1. Introduction

Globally, most all countries want to grow and prosper economically. Foreign direct investment (FDI) into a country and especially a developing country is a key driver of itseconomic prosperity. Understanding and having insights into the factors that motivate increased FDI area critical vein of research which sheds light on those actions a country can take to promote the most beneficial FDI for its economy. Multi-national corporations (MNCs) look for those characteristics within a country that will give them the greatest chance of success. But just as importantly, they look at the risks that can undermine their success. Some variables serve to enhance FDI while other variables negatively impact FDI. Countries wanting to increase FDI should promote those areas that increase beneficial FDI while avoiding those issues that inhibit FDI. These factors include everything from geopolitical risk (GPR) to economic, financial, and technological development.

A key factor multinationals incorporate in their decisions on FDI to countries like Vietnam is the GPR of a particular country or region. Research indicates that GPR’s impact is moresignificant for emerging market economies than for developed economies. The question of interest is in what ways and under what conditions GPR most impacts FDI both positively and negatively, and alsowhich components of GPR are most influential on FDI. There are a number of factors that MNCs look at to evaluate these risks. The International Country Risk Guide Index identifies 12 components of GPR including government stability, socio-economic pressure, investment profile, internal conflict, external conflict, corruption, military influence, religious tensions, law and order, ethnic tension, democratic accountability, and, lastly, bureaucracy quality.

Vietnam is an economy on the verge of moving from a frontier market to an emerging market via its transition from a central planning to a market-based economy with a wealth of economic opportunities. Vietnam’s economy has been significantly integrated in the world economy since Doi Moi (

