Control-Enhancing Mechanisms and Earnings Management: Empirical Evidence from Pakistan

Abstract

:1. Introduction

2. The Literature Review and Hypothesis Development

3. Data and Research Methods

3.1. Sample Selection and Data Sources

3.2. Measurement of Variables

3.2.1. Ownership Types

- Family ownership (FAMO)

- Foreign ownership (FORO)

- Institutional ownership (INSO)

- Widely held (WIDO)

- State-owned (STAO)

- Managerial ownership (MANO)

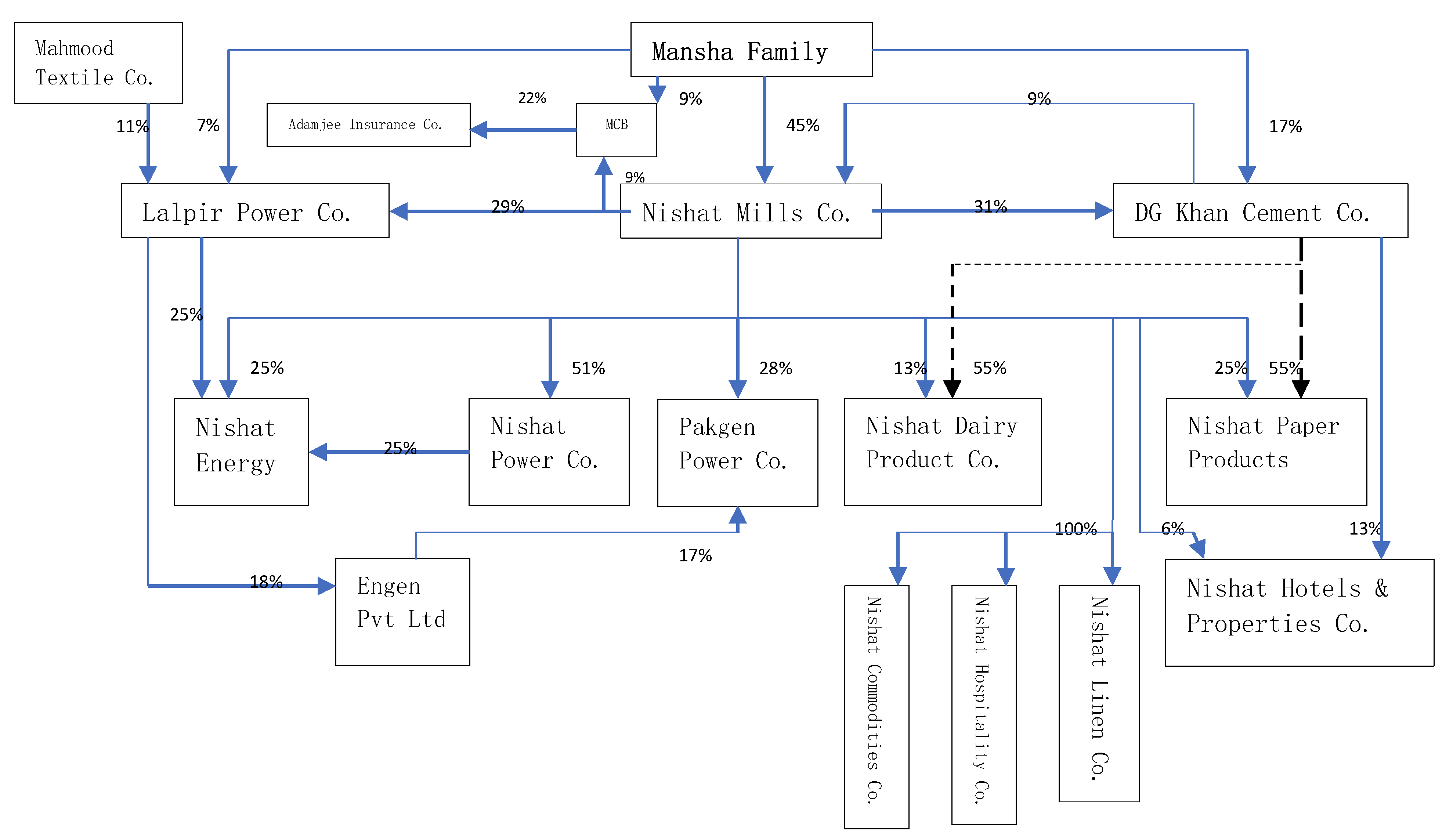

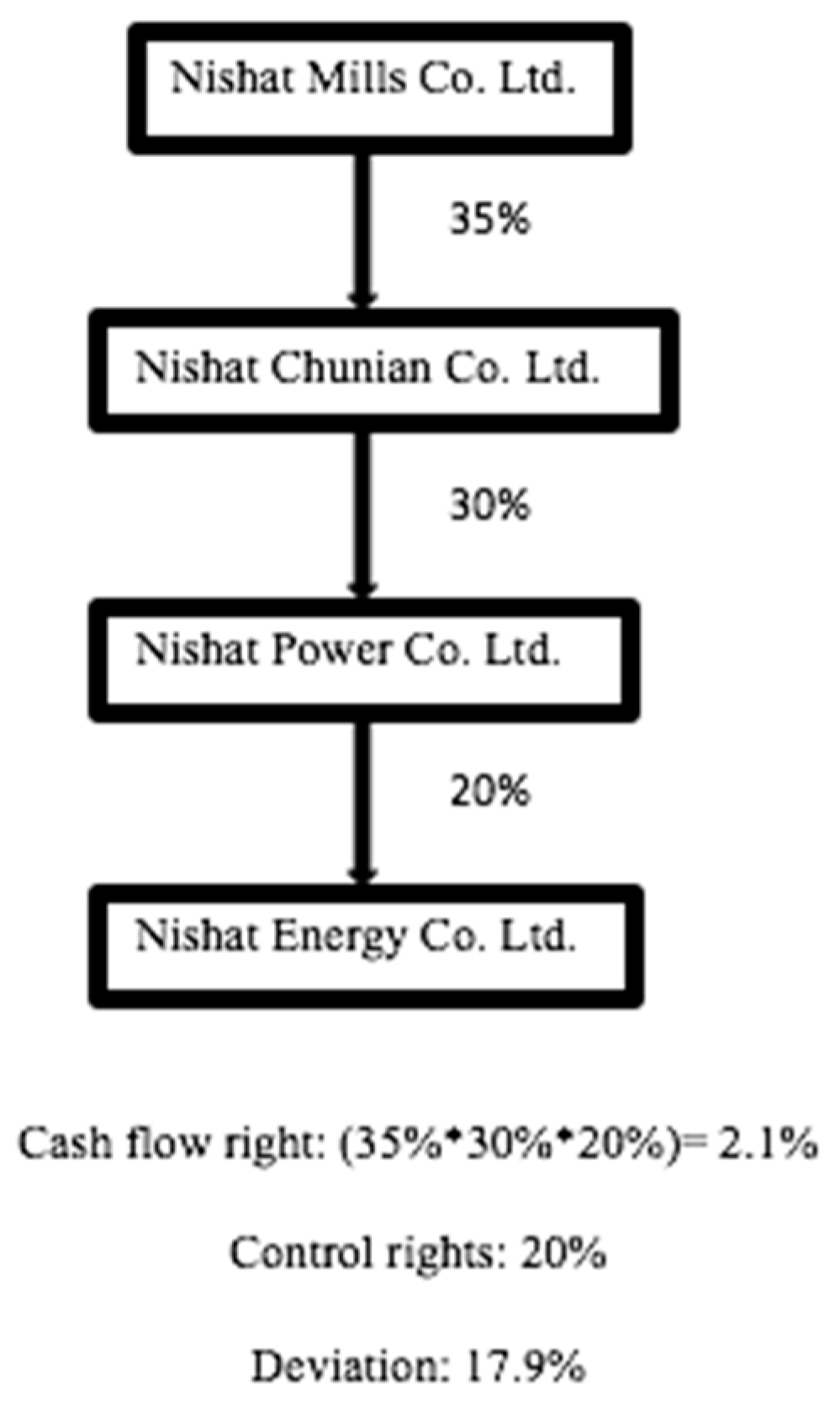

3.2.2. Calculation of Cash Flow Right and Control Right

- Pyramidal structure (PYO)

- Multiple control chains structure (MCH)

- Cross-holding structure (CHO)

3.2.3. Measurement of Earnings Management

Accruals Earnings Management (AEM)

Measurement of Real Earnings Management

4. Empirical Results and Discussion

4.1. Control-Enhancing Mechanisms and Accruals Earnings Management

4.2. Control-Enhancing Mechanisms and Real Earnings Management

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variable Name (Notation) | Variable Definition |

|---|---|

| Family ownership (FAMO) | A dummy variable, which equals to one if the family has 20 or more percentage of ownership and is the largest shareholder of the firm having a family member as a representative on board, otherwise zero. This proxy has been used by Bhaumik and Gregoriou (2010); Bodnaruk et al. (2017). |

| Foreign ownership (FORO) | A dummy variable equals to 1 if a foreign investor or foreign firm is holding 10% or more in the shares of the firm, otherwise zero. |

| Institutional ownership (INSO) | A dummy variable equals to 1 if 5 or more percentage of firm’s shares are owned by institutions (mutual funds, pension funds, insurance companies, investment firms, endowments, privately held firms or any other firm providing services of managing funds on behalf of others), otherwise zero. This proxy has been used in Bodnaruk et al. (2017) and (Guo and Ma 2015). |

