People Financing Entrepreneurs within and outside the Family: Pandemic Decline and Resilience in Cultures around the World

Abstract

:1. Introduction

2. Theoretical Perspective

3. Hypotheses

3.1. Impact of the Pandemic

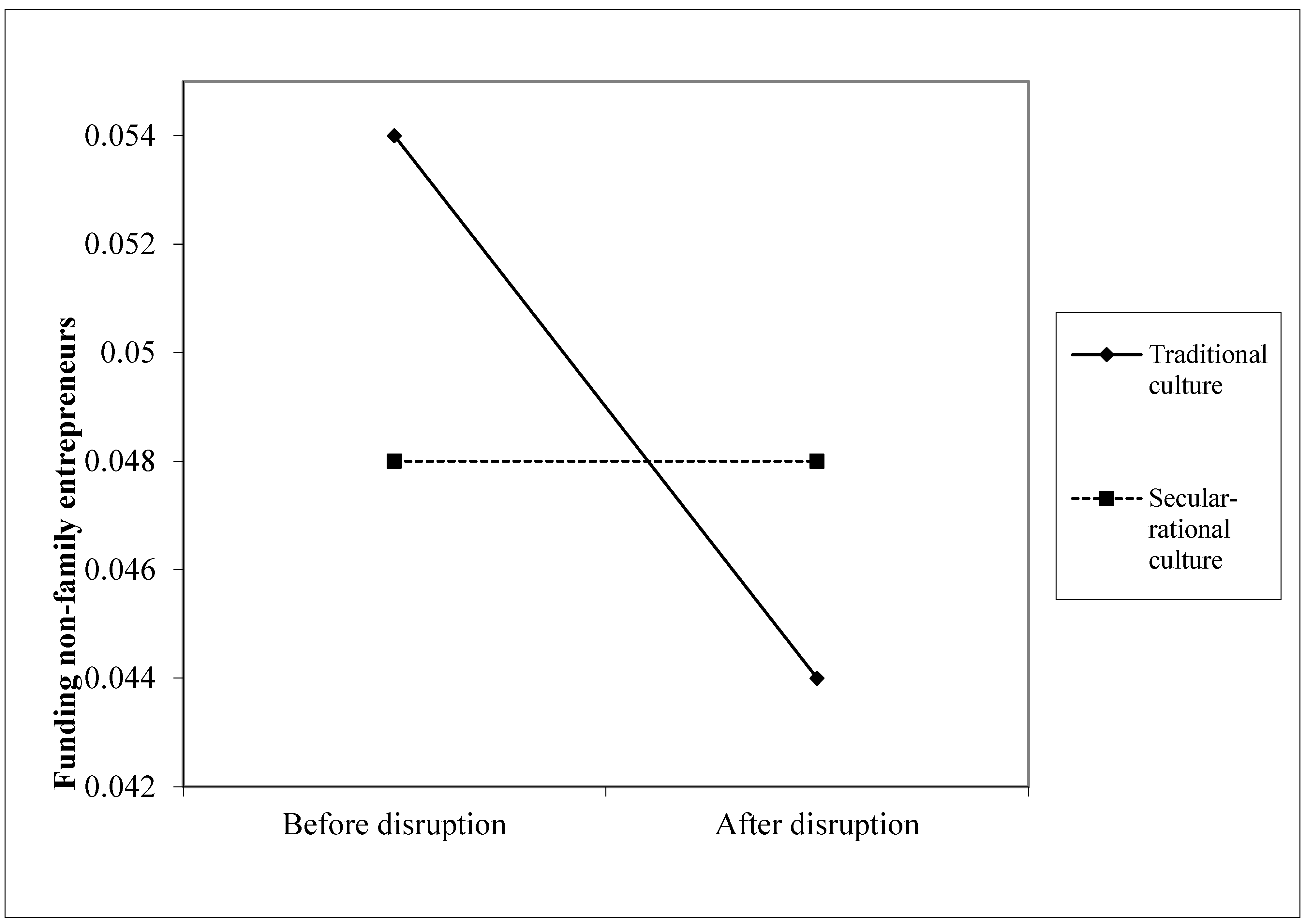

3.2. The Cultural Context Influencing Funding

4. Research Design

4.1. Design: Experiment

4.2. Sampling Societies and Adults

4.3. Measurements

4.3.1. Secular-Rational Culture

4.3.2. Family Business Culture

4.3.3. Adults Funding Family-Related Entrepreneurs and Family-Unrelated Entrepreneurs

Have you, in the past three years, personally provided funds for a new business started by someone else, excluding any purchases of stocks or mutual funds?

