Board Characteristics and the Insolvency Risk of Non-Financial Firms †

Abstract

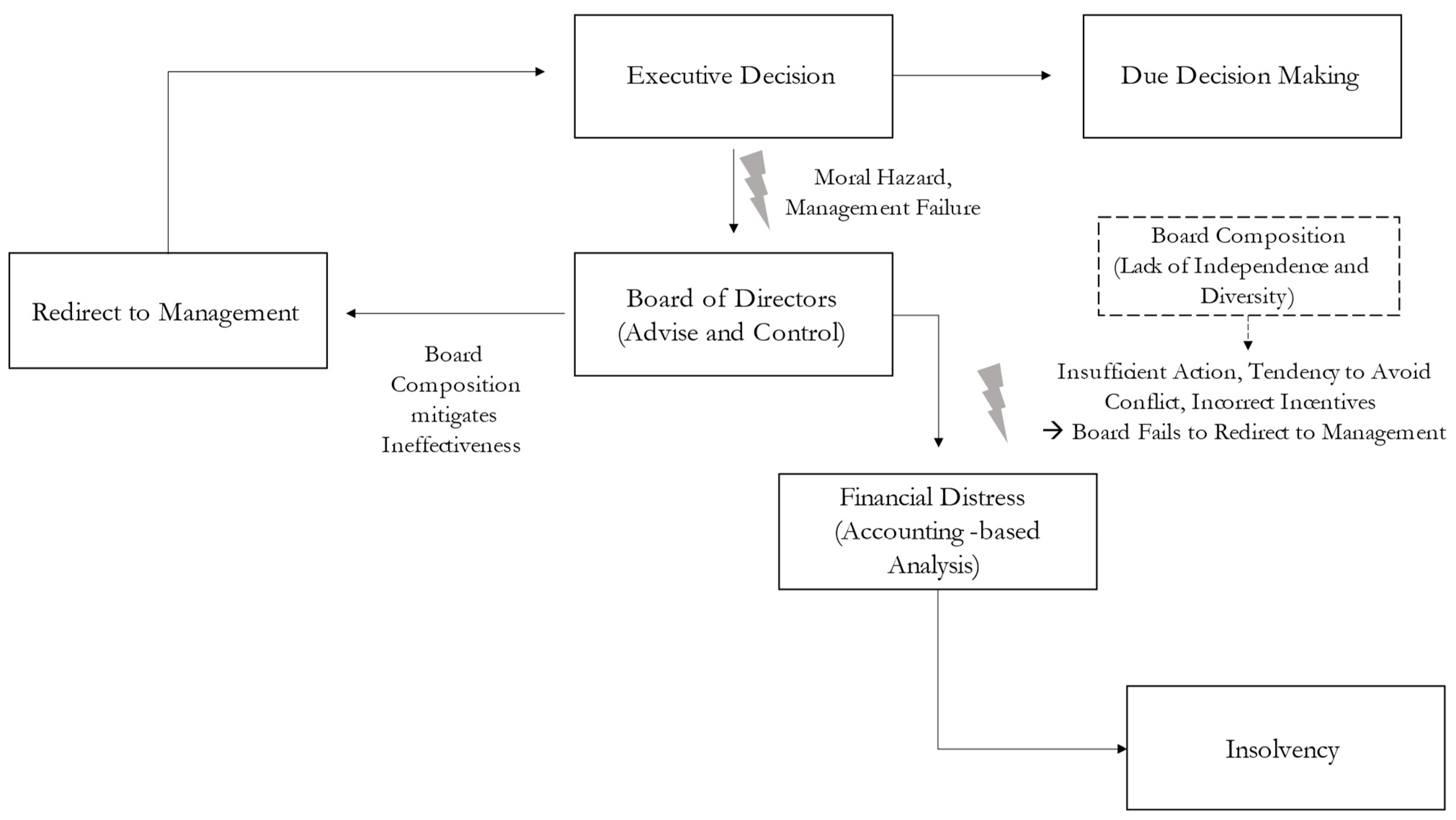

:1. Introduction

2. Literature Review and Motivation

Board Diversity

3. Methodology and Data

3.1. Insolvency Risk

3.2. Econometric Model

3.3. Covariates

3.4. Data

4. Results

4.1. Tests of Hypotheses 1–8

4.2. Alternative Specifications

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Adams, Renée B. 2017. Chapter 6—Boards, and the directors who sit on them. In The Handbook of the Economics of Corporate Governance. Amsterdam: Elsevier, vol. 1, pp. 291–382. [Google Scholar]

