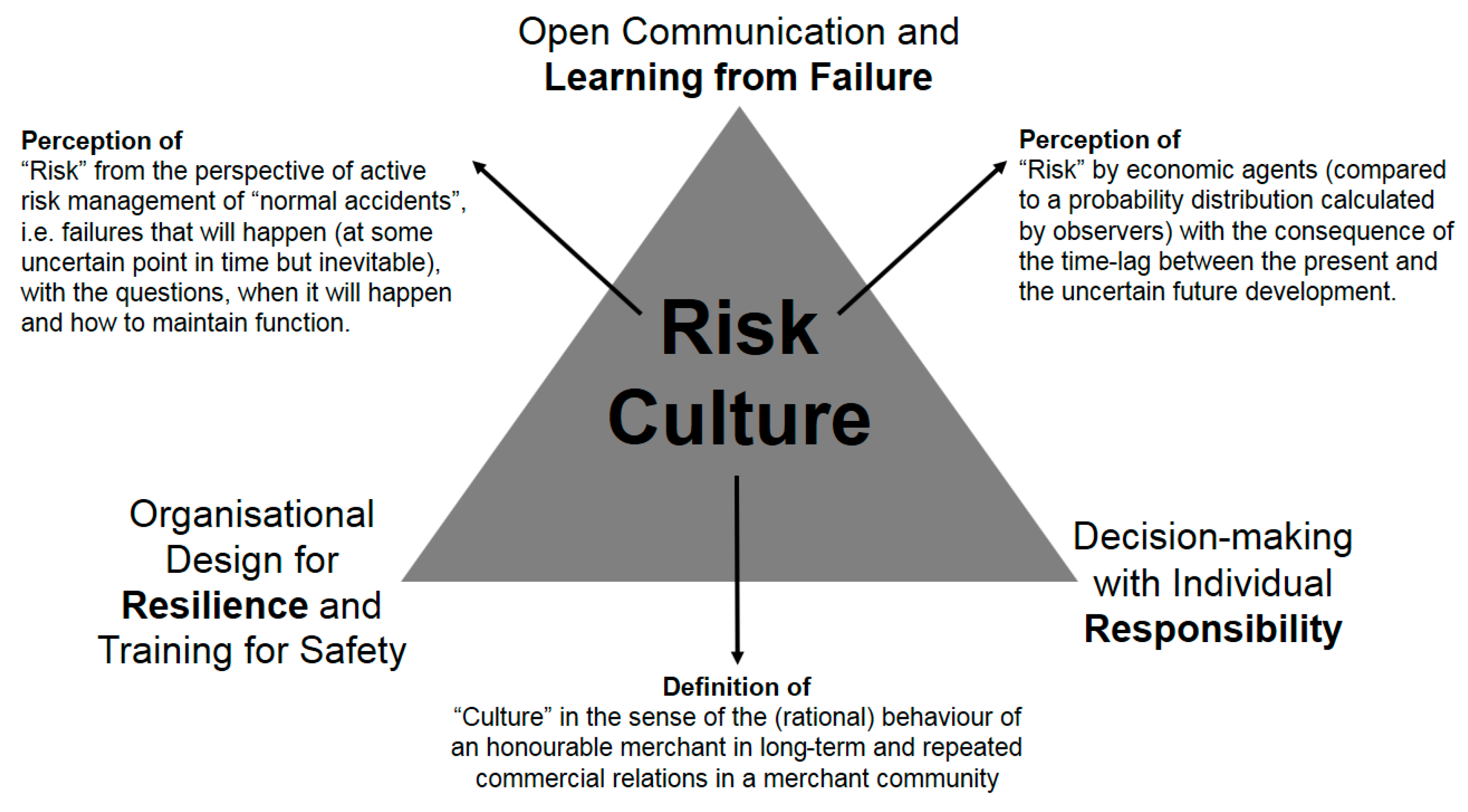

6. Three Dimensions of Risk Culture

Cultures of risk dare to do more in handling dangerous and perilous situations compared to worlds of safety. Cultures of risk are designed to see an opportunity together with some danger. [...]. Worlds of safety are based on the implicit promise of a “safe world” and promote experiences to be measured to. In the course of this, the fact emerges with large regularity that such “worlds of safety” cannot fulfill the promises.

Cheat not rich man nor poor—since you know not what you may encounter a man may buy other things—but not fortune.

“All Life is Problem Solving”.

