Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market

Abstract

:1. Introduction

- How are Swiss insurance companies addressing the opportunities offered by data-driven services and do they see a long-term impact on the structure of the industry?

- Which insurance-related services are Swiss customers interested in, and how do they value the information needed to provide them? How do these results differ by gender, age cohort, and current insurance provider?

- How open are Swiss insurance customers to sourcing insurance-related services from non-insurers?

- How well does the view of insurance experts match customer priorities?

2. Materials and Methods

3. Results

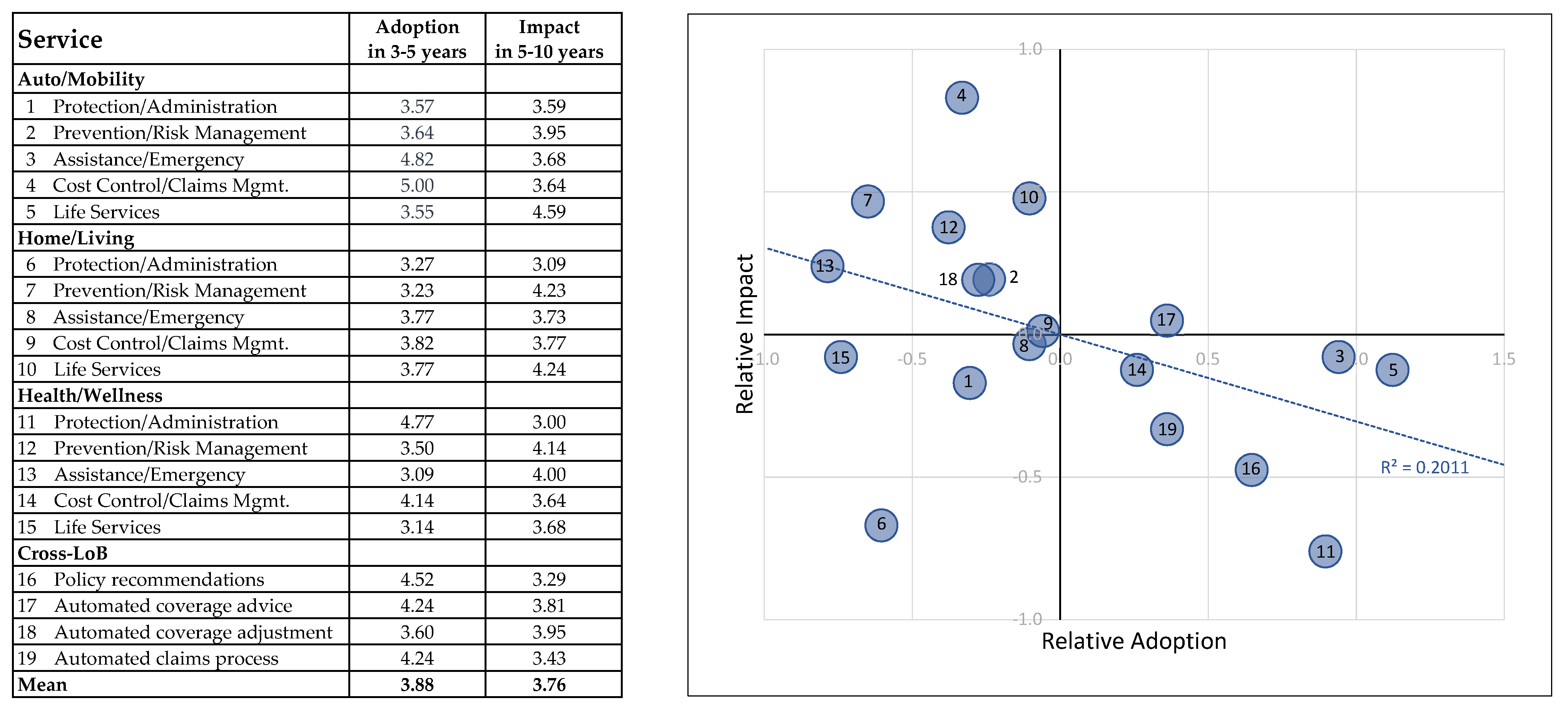

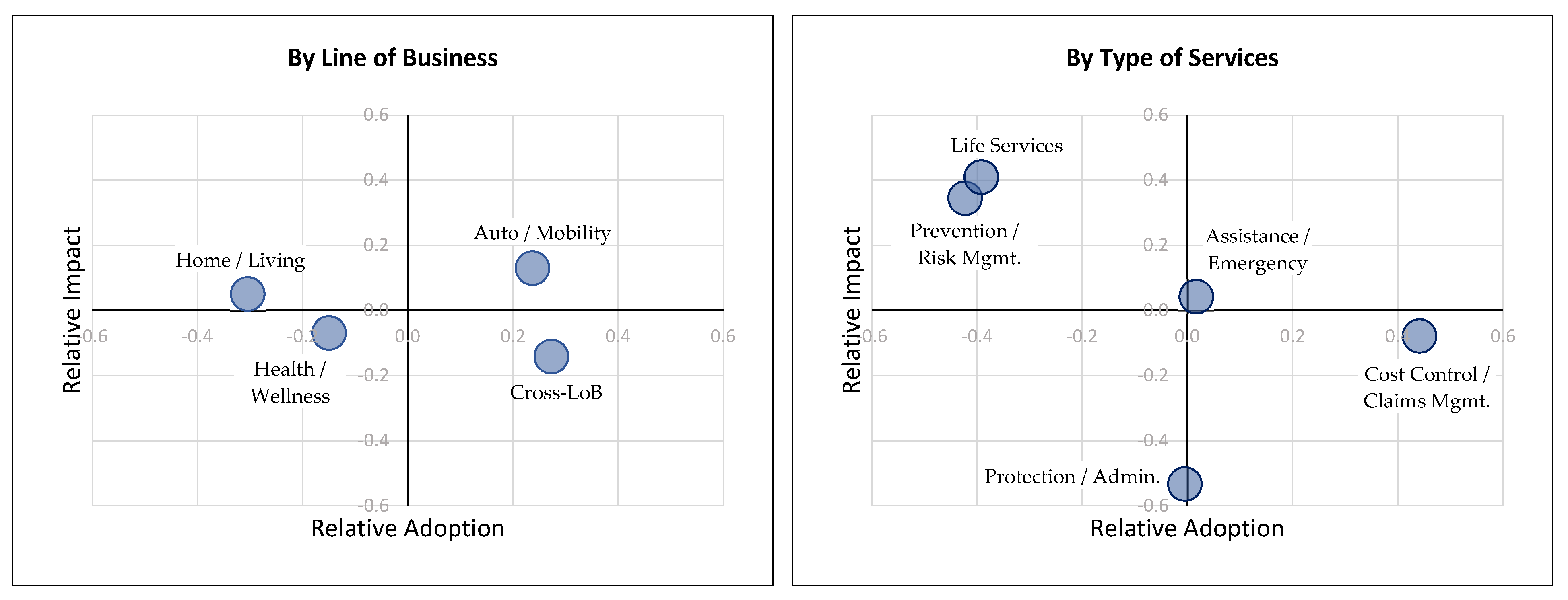

3.1. Expert Survey

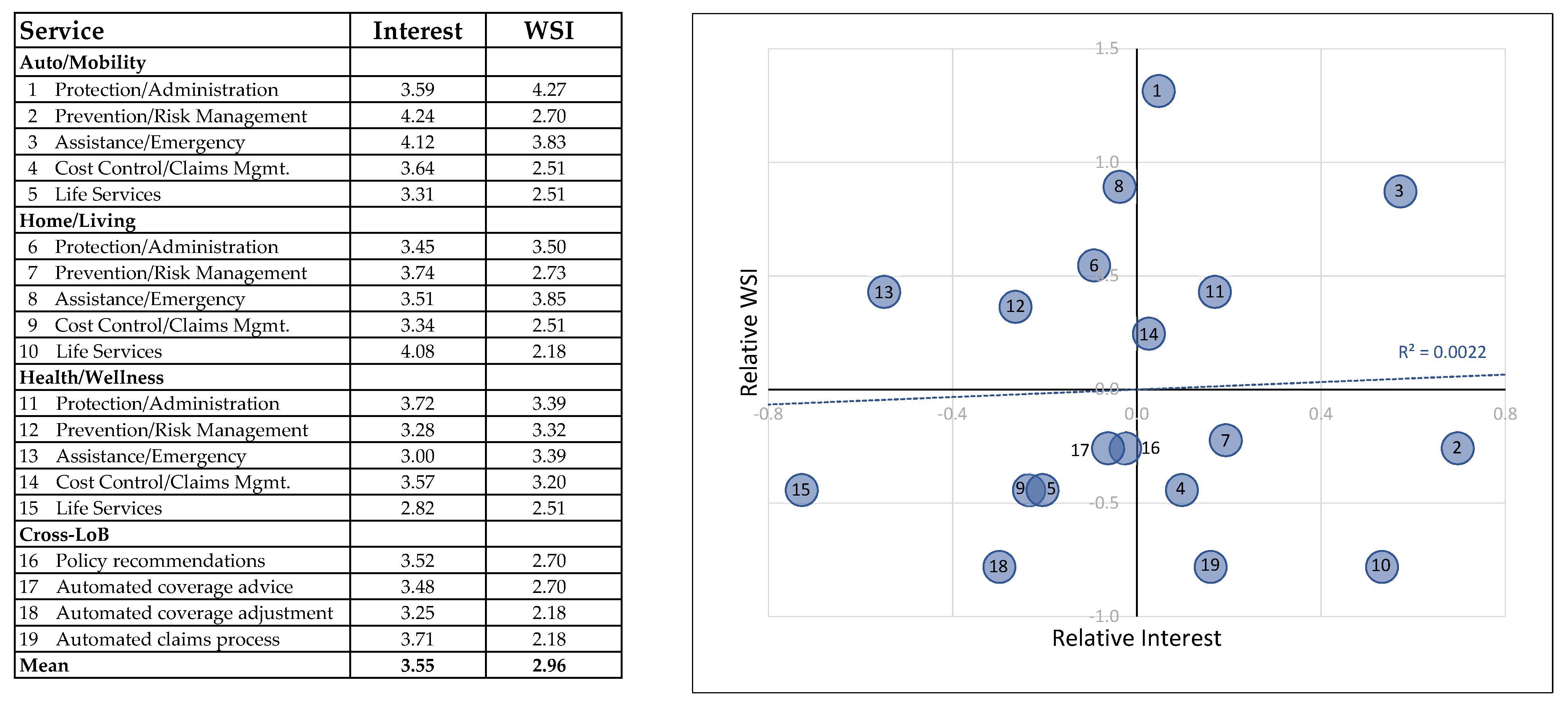

