Tax Rates and Tax Revenues in the Context of Tax Competitiveness

Abstract

:1. Introduction

2. Materials and Methods

- —average corporate tax revenues of member states in year .

- —average statutory tax rate of member states in year ,

- —average effective average tax rate of member states in year ,

- —average gross domestic product of member states in year ,

- —average foreign direct investment of member states in year ,

- —average inflation rate of member states in year ,

- —average unemployment rate of member states in year .

- —level constant,

- —regression coefficients, i.e., model parameters that express the value of the change of the explanatory variable to the explained variable ,

- —random model error, i.e., a random variable that captures other influences that may affect the explanatory variable .

3. Results and Discussion

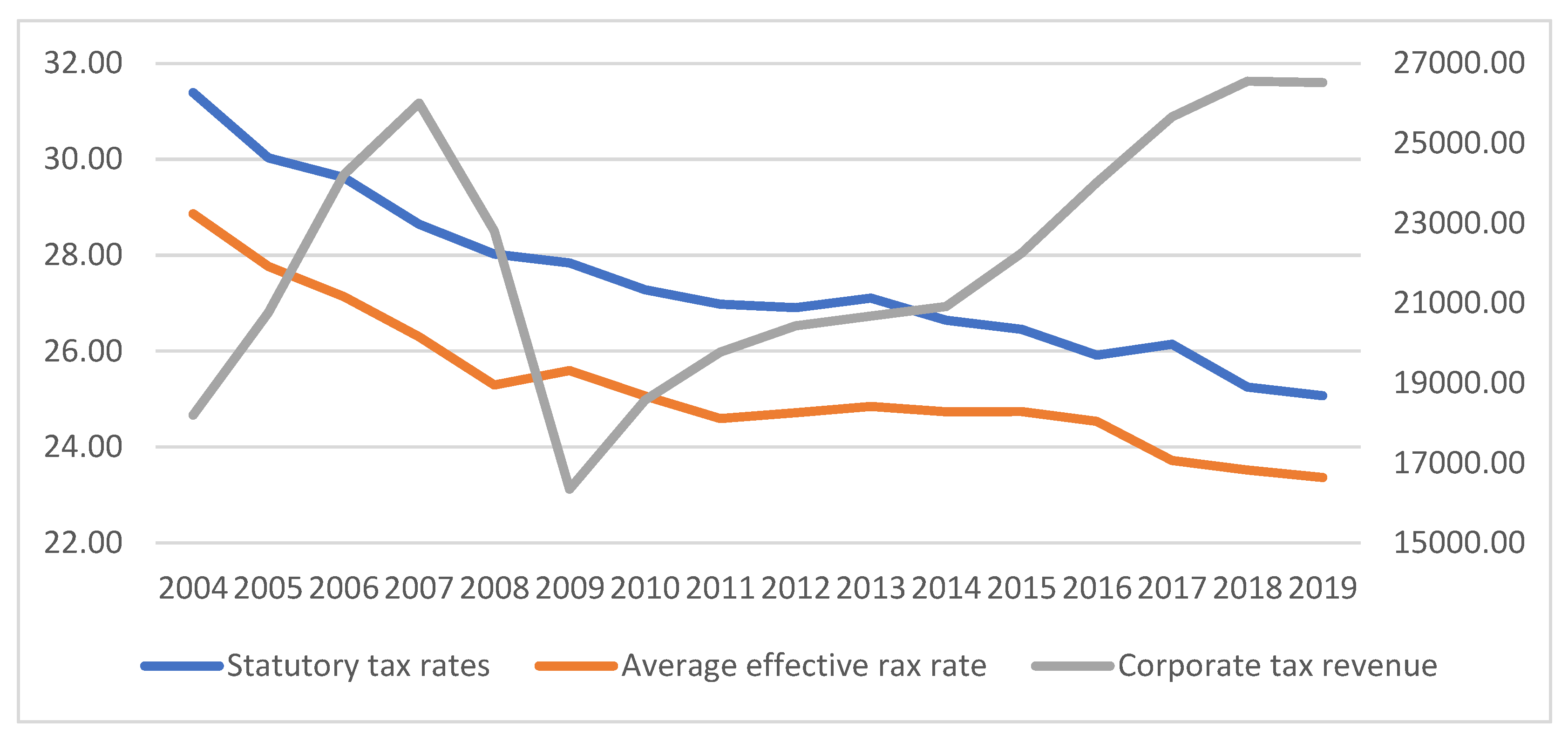

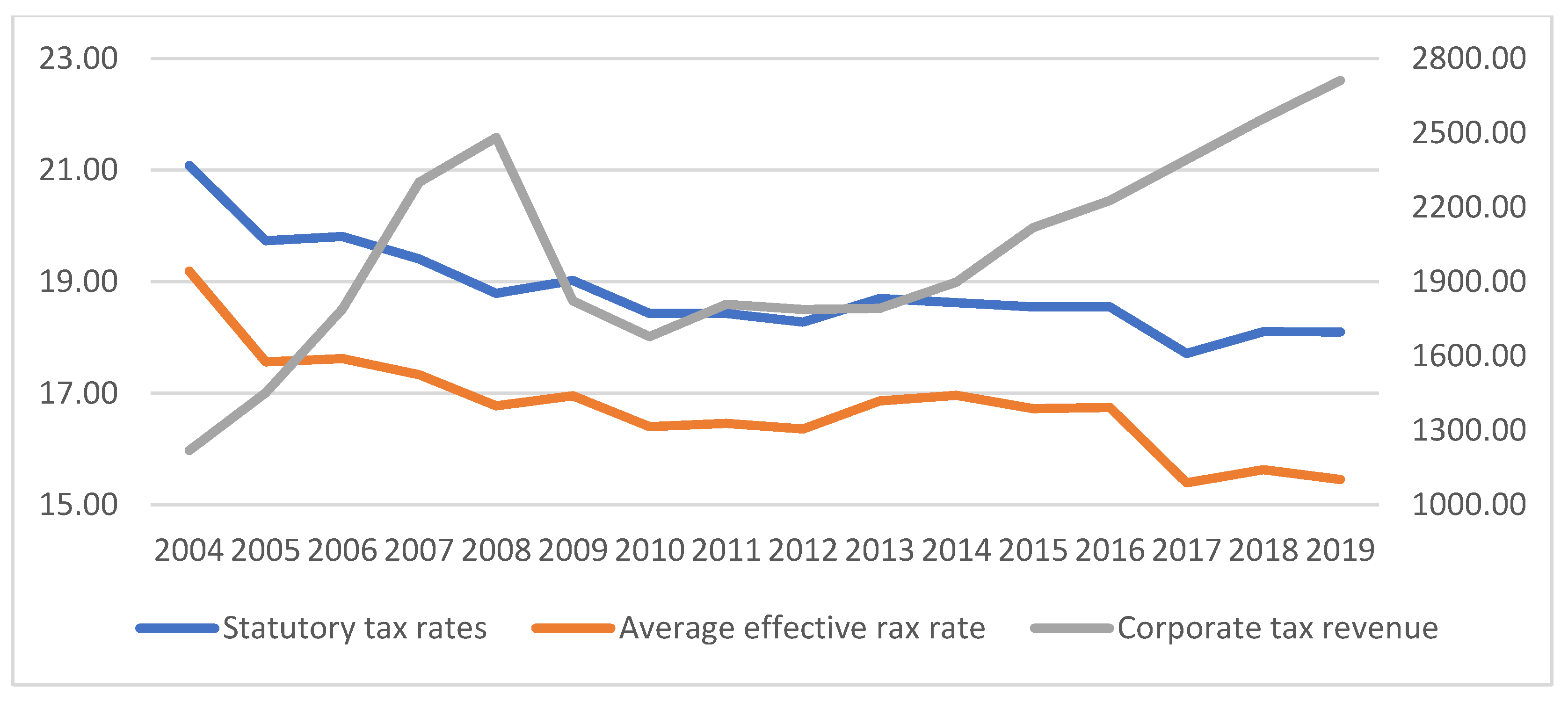

3.1. Analysis and Comparison of Tax Indicators and Corporate Tax Revenues

3.2. Regression Analysis

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Country | Statutory Tax Rate (%) | Average Effective Tax Rate (%) | Corporate Tax Revenues (in EUR million) | ||||||

