Time-Varying Bidirectional Causal Relationships between Transaction Fees and Economic Activity of Subsystems Utilizing the Ethereum Blockchain Network

Abstract

:1. Introduction

2. Conceptual Background

2.1. Transaction Cost Theory

- Information costs: Imperfect information, price volatility, and complexity contribute to information transaction costs in the Ethereum network. Users may lack accurate information about gas prices, leading to overpaying or underpaying, thereby contributing to resource allocation inefficiencies. Gas price volatility and the intricacies of understanding and calculating gas fees further complicate decision-making for users, especially for those without technical expertise in blockchain technology (Abel et al. 2013; Holmstrom and Milgrom 1991; Arrow 1974).

- Bargaining costs: The Ethereum network handles a vast number of transactions daily, making individual bargaining for each transaction time-consuming and impractical. Ethereum is designed to maintain pseudonymity, and direct negotiation of fees could jeopardize this anonymity. Additionally, the dynamic nature of gas prices and fluctuating demand for transaction fee negotiation are challenging and unrealistic (Milgrom and Roberts 1990; Hart and Moore 1990; Grossman and Hart 1986).

- Enforcement costs: In Ethereum’s trustless, decentralized environment, enforcing agreed-upon fees and transaction inclusion can be challenging without a centralized authority. Resolving disputes related to transaction fees or performance is difficult and costly. Aligning incentives for users and miners or validators is crucial and can be achieved through well-designed economic mechanisms and consensus algorithms (Dyer and Singh 1998; Zaheer and Venkatraman 1995).

