1. Introduction

The significance of financial development and its function in the intermediation of finance has been contentious about, as it has played a major part in economic progress over the last few decades and has assumed a prominent place in financial development. Many scholars have proposed that financial development importantly stimulates economic progress by promoting industries, investments, the distribution of loanable funds, and the accumulation of capital (

Ahmad et al. 2020b). In fact, they claimed that emerging countries require it to obtain well-developed capital markets. On the other hand,

Khalikov (

2017) used economic analysis to claim that financial development and economic progress obtain immense traction from each other. Yet, the nature of their interaction has remained inconclusive depending on the type of models, data, and empirical methodologies used to assess it.

There are several drivers of non-savings and credit markets in developed countries. The allocation of sufficient capital depends primarily on a country’s economic progress and success in the production cycle, as well as the fair distribution of income among the persons in that specific society (

Ahmad et al. 2021e). As a further argument,

Phong et al. (

2018) claimed that real national gross domestic product (GDP), overall country population, and per capita output are significant in the long-term economic progress cycle. Additionally,

Khairutdinov et al. (

2018) stated that economic progress is a trend that is continuously affected by a country’s competitiveness and that increases over a sustained period. Many researchers have addressed the unpredictability of increasing concentrations within diverse states. Capital and labor are the main factors that trigger differences between growth rates, and their impacts are attributable to differences in opportunities (

Alvarez–Cuadrado et al. 2017). In the Pakistani context, several contributing factors have caused a low level of economic progress. These factors involve inflation levels, export reductions, foreign loans, service volatility, weak social asset management, regulatory scenarios, and the instability prevalent in the country (

Komal and Abbas 2015). Likewise, the role of commercial liberalization in macroeconomic performances in Pakistan was reported by

Chaudhry et al. (

2012). Along these lines,

Evan et al. (

2002) analyzed 82 countries and demonstrated that development relied on income distribution. They also stressed the complementarities of financial and capital development.

A widely discussed topic in the academic literature is the correlation between financial stability and economic progress. A substantial amount of analytical literature argues that economic progress is driven by financial stability (

Ibrahim and Alagidede 2018). Those studies considered that an appropriately planned financial framework should be a requirement for a high level of economic progress. The pioneering research (

Schumpeter 1911) in this area primarily proposed the linkage between financial development and economic progress. Schumpeter claimed that economic prosperity relies on a healthy financial system, whereas the supporters of economic progress argued that financial structures are essentially required for urbanization, a view which

Turok (

2016) and

Wu et al. (

2019) also endorsed. It was concluded that financial markets that are more liberal accelerated economic progress, whereas conservative financial markets slowed economic progress. Consequently,

Carroll and Jarvis (

2015) and

Spolander et al. (

2016) advocated that to sustain economic progress, implementing liberal policies is important.

In the late 1980s and early 1990s, it was often suggested by the contemporary growth theories that financial progress is a key determining factor of economic progress (

Nelson 1998). The theorists of economic progress concluded that financial progress tends to increase the productivity of capital allotment, increase equity risk management, efficiently diversify investments of creditors, and boost the efficacy of investment ventures (

Ahmad et al. 2021c). Such factors can enhance the competitiveness of capital, which positively affects economic progress (

Soekapdjo et al. 2020). On the other side,

Pece et al. (

2015) argued that theoretical debates overemphasize capital markets’ role in economic progress. Additionally,

Pearson and Elson (

2015) argued that in the absence of adequate laws and guidelines, finance would have negative consequences on social security and economic progress.

From an empirical perspective, finance and development analysis generally shows that countries with improved banking and financial markets are growing rapidly. An improved financial sector makes it easier for businesses to avoid funding constraints, allowing for a smoother investment flow and faster expansion (

Ahmad et al. 2021b). However, overall, the main criticism of econometric research on financial development and economic progress is that it is unable to endorse or disprove theoretical models. This is because they are unable to quantify the principles that can be derived from hypothetical modeling (

Alvarado et al. 2021). Similarly,

Dellink et al. (

2017) attempted to alleviate this issue by employing various financial stability indicators and concluded that financial stability predicts long-term growth.

The literature has introduced the bilateral correlation between financial development and growth. In

Greenwood and Jovanovic (

1990)’s model, on the one hand, financial institutions encourage financial development by efficient capital distribution, even though it involves a cost for accessing them. On the other hand, urbanization makes it comparatively cheaper to enter financial intermediation. This scenario would allow more agents to participate, thus, having positive second-order effects on the expansion (

Irfan et al. 2020). Both the sum of savings available for investment and its returns do matter for economic progress. Additionally, the advancement of financial intermediation helps to gain a better return on invested capital, which consequently feeds on economic progress (

Ahmad et al. 2020a). There is broad and rather diverse section of the analytical literature on the connections between financial and economic expansion. Despite the enormous amount of the literature that focused on this connection (using a diverse range of estimation techniques), no unique consensus has been developed on this connection, which leaves ambiguity.