- Decision-making with Individual Responsibility

- Learning from Failure

- Organizational Resilience

- clockwork (mechanical, deterministic, and parts without individuality)

- equilibrium (with risk as variance of small variations around a design value)

- model-based prediction (of probability distributions for risk by simple numbers)

7. An Honorable Merchant in a Complex World

8. Conclusions

The outside world itself knows no risks, for it knows neither distinction, nor expectations, nor evaluations, nor probabilities—unless self-produced by observer systems in the environment of other systems.

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Aven, Terje. 2012. The risk concept—Historical and recent development trends. Reliability Engineering and System Safety 99: 33–44. [Google Scholar] [CrossRef]

- BaFin (Bundesanstalt für Finanzdienstleistungsaufsicht). 2017. Anlage 1: Erläuterungen zu den MaRisk in der Fassung vom. October 27. Available online: https://www.bafin.de/SharedDocs/Veroeffentlichungen/DE/Rundschreiben/2017/rs_1709_marisk_ba.html?nn=9021442 (accessed on 27 October 2017).

- Basel Committee on Banking Supervision (BCBS). 2015. Guidelines—Corporate Governance Principles for Banks, 2015 July. Available online: www.bis.org/bcbs/publ/d328.htm (accessed on 28 August 2017).

- Bernstein, Peter L. 1996. Against the Gods: The Remarkable Story of Risk. Hoboken: John Wiley & Sons. [Google Scholar]

- Ceccarelli, Giovanni. 2015. Renaissance Risk Takers: Culture and Practice in Florentine Society. Talk Given at 2 December 2015. Available online: www.uni-due.de/graduiertenkolleg_1919/wagnisse (accessed on 2 September 2017).

- D’Aveni, Richard A. 1998. Waking Up to the New Era of Hypercompetition. Washington Quarterly 21: 183–95. [Google Scholar] [CrossRef]

- De Moivre, Abraham. 1718. The Doctrine of Chance. London: W. Pearson. [Google Scholar]

- Dotson, John E. 1994. Merchant Culture in Fourteenth Century Venice: The Zibaldone da Canal. Tempe: Medieval and Renaissance Texts and Studies. [Google Scholar]

- Dotson, John E. 2002. Fourteenth Century Merchant Manuals and Merchant Culture. In Vierteljahrschrift für Sozial- und Wirtschaftsgeschichte. Merchant’s Books and Mercantile Pratiche from the Late Middle Ages to the Beginning of the 20th Century. Edited by Markus A. Denzel, Jean Claude Hocquet and Harald Witthöft. Stuttgart: Franz Steiner Verlag GmbH, vol. 163, pp. 75–88. [Google Scholar]

- Douglas, Mary, and Aaron Wildavsky. 1982. Risk and Culture: An Essay on the Selection of Technical and Environmental Dangers. Berkeley: University of California Press. [Google Scholar]

- Edmondson, Amy C. 2011. Strategy for Learning from Failure. In Harvard Business Review. Brighton: Harvard Business School Publishing. [Google Scholar]

- Fortunati, Maura. 2005. The fairs between lex mercatoria and ius mercatorum. In From lex Mercatoria to Commercial Law. Comparative Studies in Continental and Anglo-American Legal History. Edited by Vito Piergiovanni. Berlin: Duncker & Humblot, pp. 143–64. [Google Scholar]

- Graham, John R., Campbell R. Harvey, Jillian Popadak, and Shivaram Rajgopal. 2017. Corporate Culture: Evidence from the Field. Paper presented at 27th Annual Conference on Financial Economics and Accounting Paper, Duke I&E Research Paper No. 2016-33—Columbia Business School Research Paper No. 16-49—NBER Working Paper No. 23255, Toronto, ON, Canada, March 3. [Google Scholar]

- Hardin, Garrett. 1968. The Tragedy of the Commons. Science 162: 1243–48. [Google Scholar] [CrossRef] [PubMed]

- Von Hayek, Friedrich A. 1982. Law, Legislation and Liberty. Abingdon: Routledge and Kegan Paul. [Google Scholar]

- Ingrao, Bruna, and Giorgio Israel. 1990. The Invisible Hand: Economic Equilibrium in the History of Science Hardcover. The MIT Press (28 June 1990). Israel, Giorgio. 2015. The Invisible Hand. Economic Equilibrium in the History of Science. Available online: www.researchgate.net/profile/Giorgio_Israel/publication/277555588_The_Invisible_Hand_Economic_Equilibrium_in_the_History_of_Science/links/556c7a2d08aec22683054100/The-Invisible-Hand-Economic-Equilibrium-in-the-History-of-Science.pdf (accessed on 1 October 2017).

- ISO. 2018. The New ISO 31000 Keeps Risk Management Simple. Geneva, Switzerland: International Organization for Standardization, February 15, Pressrelease. Available online: https://www.iso.org/news/ref2263.html (accessed on 7 March 2018).