2.2. Ethereum Transaction Fees

3. Methods and Data

3.1. Ethereum Transaction Fees

3.2. Data

3.2.1. Transaction Fees on the Ethereum Blockchain

3.2.2. Underlying Economic Systems on the Ethereum Blockchain

3.3. Empirical Approach

3.3.1. Granger Causality

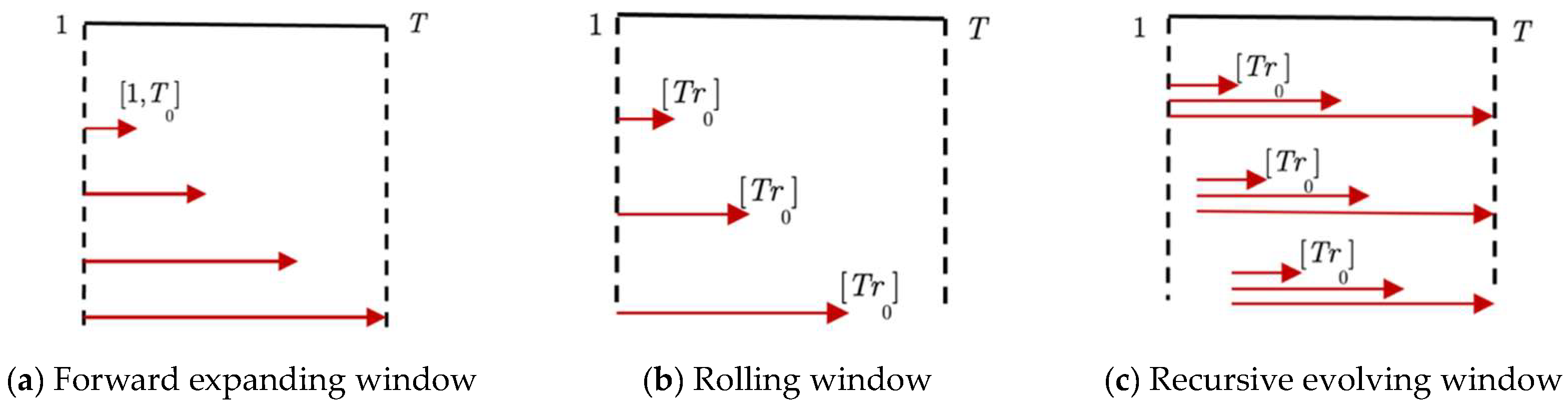

3.3.2. Time-Varying Granger Causality

4. Results

4.1. Baseline Estimation

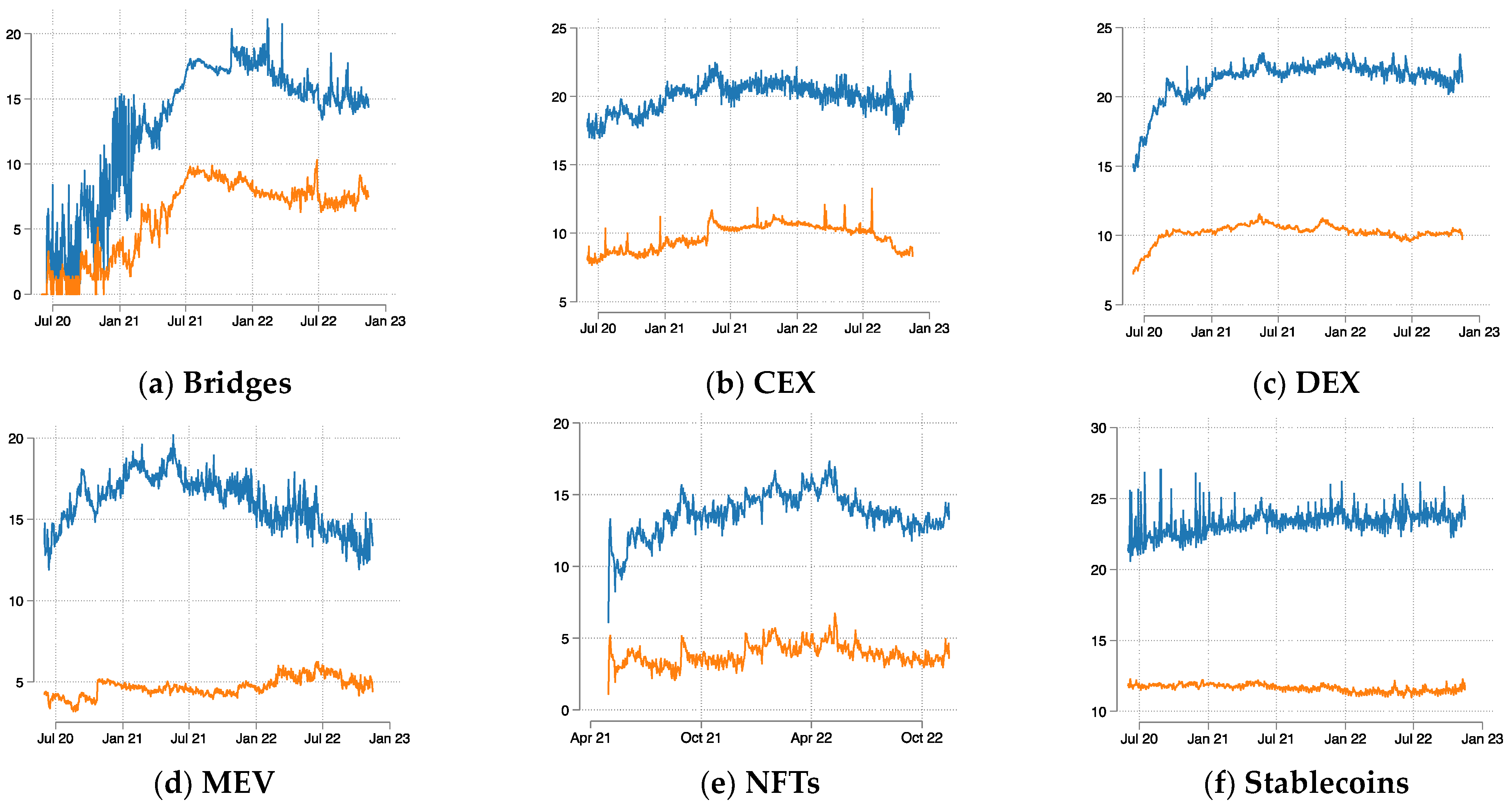

4.2. Bridges

4.3. Centralized Exchanges (CEX)

4.4. Decentralized Exchanges (DEX)

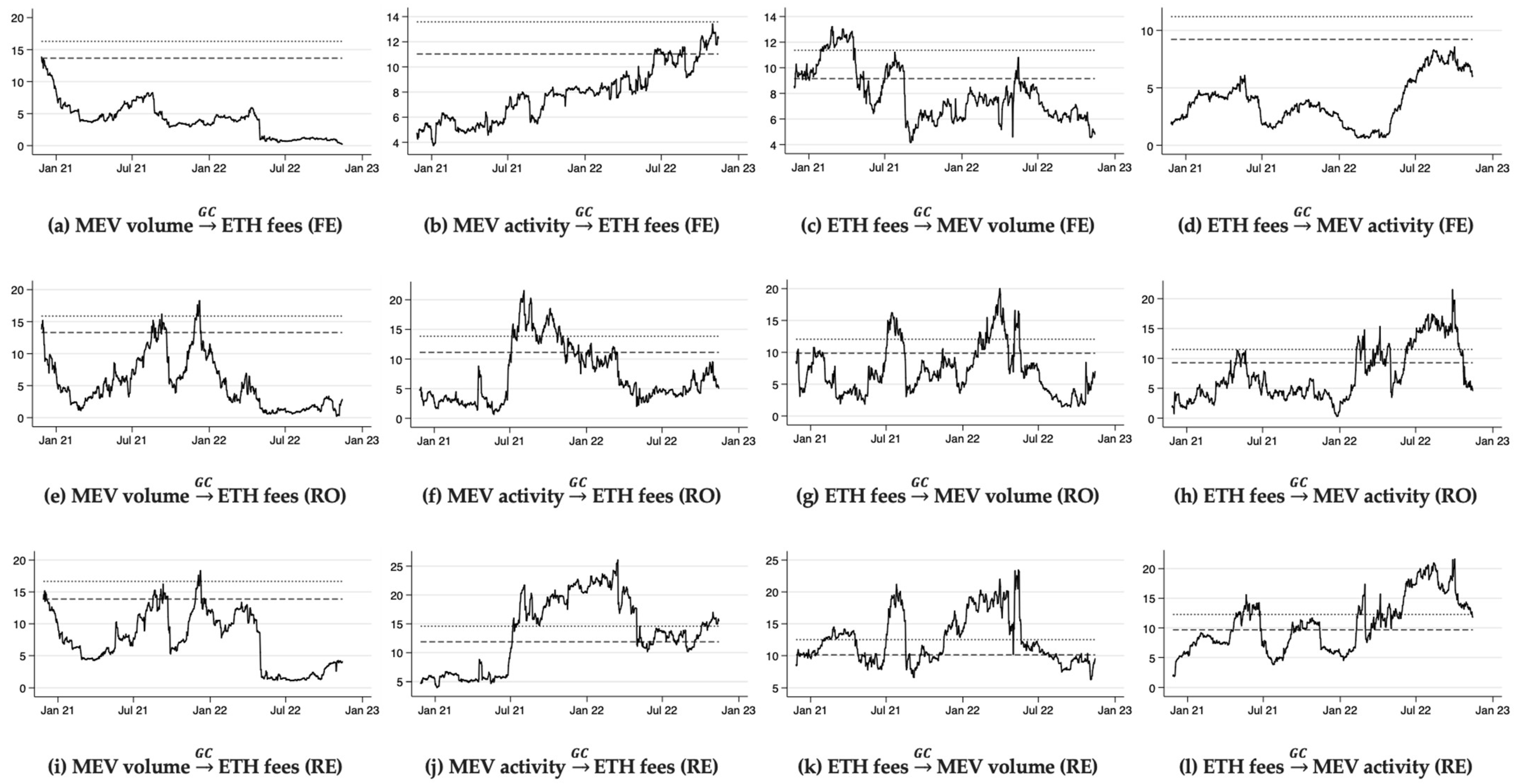

4.5. Maximal Extractable Value (MEV)

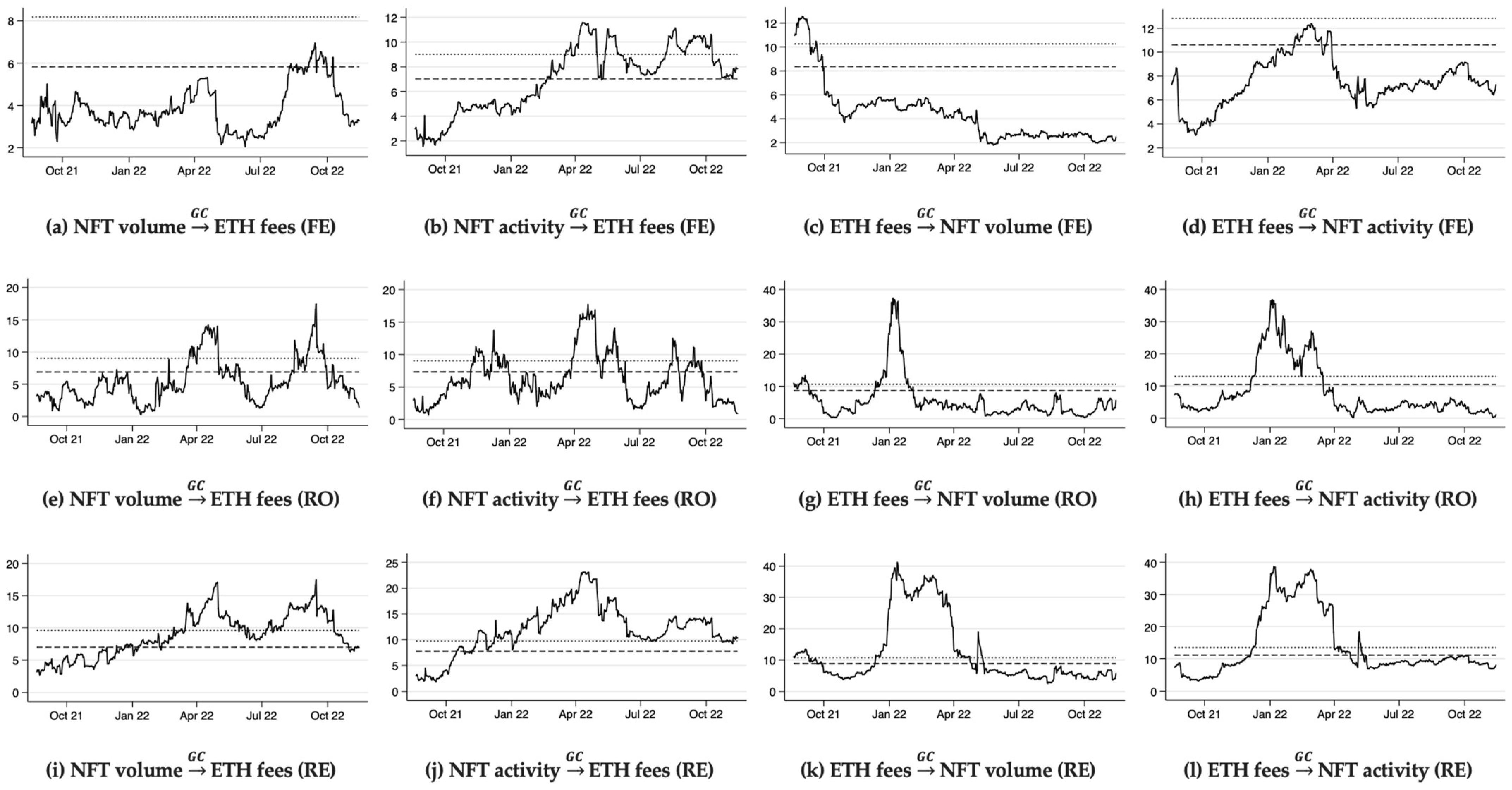

4.6. Non-Fungible Tokens (NFTs)

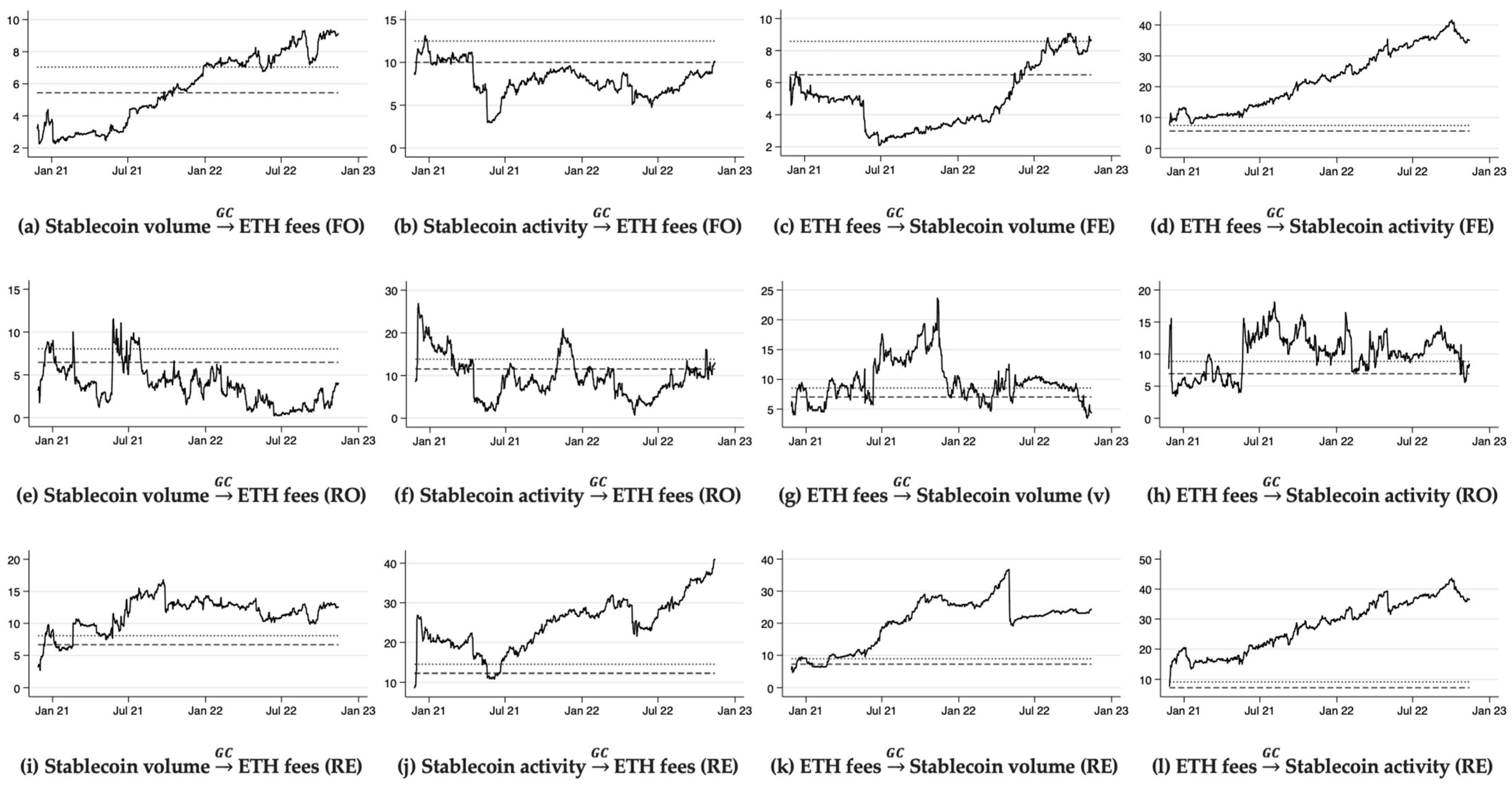

4.7. Stablecoins

5. Discussion, Future Research, and Conclusions

- (a) Bridges: For bridges, the results reveal a bidirectional causality between the number of unique active wallets associated with bridge protocols and the mean transaction fees within the Ethereum network. The observed feedback loop potentially indicates a migration of users towards alternative blockchain infrastructures. Despite the considerable decrease in transaction fees over the analyzed duration, it underscores Ethereum’s diminished competitiveness in comparison to other blockchain networks and layer-2 solutions. These insights highlight the role of transaction fees in influencing user migration trends and the ensuing need for judicious oversight.

- (b) CEXs: For Ethereum network stakeholders, the findings highlight the crucial role of CEX deposits and withdrawals in the fee network’s operation. The strengthening, bidirectional Granger-causal relationship between Ethereum fees and CEX transaction volume is underpinned by a feedback loop. This suggests that increasing CEX transaction volume catalyzes demand for block space and transaction processing competition, resulting in higher gas fees. This, in turn, influences trading and transferring costs on CEXs, prompting users to pursue higher-value transactions, thereby reinforcing the causal nexus. Market participants may also monitor this interplay, capitalizing on arbitrage opportunities or market volatility, and perpetuating a self-reinforcing cycle of network congestion and escalating fees. Our findings contribute to the literature on centralized exchanges and decentralized blockchain networks (Ante et al. 2021a; Ante 2020; Aspris et al. 2021).

- (c) DEXs: The causal relationship between DEX volume, DEX users, and network fees illuminates the interplay among these three elements in the Ethereum network. The findings suggest that an increase in DEX volume causally influences higher fees, which subsequently have a significant causal influence on the DEX user counts. Over time, this relationship weakens, likely due to the diminished economic significance of the DeFi system (i.e., bubbles) (Maouchi et al. 2022; Wang et al. 2022). However, decreasing fees positively impacts the DEX user counts by rendering smaller trades economically viable again. Future scholarly inquiry is required to validate these postulations. For Ethereum network stakeholders, these findings underscore the need for DEXes to balance the trade-off between attracting more users and ensuring manageable fees, thus explaining why, e.g., Uniswap and SushiSwap also launched on other blockchain networks (Shen 2021) and continue to explore this option (Malwa 2023). Furthermore, DEXs need to consider the impact of fees on their user base when making fee-related decisions (i.e., network fees, not DEX-specific transaction fees). Additionally, the decline in fees’ significance over time suggests that the impact of fees on users may differ depending on the economic context.

- (d) MEVs: A discernible causal linkage between Ethereum network fees and MEV volume/activity emerges during certain periods, signifying the intermittent importance of MEV within the Ethereum ecosystem. This phenomenon may be ascribed to elements such as the advent of alternative value-extraction approaches, alterations in searcher tactics, or adjustments in the Ethereum environment. Furthermore, market actors may have recalibrated their actions in response to the shifting interplay between MEV prospects and transaction fees, culminating in novel equilibrium points within the competitive arena. Subsequent investigations may consider delving into the potential ramifications of additional MEV market participants by employing a more exhaustive dataset, as the current findings, predicated on the activities of five eminent MEV bots, may not encompass the entirety of the MEV market landscape.8