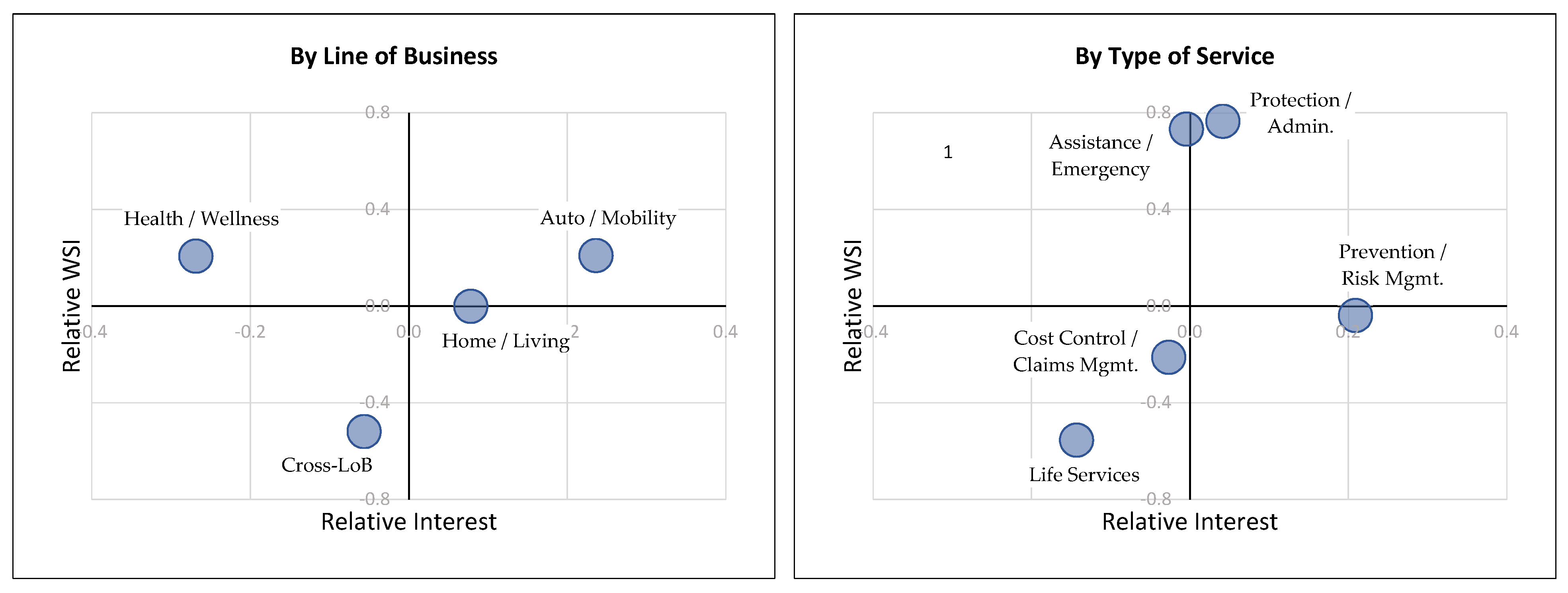

3.2. Customer Survey—Services

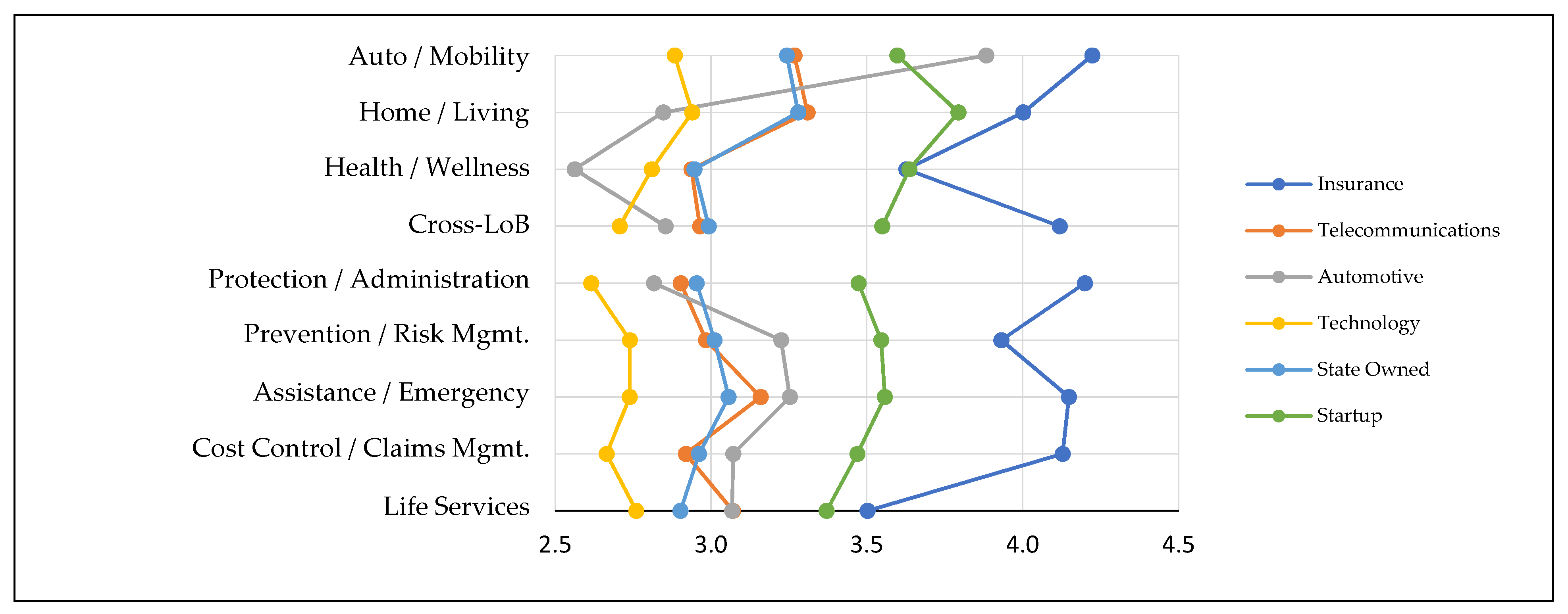

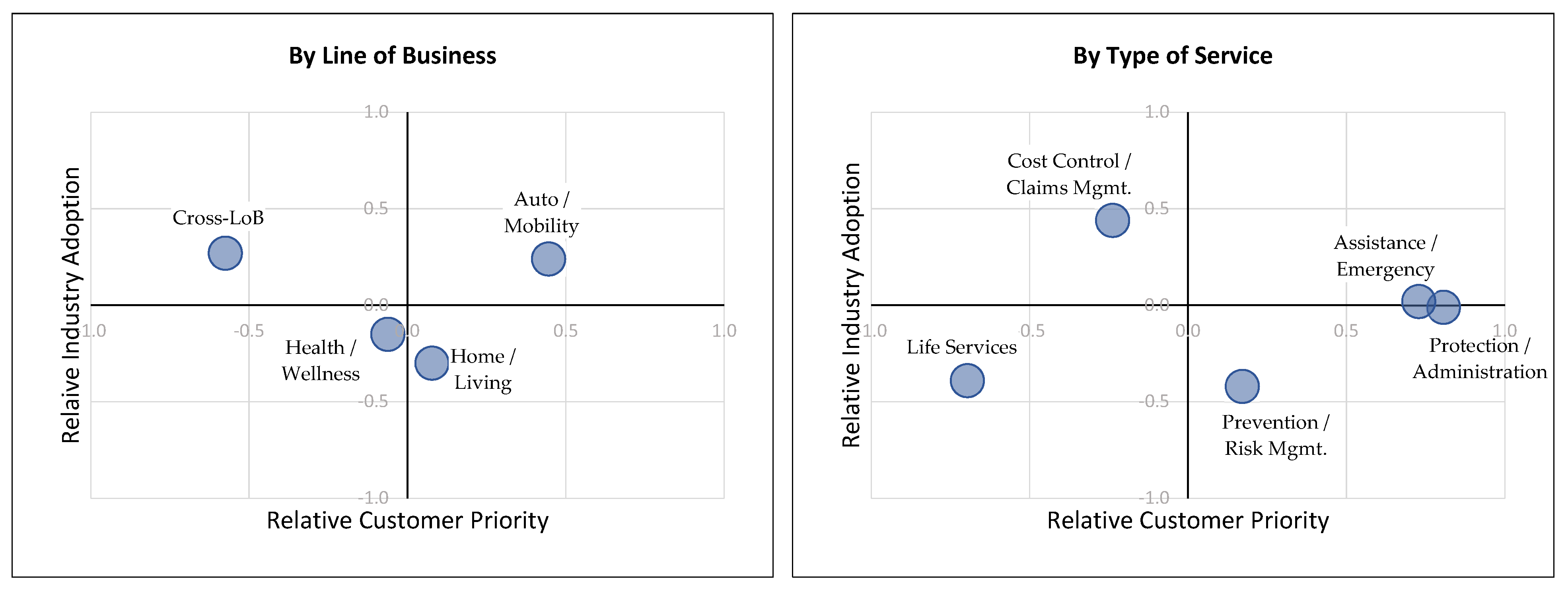

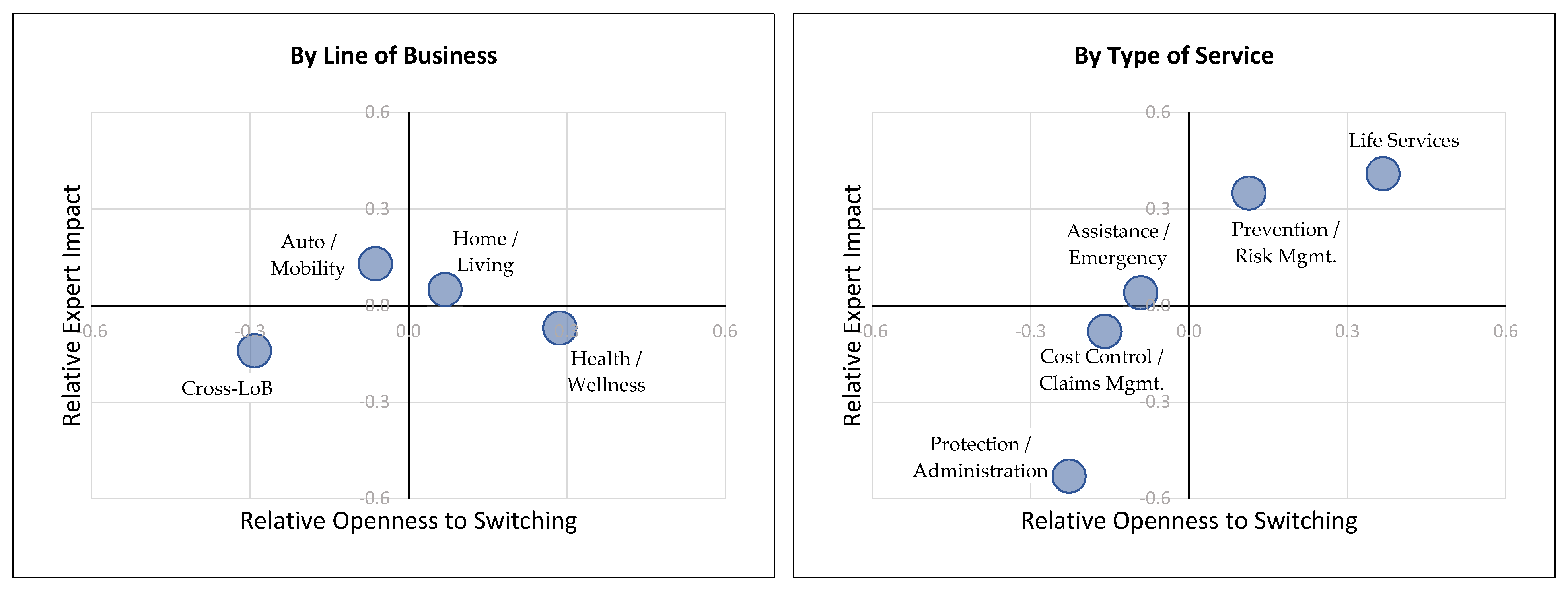

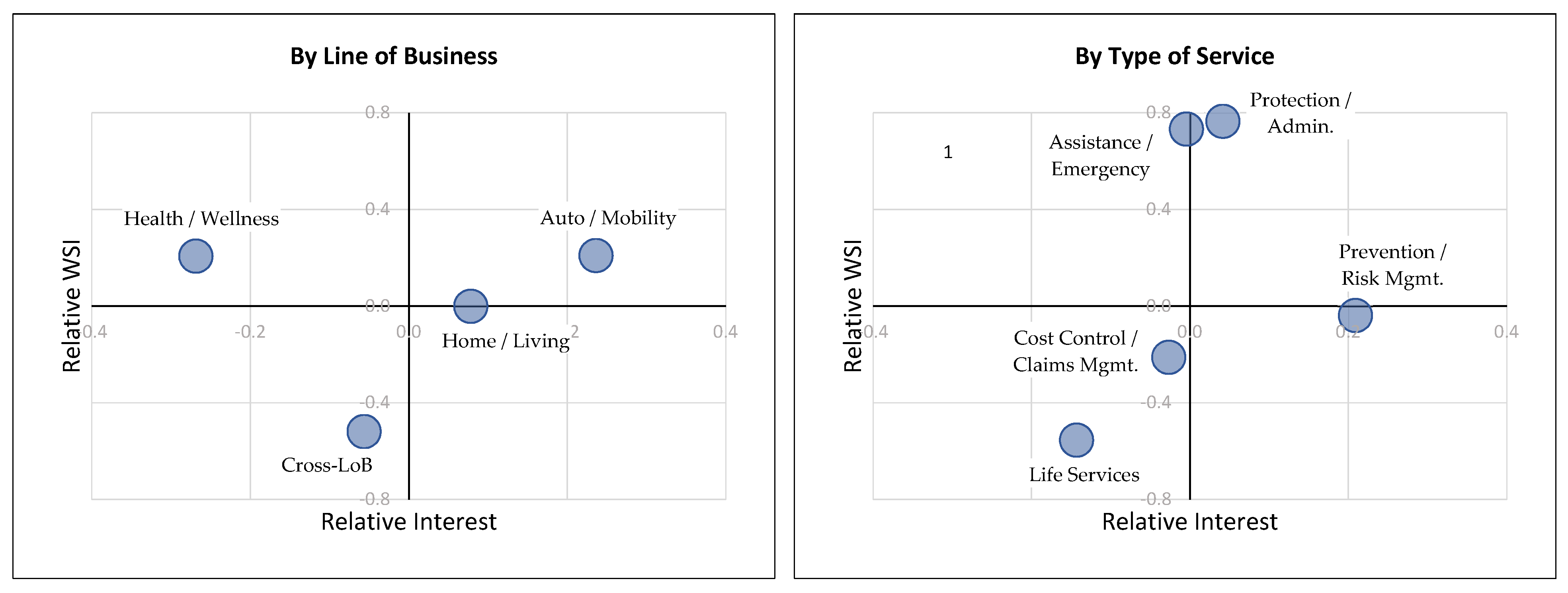

