1. Introduction

Housing markets are characterised by incomplete information, costly search, decentralised transactions, and low trading volume (

Quan and Quigley 1991). The price discovery process of housing assets can be inferred from recent limited transactions or from appraisal values set by valuers. In Commonwealth countries, including New Zealand, governments periodically provide the general public with their official appraisal values of properties, also known as capital values (

CVs), for the purpose of collecting rates. Market participants in those property markets commonly refer to these appraisal values in setting the listed prices. However, government appraisals constantly refer to the market transaction prices (

TPs) to estimate

CVs. Many studies have demonstrated the phenomenon of “appraisal smoothing”, in which appraisers rely on historical prices to determine the appraised values (

Ibbotson and Siegel 1984). From a behavioural science perspective, the

CV is argued to be a price “anchor” because market participants, either buyers or sellers, refer to the

CV as a price point at which to start their negotiation process. More importantly, this information is publicly available at no cost.

Using the terminology of time series analysis, the movement of transaction prices (TPs) is said to lead the capital values (CVs) in the appraisal process. In contrast, capital values (CVs) lead the transaction prices (TPs) in the negotiation process. This study aims to test the hypothesis of such a lead-lag relationship between the TP and the CV movement over time. We make use of the primary (first-hand) and secondary (second-hand) housing markets in New Zealand to test two hypotheses on CV and TP (i.e., anchoring effect). The less trivial implication is to exploit the fact that no CV is available for buyers in the primary housing market. Thus, in the primary housing market, the TP is hypothesised to lead the CV, whereas in the secondary housing market, the TP and the CV are hypothesised to have a bi-directional lead–lag relationship. Primary housing transactions refer to the sale of newly or to-be-completed (first-hand) houses from developers, whereas secondary housing transactions are the sale of existing (second-hand) houses from house owners. In this study, the house transaction data of New Zealand from January 1990 to December 2020 is used. The dataset is subscribed from Corelogic, an international real estate data services provider. The apartment type property, vacant lands, and leasehold properties are excluded from the dataset to keep the consistency of property type.

This paper is structured as follows. In

Section 2, we review the literature on the effect of property valuations on transaction prices and the anchoring effects of appraised values in the property market. In

Section 3, we outline the research design. In

Section 4, we present the data with the empirical results. In

Section 5, we conclude with our findings and the implications of the study.

2. Literature Review

Property appraisal values and transaction prices affect each other in a real-life context. The development of valuation theory is worthwhile for empirical testing (

Parker 2006). In property valuation, the most common appraisal method is using comparables. This method requires appraisers to make reference to the market prices of recently transacted properties (

RICS 2019). Property appraisal values are therefore intrinsically reliant on market prices, and it is expected that changes in market prices cause changes in appraisal values.

Kain and Quigley (

1972) found a systematic error in estimated house prices, which was attributable to the socio-economic characteristics of the owner-occupants, and the knowledge of these estimation biases can be used to improve the accuracy of both the individual and aggregate estimates of market value.

Raymond and Love (

2000) also suggested that, when buyers set their initial offers, they always take the appraised value as a useful estimate to start with the negotiation process.

With the availability of online market transaction data at almost zero cost, an interesting question is whether home buyers and sellers refer to usually out-of-date appraised home values, recent market house prices transacted nearby, or both.

Seiler et al. (

2014) suggested that homeowners are prone to accept information from experts or authorities instead of that from other participants on the market. This finding suggests that the appraised value from the government is prone to be considered an “authorised” benchmark for many homeowners.

Diaz and Hansz (

2001) raised the hypothesis that there is an anchoring and adjustment heuristic by testing whether valuers rely on any reference point when making judgements. The results show that, when valuers face uncertainty in an unfamiliar area, they are more likely to rely on previous price information to make their judgements. This result also applies to laypeople participating in the property market. Ordinary buyers and sellers are usually more vulnerable than valuers in an unfamiliar area and are more likely to rely on “reference points”.

Chandrashekaran and Grewal (

2006) studied how “selling price” and “advertised price” influence buyers’ internal reference price. The results show that, when the selling price exceeds the internal reference price of buyers, the price discrepancy exerts upward pressure on buyers’ internal reference prices. The opposite outcome follows when the selling price falls below this internal reference price. In addition, the advertised price also partially affects the internal reference price. When the “internal reference price” aligns with the property buyer’s estimate, the listed or advertised price influences homebuyers’ perceptions by “anchoring” such external information. Studies on anchoring can be traced back to

Simon and Newell (

1971), who indicated that people’s limited problem-solving capacity needs cognitive efficiency or shortcuts to decision making.

