1. Introduction

The hypothesis that the price of primary commodities relative to those of manufacturers presents a downward secular trend (

Prebisch 1950;

Singer 1950), or the Prebisch-Singer (PS) hypothesis, is central for least developed economies that specialize in producing and exporting primary products while importing manufacturers. The hypothesis, which is independently posed by

Prebisch (

1950) and

Singer (

1950), asserts that such specialization causes a steady decline in the economy’s net barter terms of trade and, hence, the real income of the country. It is, therefore, important for policymakers to assess the empirical validity of this hypothesis as the decision to accept or to reject the hypothesis can have profound policy implications. For instance, strong evidence supporting a long-run downward trend in a country’s key primary exports might lead to a change in policy or a restructure in the country’s export portfolio to include manufacturers and services.

To this day, the PS hypothesis remains at the core of a continuing debate among policymakers and international trade economists. The main reason for the sustained interest in the topic is that the fundamental question implied by the PS hypothesis is impossible to answer without turning to data (

Balagtas and Holt 2009). The answer, however, varies according to the starting point of the analysis, i.e., the statistical/technical properties of the price series, and other non-technical factors, such as commodity classifications and aggregations. While the statistical properties of the price series have been extensively discussed in the literature, studying the impact of other non-technical factors remains a fruitful research area. The empirical literature on the subject uses various techniques to test the PS hypothesis and the consensus is that the result whether to accept or reject the hypothesis depends on the starting point of the analysis, i.e., the stationarity of the data generating process (

Ardeni and Wright 1992;

Bleaney and Greenaway 1993;

Cuddington and Urzua 1989;

Grilli and Yang 1988;

Harvey et al. 2010;

Helg 1991;

Lutz 1999;

Newbold and Vougas 1996;

Powell 1991;

Sapsford 1985;

Spraos 1980;

Thirlwall and Bergevin 1985;

Trivedi 1995), nonlinearity (

Balagtas and Holt 2009;

Persson and Teräsvirta 2003), and the existence of structural breaks (

Cuddington and Urzua 1989;

Kellard and Wohar 2006;

Leon and Soto 1997;

Newbold and Vougas 1996;

Zanias 2005).

In addition to stationarity, nonlinearity, and the existence of structural breaks,

Fahmy (

2011,

2014,

2017) shows that the terms of trade, i.e., the international sales terms of commodity prices (also known as border prices or Incoterms) contain significant information that contribute to our understanding of the behavior of the price series. The author shows that nonlinear free on board (FOB) and cost insurance and freight (CIF) real commodity prices that are driven by exogenous regime-driving macroeconomic variables, e.g., inflation and oil price, do not display downward trends because the fluctuations in the exogenous regime-driving variables impact their nonlinear behavior. Thus, the PS hypothesis is unlikely to be supported for this type of border prices.

The objective of this paper is to re-examine the PS hypothesis by employing a novel multiresolution wavelets decomposition to the

Grilli and Yang (

1988) data set. The intention is to separate the real price series into time and scale components and to test the PS hypothesis in the short- and long-run using a bivariate co-integration framework. Furthermore, the paper seeks to assess whether the results of the analysis depend on the information contained in the terms of trade of commodity prices. More formally, the study seeks to answering two research questions (RQs):

RQ1: When the data generating process is decomposed into various time and scale components, does the analysis support the PS hypothesis in the short- and long-run?

RQ2: In addition to stationarity, nonlinearity, and model type, do the tests results depend on the terms of trade of commodity prices?

