Designing a Roadmap for Human Resource Management in the Banking 4.0

Abstract

:1. Introduction

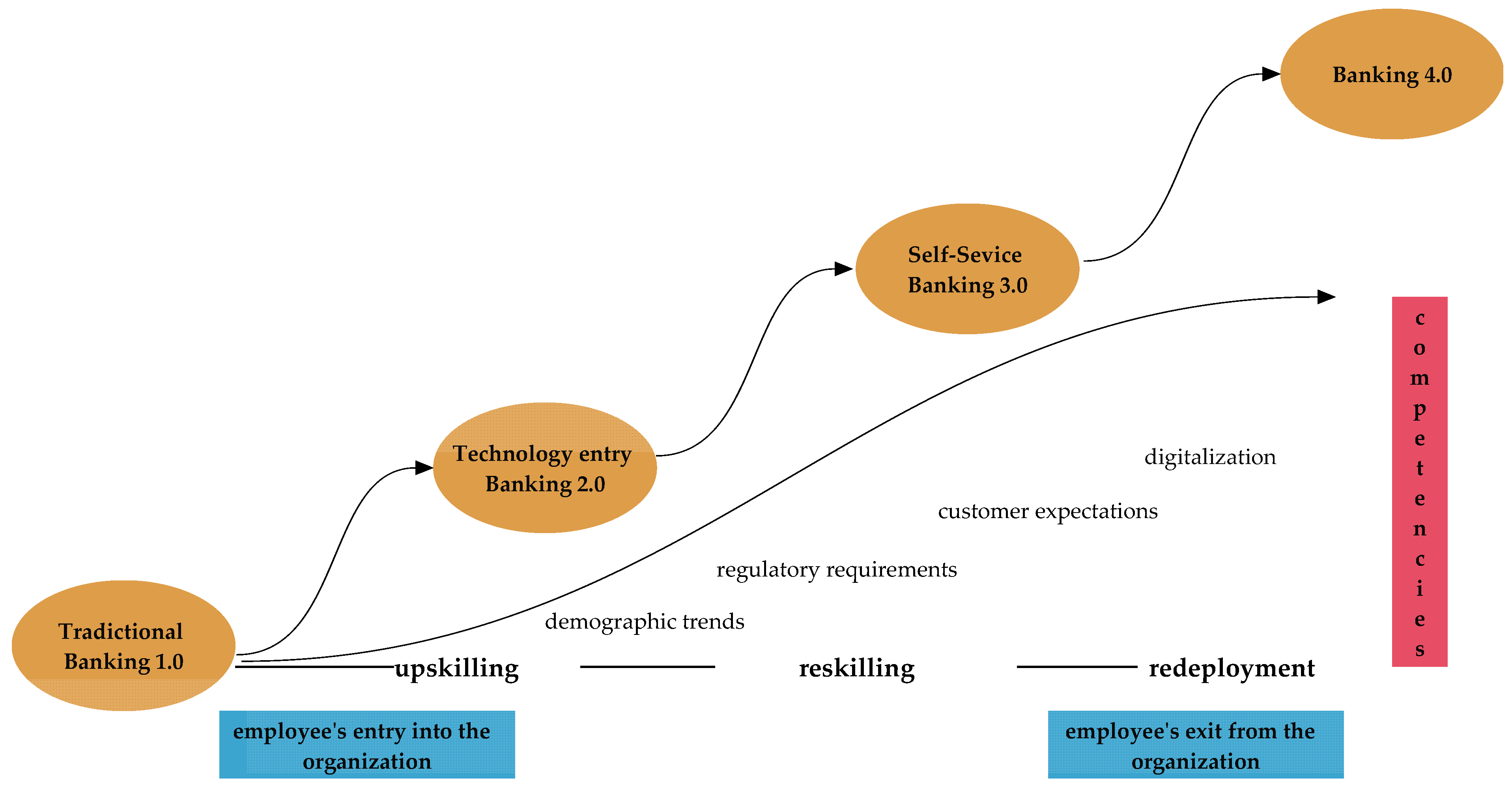

2. Banking 4.0 in the Context of Human Resource Management

- −

- removing barriers to customer service,

- −

- the use of Big Data, advanced analytics, and artificial intelligence,

- −

- improving integrated omnichannel support by implementing open API technologies,

- −

- building collaboration between banks and FinTechs,

- −

- mobile payment expansion,

- −

- adapting to regulatory changes,

- −

- exploring modern technologies (Internet of Things, voice forwarding, blockchain),

- −

- the emergence of new challenger banks

- −

- investing in innovations.