| Widely-held ownership (WIDO) | A dummy variable equals one if firms’ shares are widely held at the control threshold which is 20%, otherwise zero. |

| State ownership (STAO) | A dummy variable, which is equal to 1 if 20 or more percentage of shares of the firm is held by government or any government-owned institute or agency, otherwise zero. |

| Managerial ownership (MANO) | A dummy variable equals to one if CEO, board chairman, or vice-chairman, or managers hold 20 or more percentage of shares in the company, zero otherwise. |

| The pyramid control mechanism (PYO) | A dummy variable equals one if a firm is owned through a pyramid structure, Otherwise 0. |

| Multiple control chain mechanism (MCH) | A dummy variable equals one if a firm is owned through a multiple control chain structure, Otherwise 0. |

| Cross-holding mechanism (CHO) | A dummy variable equals one if a firm is owned through a cross-holding structure, Otherwise 0. |

ACCRUALS EARNINGS MANAGEMENT:

| ABSDAJ: The absolute value of the residual taken from the Jones (1991) model. ABSDAMJ: The absolute value of residual taken from the modified Jones model (1995). ABSDAK: The absolute value of the residual taken from the Kothari et al. (2005) model. |

REAL EARNINGS MANAGEMENT:

| ABSOVP: The absolute value of the residual taken from the Roychowdhury (2006) model. DISEXP: The absolute value of the residual taken from the Roychowdhury (2006) model. TREM: The aggregate sum of both residuals (OP and DISEXP). |

References

- Achleitner, Ann-Kristin, and Reiner Braun. 2014. Entrepreneurial Finance: EinÜberblick. In Handbuch Entrepreneurship. Berlin: Springer, pp. 1–20. [Google Scholar]

- Aharony, Joseph, Wang Jiwei, and Yuan Hongqi. 2010. Tunneling as an incentive for earnings management during the IPO process in China. Journal of Accounting and Public Policy 29: 1–26. [Google Scholar] [CrossRef]

