5.3. Regressions on Asset Classes

The results of the regressions for each asset class for the low and the high volatility regime are presented in

Table 6 and

Table 7, respectively. Under the low volatility regime, we find empirical evidence that a significant exposure exists across almost all assets of our panel to changes in interest rates, with the exception of materials and communication services equity sectors as well as oil-related commodities. For equities, the impact of a positive change in interest rates is globally negative, which can be explained by both a higher discount factor used for DCF-based valuations (widely used for sectors such as information technology) and a higher cost of debt (for the most indebted sectors such as utilities and real estate for instance). As one can see in

Table 7, the return exposure for these sectors to interest rates remains strong in the regime of high volatility of inflation forecasts. As expected, the full panel of fixed income assets presents a significant negative exposure to interest rates variations in both regimes, with convertible bonds showing the lowest beta, which is consistent when considering the hybrid structure of this asset.

Regarding the exposure of our panel to changes in implied inflation, inflation-linked government bonds and oil products present a significant and positive exposure to the variable in both regimes, making them the best hedges to rising inflation forecasts. This result is consistent with the fact that, when investors revise their inflation forecasts upward, they expect a higher coupon from these products due to the inflation indexation. However, as one can see in

Table 6 and

Table 7, the response of inflation-linked bonds is higher in the high volatility regime, which can be counter-intuitive given that we have just seen that the low volatility regime corresponds to periods of large trends in realized inflation to which the coupon is indexed. In fact, it seems that investors quickly incorporate their views in inflation-linked bonds prices and that the rallying realized inflation is mostly priced at the end of the reverting period. This is why the coefficient associated with changes in implied inflation in regime 1 (0.442) remains relatively low when compared to the coefficient associated with changes in interest rates (−3.862). The positive link between Brent/WTI and implied inflation is less surprising, considering that energy prices are one of the major components of inflation.

For other (non inflation-linked) fixed income products as well as for equity sectors, the situation is slightly different. Indeed, we find evidence of a time-varying loading depending on the regime of inflation forecasts. As expected, in the regime of low uncertainty on future inflation, we find no evidence of a significant effect of implied inflation on these assets, indicating that an upward revision does not lead to any movement in equity returns in this regime. This means that, in regime 1, changes in implied inflation are not priced in equity returns by market participants, supporting the fact that the variable is not of interest for equity investors in this regime. The same conclusion applies to fixed-income products (except inflation-linked bonds), as well as to gold returns.

In our second identified regime, however, we find empirical evidence that the equity sectors are impacted by changes in inflation forecasts. Indeed, when inflation is highly scrutinized and forecasts are subject to larger revisions, healthcare and energy show an exposure to implied inflation that is significant at a 1% level with −2.218 and 4.098 coefficients, respectively, while the real estate sector shows a coefficient of 2.152 that is significant at a 5% threshold. Hence, the findings of

Amenc et al. (

2009) regarding the inflation-hedging properties of real estate and commodities as real assets have to be mitigated for the corresponding equity sectors. However, our findings support the conclusions of

Bampinas and Panagiotidis (

2016) and

Ang et al. (

2018), which evidenced the good inflation hedging properties of energy-related stocks. On the one hand, energy and real estate equity sectors are good inflation hedges when investors revise their inflation forecasts substantially, corresponding to periods of reverting realized inflation. However, on the other hand, our findings support that only oil as a real asset benefits from upward anticipated inflation in both regimes. Moreover, among equity sectors, energy stocks are the only ones that are positively exposed to implied inflation and for which the exposure to changes in interest rates is not significant. Consequently, in a regime of large upward revisions of inflation forecasts by market participants with increasing interest rates, energy stocks appear to be the best alternative to inflation-linked securities and oil.

Surprisingly, all interest rate assets show a positive relationship to anticipated inflation in regime 2 when controlling for nominal interest rates. Indeed, bond yields can be decomposed between real yield and anticipated inflation, and, therefore, higher anticipated inflation should lead to higher yields and lower bond prices. However, this effect only exists in one of our two regimes and remains quite low, with changes of 0.4%, 0.6%, and 0.5%, for investment grade bonds, high yield bonds, and convertible bonds, respectively, for a 1% change in implied inflation. The inflation beta of nominal and convertible bonds between 0 and 1 indicates that these assets only offer a partial inflation hedging ability. Thus, our findings support the poor inflation-hedging properties of nominal bonds evidenced by

Spierdijk and Umar (

2015). As expected, inflation-linked bonds remain strongly correlated with inflation forecasts with a return of 5.9% for a 1% change in implied inflation. As expected too, the sign of the Z-spread coefficient is negative in both regimes for all fixed-income products, consistent with the fact that, all things being equal, bond prices decrease with a higher credit risk.