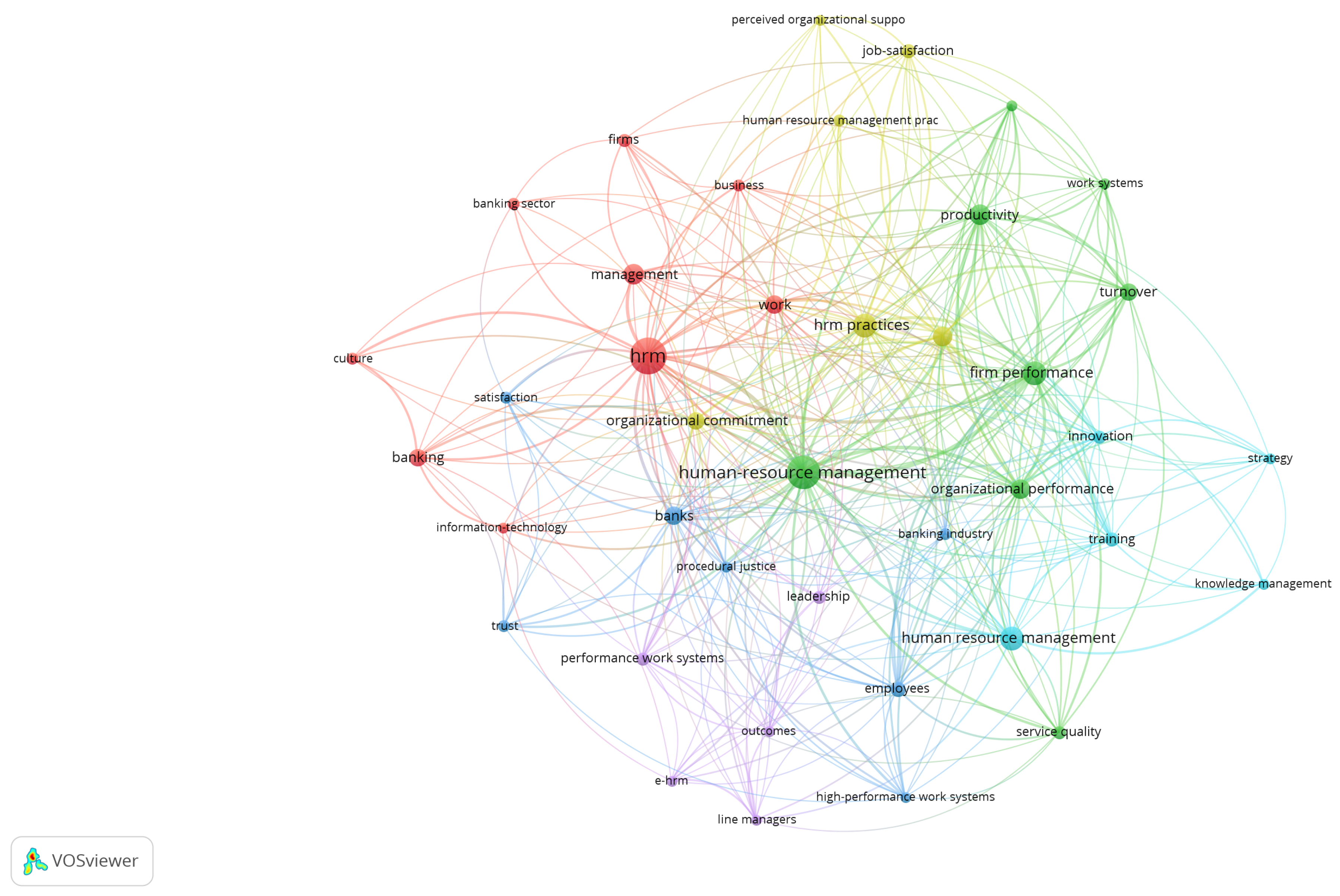

3. Data and Methods

4. Results

4.1. Good Practice form Analysis

- Development practices, mentoring and reverse mentoring; training, lifelong learning practices

- Practices focused on employees’ health and wellbeing

- An information campaign targeted at employees, promoting of intergeneration co-operation

- Recruitment, selection, and adaptation of employees and apprentices

- Organization of work, job-sharing, e-work, temporary work

- Inclusion culture

- Agreement/dialog

- Motivational aspects

- Retirement plan based on resource analysis

- Talent management

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Name of the Organization | Country/Headquarters | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Barclays | Great Britain | ||||||||||