Tversky and Kahneman (

1974) showed that people are prone to use heuristics to achieve a more straightforward judgemental operation. “Anchoring and adjustment” is one of these heuristics.

Einhorn and Hogarth (

1986) indicated that information from the external environment is often used as anchors when people make estimations under uncertainties, especially in housing markets where heterogeneous characteristics are always a problem.

The anchoring effect is a widely accepted theory supported by empirical evidence from stock market decision making (

Chang et al. 2013), auctions (

Dodonova and Khoroshilov 2004;

Gao and Cao 2019), and consumer price negotiation (

Kristensen and Gärling 2000). In the property literature, researchers have also found the anchoring effect in the home purchase decision-making process.

Gallimore (

1994) showed that valuers are affected by heuristic biases in the valuation process.

Diaz and Hansz (

2007) found that real estate professionals seek simplified heuristics to facilitate information processing. More specifically,

Diaz and Wolverton (

1998) revealed that the appraisal value is anchored with previous value judgement, causing the appraisal smoothing problem. Compared with property professionals, ordinary home buyers and sellers, who are less experienced and have access to less market information, tend to be influenced by the anchoring effect to a larger extent.

Northcraft’s and Neale’s (

1987) findings suggest that anchoring biases influenced both professionals and laypersons but that the laypersons appeared to be more reliant on the pre-set “anchor”.

Silva et al. (

2019) also demonstrated that the anchoring effect influences both property professionals and non-professionals, and non-professionals are more prone to be influenced.

Scott and Lizieri (

2012) found a strong anchoring effect on the price perceptions of homebuyers. In terms of residential property auctions,

Bucchianeri and Minson (

2013) indicated that a higher listing price (anchor) is associated with a higher transaction price. An anchoring bias even exists in public housing purchases (

Arbel et al. 2014).

More recent research also provides evidence that the anchoring effect is likely to influence the price perceptions of market participants.

Khezr and Ahmad (

2018) found that property buyers tend to use the asking price as the anchor or reference point of the desired price. They suggested that buyers consider that the subject property may have some unobserved characteristics, so they raise their expectations and then raise the price.

Shie (

2019) found that property historical peak price is used as a reference point. They found that the 9-year-high price positively correlates with the price return.

Cheung et al. (

2021) conducted a natural experiment and found that anchoring effects dominated the asymmetric information effect in the housing market of Hong Kong.

Although many studies have already suggested that home buyers and sellers rely on price anchors in their decision-making process, most of this literature was conducted a decade or more ago. Market information was not as readily available as it is now on the Internet. Property technologies such as “Blockchain”, “Property Passports”, or “Automated Valuation Models” in recent years have made valuation much faster and cheaper.

Abidoye et al. (

2022) investigate the barriers, drivers, and prospects of adopting artificial intelligence valuation methods in practice. Whether home buyers and sellers anchor to the traditional appraisal values or to market transaction information is the fundamental research question of this study.

3. Development of Hypotheses

Many previous works in the literature suggest that the anchoring effect plays a significant role in the property industry, especially when market participants estimate property values. They seem more prone to anchor to some external information. In New Zealand, capital value, or

CV, is the value of the property appraised by the government used for collecting property rates. The Government of New Zealand is required to carry out an assessment of property value to set rates every three years according to the Rating Valuations Act 1998.

CV is also sometimes called Government Valuation (GV) or Rateable Value (RV). The

CV is defined as “the most likely selling price at the date of valuation” (

Auckland Council 2021). Even though it is explicitly stated that “the aim of the general property revaluation is not to provide values for property owners to use for marketing, sales or any other purposes” (

Auckland Council 2021), the information of the

CV becomes trusted pricing information, which market participants often use to assess property values. Property sellers sometimes use the current

CV in marketing efforts for their properties, and

CV becomes a reference point in buyers’ decision making (

Filippova 2014).

This research exploits the lead–lag relationship between the appraisal values and market prices of residential properties in New Zealand to examine whether anchoring effects exist. The lead–lag relationship plays a crucial role in asset markets. Some stock pairs may not have a concurrent correlation in financial markets but may be highly correlated during certain lead–lag periods. This phenomenon, whereby a time series partially or entirely replicates the movements of another at a specific time lag, is called the lead–lag relationship. Provided that home buyers and sellers use the

CV as an anchor in their price negotiation, the movement of the

CV leads the movement of transaction prices (

TP). Nevertheless, when considering the method used in estimating

CVs, the movement of the

TP leads the movement of the

CV instead. The Rating Valuation Rules 2008 (

Land Information 2010, p. 25) also explicitly states that

CV estimation is “compared to the market sales evidence”. Theoretically,

CVs are always lagging behind

TPs in the valuation process.