- (e) NFTs: The analysis highlights a sophisticated causal interplay among NFT volume, NFT activity, and Ethereum network fees, where speculative bubbles may have significantly impacted relationships (Maouchi et al. 2022; Wang et al. 2022). Results show that fees causally influenced NFT activity and transaction volumes. This causal relationship can be interpreted as heightened fees acting as an entry barrier for users, discouraging (encouraging) NFT participation and resulting in reduced (increased) transaction volumes. Nonetheless, the evidence for the causal influence of NFT user activity or transaction volume on fees is not definitive, indicating a complex causal interplay. The lack of a consistent causal connection may be due to several confounding factors, such as network capacity, miner preferences, and overall transaction demand, with non-NFT-related transactions potentially exacerbating network congestion and raising fees independently of NFT activity or volume.

- (f) Stablecoins: Findings indicate that Ethereum transaction fees causally influenced stablecoin user activity and transaction volumes. Furthermore, evidence suggests a shift in causal directionality commencing from Q2 2022, wherein stablecoin user activity and transaction volume causally impacted transaction fees. This feedback mechanism infers a bidirectional causality, attributable to the burgeoning prominence and adoption of stablecoins within the cryptocurrency domain. The escalating influence of stablecoins on the Ethereum network precipitated heightened transaction demand, consequently leading to an increase in Ethereum transaction fees. These findings underscore the complex interdependencies between stablecoin dynamics and the Ethereum network as they collaboratively mold the dynamic cryptocurrency market landscape.

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

| 1 | On 15 September 2022, the Ethereum blockchain underwent a substantial upgrade at block 15537393, commonly referred to as the Merge. This pivotal transition replaced the traditional proof-of-work (PoW) consensus mechanism with the more energy-efficient proof-of-stake (PoS) mechanism, where validators stake Ether in lieu of relying on hardware-based miners. Before the upgrade, the average block time experienced significant fluctuations due to network congestion. Post-merge, however, the block time has become more predictable and consistent, averaging approximately 12 s. This enhancement in block time can be ascribed to the accelerated and more efficient block processing facilitated by the PoS mechanism, as well as alterations to the transaction fee structure that have effectively mitigated congestion and augmented overall network efficiency. |

| 2 | Ethereum transaction fees are remitted in Ether; however, the associated ‘gas’ fees are denominated in Gwei, where one Gwei is equivalent to 0.000000001 Ether. |

| 3 | (Reijsbergen et al. 2021; Leonardos et al. 2021) determined that Ethereum Improvement Proposal (EIP) 1559 generally achieved its objectives, but suggested an alternative base fee adjustment rule employing variable learning rate mechanisms. Concurrently, Laurent et al. (Laurent et al. 2022; Azevedo Sousa et al. 2021) devised a novel Monte Carlo method to ascertain the minimum fee a user ought to pay for their transaction to be processed with a given probability within a specified timeframe. In contrast, Azevedo Sousa et al. (2021) found no evident correlation between Ethereum fee-related characteristics, such as user-defined gas and gas price, and the pending time of transactions. Lastly, Werner et al. (2020) introduced a gas price recommendation mechanism that amalgamates a deep-learning-based price forecasting model with an algorithm parameterized by a user-specific urgency value. This mechanism led to average cost savings exceeding 50% compared to existing recommendation mechanisms while incurring only a slight delay. |

| 4 | This study opts to utilize the USD value of the transaction fee as opposed to the Gwei value, as the former exhibits greater stability and is less susceptible to fluctuations. For instance, should the value of Ether experience rapid appreciation or depreciation, the corresponding Gwei value in USD would undergo swift alterations, which ultimately impacts users’ focus and considerations. In addition, it can be assumed that economic players will want to use a stable currency such as the USD for their planning. |

| 5 | For comparison purposes, it is noteworthy to mention that PayPal’s transaction fee structure involves a charge of 5% of the paid amount plus USD 0.05 (Khan and State 2020). Thus, only transactions exceeding USD 262 on PayPal would surpass the average transaction fee of USD 13.18 on the Ethereum network. |

| 6 | We validated this result using the KPSS and Augmented Dickey–Fuller test (Kwiatkowski et al. 1992). |

| 7 | See note 6 above. |

| 8 | In interpreting the results, it is vital to recognize the presence of survivorship bias within the underlying data. This bias arises from the consideration of only successful and valuable NFT collections (e.g., the five selected in this study), while numerous less successful or failed projects are excluded. These overlooked projects may constitute a larger market share and exhibit a distinct relationship with network fees. Consequently, the findings should not be generalized to the entire NFT market but rather pertain specifically to the upper echelon. This limitation extends to the analysis of MEV bots as well. |