| Deutsche Bank | Germany | ||||||||||

| Bank of France | France | ||||||||||

| Nordea Bank | Denmark | ||||||||||

| Axa | France | ||||||||||

| KBC | Belgium | ||||||||||

| ING-DIBA | Denmark/Germany | ||||||||||

| Unicredit | Italy | ||||||||||

| Credit Industriel at Commercial | France | ||||||||||

| Groupama | France | ||||||||||

| Rabobank | Denmark | ||||||||||

| Wij(s) Rabo | Netherland | ||||||||||

| Achmea Holding NV | Belgium/Netherland/Luxemburg | ||||||||||

| Dekabank Deutche Girozentrale | Germany | ||||||||||

| Danske Bank A/S Finland Branch | Denmark | ||||||||||

| Fondo Banche Assicurazioni | Italy | ||||||||||

| CIB Bank | Hungary | ||||||||||

| Bank Generational Relay | Italy | ||||||||||

| National Bank of Greece | Greece | ||||||||||

| Dikete | Greece/Cyprus | ||||||||||

| Santander Group | Spain | ||||||||||

| Towarzystwo Ubezpieczeń Wzajemnych | Poland | ||||||||||

| Credit Agricole Bank Polska SA | Poland |

4.2. Delphi Results Analysis

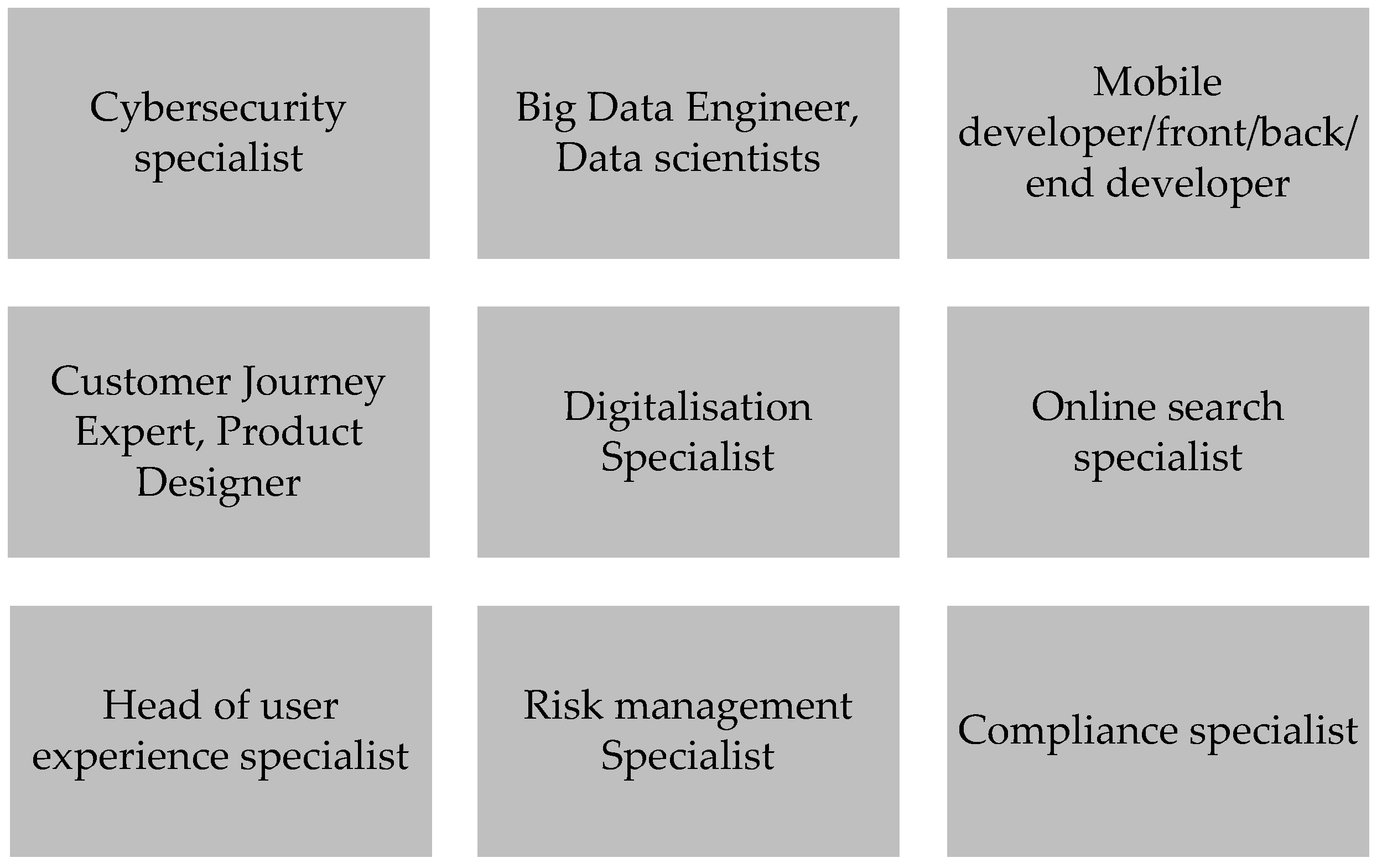

5. Proposed Roadmap for Human Resource Management in Banking 4.0

- −

- managing competencies, including knowledge,

- −

- increasing the motivation to work, commitment, and well-being,

- −

- work-life balance programs (Warwas 2017).

6. Discussion

7. Conclusions and Contributions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Accenture. 2021a. Digital Banking Redefined in 2021. Available online: https://www.deloittedigital.com/us/en/offerings/next-gen-digital-banking/digital-banking-redefined-in-2021.html (accessed on 11 October 2021).

- Accenture. 2021b. The Future of Work: Productive Anywhere. Available online: https://www.accenture.com/_acnmedia/PDF-155/Accenture-Future-Of-Work-Global-Report.pdf#zoom=40 (accessed on 11 October 2021).

- Acharya, Viral V., Robert Engle, and Steffen Sascha. 2021. Why Did Bank Stocks Crash during COVID-19? CEPR Discussion Papers 15901. C.E.P.R. Discussion Papers. Cambridge: NBER. [Google Scholar] [CrossRef]

- Adesina, Kolade Sunday. 2021. How diversification affects bank performance: The role of human capital. Economic Modelling 94: 303–19. [Google Scholar] [CrossRef]

- Afroz, Nushrat N. 2018. Effects of Training on Employee Performance—A Study on Banking Sector, Tangail Bangladesh. Global Journal of Economic and Business 4: 111–24. [Google Scholar] [CrossRef]

- Ahamed, Mostak M. 2017. Asset quality, non-interest income, and bank profitability: Evidence from Indian banks. Economic Modelling 63: 1–14. [Google Scholar] [CrossRef]

- Alhajjar, Anas A., Rezian-na Muhammed Kassim, Valliappan Raju, and Tarek Alnachef. 2018. Driving Industry 4.0 Business Through Talent Management of Human Resource System: The Conceptual Framework for Banking Industry. World Journal of Research and Review 7: 53–57. [Google Scholar]

- Al-Musali, M. A., and K. N. I. Ku Ismail. 2016. Cross-country comparison of intellectual capital performance and its impact on financial performance of commercial banks in GCC countries. International Journal of Islamic and Middle Eastern Finance and Management 9: 512–31. [Google Scholar] [CrossRef]

- Alsafadi, Yousef, and Shadi Altahat. 2021. Human Resource Management Practices and Employee Performance: The Role of Job Satisfaction. Journal of Asian Finance, Economics and Business 8: 519–29. [Google Scholar] [CrossRef]

- Ananda, S. Upadhyaya, Devesh Sonal, and Anis Moosa Al Lawati. 2020. What factors drive the adoption of digital banking? An empirical study from the perspective of Omani retail banking. Journal of Financial Services Marketing 25: 14–24. [Google Scholar] [CrossRef]