What was your relationship with the person that received your most recent personal investment?Was this a

- -

- -

- -

- -

- -

- -

4.3.4. Time

4.3.5. Controls

- gender, coded 0 for men and 1 for women;

- age, coded in years, from 18 to 64;

- education, coded in years for the highest completed degree;

- income, measured on a scale of 1, 2, and 3 for being in the lowest third, the middle third, or the highest third of family incomes among the respondents in each country;

- experience as owner–manager; a 0–1 dummy for whether or not the adult had stopped owning and managing a business within the last three years; and

- occupation, a categorical variable for whether the respondent at the time of the interview was self-employed, an employee, unemployed, a homemaker, or a student.

4.4. Techniques for Analyzing the Data

5. Results

5.1. Background

5.2. Change in Adults’ Funding of Family-Related Entrepreneurs and Non-Family-Related Entrepreneurs

5.3. Effects on Funding of Family-Related Entrepreneurs and Non-Family-Related Entrepreneurs

6. Discussion

6.1. Findings

6.2. Contributions

6.3. Limitation

6.4. Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Au, Kevin, and Ho Kwong Kwan. 2009. Start–up capital and Chinese entrepreneurs: The role of family. Entrepreneurship Theory and Practice 33: 889–908. [Google Scholar]

- Berrone, Pascual, Patricio Duran, Luis Gómez-Mejía, Pursey P. M. A. R. Heugens, Tatiana Kostova, and Marc van Essen. 2021. Impact of informal institutions on the prevalence, strategy, and performance of family firms: A meta-analysis. Journal of International Business Studies, 1–25. [Google Scholar]

- Bosma, Niels, Stephen Hill, Aileen Ionescu-Somers, Donna Kelley, Maribel Guerrero, and Thomas Schøtt. 2021. Global Entrepreneurship Monitor 2020/2021 Global Report. Available online: www.gemconsortium.org (accessed on 1 June 2021).

- Burke, Andrew, Chantal Hartog, André van Stel, and Kashifa Suddle. 2010. How does entrepreneurial activity affect the supply of informal investors? Venture Capital 12: 21–47. [Google Scholar] [CrossRef]

- Bygrave, William, Michael Hay, Emily Ng, and Paul Reynolds. 2003. Executive forum: A study of informal investing in 29 nations composing the Global Entrepreneurship Monitor. Venture Capital: An International Journal of Entrepreneurial Finance 5: 101–16. [Google Scholar] [CrossRef]

- Davidsson, Per, Jan Recker, and Frederik von Briel. 2021. COVID−19 as External Enabler of entrepreneurship practice and research. Business Research Quarterly 24: 214–223. [Google Scholar] [CrossRef]

- DeGennaro, Ramon P. 2010. Angel investors: Who they are and what they do; Can I be one, too? The Journal of Wealth Managemen 13: 55–60. [Google Scholar] [CrossRef]

- Ding, Zhujun, Kevin Au, and Flora Chiang. 2015. Social trust and angel investors’ decisions: A multilevel analysis across nations. Journal of Business Venturing 30: 307–21. [Google Scholar] [CrossRef] [Green Version]

- Ding, Zhujun, Sunny Li Sun, and Kevin Au. 2014. Angel investors’ selection criteria: A comparative institutional perspective. Asia Pacific Journal of Management 31: 705–31. [Google Scholar] [CrossRef]

- El Kolaly, Hoda, Mahsa Samsami, and Thomas Schøtt. 2021. Female and male business angels funding entrepreneurs: Embedded in high growth and low wealth in emerging economies. (in review) [Google Scholar]

- Inglehart, Ronald, and Christian Welzel. 2005. Modernization, Cultural Change, and Democracy: The Human Development Sequence. Cambridge: Cambridge University Press. [Google Scholar]