The present paper contributes to the existing literature in several ways: First, to the best of our knowledge, it is the first paper that employs wavelets analysis to the

Grilli and Yang (

1988) data set to test the empirical validity of the PS hypothesis over different time scales. Second, the paper makes a significant contribution to the consensus that the assessment of the PS hypothesis depends on the starting point of the analysis. This contribution is twofold: First, the paper reaffirms our understanding that the results of testing the PS hypothesis depend on stationarity, nonlinearity, and the existence of structural breaks in the data generating process. Second, the paper shows that, in addition to the previous factors, the term of trade, i.e., the sales contract of the commodity price, is a key factor that impacts the assessment of the PS hypothesis. As we will demonstrate shortly, the results show that the PS hypothesis is not supported for all nonlinear stationary FOB and CIF prices in the Grilli and Yang commodity prices that are driven by exogenous transition variables. This finding is of particular importance to international trade regulators and policymakers of developing economies that depend mainly on primary commodities in their exports. The results also improve our understanding of the behavior of nonlinear real border prices.

The remainder of the paper is organized as follows:

Section 2 reviews the relevant literature.

Section 3 describes the data set and discusses the previous classifications. This section also discusses the multiresolution methodology that is used in the decomposition of the time series.

Section 4 discusses the empirical results. Finally,

Section 5 concludes.

2. Literature Review

The literature on the subject provides different explanations of the secular decline in relative commodity prices, e.g., lack of differentiation among commodity producers, low income elasticity of demand for primary commodities, and asymmetric market structure (

Harvey et al. 2010). It is worth noting, however, that these explanations are not founded on theoretical models of price formation. The basic model of commodity price formation is due to the early contributions of

Gustafson (

1958) and

Muth (

1961) on the theory of competitive storage, which postulates that speculative arbitrage is what generates the observed serial dependence in commodity prices.

Beck (

2001) applies a variation of ARCH techniques to commodity prices and finds an ARCH process in storable but not in non-storable commodity data.

Fahmy (

2011) reports similar results. A theoretical account of commodity price determination that implies a zero trend in relative commodity prices of some primary commodities (

Deaton 1999) is due to

Lewis (

1954), who suggests that unlimited supplies of labor in poor countries prevents growth of real wage. This, in turn, prevents the prices of primary commodities from exceeding the costs of production in the long run.

In the empirical literature on the existence of a downward trend in the net barter terms of trade, the data generating process, which is denoted by

in the text, is usually taken to be the logarithm of a primary commodity price relative to an index of manufactured goods’ unit values, i.e., the logarithm of a real commodity price time series. The PS hypothesis is commonly tested by fitting either trend stationary (TS) or difference stationary (DS) model to

A TS model regresses

on a constant and a time trend as

where

is a white noise process. A negative sign of the estimated slope coefficient

indicates the presence of a downward trend in the relative price of the primary commodity, thus supporting the PS hypothesis. Alternatively, the DS model regresses the first difference of

on a constant and an error term; that is,

where

is stationary and invertible.

Grilli and Yang (

1988) use the TS approach to study the long-run behavior of the net barter terms of trade. The authors develop a commodity price index, known as the Grilli and Yang Commodity Price Index (

), that consists of 24 annual primary commodity prices from 1900 to 1986. The authors deflate the

by an index of manufactured goods’ unit values (

) and fit the TS model in Equation (

1) to the logarithm of the ratio

, i.e.,

, as well as to the individual commodities forming the index.

1 They document a significant downward trend and, therefore, support the PS hypothesis. Using the data set published by

Grilli and Yang (

1988), several authors have investigated the empirical validity of the PS hypothesis.

Cuddington and Urzua (

1989) point out that the residuals of the TS model might possibly be nonstationary, which, in turn, renders the OLS estimate of the trend coefficient to be unreliable. The authors, therefore, assume that the Grilli and Yang series has a unit root and could not reject the unit root hypothesis (nonstationarity) in the price series using the

Dickey and Fuller (

1979) test. Based on this nonstationarity assumption, they fit a DS model to

, where they regress the first difference of

on a constant, a dummy to account for a structural shift in 1921, and a moving average error process. Apart from the one-time drop in the price series after 1920, the authors’ results do not support the PS hypothesis of a secular decline in the price of primary commodities.

Powell (

1991) also assumes that the data generating process is nonstationarity and fits the same DS model with several structural breaks in 1921, 1937, and 1975. Powell finds no support of the PS hypothesis.

