J. Risk Financial Manag. 2026, 19(6), 449; https://doi.org/10.3390/jrfm19060449 (registering DOI) - 21 Jun 2026

Abstract

The study investigates the state-dependent dynamics of overconfidence in the Bangladesh equity market by exploring the relationship between market returns and trading volume within a nonlinear information-theoretic framework. Building up on the traditional return–volume literature, the study differentiates between total market returns and

[...] Read more.

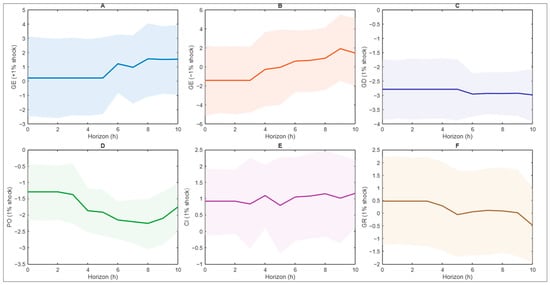

The study investigates the state-dependent dynamics of overconfidence in the Bangladesh equity market by exploring the relationship between market returns and trading volume within a nonlinear information-theoretic framework. Building up on the traditional return–volume literature, the study differentiates between total market returns and unexpected returns, with the latter representing unexpected information shocks obtained using the Market Index Model. Transfer Entropy with bootstrap inference estimates the directional and asymmetric information flows across five different market states, namely: bullish, bearish, crisis, extended crisis, and COVID-19. The evidence suggests that the overconfidence biases in aggregate market returns are small and intermittent and are reflected in poor and unstable information flow between market returns and trading volume. In comparison, unexpected market returns have a directionally significant impact on trading behavior, which supports the behavior of state-dependent overconfidence. The findings also reveal that overconfidence is higher in normal and bullish market situations but drops significantly in crisis-based situations. The asymmetric analysis indicates increased trading responses to negative returns shocks, as it is more evident that investors are more sensitive to losses and recovery expectations. The research adds to behavioral finance literature on frontier markets through an unexpected return decomposition with nonlinear causality model. The results have serious implications on market surveillance, assessment of investor behavior and design of regulatory policies.

Full article

(This article belongs to the Section Financial Markets)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}