References

- Abel, Andre B., Janice C. Eberly, and Stabros Panageas. 2013. Optimal Inattention to the Stock Market with Information Costs and Transactions Costs. Econometrica 81: 1455–81. [Google Scholar] [CrossRef]

- Ante, Lennart. 2020. Bitcoin Transactions, Information Asymmetry and Trading Volume. Quantitative Finance and Economics 4: 365–81. [Google Scholar] [CrossRef]

- Ante, Lennart. 2022. Non-Fungible Token (NFT) Markets on the Ethereum Blockchain: Temporal Development, Cointegration and Interrelations. Economics of Innovation and New Technology 32: 1216–34. [Google Scholar] [CrossRef]

- Ante, Lennart, Ingo Fiedler, and Elias Strehle. 2021a. The Impact of Transparent Money Flows: Effects of Stablecoin Transfers on the Returns and Trading Volume of Bitcoin. Technological Forecasting and Social Change 170: 120851. [Google Scholar] [CrossRef]

- Ante, Lennart, Ingo Fiedler, and Elias Strehle. 2021b. The Influence of Stablecoin Issuances on Cryptocurrency Markets. Finance Research Letters 41: 101867. [Google Scholar] [CrossRef]

- Antonio Pierro, Giuseppe, Henrique Rocha, Roberto Tonelli, and Stephane Ducasse. 2020. Are the Gas Prices Oracle Reliable? A Case Study Using the EthGasStation. Paper presented at the 2020 IEEE International Workshop on Blockchain Oriented Software Engineering (IWBOSE), London, ON, Canada, February 18; pp. 1–8. [Google Scholar] [CrossRef]

- Arora, Vipin, and Shuping Shi. 2016. Energy Consumption and Economic Growth in the United States. Applied Economics 48: 3763–73. [Google Scholar] [CrossRef]

- Arrow, Kenneth J. 1974. The Limits of Organizations. New York: WW Norton & Company. [Google Scholar]

- Aspris, Angelo, Sean Foley, Jiri Svec, and Leqi Wang. 2021. Decentralized Exchanges: The ‘Wild West’ of Cryptocurrency Trading. International Review of Financial Analysis 77: 101845. [Google Scholar] [CrossRef]

- Axie. 2021. The Great Migration-Ronin Phase 2 Is Live! Available online: https://axie.substack.com/p/migration (accessed on 23 July 2023).

- Azevedo Sousa, José Eduardo, Vinícius Oliveira, Júlia Valadares, Glauber Dias Gonçalves, Saulo Moraes Villela, Heder Soares Bernardino, and Alex Borges Vieira. 2021. An Analysis of the Fees and Pending Time Correlation in Ethereum. International Journal of Network Management 31: e2113. [Google Scholar] [CrossRef]

- Bartoletti, Massimo, James Hsin-yu Chiang, and Alberto Lluch Lafuente. 2022. Maximizing Extractable Value from Automated Market Makers. In International Conference on Financial Cryptography and Data Security. Cham: Springer International Publishing, pp. 3–19. [Google Scholar] [CrossRef]

- Baum, Christopher F., Stan Hurn, and Jesús Otero. 2021. The Dynamics of U.S. Industrial Production: A Time-Varying Granger Causality Perspective. Econometrics and Statistics. [Google Scholar] [CrossRef]

- Baum, Christopher F., Stan Hurn, and Jesús Otero. 2022. Testing for Time-Varying Granger Causality. The Stata Journal: Promoting Communications on Statistics and Stata 22: 355–78. [Google Scholar] [CrossRef]

- BBC. 2017. CryptoKitties Craze Slows down Transactions on Ethereum. Available online: https://www.bbc.com/news/technology-42237162 (accessed on 23 July 2023).

- Belchior, Rafael, André Vasconcelos, Sérgio Guerreiro, and Miguel Correia. 2022. A Survey on Blockchain Interoperability: Past, Present, and Future Trends. ACM Computing Surveys 54: 1–41. [Google Scholar] [CrossRef]

- Bianchi, Daniele, Mykola Babiak, and Alexander Dickerson. 2022. Trading Volume and Liquidity Provision in Cryptocurrency Markets. Journal of Banking & Finance 142: 106547. [Google Scholar] [CrossRef]

- Bouraga, Sarah. 2020. An Evaluation of Gas Consumption Prediction on Ethereum Based on Transaction History Summarization. Paper presented at the 2020 2nd Conference on Blockchain Research & Applications for Innovative Networks and Services (BRAINS), Paris, France, September 28–30; pp. 49–50. [Google Scholar] [CrossRef]

- Brandvold, Morten, Peter Molnár, Kristian Vagstad, Ole Christian, and Andreas Valstad. 2015. Price Discovery on Bitcoin Exchanges. Journal of International Financial Markets, Institutions & Money 36: 18–35. [Google Scholar] [CrossRef]

- Briola, Antonio, David Vidal-Tomás, Yuanrong Wang, and Tomaso Aste. 2022. Anatomy of a Stablecoin’s Failure: The Terra-Luna Case. arXiv arXiv:2207.13914. [Google Scholar] [CrossRef]

- Buterin, Vitalik. 2014. Ethereum White Paper-A Next Generation Smart Contract & Decentralized Application Platform. Available online: http://blockchainlab.com/pdf/Ethereum_white_paper-a_next_generation_smart_contract_and_decentralized_application_platform-vitalik-buterin.pdf (accessed on 23 July 2023).

- Buterin, Vitalik, Eric Conner, Rick Dudley, Matthew Slipper, Ian Norden, and Abdelhamid Bakhta. 2019. EIP-1559: Fee Market Change for ETH 1.0 Chain. Ethereum Foundation. April 13. Available online: https://eips.ethereum.org/EIPS/eip-1559 (accessed on 23 July 2023).

- Campbell, John Y., and Pierre Perron. 1991. Pitfalls and Opportunities: What Macroeconomists Should Know about Unit Roots. NBER Macroeconomics Annual 6: 141–201. [Google Scholar] [CrossRef]

- Churiwala, Dev, and Bhaskar Krishnamachari. 2022. CoMMA Protocol: Towards Complete Mitigation of Maximal Extractable Value (MEV) Attacks. arXiv arXiv:2211.14985. [Google Scholar]

- Coase, Ronald Harry. 1937. The Nature of the Firm. Econometrica 4: 386–405. [Google Scholar] [CrossRef]

- Daian, Philip, Steven Goldfeder, Tyler Kell, Yunqi Li, Xueyuan Zhao, Iddo Bentov, Lorenz Breidenbach, and Ari Juels. 2020. Flash Boys 2.0: Frontrunning in Decentralized Exchanges, Miner Extractable Value, and Consensus Instability. Paper presented at the 2020 IEEE Symposium on Security and Privacy (SP), San Francisco, CA, USA, May 18–21; pp. 910–27. [Google Scholar] [CrossRef]

- Dolado, Juan J., and Helmut Lütkepohl. 1996. Making Wald Tests Work for Cointegrated VAR Systems. Econometric Reviews 15: 369–86. [Google Scholar] [CrossRef]

- Donmez, Anil, and Alexander Karaivanov. 2022. Transaction Fee Economics in the Ethereum Blockchain. Economic Inquiry 60: 265–92. [Google Scholar] [CrossRef]

- Dune Analytics. 2023. Dune Analytics. Available online: https://dune.com (accessed on 23 July 2023).

- Dyer, Jeffrey H., and Harbir Singh. 1998. The Relational View: Cooperative Strategy and Sources of Interorganizational Competitive Advantage. Academy of Management Review 23: 660–79. [Google Scholar] [CrossRef]

- Engle, Robert F., and Clive W. J. Granger. 1987. Co-Integration and Error Correction: Representation, Estimation, and Testing. Econometrica 55: 251–76. [Google Scholar] [CrossRef]

- Ethereum Foundation. 2023. Maximal Extractable Value (MEV). Ethereum.Org. Available online: https://ethereum.org/en/developers/docs/mev/ (accessed on 23 July 2023).

- Etherscan. 2021. Ethereum Gas Tracker. Available online: https://etherscan.io/gastracker#historicaldata (accessed on 23 July 2023).

- Etherscan. 2022. Ethereum Daily Transactions Chart. November 15. Available online: https://etherscan.io/chart/tx (accessed on 23 July 2023).