- Anusara, Jhensanam, Md Rasel, Ayrin Sultana, Bouasone Chanthamith, Md Humayun Kabir, and Md Arafatul Hasan. 2019. Comparative Study on Human Resource Management Practices in Banking Sector. American Journal of Marketing Research 5: 36–41. [Google Scholar]

- Aryee, Samuel, Fred O. Walumbwa, Emmanuel Y. M. Seidu, and Lilian Otaye. 2012. Impact of high-performance work systems on individual- and branch-level performance: Test of a multilevel model of intermediate linkages. The Journal of Applied Psychology 97: 287–300. [Google Scholar] [CrossRef] [PubMed]

- Auer, Raphael, Giulio Cornelli, and Jon Frost. 2020. COVID-19, Cash, and the Future of Payments. BIS Bulletin No 3. Available online: https://www.bis.org/publ/bisbull03.pdf (accessed on 12 October 2021).

- Bartel, Ann P. 2004. Human Resource Management and Organizational Performance: Evidence from Retail Banking. ILR Review 57: 181–203. [Google Scholar] [CrossRef]

- Bastari, Ary, Anis Eliyana, Agus Syabarrudin, Zainal Arief, and Alvin Permana Emur. 2020. Digitalization in Banking Sector: The Role of Intrinsic Motivation. Heliyon 6: e05801. [Google Scholar] [CrossRef]

- Beck, Thorsten, Tao Chen, Chen Lin, and Frank Song. 2016. Financial innovation: The bright and the dark sides. Journal of Banking and Finance 72: 28–51. [Google Scholar] [CrossRef]

- Bharadway, Sundar G., P. Rajan Varadarajan, and John Fahy. 1993. Sustainable Competitive Advantage in Service Industries: A Conceptual Model and Research Propositions. Journal of Marketing 57: 83–99. [Google Scholar] [CrossRef]

- Bretschneider, Stuart, Frederick J. Marc-Aurele, and Jiannan Wu. 2015. Best Practices. Research: A Methodological Guide for the Perplexed. Journal of Public Administration Research and Theory: J-PART 15: 307–23. [Google Scholar] [CrossRef]

- Canals, Jordi. 1993. Competitive Strategies in European Banking. Oxford: Clarendon Press. [Google Scholar]

- Capiga, Mirosława, Witold Gradoń, and Grażyna Szustak. 2016. Kreowanie Wartości Banku. Warszawa: Wydawnictwo CeDeWu. [Google Scholar]

- CEDEFOP. 2015. National Qualifications Framework Developments in Europe Analysis and Overview 2015–16. Available online: http://www.cedefop.europa.eu/files/5565_en.pdf (accessed on 10 October 2021).

- Chen, Tser-yieth. 1999. Critical Success Factors for Various Strategies in the Banking. International Journal of Bank Marketing 17: 83–92. [Google Scholar] [CrossRef]

- Cherif, Fatma. 2020. The role of human resource management practices and employee job satisfaction in predicting organizational commitment in Saudi Arabian banking sector. International Journal of Sociology and Social Policy 40: 529–41. [Google Scholar] [CrossRef]

- Dang, Nhan Truong Thanh, Quynh Thi Nguyen, Raymund Habaradas, Van Dung HA, and Van Thuy Nguyen. 2020. Talent Conceptualization and Talent Management Approaches in the Vietnamese Banking Sector. Journal of Asian Finance, Economics and Business 7: 453–62. [Google Scholar] [CrossRef]

- Deloitte. 2019. What Is the Future of Work? Redefining Work, Workforces, and Workplaces. Available online: https://www2.deloitte.com/us/en/insights/focus/technology-and-the-future-of-work/redefining-work-workforces-workplaces.html (accessed on 5 October 2021).

- Demirgüç-Kunt, Asli, Alvaro Pedraza, and Claudia Ruiz-Ortega. 2021. Banking sector performance during the COVID-19 crisis. Journal of Banking & Finance 133: 106305. [Google Scholar] [CrossRef]

- Deng, Xiang, Zhi Huang, and Xiang Cheng. 2019. FinTech and Sustainable Development: Evidence from China Based on P2P Data. Sustainability 11: 6434. [Google Scholar] [CrossRef] [Green Version]

- Devlin, Jim, and Christine Ennew. 1997. Understanding competitive advantage in retail financial services. International Journal of Bank Marketing 15: 73–82. [Google Scholar] [CrossRef]

- Dratva, Richard. 2020. Is open banking driving the financial industry towards a true electronic market? Electronic Markets 30: 65–67. [Google Scholar] [CrossRef]

- Dubois, Michel, Marc-Eric Bobillier Chaumon, and Didier Retour. 2011. The impact of development of customer online banking skills on customer adviser skills. New Technology, Work and Employment 26: 156–73. [Google Scholar] [CrossRef]

- ECB. 2021. EU Structural Financial Indicators. Available online: https://www.ecb.europa.eu/press/pr/date/2021/html/ecb.pr210526_annex~b5ce7a6554.en.pdf (accessed on 10 October 2021).