- Ahmed, Hafeez, and Attiya Yasmin Javid. 2008. Dynamics and determinants of dividend policy in Pakistan (evidence from Karachi stock exchange non-financial listed firms). International Research Journal of Finance and Economics 25: 148–71. [Google Scholar]

- Ahmad, Hafeez, and Attiya Javid. 2010. The ownership structure and dividend pay-out policy in Pakistan (evidence from Karachi stock exchange 100 index). International Journal of Business Management and Economic Research 1: 58–69. [Google Scholar]

- Anagnostopoulou, Seraina, and Tsekrekos Andrianos. 2017. The effect of financial leverage on real and accrual-based earnings management. Accounting and Business Research 47: 191–36. [Google Scholar] [CrossRef]

- Ball, Ray. 2013. Accounting informs investors and earnings management is rife: Two questionable beliefs. Accounting Horizons 27: 847–53. [Google Scholar] [CrossRef]

- Ball, Ray, and Lakshmanan Shivakumar. 2008. Earnings Quality at Initial Public Offerings. Journal of Accounting and Economics 45: 324–49. [Google Scholar] [CrossRef]

- Banko, John, Melissa Frye, Weishen Wang, and Ann Marie Whyte. 2013. Earnings Management and Annual General Meetings: The Role of Managerial Entrenchment. The Financial Review 48: 259–82. [Google Scholar] [CrossRef]

- Bao, Shuji Rosey, and Krista Lewellyn. 2017. Ownership structure and earnings management in emerging markets—An institutionalized agency perspective. International Business Review 26: 828–38. [Google Scholar] [CrossRef]

- Bebchuck, Lucian Arye, Reinier Kraakman, and George Triantis. 2000. Stock Pyramids, Cross-Ownership, and Dual Class Equity. In Concentrated Corporate Ownership. Edited by Randall K. Mork. Chicago: University of Chicago Press. [Google Scholar]

- Becker, Connie L., Mark L DeFond, James Jiambalvo, and K. R. Subramanyam. 1998. The effect of audit quality on earnings management. Contemporary Accounting Research 15: 1–24. [Google Scholar] [CrossRef]

- Berle, Adolf, and Gardiner Means. 1932. Private Property and the Modern Corporation. New York: Mac-Millan. [Google Scholar]

- Beuselinck, Christof, and Marc Deloof. 2014. Earnings management in business groups: Tax incentives or expropriation concealment? The International Journal of Accounting 49: 27–52. [Google Scholar] [CrossRef]

- Bhaumik, Sumon Kumar, and Andros Gregoriou. 2010. ‘Family’ ownership, tunneling and earnings management: A review of the literature. Journal of Economic Surveys 24: 705–30. [Google Scholar] [CrossRef]

- Bhutta, Aamir, Johan Knif, and Muhammad Fayyaz Sheikh. 2016. Ownership Concentration, Client Importance, and Earnings Management: Evidence from Pakistani Business Groups. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Bodnaruk, Andriy, Massimo Massa, and Vijay Yadav. 2017. Family ownership, country governance, and foreign portfolio investment. Journal of Empirical Finance 41: 96–115. [Google Scholar] [CrossRef]

- Briamonte, Massimiliano Farina, Felice Addeo, Fabio Fiano, and Marco Sorrentino. 2017. The Effect of Pyramidal Structures on Earnings Management: Evidence from Italian Listed Companies. Corporate Ownership & Control 14: 64–73. [Google Scholar]

- Brown, Kareen, Changling Chen, and Duane Kennedy. 2017. Target ownership plans and earnings management. Advances in Accounting 36: 87–101. [Google Scholar] [CrossRef]

- Butt, Safdar, and Arshad Hasan. 2009. Impact of ownership structure and corporate governance on the capital structure of Pakistani listed companies. International Journal of Business & Management 4: 8. [Google Scholar]

- Byun, Hae-Young, Sunhwa Choi, Lee-Seok Hwang, and Robert G. Kim. 2013. Business group affiliation, ownership structure, and the cost of debt. Journal of Corporate Finance 23: 311–31. [Google Scholar] [CrossRef]

- Chan, Lilian H., Kevin CW Chen, Tai Yuan Chen, and Yangxin Yu. 2014. Substitution between real and accruals-based earnings management after voluntary adoption of compensation clawback provisions. The Accounting Review 90: 147–74. [Google Scholar] [CrossRef]

- Chang, Sea Jin. 2003. Ownership structure, expropriation, and performance of group-affiliated companies in Korea. Academy of Management Journal 46: 238–53. [Google Scholar]

- Chen, Xia, Jarrad Harford, and Kai Li. 2007. Monitoring: Which institutions matter? Journal of financial Economics 86: 279–305. [Google Scholar] [CrossRef]

- Chen, Charles J.P., Zengquan Li, Xijia Su, and Zheng Sun. 2011. Rent-seeking incentives, corporate political connections, and the control structure of private firms: Chinese evidence. Journal of Corporate Finance 17: 229–43. [Google Scholar] [CrossRef]

- Choi, Suk Bong, Soo Hee Lee, and Christopher Williams. 2011. Ownership and firm innovation in a transition economy: Evidence from China. Research Policy 40: 441–52. [Google Scholar] [CrossRef]

- Claessens, Stijn, and Joseph PH Fan. 2002. Corporate governance in Asia: A survey. International Review of Finance 3: 71–103. [Google Scholar] [CrossRef]

- Claessens, Stijn, Simeon Djankov, and Larry HP Lang. 2000. The separation of ownership and control in East Asian corporations. Journal of Financial Economics 58: 81–112. [Google Scholar] [CrossRef]

- Cohen, Daniel A., and Paul Zarowin. 2010. Accrual-Based and Real Earnings Management Activities Around Seasoned Equity Offerings. Journal of Accounting and Economics 50: 2–19. [Google Scholar] [CrossRef]