Researchers have tried several alternatives to rectify estimation issues. For instance,

Boldeanu and Tache (

2016) have designed two measures to assess the financial sector component, i.e., the financial system liabilities as a part of GDP and the percentage of funds granted to corporations.

Claessens et al. (

2018) have employed two indicators of the financial system’s performance. They first assessed the share of overall credit, directly issued by banks in the private sector rather than the central bank. In contrast, the second estimated the component of overall funds available to private corporations. These two indicators assume that a market with more corporate credit and investment in the private sector should provide a more effective allocation of foreign funding. A bank in the corporate sector, aiming to maximize earnings, would be more inclined to finance profitable infrastructure ventures than a government bank. The latter aims to meet specific guidelines for determining loans. It has been further argued that the level of financial depth predicts long-term economic progress.

Feldstein (

2017) affirmed an economically robust and statistically noteworthy association of financial growth with real GDP growth per capita and overall productivity. However, the positive moderating influence of financial growth on the physical accumulation of capital, and the rate of personal saving, remained uncertain in their analysis.

Regarding causality, the top of the line is the “allow to disagree”, as variations in a long-term correlation, and short-term association or in the non-linearity of the correlation itself, is often taken up in various analyses, which makes it difficult to draw a conclusive decision regarding which course of causality to take. Nevertheless, with a 17-country regression,

Loayza and Ranciere (

2006) found an optimistic long-term correlation among financial intermediation and output development interacts with mainly a short-term negative interaction. Additionally, with a threshold regression,

Deidda and Fattouh (

2002) found a significant positive association between the degree of financial depth and economic progress for wealthier countries and no meaningful association for poorer countries, which is compatible with the non-monotonic correlation, as suggested in the study.

This study aims to assess the impact of economic openness and financial development on economic progress in Pakistan during 1975–2018. Past research mostly used panel data analysis, overlooking the country-specific characteristics of the stated impacts. For policymaking, a pooled panel data analysis is not very helpful, since it gives a general idea regarding the relationship among variables, disregarding the individual country’s particular situation of variables under investigation. While resolving a specific problem, studies that have focused on a particular country could provide more helpful insights. This study is an excellent addition to the literature, as it focuses on country-specific features of an emerging economy that would assist in practical policymaking. This research included the variable of financial development to address the impact of the fast-developing financial sector on economic progress. The inclusion of economic openness benefits the study, as Pakistan has open economy-oriented policies, providing the opportunity to earn on exports to boost economic progress. The Autoregressive Distributed Lag (ARDL) cointegration of

Pesaran et al. (

2001) is used in this study for data analysis purposes. Granger causality is applied to the causal direction among those variables, since it is a practical approach for series with mixed integration order.

This study is divided into the following sections: The literature review regarding the finance–trade–growth nexus is described in

Section 2. Description of data, model, and econometric methodology is in

Section 3. Next,

Section 4 exhibits the econometric findings of this study. Finally,

Section 5 contains the conclusion and recommendations for policymakers.

2. Review of the Literature

The varied economic literature has been drawn up on the avenues through which the development of the financial sector influences the real economic field’s development cycle.

Lane and Milesi-Ferretti (

2018) put forward their arguments that financial progress is a critical component of a nation’s rapid economic progress. The exploration of the financial growth nexus owes the concrete foundation of Schumpeterian Growth Theory. The literature advocates two essential arguments while linking the progress of the financial sector and economic progress.

Haiss and Sümegi (

2008) posed the first argument in their study that the intensity of the financial sector’s relationship with the real economic industry goes beyond a shift in the savings rate. There is no indication of a persistent long-term correlation between the increase in physical capital accumulation and real economic progress in the financial growth literature. Hence, while evaluating the technical help of financial–economic nexus, one can look for specific theories that explain resource allocation decision-making that encourages productive growth.

The second argument focuses on two obscurities about the partnership between the emergence of financial sector structures for productive resource distribution and the rise in the real economy (

Irfan et al. 2019b;

Ibrahim and Alagidede 2018). If higher returns are anticipated, the savings rate may react uncertainly and increase or decrease due to higher income and replacement impact returns. In the case of a lower risk and productive distribution of resources, the reverse can occur regardless of the increase in the savings rate. Saving rates will decline due to effective resource management and the reduction in risk resulting from financial reforms (

DeAngelo and Stulz 2015).

The spectrum of financial intermediaries’ services includes savings and resource allocation, investment strategy assessment, risk control by providing diversified investment choices, corporate governance by controlling companies and executives, and promoting the transaction phase. Consequently, these facilities contribute to innovation and technical improvements in industrial processes (

Ahmad et al. 2021d). Throughout the sense of Schumpeter’s statements of positive relations, debates were arising about the financial-growth correlation (

Rohde and Breuer 2016). Nevertheless, some empirical evidence has been given to prove the positive correlation between financial innovations and progress.