- Elia, Pamela T., Kalil Ghazzawi, and Badih Arnaout. 2017. Talent Management Implications in the Lebanese Banking Industry. Human Resource Management Research 7: 83–89. [Google Scholar] [CrossRef]

- EU. 2015. Directive (EU) 2015/2366 of the European Parliament and of the Council of 25 November 2015 on payment services in the internal market, amending Directives 2002/65/EC, 2009/110/EC and 2013/36/EU and Regulation (EU) No 1093/2010, and repealing Directive 2007/64/EC. OJ L 337: 35–127. [Google Scholar]

- EU. 2018. Directive (EU) 2018/843 of the European Parliament and of the Council of 30 May 2018 amending Directive (EU) 2015/849 on the prevention of the use of the financial system for the purposes of money laundering or terrorist financing, and amending Directives 2009/138/EC and 2013/36/EU. OJ L 156: 43–74. [Google Scholar]

- EU. 2019. Directive (EU) 2019/878 of the European Parliament and of the Council of 20 May 2019 amending Directive 2013/36/EU as regards exempted entities, financial holding companies, mixed financial holding companies, remuneration, supervisory measures and powers and capital conservation measures. OJ L 150: 253–95. [Google Scholar]

- Fintech Circle. 2017. 94% of People in Financial Services Suspect Colleagues Are Bluffing about Their Fintech Knowledge. Available online: https://www.finextra.com/pressarticle/70717/94-of-people-in-financial-services-suspect-colleagues-are-bluffing-about-their-fintech-knowledge (accessed on 22 August 2021).

- Gelade, Garry A., and Mark Ivery. 2003. The impact of human resource management and work climate on organizational performance. Personnel Psychology 56: 383–404. [Google Scholar] [CrossRef]

- Górniak, Jarosław, Kocór Marcin, Kwinta Odrzywołek Joanna, Maźnica Łukasz, Worek Barbara, and Jakub Wróblewski. 2018. Centrum Ewaluacji i Analiz Polityk Publicznych Uniwersytetu Jagiellońskiego. Available online: https://www.parp.gov.pl/storage/publications/pdf/37-RAPORT-sektor-finansowy-210x270-inter_200511.pdf (accessed on 9 October 2021).

- Guest, David E. 2017. Human resource management and employee well-being: Towards a new analytic framework. Human Resource Management Journal 27: 22–38. [Google Scholar] [CrossRef] [Green Version]

- Haddad, Christian, and Lars Hornuf. 2019. The emergence of the global fintech market: Economic and technological determinants. Small Business Economics 53: 81–105. [Google Scholar] [CrossRef] [Green Version]

- Hitt, Michael A., Leonard Bierman, Katsuhiko Shimizu, and Rahul Kochhar. 2001. Direct and Moderating Effects of Human Capital on Strategy and Performance in Professional Service Firms: A Resource-Based Perspective. The Academy of Management Journal 44: 13–28. [Google Scholar] [CrossRef]

- Huynh, Quang Linh, Thanh Thuy Nguyen Thi, Tan Khuong Huynh, Tuyet Anh Duong Thi, and Thuy Lan Le Thi. 2020. Comparative significance of human resource management practices on banking financial performance with analytic hierarchy process. Accounting 6: 1323–28. [Google Scholar] [CrossRef]

- Jeni, Fatema Akter, Momota, and Md. Al-Amin. 2021. The Impact of Training and Development on Employee Performance and Productivity: An Empirical Study on Private Bank of Noakhali Region in Bangladesh. South Asian Journal of Social Studies and Economics 9: 1–18. [Google Scholar] [CrossRef]

- Kaur, Navleen, Supriya Lamba Sahdev, Monika Sharma, and Laraibe Siddiqui. 2020. Banking 4.0: ‘The Influence of Artificial Intelligence on the Banking Industry & How AI Is Changing the Face of Modern Day Banks. International Journal of Management 11: 577–85. [Google Scholar] [CrossRef]

- King, Brett. 2018. Bank 4.0, Banking Everywhere, Never at a Bank. Singapore: Marshall Cavendish International (Asia) Pte Ltd. [Google Scholar]

- Kitsios, Fotis, Ioannis Giatsidis, and Maria Kamariotou. 2021. Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services. Journal of Open Innoation: Technology, Market, and Complexity 7: 204. [Google Scholar] [CrossRef]

- Kołodziejczyk-Olczak, Izabela. 2014. Zarządzanie Pracownikami w Dojrzałym Wieku. Wyzwania i Problemy. Lodz: Lodz University Press. [Google Scholar]

- Kozar, Łukasz, Justyna Wiktorowicz, Izabela Warwas, and Iwa Kuchciak. 2020. Solidarity between Generations in the Financial Sector. Inventory of the Best Practices. Łódź (Internal Project Materials). Łódź: University of Lodz. [Google Scholar]

- KPMG. 2020. Digitalization in Banking Beyond Covid-19. Available online: https://assets.kpmg/content/dam/kpmg/be/pdf/2021/Digitalization-in-banking-beyond-Covid-19.pdf (accessed on 9 October 2021).

- Kuchciak, Iwa, and Justyna Wiktorowicz. 2020. Individual Determinants for the Transfer of Knowledge in the Financial Sector. Intergenerational Human Capital Management in Organizations 2: 81–87. [Google Scholar] [CrossRef]

- Kuchciak, Iwa, Justyna Wiktorowicz, and Izabela Warwas. 2020. Chapter 3: Age Management in the Financial Sector: Opportunities and Challenges. In Intergenerational Divide and Employee Solidarity. Inclusive Bargaining as a Drive for Change in the Digital Era. Edited by Domenico Iodice. Bergamo: Adapt University Press. [Google Scholar]

- Kumar, Ananda, and Balaji K. Mathimaran. 2017. Employee Retention Strategies. An Empirical Research. Global Journal of Management and Business 17. Available online: https://journalofbusiness.org/index.php/GJMBR/article/view/2243 (accessed on 9 October 2021).

- Kusumawati, Rizqi Adhyka. 2019. The change of human resources role in the banking digitalization era. The European Proceedings of Social & Behavioural Sciences. Available online: https://www.europeanproceedings.com/files/data/article/94/5421/article_94_5421_pdf_100.pdf (accessed on 9 October 2021).