Helg (

1991) tests the series

for stationarity and rejects the nonstationarity hypothesis using the

Dickey and Fuller (

1979) test. The author also applies

Phillips and Schmidt’ (

1989) test and rejects the unit root hypothesis in

. The result is in favor of a TS model with a negative trend coefficient for most of the century (1900–1988) and a major structural break at the end of the World War One.

Ardeni and Wright (

1992) point out that the TS or DS models, resulting from the

Box and Jenkins’ (

1970) identification framework, require making a preliminary hypothesis regarding the stationarity of the data generating process. To avoid this complication, the authors follow a structural time series approach that does not rest on any prior stationarity assumption. By examining the behavior of

over the period from 1900 to 1988, the authors find support of the PS hypothesis. The authors also report that the inclusion of a dummy variable to account for the 1921 break claimed by

Cuddington and Urzua (

1989) has no effect on the results.

Bleaney and Greenaway (

1993) extend the Grilli and Yang data series to 1991. The authors fit an autoregressive model with a time trend to

and reject the PS hypothesis in favor of a one-off drop in 1980.

Newbold and Vougas (

1996) find that the starting point of the econometric analysis, i.e., whether the data generating process is TS or DS, is crucial in testing the PS hypothesis. The authors find that there is strong evidence of the PS hypothesis when the relative price series is TS, but when the series is DS, the PS hypothesis is rejected. The authors also find that allowing for the possibility of structural break in the series does not help in assessing whether the time series is TS or DS.

Trivedi (

1995) also concludes that the empirical results of whether the relative price process is TS or DS are not clear-cut.

Harvey et al. (

2010) use new tests for the TS model and show that eleven price series present a downward trend over all or some fraction of the sample period. The authors accept the PS hypothesis in the very long run for a significant portion of primary commodity prices.

An alternative approach to the conventional TS and DS specifications in Equations (1) and (2) is the co-integration approach, which posits that if the series

and

are co-integrated, or

then there is a number

such that

has a stationary, invertible, autoregressive moving average (ARMA) representation

where

L is the lag operator,

and

are polynomials in

L with all roots lying outside the unit circle, and

is a white noise error. Thus, if the series

and

are co-integrated, then the data generating process

can be expressed as

which can be written as

where

and

. Since

in Equation (

6) is

, the relative price

is not a stationary process unless

, or equivalently,

In addition, note that, if

, or

the relative price,

, decreases as the price of manufacturers,

, increases. Therefore, the PS hypothesis can be assessed from Equation (

6) by testing the restriction

.

Von Hagen (

1989) provides a comparison between both approaches and argues that the co-integration approach is superior to the conventional TS/DS model. Using the previous bivariate framework, the author shows that the series are co-integrated, and uses the error-correction model of

Engel and Granger (

1987) to capture the short- and long-run features of the co-integrated series. The author’s findings do not support the PS hypothesis.

Lutz (

1999) extends the Grilli and Yang data set from 1986 to 1995 and argues that the reason behind the various findings is the choice of the econometric model. The author combines the TS, DS, and the co-integration relation between

and

into an encompassing first-order distributed lag model with its error-correction equivalent. Using the Johansen procedure, Lutz supports the PS hypothesis contrary to the findings of other authors who employ the bivariate framework (e.g.,

Powell 1991;

Von Hagen 1989).

Persson and Teräsvirta (

2003) assume, as a starting point to the analysis, that the series

is stationary. Using the extended series of

Lutz (

1999), the authors, unlike all the previous studies, consider the hypothesis that the series might be nonlinear. They test the linearity hypothesis in

against a parametric nonlinear model (the smooth transition autoregressive model) and do not reject the nonlinearity in the price series given the stationarity assumption. If the price series is nonlinear and stationary, the resulting mean reversion behavior will contradict the PS hypothesis. Therefore, the authors reach the same conclusion as of

Newbold and Vougas (

1996) that the findings vary according to the starting point of the analysis.

