1. Introduction

Cryptocurrency is a digital or virtual currency that is exchanged between peers without the need of a third party. Transactions of the cryptocurrency involve no centralized authority, clearing house, or institution. For example, the first cryptocurrency, Bitcoin, operates with block chain technology, in which a transparent and secure system of accounting is used that transfers ownership. Because cryptocurrencies have exploded in value and the use of cryptocurrencies has increased for various reasons such as investment purposes, cryptocurrency has received growing attention from the media, academia, and the finance industry. Since the inception of Bitcoin in 2009, over 2000 alternative digital currencies have been developed and there have been a number of studies on the analysis of the exchange rates of cryptocurrency.

The early work on cryptocurrencies naturally concentrated on Bitcoin.

Kristoufek (

2013) used vector autoregression (VAR) and vector error correction (VEC) models to search for the relationship between Bitcoin’s price and the interest in Bitcoin represented by Google Trends and Wikipedia search queries, and found that there is the statistically significant bi-directional relationship between Bitcoin and Google Trends, while the relationship between Bitcoin and Wikipedia is not significant. The results also indicate that, if the price of Bitcoin increases, so does the public interest in it pushing the Bitcoin price to increase even more.

Hencic and Gourieroux (

2015) proposed a non-causal autoregressive process with Cauchy errors to predict the exchange rates of the Bitcoin electronic currency against the US Dollar.

Dyhrberg (

2016) applied the generalized autoregressive conditional heteroskedasticity (GARCH) model to examine Bitcoin’s capabilities of being a financial asset and found that it is more characteristic of an asset rather than a currency and it also possesses risk management and hedging capabilities.

Gkillas and Katsiampa (

2018) studied the tail behavior of returns of five major cryptocurrencies (Bitcoin, Bitcoin Cash, Ethereum, Litecoin, and Ripple) using extreme value analysis and estimating Value-at-Risk and Expected Shortfall as tail risk measures. They found that Bitcoin Cash is the riskiest, while Bitcoin and Litecoin are the least risky cryptocurrencies. Meanwhile,

Katsiampa (

2017) compared GARCH-type models to examine which conditional heteroskedasticity model can describe the Bitcoin price volatility better and proposed the AR-CGARCH model to estimate the volatility of Bitcoin.

Despite all these various efforts to analyze the forecasting performances of cryptocurrencies, understanding the relationship among cryptocurrencies is important for investors whose investment portfolios contain a portion of cryptocurrencies as well as for policymakers whose role is to maintain the stability of financial markets.

Bação et al. (

2018) used a VAR modelling approach to investigate transmission between cryptocurrencies and

Corbet et al. (

2018) explored the dynamic relationships between cryptocurrencies and other financial assets.

Katsiampa (

2019) employed an asymmetric Diagonal BEKK model (the acronym comes from synthesized work on multivariate models by Baba, Engle, Kraft and Kroner); studied the volatility dynamics of Bitcoin, Ethereum, Litecoin, Ripple, and Stellar to examine interdependencies within cryptocurrency markets for those five major cryptocurrencies; and found evidence of significant interdependencies in the cryptocurrency market. Given the dramatic Bitcoin price rise in 2016 and 2017 and fadeaway in 2018,

Bouri et al. (

2019a) detected multiple periods of explosivity in cryptocurrencies and investigated whether price explosivity in one cryptocurrency affects the explosivity of other cryptocurrencies using the generalized supremum augmented Dickey–Fuller test of

Phillips et al. (

2015) and the logistic regression. They revealed evidence of co-explosivity and showed the probability of the explosivity in one cryptocurrency generally depends on the presence of explosivity in other cryptocurrencies.

Bouri et al. (

2019b) studied the presence of herd investing behavior in the cryptocurrency market. Results from the static model inspired by the approach of

Chang et al. (

2000) suggest no significant herding. However, with a time-varying rolling-window approach (

Stavroyiannis and Babalos 2017), they found significant herding behavior and showed that the cryptocurrency market is subject to herding behavior that tends to occur as uncertainty increases.

Instead of using aforementioned approaches to examine the association and/or causality between financial time series, using a copula-based approach, however, has several attractive properties and copula models have been widely used to model dependence between financial time series (

Cherubini et al. 2011). Among several references on dynamic dependence using copulas,

Masarotto and Varin (

2012) developed the class of Gaussian copula models for marginal regression analysis of non-normal dependent observations. This class provides a natural extension of traditional linear regression models with normal correlated errors.