- Marcinkowska, Monika. 2013. Kapitał Relacyjny Banków. Łódź: Wydawnictwo Uniwersytetu Łódzkiego. [Google Scholar]

- Mawlawi, Allam, and Abir El Fawal. 2018. Talent Management in the Lebanese Banking Sector. Management 8: 80–85. [Google Scholar] [CrossRef]

- Mbama, Cajetan I., and Patrick O. Ezepue. 2018. Digital banking, customer experience and bank financial performance: UK customers’ perceptions. International Journal of Bank Marketing 36: 230–55. [Google Scholar] [CrossRef]

- Mehdiabadi, Amir, Mariyeh Tabatabeinasab, Cristi Spulbar, Amir Karbassi Yazdi, and Ramona Birau. 2020. Are We Ready for the Challenge of Banks 4.0? Designing a Roadmap for Banking Systems in Industry 4.0. International Journal of Financial Studies 8: 32. [Google Scholar] [CrossRef]

- Mekinjić, Boško. 2019. The impact of Industry 4.0 on the transformation of the banking sector. Journal of Contemporary Economics 1. [Google Scholar] [CrossRef]

- Meles, Antonio, Claudio Porzio, Gabriele Sampagnaro, and Vincenzo Verdoliva. 2016. The impact of the intellectual capital efficiency on commercial banks performance: Evidence from the US. Journal of Multinational Financial Management 36: 64–74. [Google Scholar] [CrossRef]

- Meyer, John P., and Catherine A. Smith. 2009. HRM practices and organizational commitment: Test of a mediation model. Canadian Journal of Administrative Sciences 17: 319–31. [Google Scholar] [CrossRef]

- Mgiba, Freddy. 2019. Merger, Upskilling, and Reskilling of the Sales—Marketing Personnel in the Fourth Industrial Revolution Environment: A Conceptual Paper. Global Journal of Management and Business Research: E Marketing 19: 12–23. [Google Scholar]

- Mohapara, Suryanarayan, Sangram Keshari Jena, Amarnath Mitra, and Aviral Kumar Tiwari. 2019. Intellectual capital and firm performance: Evidence from Indian banking sector. Applied Economics 51: 6054–67. [Google Scholar] [CrossRef]

- Motlokoa, Mamofokeng Eliza, Lira Peter Sekantsi, and Rammuso Paul Monyolo. 2018. The Impact of Training on Employees’ Performance: The Case of Banking Sector in Lesotho. International Journal of Human Resource Studies 8: 16–46. [Google Scholar] [CrossRef]

- Munjuri, Mercy Gacheri, and Rachael Muthoni Maina. 2013. Workforce diversity management and employee performance in the banking sector in Kenya. DBA Africa Management Review 3: 1–21. Available online: http://journals.uonbi.ac.ke/damr/article/view/1088 (accessed on 7 October 2021).

- Naegele, Gerhard, and Alan Walker. 2006. A Guide to Good Practice in Age Management. Office for Official Publications of the European Communities. Available online: https://www.eurofound.europa.eu/sites/default/files/ef_publication/field_ef_document/ef05137en_1.pdf (accessed on 13 October 2021).

- Nagarajan, Renuga, Mineko Wanda, Mei Lan Fang, and Andrew Sixmith. 2019. Defining organizational contributions to sustaining an ageing workforce: A bibliometric review. European Journal of Ageing 9: 1–25. [Google Scholar] [CrossRef] [Green Version]

- Nguyen, Thi Lam Anh. 2018. Diversification and bank efficiency in six ASEAN countries. Global Finance Journal 37: 57–78. [Google Scholar] [CrossRef]

- Nüesch, Rebecca, Rainer Alt, and Thomas Puschmann. 2015. Hybrid customer interaction. Business & Information Systems Engineering. The International Journal of Wirtschaftsinformatik 57: 73–78. [Google Scholar] [CrossRef]

- Park, Cyn-Young, and Jinyoung Kim. 2020. Education, Skill Training, and Lifelong Learning in the Era of Technological Revolution. Asian Development Bank Economics Working Paper Series 606; Mandaluyong: Asian Development Bank. [Google Scholar] [CrossRef]

- Paul, Achandy Kuriappan, and R. N. Anantharaman. 2004. Influence of HRM practices on organizational commitment: A study among software professionals in India. Human Resource Development Quarterly 15: 77–88. [Google Scholar] [CrossRef]

- Premchand, Anshu, and Anurag Choudhry. 2018. Open Banking & APIs for Transformation in Banking. Paper presented at 2018 International Conference on Communication, Computing and Internet of Things (IC3IoT), Chennai, India, February 15–17. [Google Scholar] [CrossRef]

- Puschmann, Thomas. 2017. Fintech. Business & Information Systems Engineering. The International Journal of Wirtschaftsinformatik 59: 69–76. [Google Scholar] [CrossRef]

- PwC. 2017. 20th CEO Survey, Key Talent Findings in the Financial Services Industry. Available online: https://www.pwc.com/gx/en/ceo-agenda/ceosurvey/2018/gx/industries/financial-services.html (accessed on 14 August 2021).

