1. Introduction

The recent global financial crisis led to significant losses due to a slowdown in the economy but also prompted a debate between several influential research scholars, such as Robert Shiller who could not resist criticizing the conventional financial systems. In this respect,

Kroszner and Shiller (

2011) invited regulators and policymakers to bring about improvements in the U.S. financial system and enrich its robustness with the acknowledgment of the human and democratic factors in finance. This debate has opened the floor for the alternative forms of finance that entail more reasonable risks than traditional conventional finance. Meanwhile, Islamic finance is considered to serve as an alternative that better implements the UN’s sustainable goals to create an impartial financing system and affect society positively (

Ahmed et al. 2015;

Paltrinieri et al. 2020). The Islamic finance industry has experienced tremendous growth over the last decade (

Shahzad et al. 2017). This growth keeps continuing with the development of the core Islamic financial markets, the wider consensus on the necessity of the standardized legal structures and the Shariah interpretation (

Ahmed 2019). Particularly, in the year 2018, Islamic assets grew to reach

$2.19 trillion (gross value) with an overall growth rate of 6.9%. Among them, the Islamic capital markets demonstrated higher growth by 27%, whereas the Islamic banking sector shrank by 4% (

IFSISR 2019). The developments in Islamic and conventional banking sectors and the associated risks are already highlighted by several studies

1. Therefore, the focus of this paper is limited to these fast-growing capital markets (i.e., equity markets).

The theoretical studies claim that the Islamic financial system is superior to the conventional financial system due to its participatory mode of financing or pure equity financing (

El-Karanshawy et al. 2015). Moreover, the Islamic equity markets move or co-move in dissimilar directions to their conventional counterparts (

Walid Mensi et al. 2015;

Masih et al. 2018). As a consequence, soon after the Global Financial Crisis of 2007 (GFC hereafter), the fast-growing literature has started to primarily assess the performance of the Islamic and conventional stock market indices (

Ibrahim 2015). Subsequently, the higher focus turned towards the identification of diversification opportunities between the two markets. In doing so, the performance of the Islamic stocks with their conventional counterparts is being justified with the help of Markowitz Portfolio Theory (MPT) (

Markowitz 1952). The theory that argues an optimal portfolio can be achieved by maximizing the utility function of investors, which can ultimately be realized through diversification. Since the investors show concern towards the risk-return profile of their portfolio, therefore, rather than only focusing on the Muslim investor’s perspective, the non-Muslim investor’s perspective is also kept under consideration. Similarly, global investors also focused on Islamic stock markets due to their resilient nature to crises and better-positioned markets that may have resulted due to their unique features i.e., ratio screening, ethical investing, low tolerance towards interest-based leverage and restricting intensively structured based financial products such as derivatives (

Saiti et al. 2014).

The researchers have addressed the performance-related issues and came up with mixed results based on both Muslim and non-Muslim investors’ perspectives

2. However, the conflicting views regarding the decoupling and recoupling of Islamic stocks with their conventional counterparts emphasize the need to scrutinize whether the former provides higher and the latter provides lower diversification benefits or not. Keeping in view the most commonly raised criticism that Islamic stocks are considered as providers of low diversification benefits, several researchers came up with mixed results. For instance, scholars suggested that Islamic stocks are either decoupled based on the characteristics they possess (

Rizvi and Arshad 2014;

Majdoub and Mansour 2014;

Mensi et al. 2015;

Kenourgios et al. 2016) or recoupled based on their similarity or by being a part of the conventional stocks (

Masih et al. 2018;

Hammoudeh et al. 2014;

Dewandaru et al. 2014;

Ajmi et al. 2014;

Yilmaz et al. 2015;

Dewandaru et al. 2016;

Grinsted et al. 2004;

Majdoub et al. 2016;

Aloui et al. 2016;