In this paper, we use a recent extended version of the

Grilli and Yang (

1988) data set, which is developed by

Pfaffenzeller et al. (

2007). The updated data set extends the annual original index and its 24 compositions to 2007. To answer RQ1, we use

Von Hagen’s (

1989) co-integration framework in Equation (

6) to study the short run and long run behavior of the time series. We employ a multiresolution wavelet decomposition to study the long run features of the co-integrated series and test the PS hypothesis over different time scales. The approach followed in the present study resembles that of

Persson and Teräsvirta (

2003) in the rationale that stationary nonlinear real commodity prices tend to reject the PS

ypothesis.

The present paper also contributes to filling the gap in the existing literature on the factors that influence the acceptance or rejection of the PS hypothesis. In addition to the statistical properties of the price series and the starting point of the econometric analysis, we argue that various aggregations and classifications of commodity prices could provide further insights regarding the assessment of the PS hypothesis. Trade flows, i.e., exports and imports, of primary commodity prices are influenced by several factors, such as specialization, competitiveness, comparative advantage, physical proximity between trading countries, and the level of aggregation of the product categories, i.e., the commodity heterogeneity of the sectors considered. Classifications of primary commodities are particularly important for understanding the behavior of price series. For instance,

Fanelli and Giglio (

2020) use the classification of agri-food products according to the Harmonized Commodity Descriptions and Coding System (HS-2) to study the factors affecting trade flows between groups of EU and Asian countries. The authors report that the HS-2 classification does not allow distinctions to be made between the trade in raw materials, semi-finished products, and final processed products. In a series of papers,

Fahmy (

2011,

2014,

2017) shows that classifying commodity prices according to the terms of trade provide a better understanding of the price series. Terms of trade, also known as Incoterms, are international sales terms that are published by the International Chamber of Commerce to define the obligations of the exporter and importer in a trading contract (