- Jung, Carl Gustav. 1921. Psychologische Typen. Zürich: Rascher. [Google Scholar]

- Kennedy, Allan A., and Terrence E. Deal. 1982. Corporate Cultures—Rites and Rituals of Corporate Life. Boston: Addison-Wesley Publishing Company. [Google Scholar]

- Luhmann, Niklas. 1991. Soziologie des Risikos. Berlin: De Gruyter. [Google Scholar]

- Luhmann, Niklas. 1993. Risk: A Sociological Theory. Berlin: De Gruyter, (English translation). [Google Scholar]

- Manapata, Michael L., Martin A. Nowaka, and David G. Rand. 2013. Information, irrationality, and the evolution of trust. Journal of Economic Behavior & Organization 90S: S57–75. [Google Scholar]

- Maschke, Erich. 1984. Das Berufsbewußtsein des mittelalterlichen Fernkaufmanns. In Die Stadt des Mittelalters. Wirtschaft und Gesellschaft. Darmstadt: Wissenschaftliche Buchgesellschaft, vol. 3. (In German) [Google Scholar]

- McChrystal, Stanley. 2015. Team of Teams: New Rules of Engagement for a Complex World. London: Penguin. [Google Scholar]

- Milkau, Udo. 2017. Risk Culture during the Last 2000 Years—From an Aleatory Society to the Illusion of Risk Control. International Journal of Financial Studies 5: 31. [Google Scholar] [CrossRef]

- Münkler, Herfried. 2010. Strategien der Sicherung: Welten der Sicherheit und Kulturen des Risikos. In Sicherheit und Risiko—Über den Umgang mit Gefahr im 21. Jahrhundert. Edited by Herfried Münkler, Matthias Bohlender and Sabine Meurer. Bielefeld: Transcript Verlag. [Google Scholar]

- Nehlsen-von Stryk, Karin. 1986. Die venezianische Seeversicherung im 15. Jahrhundert. Abhandlungen zur rechtswissenschaftlichen Grundlagenforschung, Bd. 64. Ebelsbach: Münchener Universitätsschriften, Juristische Fakultät, p. 239. [Google Scholar]

- Ostrom, Elinor. 1999. Coping with Tragedies of the Commons. Annual Review of Political Science 1999: 491–535. [Google Scholar] [CrossRef]

- Perrow, Charles. 1984. Normal Accidents: Living with High-Risk Technologies. New York: Basic Books. [Google Scholar]

- Pettigrew, Andrew M. 1979. On Studying Organizational Cultures. Administrative Science Quarterly 24: 570–81. [Google Scholar] [CrossRef]

- Piergiovanni, Vito, ed. 2005. From lex Mercatoria to Commercial law. Comparative Studies in Continental and Anglo-American Legal History. Berlin: Duncker & Humblot. [Google Scholar]

- Poincaré, Henri. 1908. Science et Méthode. Paris: Flammarion. [Google Scholar]

- Popper, Karl R. 1991. Alles Leben ist Problemlösen (All Life is Problem Solving). In Alles Leben ist Problemlösen. Edited by Karl R. Popper. Munich and Berlin: Piper. [Google Scholar]

- Pryor, John H. 1977. The Origins of the Commenda Contract. Speculum 52: 5–37. [Google Scholar] [CrossRef]

- Puga, Diego, and Daniel Trefler. 2012. International Trade and Institutional Change: Medieval Venice’s Response to Globalization. NBER Working Paper 18288. August. Available online: http://www.nber.org/papers/w18288 (accessed on 17 September 2017).

- Quinn, Robert E., and John Rohrbaugh. 1983. A Spatial Model of Effectiveness Criteria: Towards a Competing Values Approach to Organizational Analysis. Management Science 29: 363–77. [Google Scholar] [CrossRef]

- Rochlin, Gene I., Todd R. La Porte, and Karlene H. Roberts. 1987. The Self-Designing High-Reliability Organization: Aircraft Carrier Flight Operations at Sea. Naval War College Review, issue Autumn 1987. Available online: www.projectwhitehorse.com/pdfs/Self_Designing_-_LaPort.pdf (accessed on 20 September 2017).