Mensi et al. 2017) in providing higher and lower diversification benefits, respectively. Similarly, another view or criticism that is linked to the issue of the decoupling or recoupling of Islamic and conventional stocks is of greater importance when it comes to the behavior of the Islamic stocks in response to turbulent periods. For instance, based on the characteristics of Islamic stocks, these Islamic stocks are said to be less volatile, less risky and safe-haven stocks. But controversies do exist when it comes to the recoupling hypothesis indicating that Islamic and conventional stocks behave in the same way during crisis periods and indicate the contagion effect (

Rizvi and Arshad 2014;

Kenourgios et al. 2016;

Mensi et al. 2017;

Nazlioglu et al. 2015;

Ftiti et al. 2015;

el Alaoui et al. 2015). However, some of the recent studies such as Ho et al., Narayan and Bannigidadmath (

Ho and Odhiambo 2014;

Narayan and Bannigidadmath 2017) argue that during the global financial crisis, the Islamic stocks were found to be more profitable than the conventional stocks. Thus, the Islamic stocks were found to be decoupled from their conventional counterparts due to their safe-haven/hedge ability (

Mensi et al. 2015;

Hkiri et al. 2017;

Azad et al. 2018). This suggests that investors could diversify their risks by investing in Islamic stocks, particularly during financial and economic downturns. However, the literature provides inconclusive results regarding the decoupling or safe-haven and the integration or contagion effects between Islamic and conventional stock markets. Thus, the above-discussed reasons are the major source of motivation for this study to sort out the challenges and controversies related to the Islamic-conventional equity market’s link.

Recently, the assessment of the Islamic-conventional equity market’s link has grown to become a well-defined focus (

Narayan and Phan 2017). The existing empirical studies have concentrated highly on the aggregate-level (global and regional indices) Islamic-conventional nexus, whereas few studies with a limited focus are found on the disaggregate-level (country-level) analysis. For instance,

Ajmi et al. (

2014) have employed only two regions, and one developed market,

Naseri and Masih (

2014) employed only two developed and two emerging economies’ Islamic stock indices,

Majdoub and Mansour (

2014) employed five emerging markets and one developed market,

Shahzad et al. (

2017) employed three developed markets,

Hkiri et al. (

2017) employed the world at large, two regions and four developed countries,

Uddin et al. (

2018) employed a set of two developed and a few emerging markets,

Ahmed and Elsayed (

2019) employed only one emerging market and

Usman et al. (

2019) employed three developed and two emerging markets. Therefore, this study differentiates its data sample from the above highlighted recent studies by including the maximum number of developed and emerging countries from the Asia Pacific, Europe, Africa and Americas regions. The purpose is to provide more generalized and comprehensive results regarding each advanced and emerging country’s Islamic and conventional equity markets correlation. In doing so, unlike prior research in this field, this study has identified several developed (Hong Kong, New Zealand, Ireland, Denmark and Spain) and emerging (China, Czech Republic, Argentina and Peru) countries whose Islamic equity markets are decoupled from their conventional counterparts and those provide diversification benefits during crisis and non-crisis periods. Therefore, based on these results of this study, the importance of our extended sample can be highlighted, as none of the past studies have investigated this phenomenon for these markets (except for China) and identified these new markets as the providers of the diversification benefits.

Similarly, to draw a comparative view of the two equity markets, the focus of the financial econometrics is turned towards modeling the volatility and correlations of the alternative assets

3. In doing so, recent studies have applied different approaches to consider either the correlation or volatility factor for examining the association or the decoupling hypothesis between Islamic and conventional equity markets. For instance, focusing on the correlation factor,

Uddin et al. (

2018) applied the wavelet squared coherence, and for the case of volatility factor,

Ahmed and Elsayed (

2019) applied the forecast error variance decompositions method to examine the decoupling hypothesis. Unlike the methods employed in the two aforementioned studies, this paper differentiates itself by focusing on the correlation as well as the volatility factors by applying the wavelet and the ADCC-GARCH based approaches, respectively.