In the pioneering work of Schumpeter (in the context of a developed economy), it was claimed that in situations where a revolutionary invention triggers the substitution of old business with a new industry, a cycle called “Creative Destruction”, in which all downturns and bubbles cannot be avoided or corrected (

Kılınç et al. 2017). In light of these findings, it can be concluded that higher-level financial progress contributes to productivity growth. In the view of a cross-country evaluation of the difference between the poorest and wealthiest countries, it is assumed that if financial progress is pursued above the threshold point, the divergent dynamics between the countries’ growth rates do not continue over the long term (

Aghion et al. 2005).

The empirical background on the nexus between trade openness and economic progress has its roots in Neoclassical Growth Theory. It is assumed that the determination of emerging economies to associate their domestic economies with different countries is influenced by economic openness. Considering this assumption,

Shahbaz et al. (

2013a,

2013b;

Shahbaz 2012) established a hypothesis that there is a correlation between economic openness and economic progress, which results in growth and profitability. A bilateral correlation between international trade and economic progress was reported by (

Omri et al. 2015), whereas (

Ahmad et al. 2020c) demonstrated a bilateral causality between financial prosperity, and economic openness. The discussion regarding the correlation between economic openness and economic progress ranges from variance in economic openness indexing to utilization of cross-sectional research and the correlational directions (

Keho 2017). Additionally,

Truby (

2018) argued that other scholars have analyzed that the interactions between the two do not comprehensively explain economic structures and trade policy choices. In comparison,

Zahonogo (

2017) claimed that trade and economic progress have a beneficial relationship.

Country-specific studies show contradictory facts. For instance,

Uddin et al. (

2013) employed Cobb-Douglas functional form, matrix-based ARDL cointegration, and structural break cointegration to recognize the long-term association between the variables of interest in Kenya’s context. A positive association was uncovered between financial performance and economic progress. Likewise, the study by

Odhiambo (

2010) applied a Granger causality test between economic output and money supply. The authors recognized a bilateral relationship among financial development indices through the money supply ratio to economic progress and GDP.

Odeniran et al. (

2010) found economic progress boost in response to the stock market turnover. However, the correlation was not strong in the long-term, with causality from economic progress to financial performance.

Bojanic (

2012) employed cointegrated multiple linear regression models, the Granger regression model, and the error correction models to analyze Bolivian data from 1940–2010. The association among economic progress, financial stability, and exchange accessibility was evaluated, and revealed long-term stability among the study variables. Furthermore, Granger’s unilateral causality was identified, varying from financial stability metrics and economic openness to economic progress.

During the last three decades, the association between economic openness and economic progress has gained substantial consideration in both (i.e., conceptual and empirical) areas of the literature; though, there is no evidence regarding whether economic progress is stimulated by economic openness. According to the theory of comparative advantage, when a nation chooses to compete with another country, the latter must manufacture products on which it has a competitive advantage. It concentrates on the field where it has more substantial component capabilities and manufactures commodities on a greater level (

Irfan et al. 2019a). Consequently, this sector’s productivity and exports will increase, which would improve overall economic progress (

Iqbal et al. 2021). Many economists have further expanded the theory.

Xuefeng and Yaşar (

2016) claim that globalization promotes consolidation in industries with economies of scale, optimizing long-term output and productivity. As a consequence of the international proliferation of emerging technology, new endogenous development mechanisms describe a favorable association between economic openness and economic progress.

An economy with such greater openness has a more substantial potential to leverage advanced economies’ technologies. This ability helps it develop more quickly than a country with less economic openness. The importance of imitation factors in the relationship of trade and growth is also indicated by (

Musila and Yiheyis 2015). If the emerging economies have fewer innovation costs than the developed world, they are expected to grow higher than the developed world. Thus, the process towards convergence will take effect. It is suggested by both arguments that countries that are in the process of development gain a lot from the foreign exchange with mature technological countries. While several other statements have been made, there may be some situations when access to markets may be unfavorable for economic progress, such as when the country does not find it necessary to use research and development for its operation (

Almeida and Fernandes 2008). The structure of trade also has an impact on product development (

Hausmann 2016). Quick learning of global technologies and adapting to the local climate also depends on whether a country profits from the international exchange (

Elavarasan et al. 2021).

The literature (

Sun et al. 2019) has indicated a correlation between economic openness and economic progress.

Rassekh (

2007) examined the link of trade and development for 150 countries. He stated that international trade is more efficient than those with higher wages for countries with lower revenues.

Chang et al. (

2009) focused on 82 countries and recorded that economic progress was motivated by economic openness.

Afzal and Hussain (

2010) found no connection between exports/imports and economic progress in Pakistan. On the contrary,

Can et al. (

2021) found a significant relationship between the two variables. Additionally,

Klasra (

2011) and

Shahbaz (

2012) challenged their claims, confirming that Pakistan’s development hypothesis is dependent on trade (economic openness).