- Schein, Edgar H. 1985. Organizational Culture and Leadership, 3rd ed.Jossey-Bass, A Wiley Imprint. San Francisco: John Wiley & Sons. [Google Scholar]

- Scheller, Benjamin. 2017. The Birth of Risk. Contingency and Mercantile Practice in Mediterrenean Sea Trade in the High and Later Middle Ages. Historische Zeitschrift 304: 305–31. [Google Scholar]

- Shapira, Roy, and Luigi Zingales. 2017. Is Pollution Value-Maximizing? The DuPont Case. Stigler Center for the Study of the Economy and the State, University of Chicago Booth School of Business. New Working Paper Series No. 13. September. Available online: research.chicagobooth.edu/-/media/research/stigler/pdfs/workingpapers/13ispollutionvaluemaximizingsep2017.pdf (accessed on 29 October 2017).

- Smircich, Linda. 1983. Concepts of Culture and Organizational Analysis. Administrative Science Quarterly 28: 339–58. [Google Scholar] [CrossRef]

- Steinbrecher, Ira (BaFin). 2015. Risk Culture: Requirements of Responsible Corporate Governance. Available online: www.bafin.de/SharedDocs/Veroeffentlichungen/EN/Fachartikel/2015/fa_bj_1508_risikokultur_en.html (accessed on 28 August 2017).

- Stiehm, Judith Hicks, and Nicholas W. Townsend. 2002. The U.S. Army War College: Military Education in a Democracy. Philadelphia: Temple University Press, p. 6. [Google Scholar]

- Taylor, Frederick Winslow. 1911. Principles of Scientific Management. New York: Harper & Brother. [Google Scholar]

- Walker, Brian, and David Salt. 2012. Resilience Practice: Building Capacity to Absorb Disturbance and Maintain Function. Washington: Island Press. [Google Scholar]

- Wilhelm, Eva-Maria. 2013. Italianismen des Handels im Deutschen und Französischen—Wege des frühneuzeitlichen Sprachkontakts. Berlin and Boston: Walter de Gruyter. [Google Scholar]

| 1 | (De Moivre 1718) as extended English version of De Mensura Sortis, Phil. Trans. Roy. Soc No. 329, January, February, March 1711, reprinted with a commentary by O. Hald in International Statistical Review 52: 229–62, 1984). |

| 2 | In Europe, only just in June 2017 a new legislation prohibits the production and distribution of C8, or PFOA, from July 2020 on (See: regulation (EU) 2017/1000). |

{kind=link}

| Organization | Title | Quote |

|---|---|---|

| Financial Stability Board (FSB; 2014) | “Guidance on Supervisory Interaction with Financial Institutions on Risk Culture” | A sound risk culture consistently supports appropriate risk awareness, behaviors and judgments about risk-taking within a strong risk governance framework. A sound risk culture bolsters effective risk management, promotes sound risk-taking, and ensures that emerging risks … are recognized, assessed, escalate, and addressed in a timely manner. Risk culture … evolves over time in relation to the events that affect the institution’s history… |

| Basel Committee on Banking Supervision (BCBS 2015) | “Corporate Governance Principles for Banks” | … norms, attitudes and behaviors related to risk awareness, risk-taking and risk management, and controls that shape decisions on risks. Risk culture influences the decisions of management and employees during the day-to-day activities and has an impact on the risks they assume. |

| German banking supervisory authority BaFin’s expert article (Steinbrecher 2015) | “Risk culture: Requirements of responsible corporate governance” | Risk culture: Requirements of responsible corporate governance |

| German banking supervisory authority BaFin (2017) | amendment to the German guidelines on risk management in banks (MaRisk) | Risk culture described in general the manner, in which staff of a banking institution (should) handle risk as part of their activities. A risk culture should support the identification and the conscious handling of risks and guarantee that decision-making leads to results, which balance all aspects of risk. An appropriate risk culture is characterized by the clear acknowledgment of the senior management to a risk-adjusted behavior, strict discipline of all staff concerning the risk appetite as communicated by the senior management and the facilitation and support of a transparent an open dialog in the bank concerning risk-relevant issues. |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bott, J.; Milkau, U. Risk Culture and the Role Model of the Honorable Merchant. J. Risk Financial Manag. 2018, 11, 40. https://doi.org/10.3390/jrfm11030040

Bott J, Milkau U. Risk Culture and the Role Model of the Honorable Merchant. Journal of Risk and Financial Management. 2018; 11(3):40. https://doi.org/10.3390/jrfm11030040

Chicago/Turabian StyleBott, Jürgen, and Udo Milkau. 2018. "Risk Culture and the Role Model of the Honorable Merchant" Journal of Risk and Financial Management 11, no. 3: 40. https://doi.org/10.3390/jrfm11030040

APA StyleBott, J., & Milkau, U. (2018). Risk Culture and the Role Model of the Honorable Merchant. Journal of Risk and Financial Management, 11(3), 40. https://doi.org/10.3390/jrfm11030040