- Adams, Renee B., and Daniel Ferreira. 2007. A theory of friendly boards. The Journal of Finance 62: 217–50. [Google Scholar] [CrossRef]

- Adams, Renee B., and Daniel Ferreira. 2009. Women in the boardroom and their impact on governance and performance. Journal of Financial Economics 94: 291–309. [Google Scholar] [CrossRef] [Green Version]

- Aktas, Nihat, Dimitris Petmezas, Henri Servaes, and Nikolaos Karampatsas. 2021. Credit ratings and acquisitions. Journal of Corporate Finance 69: 101986. [Google Scholar] [CrossRef]

- Aktas, Nihat, Eric de Bodt, Frédéric Lobez, and Jean-Christophe Statnik. 2012. The information content of trade credit. Journal of Banking & Finance 36: 1402–13. [Google Scholar]

- Altman, Edward I. 1968. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance 23: 589–609. [Google Scholar] [CrossRef]

- Altman, Edward I., Małgorzata Iwanicz-Drozdowska, Erkki K. Laitinen, and Arto Suvas. 2017. Financial distress prediction in an international context: A review and empirical analysis of Altman’s Z-score model. Journal of International Financial Management & Accounting 28: 131–71. [Google Scholar]

- Bathala, Chenchuramaiah T., and Ramesh P. Rao. 1995. The determinants of board composition: An agency theory perspective. Managerial & Decision Economics 16: 59–69. [Google Scholar]

- Bhargava, Alok, and J. Dennis Sargan. 1983. Estimating dynamic random effects models from panel data covering short time periods. Econometrica 51: 1635–60. [Google Scholar] [CrossRef]

- Blume, Marshall E., Felix Lim, and A. Craig MacKinlay. 1998. The declining credit quality of U.S.corporate debt: Myth or reality? Journal of Finance 53: 1389–413. [Google Scholar] [CrossRef]

- Boone, Audra L., Laura Casares Field, Jonathan M. Karpoff, and Charu G. Raheja. 2007. The determinants of corporate board size and composition: An empirical analysis. Journal of Financial Economics 85: 66–101. [Google Scholar] [CrossRef]

- Boyd, Brian K. 1990. Corporate linkages and organizational environment: A test of the resource dependence model. Strategic Management Journal 11: 419–30. [Google Scholar] [CrossRef]

- Boyd, Brian K. 1995. Ceo duality and firm performance: A contingency model. Strategic Management Journal 16: 301–12. [Google Scholar] [CrossRef]

- Bui, Tat Dat, Mohd Helmi Ali, Feng Ming Tsai, Mohammad Iranmanesh, Ming-Lang Tseng, and Ming K. Lim. 2020. Challenges and trends in sustainable corporate finance: A bibliometric systematic review. Journal of Risk and Financial Management 13: 264. [Google Scholar] [CrossRef]

- Campbell, John Y., Jens Hilscher, and Jan Szilagyi. 2008. In search of distress risk. Journal of Finance 63: 2899–939. [Google Scholar] [CrossRef] [Green Version]

- Cao, Zhiyan, Fei Leng, Ehsan H. Feroz, and Sergio V. Davalos. 2015. Corporate governance and default risk of firms cited in the sec’s accounting and auditing enforcement releases. Review of Quantitative Finance and Accounting 44: 113–38. [Google Scholar] [CrossRef]

- Cathcart, Lara, Alfonso Dufour, Ludovico Rossi, and Simone Varotto. 2020. The differential impact of leverage on the default risk of small and large firms. Journal of Corporate Finance 60: 101541. [Google Scholar] [CrossRef]

- CGLytics. 2020. Wirecard pre- and Post-Scandal: A Board Effectiveness Analysis. Available online: https://www.mondaq.com/directors-and-officers/961974/wirecard-pre-and-post-scandal-a-board-effectiveness-analysis (accessed on 6 May 2022).