Ferrari and Cribari-Neto (

2004) proposed a beta regression model for continuous variables that assumes values in the standard unit interval

as practitioners often encounter bounded time series consisting of rates or proportions in practice, and

Guolo and Varin (

2014) proposed a practical approach to analyze bounded time series through a beta regression model. Using the Gaussian copula marginal regression method by

Masarotto and Varin (

2012) and the beta regression model by

Guolo and Varin (

2014),

Kim and Hwang (

2017) proposed a new copula directional dependence and explored a relationship between two financial time series via the Gaussian copula marginal beta regression model.

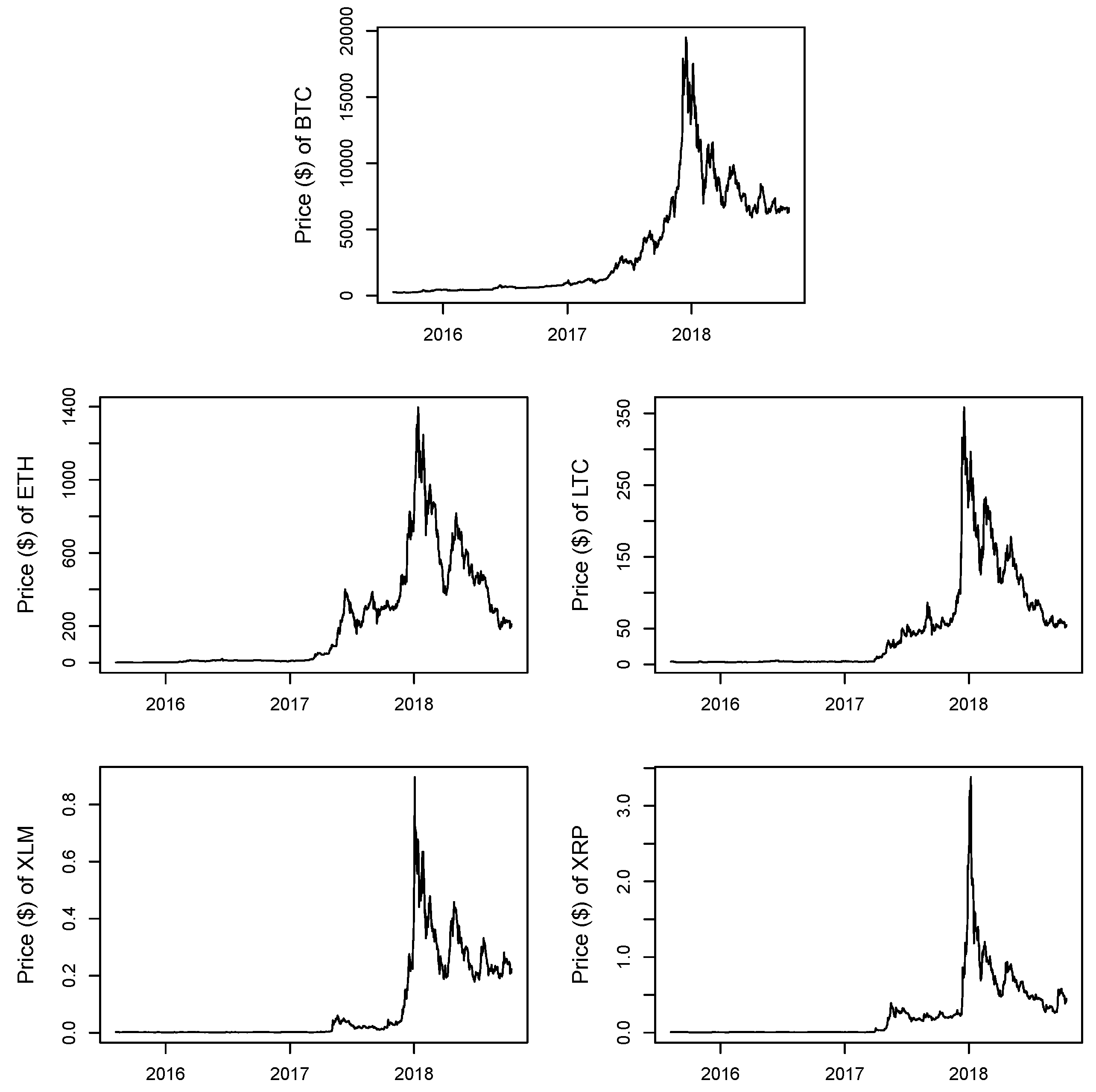

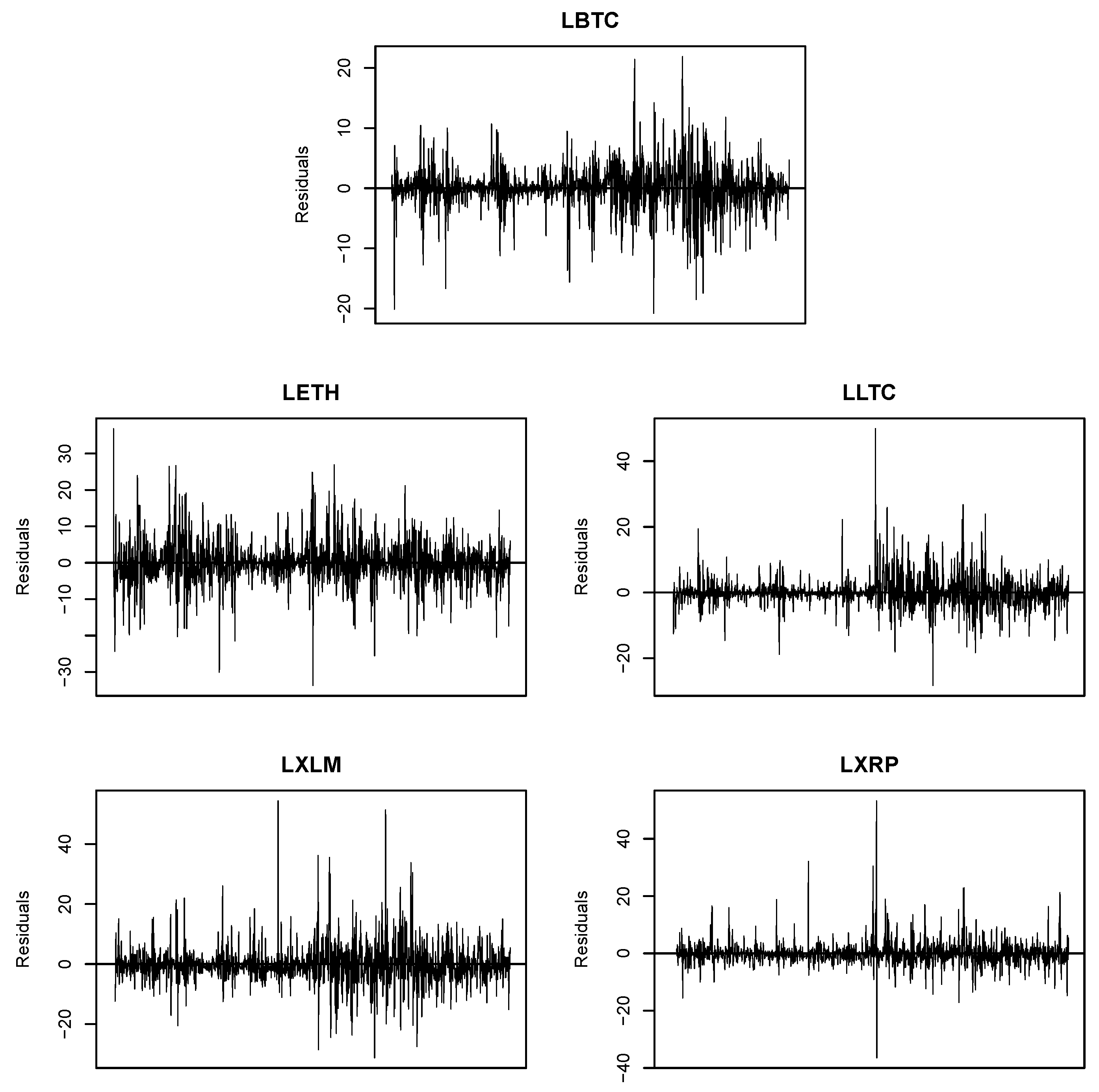

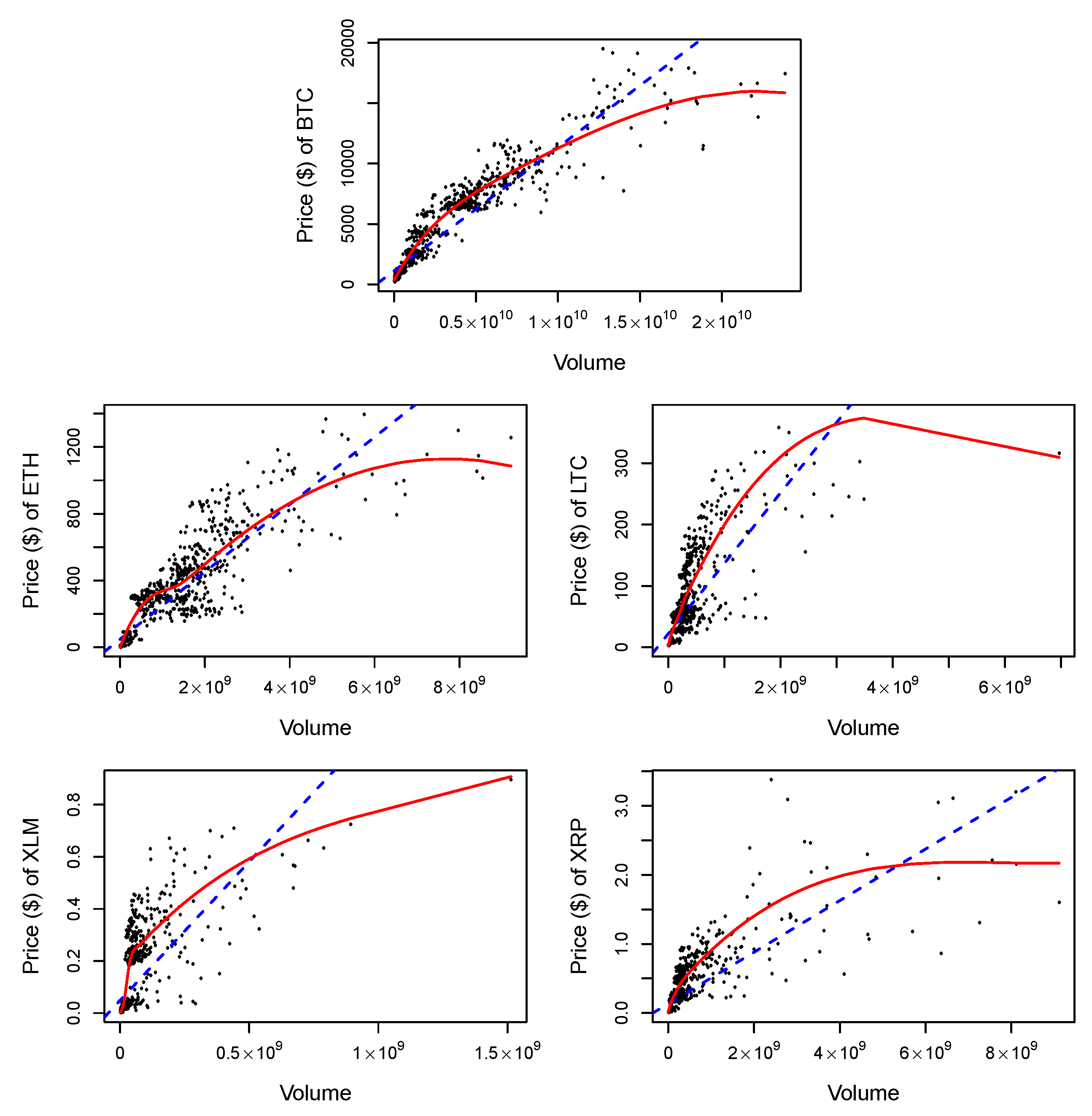

In this paper, we explore directional dependence among the five well-known cryptocurrencies using the Gaussian copula beta regression model and neural networks. First, we apply a neural network autoregression model to the data and generate residuals. Through this procedure we avoid the serial dependence in the component of a cryptocurrency (

Kojadinovic and Yan 2010). Then, the two sets of residuals are transformed to two uniform distributions, and we perform directional dependence via the Gaussian copula marginal beta regression.