|---|---|---|---|---|---|---|---|---|---|

| 2004 | 2019 | Average 2004–2019 | 2004 | 2019 | Average 2004–2019 | 2004 | 2019 | Average 2004–2019 | |

| Belgium | 34.0 | 29.6 | 33.4 | 29.5 | 25.0 | 26.6 | 8985.90 | 17,684.50 | 12,607.73 |

| Bulgaria | 19.5 | 10.0 | 11.2 | 17.1 | 9.0 | 10.0 | 519.35 | 1212.25 | 901.71 |

| Czechia | 28.0 | 19.0 | 20.8 | 24.6 | 16.7 | 18.3 | 4034.52 | 7384.22 | 5663.25 |

| Denmark | 30.0 | 22.0 | 24.8 | 26.8 | 19.8 | 22.3 | 5879.85 | 9549.32 | 7193.90 |

| Germany | 38.3 | 29.9 | 31.9 | 35.8 | 28.9 | 30.2 | 46,067.00 | 93,586.00 | 68,795.81 |

| Estonia | 26.0 | 20.0 | 21.4 | 20.4 | 13.9 | 16.7 | 161.19 | 509.10 | 300.53 |

| Ireland | 12.5 | 12.5 | 12.5 | 14.3 | 14.1 | 14.3 | 5487.78 | 11,000.00 | 6184.54 |

| Greece | 35.0 | 28.0 | 28.2 | 30.4 | 26.6 | 24.9 | 5259.00 | 4071.00 | 4439.13 |

| Spain | 35.0 | 25.0 | 29.7 | 36.5 | 30.1 | 32.8 | 28,793.00 | 25,757.00 | 27,480.44 |

| France | 35.4 | 34.4 | 36.0 | 35.0 | 33.4 | 34.9 | 40,584.00 | 68,517.00 | 55,013.31 |

| Croatia | 20.0 | 18.0 | 19.6 | 18.1 | 14.8 | 16.3 | 611.97 | 1285.43 | 1020.89 |

| Italy | 37.3 | 27.8 | 32.2 | 31.8 | 24.6 | 26.8 | 33,149.00 | 34,708.00 | 37,853.13 |

| Cyprus | 10.0 | 12.5 | 11.1 | 14.8 | 13.4 | 12.4 | 468.10 | 1304.20 | 1050.17 |

| Latvia | 15.0 | 20.0 | 15.6 | 14.3 | 16.7 | 14.0 | 185.13 | 47.69 | 346.12 |

| Lithuania | 15.0 | 15.0 | 15.8 | 12.7 | 12.7 | 13.7 | 338.55 | 759.15 | 548.21 |

| Luxembourg | 30.4 | 24.9 | 28.7 | 26.5 | 21.8 | 25.1 | 1571.15 | 3761.12 | 2333.60 |

| Hungary | 17.6 | 10.8 | 18.3 | 17.8 | 11.1 | 17.3 | 1740.59 | 1728.47 | 1843.03 |

| Malta | 35.0 | 35.0 | 35.0 | 32.2 | 25.3 | 30.8 | 167.51 | 763.72 | 451.67 |

| Netherlands | 34.5 | 25.0 | 26.4 | 31.0 | 22.5 | 23.6 | 16,266.00 | 30,001.00 | 19,240.13 |

| Austria | 34.0 | 25.0 | 25.6 | 31.2 | 23.1 | 23.5 | 5607.00 | 10,983.76 | 7379.82 |

| Poland | 19.0 | 19.0 | 19.0 | 17.1 | 16.6 | 17.4 | 4003.71 | 11,775.64 | 7822.07 |

| Portugal | 27.5 | 31.5 | 29.1 | 24.6 | 21.4 | 24.9 | 4308.52 | 6662.13 | 5449.85 |