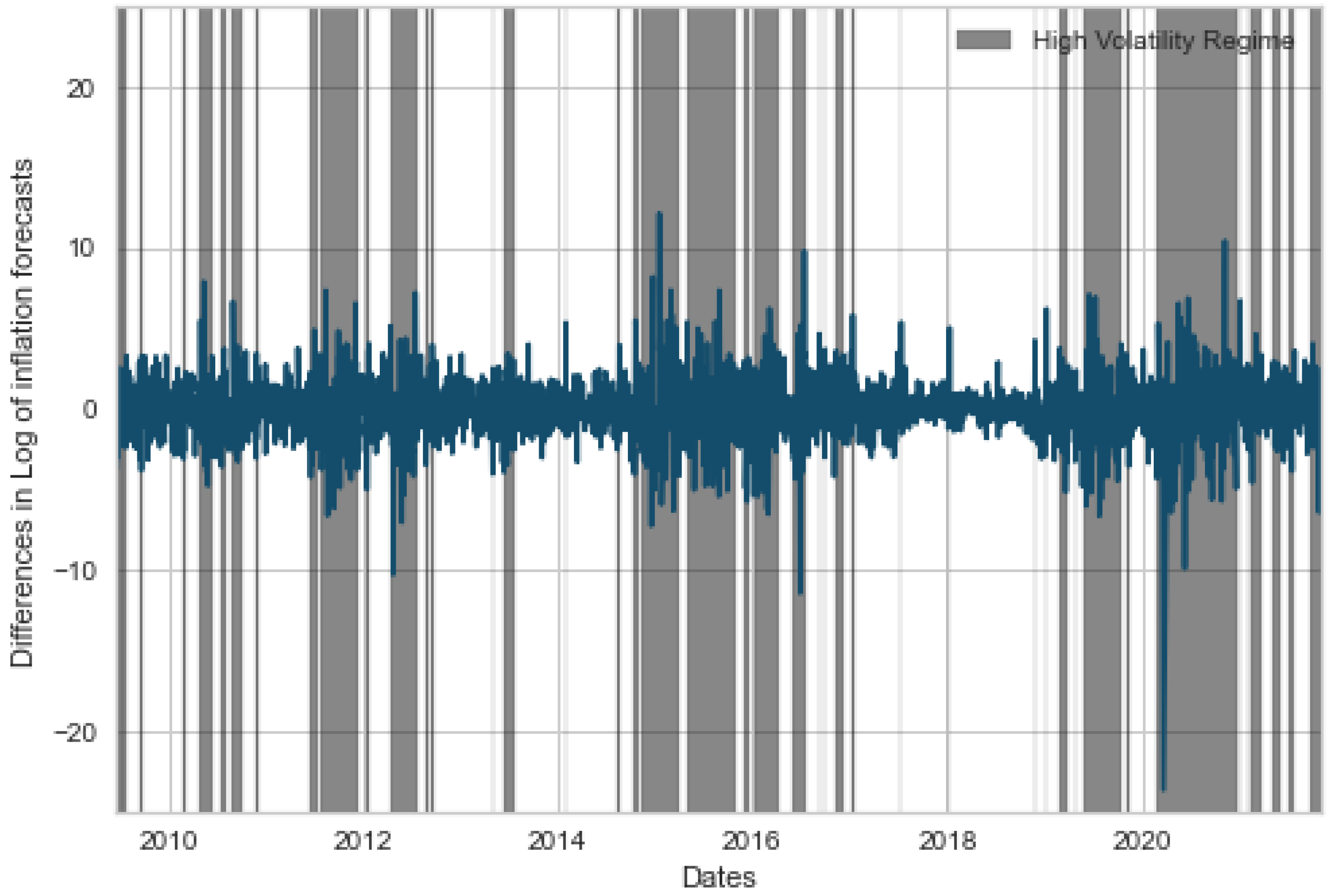

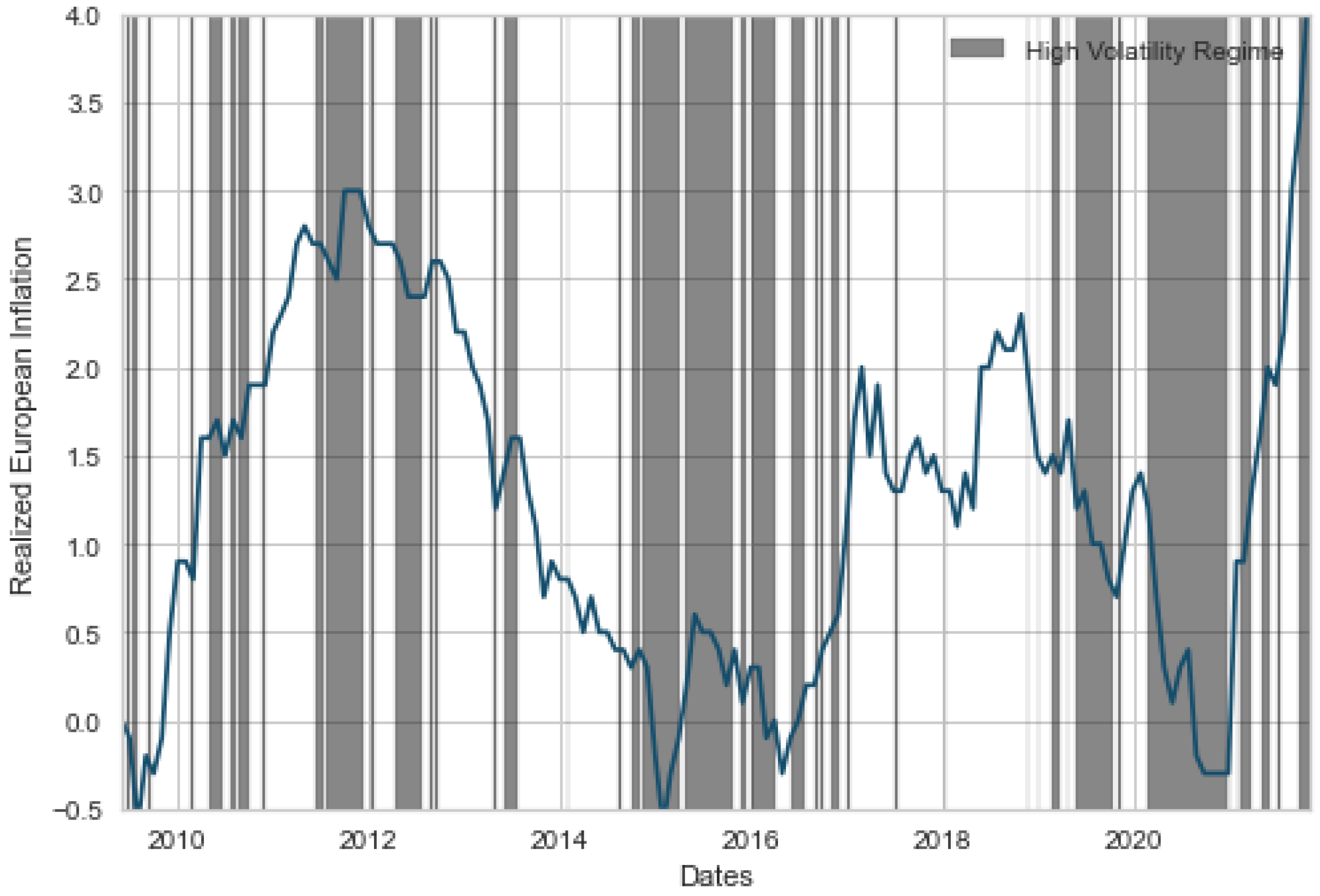

To ensure the robustness of our results, we have conducted similar regressions on various sub-periods of our sample. The persistence of each regime allows to identify periods featuring both a dominant regime and a sufficient number of observations, so as to obtain meaningful results. More precisely, we have identified four sub-periods, each of them associated with a dominant regime. For each sub-period, we conduct regressions using the data points identified by our regime-switching model as being in the dominant regime. The identified sub-periods are the following: from 19 September 2012 to 12 August 2014 and from 13 January 2017 to 25 February 2019, we consider the dominant regime to be the low uncertainty and low interest about inflation. From 7 October 2014 to 7 December 2016 and from 26 February 2019 to 23 December 2020, we consider the high uncertainty and high interest about inflation to be dominant. For the sake of clarity, results are reported in

Appendix A. As one can see, most of the conclusions previously exposed still hold true. Indeed, out of the four sub-periods, oil and inflation-linked securities present a significant inflation beta for three of them. More specifically, for the period from 19 September 2012 to 12 August 2014, none of the assets of our panel show a statistically significant beta to inflation forecasts.

1 Among stock sectors, energy stocks confirm their status of best hedgers with a significant and high inflation beta in both high volatility regimes. On the other hand, real estate stocks, however, do not show empirical evidence of good inflation hedging properties under the high volatility regime between