To avoid this simultaneous causality bias and to examine whether anchoring effects to the

CV exist, we exploit a less trivial implication between the primary and secondary housing markets to infer the anchoring effect. We make use of the fact that no

CV is available for buyers in the primary housing market. In Auckland, primary residential properties are pre-sold before completion of their construction. When a first-hand property is sold, its

CV is not yet appraised by the government. Meanwhile, the

CV of a second-hand property is appraised every three years, and therefore it has at least a three-year new appraised value for the second-hand property. The valuers of an independent organisation value the

CV by using mass valuation technology. The recent sales transaction data in the area and other factors of the subject property, including property type, location, land size, zoning, floor area, and improvement work, are considered. The property values are audited by the Valuer-General to ensure accuracy (

Auckland Council 2021). Therefore, in this research, we separate primary and secondary sales transaction data to distinguish properties with different statuses of

CV appraisal. Thus, in the primary housing market, the

TP is hypothesised to lead the

CV, whereas in the secondary housing market, the

TP and the

CV are hypothesised to have a bi-directional lead–lag relationship. Thus, we hypothesise that at the aggregate market level:

Hypothesis 1. (H1-Anchoring Effects) In the primary housing market, the index of the TP unidirectionally leads the CV, whereas in the secondary market, the TP and the CV has a bi-directional lead–lag relationship.

To confirm the anchoring effect of

CVs, we further derive a testable implication based on the availability heuristic, which influences probability judgements according to a person’s ease in recalling previous occurrences of an event or in imagining an event occurring (

Tversky and Kahneman 1973;

Bazerman and Moore 2012). For example, investors may judge the quality of an investment based on information that has recently been in the news, ignoring other relevant facts.

CVs are well-known public information among property market participants in New Zealand, and the public can easily access the information. The release of

CVs is also the headline news in the local media (

Leahy 2021). For property market participants, such availability of

CVs serves as a pre-condition of the availability heuristic.

In consumer research, the availability heuristic can play a role in various estimates, such as store pricing (

Ofir et al. 2008) or product failure (

Folkes 1988). The availability of information in memory also underlies anchoring effects. In property research,

Gallimore and Wolverton (

1997) studied whether the “pending price” as readily available information influences property valuers’ judgement. The results showed that, when “pending price” becomes readily available in the property information package, it influences the resulting valuation.

Black (

1997) found that during property negotiation processes, the negotiators tended to increase the importance of the readily available information, such as asking prices, whereas information that was hard to cognitively recognise was neglected.

Havard (

2001) contended that people tend to use their experience in similar situations, especially the most recent information, to make a decision.

Evans et al. (

2019) suggested that limited access to information sources increases the use of the availability heuristic. When buyers and sellers do not have enough sources of information, they tend to use the most readily accessible information, such as a

CV, to support their judgements.

In the context of property valuation, when trying to make a home purchase decision, the government valuation of the property immediately springs to the forefront of buyers’ thoughts. As a result, they may give greater credence to this information and tend to overestimate the relevance of this government appraisal value when an updated appraisal is available. The availability heuristic operates on the principle that the information must be important if one can think of it when making a decision. All people tend to believe that things that come more easily to mind are more accurate reflections of the real world, and the available information regarding property values is no exception. The longer we preoccupy ourselves with such pricing information, the more available it is in our minds. Moreover, we are more likely to treat this pricing information as an anchor (or a price point). Excessive media coverage can also cause this to happen. Thus, we further hypothesise that in each transaction:

Hypothesis 2. (H2-Availability Heuristic) The impact of the CV anchoring effect is larger in the year of reassessment, and the effect diminishes over time.