- Cohen, Daniel A., Aiyesha Dey, and Thomas Z. Lys. 2008. Real and accrual-based earnings management in the pre-and post-Sarbanes-Oxley periods. The Accounting Review 83: 757–87. [Google Scholar] [CrossRef]

- Dechow, Patricia M., Richard G. Sloan, and Amy P. Sweeney. 1995. Detecting earnings management. Accounting Review 70: 193–225. [Google Scholar]

- Ducassy, Isabelle, and Alexis Guyot. 2017. Complex ownership structures, corporate governance, and firm performance: The French context. Research in International Business and Finance 39: 291–306. [Google Scholar] [CrossRef]

- Dye, Ronald A., and Robert E. Verrecchia. 1995. Discretion vs. uniformity: Choices under GAAP. The Accounting Review 70: 389–415. [Google Scholar]

- Evans, John H., and Sri S. Sridhar. 1996. Multiple control systems, accrual accounting, and earnings management. Journal of Accounting Research 34: 45–65. [Google Scholar]

- Faccio, Mara, and Larry HP Lang. 2002. The ultimate ownership of Western European corporations. Journal of Financial Economics 65: 365–95. [Google Scholar] [CrossRef]

- Fan, Joseph PH, and Tak Jun Wong. 2002. Corporate ownership structure and the informativeness of accounting earnings in East Asia. Journal of Accounting and Economics 33: 401–25. [Google Scholar] [CrossRef]

- Gedajlovic, Eric, and Daniel M. Shapiro. 2002. Ownership structure and firm profitability in Japan. Academy of Management Journal 45: 565. [Google Scholar]

- Gunny, Katherine A. 2009. The relation between earnings management using real activities manipulation and future performance: Evidence from meeting earnings benchmarks. Contemporary Accounting Research 27: 855–88. [Google Scholar] [CrossRef]

- Guo, Fei, and Shiguang Ma. 2015. Ownership Characteristics and Earnings Management in China. Chinese Economy 48: 372–95. [Google Scholar] [CrossRef]

- Hayn, Carla. 1995. The information content of losses. Journal of Accounting and Economics 20: 125–53. [Google Scholar] [CrossRef]

- He, Wei, and NyoNyo A. Kyaw. 2018. Ownership structure and investment decisions of Chinese SOEs. Research in International Business and Finance 43: 48–57. [Google Scholar] [CrossRef]

- Healy, Paul M., and James M. Wahlen. 1999. A review of the earnings management literature and its implications for standard setting. Accounting Horizons 13: 365–83. [Google Scholar] [CrossRef]

- Holderness, Clifford G., Randall S. Kroszner, and Dennis P. Sheehan. 1999. Were the good old days that good? Changes in managerial stock ownership since the great depression. The Journal of Finance 54: 435–69. [Google Scholar] [CrossRef]

- Hribar, Paul, and Daniel W. Collins. 2002. Errors in estimating accruals: Implications for empirical research. Journal of Accounting Research 40: 105–34. [Google Scholar] [CrossRef]

- Huang, Hua-Wei, Suchismita Mishra, and Kanan Raghunandan. 2007. Types of nonaudit fees and financial reporting quality. Auditing: A Journal of Practice & Theory 26: 133–45. [Google Scholar]

- Ikram, Atif, Syed Ali, and Asjad Naqvi. 2005. Family Business Groups and Tunneling Framework: Application and Evidence from Pakistan. Lahore: Centre for Management and Research Lahore University of Management Sciences. [Google Scholar]

- Iqbal, Nadeem, Naveed Ahmad, and Hamad Naqvi. 2014. Corporate social responsibility and its possible impact on a firm’s financial performance in the banking sector of Pakistan. Arabian Journal of Business and Management Review 3: 150–55. [Google Scholar]

- Jaggi, Bikki, and Picheng Lee. 2002. Earnings management response to debt covenant violations and debt restructuring. Journal of Accounting, Auditing & Finance 17: 295–324. [Google Scholar]

- Jaggi, Bikki, and Sidney Leung. 2007. Impact of family dominance on monitoring of earnings management by audit committees: Evidence from Hong Kong. Journal of International Accounting, Auditing and Taxation 16: 27–50. [Google Scholar] [CrossRef]

- Javid, Attiya Y., and Eatzaz Ahmed. 2008. The Conditional Capital Asset Pricing Model: Evidence from Karachi Stock Exchange. No. 2008: 48. Islamabad: Pakistan Institute of Development Economics. [Google Scholar]

- Jiambalvo, James, Shivaram Rajgopal, and Mohan Venkatachalam. 2002. Institutional ownership and the extent to which stock prices reflect future earnings. Contemporary Accounting Research 19: 117–45. [Google Scholar] [CrossRef]

- Jiraporn, Pornsit, Gary A. Miller, Soon Suk Yoon, and Young S. Kim. 2008. Is earnings management opportunistic or beneficial? An agency theory perspective. International Review of Financial Analysis 17: 622–34. [Google Scholar] [CrossRef]

- Jones, Jennifer J. 1991. Earnings management during import relief investigations. Journal of Accounting Research 29: 193–28. [Google Scholar] [CrossRef]

- Jung, Kooyul, and Soo Young Kwon. 2002. Ownership structure and earnings informativeness: Evidence from Korea. The International Journal of Accounting 37: 301–25. [Google Scholar] [CrossRef]

- Jungeun, Cho, Goh Jaimin, and Lee Jaehong. 2012. Chaebol firms’ real and accrual-based earnings management in the pre-and post-Asian financial crisis periods. Journal of Modern Accounting and Auditing 8: 915. [Google Scholar]

- Kaul, Aditya, Vikas Mehrotra, and Randall Morck. 2000. Demand curves for stocks do slope down: New evidence from an index weights adjustment. The Journal of Finance 55: 893–912. [Google Scholar] [CrossRef]