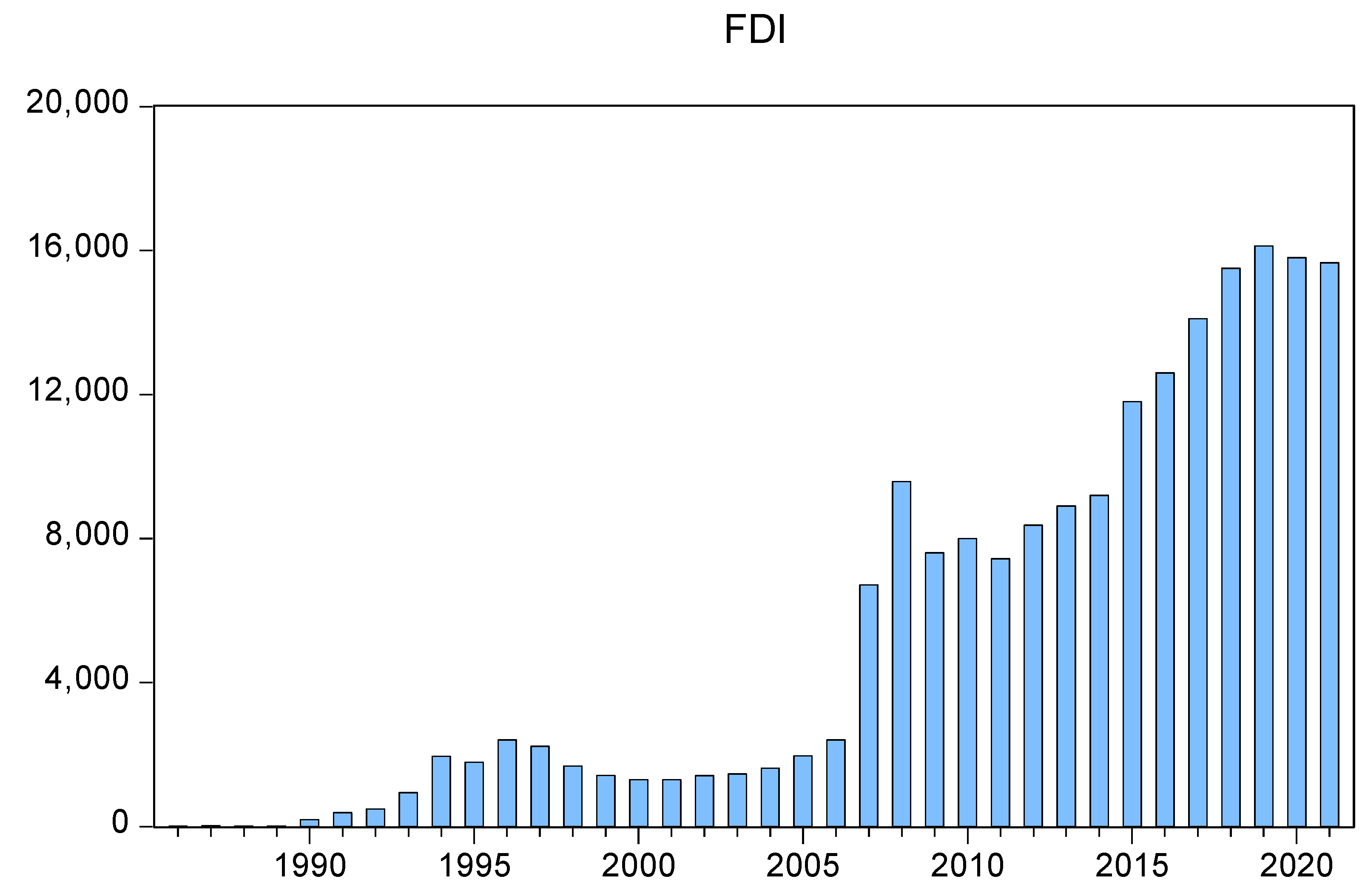

Truong and Vo 2023). In addition, foreign direct investment (FDI) inflows to Vietnam have continuously increased during the pastfew decades. Specifically, the statistics of the World Bank show that Vietnam’s FDI inflows increased by nearly 400 times its 1986 value of USD 40 million to USD 15,660 million in 2021.

Many things are driving thisdevelopment success. Vietnam stands to be a big winner from Western economies looking to disentangle their supply chain exposure to China. First and foremost, MNCs headquartered in the West are looking for countries with a qualified and low-cost labor pool and the infrastructure in place to sustain the MNCs’ supply chain needs. However, equallyimportant is the political and legal environment of the country. These risks can easily derail MNCs’ plans and cost significant resources. Although the effects of GPR on FDI inflows have been extensively studied in many countries, to our knowledge, no study has investigated the effects of GPR on Vietnam’s FDI inflows. Therefore, this study is devoted to exploring the effects of GPR on FDI inflows to Vietnam, a transition economy.

The contributions of this study to the literature are as follows. First, this study enriches our knowledge on the effects of GPR on FDI inflows in a transition economy. Vietnam provides fertile ground for a unique investigation of the effects of GPR on FDI inflows due to the fact that Vietnam’s economy has been in the transitional period with a deep and wide integration in the world economy. In addition, Vietnam has adopted the socialist-oriented market economy that is a unique model with its own characteristics in institutions and policies. By pursuing this model, Vietnam has remarkably achieved macro-economic performances in recent decades. Second, by using the ARDL (autoregressive distributed lag) bounds test approach, the short-term and long-term effects of GPR on the FDI are estimated. It is noted that the ARDL approach is proved to have some advantages in comparison with other co-integration techniques. Third, this study employs a comprehensive dataset covering the period from 1986 through to 2021 that allows for an in-depth analysis of both short-term and long-term effects of GPR on FDI.

The findings derived from the ARDL approach indicate that GPR has a significantlynegative effect on Vietnam’s FDI inflows in the long-term. Interestingly, the ARDL model reveals a positive effect of GPR on FDI in the short-term, indicating possible opportunistic FDI by these MNCs during increased GPR. In addition, an analysis using an error correction model shows that nearly half of the previousyear’s disequilibria converges back in the current year to the long-term equilibria level. Based on the findings, some policy implications are drawn for policymakers in transitional countries, like Vietnam, to mitigate the negative impact of GPR on FDI.