4. Empirical Results and Discussions

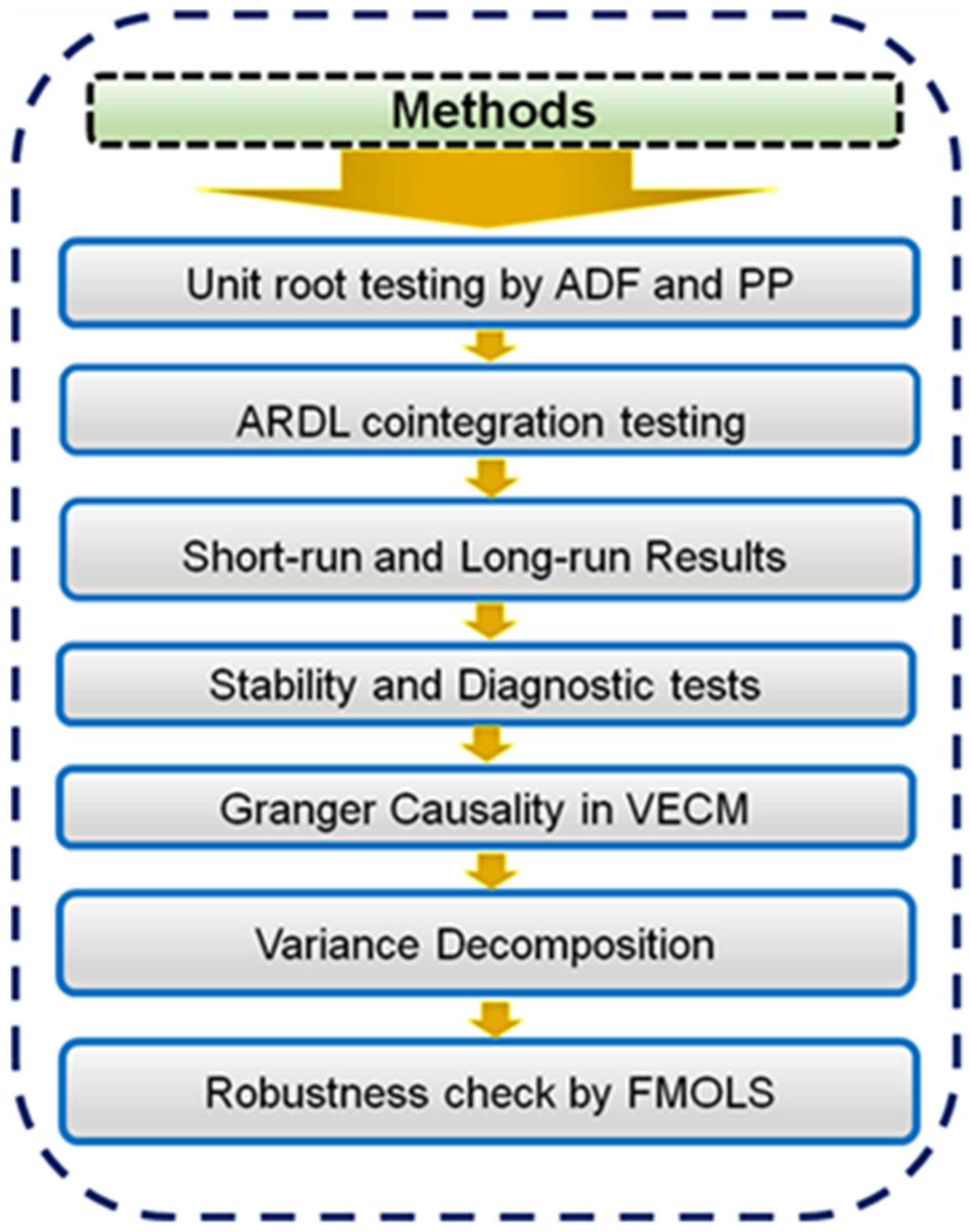

To ensure that the time series data are stationary, the integration order of those series is important. For series integration at both

I(0) and

I(1), the ARDL cointegration method application is justified. The long-term relationship may also be investigated by Johansen and Juselius’ (

Johansen and Juselius 1990) technique. This study included unit root tests, Augmented Dicky-Fuller, and the Phillips-Perron (PP), in determining the integration order of concerned variables (see

Table A1 in

Appendix A). The outline of applied methods is shown in

Figure 1.

It, thus, defines the integration order as a mixture of the level and the first difference, rendering the usage of the ARDL cointegration valid. The AIC and SBC determine the optimal lag length. The F-statistics appeared significant, concluding the long-term association among the variables of interest (see

Table A2 in

Appendix A). This infers that cointegration among the variables exists. The values estimated by F-statistics are greater than the values for the upper bound, which are the critical values with constant and no trend (

Shahbaz 2012).