- Closset, Frédéric, and Daniel Urban. 2019. The balance of power between creditors and the firm: Evidence from German insolvency law. Journal of Corporate Finance 58: 454–77. [Google Scholar] [CrossRef]

- Dahya, Jay, Orlin Dimitrov, and John J. McConnell. 2008. Dominant shareholders, corporate boards, and corporate value: A cross-country analysis. Journal of Financial Economics 87: 73–100. [Google Scholar] [CrossRef] [Green Version]

- Darrat, Ali F., Stephen Gray, Jung Chul Park, and Yanhui Wu. 2016. Corporate governance and bankruptcy risk. Journal of Accounting, Auditing & Finance 31: 163–202. [Google Scholar]

- Davies, Paul, Klaus Hopt, Richard Nowak, and Gerard van Solinge, eds. 2013. Corporate Boards in Law and Practice: A Comparative Analysis in Europe. Oxford: Oxford University Press. [Google Scholar]

- Donaldson, Lex, and James H. Davis. 1991. Stewardship theory or agency theory: CEO governance and shareholder returns. Australian Journal of Management 16: 49–64. [Google Scholar] [CrossRef] [Green Version]

- European Commission. 2012. Directive of the European Parliament and of the Council on Improving the Gender Balance among Non-Executive Directors of Companies Listed on Stock Exchanges and Related Measures, Brussels (14.11.2012), COD(2012/0299). Brussels: European Commission. [Google Scholar]

- European Commission. 2022. Directive of the European Parliament and of the Council on Improving the Gender Balance among Directors of Companies Listed on Stock Exchanges, and Related Measures, Brussels (4.03.2022, 6468/22). Brussels: European Commission. [Google Scholar]

- Fama, Eugene F., and Michael C. Jensen. 1983. Separation of ownership and control. The Journal of Law and Economics 26: 301–25. [Google Scholar] [CrossRef]

- Fauver, Larry, and Michael E. Fuerst. 2006. Does good corporate governance include employee representation? Evidence from German corporate boards. Journal of Financial Economics 82: 673–710. [Google Scholar] [CrossRef]

- Fich, Eliezer M., and Steve L. Slezak. 2008. Can corporate governance save distressed firms from bankruptcy? An empirical analysis. Review of Quantitative Finance and Accounting 30: 225–51. [Google Scholar] [CrossRef]

- Gorton, Gary, and Frank A. Schmid. 2004. Capital, labor, and the firm: A study of German codetermination. Journal of the European Economic Association 2: 863–905. [Google Scholar] [CrossRef]

- Green, Colin P., and Swarnodeep Homroy. 2018. Female directors, board committees and firm performance. European Economic Review 102: 19–38. [Google Scholar] [CrossRef] [Green Version]

- Grice, John Stephen, and Robert W. Ingram. 2001. Tests of the generalizability of Altman’s bankruptcy prediction model. Journal of Business Research 54: 53–61. [Google Scholar] [CrossRef]

- Gul, Ferdinand A., and Sidney Leung. 2004. Board leadership, outside directors’ expertise and voluntary corporate disclosures. Journal of Accounting and Public Policy 23: 351–79. [Google Scholar] [CrossRef]

- Hermalin, Benjamin E., and Michael S. Weisbach. 1998. Endogenously chosen boards of directors and their monitoring of the CEO. American Economic Review 88: 96–118. [Google Scholar]

- Hermalin, Benjamin E., and Michael S. Weisbach. 2003. Boards of directors as an endogenously determined institution: A survey of the economic literature. Economic Policy Review 9: 7–26. [Google Scholar]

- Hillegeist, Stephen A., Elizabeth K. Keating, Donald P. Cram, and Kyle G. Lundstedt. 2004. Assessing the probability of bankruptcy. Review of Accounting Studies 9: 5–34. [Google Scholar] [CrossRef]

- Huang, Hui, Xiaojun Shi, and Shunming Zhang. 2011. Counter-cyclical substitution between trade credit and bank credit. Journal of Banking & Finance 35: 1859–78. [Google Scholar]

- Huang, Sterling, and Gilles Hilary. 2018. Zombie board: Board tenure and firm performance. Journal of Accounting Research 56: 1285–329. [Google Scholar] [CrossRef]

- Jensen, Michael C. 1993. The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance 48: 831–80. [Google Scholar] [CrossRef]

- Jo, Hoje, Annie Hsu, Rosamaria Llanos-Popolizio, and Jorge Vergara-Vega. 2021. Corporate governance and financial fraud of wirecard. European Journal of Business and Management Research 6: 96–106. [Google Scholar] [CrossRef]

- Kahane, Leo, Neil Longley, and Robert Simmons. 2013. The effects of coworker heterogeneity on firm-level output: Assessing the impacts of cultural and language diversity in the national hockey league. Review of Economics and Statistics 95: 302–14. [Google Scholar] [CrossRef] [Green Version]