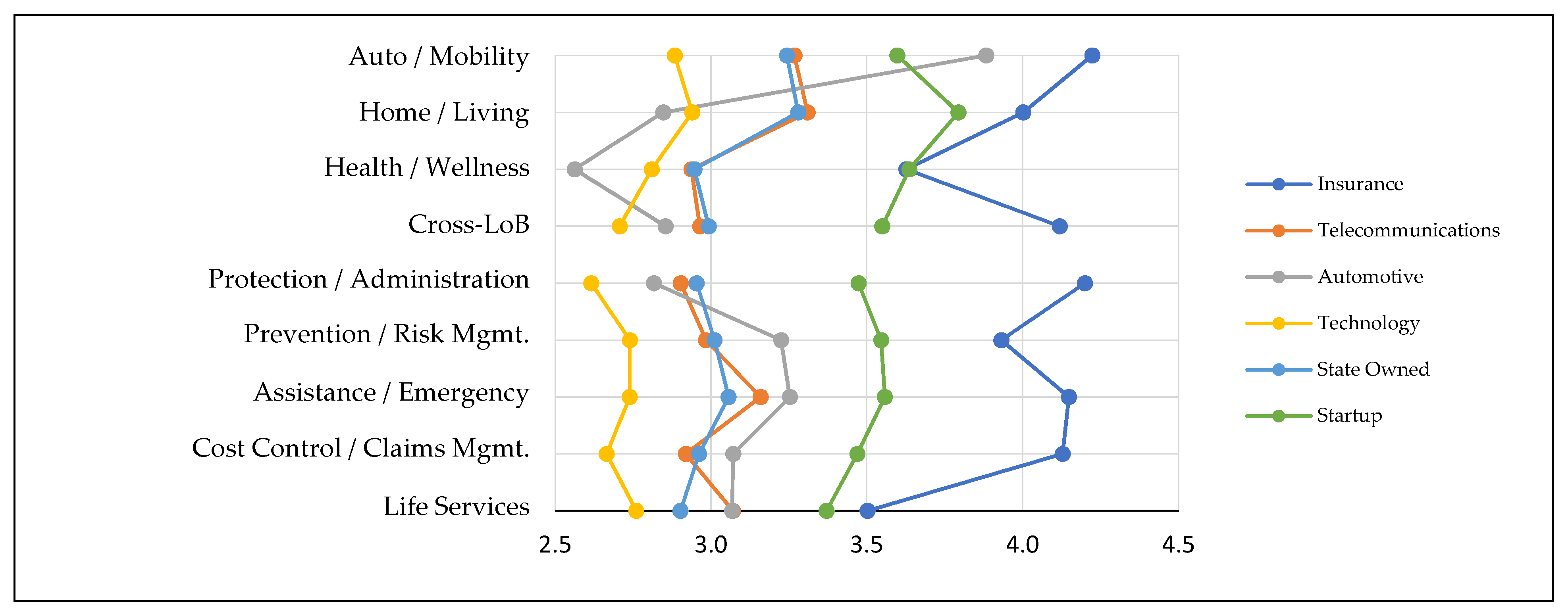

3.3. Customer Survey—Providers

3.4. Expert and Customer View

4. Discussion

- 1. How are Swiss insurance companies addressing the opportunities offered by data-driven services and do they see a long-term impact on the structure of the industry?