- Etherscan. 2023a. Accounts: Bridge. Etherscan. Available online: https://etherscan.io/accounts/label/bridge (accessed on 23 July 2023).

- Etherscan. 2023b. Etherscan. Available online: https://etherscan.io (accessed on 23 July 2023).

- Faqir-Rhazoui, Youssef, Miller-Janny Ariza-Garzón, Javier Arroyo, and Samer Hassan. 2021. Effect of the Gas Price Surges on User Activity in the DAOs of the Ethereum Blockchain. In Extended Abstracts of the 2021 CHI Conference on Human Factors in Computing Systems. New York: ACM, pp. 1–7. [Google Scholar] [CrossRef]

- Feng, Yunxia, Yuan Sun, and Jing Qu. 2023. An Attention-GRU Based Gas Price Prediction Model for Ethereum Transactions. In Paper presented at the Signal and Information Processing, Networking and Computers: Proceedings of the 8th International Conference on Signal and Information Processing, Networking and Computers (ICSINC), Ji’nan, China, September 13–17; pp. 1058–66. [Google Scholar] [CrossRef]

- Fiedler, Ingo, and Lennart Ante. 2023. Stablecoins. In The Emerald Handbook on Cryptoassets: Investment Opportunities and Challenges. Edited by Kent H. Baker, Hugo Benedetti, Ehrsan Nikbakht and Sean Stein Smith. Bingley: Emerald Publishing Limited, vol. 1. [Google Scholar]

- Flipside Crypto. 2023. Flipside Crypto. Available online: https://flipsidecrypto.xyz (accessed on 23 July 2023).

- Freeman, R. Edward. 1984. Strategic Management: A Stakeholder Approach. Boston: Pitman. [Google Scholar]

- Glassnode. 2020. Glassnode.Com. Available online: https://glassnode.com (accessed on 23 July 2023).

- Granger, Clive W. J. 1981. Some Properties of Time Series Data and Their Use in Econometric Model Specification. Journal of Econometrics 16: 121–30. [Google Scholar] [CrossRef]

- Griffin, John M., and Amin Shams. 2020. Is Bitcoin Really Un-Tethered? The Journal of Finance 75: 1913–64. [Google Scholar] [CrossRef]

- Grobys, Klaus, Juha Junttila, James W. Kolari, and Niranjan Sapkota. 2021. On the Stability of Stablecoins. Journal of Empirical Finance 64: 207–23. [Google Scholar] [CrossRef]

- Grossman, Sanford J., and Oliver D. Hart. 1986. The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration. Journal of Political Economy 94: 691–719. [Google Scholar] [CrossRef]

- Hall, Alastair. 1994. Testing for a Unit Root in Time Series with Pretest Data-Based Model Selection. Journal of Business & Economic Statistics 12: 461. [Google Scholar] [CrossRef]

- Hardjono, Thomas. 2021. Blockchain Gateways, Bridges and Delegated Hash-Locks. arXiv arXiv:2102.03933. [Google Scholar]

- Hart, Oliver, and John Moore. 1990. Property Rights and the Nature of the Firm. Journal of Political Economy 98: 1119–58. [Google Scholar] [CrossRef]

- Hennart, Jean-François. 1982. A Theory of Multinational Enterprise. Ann Arbor: University of Michigan. [Google Scholar]

- Hoang, Lai T., and Dirk G. Baur. 2021. How Stable Are Stablecoins? The European Journal of Finance, 1–17. [Google Scholar] [CrossRef]

- Holmstrom, Bengt, and Paul Milgrom. 1991. Multitask Principal-Agent Analyses: Incentive Contracts, Asset Ownership, and Job Design. Journal of Law, Economics and Organization 7: 24–52. [Google Scholar] [CrossRef]

- Khan, Muhammad Milhan Afzal, Hafiz Muhammad Azeem Sarwar, and Muhammad Awais. 2022. Gas Consumption Analysis of Ethereum Blockchain Transactions. Concurrency and Computation: Practice and Experience 34: e6679. [Google Scholar] [CrossRef]

- Khan, Nida, and Radu State. 2020. Lightning Network: A Comparative Review of Transaction Fees and Data Analysis. In International Congress on Blockchain and Applications. Cham: Springer International Publishing, pp. 11–18. [Google Scholar] [CrossRef]

- Kulkarni, Kshitij, Theo Diamandis, and Tarun Chitra. 2022. Towards a Theory of Maximal Extractable Value I: Constant Function Market Makers. arXiv arXiv:2207.11835. [Google Scholar]

- Kwiatkowski, Denis, Peter C. B. Phillips, Peter Schmidt, and Yongcheol Shin. 1992. Testing the Null Hypothesis of Stationarity against the Alternative of a Unit Root. Journal of Econometrics 54: 159–78. [Google Scholar] [CrossRef]

- Lan, Rongjian, Ganesha Upadhyaya, Stephen Tse, and Mahdi Zamani. 2021. Horizon: A Gas-Efficient, Trustless Bridge for Cross-Chain Transactions. arXiv arXiv:2101.06000. [Google Scholar]

- Laurent, Arnaud, Luce Brotcorne, and Bernard Fortz. 2022. Transaction Fees Optimization in the Ethereum Blockchain. Blockchain: Research and Applications 3: 100074. [Google Scholar] [CrossRef]

- Lee, Sung-Shine, Alexandr Murashkin, Martin Derka, and Jan Gorzny. 2022. SoK: Not Quite Water Under the Bridge: Review of Cross-Chain Bridge Hacks. Paper presented at the 2023 IEEE International Conference on Blockchain and Cryptocurrency (ICBC), Dubai, United Arab Emirates, May 1–5. [Google Scholar]

- Leonardos, Stefanos, Barnabé Monnot, Daniël Reijsbergen, Efstratios Skoulakis, and Georgios Piliouras. 2021. Dynamical Analysis of the EIP-1559 Ethereum Fee Market. In Proceedings of the 3rd ACM Conference on Advances in Financial Technologies. New York: ACM, pp. 114–26. [Google Scholar] [CrossRef]

- le Pennec, Guénolé, Ingo Fiedler, and Lennart Ante. 2021. Wash Trading at Cryptocurrency Exchanges. Finance Research Letters 43: 101982. [Google Scholar] [CrossRef]

- Leybourne, Stephen J. 1995. Testing for Unit Roots Using Forward and Reverse Dickey-Fuller Regressions. Oxford Bulletin of Economics and Statistics 57: 559–71. [Google Scholar] [CrossRef]

- Li, Chao, and Haijun Yang. 2022. Will Memecoins’ Surge Trigger a Crypto Crash? Evidence from the Connectedness between Leading Cryptocurrencies and Memecoins. Finance Research Letters 50: 103191. [Google Scholar] [CrossRef]

- Li, Chunmiao. 2021. Gas Estimation and Optimization for Smart Contracts on Ethereum. Paper presented at the 2021 36th IEEE/ACM International Conference on Automated Software Engineering (ASE), Melbourne, Australia, November 15–19; pp. 1082–86. [Google Scholar] [CrossRef]

- Li, Chunmiao, Shijie Nie, Yang Cao, Yijun Yu, and Zhenjiang Hu. 2020. Trace-Based Dynamic Gas Estimation of Loops in Smart Contracts. IEEE Open Journal of the Computer Society 1: 295–306. [Google Scholar] [CrossRef]

- Liu, Fangxiao, Xingya Wang, Zixin Li, Jiehui Xu, and Yubin Gao. 2020. Effective GasPrice Prediction for Carrying Out Economical Ethereum Transaction. Paper presented at the 2019 6th International Conference on Dependable Systems and Their Applications (DSA), Harbin, China, January 3–6; pp. 329–34. [Google Scholar] [CrossRef]

- Liu, Yiying, Guangxing Shan, Yucheng Liu, Abdullah Alghamdi, Iqbal Alam, and Sujit Biswas. 2022. Blockchain Bridges Critical National Infrastructures: E-Healthcare Data Migration Perspective. IEEE Access 10: 28509–19. [Google Scholar] [CrossRef]

- Liu, Yulin, Yuxuan Lu, Kartik Nayak, Fan Zhang, Luyao Zhang, and Yinhong Zhao. 2022. Empirical Analysis of EIP-1559: Transaction Fees, Waiting Time, and Consensus Security. Paper presented at the 2022 ACM SIGSAC Conference on Computer and Communications Security, Los Angeles, CA, USA, November 7–11. [Google Scholar]

- Makarov, Igor, and Antoinette Schoar. 2020. Trading and Arbitrage in Cryptocurrency Markets. Journal of Financial Economics 135: 293–319. [Google Scholar] [CrossRef]

- Malkhi, Dahlia, and Pawel Szalachowski. 2022. Maximal Extractable Value (MEV) Protection on a DAG. arXiv arXiv:2208.00940. [Google Scholar]

- Malwa, Shaurya. 2023. Uniswap Poll Shows 80% Support Decentralized Crypto Exchange’s Move to BNB Chain. CoinDesk. Available online: https://www.coindesk.com/tech/2023/01/23/uniswap-poll-shows-80-support-decentralized-crypto-exchanges-move-to-bnb-chain/ (accessed on 23 July 2023).