- Karampatsas, Nikolaos, Dimitris Petmezas, and Nickolaos G. Travlos. 2014. Credit ratings and the choice of payment method in mergers and acquisitions. Journal of Corporate Finance 25: 474–93. [Google Scholar] [CrossRef]

- Kim, Daehyun, and Laura T. Starks. 2016. Gender diversity on corporate boards: Do women contribute unique skills? American Economic Review 106: 267–71. [Google Scholar] [CrossRef]

- Kirsch, Anja. 2018. The gender composition of corporate boards: A review and research agenda. The Leadership Quarterly 29: 346–64. [Google Scholar] [CrossRef]

- Krause, Ryan, Matthew Semadeni, and Albert A. Cannella. 2014. CEO duality. Journal of Management 40: 256–86. [Google Scholar] [CrossRef]

- Lee, Sang Cheol, Mooweon Rhee, and Jongchul Yoon. 2018. The effects of foreign monitoring on audit quality: Evidence from Korea. Sustainability 10: 3151. [Google Scholar] [CrossRef] [Green Version]

- Levinson, Klas. 2001. Employee representatives on company boards in Sweden. Industrial Relations Journal 32: 264–74. [Google Scholar] [CrossRef]

- Li, Hong-Xia, Zong-Jun Wang, and Xiao-Lan Deng. 2008. Ownership, independent directors, agency costs and financial distress: Evidence from Chinese listed companies. Corporate Governance 8: 622–36. [Google Scholar] [CrossRef]

- Lin, Chen, Thomas Schmid, and Yuhai Xuan. 2018. Employee representation and financial leverage. Journal of Financial Economics 127: 303–24. [Google Scholar] [CrossRef] [Green Version]

- Linck, James S., Jeffry M. Netter, and Tina Yang. 2008. The determinants of board structure. Journal of Financial Economics 87: 308–28. [Google Scholar] [CrossRef]

- Livnat, Joshua, Gavin Smith, Kate Suslava, and Martin Tarlie. 2019. Do directors have a use-by date? Examining the impact of board tenure on firm performance. American Journal of Management 19: 97–125. [Google Scholar] [CrossRef] [Green Version]

- Mannheim, Karl. 1949. Man and Society in an Age of Construction. New York: Harcour, Brace. [Google Scholar]

- McCrum, Dan. 2019. Wirecard’s suspect accounting practices revealed. Financial Times, October 14. [Google Scholar]

- McCrum, Dan. 2020. Wirecard: The timeline. Financial Times, June 25. [Google Scholar]

- McCrum, Dan, and Olaf Storbeck. 2022. Wirecard: The Case Against Markus Braun. Financial Times, March 22. [Google Scholar]

- McIntyre, Michael L., Steven A. Murphy, and Paul Mitchell. 2007. The top team: Examining board composition and firm performance. Corporate Governance: The International Journal of Business in Society 7: 547–61. [Google Scholar] [CrossRef]

- Molina, Carlos A. 2005. Are firms underleveraged? An examination of the effect of leverage on default probabilities. Journal of Finance 60: 1427–59. [Google Scholar] [CrossRef]

- Ohlson, James A. 1980. Financial ratios and the probabilistic prediction of bankruptcy. Journal of Accounting Research 19: 109–31. [Google Scholar] [CrossRef] [Green Version]

- Oliveira, Mauro, and Shage Zhang. 2022. The trends and determinants of board gender and age diversities. Finance Research Letters 46: 102798. [Google Scholar] [CrossRef]

- Pfeffer, Jeffrey, and Gerald R. Salancik. 1978. The External Control of Organizations: A Resource Dependence Perspective. Manhattan: Harper & Row. [Google Scholar]

- Raheja, Charu G. 2005. Determinants of board size and composition: A theory of corporate boards. Journal of Financial and Quantitative Analysis 40: 283–306. [Google Scholar] [CrossRef]

- Reisz, Alexander S., and Claudia Perlich. 2007. A market-based framework for bankruptcy prediction. Journal of Financial Stability 3: 85–131. [Google Scholar] [CrossRef]

- Rhodes, Susan R. 1983. Age-related differences in work attitudes and behavior: A review and conceptual analysis. Psychological Bulletin 93: 328. [Google Scholar] [CrossRef]