- 2. Which insurance-related services are Swiss customers interested in, and how do they value the information needed to provide them? How do these results differ by gender, age cohort, and current insurance provider?

- 3. How open are Swiss insurance customers to sourcing insurance-related services from non-insurers?

- 4. How well does the view of insurance experts match customer priorities?

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Service | Interest | Gender | M | F | p-Value | Age | 18–25 | 26–35 | 36–50 | >50 | p-Value |

|---|---|---|---|---|---|---|---|---|---|---|---|

| N= | 592 | 759 | N= | 331 | 369 | 342 | 312 | ||||

| Auto/Mobility | |||||||||||

| Protection/Administration | 3.59 | 3.71 | 3.51 | 0.02 | 3.66 | 3.54 | 3.73 | 3.45 | 0.11 | ||

| Prevention/Risk Management | 4.24 | 4.20 | 4.29 | 0.25 | 4.32 | 4.21 | 4.24 | 4.21 | 0.72 | ||

| Assistance/Emergency | 4.12 | 4.08 | 4.16 | 0.34 | 4.23 | 4.03 | 4.13 | 4.09 | 0.28 | ||

| Cost Control/Claims Management | 3.64 | 3.67 | 3.63 | 0.63 | 3.80 | 3.72 | 3.65 | 3.39 | <0.01 * | ||

| Life Services | 3.31 | 3.36 | 3.28 | 0.36 | 3.51 | 3.29 | 3.30 | 3.14 | 0.02 | ||

| Home/Living | |||||||||||

| Protection/Administration | 3.45 | 3.50 | 3.42 | 0.30 | 3.63 | 3.43 | 3.53 | 3.22 | <0.01 * | ||

| Prevention/Risk Management | 3.74 | 3.76 | 3.73 | 0.72 | 3.82 | 3.74 | 3.82 | 3.57 | 0.13 | ||

| Assistance/Emergency | 3.51 | 2.38 | 2.19 | 0.30 | 3.76 | 3.53 | 3.56 | 3.16 | <0.001 ** | ||

| Cost Control/Claims Management | 3.34 | 3.38 | 3.32 | 0.50 | 3.52 | 3.46 | 3.39 | 2.97 | <0.001 ** | ||

| Life Services | 4.08 | 3.98 | 4.16 | 0.02 | 4.19 | 4.02 | 4.09 | 4.02 | 0.34 | ||

| Health/Wellness | |||||||||||

| Protection/Administration | 3.72 | 3.72 | 3.72 | 0.98 | 3.90 | 3.85 | 3.67 | 3.40 | <0.001 ** | ||

| Prevention/Risk Management | 3.28 | 3.24 | 3.32 | 0.37 | 3.75 | 3.38 | 3.27 | 2.69 | <0.001 ** | ||

| Assistance/Emergency | 3.00 | 3.08 | 2.94 | 0.09 | 3.25 | 3.04 | 2.99 | 2.69 | <0.001 ** | ||

| Cost Control/Claims Management | 3.57 | 3.62 | 3.54 | 0.36 | 3.81 | 3.53 | 3.64 | 3.29 | <0.001 ** | ||

| Life Services | 2.82 | 2.92 | 2.74 | 0.04 | 3.27 | 2.91 | 2.82 | 2.23 | <0.001 ** | ||

| Cross-LoB | |||||||||||

| Policy recommendations | 3.52 | 3.56 | 3.49 | 0.44 | 3.62 | 3.55 | 3.64 | 3.25 | <0.01 * | ||

| Automated coverage advice | 3.48 | 3.52 | 3.46 | 0.49 | 3.74 | 3.43 | 3.55 | 3.21 | <0.001 ** | ||

| Automated coverage adjustment | 3.25 | 3.31 | 3.21 | 0.22 | 3.55 | 3.22 | 3.32 | 2.88 | <0.001 ** | ||

| Automated claims process | 3.71 | 3.72 | 3.70 | 0.80 | 3.87 | 3.79 | 3.77 | 3.37 | <0.001 ** |

| Information | WSI | Gender | M | F | p-Value | Age | 18–25 | 26–35 | 36–50 | >50 | p-Value |

|---|---|---|---|---|---|---|---|---|---|---|---|

| N= | 592 | 759 | N= | 331 | 369 | 342 | 312 | ||||

| New car purchase | 4.27 | 4.40 | 4.18 | 0.01 | 4.30 | 4.44 | 4.30 | 4.01 | <0.01 * | ||

| Vehicle information | 4.08 | 4.13 | 4.04 | 0.33 | 4.15 | 4.08 | 4.09 | 3.97 | 0.59 | ||

| Crash sensor data | 3.83 | 3.95 | 3.74 | 0.02 | 3.80 | 3.96 | 3.85 | 3.68 | 0.21 | ||

| Daily schedule | 2.51 | 2.63 | 2.42 | 0.02 | 2.72 | 2.52 | 2.42 | 2.39 | 0.05 | ||

| Current location and history | 2.70 | 2.88 | 2.56 | <0.001 ** | 2.69 | 2.51 | 2.73 | 2.90 | 0.02 | ||

| Purchasing information | 3.50 | 3.48 | 3.53 | 0.57 | 3.63 | 3.57 | 3.42 | 3.36 | 0.16 | ||

| Emergency sensors in the house | 3.85 | 4.00 | 3.73 | <0.01 * | 3.87 | 3.97 | 3.82 | 3.72 | 0.28 | ||

| Smart home data w/o camera | 2.73 | 2.85 | 2.64 | 0.03 | 2.87 | 2.67 | 2.73 | 2.67 | 0.37 | ||

| Smart home data w/camera | 2.18 | 2.35 | 2.05 | <0.001 ** | 2.26 | 2.17 | 2.19 | 2.08 | 0.59 | ||

| Sports: training plan and activities | 3.32 | 3.39 | 3.27 | 0.21 | 3.77 | 3.42 | 3.13 | 2.93 | <0.001 ** | ||

| Health monitoring | 3.39 | 3.43 | 3.35 | 0.40 | 3.80 | 3.46 | 3.18 | 3.08 | <0.001 ** | ||

| Chronic conditions | 3.20 | 3.31 | 3.13 | 0.06 | 3.72 | 3.20 | 2.97 | 2.91 | <0.001 ** |