| Romania | 25.0 | 16.0 | 16.6 | 22.4 | 14.7 | 15.2 | 1934.93 | 4685.18 | 3258.50 |

| Slovenia | 25.0 | 19.0 | 20.3 | 21.5 | 17.3 | 18.3 | 522.89 | 953.54 | 715.14 |

| Slovakia | 19.0 | 21.0 | 20.2 | 16.5 | 18.7 | 17.9 | 1171.95 | 2840.53 | 2109.63 |

| Finland | 29.0 | 20.0 | 23.8 | 27.2 | 19.6 | 22.4 | 5357.00 | 6069.00 | 5206.50 |

| Sweden | 28.0 | 21.4 | 24.9 | 23.1 | 19.4 | 21.9 | 8511.45 | 14,169.19 | 11,705.26 |

| United Kingdom | 30.0 | 19.0 | 24.7 | 29.3 | 20.2 | 25.3 | 57,159.70 | 61,273.45 | 60,711.58 |

| Average EU-28 | 26.6 | 21.8 | 23.5 | 24.4 | 19.7 | 21.3 | 10,315.95 | 15,465.77 | 12,772.34 |

| Average EU-13 | 21.1 | 18.1 | 18.8 | 19.2 | 15.5 | 16.8 | 1220.03 | 2711.47 | 2002.38 |

| Average EU-15 | 31.4 | 25.1 | 27.5 | 28.9 | 23.4 | 25.3 | 18,199.09 | 26,519.50 | 22,106.31 |

References

- Abbas, S. M. Ali, and Alexander Klemm. 2012. A Partial Race to the Bottom: Corporate Tax Developments in Emerging and Developing Economies. Washington, DC: International Monetary Fund. [Google Scholar]

- Barro, Robert J., and Jason Furman. 2018. Macroeconomic Effects of the 2017 Tax Reform. Brookings Papers on Economic Activity 49: 257–345. [Google Scholar] [CrossRef] [Green Version]

- Barrios, Salvador, Per Iversen, Magdalena Lewandowska, and Ralph Setzer. 2009. Determinants of intra-euro area government bond spreads during the financial crisis. In European Economy—Economic Papers. Brussels: European Commission, vol. 388, pp. 1–28. [Google Scholar] [CrossRef]

- Bayer, Ondřej. 2011. Vládní daňové predikce: Ex ante odhady expost hodnocení přesnosti v České Republice. Český Finanční a Účetní Časopis 6: 42–54. [Google Scholar] [CrossRef] [Green Version]

- Candau, Fabien, and Jacques Le Cacheux. 2018. Taming Tax Competition with a European Corporate Income Tax. Revue D’économie Politique 128: 575–611. [Google Scholar] [CrossRef]

- Castro, G. Ángeles, and D. B. Remírez Camarillo. 2014. Determinants of tax revenue in OECD countries over the period 2001–2011. Contaduría y Administración 59: 35–59. [Google Scholar] [CrossRef] [Green Version]

- Clausing, A. Kimberly. 2007. Corporate tax revenues in OECD countries. International Tax and Public Finance 14: 115–33. [Google Scholar] [CrossRef]

- Dalton, Hugh. 2003. Priciples of Public Finance, 1st ed. London: Routledge. [Google Scholar] [CrossRef]

- European Commission. 2021. Data on Taxation. Available online: https://ec.europa.eu/taxation_customs/business/economic-analysis-taxation/data-taxation_en (accessed on 3 March 2021).

- Fedeli, Silvia, and Francesco Forte. 2012. Public debt and unemployment growth: The need for fiscal and monetary rules. Evidence from OECD countries (1981–2009). Economia Politica 29: 409–38. [Google Scholar] [CrossRef]

- Ganghof, Steffen, and Philipp Genschel. 2008. Taxation and democracy in the EU. Journal of European Public Policy 15: 58–77. [Google Scholar] [CrossRef]

- Garrett, Geoffrey. 1995. Capital mobility, trade, and the domestic politics of economic policy. International Organization 49: 657–87. [Google Scholar] [CrossRef]