Our proposed approach provides several advantages. First, it is common that financial asset returns are generally fat-tailed and have negative skewness and that financial time series volatility is correlated in a non-Gaussian way. In addition, due to the occurrence of extreme observations and the complex structure of the dependence among asset returns, traditional approaches often fail to incorporate the influences of asymmetries in individual distributions and in dependence. By introducing a copular function linking univariate marginals to their multivariate distribution, these issues can be treated properly.

Secondly, our approach allows us to examine the direction of contemporary dependences among return series rather than dynamic dependences and also to obtain the more randomized residuals for the input of our copula model by employing the neural network autoregression model. We can apply GARCH models to generate the marginal distribution of the data. However, we show that the fitting of the GARCH to return series of cryptocurrencies is inferior to the neural network model. The residuals obtained from traditional time series analysis such as GARCH and/or VAR may be contaminated by other explainable portions of the volatility of the return series, but the neural network model allows a great deal of flexibility and complexity in identifying directional dependence for the joint marginal distributions.

Finally, the proposed method is based on the copula regression model using a beta regression, which can effectively and flexibly detect nonlinear relationships. To the best of our knowledge, our paper is the first study to apply this methodological approach to the cryptocurrency data and this paper contributes to the existing literature by investigating the directional connections between major cryptocurrencies.

The remainder of this paper is organized as follows.

Section 2 describes the neural network autoregression model, directional dependence by copula, and Gaussian copula marginal beta regression. In

Section 3, we illustrate the proposed method on the five cryptocurrencies.

Section 4 concludes the paper with some discussions.