References

- Adrodegari, Federico, and Nicola Saccani. 2017. Business models for the service transformation of industrial firms. The Service Industries Journal 37: 57–83. [Google Scholar] [CrossRef]

- Arisov, Elisabeth, Johannes Becker, Matthias Erny, and Angela Zeier Röschmann. 2019. Individualisierte Versicherungslösungen in einer Digitalen Welt. Winterthur: ZHAW School of Management and Law. [Google Scholar] [CrossRef]

- Baecke, Philippe, and Lorenzo Bocca. 2017. The Value of Vehicle Telematics Data in Insurance Risk Selection Processes. Decision Support Systems 98: 69–79. [Google Scholar] [CrossRef]

- Bain & Company. 2017. Building Connections—And Profits—With Ecosystem Services. In Customer Behavior and Loyalty in Insurance: Global Edition 2017. Boston: Bain & Company. [Google Scholar]

- Bain & Company. 2018. Customers Know What They Want. Are Insurers Listening? In Customer Behavior and Loyalty in Insurance: Global Edition 2018. Boston: Bain & Company. [Google Scholar]

- Beer, Simone, Alexander Braun, Pascal Bühler, Martin Eling, Peter Maas, Lukas Reichel, Matthias Rüfenacht, Philipp Schaper, Hato Schmeiser, Florian Schreiber, and et al. 2017. Assekuranz 2025: Quo Vadis? St. Gallen: Verlag Institut für Versicherungswirtschaft der Universität St. Gallen. [Google Scholar]

- Borna, Shaheen, and Stephen Avila. 1999. Genetic Information: Consumers’ Right to Privacy Versus Insurance Companies’ Right to Know a Public Opinion Survey. Journal of Business Ethics 19: 355–62. [Google Scholar] [CrossRef]

- Bouwman, Harry, Shahrokh Nikou, Francisco J. Molina-Castillo, and Mark de Reuver. 2018. The Impact of Digitalization on Business Models. Digital Policy, Regulation and Governance 20: 105–24. [Google Scholar] [CrossRef]

- Buehler, Pascal, and Peter Maas. 2016. Kunden Transformieren die Versicherungsmärkte|Digitale Transformation im Unternehmen Gestalten. Munich: Carl Hanser Verlag, pp. 99–113. [Google Scholar]

- Cappiello, Antonella. 2020. The Digital (R)evolution of Insurance Business Models. American Journal of Economics and Business Administration 1: 13. [Google Scholar] [CrossRef]

- Cardon, James H., and Igal Hendel. 2001. Asymmetric Information in Health Insurance: Evidence from the National Medical Expenditure Survey. The RAND Journal of Economics 32: 408–27. [Google Scholar] [CrossRef]

- Culnan, Mary J., and Pamela K. Armstrong. 1999. Information Privacy Concerns, Procedural Fairness, and Impersonal Trust: An Empirical Investigation. Organization Science 10: 104–15. [Google Scholar] [CrossRef]

- Deraëd, Pierre, and Julia Henry. 2012. Was Versicherungskunden Wirklich Wollen. Zurich: Bain & Company. [Google Scholar]

- Eling, Martin, and Martin Lehmann. 2018. The Impact of Digitalization on the Insurance Value Chain and the Insurability of Risks. The Geneva Papers 43: 359–96. [Google Scholar] [CrossRef]

- Garth, Denise, and Glenn Westlake. 2018. Digital Insurance 2.0: Playbooks for P&C Insurers to Win in the Digital Age. New York: Majesco, Available online: https://www.majesco.com/resources/digital-insurance-2-playbooks-for-pc-insurers/data (accessed on 23 June 2018).

- Kehr, Flavius, Daniel Wentzel, and Peter Mayer. 2013. Rethinking the Privacy Calculus: On the Role of Dispositional Factors and Affect. Presented at the Thirty Fourth International Conference on Information Systems, Milan, Italy, December 15–18. [Google Scholar]

- Kotalakidis, Nikos, Henrik Naujoks, and Florian Mueller. 2016. Digitalisierung der Versicherungswirtschaft: Die 18-Milliarden-Chance. Munich and Zurich: Bain & Company. [Google Scholar]

- Manyika, James, Michael Chui, Brad Brown, Jacques Bughin, Richard Dobbs, Charles Roxburgh, and Angela Hung Byers. 2011. Big Data, the New Frontier for Innovation, Competition and Productivity. McKinsey Global Institute. [Google Scholar]

- Metzger, Miriam J. 2004. Privacy, Trust, and Disclosure: Exploring Barriers to Electronic Commerce. Journal of Computer-Mediated Communication 9: JCMC942. [Google Scholar] [CrossRef]

- Milne, George R., and Mary Ellen Gordon. 1993. Direct Mail Privacy-Efficiency Trade-offs within an Implied Social Contract Framework. Journal of Public Policy & Marketing 12: 206–15. [Google Scholar]

- Neely, Andy. 2008. Exploring the financial consequences of the servitization in manufacturing. Operations Management Research 1: 103–18. [Google Scholar] [CrossRef] [Green Version]