- Kim, Jeong-Bon, and Cheong H. Yi. 2006. Ownership structure, business group affiliation, listing status, and earnings management: Evidence from Korea. Contemporary Accounting Research 23: 427–64. [Google Scholar] [CrossRef]

- Kim, Jeong-Bon, Dan A. Simunic, Michael T. Stein, and Cheong H. Yi. 2011. Voluntary audits and the cost of debt capital for privately held firms: Korean evidence. Contemporary Accounting Research 28: 585–615. [Google Scholar] [CrossRef]

- Klassen, Kenneth J. 1997. The impact of inside ownership concentration on the trade-off between financial and tax reporting. Accounting Review 72: 455–74. [Google Scholar]

- Klein, April. 2002. Audit committee, the board of director characteristics, and earnings management. Journal of Accounting and Economics 33: 375–400. [Google Scholar] [CrossRef]

- Kothari, Sagar P., Andrew J. Leone, and Charles E. Wasley. 2005. Performance Matched Discretionary Accrual Measures. Journal of Accounting and Economics 39: 163–97. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert W. Vishny. 1998. Law and finance. Journal of Political Economy 106: 1113–55. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert W. Vishny. 1999. Corporate ownership around the world. The Journal of Finance 54: 471–517. [Google Scholar] [CrossRef]

- La Porta, Rafael, Florencio Lopez-de-Silanes, Andrei Shleifer, and Robert W. Vishny. 2000. Investor Protection and Corporate Governance. Journal of Financial Economics 58: 3–27. [Google Scholar] [CrossRef]

- Lemmon, Michael L., and Karl V. Lins. 2003. Ownership structure, corporate governance, and firm value: Evidence from the East Asian financial crisis. The Journal of Finance 58: 1445–68. [Google Scholar] [CrossRef]

- Leuz, Christian, Dhananjay Nanda, and Peter D. Wysocki. 2003. Earnings management and investor protection: an international comparison. Journal of Financial Economics 69: 505–27. [Google Scholar] [CrossRef]

- Li, Kuei-Fu, and Yi-Ping Liao. 2014. Directors’ and officers’ liability insurance and investment efficiency: Evidence from Taiwan. Pacific-Basin Finance Journal 29: 18–34. [Google Scholar] [CrossRef]

- Li, Shaomin, David D. Selover, and Michael Stein. 2011. “Keep silent and make money”: Institutional patterns of earnings management in China. Journal of Asian Economics 22: 369–82. [Google Scholar] [CrossRef]

- Malan, Irfah Najihah Binti Basir, Norhana Binti Salamudin, and Noryati Binti Ahmad. 2012. The impact of pyramid structure towards corporate value among Malaysian firms. International Journal of Management and Business Studies 2: 18–24. [Google Scholar]

- Malik, Hilal Ahmed, Syed Muhammad Ahsan, and Jan Shair Khan. 2017. Impact of ownership structure on corporate social responsibility evidence from Pakistan. International Journal of Scientific & Engineering Research 8: 1938–52. [Google Scholar]

- Mindzak, Justin, and Tao Zeng. 2018. The impact of pyramid ownership on earnings management. Asian Review of Accounting 26: 208–24. [Google Scholar] [CrossRef]

- Peasnell, Ken V., Peter F. Pope, and Steven Young. 2005. Board Monitoring and Earnings Management: Do Outside Directors Influence Abnormal Accruals? Journal of Business Finance & Accounting 32: 1311–46. [Google Scholar]

- Rangan, Srinivasan. 1998. Earnings management and the performance of seasoned equity offerings. Journal of Financial Economics 50: 101–22. [Google Scholar] [CrossRef]

- Rodríguez-Pérez, Gonzalo, and Stefan van Hemmen. 2010. Debt, diversification and earnings management. Journal of Accounting and Public Policy 29: 138–59. [Google Scholar] [CrossRef]

- Roychowdhury, Sugata. 2006. Earnings management through real activities manipulation. Journal of Accounting and Economics 42: 335–70. [Google Scholar] [CrossRef]

- Sarkar, Jayati, Subrata Sarkar, and Kaustav Sen. 2013. Insider Control, Group Affiliation and Earnings Management in Emerging Economies: Evidence from India. SSRN Electronic Journal. [Google Scholar] [CrossRef] [Green Version]

- Shivakumar, Lakshmanan. 2000. Do Firms Mislead Investors by Overstating Earnings before Seasoned Equity Offerings? Journal of Accounting and Economics 29: 339–71. [Google Scholar] [CrossRef]

- Shleifer, Andrei, and Robert W. Vishny. 1986. Large shareholders and corporate control. Journal of Political Economy 94: 461–88. [Google Scholar] [CrossRef]

- Sun, Lan, and Subhrendu Rath. 2010. Earnings management research: a review of contemporary research methods. Global Review of accounting and Finance 1: 121–35. [Google Scholar]

- Uddin, Shahab, Muhammad Arshad Khan, and Attiya Yasmin Javid. 2017. The effects of ownership structure on the likelihood of financial distress: Empirical evidence. Corporate Governance: The International Journal of Business in Society 17: 589–612. [Google Scholar]

- Wang, Dechun. 2006. Founding family ownership and earnings quality. Journal of Accounting Research 44: 619–56. [Google Scholar] [CrossRef]

- Wang, Liu, and Kenneth Yung. 2011. Do state enterprises manage earnings more than privately owned firms? The case of China. Journal of Business Finance & Accounting 38: 794–812. [Google Scholar]

- Warfield, Terry D., John J. Wild, and Kenneth L. Wild. 1995. Managerial ownership, accounting choices, and informativeness of earnings. Journal of Accounting and Economics 20: 61–91. [Google Scholar] [CrossRef]

- Watts, Ross L., and Jerold L. Zimmerman. 1986. Positive Accounting Theory. Englewood Cliffs: Prentice-Hall. [Google Scholar]