This paper is organized as follows.

Section 2 reviews the previous literature while

Section 3 provides the data and methodology employed in the analysis.

Section 4 contains the results of the analysis.

Section 5 discusses the results, and

Section 6 concludes the study.

2. Literature Review

The effects of GPR on FDI havebeen widely investigated and documented in the literature in recent decades. There is a broad array of research examining GPR’s influence on FDI for many other countries and regions. Past research has documented that geopolitical risk (GPR) significantly affects FDI. The literature takes a number of different approaches to identify factors that either enhance or diminish the influence of GPR on FDI. Earlier research in this field focuses mainly on the impact of political and economic risks on FDI.

Ramcharran (

1999) investigates the effects of political and economic risks on FDI for 26 countries over the period 1992–1994. Using Euromoney’s Country Risk Data indexes as indicators of political and economic risks, the author finds a significant negative impact on FDI from increased political and economic risks. Subsequently,

Mudambi and Navarra (

2003) take a different approach by examining the effect of political traditions within a single country, Italy, to identify multinational FDI locational choices within this particular country. The authors contend that regional political traditions vary substantially across regions within Italy. Using a two-step econometric model, they examine the impact of local government’s political orientation on FDI within each region across Italy. Interestingly, the authors find that a transition within the local government towards a center-right political orientation positively impacts regional FDI, while the opposite is true for a change to a center-left political orientation which has a negative influence on regional FDI. The move to a far-left political orientation within a region is mostly associated with a negative change in FDI. Subsequently,

Hayakawa et al. (

2013) examine the impact of both financial and political risks on FDI inflows for 89 countries over the period 1985–2007. The authors use both the level of these risks and their change over time. Interestingly, the authors find that only political risk and not financial risk adversely affects FDI. For developing countries in the sample, internal conflict, corruption, military influence on politics, and bureaucratic quality were negatively related to FDI. Conversely, the authors not only find that lower financial risk levels do not increase FDI, but that for developing countries, greater financial risk may actually increase FDI. The authors contend that these results are indications of a merger and acquisition fire sale phenomenon surrounding different financial crises. If this is the case, the authors posit that financial risk may have a differing impact on green field FDI versus M&A-motivated FDI. Moreover, in a study that includes 91 countries over the period 2002–2012,

Erkekoglu and Kilicarslan (

2016) use panel data analysis to examine the influence on FDI of various factors including political risks. The authors identify six political risk variables which are freedom of expression and transparency, political stability and absence of violence, management effectiveness, regulatory quality, rule of law, and prevention of corruption. They also use fivecontrol variables that are FDI, consumer price inflation, GDP, exportation of goods and services, and population size. To control for interdivisional correlation, autocorrelation, and heteroscedasticity, the authors use a Driscoll–Kraay fixed-effects model. The findings indicate that FDI is positively associated with the exportation of goods and services, population, and logarithms of GDP. However, political stability and the absence of violence along with administration efficacy negatively impact FDI. Also employing panel data,

Weiling and Martek (

2021) use 74 developing countries for the period 2008–2017 to delve into the influence of certain political risks on sustainable development and access to clean energy by looking at FDI related to energy investment. The authors find that the risk of investment profile, law and order, religious tensions, and corruption have a significant negative impact on foreign energy investments. But, these factors’ influence can be reduced by gross domestic product, economic freedom, and host country energy demand. The authors go on to use clustering techniques to Identify commonality within sub-groups of the 74 countries, finding that developing countries will share similar political risk and macro-environmental profiles with some countries but not others. They find five clusters ranging in size from 7 to 25 countries in each similar grouping. Haiti and Iraq were outliers not paired with any cluster.