- Glova, Jozef, and Silvia Mrázková. 2018. Impact of Intangibles on Firm Value: An Empirical Evidence from European Public Companies. Ekonomický Časopis 66: 665–80. [Google Scholar]

- Glova, Jozef, Silvia Mrázková, and Darya Dancaková. 2018. Measurement of intangibles and knowledge: An empirical evidence. AD ALTA-Journal of Interdisciplinary Research 8: 76–80. [Google Scholar]

- Gravelle, G. Jane. 1994. The Economic Effects of Taxing Capital Income. Cambridge: MIT Press, 358p, ISBN 9780262071581. [Google Scholar]

- Gropp, Reint, and Kristina Kostial. 2000. The Disappearing Tax Base: Is Foreign Direct Investment(FDI) Eroding Corporate Income Taxes? IMF Working Paper. WP/00/173. Washington, DC: International Monetary Fund. [Google Scholar]

- Guziejewska, Beata, Wojciech Grabowski, and Szymon Bryndziak. 2015. Tax competition strategies in corporate income tax—The case of EU countries. Business and Economic Horizons 10: 253–71. [Google Scholar] [CrossRef] [Green Version]

- Hines, R. James. 2003. Sensible Tax Policies in Open Economies. Dublin. Journal of the Statistical and Social Inquiry Society of Ireland 33: 1–39. [Google Scholar]

- Johansson, Asa, Christopher Heady, Jens Arnold, Bert Brys, and Laura Varia. 2008. Taxation and economic growth. In OECD Economics Department. Working papers No. 620. Paris: OECD Publishing. [Google Scholar] [CrossRef]

- Karpowicz, Andrzej, and Elzbieta Majewska. 2018. Corporate Income Tax Determinants: How Important Is the Tax Rate? Paper presented at the 27th International Scientific Conference on Economic and Social Development, Rome, Italy, March 1. [Google Scholar]

- Kawano, Laura, and Joel Slemrod. 2012. The Effect of Tax Rates and Tax Bases on Corporate Tax Revenues: Estimates with New Measures of the Corporate Tax Base. NBER Working Paper 18440. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Kenny, W. Lawrence, and Stanley L. Winner. 2006. Tax Systems in the World: An Empirical Investigation Into the Importance of Tax Bases, Administration Costs, Scale and Political Regime. International Tax and Public Finance 13: 181–215. [Google Scholar] [CrossRef]

- Kubátová, Květa, and Lucie Řihová. 2009. Regresní analýza faktoru ovplyvňujícich výnosy korporativní daně v zemích OECD. Politická Ekonómie 4: 451–71. [Google Scholar] [CrossRef]

- Lee, Young, and Roger Gordon. 2005. Tax Structure and Economic Growth. Journal of Public Economics 89: 1027–43. [Google Scholar] [CrossRef]

- Nerudová, Danuše. 2008. Harmonizace Daňových Systémů Zemí EVROPSKÉ Unie. Praha: ASPI, 257p, ISBN 9788073573867. [Google Scholar]

- Remeur, Cécile. 2015. Tax Policy in the EU: Issues and Challenges. Luxembourg: EPRS|European Parliamentary Research Service. [Google Scholar] [CrossRef]

- Rodrik, Dani. 1998. Has Globalisation Gone Too Far? Challenge 41: 81–94. [Google Scholar] [CrossRef]

- Rosen, S. Harvey, and Ted Gayer. 2010. Public Finance. New York: The McGraw-Hill Companies. [Google Scholar]

- Slemrod, Joel. 2004. Are corporate tax rates, or countries, converging? Journal of Public Economics 88: 1169–86. [Google Scholar] [CrossRef]

- Swank, Duane. 2001. Mobile capital, democratic institutions, and the public economy in advanced industrial societies. Journal od Comparative Policy Analysis: Research and Practice 3: 133–62. [Google Scholar] [CrossRef]

- Teather, Richard. 2005. The Benefits of Tax Competition. London: The Institute of Economic Affairs, pp. 1–91. ISBN 0255365691. [Google Scholar]

- The World Bank. 2021. World Bank Open Data. Available online: https://data.worldbank.org/ (accessed on 8 March 2021).