Therefore, the threefold contribution of this paper is summarized as follows; first, this paper aims to be the first of its nature that attempts to generalize the results regarding the dynamics of decoupling or recoupling hypotheses and the safe-haven or contagion effect between the Islamic and the conventional stock markets. However, in perusing this issue of weakly positive (decoupling) or strongly positive (recoupling) dependence of Islamic and conventional stocks, this paper explores the Islamic-conventional stock returns dependence based on the time-frequency (wavelet) and the time-domain (ADCC-GARCH) based correlations. Second, to examine the features of the Islamic-conventional stock return correlations in the form of evolving correlations and common trends, this paper compares the patterns of differing multi-horizons (short, medium and long-term) wavelet-based stock return correlations with the asymmetric dynamic conditional stock returns correlations. Finally, this paper contributes to this field of knowledge by investigating the Islamic-conventional stock returns correlation (either decoupling or integration) in both crisis and non-crisis periods.

The rest part of this paper is ordered as follows.

Section 2 discusses the data and methodological approaches.

Section 3 reports the results.

Section 4 provides the discussion and

Section 5 concludes the paper.

4. Discussion

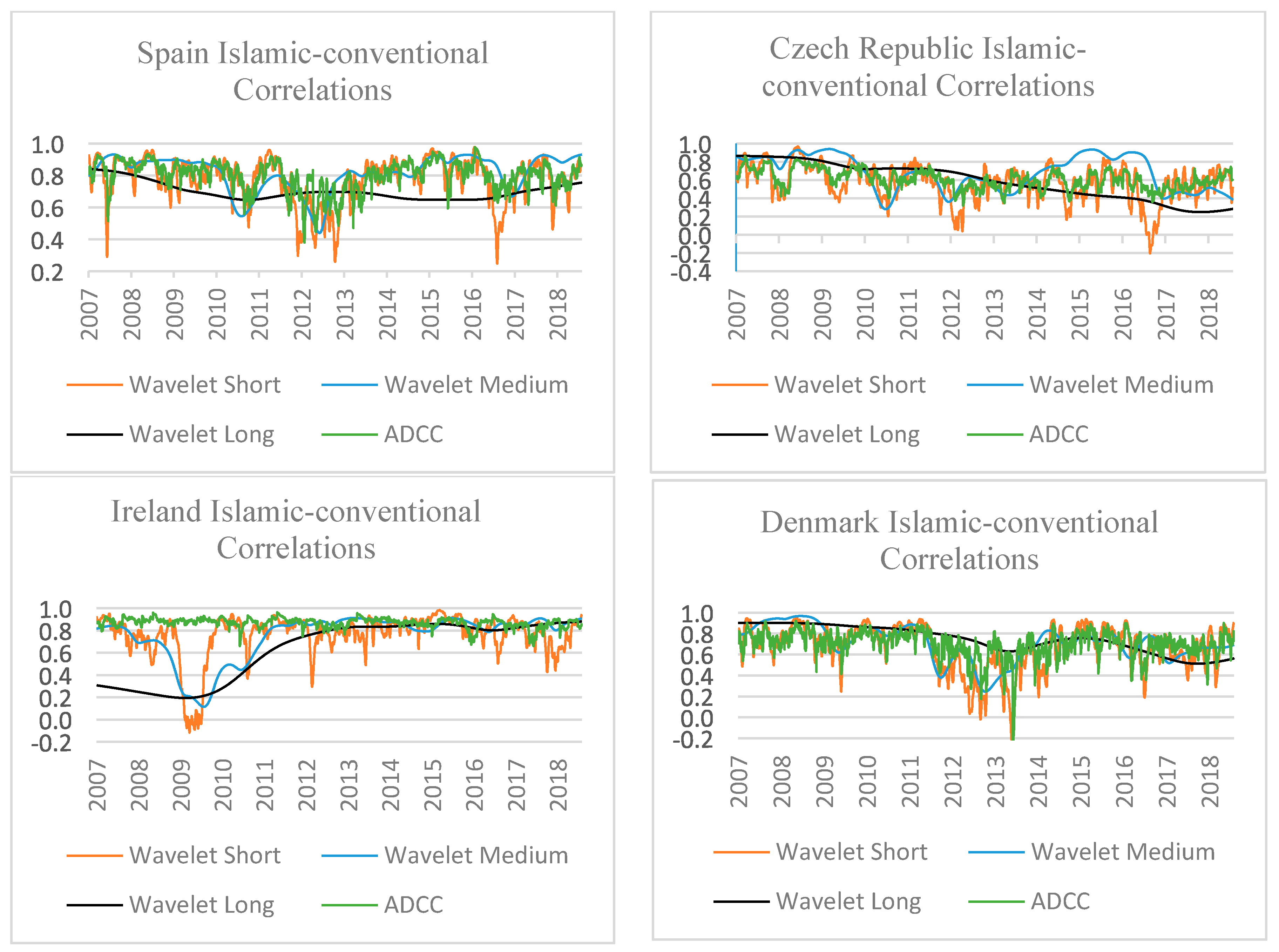

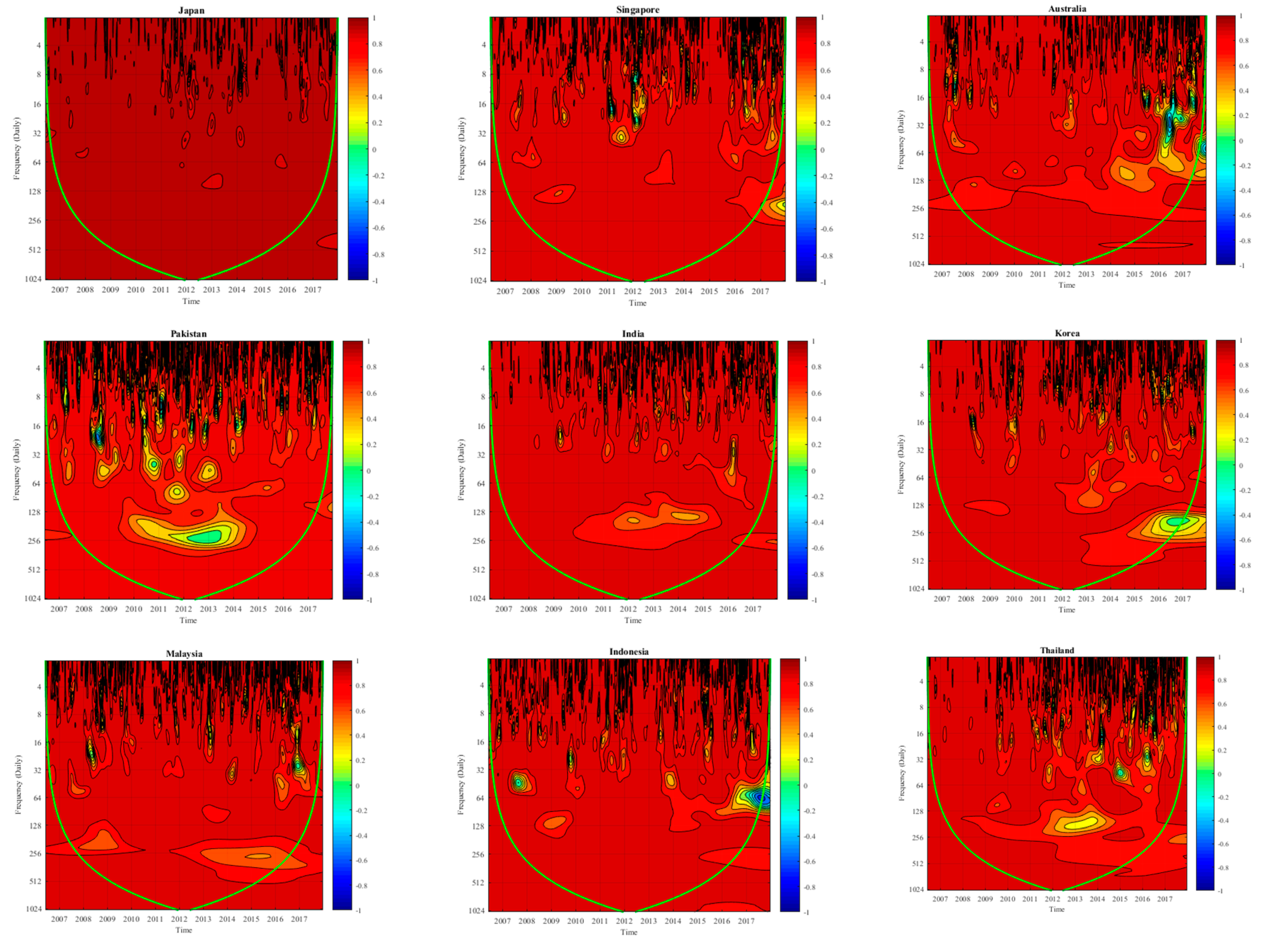

In this section, the findings and detailed discussion regarding the evidence of decoupling or integration for region-wise developed and emerging markets as well as the contagion or safe-haven phenomenon are provided. For the developed countries’ time-frequency analysis, the rejection of decoupling hypothesis or the evidence of integration was found for almost all major developed markets (e.g., the