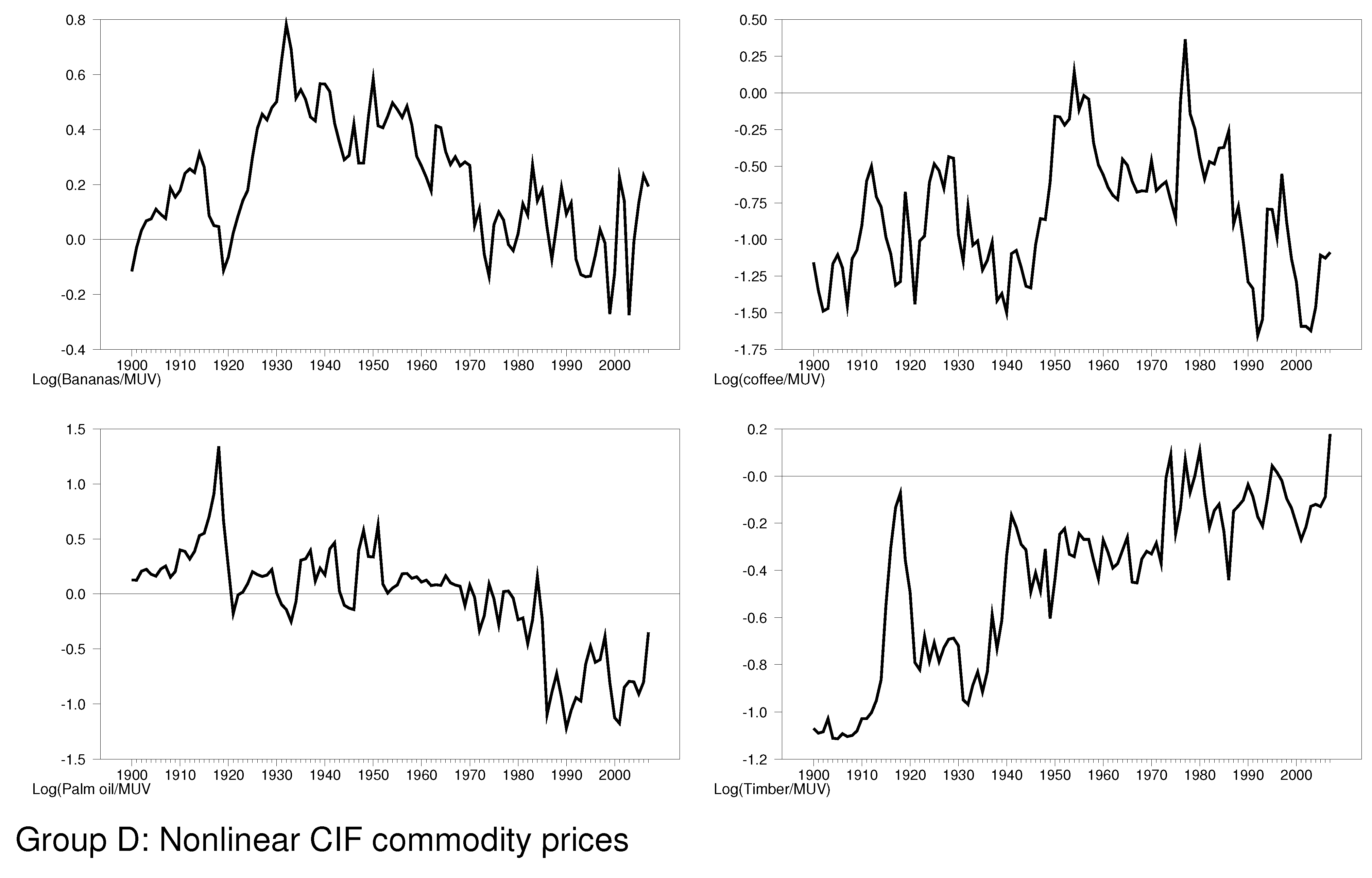

Fahmy 2017). Free on board (FOB) and cost insurance and freight (CIF) are the most commonly used Incoterms. FOB prices imply that the exporter bears all the risks and costs of transporting the cargo from the point of origin to the port of export in the country of origin. This means that FOB prices do not include the freight cost, which is heavily impacted by the price of oil. CIF prices, on the other hand, are basically FOB prices plus insurance plus freight. Thus, oil price acts as a regime-driving variable for CIF prices. This border price classification is relevant in the present analysis since the 24 commodities in the

Grilli and Yang (

1988) data set are either FOB, CIF, or settlement prices. Therefore, it stands to reason that fluctuations in oil price, which never follow a downward trend, have an impact on the short run and long run behavior of real CIF prices. This rationale implies that a downward trend in real CIF prices is unlikely. In fact, as we will demonstrate shortly when answering RQ2, our results confirm this rationale; the PS hypothesis is not supported in the long run for all nonlinear CIF prices in the

Grilli and Yang (

1988) data series.

The paper also reveals that testing the PS hypothesis depends on whether the nonlinearity in the data generating process, i.e., the log of the real commodity price, is in the mean or the variance of time series.

Fahmy (

2011,

2014) examines the nonlinearity in the mean of the log of the real Grilli and Yang commodity price index,

using a variant of

Granger and Teräsvirta (

1993) and

Teräsvirta (

1994)’s smooth transition regression (STR) model, where inflation and oil price are exogenous threshold variables instead of the conventional autoregressive lags of

. The author confirms the finding of

Persson and Teräsvirta (

2003) that

is nonlinear and stationary when oil price and inflation rate are the regime-driving variables in the STR model. The author shows that nonlinear FOB prices are driven by inflation, whereas nonlinear CIF prices are driven by the price of oil.