- Wongsunwai, Wan. 2013. The effect of external monitoring on accrual-based and real earnings management: evidence from venture-backed initial public offerings. Contemporary Accounting Research 30: 296–24. [Google Scholar] [CrossRef]

- Xie, Biao, Wallace N. Davidson III, and Peter J. Dadalt. 2003. Earnings management and corporate governance: the role of the board and the audit committee. Journal of Corporate Finance 9: 295–316. [Google Scholar] [CrossRef]

- Yakura, Shinksuke, and Li Guo. 2009. The Cross Holding of Company Shares: A Preliminary Legal Study of Japan and China. Frontiers of Law in China 4: 507–22. [Google Scholar] [CrossRef]

- Zang, Amy Y. 2012. Evidence on the Trade-Off between Real Activities Manipulation and Accrual-Based Earnings Management. The Accounting Review 87: 675–703. [Google Scholar] [CrossRef]

| Sector | Sector Code | No. of Firm Years | Percentage (%) |

|---|---|---|---|

| Automobile Assembler | 801 | 144 | 4% |

| Automobile Part and Accessories | 802 | 84 | 2.3% |

| Cable and Electrical Goods | 803 | 48 | 1.3% |

| Cement | 804 | 204 | 5.6% |

| Chemical | 805 | 288 | 8% |

| Engineering | 808 | 96 | 2.6% |

| Fertilizer | 809 | 48 | 1.3% |

| Food and Personal Care Products | 810 | 204 | 5.6% |

| Glass and Ceramics | 811 | 72 | 2% |

| Jute | 814 | 12 | 0.03% |

| Leather and Tanneries | 816 | 24 | 0.6% |

| Miscellaneous | 818 | 144 | 4% |

| Oil and Gas Exploration | 820 | 36 | 0.09% |

| Oil and Gas Marketing | 821 | 48 | 1.4% |

| Paper and Board | 822 | 96 | 2.6% |

| Pharmaceuticals | 823 | 96 | 2.6% |

| Power Generation and Distribution | 824 | 96 | 2.6% |

| Refinery | 825 | 48 | 1.4% |

| Sugar and Allied Industries | 826 | 288 | 8% |

| Synthetic and Rayon | 827 | 72 | 2% |

| Technology and Communication | 828 | 108 | 2.9% |

| Textile Composite | 829 | 432 | 11% |

| Textile Spinning | 830 | 744 | 20.5% |

| Textile Weaving | 831 | 120 | 3.3% |

| Tobacco | 832 | 24 | 0.06% |

| Transport | 833 | 36 | 0.09% |

| Vanaspati and Allied Industries | 834 | 48 | 1.4% |

| Woolen | 835 | 12 | 0.03% |

| Variable | Obs | Mean | Median | Std. Dev | Minimum | Maximum |

|---|---|---|---|---|---|---|

| ABSDAMJ | 3119 | 0.1748 | 0.0955 | 0.8472 | 0.0000 | 34.2804 |

| ABSDAK | 3119 | 0.1813 | 0.0986 | 0.8472 | 0.0000 | 33.8436 |

| ABSDAJ | 3119 | 0.1654 | 0.0884 | 0.8434 | 0.0000 | 34.2558 |

| ABSOVP | 2839 | 0.1110 | 0.0800 | 0.1203 | 0.0000 | 1.47219 |

| DISEXP | 2839 | −0.000 | 0.0403 | 0.1330 | −2.1745 | 0.1893 |

| TREM | 2839 | 0.1106 | 0.1119 | 0.1393 | −1.4999 | 1.4612 |

| PYO | 3624 | 0.4370 | 0 | 0.4960 | 0 | 1 |

| MCH | 3624 | 0.1026 | 0 | 0.3035 | 0 | 1 |

| CHO | 3624 | 0.0943 | 0 | 0.5671 | 0 | 1 |

| Age | 3408 | 32.9278 | 29 | 17.1680 | 3 | 155 |

| Loss | 3410 | 0.5374 | 0.5510 | 0.2237 | 0 | 0.8899 |

| Sales Growth | 3104 | 0.0959 | 0.0738 | 0.3448 | −1.1552 | 1.2690 |

| Size | 3410 | 14.7704 | 14.7336 | 1.7585 | 7.1412 | 20.1949 |

| Leverage | 3169 | 0.6702 | 0.6091 | 0.4980 | 0.0820 | 3.7389 |

| CFO | 2758 | 12.8590 | 12.8310 | 2.0186 | 3.6109 | 19.2226 |

| ROA | 3371 | 0.0809 | 0.0568 | 0.1559 | −3.8502 | 1.9043 |

| ABSDAMJ | ABSDAK | ABSDAJ | ABSOVP | DISEXP | TREM | PYO | MCH | CHO | Age | Sales G | Size | Leverage | CFO | ROA | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ABSDAMJ | 1 | ||||||||||||||

| ABSDAK | 0.9984 | 1 | |||||||||||||

| ABSDAJ | 0.9997 | 0.9981 | 1 | ||||||||||||

| ABSOVP | 0.0893 | 0.0906 | 0.0876 | 1 | |||||||||||

| DISEXP | −0.0502 | −0.0467 | −0.0461 | −0.4021 | 1 | ||||||||||

| TREM | 0.0267 | 0.0312 | 0.0292 | 0.4544 | 0.6329 | 1 | |||||||||

| PYO | 0.0371 | 0.0385 | 0.0373 | 0.0709 | 0.1691 | 0.1046 | 1 | ||||||||

| MCH | 0.0099 | 0.0122 | 0.0115 | 0.0222 | 0.2814 | 0.2550 | −0.2883 | 1 | |||||||

| CHO | 0.0010 | 0.0004 | 0.0015 | −0.0336 | −0.0179 | −0.0110 | −0.0901 | −0.0383 | 1 | ||||||

| Age | 0.0155 | 0.0164 | 0.0152 | 0.0206 | 0.1130 | 0.0925 | 0.0366 | 0.1054 | −0.0418 | 1 | |||||