- Sun, Mengqi. 2019. More U.S. Companies Separating Chief Executive and Chairman Roles. Wall Street Journal, January 23. [Google Scholar]

- Talavera, Oleksandr, Yin Shuxing, and Zhang Mao. 2018. Age diversity, directors’ personal values, and bank performance. International Review of Financial Analysis 55: 60–79. [Google Scholar] [CrossRef]

- Tirole, Jean. 2010. The Theory of Corporate Finance. Princeton: Princeton University Press. [Google Scholar]

- Traczynski, Jeffrey. 2017. Firm default prediction: A bayesian model-averaging approach. The Journal of Financial and Quantitative Analysis 52: 1211–45. [Google Scholar] [CrossRef]

- Tsui, Anne S., Terri D. Egan, and Katherine R. Xin. 1995. Diversity in organizations: Lessons from demography research. In An Earlier Version of This Chapter Was Presented as a Paper at the American Psychological Society Meeting, Chicago, IL, June 1993. Southend Oaks: Sage Publications, Inc. [Google Scholar]

- Turetsky, Howard F., and Ruth A. McEwen. 2001. An empirical investigation of firm longevity: A model of the ex ante predictors of financial distress. Review of Quantitative Finance and Accounting 16: 323–43. [Google Scholar] [CrossRef]

- Vafeas, Nikos. 1999. Board meeting frequency and firm performance. Journal of Financial Economics 53: 113–142. [Google Scholar] [CrossRef]

- Vafeas, Nikos. 2003. Length of board tenure and outside director independence. Journal of Business Finance & Accounting 30: 1043–64. [Google Scholar]

- Weisbach, Michael S. 1988. Outside directors and CEO turnover. Journal of Financial Economics 20: 431–60. [Google Scholar] [CrossRef]

- Whitaker, Richard B. 1999. The early stages of financial distress. Journal of Economics and Finance 23: 123–132. [Google Scholar] [CrossRef]

- Williams, Katherine Y., and Charles A. O’Reilly III. 1998. Demography and diversity in organizations: A review of 40 years of research. Research in Organizational Behavior 20: 77–140. [Google Scholar]

- Wruck, Karen Hopper. 1990. Financial distress, reorganization, and organizational efficiency. Journal of Financial Economics 27: 419–444. [Google Scholar] [CrossRef]

- Zahra, Sahker A., and John A. Pearce. 1989. Boards of directors and corporate financial performance: A review and integrative model. Journal of Management 15: 291–334. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Definition |

|---|---|

| Board Characteristics | |

| % Independent Directors | Number of independent directors/Board size |

| CEO Duality | 1 if Chairman is CEO, 0 otherwise |

| % Employee Representatives | Number of Employee representatives on board/Board size |

| Tenure | Years in current role: Role end year–Role start year |

| % Female Directors | Number of female directors/Board size |

| % Foreign Directors | Number of foreign directors/Board size |

| Age | Average age of directors |

| Other Covariates | |

| ln(Board Size) | Natural logarithm of number of directors on board |

| Firm Size | Natural logarithm of total assets in year t − 1 |

| Quick Ratio | Current assets/Current liabilities in year t − 1 |

| Leverage | Total liabilities/Total assets in year t − 1 |

| Sales Growth | (Salest/Salest−1) − 1 |

| Capex | Capital Expenditures/Total assets in year t − 1 |

| Financial Crisis Dummy | 1 if year = 2011, 2012, 2013, 2020, 0 otherwise |

| Country | N | Z-Score | % Independent Directors | CEO Duality | % Employee Representation | Tenure | % Female Directors | %Foreign Directors | Age | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | S.D. | Mean | S.D. | Mean | S.D. | Mean | S.D. | Mean | S.D. | Mean | S.D. | Mean | S.D. | Mean | S.D. | ||

| Austria | 257 | 2.66 | 1.41 | 31.90 | 20.14 | 0 | 0 | 14.13 | 15.51 | 4.55 | 2.2 | 14.58 | 12.64 | 12.09 | 16.3 | 56.61 | 4.02 |

| Belgium | 675 | 2.93 | 4.94 | 22.57 | 19.25 | 0.04 | 0.19 | 0 | 0 | 4.18 | 2.18 | 21.36 | 15.34 | 17.02 | 20.45 | 57.31 | 4.32 |