- Ragin, Charles C. 1987. The Comparative Method: Moving beyond Qualitative and Quan-Titative Strategies. Berkeley, Los Angeles and London: University of California Press. [Google Scholar]

- Ray, Shimul, Sraboni Bagchi, Md. Shahbub Alam, and Umme Salma Luna. 2021. Human Resource Management Practices in Banking Sector of Bangladesh: A Critical Review. OSR Journal of Business and Management 23: 1–7. [Google Scholar] [CrossRef]

- Rihoux, Benoît, and Charles C. Ragin. 2009. Configurational Comparative Methods: Qualitative Comparative Analysis (QCA) and Related Techniques. Thousand Oaks: SAGE Publications, Inc. [Google Scholar] [CrossRef]

- Rotatori, Denise, Eun Jeong Lee, and Sheryl Sleeva. 2020. The evolution of the workforce during the fourth industrial revolution. Human Resource Development International 24: 92–103. [Google Scholar] [CrossRef]

- Rožman, Maja, Sonja Treven, and Vesna Čančer. 2020. The impact of promoting intergenerational synergy on the work engagement of older employees in Slovenia. Journal of East European Management Studies 25: 9–34. [Google Scholar] [CrossRef]

- Rubel, Mohammad Rabiul Basher, Daisy Mui Hung Kee, and Nadia Newaz Rim. 2020. Matching People with Technology: Effect of HIWP on Technology Adaptation. South Asian Journal of Human Resources Management 7: 9–33. [Google Scholar] [CrossRef]

- Saint-Onge, Hubert. 1996. Tacit Knowledge: The key to the strategic alignment of intellectual capital. Planning Review 24: 10–16. [Google Scholar] [CrossRef]

- Saleem, Irfan, and Aitzaz Khurshid. 2014. Do human resource practices affect employee performance? Pakistan Business Review 15: 669–88. [Google Scholar]

- Schröder, Heike, Michael Muller-Camen, and Matthew Flynn. 2014. The management of an ageing workforce: Organisational policies in Germany and Britain. Journal of Human Resource Management 24: 394–409. [Google Scholar] [CrossRef]

- Shahnawaz, Muhhamed, and Rakesh C. Juyal. 2006. Human resource management practices and organizational commitment in different organizations. The Journal of the Indian Academy of Applied Psychology 32: 267–74. [Google Scholar]

- Sima, Violeta, I. G. Gheorghe, J. Subić, and D. Nancu. 2020. Influences of the Industry 4.0 Revolution on the Human Capital Development and Consumer Behavior: A Systematic Review. Sustainability 12: 4035. [Google Scholar] [CrossRef]

- Sveiby, Karl Erik. 1997. The Intangible Assets Monitor. Journal of Human Resource Costing and Accounting 2: 73–97. [Google Scholar] [CrossRef]

- Van Eck, Nees Jan, and Ludo Waltman. 2010. Software survey: VOSviewer, a computer program for bibliometric mapping. Scientometrics 84: 523–38. [Google Scholar] [CrossRef] [Green Version]

- Vulpe, Simona, and Andrei Crăciun. 2019. Silver surfers from a European perspective: Technology communication usage among European seniors. European Journal of Ageing 17: 125–34. [Google Scholar] [CrossRef] [PubMed]

- Wahab, Siti Norida, Salini Devi Rajendran, and Swee Pin Yeap. 2021. Upskilling and reskilling requirement in logistics and supply chain industry for the fourth industrial revolution. Scientific Journal of Logistics 17: 399–410. [Google Scholar]

- Wall, Anthony. 2007. The Measurement and Management of Intellectual Capital in the Public Sector. Public Management Review 7: 289–303. [Google Scholar] [CrossRef]

- Waltman, Ludo, Nees Jan van Eck, and Ed C.M. Noyons. 2010. A unified approach to mapping and clustering of bibliometric networks. Journal of Informetrics 4: 629–35. [Google Scholar] [CrossRef] [Green Version]

- Warwas, Izabela. 2017. Zarządzanie Wiekiem w Polsce—Stan i Perspektywy Rozwoju. Polityka Społeczna 4: 33–38. [Google Scholar]

- Wolor, Christian Wiradendi, Hera Khairunnisa, and Dedi Purwana. 2019. Implementation Talent Management to Improve Organization’s Performance in Indonesia To Fight Industrial Revolution 4.0. International Journal of Scientific and Technology Research 9: 1243–47. [Google Scholar]

- World Economic Forum. 2020. The Future of Jobs Report. October. Available online: https://www3.weforum.org/docs/WEF_Future_of_Jobs_2020.pdf (accessed on 5 October 2021).

- Wright, Patrick M., and Gary C. McMahan. 2011. Exploring human capital: Putting ‘human’ back into strategic human resource management. Human Resource Management Journal 21: 93–104. [Google Scholar] [CrossRef]

- Zhao, Qun, Pei-Hsuan Tsai, and Jin-Long Wang. 2019. Improving financial service innovation strategies for enhancing China’s banking industry competitive advantage during the fintech revolution: A Hybrid MCDM model. Sustainability 11: 1419. [Google Scholar] [CrossRef] [Green Version]

| EDU07 | FLEX07 | LMP07 | TEMCYC07 | OUT | n | incl | Cases |

|---|---|---|---|---|---|---|---|

| 0 | 1 | 1 | 0 | 1 | 4 | 1.00 | Belgium, Denmark, Ireland, Netherlands |

| 1 | 0 | 0 | 1 | 1 | 3 | 1.00 | Czech Republic, Estonia, Slovenia |

| 1 | 1 | 0 | 1 | 1 | 3 | 1.00 | Latvia, Hungary, Slovakia |

| 1 | 1 | 0 | 0 | 1 | 2 | 1.00 | Bulgaria, United Kingdom |

| 0 | 0 | 0 | 0 | 1 | 1 | 1.00 | Greece |

| 0 | 0 | 1 | 1 | 1 | 1 | 1.00 | Spain |

| 0 | 1 | 0 | 1 | 1 | 1 | 1.00 | Italy |

| 1 | 0 | 1 | 0 | 1 | 1 | 1.00 | Finland |

| 1 | 1 | 1 | 0 | 1 | 1 | 1.00 | Sweden |

| 0 | 0 | 1 | 0 | 0 | 3 | 0.67 | France, Luxembourg, Norway |

| 0 | 0 | 0 | 1 | 0 | 2 | 0.50 | Portugal, Romania |

| 1 | 1 | 1 | 1 | 0 | 2 | 0.00 | Austria, Poland |

| 1 | 0 | 1 | 1 | 0 | 1 | 0.00 | Germany |

| COD | Independent Variables or Conditions | Calibration |

|---|---|---|

| TECH | 1—Perception of technology’s impact | Technological as main driver of change in EU financial sector workplaces [1] = Yes; [0] = No |