- Landström, Hans, and Colin Mason, eds. 2016. Handbook of Research on Business Angels. Cheltenham: Edward Elgar Publishing. [Google Scholar]

- Li, Yong, and Shaker A. Zahra. 2012. Formal institutions, culture, and venture capital activity: A cross-country analysis. Journal of Business Venturing 27: 95–111. [Google Scholar] [CrossRef]

- Mason, Colin M., and Richard T. Harrison. 2000. The size of the informal venture capital market in the United Kingdom. Small Business Economics 15: 137–48. [Google Scholar] [CrossRef]

- Mason, Colin, and Matthew Stark. 2004. What do investors look for in a business plan? A comparison of the investment criteria of bankers, venture capitalists and business angels. International Small Business Journal 22: 227–48. [Google Scholar] [CrossRef]

- Maxwell, Andrew L., Scott A. Jeffrey, and Moren Lévesque. 2011. Business angel early stage decision making. Journal of Business Venturing 26: 212–25. [Google Scholar] [CrossRef]

- Van Osnabrugge, Mark, and Robert J. Robinson. 2000. Angel Investing: Matching Start-Up Funds with Start-Up Companies: The Guide for Entrepreneurs, Individual Investors, and Venture Capitalists. San Francisco: John Wiley & Sons. [Google Scholar]

- Paul, Stuart, Geoff Whittam, and Janette Wyper. 2007. Towards a model of the business angel investment process. Venture Capital 9: 107–25. [Google Scholar] [CrossRef]

- Perkins, Dwigh. 2000. Law, family ties, and the East Asian way of business. In Culture Matters: How Values Shape Human Progress. New York: Basic Books, pp. 232–43. [Google Scholar]

- Ramadani, Veland. 2009. Business angels: Who they really are. Strategic Change: Briefings in Entrepreneurial Finance 18: 249–58. [Google Scholar] [CrossRef]

- Samsami, Mahsa. 2018. The Effect of Electronic Word of Mouth on Brand Social Power. Master’s thesis, Tehran University, Tehran, Iran. [Google Scholar]

- Samsami, Mahsa. 2021. Business angels’ ties with entrepreneurs in traditional and secular-rational societies: China, Egypt and Iran contrasted Germany and Norway. European Journal of International Management. in press. [Google Scholar]

- Samsami, Mahsa, Hoda El Kolaly, and Thomas Schøtt. Forthcoming. Business angels’ ties with entrepreneurs: Embedded in traditional and secular-rational cultures. In Developments in Entrepreneurial Finance and Technology. Edited by David Audretsch, Maksim Belitski, Nada Khachlouf and Rosa Caiazza. Cheltenham: Edward Elgar Publishing.

- Shane, Scott. 2008. Fool’s Gold?: The Truth behind Angel Investing in America. Oxford: Oxford University Press. [Google Scholar]

- Snijders, Tom A. B., and Roel J. Bosker. 2012. Multilevel Analysis: An Introduction to Basic and Advanced Multilevel Modeling, 2nd ed. Los Angeles: Sage. [Google Scholar]

- Sørheim, Roger. 2003. The pre-investment behaviour of business angels: A social capital approach. Venture Capital 5: 337–64. [Google Scholar] [CrossRef]

- Sørheim, Roger, and Hans Landström. 2001. Informal investors—A categorization, with policy implications. Entrepreneurship and Regional Development 13: 351–70. [Google Scholar] [CrossRef]

- Sudek, Richard. 2006. Angel investment criteria. Journal of Small Business Strategy 17: 89–103. [Google Scholar]

- White, Brett A., and John Dumay. 2017. Business angels: A research review and new agenda. Venture Capital 19: 183–216. [Google Scholar] [CrossRef]

- Wong, Poh Kam, and Yuen Ping Ho. 2007. Characteristics and determinants of informal investment in Singapore. Venture Capital 9: 43–70. [Google Scholar] [CrossRef]