US, UK, Japan, Canada, etc.) with a few exceptions (e.g., Hong Kong, New Zealand, Ireland, Denmark and Spain). However, for these few developed markets, the decoupling hypothesis was predominantly rejected at both short- and long-term horizons but differentiating results are observed only at the medium-term horizon. For instance, the evidence of weak (low positive) correlation was found only for five developed market equity indices return pairs such as Hong Kong, New Zealand, Ireland, Denmark and Spain, as those markets have depicted temporarily low positive Islamic-conventional stock return correlations at medium-term horizons. The reason behind this weak positive correlation (decoupling) can possibly be a consequence of the improving performance of the constituents of an Islamic (Shariah-compliant) stock index generally, rather than only the greater differential exposure to a specific sector or the exclusion of a major proportion of financials. For these five developed markets (Hong Kong, New Zealand, Ireland, Denmark and Spain), we did not find consistent or inconsistent results from the past studies, as none of the studies has investigated this phenomenon for these markets.

However, consistent and inconsistent results from several past studies were found regarding our evidence of integration between the selected developed Islamic and conventional equity markets (e.g., US, UK, Japan, Canada, etc.). Although this study has applied different methodologies than the past studies, some of the findings of this study are supported with the findings of those studies such as

el Alaoui et al. (

2015) who provided the evidence of integration between the US Islamic and conventional equity markets by applying the wavelet squared coherence and asymmetric-based causality methodologies and

Majdoub et al. (

2016) who applied cointegration and ADCC-GARCH models and found integration between Islamic and conventional equity markets of the US and UK. Similarly,