- Maouchi, Youcef, Lanouar Charfeddine, and Ghassen el Montasser. 2022. Understanding Digital Bubbles amidst the COVID-19 Pandemic: Evidence from DeFi and NFTs. Finance Research Letters 47: 102584. [Google Scholar] [CrossRef]

- Mars, Rawya, Amal Abid, Saoussen Cheikhrouhou, and Slim Kallel. 2021. A Machine Learning Approach for Gas Price Prediction in Ethereum Blockchain. Paper presented at the 2021 IEEE 45th Annual Computers, Software, and Applications Conference (COMPSAC), Madrid, Spain, July 12–16; pp. 156–65. [Google Scholar] [CrossRef]

- Masten, Scott E., Jr., James W. Meehan, and Edward A. Snyder. 1991. The Costs of Organization. Journal of Law, Economics & Organization 7: 1–25. [Google Scholar]

- Milgrom, Paul, and John Roberts. 1990. Bargaining Costs, Influence Costs, and the Organization of Economic Activity. In Perspectives on Positive Political Economy. Edited by James E. Alt and Kenneth A. Shepsie. Cambridge: Cambridge University Press, pp. 57–89. [Google Scholar]

- Moin, Amani, Kevin Sekniqi, and Emin Gun Sirer. 2020. SoK: A Classification Framework for Stablecoin Designs. Paper presented at the Financial Cryptography and Data Security: 24th International Conference, Kota Kinabalu, Malaysia, February 10–14; pp. 174–97. [Google Scholar] [CrossRef]

- Obadia, Alexandre, Alejo Salles, Lakshman Sankar, Tarun Chitra, Vaibhav Chellani, and Philip Daian. 2021. Unity Is Strength: A Formalization of Cross-Domain Maximal Extractable Value. arXiv arXiv:2112.01472. [Google Scholar]

- Otero, Jesús, and Christopher F. Baum. 2018. Unit-Root Tests Based on Forward and Reverse Dickey–Fuller Regressions. The Stata Journal: Promoting Communications on Statistics and Stata 18: 22–28. [Google Scholar] [CrossRef]

- Petukhina, Alla, Raphael C. G. Reule, and Wolfgang Karl Härdle. 2021. Rise of the Machines? Intraday High-Frequency Trading Patterns of Cryptocurrencies. The European Journal of Finance 27: 8–30. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., Shuping Shi, and Jun Yu. 2014. Specification Sensitivity in Right-Tailed Unit Root Testing for Explosive Behaviour. Oxford Bulletin of Economics and Statistics 76: 315–33. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., Shuping Shi, and Jun Yu. 2015a. Testing for Multiple Bubbles: Historical Episodes of Exuberance and Collapse in the S&P 500. International Economic Review 56: 1043–78. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., Shuping Shi, and Jun Yu. 2015b. Testing for Multiple Bubbles: Limit Theory of Real-time Detectors. International Economic Review 56: 1079–1134. [Google Scholar] [CrossRef]

- Phillips, Peter C. B., Yangru Wu, and Jun Yu. 2011. Explosive Behavior in the 1990s Nasdaq: When Did Exuberance Escalate Asset Values? International Economic Review 52: 201–26. [Google Scholar] [CrossRef]

- Pierro, Giuseppe Antonio, and Henrique Rocha. 2019. The Influence Factors on Ethereum Transaction Fees. Paper presented at the 2019 IEEE/ACM 2nd International Workshop on Emerging Trends in Software Engineering for Blockchain (WETSEB), Montreal, QC, Canada, May 27; pp. 24–31. [Google Scholar] [CrossRef]

- Pierro, Giuseppe Antonio, Henrique Rocha, Stéphane Ducasse, Michele Marchesi, and Roberto Tonelli. 2022. A User-Oriented Model for Oracles’ Gas Price Prediction. Future Generation Computer Systems 128: 142–57. [Google Scholar] [CrossRef]

- Qasse, Ilham A., Manar Abu Talib, and Qassim Nasir. 2019. Inter Blockchain Communication. In Proceedings of the ArabWIC 6th Annual International Conference Research Track. New York: ACM, pp. 1–6. [Google Scholar] [CrossRef]

- Qin, Kaihua, and Arthur Gervais. 2021. Quantifying Blockchain Extractable Value: How Dark Is the Forest? arXiv arXiv:2101.05511. [Google Scholar]

- Reijsbergen, Daniel, Shyam Sridhar, Barnabe Monnot, Stefanos Leonardos, Stratis Skoulakis, and Georgios Piliouras. 2021. Transaction Fees on a Honeymoon: Ethereum’s EIP-1559 One Month Later. Paper presented at the 2021 IEEE International Conference on Blockchain (Blockchain), Melbourne, Australia, December 6–8; pp. 196–204. [Google Scholar] [CrossRef]

- Ren, Xiaohang, Jingyao Li, Feng He, and Brian Lucey. 2023. Impact of Climate Policy Uncertainty on Traditional Energy and Green Markets: Evidence from Time-Varying Granger Tests. Renewable and Sustainable Energy Reviews 173: 113058. [Google Scholar] [CrossRef]

- Saggu, Aman. 2022. The Intraday Bitcoin Response to Tether Minting and Burning Events: Asymmetry, Investor Sentiment, and ‘Whale Alerts’ on Twitter. Finance Research Letters 49: 103096. [Google Scholar] [CrossRef]

- Shen, Muyao. 2021. Uniswap Launches on Polygon, Driving MATIC to All-Time Highs. CoinDesk. Available online: https://www.coindesk.com/markets/2021/12/22/uniswap-launches-on-polygon-driving-matic-to-all-time-highs/ (accessed on 23 July 2023).

- Shi, Shuping, Peter C. B. Phillips, and Stan Hurn. 2018. Change Detection and the Causal Impact of the Yield Curve. Journal of Time Series Analysis 39: 966–87. [Google Scholar] [CrossRef]

- Shi, Shuping, Stan Hurn, and Peter C. B. Phillips. 2020. Causal Change Detection in Possibly Integrated Systems: Revisiting the Money–Income Relationship. Journal of Financial Econometrics 18: 158–80. [Google Scholar] [CrossRef]

- Spain, Michael, Sean Foley, and Vincent Gramoli. 2020. The Impact of Ethereum Throughput and Fees on Transaction Latency during Icos. In International Conference on Blockchain Economics, Security and Protocols (Tokenomics 2019). Schloss Dagstuhl: Leibniz-Zentrum für Informatik. [Google Scholar] [CrossRef]

- Stone, Drew. 2021. Trustless, Privacy-Preserving Blockchain Bridges. arXiv arXiv:2102.04660. [Google Scholar]

- Swanson, Norman R. 1998. Money and Output Viewed through a Rolling Window. Journal of Monetary Economics 41: 455–74. [Google Scholar] [CrossRef]

- Szabo, Nick. 1994. “Smart Contracts.” Nick Szabo’s Essays, Papers, and Concise Tutorials. Available online: https://www.fon.hum.uva.nl/rob/Courses/InformationInSpeech/CDROM/Literature/LOTwinterschool2006/szabo.best.vwh.net/smart.contracts.html (accessed on 23 July 2023).

- Teutsch, Jason, Michael Straka, and Dan Boneh. 2019. Retrofitting a Two-Way Peg between Blockchains. arXiv arXiv:1908.03999. [Google Scholar]

- Thoma, Mark A. 1994. Subsample Instability and Asymmetries in Money-Income Causality. Journal of Econometrics 64: 279–306. [Google Scholar] [CrossRef]

- Toda, Hiro Y., and Taku Yamamoto. 1995. Statistical Inference in Vector Autoregressions with Possibly Integrated Processes. Journal of Econometrics 66: 225–50. [Google Scholar] [CrossRef]

- Wang, Gang-Jin, Xin-yu Ma, and Hao-yu Wu. 2020. Are Stablecoins Truly Diversifiers, Hedges, or Safe Havens against Traditional Cryptocurrencies as Their Name Suggests? Research in International Business and Finance 54: 101225. [Google Scholar] [CrossRef]

- Wang, Yizhi, Florian Horky, Lennart J. Baals, Brian M. Lucey, and Samuel A. Vigne. 2022. Bubbles All the Way down? Detecting and Date-Stamping Bubble Behaviours in NFT and DeFi Markets. Journal of Chinese Economic and Business Studies 20: 415–36. [Google Scholar] [CrossRef]

- Weintraub, Ben, Christof Ferreira Torres, Cristina Nita-Rotaru, and Radu State. 2022. A Flash(Bot) in the Pan: Measuring Maximal Extractable Value in Private Pools. Paper presented at the 22nd ACM Internet Measurement Conference, Nice, France, October 25–27. [Google Scholar]