- Wong, Poh Kam, Yuen Ping Ho, and Erkko Autio. 2004. Determinants of angel investing propensity: Empirical evidence from the 29-country GEM dataset. Frontiers of Entrepreneurship Research, 48–62. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

| Society | Years of Surveys Used | Sample of Adults before Pandemic | Sample of Adults in 2020 | Sample of Business Angels before the Pandemic | Sample of Business Angels in 2020 |

|---|---|---|---|---|---|

| Angola | 2018, 2020 | 2014 | 1958 | 197 | 279 |

| Arab Emirates | 2019, 2020 | 1954 | 1980 | 163 | 54 |

| Austria | 2018, 2020 | 4377 | 4427 | 336 | 262 |

| Brazil | 2019, 2020 | 2000 | 2000 | 71 | 134 |

| Burkina Faso | 2016, 2020 | 2325 | 2320 | 296 | 150 |

| Canada | 2019, 2020 | 7336 | 2306 | 515 | 148 |

| Chile | 2019, 2020 | 8091 | 8349 | 1711 | 1800 |

| Colombia | 2019, 2020 | 2097 | 2096 | 170 | 177 |

| Croatia | 2019, 2020 | 1975 | 1962 | 85 | 87 |

| Cyprus | 2019, 2020 | 2012 | 2003 | 95 | 70 |

| Egypt | 2019, 2020 | 2537 | 2780 | 79 | 96 |

| Germany | 2019, 2020 | 2991 | 2998 | 183 | 175 |

| Greece | 2019, 2020 | 1991 | 1992 | 91 | 72 |

| Guatemala | 2019, 2020 | 2958 | 2903 | 435 | 385 |

| India | 2019, 2020 | 3201 | 3194 | 133 | 53 |

| Indonesia | 2018, 2020 | 3031 | 2445 | 64 | 70 |

| Iran | 2019, 2020 | 3100 | 3134 | 213 | 126 |

| Israel | 2019, 2020 | 1968 | 1955 | 64 | 58 |

| Italy | 2019, 2020 | 1994 | 1995 | 14 | 6 |

| Kazakhstan | 2017, 2020 | 1784 | 1140 | 184 | 303 |

| S. Korea | 2019, 2020 | 1994 | 1996 | 44 | 55 |

| Kuwait | 2014, 2020 | 1836 | 2091 | 324 | 166 |

| Latvia | 2019, 2020 | 1593 | 1609 | 85 | 72 |

| Luxemburg | 2019, 2020 | 2055 | 1985 | 156 | 113 |

| Morocco | 2019, 2020 | 3506 | 3512 | 105 | 63 |

| Netherlands | 2019, 2020 | 1742 | 1694 | 87 | 136 |

| Norway | 2019, 2020 | 1994 | 1993 | 111 | 94 |

| Oman | 2019, 2020 | 1942 | 1932 | 282 | 149 |

| Panama | 2019, 2020 | 2018 | 1997 | 128 | 166 |

| Poland | 2019, 2020 | 7961 | 7992 | 283 | 225 |

| Qatar | 2019, 2020 | 2993 | 3003 | 373 | 261 |

| Russia | 2019, 2020 | 1994 | 1983 | 105 | 84 |

| Saudi Arabia | 2019, 2020 | 3978 | 3978 | 596 | 599 |

| Slovakia | 2019, 2020 | 1986 | 1988 | 132 | 113 |

| Slovenia | 2019, 2020 | 1571 | 1559 | 79 | 58 |

| Spain | 2019, 2020 | 23,164 | 25,993 | 683 | 757 |

| Sweden | 2019, 2020 | 3556 | 3583 | 297 | 220 |

| Switzerland | 2019, 2020 | 1543 | 1501 | 153 | 77 |

| Taiwan | 2019, 2020 | 2339 | 2225 | 102 | 88 |

| United Kingdom | 2019, 2020 | 1606 | 1587 | 45 | 36 |

| United States | 2019, 2020 | 2657 | 1762 | 209 | 125 |

| Uruguay | 2018, 2020 | 1604 | 1715 | 91 | 95 |

| Totals | 135,368 adults | 131,615 adults | 9569 business angels | 8257 business angels |