| Croatia | 30 | 3 | 1.71 | 3.38 | 6.68 | 0 | 0 | 9.39 | 4.93 | 2.88 | 1.33 | 21.58 | 17.72 | 3.52 | 6.39 | 53.91 | 4.53 |

| Cyprus | 93 | 1.59 | 3.02 | 25.20 | 23.32 | 0 | 0 | 0 | 0 | 3.22 | 1.89 | 16.77 | 14.02 | 34.52 | 20.04 | 52.91 | 6.13 |

| Czech Republic | 35 | 3.38 | 1.33 | 0.52 | 2.17 | 0 | 0 | 9.75 | 12.72 | 1.48 | 0.81 | 15.27 | 14.47 | 6.46 | 12.46 | 49.01 | 4.85 |

| Denmark | 469 | 9.23 | 20.11 | 35.04 | 19.13 | 0 | 0 | 19.24 | 18.21 | 3.79 | 2.43 | 17.76 | 13.04 | 19.79 | 21.77 | 56.35 | 3.70 |

| Estonia | 18 | 1.97 | 0.61 | 0 | 0 | 0.44 | 0.51 | 0 | 0 | 6.03 | 1.29 | 9.52 | 8.37 | 4.11 | 4.75 | 50.47 | 3.20 |

| Faroe Islands | 16 | 3.47 | 4.97 | 30.10 | 21.86 | 0 | 0 | 0 | 0 | 3.80 | 2.34 | 18.33 | 13.5 | 23.65 | 27.04 | 53.53 | 5.02 |

| Finland | 912 | 3.31 | 4.25 | 53.67 | 19.7 | 0 | 0.07 | 0.35 | 2.62 | 3.04 | 2.1 | 24.65 | 14.61 | 13.8 | 19.87 | 55.52 | 4.63 |

| France | 3631 | 2.54 | 4.57 | 29.36 | 22.36 | 0.55 | 0.5 | 2.07 | 5.37 | 4.88 | 3.46 | 27.25 | 17.04 | 8.95 | 15.36 | 56.49 | 6.13 |

| Germany | 3013 | 3.5 | 6.2 | 12.93 | 20.11 | 0 | 0 | 12.5 | 18.34 | 4.20 | 2.79 | 14.37 | 16.49 | 10.36 | 16.92 | 56.37 | 6.25 |

| Great Britain | 2279 | 3.32 | 15.07 | 41.19 | 39.14 | 0 | 0.07 | 0 | 0 | 3.20 | 2.88 | 20.03 | 32.12 | 37.04 | 40.19 | 57.02 | 7.09 |

| Greece | 234 | 2.01 | 1.71 | 26.16 | 14.99 | 0.2 | 0.4 | 2.06 | 5.72 | 5.19 | 3.43 | 6.87 | 7.94 | 7.14 | 10.44 | 59.31 | 7.48 |

| Hungary | 67 | 2.20 | 1.01 | 45.60 | 23.02 | 0.18 | 0.39 | 0.15 | 1.22 | 4.96 | 2.54 | 6.43 | 10.29 | 8.37 | 10.80 | 56.86 | 7.00 |

| Ireland | 250 | 2.51 | 4.36 | 31.21 | 19.93 | 0.02 | 0.14 | 0 | 0 | 4 | 2.99 | 10.23 | 11.08 | 29.57 | 29.41 | 56.92 | 4.24 |

| Island | 34 | 69.7 | 48.03 | 43.68 | 18.11 | 0 | 0 | 0 | 0 | 3.37 | 2.46 | 41.30 | 13.76 | 15.08 | 14.01 | 54.59 | 3.08 |

| Italy | 1332 | 2.57 | 3.92 | 38.43 | 18.83 | 0.16 | 0.37 | 0 | 0 | 3.93 | 2.74 | 25.08 | 15.19 | 6.75 | 15.91 | 56.38 | 4.76 |

| Luxembourg | 217 | 3.78 | 4.63 | 29.78 | 23.57 | 0.23 | 0.42 | 0 | 0 | 5.13 | 4.43 | 11.72 | 14.77 | 60.42 | 28.64 | 57.35 | 5.25 |

| The Netherlands | 735 | 2.71 | 4.87 | 35.51 | 20.44 | 0.4 | 0.49 | 0.01 | 0.37 | 3.47 | 1.94 | 15.88 | 14.18 | 33.09 | 28.74 | 57.24 | 5.09 |