| Sales G | −0.2536 | −0.2532 | −0.2557 | −0.1143 | −0.1684 | −0.0672 | −0.0603 | 0.0766 | −0.0189 | −0.0052 | 1 | ||||

| Size | −0.0968 | −0.1031 | −0.0923 | −0.0671 | 0.0782 | −0.0193 | 0.1424 | 0.0578 | −0.0235 | 0.0515 | 0.0228 | 1 | |||

| Leverage | 0.3064 | 0.3153 | 0.3018 | 0.0090 | 0.0071 | 0.0145 | 0.0327 | −0.0337 | −0.0058 | −0.1097 | −0.1922 | −0.2861 | 1 | ||

| CFO | 0.0291 | 0.0263 | 0.0321 | −0.0901 | 0.0714 | 0.0067 | 0.0954 | 0.1023 | −0.0300 | 0.0401 | 0.0820 | 0.8754 | −0.1924 | 1 | |

| ROA | 0.1707 | 0.1856 | 0.1707 | −0.2113 | −0.1932 | −0.0093 | −0.0049 | 0.0432 | −0.0349 | 0.0081 | −0.0787 | −0.0171 | 0.1833 | 0.1680 | 1 |

| Ownership Type | Proportion of Firms |

| Family ownership (FAMO) | 0.807 or 80.7% |

| Foreign ownership (FORO) | 0.152 or 15.2% |

| Institutional ownership (INSO) | 0.432 or 43.2% |

| Widely-held ownership (WIDO) | 0.032 or 3.2% |

| State ownership (STAO) | 0.033 or 3.3% |

| Managerial ownership (MANO) | 0.039 or 3.9% |

| Control-Enhancing Mechanisms | Proportion of Firms |

| Pyramid control mechanism (PYO) | 0.437 or 43.7% |

| Multiple control chain mechanism (MCH) | 0.102 or 10.2% |

| Cross-holding mechanism (CHO) | 0.094 or 9.4% |

| Modified Jones Model (1995) ABSDAMJ | Jones Model (1991) ABSDAJ | Kothari et al., Model (2005) ABSDAK | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variables | 1 | 2 | 3 | 1 | 2 | 3 | 1 | 2 | 3 |

| PYO | 0.0946 ** | 0.0955 ** | 0.1026 ** | ||||||

| (1.96) | (1.97) | (2.13) | |||||||

| MCH | 0.1004 ** | 0.1015 ** | 0.1082 ** | ||||||

| (2.1) | (2.12) | (2.27) | |||||||

| CHO | 0.1689 | 0.1726 | 0.1672 | ||||||

| (0.77) | (0.79) | (0.77) | |||||||

| Age | 0.0009 | 0.0009 | 0.0013 | 0.0009 | 0.001 | 0.0014 | 0.0009 | 0.001 | 0.0014 |

| (0.62) | (0.65) | −(0.90) | (0.64) | (0.67) | (0.92) | (0.63) | (0.66) | (0.94) | |

| Loss | 0.1679 | 0.1689 | 0.1731 | 0.1703 | 0.1714 | 0.1755 | 0.1677 | 0.1689 | 0.1733 |

| (0.148) | (1.49) | (1.53) | (1.51) | (1.52) | (1.55) | (1.48) | (1.49) | (1.53) | |

| Sales Growth | −0.0065 | −0.0062 | −0.0051 | −0.0053 | −0.005 | −0.0039 | −0.008 | −0.0078 | −0.0066 |

| (−0.22) | (−0.21) | (−0.17) | (−0.18) | (−0.17) | (−0.13) | (−0.27) | (−0.26) | (−0.22) | |

| Size | −0.1270 *** | −0.1276 *** | −0.0123 *** | −0.1260 *** | −0.1266 *** | −0.0122 *** | −0.1309 *** | −0.1316 *** | −0.0126 *** |

| (−2.75) | (−2.76) | (−2.67) | (−2.73) | (−2.74) | (−2.65) | (−2.83) | (−2.85) | (−2.74) | |

| Leverage | 0.5949 *** | 0.5951 *** | 0.5963 *** | 0.5933 *** | 0.5935 *** | 0.5947 *** | 0.6189 *** | 0.6171 *** | 0.6183 *** |

| (10.70) | (10.67) | (10.68) | (10.66) | (10.66) | (10.67) | (11.12) | (11.13) | (11.14) | |

| CFO | 0.0499 *** | 0.0498 *** | 0.0518 *** | 0.0497 *** | 0.0495 *** | 0.0516 *** | 0.0474 *** | 0.0473 *** | 0.0495 *** |

| (3.14) | (3.13) | (3.26) | (3.12) | (3.12) | (3.25) | (2.99) | (2.99) | (3.13) | |

| ROA | 2.1062 *** | 2.1084 *** | 2.1123 *** | 2.1019 *** | 2.1041 *** | 2.1082 *** | 2.1168 *** | 2.1191 *** | 2.1239 *** |

| (8.62) | (8.63) | (8.63) | (8.61) | (8.62) | (8.63) | (8.70) | (8.71) | (8.72) | |

| Cons | −0.9150 ** | −0.9167 ** | −0.906 ** | −0.9115 ** | −0.9133 ** | −0.9033 ** | −0.8617 ** | −0.8634 ** | −8.550 ** |

| (−2.45) | (−2.46) | (−2.43) | (−2.44) | (−2.45) | (−2.42) | (−2.32) | (−2.33) | (−2.30) | |

| Year Control | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry Control | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Highest VIF | 1.92 | 1.92 | 1.92 | 1.8 | 1.92 | 1.92 | 1.92 | 1.92 | 1.91 |