Following up on the impact of political elections,

Julio and Yook (

2016) identify national elections as times of political uncertainty and examine US multinational FDI across 43 countries surrounding these elections. The authors find that US multinational FDI drops by 13% on average for the time period just preceding a national election. The more competitive the election, the greater the impact on FDI. They also report that the drop in foreign FDI significantly exceeds any drop in domestic investment over the same period. Once the election is over, FDI then increases as greater political certainty returns. Though greater for emerging markets, the results were also robust for developed countries, indicating that political uncertainty universally affects a country’s FDI. Countries identified as having higher quality legal and political institutional quality have significantly less FDI variation surrounding elections. In another analysis,

DesBordes (

2010) delves into whether multinationals consider both global and diplomatic risk when considering FDI. The author contends that these risks are different in that diplomatic risk is country-specific based on governmental relations. However, GPR is the same for all multinationals regardless of location. Using modeling from bilateral FDI panel data with included dyadic effects, the authorfinds that both global and diplomatic political risks negatively impact FDI by US multinationals who demand higher returns when faced with these risks. Similar to GPR, a one-standard-deviation rise in diplomatic risk increases the required return by approximately 0.80%. Also employing a dyadic approach for the period 1980–2000, using a GMM estimator to a gravity model of FDI for 58 countries with 1117 dyads,

Li and Vashchilko (

2010) examine the impact of military conflicts as a source of political risk and uncertainty on bilateral capital flows. The authors find that for the 18 countries with a per capita real income above USD 12,000, conflicts do not significantly impact capital flows. They also report that security alliances increase cross-border capital flows, with defense pacts having the greatest influence.

From a different perspective, several empirical studies investigate the effects of GPR indexes on FDI.

Busse and Hefeker (

2007) look at the impact of GPR on FDI across 83 developing countries for the period 1984–2003 using the 12 components of political risk tracked by the Political Risk Services (PRS) group reported in their International Country Risk Guide. These 12 components of political risk includegovernment stability, socio-economic pressure, investment profile, internal conflict, external conflict, corruption, military influence, religious tensions, law and order, ethnic tension, democratic accountability, and, lastly, bureaucracy quality. Using an Arellano–Bond GMM dynamic estimator to control for autocorrelation and endogeneity for the time-series analysis, the authors find that government stability, internal and external conflicts, law and order, ethnic tensions, and bureaucratic quality are highly significant determinants of FDI, while a significant but weaker relationship is found between FDI, corruption, and democratic accountability. Similarly,

Al-Khouri and Khalik (

2013) examine the impact of political risk on FDI over the period from 1984 to 2011 for the MENA region which consists of the Middle East and North Africa by using the 12 components of political risk tracked by the Political Risk Services (PRS) group. They find that market size and, in some cases, political risk are positively related to the change in FDI. Corruption and external conflict are most correlated with FDI flows for the 12 political risk components. Results show that market size and growth, agglomeration, and openness are all positively related to FDI. The authors further find that bureaucracy and ethnic tension negatively affect FDI. Counterintuitively, the authors report that countries with higher corruption, less democracy, and high internal conflicts are more able to attract FDI. Similar to

Al-Khouri and Khalik (

2013) and

Busse and Hefeker (

2007),

Rafat and Farahani (

2019) also use the 12 political risk indexesfrom the International Country Risk Guide to study the link between GPR and FDI in Iran over the period 1985–2016. They use a two-stage least squares model and find that of the 12 political risk indexes, external conflict, ethnic tensions, socioeconomic condition, investment profile, and military and religious tensions have a highly significant influence on multinational FDI for Iran. Using a generalized linear model,

Fania et al. (

2020) examines the influence of GPR on FDI for 16 West African countries. Like previous research, the authors report that the influence of GPR on FDI varies significantly across GPR’s sub-components. Taking a different approach from the research using GPR indexes,

Jensen (

2008) contends that these indexes only indirectly measure the relation between political risk and political institutions. To get a more direct measure, the author uses the political risk insurance agency premiums that multinationals are charged to cover government expropriations and contract disputes. Using this unique metric, the author reports that democratic governments reduce FDI risk for multinationals primarily by placing greater constraints on the executive leaders of the countries. To better explore the relationship between democracies and lower political risk, the author goes on to collect qualitative data from 28 investors, political risk insurers, plant location consultants, and multinational international lawyers. Overall, the author finds that the possibility of expropriation and other executive policy changes is significantly increased in countries with few constraints on the leader such as Russia, Bolivia, and Venezuela.