| Before Disruption | After Disruption | |

|---|---|---|

| Number of adults surveyed | 135,368 | 131,615 |

| Percentage of females | 49.4% | 48.8% ** |

| Mean years of age | 40.2 years | 40.2 years |

| Mean years of education | 12.8 years | 12.9 years *** |

| Percentage of former owner–managers | 5.0% | 5.3% *** |

| Mean income on a scale of 1 to 3 | 2.03 | 1.98 *** |

| Percentage self-employed | 12% | 13% *** |

| Percentage of employees | 58% | 54% *** |

| Percentage unemployed | 11% | 14% *** |

| Percentage of homemakers | 12% | 11% *** |

| Percentage of students | 7% | 8% *** |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | ||||||||||||||

| 2 | 0.02 | |||||||||||||

| 3 | 0.01 | −0.63 | ||||||||||||

| 4 | −0.01 | 0.05 | −0.03 | |||||||||||

| 5 | −0.01 | 0.00 | 0.00 | −0.03 | ||||||||||

| 6 | −0.01 | −0.02 | 0.06 | −0.01 | −0.06 | |||||||||

| 7 | 0.00 | −0.18 | 0.19 | 0.00 | −0.02 | 0.02 | ||||||||

| 8 | 0.01 | −0.10 | 0.03 | 0.02 | 0.04 | −0.02 | −0.06 | |||||||

| 9 | −0.03 | −0.02 | −0.04 | 0.06 | 0.06 | −0.09 | −0.01 | 0.26 | ||||||

| 10 | 0.01 | 0.10 | −0.09 | 0.09 | 0.07 | −0.02 | −0.02 | −0.01 | 0.00 | |||||

| 11 | 0.02 | 0.05 | −0.01 | 0.00 | 0.01 | −0.09 | 0.07 | −0.03 | 0.06 | 0.00 | ||||

| 12 | −0.04 | −0.15 | 0.07 | 0.02 | 0.02 | −0.10 | −0.03 | 0.23 | 0.14 | −0.03 | −0.43 | |||

| 13 | 0.04 | 0.10 | −0.07 | −0.01 | −0.01 | 0.07 | −0.02 | −0.13 | −0.16 | 0.06 | −0.14 | −0.42 | ||

| 14 | −0.01 | 0.03 | 0.00 | −0.01 | −0.03 | 0.16 | 0.28 | −0.17 | −0.11 | −0.01 | −0.14 | −0.41 | −0.14 | |

| 15 | 0.01 | 0.06 | −0.04 | −0.02 | −0.01 | 0.01 | −0.36 | −0.02 | −0.02 | −0.01 | −0.11 | −0.32 | −0.10 | −0.10 |

| Before Disruption | After Disruption | Change | |

|---|---|---|---|

| Percent of adults funding family-related entrepreneurs | 3.90% | 3.60% | −0.30% *** |

| Percent of adults funding non-family-related entrepreneurs | 3.12% | 2.64% | −0.48% *** |

| N adults | 135,368 | 131,615 | |

| Percentage of business angels funding family-related entrepreneurs | 55.2% | 57.4% | 2.2% *** |

| Percentage of business angels funding non-family-related entrepreneurs | 44.8% | 43.6% | −2.2% *** |

| Sum | 100% | 100% | |

| N business angels | 9569 | 8257 |

| Adults’ Funding of Family-Related Entrepreneurs | Adults’ Funding of Non-Family-Related Entrepreneurs | |||

|---|---|---|---|---|

| Main Effects | Moderation Included | Main Effects | Moderation Included | |

| Model A | Model B | Model C | Model D | |

| Time (before 0, after 1) | −0.002 ** | −0.002 ** | −0.005 *** | −0.005 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Family business culture | 0.007 | 0.006 | −0.004 | −0.004 |

| (0.005) | (0.005) | (0.004) | (0.004) | |

| Secular-rational culture | −0.002 | −0.005 | 0.000 | −0.003 |

| (0.005) | (0.005) | (0.003) | (0.003) | |

| Time * Family business culture | 0.002 † | 0.001 | ||

| (0.001) | (0.001) | |||

| Time * Secular-rational culture | 0.005 *** | 0.005 *** | ||

| (0.001) | (0.001) | |||

| Gender: female | −0.001 | −0.001 | −0.020 *** | −0.020 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Age | 0.002 *** | 0.002 *** | −0.004 *** | −0.004 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Education | 0.004 *** | 0.004 *** | 0.005 *** | 0.005 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Income | 0.009 *** | 0.009 *** | 0.007 *** | 0.007 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Experience as owner–manager | 0.064 *** | 0.064 *** | 0.047 *** | 0.047 *** |