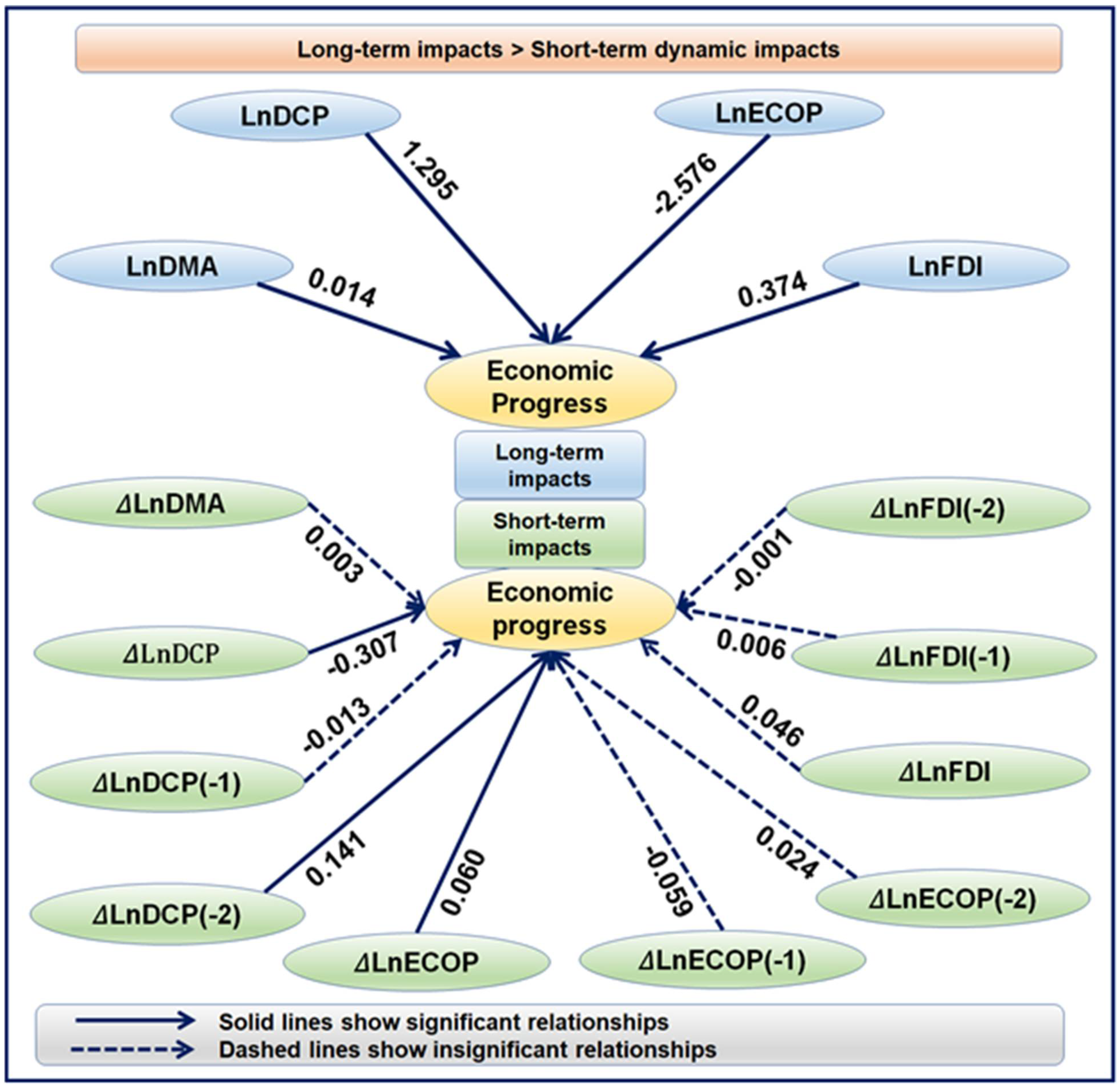

Table A3 provides the long-term forecasts for the ARDL method with specific diagnostic test statistics (see

Appendix A). The findings indicate that the long-term association with DMA is significantly positive, showing the

vanishing effect of financial development (

Osei and Kim 2020). More specifically, an increase of 1 unit in deposit money reserves corresponds to an improvement of 0.0140 units in economic progress. In the long-term, deposits will therefore be seen as the leading source for a long-term investment with significant economic progress implications. The findings further show a negative association between lending to the private sector domestically and long-term economic progress. This is not aligned with the

growth effect of financial development (

Nasreen et al. 2020). Additionally, this finding did not lend credence to (

Ahmad et al. 2019). Yet, in the short term, this impact is significantly positive. It entails that the effective distribution of private credit to productive domestic ventures can boost business operations and economic progress. In the same vein,

Wang and Tan (

2021) found economic development promotion effect of financial development across Chinese provinces. The literature (

Ernst 2019) found similar findings by revealing that financial market development leads to economic development. Along these lines,

Vo et al. (

2019) presented interesting empirical outcomes. In the short term, financial derivatives were revealed to boost economic progress in India, the United States, and Japan. This effect vanished in the long-term process for these countries. However, for China, those derivatives provided a short-term negative and long-term positive impact on economic progress. In 20 Indian states,

Pradhan et al. (

2021) revealed economic growth boosting the impact of financial inclusion, which is consistent with our results in the short term, and vice versa. In contrast,

Cheng et al. (

2021) spun out the negative influence of financial development on economic development across selected 72 global economies.