- Tosun, Mehmet. 2006. Explaining the Variation in Tax Structures in the MENA Region. UNR Economics Working Paper. WP/06/018. Reno: University of Nevada. [Google Scholar]

- Výškrabka, Milan, and Jana Antalicová. 2018. Daňový report Slovenskej republiky. In Inštitút Finančnej Politiky. October. Available online: https://www.mfsr.sk/sk/financie/institut-financnej-politiky/publikacie-ifp/ekonomicke-analyzy/50-danovy-report-slovenskej-republiky-2018-oktober-2018-2.html (accessed on 15 March 2021).

| Variable | Author (Year) | Relationship between Corporate Tax Revenue and Variable | Expected Relationship | Interpretation of Impact |

|---|---|---|---|---|

| Statutory tax rate and Average effective tax rate | Lee and Gordon (2005); Teather (2005); Ganghof and Genschel (2008); Guziejewska et al. (2015) | negative | + | An increase in the tax rate will increase income from corporate tax |

| Clausing (2007) | positive | |||

| Gross domestic product | Gropp and Kostial (2000); Clausing (2007); Kubátová and Řihová (2009); Bayer (2011); Karpowicz and Majewska (2018) | positive | + | Higher GDP leads to higher incomes from corporate tax |

| Net foreign direct investment | Gropp and Kostial (2000); Clausing (2007) | positive | + | The growth of foreign direct investment increases corporate tax revenues |

| Inflation rate | Kubátová and Řihová (2009); Barro and Furman (2018) | positive | + | Higher inflation rates lead to higher incomes from corporate tax |

| Unemployment rate | Gropp and Kostial (2000); Tosun (2006); Clausing (2007); Kubátová and Řihová (2009); Fedeli and Forte (2012) | negative | − | Higher unemployment rates reduce incomes from corporate tax |

| Model EU13 | Model EU15 | |||||

|---|---|---|---|---|---|---|

| t Value | p-Value | t Value | p-Value | |||

| cit (Intercept ) | 4049.624 | 2.676 | 0.02539 * | −66,803.55 | −2.577 | 0.029826 * |

| STR | −472.974 | −4.422 | 0.00167 ** | 1198.23 | 0.714 | 0.493491 |

| EATR | 400.08 | 4.731 | 0.00107 ** | 237.22 | 0.146 | 0.887021 |

| GDP | 13.194 | 3.512 | 0.00660 ** | 62.35 | 5.409 | 0.000428 *** |

| FDI | 4.575 | 2.352 | 0.04319 * | 208.15 | 2.085 | 0.066702 |

| INF | 28.331 | 2.706 | 0.02414 * | 949.31 | 1.921 | 0.086970 |

| UN | −128.921 | −7.976 | 2.27 × 10−5 *** | −603.11 | −2.151 | 0.059900 |

| Coefficient of determination | 0.9888 | 0.9078 | ||||

| Corrected coefficient of determination | 0.9813 | 0.8464 | ||||

| p-value for the model | 2.97 × 10−8 | 0.0003347 | ||||

| Normatila residues shapiro.test(resid()) | 0.1684 | 0.8132 | ||||

| Heteroskedasticity bptest() | 0.2108 | 0.8995 | ||||

| Autocorrelation bgtest() | 0.3207 | 0.8206 | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Helcmanovská, M.; Andrejovská, A. Tax Rates and Tax Revenues in the Context of Tax Competitiveness. J. Risk Financial Manag. 2021, 14, 284. https://doi.org/10.3390/jrfm14070284

Helcmanovská M, Andrejovská A. Tax Rates and Tax Revenues in the Context of Tax Competitiveness. Journal of Risk and Financial Management. 2021; 14(7):284. https://doi.org/10.3390/jrfm14070284

Chicago/Turabian StyleHelcmanovská, Martina, and Alena Andrejovská. 2021. "Tax Rates and Tax Revenues in the Context of Tax Competitiveness" Journal of Risk and Financial Management 14, no. 7: 284. https://doi.org/10.3390/jrfm14070284