- Werner, Sam M., Paul J. Pritz, and Daniel Perez. 2020. Step on the Gas? A Better Approach for Recommending the Ethereum Gas Price. Paper presented at the Mathematical Research for Blockchain Economy: 2nd International Conference MARBLE 2020, Vilamoura, Portugal, August 20; pp. 161–77. [Google Scholar] [CrossRef]

- Williamson, Oliver E. 1979. Transaction-Cost Economics: The Governance of Contractual Relations. The Journal of Law & Economics 22: 233–61. [Google Scholar]

- Xia, Pengcheng, Haoyu Wang, Bingyu Gao, Weihang Su, Zhou Yu, Xiapu Luo, Chao Zhang, Xusheng Xiao, and Guoai Xu. 2021. Trade or Trick? Detecting and Characterizing Scam Tokens on Uniswap Decentralized Exchange. In Proceedings of the ACM on Measurement and Analysis of Computing Systems. New York: Association for Computing Machinery, vol. 5. [Google Scholar] [CrossRef]

- Xie, Tiancheng, Jiaheng Zhang, Zerui Cheng, Fan Zhang, Yupeng Zhang, Yongzheng Jia, Dan Boneh, and Dawn Song. 2022. ZkBridge: Trustless Cross-Chain Bridges Made Practical. Paper presented at the 2022 ACM SIGSAC Conference on Computer and Communications Security, Los Angeles, CA, USA, November 7–11. [Google Scholar]

- Zaheer, Akbar, and Natarjan Venkatraman. 1995. Relational Governance as an Interorganizational Strategy: An Empirical Test of the Role of Trust in Economic Exchange. Strategic Management Journal 16: 373–92. [Google Scholar] [CrossRef]

- Zarir, Abdullah A., Gustavo A. Oliva, Zhen M. (Jack) Jiang, and Ahmed E. Hassan. 2021. Developing Cost-Effective Blockchain-Powered Applications. ACM Transactions on Software Engineering and Methodology 30: 1–38. [Google Scholar] [CrossRef]

- Zhang, Lin, Brian Lee, Yuhang Ye, and Yuansong Qiao. 2021. Evaluation of Ethereum End-to-End Transaction Latency. Paper presented at the 2021 11th IFIP International Conference on New Technologies, Mobility and Security (NTMS), Paris, France, April 19–21; pp. 1–5. [Google Scholar] [CrossRef]

- Zhang, Shenhui, Ming Tang, Xiulai Li, Boyi Liu, Bo Zhang, Fei Hu, Sirui Ni, and Jieren Cheng. 2022. ROS-Ethereum: A Convenient Tool to Bridge ROS and Blockchain (Ethereum). Security and Communication Networks 2022: 1–14. [Google Scholar] [CrossRef]

- Zhou, Liyi, Kaihua Qin, Antoine Cully, Benjamin Livshits, and Arthur Gervais. 2021. On the Just-In-Time Discovery of Profit-Generating Transactions in DeFi Protocols. Paper presented at the 2021 IEEE Symposium on Security and Privacy (SP), San Francisco, CA, USA, May 24–27; pp. 919–36. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| System | Description | Name | Address | Creation Date/First Transaction | Number of Transactions |

|---|---|---|---|---|---|

| Bridges | Blockchain protocols or platforms that allow for interoperability between different blockchain networks (Lan et al. 2021; Teutsch et al. 2019; Zhang et al. 2022; Lee et al. 2022; Xie et al. 2022; Yiying Liu et al. 2022; Qasse et al. 2019; Belchior et al. 2022; Stone 2021; Hardjono 2021). | Axie Infinity: Ronin Bridge | 0x1a2a1c938ce3ec39b6d47113c7955baa9dd454f2 | 25 January 2021 | 3,090,670 |

| zkSync | 0xabea9132b05a70803a4e85094fd0e1800777fbef | 15 June 2020 | 825,134 | ||

| Hop Protocol | 0xb8901acb165ed027e32754e0ffe830802919727f | 1 October 2021 | 497,580 | ||

| Immutable X: Bridge | 0x5fdcca53617f4d2b9134b29090c87d01058e27e9 | 10 March 2021 | 384,515 | ||

| Optimism: Gateway | 0x99c9fc46f92e8a1c0dec1b1747d010903e884be1 | 22 June 2021 | 300,528 | ||

| CEX | Deposits and withdrawals from wallets of centralized crypto asset exchanges (Ante et al. 2021a; le Pennec et al. 2021; Brandvold et al. 2015; Makarov and Schoar 2020; Ante 2020; Bianchi et al. 2022; Petukhina et al. 2021). | Binance Hot Wallet A | 0x3f5ce5fbfe3e9af3971dd833d26ba9b5c936f0be | 4 August 2017 | 17,017,383 |

| Binance Hot Wallet B | 0x28c6c06298d514db089934071355e5743bf21d60 | 22 April 2021 | 11,507,057 | ||

| Bittrex Wallet | 0xfbb1b73c4f0bda4f67dca266ce6ef42f520fbb98 | 10 August 2015 | 11,492,410 | ||

| Coinbase Wallet A | 0x3cd751e6b0078be393132286c442345e5dc49699 | 27 April 2021 | 9,852,269 | ||

| Coinbase Wallet B | 0xb5d85cbf7cb3ee0d56b3bb207d5fc4b82f43f511 | 27 April 2021 | 9,351,971 | ||

| DEX | Decentralized exchanges (DEX), which allow for peer-to-peer trading of crypto assets (Lan et al. 2021; Teutsch et al. 2019; Zhang et al. 2022; Lee et al. 2022; Xie et al. 2022; Yiying Liu et al. 2022; Qasse et al. 2019; Belchior et al. 2022; Stone 2021; Hardjono 2021). | SushiSwap Router | 0xd9e1ce17f2641f24ae83637ab66a2cca9c378b9f | 4 September 2020 | 4,131,024 |

| Uniswap v2 Router | 0x7a250d5630b4cf539739df2c5dacb4c659f2488d | 5 June 2020 | 58,660,014 | ||

| Uniswap v3 Router | 0xe592427a0aece92de3edee1f18e0157c05861564 | 4 May 2021 | 5,673,190 | ||

| MEV | Bots that exploit market inefficiencies to extract profit, known as miner extractable value or maximal extractable value (MEV) (Daian et al. 2020; Qin and Gervais 2021; Zhou et al. 2021; Churiwala and Krishnamachari 2022; Obadia et al. 2021; Kulkarni et al. 2022; Malkhi and Szalachowski 2022; Weintraub et al. 2022; Bartoletti et al. 2022). | MEV Bot 1 | 0xa57bd00134b2850b2a1c55860c9e9ea100fdd6cf | 26 March 2019 | 3,641,491 |

| MEV Bot 2 | 0x0000000000007f150bd6f54c40a34d7c3d5e9f56 | 23 October 2020 | 2,327,098 | ||

| MEV Bot 3 | 0x860bd2dba9cd475a61e6d1b45e16c365f6d78f66 | 11 February 2020 | 2,175,487 | ||

| MEV Bot 4 | 0x000000000000006f6502b7f2bbac8c30a3f67e9a | 1 May 2020 | 1,438,193 | ||

| MEV Bot 5 | 0x4cb18386e5d1f34dc6eea834bf3534a970a3f8e7 | 26 February 2021 | 732,871 | ||

| NFTs | Non-fungible tokens, which are unique digital assets that can represent ownership of things like artwork or collectibles (Daian et al. 2020; Qin and Gervais 2021; Zhou et al. 2021; Churiwala and Krishnamachari 2022; Obadia et al. 2021; Kulkarni et al. 2022; Malkhi and Szalachowski 2022; Weintraub et al. 2022; Bartoletti et al. 2022). | Azuki | 0xed5af388653567af2f388e6224dc7c4b3241c544 | 20 January 2022 | 87,238 |

| Bored Ape Yacht Club | 0xbc4ca0eda7647a8ab7c2061c2e118a18a936f13d | 22 April 2021 | 141,249 | ||

| CloneX | 0x49cf6f5d44e70224e2e23fdcdd2c053f30ada28b | 12 December 2021 | 100,589 | ||

| Mutant Ape Yacht Club | 0x60e4d786628fea6478f785a6d7e704777c86a7c6 | 28 August 2021 | 121,620 | ||

| CryptoPunks | 0xb47e3cd837ddf8e4c57f05d70ab865de6e193bbb | 22 June 2017 | 50,630 | ||

| Stablecoins | Crypto assets that are pegged to the value of a specific asset, such as the US dollar, in order to reduce volatility in their value (Fiedler and Ante 2023; Hoang and Baur 2021; Briola et al. 2022; Ante et al. 2021a, 2021b; Grobys et al. 2021; Moin et al. 2020; Saggu 2022; Griffin and Shams 2020; Wang et al. 2020). | BUSD | 0x4fabb145d64652a948d72533023f6e7a623c7c53 | 5 September 2019 | 1,740,628 |

| DAI | 0x6b175474e89094c44da98b954eedeac495271d0f | 13 November 2019 | 16,642,305 | ||