Moreover, the connection between economic progress and economic openness is negative in the long term but positive in the short-term. This result is consistent with (

Huang and Sun 2019) in the case of Korea, China, and the United States. At the same time, it diverges from (

Rajan and Zingales 2003), since they showed a positive link between economic progress and economic openness in the long term. Similarly,

Majumder et al. (

2020) found a statistically significant and positive impact of trade openness on economic growth in 95 economies worldwide. In addition,

Arvin et al. (

2021) revealed a positive influence of trade openness on the economic growth of G-20 countries, which is aligned with our results in the short term.

Li and Wei (

2021) found a positive impact of openness and financial development on economic growth with a differentiated degree of influence across 30 Chinese provinces.

In the same way,

Atil et al. (

2020) disclosed a positive linkage between economic growth and financial development in Pakistan. Furthermore,

Ghazouani et al. (

2020) found that trade openness accelerated the economic progress of Asia-Pacific nations. Finally,

Kong et al. (

2021) found an interesting finding, demonstrating that trade openness promoted economic growth quality in both the long and short-term for the Chinese economy. There is a statistically significant negative association between GDP and ECOP in the long term, while a positive relationship in the short term. This finding calls for adaptations in dealing with international trade policy to enhance economic openness. It is essential to say that, provided this condition, the policymakers should be very cautious in manipulating their actions in the opening of an emerging economy in the light of long-term negative effects.

For short-term links, the error correction method (ECM) is applied. A short-term correlation among finance–trade–growth exists when the error correction term’s coefficient is significantly negative (see

Table A4 in

Appendix A). The findings reveal that the error correction term has a negative and statistically significant value of 23.8%, which tells that concerned variables are connected in the long term. This demonstrates that any instability in economic progress would be resolved in the long term with a pace of 23.8%. The long-term and short-term relationships are graphically presented in

Figure 2.

This study employed sensitivity analysis to analyze the model’s reliability. In the lower panel of

Table A3, findings for normality of the model, serial correlation, heteroscedasticity, and Ramsey reset test’s functional form are shown (see

Appendix A).