5. Empirical Data and Results

The models are empirically tested using housing transaction data of New Zealand, from January 1990 to December 2020 (372 months), which provide about three million housing transactions. An extensive housing transaction dataset helps to exclude any potential estimation problems due to insufficient data. The dataset is subscribed from an international real estate data provider, CoreLogic. This study confines freehold house-type transactions by excluding apartment-type housing, vacant sites, and leasehold interests from the dataset to keep housing type and land tenure uniform. The dataset provides a comprehensive list of housing characteristics and neighbourhood characteristics, including the age of houses, to identify whether they are transacted in the primary or secondary markets. Typically, the government’s official district valuation roll only includes the built cohorts in the decade for each individual property. The building age variable is unavailable from those official property data sources, including the property data we purchased from CoreLogic. Therefore, this study gathers information on the home-built year from online property platforms, such as OneRoof.co.nz (

Yiu and Cheung 2022). Other attributes include the number of bedrooms and bathrooms, building floor area, regions, and views.

In Auckland, primary residential properties are mostly pre-sold before construction is complete. When the first-hand property is sold, its CV is not yet appraised by the government. In contrast, as per the conduct rule of revaluation, the CVs of second-hand properties are appraised every three years, so all properties in the secondary market have at least a three-year new appraised value. Therefore, in this research, we separate the primary sales transaction data and the second-hand transaction data to distinguish properties with different statuses of CV appraised.

Among 3,203,047 total observations, 2,838,747 observations contain data on the building’s age; therefore, we can only use 2,838,747 observations to conduct the tests. We can separate the primary and second-hand residential properties by extracting the properties with building age equal zero. After separating the first-hand and second-hand transactions, we have 2,387,483 s-hand transactions and 451,264 first-hand transactions. The data on property transactions and the CV information are not directly used in the test as heterogeneous characteristics of properties. In order to control the quality differences in the transacted properties and produce the appropriate indices for the TP and the CV, we use the hedonic regression model to produce the indices. Using this method, we can produce price indices that control the implicit prices of property characteristics.

