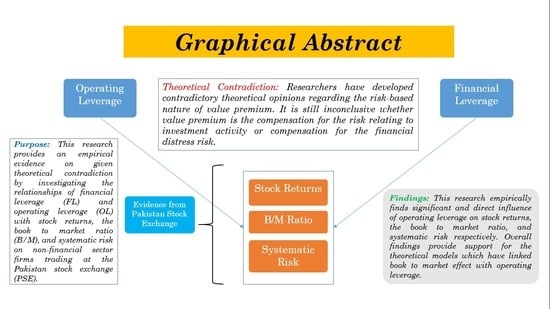

4.2. Multivariate Regression Analysis

In a panel regression analysis, firstly we estimate an empirical model for examining the relationship of stock returns with DOL, DFL, systematic risk (β), and size (ME) by controlling sale growth (SG), P/E ratio, and EPS. The estimates obtained on stock return regressions are reported in

Table 4, where coefficients and t-statistics indicate direction and strength of the estimates. Results reported in the first column of

Table 4, reveal that DOL is found directly influencing stock returns at 5% significant level. Firm size (ME) and systematic risk (β) are also found positively associated with stock returns at 1% and 10% levels of significance, respectively, while DFL is found insignificantly influencing stock returns. These findings provide support to the theoretical models which suggest a positive association of operating leverage with stock returns. In addition to this, these findings also provide support to the theoretical association of beta with stock returns. Similarly, our findings are also consistent with the existing empirical literature, which state that beta is not the only variable influencing stock returns, as coefficients of DOL and size (ME) are also found positive and significant. We also verify our results by estimating same regression model using alternate variable measurement for dependent, which is average monthly stock returns (R01). Estimates reported in the third column of

Table 4, show that DOL is again found directly influencing stock returns at 5% significance level. Similarly, firm size (ME) is also found to have positive influence on stock returns at 1% significance level. On the other hand, results again show that DFL is not significantly related with stock returns.

Furthermore, we also test robustness using alternative proxies of major explanatory variables that are both financial and operating leverages. Stock return models are estimated again incorporating point-to-point measures (lnDOL01 and lnDFL01) of operating and financial leverages. The results of these alternative variable regressions are given in second and fourth columns of

Table 4. First of all, annual stock returns (R) are regressed on alternative proxies DOL01 and DFL01 along with other independent variables; in this structure, coefficient of DOL01 is found positive and highly significant (1% level) whereas systematic risk (β) and size (ME) are found positively related with stock returns at 10% level of significance. However, DFL01 is again found insignificantly negatively influencing stock returns. In the last, alternative measurements of both explained and explanatory variables are also used in the same model where average monthly stock returns (R01) are regressed on alternative proxies of operating and financial leverages (DOL01 and DFL01) along with other independent variables. In this structure, we found more significant effects;: firstly, DOL01 and firm size (ME) are found directly affecting stock returns at 1% significance level; secondly, systematic risk (β) is also found to have significant direct influence on stock returns at 5%. On the other hand, this time DFL01 is also found inversely related with individual stock returns at 10% level. Drawing on our results, the positive effect of beta provides support to the Sharpe’s CAPM which states that beta positively affects stock returns but our results also prove that beta is not the only variable influencing stock returns. The negative relationship of DFL is consistent with the results of

Mandelker and Rhee (

1984) which state that DFL and DOL have a tradeoff relationship related with firm’s systematic risk; this negative relation can lead to negative relationship of DFL with stock returns. More specifically, this negative relation of DFL with stock returns is also consistent with results of

Melicher (

1974), which state that DFL has negative relationship with firms’ stock returns and market risk.

Considering results from the first model, we report that DOL has a significant and direct determining impact on stock returns while DFL is inversely associated with stock returns; however, the significance of DFL is not persistent. We also report that systematic risk (β) and firm size (ME) are also found significantly predicting stock returns. The relationship of firm’s size is consistent with

Fama and French (

1992), who report size of the firm and B/M ratio as significantly predicting stock returns. Empirical results from this section are consistent with the existing findings of

García-Feijóo and Jorgensen (

2010). In addition to this, our findings also provide support to theoretical views (

Carlson et al. 2004;

Cooper 2006;

Zhang 2005;

Berk et al. 1999) which state that value premium is the reward for risk relating to investment activity (operating leverage). It means that firms with higher B/M ratios experience higher returns because these face higher systematic risk due to higher levels of operating leverage, thus suggesting direct association of operating leverage and stock returns.