February 2019 and December 2020. However, the Covid-19 crisis has particularly affected real estate stocks in this period and have most likely affected the results for this sub-sample. This brings us to moderate our conclusions on this specific sector: even if there exists evidence of significant exposure of real estate stocks to implied inflation in periods of high uncertainty about inflation in the long run, their short term inflation-hedging properties can be disappointing. Concerning fixed-income products, our observations are confirmed with stronger betas in the high volatility regime for nominal and inflation-indexed bonds. We also confirm that nominal bonds offer partial inflation hedging ability with inflation betas constantly below 1. Moreover, the weak link between expected inflation and convertible returns seems to be confirmed, with no evidence of a significant inflation beta in any sub-period.

Overall, our results support the hypothesis that inflation-hedging properties of asset classes are regime-dependent

Briere and Signori (

2012),

Spierdijk and Umar (

2015). We find that some asset returns can be good hedges when inflation forecasts are significantly revised in the Euro area. More importantly, all asset classes display better inflation-hedging properties in these periods when they are the most needed. However, we confirm that the overall equity market as well as the nominal bond market offer poor hedging properties in the long run in the Euro area, which contradicts the findings of

Salisu et al. (

2020) in the US stock market. From our perspective, oil-related commodities and inflation-linked government bonds remain the best assets to hedge inflation for a passive investor.

{kind=link}

{kind=link}