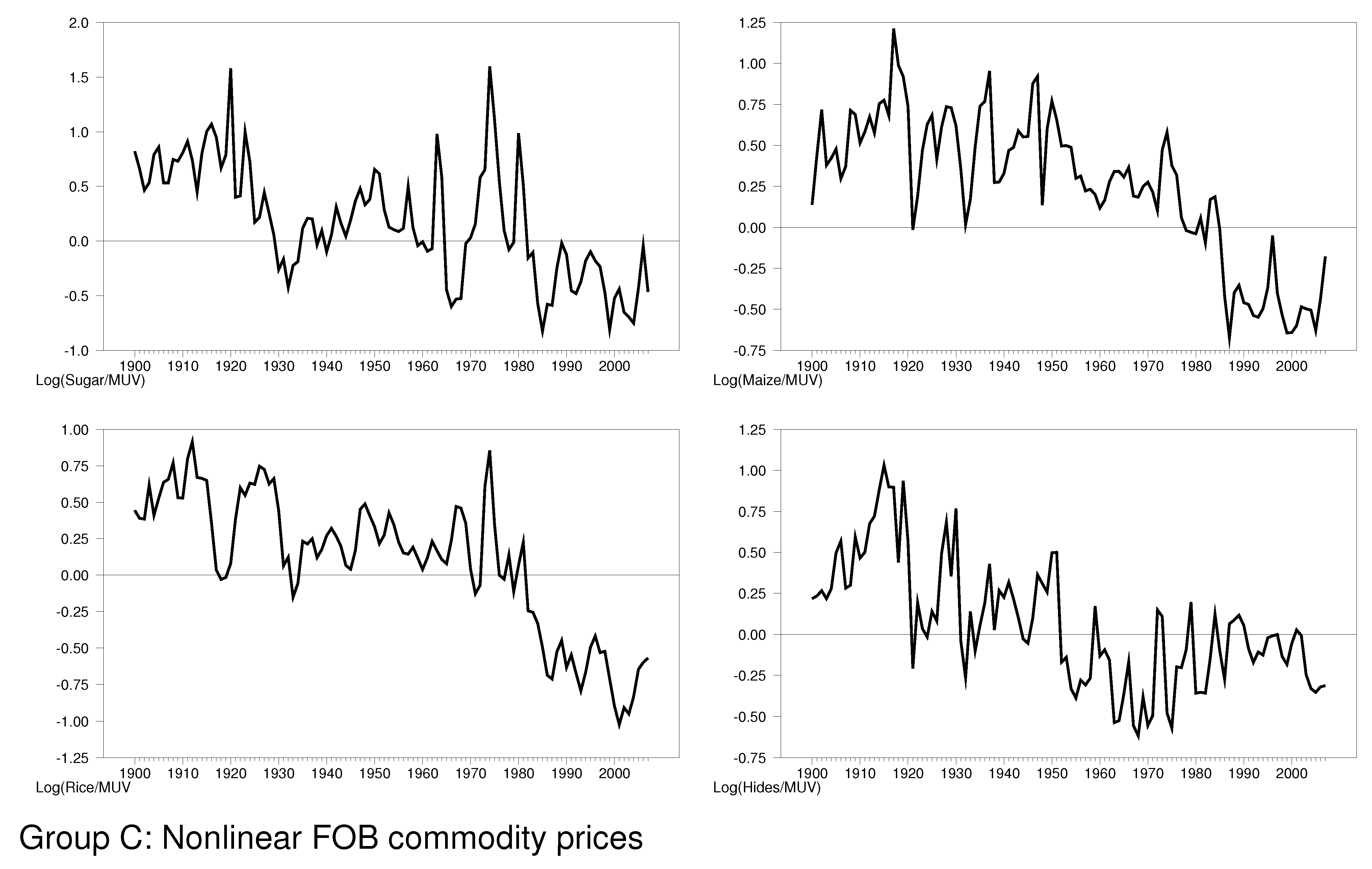

Fahmy (

2017) investigates further the nonlinearity in the 24 individual commodity series and documents four classifications of nonlinearity modeling. The first group, denoted by Group A in the text, is the ARCH group, where nonlinearity is captured in the variance of the real commodity price series using ARCH model or one of its variants. The author reports that the null hypothesis of no ARCH up to order 4 is rejected at the 5% level of significance for Tobacco, silver, jute, lead, cotton, wool, aluminum, and tea. The author fits ARCH and smooth transition ARCH models to these series and successfully captures their nonlinear dynamics. These models are sensible since most of these prices (except for wheat and beef) are settlement or auction prices (see