Shahzad et al. (

2017) applied a forecast error variance decomposition technique and provided evidence of integration between Islamic and conventional equity markets of the US, UK and Japan. Though contrasting results are also provided by some of the past studies, those do not support the findings of this study such as Majdoub and Mansour, who (

Majdoub and Mansour 2014) applied the GARCH-BEKK, CCC and DCC models and did not find evidence of integration between the US Islamic and conventional equity markets as well as

Kenourgios et al. (

2016) who applied the A-DCC model and found the decoupling of the US, UK and Japan’s Islamic equity markets from their conventional counterparts. Similarly,

El Mehdi and Mghaieth (

2017) as well as Trabelsi and

Naifar (

2017) applied the DCC-FIAPARCH and the CoVaR models, respectively, and they also did not find evidence of integration between the Islamic and conventional equity markets of the US and UK. Thus, for 16 out of 21 developed markets, the results of this study indicate high positive correlations between the Islamic equity prices and the corresponding conventional ones, which means that the majority of the developed market’s Islamic equity markets are highly dependent on their conventional counterparts, they behave in the same way and do not provide diversification benefits. However, for 5 out of 21 developed markets, the results of this study indicate weak positive correlations, meaning very few developed markets’ Islamic equity markets show different behavior or dependency from their conventional counterparts and provide diversification benefits to investors. However, one of the reasons for the weak correlation or the rejection of the decoupling hypothesis can be the contingency among the capital markets and their regional trade partnerships.