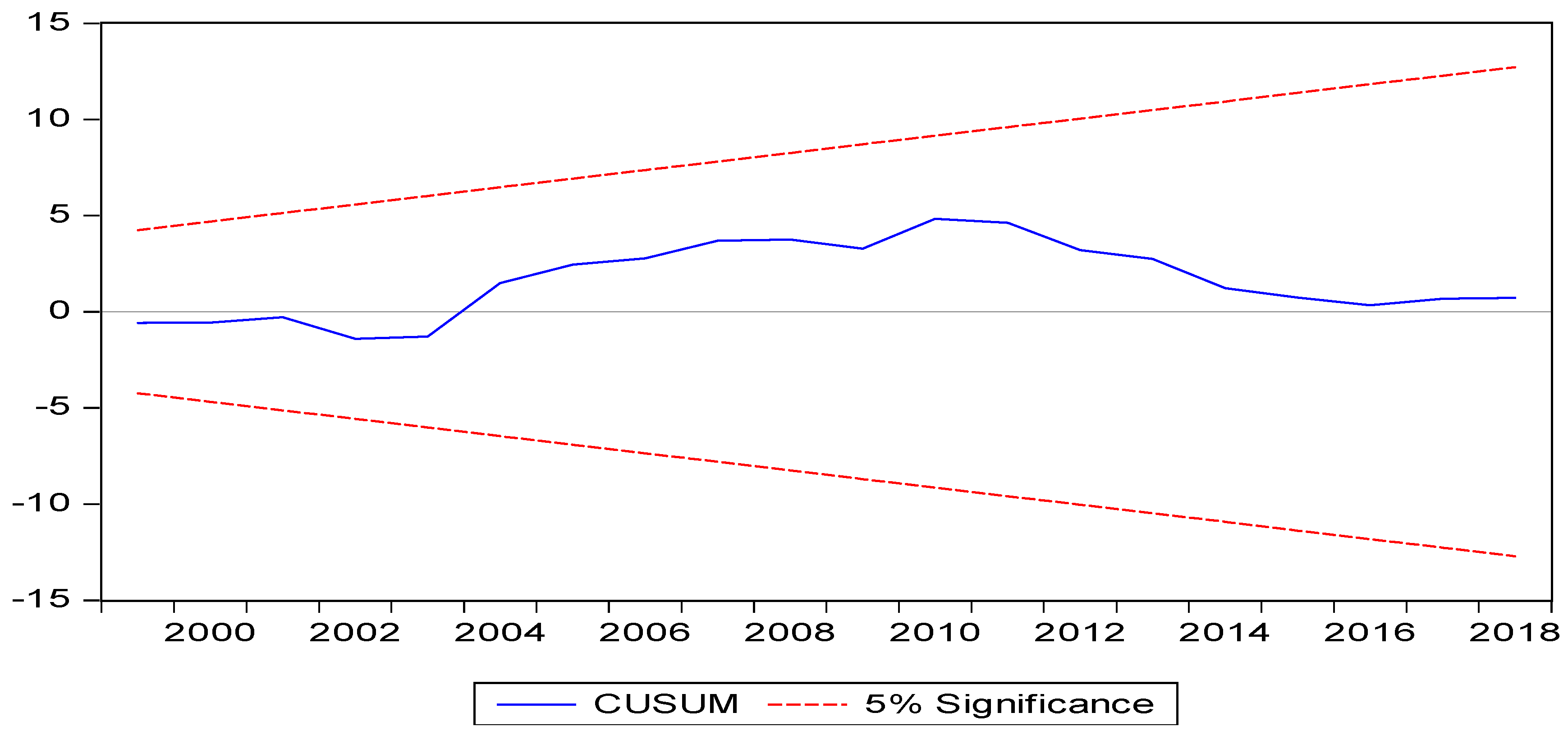

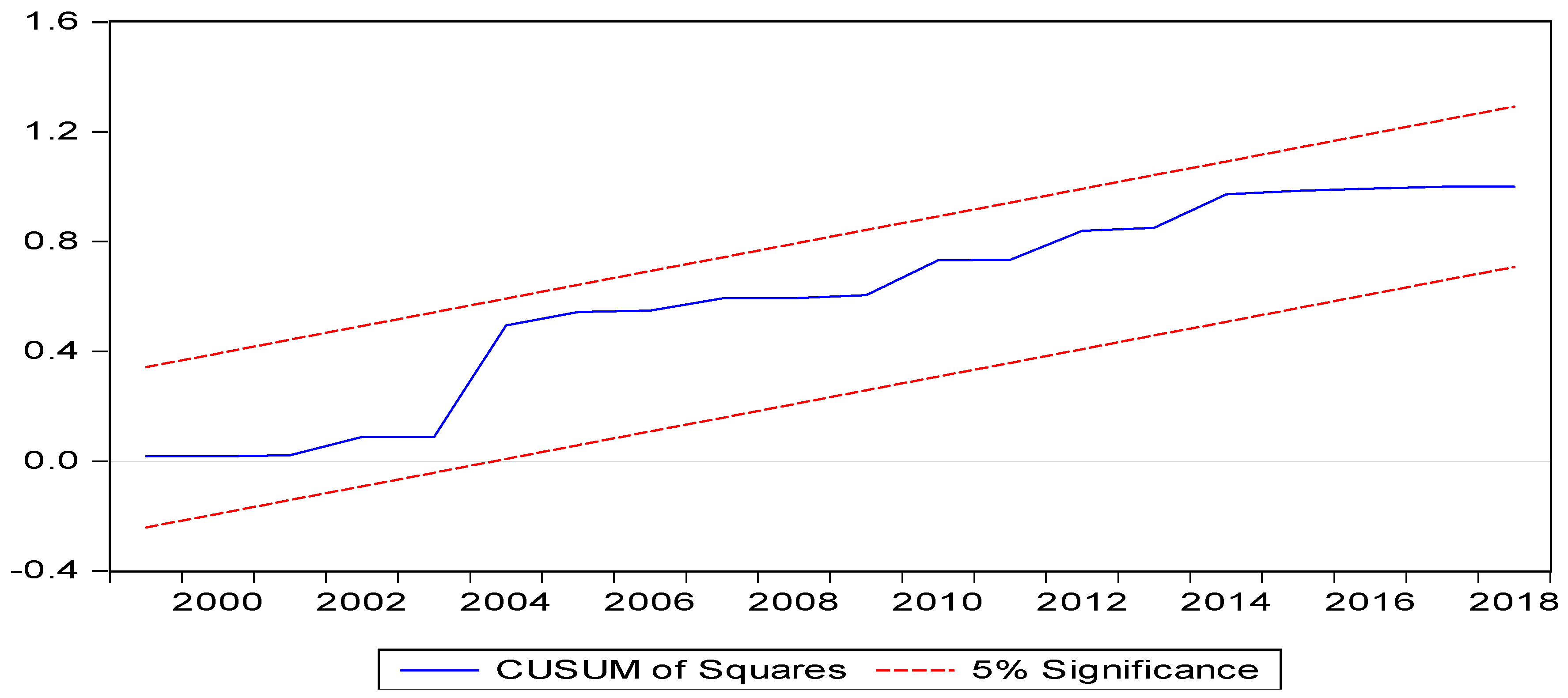

The research model’s stability is examined through the cumulative sum (CUSUM) and the cumulative sum of the squares (CUSUMSQ) tests. The estimated graphs of the CUSUM and the CUSUM square are shown in

Figure 3 and

Figure 4. The ARDL cointegration is applied to observe the coefficient’s stability. All the figures illustrate that the assessed line is reasonable and within the critical boundaries at a 5% significance level. Thus, models are found to be reliable and stable after estimation.