| FRAX | 0x853d955acef822db058eb8505911ed77f175b99e | 16 December 2020 | 575,751 | ||

| USDC | 0xa0b86991c6218b36c1d19d4a2e9eb0ce3606eb48 | 3 August 2018 | 59,242,016 | ||

| USDT | 0xdac17f958d2ee523a2206206994597c13d831ec7 | 28 November 2017 | 174,406,655 |

| Log-Transformed | First-Differenced | |||||

|---|---|---|---|---|---|---|

| Lags | ADFmax | p-Value | Lags | ADFmax | p-Value | |

| AIC | 6 | −1.018 | 0.536 | 7 | −12.233 *** | 0.000 |

| SIC | 5 | −1.196 | 0.444 | 4 | −19.770 *** | 0.000 |

| GTS05 | 6 | −1.018 | 0.537 | 7 | −12.233 *** | 0.000 |

| Transaction Volume (USD) | Active Users | ||||||

|---|---|---|---|---|---|---|---|

| System | Lags | ADFmax | p-Value | Lags | ADFmax | p-Value | |

| (a) Bridges | AIC | 7 | −15.85 *** | 0.000 | 5 | −16.25 *** | 0.000 |

| SIC | 5 | −20.52 *** | 0.000 | 2 | −22.99 *** | 0.000 | |

| GTS05 | 7 | −15.85 *** | 0.000 | 5 | −16.25 *** | 0.000 | |

| (b) CEX | AIC | 6 | 17.56 *** | 0.000 | 5 | −17.75 *** | 0.000 |

| SIC | 5 | 23.80 *** | 0.000 | 5 | −17.75 *** | 0.000 | |

| GTS05 | 5 | 23.80 *** | 0.000 | 5 | −17.75 *** | 0.000 | |

| (c) DEX | AIC | 5 | −19.85 *** | 0.000 | 4 | −15.40 *** | 0.000 |

| SIC | 5 | −19.85 *** | 0.000 | 1 | −25.49 *** | 0.000 | |

| GTS05 | 5 | −19.85 *** | 0.000 | 4 | −15.40 *** | 0.000 | |

| (d) MEV | AIC | 6 | −15.84 *** | 0.000 | 2 | −22.57 *** | 0.000 |

| SIC | 4 | −19.05 *** | 0.000 | 2 | −22.57 *** | 0.000 | |

| GTS05 | 6 | −15.84 *** | 0.000 | 2 | −22.57 *** | 0.000 | |

| (e) NFTs | AIC | 3 | −17.27 *** | 0.000 | 3 | −19.39 *** | 0.000 |

| SIC | 0 | −33.10 *** | 0.000 | 3 | −19.39 *** | 0.000 | |

| GTS05 | 3 | −17.27 *** | 0.000 | 3 | −13.39 *** | 0.000 | |

| (f) Stablecoins | AIC | 7 | −17.92 *** | 0.000 | 7 | −12.02 *** | 0.000 |

| SIC | 6 | −20.63 *** | 0.000 | 6 | −14.03 *** | 0.000 | |

| GTS05 | 6 | −20.63 *** | 0.000 | 6 | −14.03 *** | 0.000 | |

| Forward | Rolling | Recursive | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Direction of Causality | Wald | 95th | 99th | Wald | 95th | 99th | Wald | 95th | 99th |

| (a) Bridges | |||||||||

| Bridge volume Fees | 7.09 | 8.98 | 14.18 | 16.73 *** | 9.86 | 15.08 | 16.81 *** | 10.19 | 15.56 |

| Bridge activity Fees | 17.20 *** | 9.48 | 15.63 | 19.71 *** | 8.71 | 15.41 | 27.63 *** | 11.03 | 16.04 |

| Fees Bridge volume | 4.13 | 7.19 | 11.29 | 15.47 *** | 7.68 | 12.87 | 15.67 *** | 7.87 | 12.87 |

| Fees Bridge activity | 9.19 ** | 6.22 | 11.92 | 13.95 *** | 6.45 | 11.84 | 15.89 *** | 6.82 | 11.92 |

| (b) CEX | |||||||||

| CEX volume Fees | 27.05 *** | 8.17 | 11.47 | 31.87 *** | 9.63 | 15.32 | 47.96 *** | 10.27 | 15.63 |

| CEX activity Fees | 3.42 | 7.39 | 13.27 | 46.99 *** | 8.74 | 15.85 | 46.99 *** | 9.06 | 16.04 |

| Fees CEX volume | 52.35 *** | 7.69 | 14.42 | 29.24 *** | 9.03 | 13.82 | 55.79 *** | 9.29 | 14.51 |

| Fees CEX activity | 16.65 *** | 7.46 | 11.31 | 33.49 *** | 7.65 | 13.53 | 33.49 *** | 7.94 | 14.51 |

| (c) DEX | |||||||||

| DEX volume Fees | 9.07 ** | 8.93 | 15.08 | 32.20 *** | 10.62 | 14.52 | 32.39 *** | 10.97 | 15.46 |

| DEX activity Fees | 30.77 *** | 9.07 | 14.38 | 29.33 *** | 9.94 | 15.47 | 36.66 *** | 10.60 | 15.86 |

| Fees DEX volume | 17.36 *** | 9.17 | 15.60 | 19.52 *** | 9.39 | 17.92 | 36.40 *** | 9.70 | 17.93 |

| Fees DEX activity | 18.98 *** | 10.85 | 16.11 | 20.69 *** | 11.97 | 15.36 | 22.04 *** | 11.98 | 16.17 |

| (d) MEV | |||||||||

| MEV volume Fees | 13.85 ** | 11.03 | 23.09 | 18.27 ** | 15.86 | 25.40 | 18.31 ** | 16.65 | 25.99 |

| MEV activity Fees | 13.41 | 13.59 | 23.09 | 21.54 *** | 13.83 | 24.30 | 26.06 *** | 14.58 | 26.01 |

| Fees MEV volume | 13.21 ** | 11.36 | 17.52 | 20.01 *** | 12.06 | 17.01 | 23.43 *** | 12.51 | 17.52 |

| Fees MEV activity | 8.56 | 11.20 | 19.01 | 21.51 *** | 11.49 | 18.74 | 21.62 *** | 12.26 | 19.01 |

| (e) NFT | |||||||||

| NFT volume Fees | 6.94 | 8.19 | 14.33 | 17.42 ** | 9.03 | 18.90 | 17.42 ** | 9.61 | 18.90 |

| NFT activity Fees | 11.58 ** | 9.00 | 12.50 | 17.67 *** | 9.03 | 12.50 | 23.13 *** | 9.71 | 13.40 |

| Fees NFT volume | 12.57 ** | 10.25 | 13.79 | 37.30 *** | 10.64 | 13.90 | 41.21 *** | 10.67 | 14.15 |

| Fees NFT activity | 12.39 | 12.82 | 16.16 | 36.77 *** | 13.02 | 17.99 | 38.66 *** | 13.46 | 17.99 |

| (f) Stablecoins | |||||||||

| Stablecoin volume Fees | 9.36 *** | 7.05 | 9.31 | 11.52 ** | 8.03 | 11.79 | 16.79 *** | 8.07 | 12.92 |

| Stablecoin activity Fees | 13.12 ** | 12.49 | 16.90 | 26.84 *** | 13.83 | 20.67 | 40.98 *** | 14.50 | 20.67 |

| Fees Stablecoin volume | 9.07 ** | 8.58 | 11.28 | 23.61 *** | 8.55 | 11.73 | 36.78 *** | 8.93 | 11.90 |

| Fees Stablecoin activity | 41.55 *** | 7.43 | 12.84 | 18.11 *** | 9.86 | 13.66 | 43.56 *** | 9.14 | 13.66 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ante, L.; Saggu, A. Time-Varying Bidirectional Causal Relationships between Transaction Fees and Economic Activity of Subsystems Utilizing the Ethereum Blockchain Network. J. Risk Financial Manag. 2024, 17, 19. https://doi.org/10.3390/jrfm17010019

Ante L, Saggu A. Time-Varying Bidirectional Causal Relationships between Transaction Fees and Economic Activity of Subsystems Utilizing the Ethereum Blockchain Network. Journal of Risk and Financial Management. 2024; 17(1):19. https://doi.org/10.3390/jrfm17010019

Chicago/Turabian StyleAnte, Lennart, and Aman Saggu. 2024. "Time-Varying Bidirectional Causal Relationships between Transaction Fees and Economic Activity of Subsystems Utilizing the Ethereum Blockchain Network" Journal of Risk and Financial Management 17, no. 1: 19. https://doi.org/10.3390/jrfm17010019

APA StyleAnte, L., & Saggu, A. (2024). Time-Varying Bidirectional Causal Relationships between Transaction Fees and Economic Activity of Subsystems Utilizing the Ethereum Blockchain Network. Journal of Risk and Financial Management, 17(1), 19. https://doi.org/10.3390/jrfm17010019