- Normann, Richard. 2001. Service Management: Strategy and Leadership in Service Business, 3rd ed. New York: Wiley & Sons, p. 256. ISBN 10: 0471494399. [Google Scholar]

- Opresnik, David, and Marco Taisch. 2015. The value of Big Data in servitization. International Journal of Production Economics 165: 174–84. [Google Scholar] [CrossRef]

- Pugnetti, Carlo, and Sandra Elmer. 2020. Self-Assessment of Driving Style and the Willingness to Share Personal Information. Journal of Risk and Financial Management 13: 53. [Google Scholar] [CrossRef] [Green Version]

- Rothschild, Michael, and Joseph Stiglitz. 1976. Equilibrium in Competitive Insurance Markets: An Essay on the Economics of Imperfect Information. Quarterly Journal of Economics 90: 629–49. [Google Scholar] [CrossRef] [Green Version]

- Simpson, Thomas W. 2012. What Is Trust? Pacific Philosophical Quarterly 93: 550–69. [Google Scholar] [CrossRef]

- Smith, H. Jeff, Tamara Dinev, and Heng Xu. 2011. Information Privacy Research: An Interdisciplinary Review. MIS Quarterly 35: 989–1015. [Google Scholar] [CrossRef] [Green Version]

- Steiner, Philipp Hendrik, and Peter Maas. 2018. When customers are willing to disclose information in the insurance industry: A multi-group analysis comparing ten countries. International Journal of Bank Marketing 36: 1015–33. [Google Scholar] [CrossRef]

- Stone, Eugene F., and Dianna L. Stone. 1990. Privacy in Organizations: Theoretical Issues, Research Findings, and Protection Mechanisms. Research in Personnel and Human Resources Management 8: 349–411. [Google Scholar]

- The Economist. 2017. The World’s Most Valuable Resource Is No Longer Oil, But Data. Available online: https://www.economist.com/leaders/2017/05/06/the-worlds-most-valuable-resource-is-no-longer-oil-but-data (accessed on 14 June 2020).

- Vandermerwe, Sandra, and Juan Rada. 1988. Servitization of business: Adding value by adding services. European Management Journal 6: 314–24. [Google Scholar] [CrossRef]

- Wamba, Samuel Fosso, Shahriar Akter, Andrew James Edwards, Geoffrey Chopin, and Denis Gnanzou. 2015. How ‘big data’ can make big impact: Findings from a systematic review and a longitudinal case study. International Journal of Production Economics 165: 234–46. [Google Scholar] [CrossRef]

- Zolnowski, Andreas, Towe Christiansen, and Jan Gudat. 2016. Business Model Transformation Patterns of Data-Driven Innovations. Research Papers, 146. Available online: https://aisel.aisnet.org/ecis2016_rp/146 (accessed on 14 June 2020).

| Industry Perspective Expert Survey | Market Perspective Customer Survey | |

|---|---|---|

| Evolution of services | Adoption in 3–5 years | Interest vs. perceived “cost” of information needed |

| Impact of services | Impact in 5–10 years | Provider preference |

| Protection/ Administration | Prevention/ Risk Mgmt. | Assistance/ Emergency | Cost Control/ Claims Mgmt. | Life Services 1 | |

|---|---|---|---|---|---|

| Auto/Mobility | Automated policy changes based on new car purchase | Real-time warnings/recommendations while driving | Automated emergency call triggered in case of accident | Coordination of repair garage, replacement car, etc. | Location-based enabled services such as wash service, pickup, etc. |

| Home/Living | Policy updates after new construction/repairs | Automatic shutoff of water, gas, etc., in case of emergency | Dispatch contractor if flooding detected | Automated scheduling of inspections, repairs, etc. | Elder care—notification if bed not used/fridge not opened for 12 h |

| Health/Wellness | Automated processing of medical bills | Automated nutrition recommendations based on health monitoring | Automated scheduling of doctor visit based on critical health stats | Access to specialized provider network for chronic health conditions | Scheduling gym time when on travel in a new location based on calendar |

| Other/Cross-LoB | Policy analysis and recommendation for changes | Individualized, automated coverage advice | Automated coverage adjustment/dynamic insurance adjustments | Automated coverage adjustment/dynamic insurance adjustments | |

| Research Question | Approach | |

|---|---|---|

| 1. | How are Swiss insurance companies addressing the opportunities offered by data-driven services and do they see a long-term impact on the structure of the industry? | Expert survey: adoption in 3–5 years and impact in 5–10 years of each service. |

| 2. | Which insurance-related services are Swiss customers interested in, and how do they value the information needed to provide them? How do these results differ by gender, age cohort, and current insurance provider? | Customer survey: interest in purchasing service and perceived value of the information required to provide the service. Analysis by gender, age cohort and named insurance provider. |

| 3. | How open are Swiss insurance customers to sourcing insurance-related services from non-insurers? | Customer survey: preference for provider by industry for each service. |

| 4. | How well does the view of insurance experts match customer priorities? | Evolution of services: comparison of customer interest in purchasing and the perceived cost of information by service vs. expert view of adoption in 3–5 years. Impact of services: comparison of customer preference in sourcing from non-insurance player vs. expert view of impact in 5–10 years. |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pugnetti, C.; Seitz, M. Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market. J. Risk Financial Manag. 2021, 14, 227. https://doi.org/10.3390/jrfm14050227

Pugnetti C, Seitz M. Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market. Journal of Risk and Financial Management. 2021; 14(5):227. https://doi.org/10.3390/jrfm14050227

Chicago/Turabian StylePugnetti, Carlo, and Mischa Seitz. 2021. "Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market" Journal of Risk and Financial Management 14, no. 5: 227. https://doi.org/10.3390/jrfm14050227

APA StylePugnetti, C., & Seitz, M. (2021). Data-Driven Services in Insurance: Potential Evolution and Impact in the Swiss Market. Journal of Risk and Financial Management, 14(5), 227. https://doi.org/10.3390/jrfm14050227