| N | 2013 | 2013 | 2013 | 2013 | 2013 | 2013 | 2000 | 2000 | 2000 |

| R-Square | 0.1528 | 0.1531 | 0.1514 | 0.1531 | 0.1533 | 0.1516 | 0.16 | 0.1602 | 0.1583 |

| F Statistic | 7.88 | 7.9 | 7.8 | 7.9 | 7.92 | 7.81 | 8.27 | 8.29 | 8.17 |

| P Value | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

| Overproduction Model (ABSOVP) | Discretionary Expenses Model (DISEXP) | Total Real Earning Management (TREM) | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Variables | 1 | 2 | 3 | 1 | 2 | 3 | 1 | 2 | 3 |

| PYO | 0.0090 * | 0.0150 *** | 0.0180 * | ||||||

| (1.83) | (3.22) | (1.85) | |||||||

| MCH | 0.0083 * | 0.0141 *** | 0.0160 * | ||||||

| (1.70) | (3.08) | (1.67) | |||||||

| CHO | −0.0103 | −0.0099 | −0.0311 | ||||||

| (−0.46) | (−0.48) | (−0.71) | |||||||

| Age | 0.0003 ** | 0.0003 ** | 0.0004 ** | 0.0003 *** | 0.0004 *** | 0.0004 *** | 0.0007 ** | 0.0007 ** | 0.0007 ** |

| (2.39) | (2.44) | (2.56) | (2.66) | (2.74) | (2.96) | (2.41) | (2.46) | (2.55) | |

| Loss | 0.0111 | 0.0112 | 0.0112 | −0.0177 | −0.0175 | −0.0174 | −0.0116 | −0.0113 | −0.0114 |

| (0.96) | (0.97) | (0.97) | (−1.63) | (−1.61) | (−1.59) | (−0.51) | (−0.50) | (−0.50) | |

| Sales Growth | −0.0089 *** | −0.0089 *** | −0.0089 *** | −0.0070 ** | −0.0069 ** | −0.0069 ** | −0.0172 *** | −0.0171 *** | −0.0172 *** |

| (−2.93) | (−2.92) | (−2.91) | (−2.35) | (−2.33) | (−2.34) | (−2.76) | (−2.76) | (−2.77) | |

| Size | −0.00098 ** | −0.00098 ** | −0.00093 ** | 0.0004 | 0.0004 | 0.0005 | −0.0012 | −0.0012 | −0.0012 |

| (−2.08) | (−2.08) | (−1.99) | (1.05) | (1.05) | (1.19) | (−1.39) | (−1.39) | (−1.30) | |

| Leverage | 0.0466 *** | 0.0467 *** | 0.0467 *** | 0.0005 | 0.0005 | 0.0006 | 0.0649 *** | 0.0649 *** | 0.0649 *** |

| (8.20) | (8.20) | (8.20) | (0.10) | (0.11) | (0.12) | (5.84) | (5.84) | (5.84) | |

| CFO | −0.0007 | −0.0007 | −0.0005 | 0.0017 | 0.0017 | 0.002 | 0.0037 | 0.0038 | 0.004 |

| (−0.47) | (−0.46) | (−0.36) | (1.15) | (1.16) | (1.36) | (1.16) | (1.18) | (1.28) | |

| ROA | −0.4139 *** | −0.4136 *** | −0.4139 *** | −0.2392 *** | −0.2389 *** | −0.2390 *** | −0.6938 *** | −0.6933 *** | −0.6940 *** |

| (−16.58) | (−16.57) | (−16.56) | (−10.24) | (−10.22) | (−10.20) | (−14.22) | (−14.21) | (−14.21) | |

| Cons | 0.0240 | 0.0241 | 0.0250 | −0.007 | −0.008 | −0.0044 | −0.0127 | −0.0124 | −0.0083 |

| (0.63) | (0.63) | (0.66) | (−0.33) | (−0.33) | (−0.18) | (−0.25) | (−0.25) | (−0.16) | |

| Year Control | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Industry Control | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Highest VIF | 1.93 | 1.90 | 1.79 | 1.92 | 1.92 | 1.91 | 1.91 | 1.92 | 1.91 |

| N | 2013 | 2013 | 2013 | 1988 | 1988 | 1988 | 1988 | 1988 | 1988 |

| R-Square | 0.2122 | 0.212 | 0.2109 | 0.5326 | 0.5324 | 0.5302 | 0.2965 | 0.2963 | 0.2955 |

| F Statistic | 11.77 | 11.67 | 11.68 | 50.32 | 50.28 | 49.83 | 18.61 | 18.59 | 18.52 |

| P Value | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shaikh, R.; Fei, G.; Shaique, M.; Nazir, M.R. Control-Enhancing Mechanisms and Earnings Management: Empirical Evidence from Pakistan. J. Risk Financial Manag. 2019, 12, 130. https://doi.org/10.3390/jrfm12030130

Shaikh R, Fei G, Shaique M, Nazir MR. Control-Enhancing Mechanisms and Earnings Management: Empirical Evidence from Pakistan. Journal of Risk and Financial Management. 2019; 12(3):130. https://doi.org/10.3390/jrfm12030130

Chicago/Turabian StyleShaikh, Ruqia, Guo Fei, Muhammad Shaique, and Muhammad Rizwan Nazir. 2019. "Control-Enhancing Mechanisms and Earnings Management: Empirical Evidence from Pakistan" Journal of Risk and Financial Management 12, no. 3: 130. https://doi.org/10.3390/jrfm12030130

APA StyleShaikh, R., Fei, G., Shaique, M., & Nazir, M. R. (2019). Control-Enhancing Mechanisms and Earnings Management: Empirical Evidence from Pakistan. Journal of Risk and Financial Management, 12(3), 130. https://doi.org/10.3390/jrfm12030130