Table 1) of commodities traded in exchanges and, therefore, tend to exhibit volatility clusters, which is a common feature of stock and option prices. It is worth noting that all commodities in this group are storable commodities and, thus, tend to display ARCH pattern (

Beck 2001;

Muth 1961). For the remaining 16 commodities, the author tests the null hypothesis of linearity against the alternative of a nonlinear STR model (

Luukkonen et al. 1988;

Teräsvirta 1994) and does not reject the linearity for tin, lamb, zinc, rubber, copper, cocoa, wheat, and Beef. The author, therefore, classifies the previous 8 commodities in Group B; the linear group. Finally, the remaining 8 commodity prices that passed the nonlinearity test were classified, based on their border prices, in two groups: nonlinear FOB prices (Group C) and nonlinear CIF prices (Group D). The last column of

Table 1 summarizes the previous classifications and their corresponding econometric models. We argue that the previous classifications are useful in explaining the results of the present analysis. For instance, as we will discuss shortly, the PS hypothesis is not supported in the long run for all storable ARCH commodities in Group A. This is sensible since these price series display volatility clusters and lack downward trends. Additionally, the PS hypothesis is not expected to be supported for Group D since CIF prices are driven by continuous turbulence in the oil market. Our results also confirm this observation. It is also sensible to expect that the linear group supports the PS hypothesis since it is likely for linear real commodity prices to display trends. Our results show that, for this group, the PS hypothesis is supported in the short run but not the long run. This could be justified by the early structural breaks in the series in 1921 (

Cuddington and Urzua 1989) and the breaks in 1937 and 1975 (

Powell 1991).

4. Empirical Analysis

We apply the DWT decomposition in Equation (

11) to

, for every commodity price

i in the data set, and

. The multiresolution analysis decomposes the 108 annual observations (1900–2007) available on the time series into four details;

, and one smooth components

The time scale

stands for the finest level in the series and represents the highest frequency that occurs at the 2-year scale,

stands for the next finest level in the series and represents the 4-year scale,

for the 8-years scale, and

for the 16-year scale. Finally,

represents the long run trend in the series. Thus,

captures the short run behavior of the time series, whereas

captures the long run. The next step is to run the regression in Equation (

6), for each commodity price

i, twice, one time for short run time scale,

, and another for the long run trend,

Finally, we test the restriction that

in the short- and the long-run.

Table 2 summarizes the previous results for the commodity index, i.e., for

in

In particular, the table shows the ordinary least squares estimates of the slope coefficient,

, in the decomposition of Equation (

6) for the Grilli and Yang commodity price index, where the value between brackets underneath the coefficient is the p-value. Although, we care about the estimation results pertaining to

(short run) and

(long run), for the sake of completeness, we report the results for all resolutions. The null hypothesis

is not rejected in the short run and in the long run. Moreover, we also note that the null hypothesis

is not rejected in the short run and long run. Thus, the results do not support the PS hypothesis for the real Grilli and Yang commodity price index. This result is consistent with the findings of

Von Hagen (

1989), who uses the same co-integration approach. It is also consistent with other studies that do not support the PS hypothesis, e.g.,

Powell (

1991).