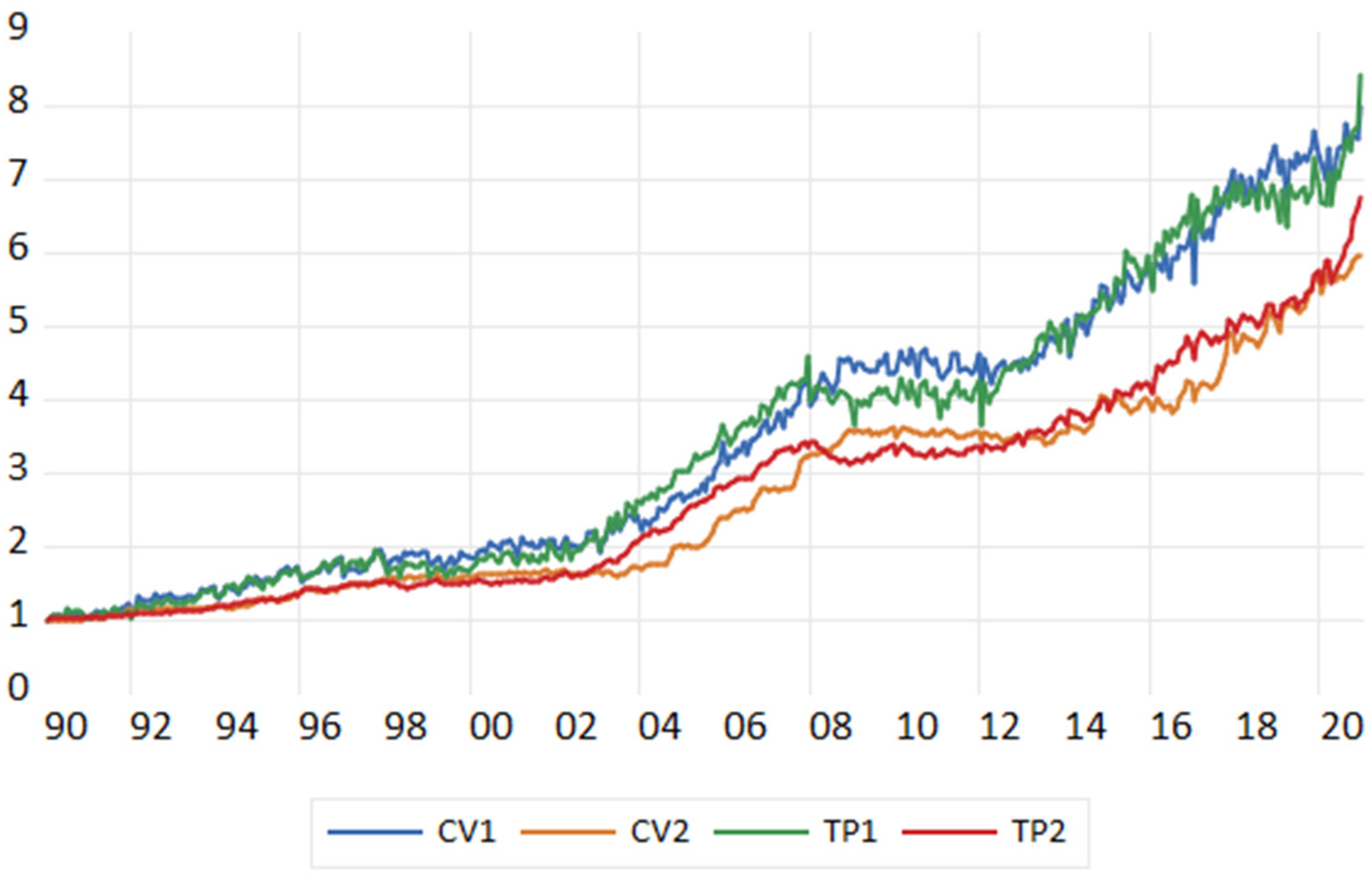

To examine the lead-lag relationship between capital values and transaction prices in both primary and secondary housing markets, four house price indices are constructed by the hedonic price model, viz., (a) hedonic house prices index in the primary market (

TP1); (b) capital values index in the secondary market (

CV2); and (c) hedonic house price index in the secondary market (

TP2). For the capital value index of the primary market (

CV1), we use the estimated

CV typically released by the government after the housing transaction. It is worth noting that, for about 10% of first-hand sales, their

CVs are released immediately before and around the sales dates. To avoid cherry-picking the data and incurring confirmation bias, we have included these cases in our

CV1 index construction to take into account the possibility that, in some cases,

CVs can be earlier than the sale date. If the results with such

CV1 remain, it provides an even stronger case to support our anchoring hypothesis.

Figure 1 shows the four house price indices.

The descriptive statistics for the data are shown in

Table 1. For the house price index of the first-hand market (

TP1), the mean of

TP1 is 3.46, whereas the mean of

TP1 from 1990 to 2009 is 2.26. The mean of

TP1 from 2009 to 2020 is 5.63, which increased by 149% after the Global Financial Crisis (GFC). For the house price index of the second-hand market, from 1990 to 2009, the index was 1.83, whereas from 2009 to 2020, it was 4.23. The

CV in the first-hand market is 2.08 for the pre-GFC period and 5.34 for the post-GFC period, and the

CV in the second-hand market is 1.78 for pre-GFC and 4.11 for post-GFC. Even though the GFC “raided” the market, the change of

TP and

CV still kept the same pace.

The descriptive statistics for the data in the hedonic models are stated below: the mean of the transaction price is NZD323256.8, whereas for the CV, the mean is NZD288902.8. In a booming property market, the earlier appraised value should be lower than the price that occurs later. The mean number of bedrooms in the dataset is 3.126, whereas the mean number of bathrooms is 1.398. The average floor area is 125.708 sm. The time dummy variable is monthly data from 1990M01 to 2020M12. The regional dummy variable includes 14 regions, and the View dummy contains three types of view: ‘No appreciable view’, ‘focal point of water view’, and ‘focal point of other views’.

Empirical Results

In order to conduct the Granger causality test between two time-series, we need to ensure the data is stationary by making sure that none of our datasets has any unit root. To test the stationarity of the variables, we use the Augmented Dickey–Fuller test and the Kwiatkowski–Phillips–Schmidt–Shin test. The results are shown in

Table 2. All the variables are not stationary at I (0), whereas at I (1), all the time series variables show as stationary. Therefore, we need to use first differenced data for all the time series variables and follow the modified Granger causality processes to conduct the test.

Using the AIC test, we are able to determine the lag periods. The AIC test results for the lag length used for the Granger causality test between the natural logarithm of the first-hand

TP and the natural logarithm of the first-hand

CV are shown in

Table 3. The optimal lag length

p is 2 (months) after first differencing

dln(TP1) and

dln(CV1), whereas the maximum order of integration

m is 1. Then, we use

p +

m, which is 3 (months), as the lag length between

dln(TP1) and

dln(CV1). At the same time, the result between the second-hand

TP and the second-hand

CV after first differencing

dln(TP2) and

dln(CV2) shows that the optimal lag length

p is 12 (months). By adding the maximum order of integration (

m) 1, the lag length we use for the Granger causality test between

dln(TP2) and

dln(CV2) is 13 (months).