| Norway | 980 | 7.44 | 19.76 | 36.03 | 26.54 | 0 | 0.05 | 9.74 | 14.97 | 3.20 | 2.51 | 40.12 | 11.82 | 14.18 | 18.51 | 54.18 | 4.95 |

| Poland | 389 | 4.02 | 9.47 | 28.59 | 21.06 | 0 | 0 | 1.46 | 5.69 | 2.81 | 2.16 | 13.75 | 14.40 | 4.54 | 10.03 | 51.15 | 7.65 |

| Portugal | 334 | 1.28 | 1.53 | 16.38 | 17.99 | 0.25 | 0.43 | 0 | 0 | 4.96 | 4.14 | 13.26 | 14.35 | 8.95 | 14.83 | 56.19 | 5.22 |

| Romania | 26 | 3.83 | 2.88 | 31.15 | 16.26 | 0 | 0 | 0 | 0 | 1.60 | 1.14 | 19.33 | 12.12 | 28.85 | 16.8 | 52.18 | 4.34 |

| Serbia | 10 | 2.08 | 0.20 | 25.33 | 6.66 | 0 | 0 | 0 | 0 | 3.88 | 1.7 | 4.29 | 6.90 | 37.57 | 10.56 | 49.00 | 2.69 |

| Slovak Republic | 8 | 3.18 | 0.36 | 0 | 0 | 1 | 0 | 0 | 0 | 3.83 | 0.67 | 10.83 | 8.12 | 20.32 | 4.53 | 56.03 | 2.37 |

| Slovenia | 20 | 4.18 | 1.19 | 0 | 0 | 0 | 0 | 11.88 | 15.25 | 3.29 | 1.95 | 35.28 | 26.34 | 22.29 | 32.92 | 49.42 | 4.58 |

| Spain | 852 | 1.76 | 3.86 | 24.04 | 18.66 | 0.24 | 0.43 | 0 | 0 | 4.34 | 2.76 | 15.72 | 12.25 | 7.89 | 13.96 | 59.53 | 6.48 |

| Sweden | 1717 | 7.91 | 17.44 | 51.44 | 20.41 | 0 | 0 | 8.82 | 12.08 | 3.72 | 2.31 | 28.25 | 14.16 | 10.39 | 16.23 | 56.22 | 3.89 |

| Switzerland | 1244 | 3.99 | 7.75 | 25.25 | 28.82 | 0.05 | 0.21 | 0 | 0 | 4.65 | 2.97 | 10.86 | 11.77 | 27.8 | 27.67 | 58.59 | 3.96 |

| Full Sample | 19877 | 3.88 | 10.77 | 31.52 | 26.95 | 0.15 | 0.36 | 4.27 | 11.05 | 4.04 | 2.92 | 21.11 | 19.25 | 16.33 | 24.91 | 56.54 | 5.81 |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

|---|---|---|---|---|---|---|---|---|

| % Independent Directors | 0.0179 *** | 0.0117 ** | ||||||

| (0.005) | (0.005) | |||||||

| CEO duality | 0.0956 | 0.193 | ||||||

| (0.198) | (0.194) | |||||||

| % Employee Representation | −0.0276 | −0.0198 | ||||||

| (0.018) | (0.018) | |||||||

| Tenure | 0.0104 | 0.0216 | ||||||

| (0.036) | (0.043) | |||||||

| % Female Directors | 0.0217 *** | 0.0209 *** | ||||||

| (0.006) | (0.007) | |||||||

| % Foreign Directors | 0.0210 ** | 0.0205 ** | ||||||

| (0.009) | (0.009) | |||||||

| Age | 0.0315 | 0.027 | ||||||

| (0.0277) | (0.030) | |||||||

| Adj.-R2 | 0.169 | 0.169 | 0.168 | 0.168 | 0.169 | 0.170 | 0.169 | 0.173 |

| Panel A. Board Governance and Risk of Insolvency for Non-Distressed Firms | ||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| % Independent Directors | 0.0196 ** | 0.0122 | ||||||

| (0.007) | (0.008) | |||||||

| CEO duality | 0.1030 | 0.275 | ||||||

| (0.274) | (0.268) | |||||||

| % Employee Representation | −0.0163 | −0.0060 | ||||||

| (0.022) | (0.023) | |||||||

| Tenure | −0.1100 ** | −0.0872 | ||||||

| (0.045) | (0.054) | |||||||

| % Female Directors | 0.0243 *** | 0.0226 *** | ||||||

| (0.008) | (0.008) | |||||||

| % Foreign Directors | 0.0323 *** | 0.0308 ** | ||||||

| (0.012) | (0.012) | |||||||

| Age | 0.0070 | 0.0197 | ||||||

| (0.038) | (0.042) | |||||||

| Adj.-R2 | 0.233 | 0.232 | 0.232 | 0.232 | 0.233 | 0.235 | 0.232 | 0.237 |

| Panel B. Board Governance and Risk of Insolvency for Distressed Firms | ||||||||