| DIG | 2—Perception of digital skills’ importance | Importance of all the following digital skills: data analytics; software development and maintenance; digital marketing and social media; digital ICT [1] = Important/very important; [0] = Neutral; No importance |

| JOBSUS | 3—Perception of job substitution | Perception of the substitution of all the following Jobs: Back office Jobs; Accounting Jobs; Mortgage and/or financial advisors; Private bankers; Commercial manager [1] = Yes; [0] = No |

| MULT | 4—Perception of the need for multitask workers | Workers performing different tasks [1] = Yes; [0] = No |

| SOFT | 5—Perception of soft skills | Importance of all the following soft skills [1] = Yes; [0] = No |

| INWAY | 6—Introduction of new workers way | [1] = with a mentor or intergenerational group; [0] = other way |

| COD | Dependent Variable | Calibration |

|---|---|---|

| Y | 1—Perception of adopting measures to deal with age management and intergenerational solidarity | Technological as main driver of change in EU financial sector workplaces [1] = lack of faith or no need; [0] = Others (lack awareness, resources…etc.) |

| Case | TECH | DIG | JOBSUS | MULT | SOFT | INWAY | Y |

|---|---|---|---|---|---|---|---|

| 1 | 1 | 1 | 1 | 1 | 1 | 0 | 1 |

| 2 | 0 | 1 | 0 | 0 | 1 | 1 | 0 |

| 3 | 0 | 1 | 0 | 1 | 1 | 1 | 0 |

| 4 | 1 | 1 | 0 | 1 | 1 | 1 | 1 |

| 5 | 1 | 0 | 0 | 1 | 1 | 0 | 1 |

| 6 | 1 | 1 | 0 | 1 | 1 | 1 | 1 |

| 7 | 1 | 1 | 0 | 1 | 1 | 1 | 0 |

| 8 | 1 | 1 | 0 | 1 | 0 | 0 | 0 |

| CaseID | TECH | DIG | JOBSUS | MULT | SOFT | INWAY | Y |

|---|---|---|---|---|---|---|---|

| 1 | 1 | 1 | 1 | 1 | 1 | 0 | 1 |

| 4 | 1 | 1 | 0 | 1 | 1 | 1 | 1 |

| 5 | 1 | 0 | 0 | 1 | 1 | 0 | 1 |

| 6 | 1 | 1 | 0 | 1 | 1 | 1 | 1 |

| CaseID | TECH | DIG | JOBSUS | MULT | SOFT | INWAY | Y |

|---|---|---|---|---|---|---|---|

| 2 | 0 | 1 | 0 | 0 | 0 | 1 | 0 |

| 3 | 0 | 1 | 0 | 1 | 1 | 1 | 0 |

| 7 | 1 | 1 | 0 | 1 | 1 | 1 | 0 |

| 8 | 1 | 1 | 0 | 1 | 1 | 0 | 0 |

| CaseID | TECH | DIG | JOBSUS | MULT | SOFT | INWAY | Y |

|---|---|---|---|---|---|---|---|

| 2 | 0 | 1 | 0 | 0 | 1 | 1 | 0 |

| 3 | 0 | 1 | 0 | 1 | 1 | 1 | 0 |

| 5 | 1 | 0 | 0 | 1 | 1 | 0 | 1 |

| 8 | 1 | 1 | 0 | 1 | 0 | 0 | 0 |

| 4, 6, 7 | 1 | 1 | 0 | 1 | 1 | 1 | C |

| 1 | 1 | 1 | 1 | 1 | 1 | 0 | 1 |

| Outcome: 1 | |||||||

| # Implicants: 3 | |||||||

| dig | 0 | 5 | |||||

| JOBSUS | 0 | 1 | |||||

| SOFT*inway | 0 | 5, 1 | |||||

| # Solutions: 1 | |||||||

| SOFT*inway | |||||||

| Human Management Area | Tools and Actions Undertaken |

|---|---|

| Reskilling and upskilling |

|

| Redeployment |

|

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kuchciak, I.; Warwas, I. Designing a Roadmap for Human Resource Management in the Banking 4.0. J. Risk Financial Manag. 2021, 14, 615. https://doi.org/10.3390/jrfm14120615

Kuchciak I, Warwas I. Designing a Roadmap for Human Resource Management in the Banking 4.0. Journal of Risk and Financial Management. 2021; 14(12):615. https://doi.org/10.3390/jrfm14120615

Chicago/Turabian StyleKuchciak, Iwa, and Izabela Warwas. 2021. "Designing a Roadmap for Human Resource Management in the Banking 4.0" Journal of Risk and Financial Management 14, no. 12: 615. https://doi.org/10.3390/jrfm14120615

APA StyleKuchciak, I., & Warwas, I. (2021). Designing a Roadmap for Human Resource Management in the Banking 4.0. Journal of Risk and Financial Management, 14(12), 615. https://doi.org/10.3390/jrfm14120615