| (0.002) | (0.002) | (0.002) | (0.002) | |

| Occupation: Employee | −0.002 * | −0.002 * | −0.004 *** | −0.004 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | |

| Occupation: Unemployed | −0.018 *** | −0.018 *** | −0.012 *** | −0.012 *** |

| (0.002) | (0.001) | (0.002) | (0.002) | |

| Occupation: Homemaker | −0.002 | −0.002 | −0.008 *** | −0.008 *** |

| (0.002) | (0.002) | (0.002) | (0.002) | |

| Occupation: Student | −0.013 *** | −0.013 *** | −0.015 *** | −0.015 *** |

| (0.002) | (0.002) | (0.002) | (0.002) | |

| Country | Yes | Yes | Yes | Yes |

| Intercept | 0.040 *** | 0.040 *** | 0.050 *** | 0.051 *** |

| (0.005) | (0.005) | (0.003) | (0.003) | |

| N countries | 42 | 42 | ||

| N adults | 211,432 | 211,432 | ||

| Business Angels’ Funding of Family-Related Entrepreneurs (Contrasted Funding of Non-Family-Related Entrepreneurs) | ||

|---|---|---|

| Main Effects | Moderation Included | |

| Model E | Model F | |

| Time (before 0, after 1) | 0.016 * | 0.016 * |

| (0.008) | (0.008) | |

| Family business culture | 0.058 *** | 0.049 * |

| (0.058) | (0.021) | |

| Secular-rational culture | −0.022 | −0.020 |

| (0.021) | (0.022) | |

| Time * Family business culture | 0.020 * | |

| (0.009) | ||

| Time * Secular-rational culture | −0.004 | |

| (0.009) | ||

| Gender: female | 0.142 *** | 0.143 *** |

| (0.008) | (0.008) | |

| Age | 0.028 *** | 0.028 *** |

| (0.004) | (0.004) | |

| Education | −0.023 *** | −0.023 *** |

| (0.005) | (0.004) | |

| Income | 0.003 | 0.004 |

| (0.004) | (0.004) | |

| Experience as owner–manager | 0.016 | 0.015 |

| (0.011) | (0.011) | |

| Occupation: Employee | 0.052 *** | 0.052 *** |

| (0.012) | (0.012) | |

| Occupation: Unemployed | −0.014 | −0.016 |

| (0.017) | (0.017) | |

| Occupation: Homemaker | 0.084 *** | 0.083 *** |

| (0.017) | (0.017) | |

| Occupation: Student | 0.015 | 0.014 |

| (0.021) | (0.021) | |

| Country | ||

| Yes | 0.429 *** | 0.429 *** |

| (0.021) | (0.021) | |

| N countries | 42 | |

| N business angels | 15,371 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tolba, A.; Ismail, A.; Schøtt, T. People Financing Entrepreneurs within and outside the Family: Pandemic Decline and Resilience in Cultures around the World. J. Risk Financial Manag. 2021, 14, 610. https://doi.org/10.3390/jrfm14120610

Tolba A, Ismail A, Schøtt T. People Financing Entrepreneurs within and outside the Family: Pandemic Decline and Resilience in Cultures around the World. Journal of Risk and Financial Management. 2021; 14(12):610. https://doi.org/10.3390/jrfm14120610

Chicago/Turabian StyleTolba, Ahmed, Ayman Ismail, and Thomas Schøtt. 2021. "People Financing Entrepreneurs within and outside the Family: Pandemic Decline and Resilience in Cultures around the World" Journal of Risk and Financial Management 14, no. 12: 610. https://doi.org/10.3390/jrfm14120610

APA StyleTolba, A., Ismail, A., & Schøtt, T. (2021). People Financing Entrepreneurs within and outside the Family: Pandemic Decline and Resilience in Cultures around the World. Journal of Risk and Financial Management, 14(12), 610. https://doi.org/10.3390/jrfm14120610