We repeat the same analysis for each individual real commodity price series and report the results in

Table 3. By looking at the results in

Table 3 and following

Fahmy’s (

2011,

2014,

2017) classification of commodity prices, we note that the PS hypothesis is not supported in the long run for all storable ARCH commodity prices (Group A), with the exception of wool. One explanation is that most of these real commodity prices are settlement and auction prices that are more likely to display ARCH pattern in their volatility rather than a downward trend. The PS hypothesis is also not supported in the long run for all linear commodity prices (Group B), with the exception of beef. It seems, however, that most of the linear group series support the PS hypothesis in the short run. This could be justified by the early structural breaks in the series in 1921 (

Cuddington and Urzua 1989) and the breaks in 1937 and 1975 (

Powell 1991).

Before discussing the results pertaining to border prices, i.e., Groups C and D, it is worth noting that the real prices of all commodities in these two groups were considered in

Fahmy (

2011). The author, as a starting point of the analysis, tests for stationarity and does not reject the stationarity in the price series. He further considers the hypothesis that they might be nonlinear. The author then proceeds to test the linearity hypothesis in

for every

i price against the smooth transition regression model with a set of potential transition/regime-driving variables that includes oil price, inflation, a time trend, and the autoregressive lags of

The author reports that, for FOB prices, the real price of sugar, rice, and maize are nonlinear and driven by their autoregressive lags, whereas the nonlinearity in hides is driven by inflation.

4 On the other hand, for CIF prices, the author documents that the price of oil is the best

exogenous transition variable that can capture the nonlinearity of CIF prices. Guided by

Fahmy’s (

2011) results and the present PS tests results for hides, bananas, palm oil, coffee, and timber in

Table 3, it seems that the PS hypothesis is not supported for all nonlinear real border prices (FOB or CIF) that are driven by

exogenous transition variables (e.g., inflation and oil price). This is sensible because if the price series is nonlinear and stationary, the resulting mean reversion behavior should contradict the PS hypothesis. This finding supports the argument that classifying commodity prices according to their border prices contribute to the assessment of the PS hypothesis (RQ2).

The puzzling result, however, is the support of the PS hypothesis for stationary nonlinear FOB series that are driven by their autoregressive lags as shown from the PS tests results for sugar, rice, and maize in

Table 3. One reasonable explanation for this anomaly is that when nonlinearity in a time series

is driven by one of its autoregressive lags

, for

, the multiresolution analysis smooths the series over various time scales, thus amplifying the effect of structural breaks. This, in turn, could lead to a rejection of

in some time scales and an acceptance in others. For instance, the PS hypothesis for all three commodities (sugar, rice, and maize) is not supported in the intermediate time scales (4-year and 8-year scales) as shown from the estimation results in the third and fourth columns of

Table 3. The implication of this finding is that the choice of the econometric model and the existence of structural breaks do impact the PS hypothesis. This is consistent with the consensus in the empirical literature that the assessment of the PS depends on the starting point of the analysis (e.g.,

Ardeni and Wright 1992;

Bleaney and Greenaway 1993;

Cuddington and Urzua 1989;

Grilli and Yang 1988;

Harvey et al. 2010;

Helg 1991;

Kellard and Wohar 2006;

Leon and Soto 1997;

Lutz 1999;

Newbold and Vougas 1996;

Powell 1991;

Sapsford 1985;

Spraos 1980;

Thirlwall and Bergevin 1985;

Trivedi 1995;

Zanias 2005) While the focus of the present study is to test the PS in the short- and long-run, i.e., in the 2-year and 16-year scale, respectively, it is worth noting that the impact of structural breaks when a different econometric model is used over the entire period of the price series is crucial on the assessment of the PS hypothesis.

Ocampo and Parra (

2004) argue that deteriorations in the terms of trade have been discontinuous aside from the 1920s and the 1980s periods.

Balagtas and Holt (

2009) add that standard unit root tests, such as

Perron’s (

1989) test, may provide misleading results price depending on the extent of structural breaks in the data. For that reason, recent research examining the PS hypothesis has focused on employing unit root tests where the possibility of structural breaks is allowed (e.g.,

Cuddington et al. 2006;

Kellard and Wohar 2006;

Leon and Soto 1997;

Zanias 2005).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}