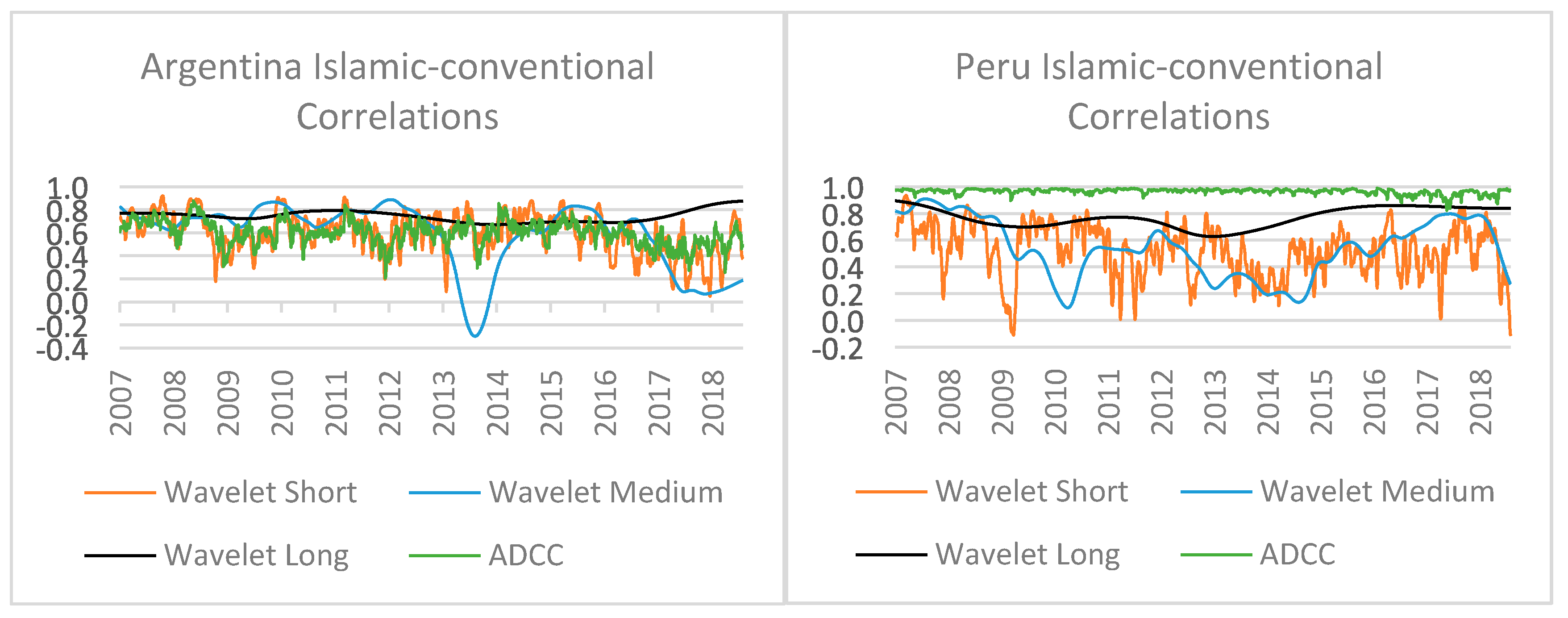

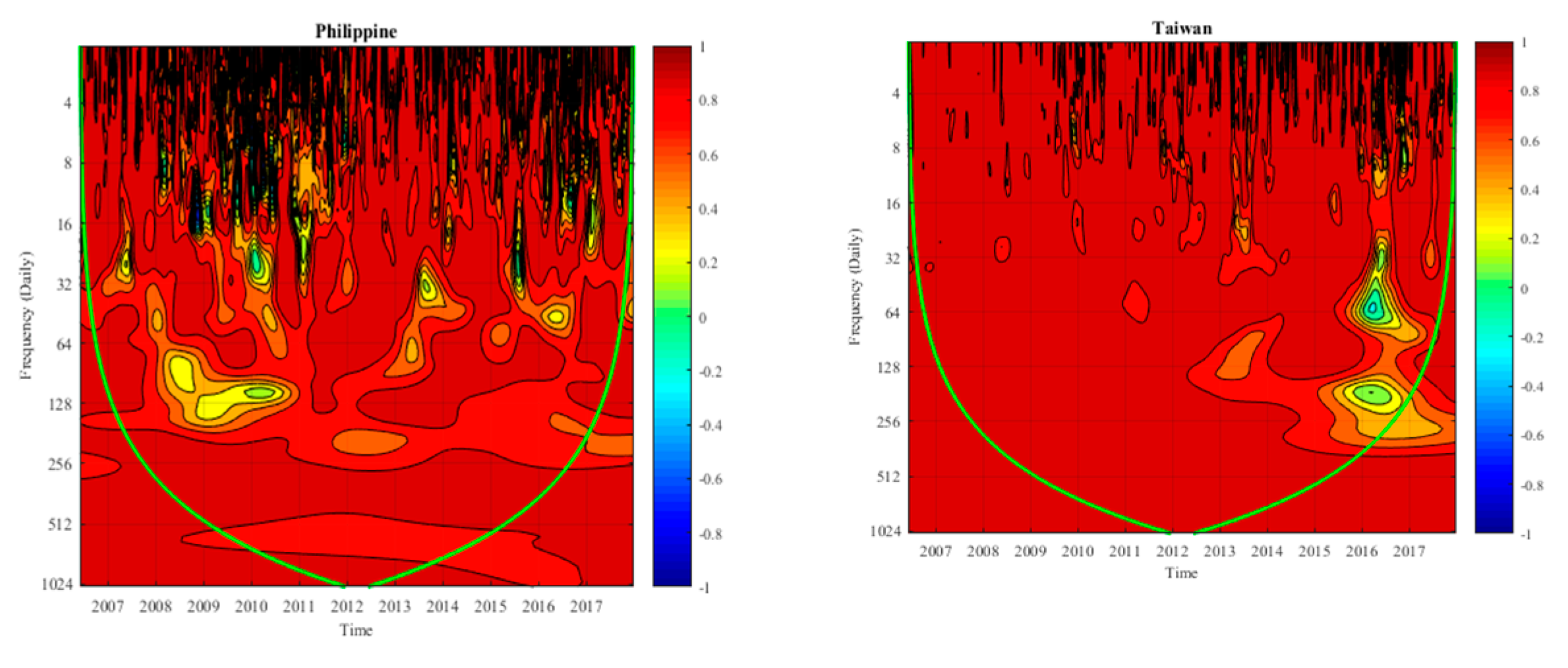

Similar to developed markets, the rejection of decoupling hypothesis or the evidence of integration is also found for almost all major emerging markets (e.g., Pakistan, India, Malaysia, Russia, Turkey, etc.) though not for a few ones (e.g., China, the Czech Republic, Argentina and Peru). Though, for these few emerging markets, the decoupling hypothesis is also predominantly rejected at both short- and long-term horizons, whereas differentiating results were observed only at the medium-term horizon. For instance, the evidence of weak (low positive) correlation is found only for four emerging equity indices returns pairs such as China, the Czech Republic, Argentina, and Peru, as those markets depicted temporarily low positive Islamic-conventional correlations at medium-term horizons. Again, we did not find consistent or inconsistent results regarding the decoupling hypothesis that are evident for the four emerging markets (China, Czech Republic, Argentina and Peru) except for the China market. Therefore, the findings of this study are supported by some of the past studies, such as

Kenourgios et al. (

2016) who applied the A-DCC model and provided evidence in favor of the decoupling hypothesis for China.