Table 4 shows the results of Granger causality tests, which in the first-hand market, the

TP does not Granger-cause the

CV, nor does the

CV Granger-cause the

TP while in the second-hand market. In the secondary market, the null hypothesis of “

dln(TP2) does not Granger-cause

dln(CV2)” is rejected at 5 × 10

−5 the

p-value, and the null hypothesis of “

dln(CV2) does not Granger cause

dln(TP2)” is also rejected at 2 × 10

−8 the

p-value. This indicates that the result shows that

CV Granger-causes

TP and vice versa in the second-hand market.

As shown in the results, in the first-hand market, CV and TP do not Granger-cause each other because the Auckland Council does not appraise the pre-sold properties at the time of being sold. The appraised value is only available for the rates payment when the property is handed over to the owner. The time of the property CV being appraised is usually 1 to 3 years later than the time the property is sold; therefore, valuers do not treat the sold price as the only piece of useful information.

Nevertheless, in the second-hand market, CV and TP Granger-cause each other, which shows that the CV influences the property transaction price. The CV as price information influences the transaction price by influencing the perception of market participants, and it is more similar to the “market news” in the stock market that directly influences the market participants’ value perception. When they receive CV information, they estimate the price based on the CV and consider that the price should be somewhere around the CV. Meanwhile, for sellers, their readily available information that they could use to assist in determining the selling price is a CV, so they can also use the CV to set the asking price.

Table 5 shows the results of the difference-in-differences test on the

CV’s outdatedness effect on the anchoring strength on the

TP from the

CV. The results show that the anchoring strength of the

TP from the

CV is as strong as 93.5%, which is statistically significant at the 1% level. However, the anchoring strength is conditioned by the timeliness of the appraisal. Every one-hundred-day increase in the

CV timeliness reduces the strength of anchoring effects by 1%. The timeliness of the anchoring strength shows that the market participants, such as home buyers and sellers, are aware that the

CV is not always up-to-date information; it only represents the value of the property at the time of being appraised. As time goes by and the market changes, the true value of the property deviates from the

CV. Therefore, farther from the valuation date of

CV, the market becomes less reliant on the

CV in the transaction.

6. Conclusions

Anchoring effects are among the most robust cognitive biases in judgement and decision making. This study explores whether the property market elicits such a decision heuristic. Many laboratory experiments have suggested that some artificial information context causes people to use heuristics that produce decision biases. However, the controlled nature of laboratory experimentation often constrains the amount and types of information. This has not allowed subjects in the experiment to interact with and explore different information sources. This study uses the property market as a case study to examine two acknowledged decision heuristics in behavioural economics, namely the anchoring effect and the availability heuristic, in an information-rich property market. The results described in this paper are consistent with both the anchoring-and-adjustment effects and the availability heuristic.

Most home buyers and sellers are laypersons of the property industry. They may be prone to use heuristics when making estimations or judgements. In New Zealand, capital value (CV) is recognised as a trustworthy external information source from the government. Such information provides a shortcut that helps laypersons set their listing prices and make their home purchase decisions. Using both the time-series and hedonic pricing model approach, this study draws a less trivial testable implication: the CV in primary housing should have no anchor effect on the TP because the CV is unavailable until the first sales occur. Exploiting the fact that no CV is available for buyers in the primary housing market, the Granger causality test results suggest that the CV and TP have a bi-directional lead-lag relationship in the secondary housing market, but not in the primary market. The finding implies the existence of anchoring effects in the property market. Furthermore, the hedonic model at the individual transaction level shows that price anchoring effects may diminish over time. This is consistent with the notion of the availability heuristic, i.e., people are more reliant on a CV when it is released near the date of reassessment.

It is also crucial to ensure the accuracy of the appraised

CV. Even though the government has accentuated that “the aim of the general property valuation is not to provide values for property owners to use for marketing, sales or any other purposes.” (

Auckland Council 2021), based on our results, it is unavoidable that people use

CV as an anchor. In practice, buyers and sellers believe that the real market price of the property should be adjusted with a certain margin based on the

CV. However, for ordinary buyers and sellers, it is hard to obtain an accurate value of the property by using the

CV only and without using any objective market information that they are unable to access, and it is also possible that the

CV is not accurate and outdated. Therefore, it reminds us that the property price may be distorted by the inaccuracy and inappropriate use of appraisal values.

_Cheung.jpeg)

{kind=link}