4.1. Granger Causality and Variance Decomposition Analysis

The details of the Granger-based causality tests are reported in

Table 2. The findings indicate that there is a clear unilateral causality between financial development and economic openness. The results also reveal that a bilateral causality exists between economic openness and economic progress. The Innovation Accounting method involving the analysis of variance decomposition was also used to observe the anticipated influence of economic openness and financial development on economic progress, as the ARDL estimates do not give any conclusion regarding the correlation outside the sample period. It has been posited that the generalized impulse response function only tells the nature of the shock but does not demonstrate the degree of that particular shock (

Shahbaz et al. 2013a). So, the variance decomposition is used to find the magnitude of this shock (see

Table 3). It determines the input of every innovation to h-step ahead dependent variable’s forecast error variance. It gives a mean value for influential shocks’ comparative significance in illuminating the deviation in the dependent variable (

Pesaran et al. 1999).

Hashimzade et al. (

2013) put forward that the outcomes revealed by the variance decomposition approach were more reliable than other econometric methods in the same domain.

Hence, this study expects the dynamic causal links of financial development and economic openness with the economic progress of Pakistan for the next ten years. The results explain that about 85.10% of economic progress is affected by its standard innovation shock. GDP responds by 6.80%, 2.84%, 3.39%, and 1.85% when the one standard deviation variation is attributed to the financial development, economic openness, and foreign direct investment, respectively. The result is confirmed by the outcome of the impulse response function, which is also anticipated for the next ten years. Financial development would be the main contributor to economic progress. Moreover, the impulse response function plots also confirmed these impacts.

4.2. Fully Modified Least Squares

The estimations accomplished for the long term from the ARDL approach are then examined for robustness by applying another single Equation estimator approach that is known as FMOLS (

Stock and Watson 1993) (see

Table 4). The most important benefit of the FMOLS approach is that it reflects the combination of integration orders of variables cointegrated in the time series data. The valuation of this approach elaborates the regression of the

I(1) variables in response to other

I(1) variables having leads (p), the first difference lags (_p), and the other variables having the integration order

I(0) having the constant term (

Kao et al. 1999). FMOLS approach is advantageous as it solves the problem of possible endogeneity and bias in a small sample.

5. Conclusions and Policy Proposals

The research explored the linkage of financial development and economic openness in Pakistan’s economic progress during 1975–2018. For assessing the existence of cointegration in the concerned variables, the ARDL cointegration was utilized. We used the deposit money bank asset (DMA) as a percentage of GDP and domestic credit to the private sector (DCP) as a percentage of GDP to reflect the calculation of financial development. At the same time, economic openness was represented by the contribution of export and import to GDP. The long-term findings indicated the long-term stability among the variables of interest. The Granger causality method is applied to assess the direction of causality among all the variables under consideration. A robustness analysis was performed using FMOLS to validate the stability and accuracy of the ARDL findings.

Unit root test revealed the mixed integration order of series under analysis. The findings of the ARDL suggested that there was a long-term association between financial development and economic progress, whereas, in the short term, the association existed between economic openness and economic progress. In comparison, the ECTt−1 coefficient (−0.2388) had the predicted sign with significant outcomes. This indicates the speed of correction from short-term imbalance to long-term balance by roughly 23.88%. In addition, the findings of the CUSUM and CUSUMSQ stability tests declared the stability of the estimated models.

To achieve the goal of economic progress, policymakers and the government should take steps to develop a solid financial system and ensure that financial institutions can offer adequate funds to the productive areas of the Pakistani economy. Policymakers should make sure that the funds given to the private sector are being utilized for innovative programs to set up a sustainable development path for the economy. In addition to that, the capital sector also needs to be consolidated to enable the utilization and effective transfer of resources into economically active areas. The financial sector should be improved to help the introduction of government privatization. Consequently, policymakers may use shifts in the economic progress or real sector to control the course of development and growth of commercial and financial regions of the economy as the economic progress is linked to economic openness and financial development. Finally, in light of our findings, the short-term macroeconomic policies should promote economic openness to support open economy macroeconomic activity in the short run to promote economic prosperity and sustainable economic progress in the long run.

{kind=link}

{kind=link}

{kind=link}

{kind=link}