However, the consistent and inconsistent results from several past studies are found regarding our evidence of integration between the selected emerging market’s Islamic and conventional equity markets (e.g., Pakistan, India, Malaysia, Russia, Turkey, etc.). For instance, the findings of this study are consistent with the studies that provided evidence of integration such as

Majdoub and Mansour (

2014) that applied the GARCH BEKK, CCC and DCC models and provided evidence of integration between the Islamic and conventional equity markets for Malaysia, Pakistan and Turkey, while

Krasicka and Nowak (

2012) also supported the evidence of integration for Malaysia. However, the findings of this study are inconsistent to those studies that applied the A-DCC model and found the decoupling effect between Islamic and conventional or equity markets of India and Russia (

Kenourgios et al. 2016). Finally, the overall results of this study for developed and emerging countries (except for Hong Kong, New Zealand, Ireland, Denmark, Spain, Argentina and Peru) are consistent with

Walkshäusl and Lobe (

2012) who applied the time-series factor regression technique and did not find any difference in the performances of both developed and emerging markets Islamic-conventional indices. Therefore, we would acknowledge the fact that the majority of the market’s Islamic equity markets show indifferent behavior from their conventional counterparts and that can be due to a faulty Shariah screening process which can be improved or there may be some economic or financial indicators that may lead the other markets to behave indifferently.

By focusing on the crisis periods, 8 out of the 41 markets (developed and emerging) Islamic stocks can be seen to serve as safe-havens during periods of financial turmoil (GFC and ESDC). For instance, during the GFC period, one developed (Ireland) and three emerging markets (China, Argentina and Peru) were safe-havens, whereas during the ESDC, three developed (the Hong Kong, New Zealand, and Denmark) and two emerging markets (the Czech Republic, and Peru) Islamic stocks serve as safe-havens. However, the reason for this safe-haven ability of Islamic stocks can be that none of the Islamic financial institutions have failed during and after GFC, since they (e.g., Islamic banks) are not allowed to invest or finance the instruments (e.g., derivatives and toxic assets) that may have badly affected their conventional counterparts and stimulated the GFC (

Hasan and Dridi 2011). Moreover, the Islamic and conventional equity markets portray similar behavior that usually diverges during the crisis periods, therefore, the Islamic equity markets of developed and emerging markets serve as safe-havens and hedges during those periods (

Saâdaoui et al. 2017). These findings regarding a market’s Islamic stocks have some implications such as during periods of financial turmoil, if investors with their short-term intraday or medium-term investments find Islamic stocks to serve as safe-havens, then they may switch their investments to these Islamic stocks and try to minimize their losses. This finding is supportive of the argument that for conventional investors, the Islamic stocks are favorable to achieve short-term profitability and obtain risk diversification benefits (

Umar 2017), and that Islamic stocks provide a cushion from a crisis (

Jawadi et al. 2014;

Dewandaru et al. 2014). Therefore, both Islamic (faith-based) and conventional investors can switch their investments to Islamic stocks and minimize the losses resulting from a systemic crisis. This argument is also supported by

Jawadi et al. (

2014) that the Muslim (faith-based) and Non-Muslim (religiously neutral) investors can invest in Islamic stocks during a normal period but to protect their investments in crisis periods, they can incline more towards Islamic stocks.

Finally, for the majority made up of 33 out of 41 markets (developed and emerging), the results of this study indicated a contagion effect between their Islamic and conventional equity indices which mean that the majority of the developed and emerging markets’ Islamic equity markets show indifferent behavior from their conventional counterparts, particularly during crisis periods. This evidence is supported by

Azad et al. (

2018) who applied quantile regressions and did not find evidence of the safe-haven ability of developed (US, UK, Japan) and emerging (India along with other four countries except for China) countries’ Islamic indices, nor any diversification benefits to investors during crisis periods. Therefore, the overall results of this study for region-wise developed and developing country pairs (except for Hong Kong, New Zealand, Ireland, Denmark, Argentina and Peru) are consistent with the argument built by

Ajmi et al. (

2014) that Islamic equity markets cannot act to hedge against risky movements in conventional equity markets, particularly during periods of financial turmoil. The reason behind this non-ability of Islamic stocks to act as diversifiers or hedges is that the whole financial system including Islamic and conventional equity markets are directly or indirectly affected by global common shocks as well as contagion risks during periods of financial turbulence. Thus, during crisis periods, investors can transfer their investments to other safe-haven assets (e.g., bond and commodities like gold) to hedge their invested funds against the severe exposure of equity markets to the crises (

Baur and Lucey 2010;

Baur and McDermott 2010).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}