4. Discussion

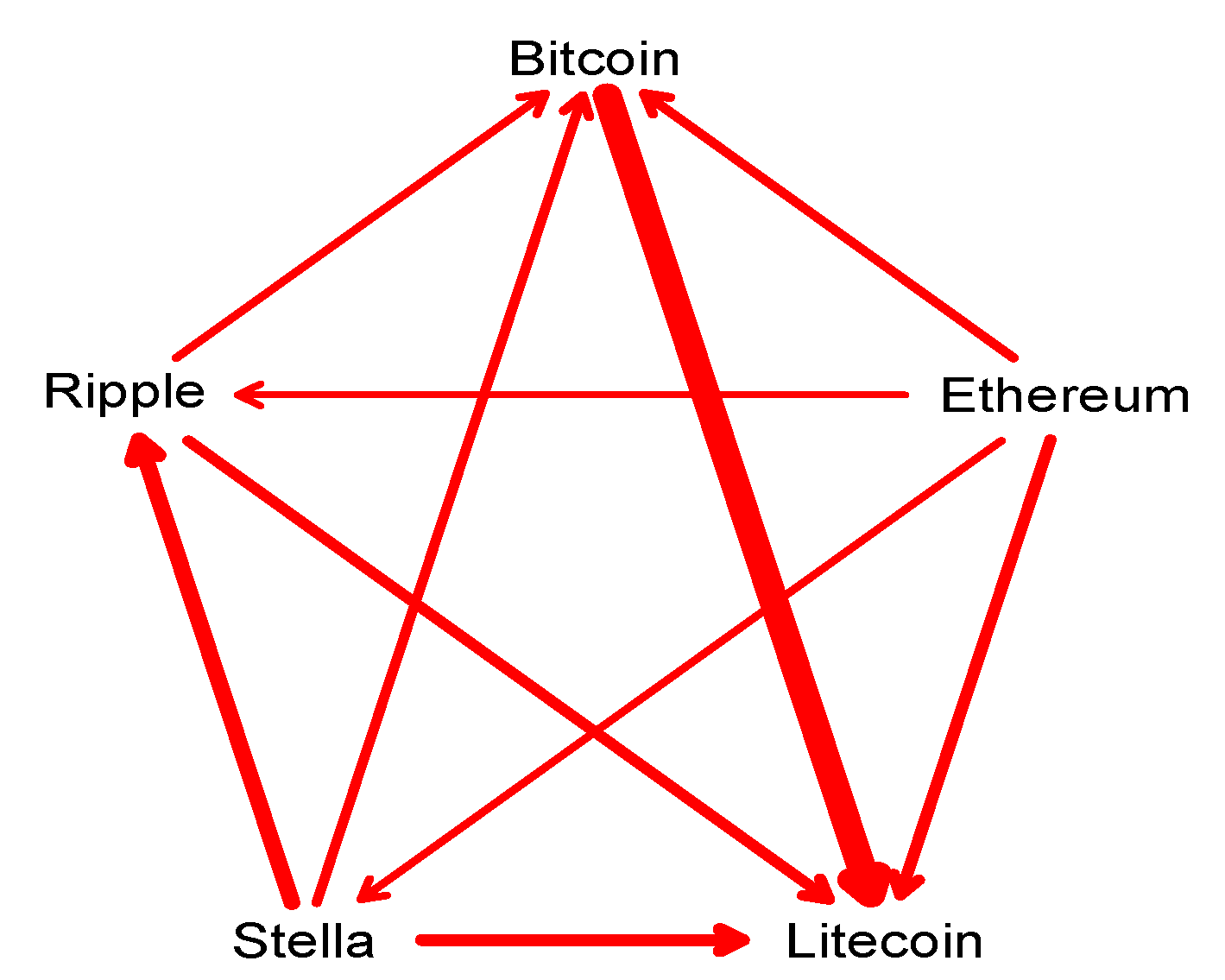

Understanding the dependence structures among cryptocurrencies is important to both investors and policymakers. In this paper, we discuss the directional dependency of five cryptocurrencies by using the bivariate Gaussian copula beta regression with the neural network model for marginal distribution. To the best of our knowledge, our paper is the first study to analyze directional dependence among cryptocurrencies using neural networks autoregression and copular regression models. We argue that the proposed methods allow us to deal with problems by violations of traditional model assumptions in financial data analysis and are even superior to other remedies introduced in the literature. Using the daily log-returns, the major finding of our analysis is that, overall, directional dependence among the five cryptocurrencies exists and the return shocks of Bitcoin have the most effect on Litecoin. In addition, Stellar has relatively stronger impact on Ripple and the return shocks of Ethereum relatively influence the shocks of the other four cryptocurrencies instead of being influenced by them. This finding is somewhat opposed to the public perception that Bitcoin has consistently been leading and influencing all other cryptocurrencies (per se Altcoins) including Ethereum. Based on what we found, however, at least during our sample period, Ethereum has more influence on the other four cryptocurrencies rather than being impacted by them.

In recent literature,

Ziȩba et al. (

2019) examined interdependencies between log-returns of cryptocurrencies applying the two-step analysis, minimum spanning tree method and vector autoregression model. They found that, despite Bitcoin’s dominance in the market, changes in Bitcoin price do not affect and are not affected by changes in prices of other cryptocurrencies. The most influential ones are Litecoin and Dogecoin. They, however, indicate that findings obtained for Bitcoin shall not be generalized to the entire cryptocurrency market.

Ji et al. (

2019) studied a set of measures developed by

Diebold and Yilmaz (

2012,

2016) to examine returns-connectedness and volatility-connectedness networks among six large cryptocurrencies. The results show that Litecoin plays a central role of return and volatility connectedness instead of the largest cryptocurrency, Bitcoin. They suggested that this finding is evidence that the dominance of Bitcoin in the cryptocurrency market has been weakened.

Bouri et al. (

2019c) also examined the linkages among the volatility surprises of eight large cryptocurrencies (Bitcoin, Ethereum, Litecoin, Ripple, Stellar, Monero, Nem, and Dash) via the Granger-causality in the frequency-domain of

Breitung and Candelon (

2006). They showed that Bitcoin does not necessarily cause volatility surprises of the other cryptocurrencies and some cryptocurrencies (Stellar and Dash) show relatively independent price volatility.

These findings go along with our results where the Bitcoin has weakened its dominance in the crypto world and the market structure has been evolved rapidly. Some results, however, do not concord with our findings in part. One plausible explanation is that this could come from either still not sufficient knowledge on cryptocurrencies or different statistical procedures and analytical methods. It would be worthwhile to compare our findings from these studies. We claim, however, that these contradictory results also address the dynamic market structure in the cryptocurrency market. These areas will be addressed in future phases of this project.

Cryptocurrencies are still new to the public but have gradually captured its attention. The techniques we use in the paper may prove useful to others interested in examining the dependence relationships among cryptocurrencies. Our findings can assist crypto-investors by providing the directional dependence among major cryptocurrencies. This allows the investors to build the market-timing strategies by observing the directional flow of return shocks among cryptocurrencies. In addition, by addressing how significantly the return shock of one cryptocurrency influences one another, investors may improve their portfolio diversification.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}