Furthermore, a second empirical model is also estimated applying OLS technique, in which the B/M ratio is regressed on DOL and DFL with the aim to analyze the impact of both leverages (DOL and DFL) on the B/M ratio. Findings are reported below in

Table 5, which clearly reveal that DOL is directly related to the B/M ratio, while DFL is inversely related with B/M ratio at 5% level of significance. For robustness, we also use alternative point-to-point measures of both DFL and DOL in this model. Findings reported in second column of

Table 5, reveal that DOL01 is positively related with B/M ratio at 5% significance level, while DFL01 is found to have negative and insignificant relationship. These findings also provide support to the theoretical notion that the B/M effect is linked with the DOL. Contrarily, the negative coefficient of DFL is consistent with the results of our main B/M ratio model given above, hence, proving that value effect is not the compensation of financial risk. This negative relationship of DFL with the B/M ratio also inversely affects stock returns, consistent with the findings of

Melicher (

1974). Drawing on findings from this model, we report that DOL has direct association with B/M ratio while DFL is found to have an inverse relationship with the B/M ratio. These results also provide support to the findings from previous literature (

García-Feijóo and Jorgensen 2010;

Gulen et al. 2011). Additionally, these also support recent theoretical notions (

Carlson et al. 2004;

Cooper 2006;

Zhang 2005;

Berk et al. 1999), which state that value premium basically compensates for risk of investment activity (operating leverage), thus suggesting positive association of operating leverage with B/M ratio.

At last, we also estimate the portfolio regression mode using the OLS technique on the basis of panel unit root testing. In this model systematic risks of portfolios are regressed on DOL and DFL of portfolios separately by controlling the size of portfolios. Results of this model are reported in

Table 6; here again we find evidence in favor of risk relating to investment activity, and it is revealed that variable

has a positive relationship with systematic risk of respective portfolios

at 1% significance level, while

is found to have negative and insignificant relationship with systematic risk of portfolios

So once again, results are consistent with the findings of

García-Feijóo and Jorgensen (

2010). Therefore, we report that operating leverage has a direct influence on systematic risk (β). This direct relation of DOL is also supported by the existing empirical studies (

Darrat and Mukherjee 1995;

Ho et al. 2004;

Huffman 1983;

Li and Henderson 1991;

Lord 1996;

Mandelker and Rhee 1984). On the other hand, the insignificant relationship of DFL with systematic risk is also consistent with a line of existing literature (

Lord 1996;

Darrat and Mukherjee 1995) which states that DFL has no relationship with systematic risk. In short, these results provide support to the recent theoretical opinion (

Carlson et al. 2004;

Cooper 2006;

Zhang 2005;

Berk et al. 1999), which suggest a positive relationship of DOL with systematic risk.

Overall results of all three empirical models reveal that operating leverage has a significant and direct relationship with stock returns, B/M ratio and market risk, respectively, whereas financial leverage is found to have an inconsistent association with all three. Drawing from these results, we accept our first hypothesis which states that operating leverage causes value premium. On the contrary, we observe no evidence in support of our second hypothesis, which states that financial leverage determines value premium. Consequently, our research reports that operating leverage derives value premium and provides support to the theoretical opinion that value premium compensates for the risk relating to the investment activity. According to this opinion, investment decisions are normally evaluated on the basis of real options, and options exercised can cause multiple variations in the firm’s risk. For instance, if growth opportunities are limited, growth option to asset ratio changes as investment decision changes. In addition to this, it also results in increasing the physical capital which in turn increases the operating leverage through long term obligations such as commitments to suppliers, wage contracts, and fixed costs. Hence, it leads to the idea that high B/M firms face higher levels of risk due to investment decisions, thus these firms earn higher returns compared to their low B/M counterparts. In short, this research provides support to the theoretical argument that high B/M firms face higher risk due to higher levels of DOL, and that is why these firms earn higher stock returns. Whereas, we do not observe evidence in support of the argument which relates financial distress risk with value effect. Finally, this research also finds that systematic risk (CAPM’s beta) is not the only variable relating to firm’s stock returns as operating leverage and firm’s size are also found to have significant relationships with stock returns.

{kind=link}