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |

| % Independent Directors | 0.0022 | 0.0025 | ||||||

| (0.0027) | (0.0028) | |||||||

| CEO duality | −0.0826 | −0.1330 | ||||||

| (0.1070) | (0.105) | |||||||

| % Employee Representation | −0.0133 * | −0.0133 * | ||||||

| (0.0070) | (0.0072) | |||||||

| Tenure | 0.0644 *** | 0.0609 *** | ||||||

| (0.0224) | (0.0198) | |||||||

| % Female Directors | −0.0005 | −0.0002 | ||||||

| (0.0038) | (0.0037) | |||||||

| % Foreign Directors | −0.00726 | −0.0075 * | ||||||

| (0.0045) | (0.00458) | |||||||

| Age | 0.0105 * | 0.0008 | ||||||

| (0.0145) | (0.0139) | |||||||

| Adj.-R2 | 0.515 | 0.515 | 0.516 | 0.515 | 0.515 | 0.516 | 0.516 | 0.520 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Full Sample | Non-Distressed | Distressed | ||||

| Firm-FE | Firm-RE | Firm-FE | Firm-RE | Firm-FE | Firm-RE | |

| % Independent Directors | 0.0059 | 0.0136 *** | 0.0078 | 0.0162 *** | 0.0035 | 0.0015 |

| (0.005) | (0.004) | (0.006) | (0.005) | (0.002) | (0.002) | |

| CEO duality | 0.0001 | −0.725 ** | 0.3820 | −0.955 * | −0.1150 | 0.1380 |

| (0.409) | (0.335) | (0.685) | (0.525) | (0.168) | (0.136) | |

| % Employee Representation | −0.0258 ** | −0.0027 | −0.0176 | 0.0059 | −0.0144 | 0.0090 |

| (0.018) | (0.013) | (0.024) | (0.017) | (0.010) | (0.006) | |

| Tenure | −0.0330 | −0.0425 | 0.0041 | −0.0669 | 0.0136 | 0.0477 *** |

| (0.041) | (0.036) | (0.056) | (0.049) | (0.021) | (0.018) | |

| % Female Directors | 0.0112 * | 0.0144 *** | 0.0175 ** | 0.0171 ** | −0.0056 * | −0.0015 |

| (0.006) | (0.005) | (0.008) | (0.007) | (0.003) | (0.002) | |

| % Foreign Directors | −0.0011 | 0.0035 | 0.0068 | 0.0175 ** | 0.0043 | −0.0038 * |

| (0.006) | (0.004) | (0.009) | (0.007) | (0.003) | (0.002) | |

| Age | 0.0437 ** | 0.0342 * | 0.1040 *** | 0.0645 ** | −0.0154 | −0.0143 * |

| (0.022) | (0.019) | (0.034) | (0.028) | (0.010) | (0.008) | |

| R2 | 0.030 | 0.055 | 0.023 | 0.115 | 0.483 | 0.273 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Maier, F.; Yurtoglu, B.B. Board Characteristics and the Insolvency Risk of Non-Financial Firms. J. Risk Financial Manag. 2022, 15, 303. https://doi.org/10.3390/jrfm15070303

Maier F, Yurtoglu BB. Board Characteristics and the Insolvency Risk of Non-Financial Firms. Journal of Risk and Financial Management. 2022; 15(7):303. https://doi.org/10.3390/jrfm15070303

Chicago/Turabian StyleMaier, Florian, and B. Burcin Yurtoglu. 2022. "Board Characteristics and the Insolvency Risk of Non-Financial Firms" Journal of Risk and Financial Management 15, no. 7: 303. https://doi.org/10.3390/jrfm15070303

APA StyleMaier, F., & Yurtoglu, B. B. (2022). Board Characteristics and the Insolvency Risk of Non-Financial Firms. Journal of Risk and Financial Management, 15(7), 303. https://doi.org/10.3390/jrfm15070303