More recently, some studies measure the effects of GPR by using the GPR index created by

Caldara and Iacoviello (

2022) on FDI. Using a pseudo Poisson maximum likelihood estimation for a gravity trade model,

Thakkar and Ayub (

2022) examine the influence of GPR on bilateral FDI data for 2001–2012 and trade data for 1948–2019. The authors find that their univariate model indicates that for a 10% increase in GPR, there is a significant drop of 3.6% for FDI and a drop of 0.5% for trade. However, for their multivariate model, the results indicate a small increase in trade of 0.04%. Some other recent research includes

Nguyen et al. (

2022), who examine the influence of GPR on FDI inflows and total factor productivity for 18 emerging market countries over the period 1985–2019. The authors use Granger causality panel data tests along with seemingly unrelated regression models to find that GPR has a significant negative impact on technological progress and FDI. They also find that technological progress and FDI act to mitigate GPR. Furthering the literature on technologies’ impact on FDI, using multiple databases,

Bussy and Zheng (

2023) conclude that greater geopolitical risk and uncertainty also negatively impact FDI. The authors report that good governance shields FDI from GPR. In addition, rather than managingGPR, multinationals with closer geographic, cultural, and commercial relationships often delay FDI at rising GPR. On the technology front, they find that FDI for R&D industries has greater resilience to GPR, hypothesizing that technology is more readily transferred outside the country. Following up, the influence of geopolitical risks on FDI for Turkey over the period 1985–2020 was examined by

Altıner and Bozkurt (

2023). Using an ARDL bounds test approach, where FDI is the dependent variable and geopolitical risk, growth, globalization, and inflation are the explanatory variables, the authors find (as hypothesized) that an increase in geopolitical risk negatively impacts FDI. For the control variables, inflation negatively affectsFDI while higher economic growth and globalization motivate FDI. Moreover,

Yu and Wang (

2023) also employ a cluster fixed-effects model on a sample of 41 countries over the period 2003–2020 to examine the influence on FDI of GPR obtained from the GPR index created by

Caldara and Iacoviello (

2022). The authors identify three possibly mitigating motives for FDI that serve to limit GPR. These three control variables are market seeking, natural resource seeking, and strategic resource seeking motives. Overall, they find that GPR significantly reduces FDI which spills over to impact the domestic economy. In addition, they find that all control variables are significant drivers of FDI. In addition, the authors find that these results are robust for sub-sample data. They then use as the core explanatory variable an interaction between GPR and trade dependency, finding that the trade dependency of a country mitigates the negative influence of GPR on FDI.The authors go on tofind that GPR has a significant impact on FDI for emerging economies but not developed economies.

Overall, research provides some interesting and generally consistent insights into thefactors most likely to positively and negatively impact FDI. Political, economic, and financial factors all have varying positive and negative influences on FDI depending on the country, and asour analysis shows, differ for the shortterm versus the longterm. For example, greater financial risk is generally shown to enhance FDI while most political risks negatively impact FDI. Also, in more developed economies, these variables are muted, while their effectsare much more pronounced in emerging market economies thatcan be far more dependent on FDI. Domestic politics is also shown to influence GPR. Voting that moves a region tothe political left wing direction can have a significant negative impact on FDI. Similarly, concentratingtoo much power in the executive leader position also negatively influences FDI while democracy and a more balanced political power dynamic generally lead to greater FDI. However, counterintuitively, factors such as higher corruption levels and financial risk can motivate higher FDI in some cases. Although the effects of GPR on FDI inflows have been widely studied in many countries, to our knowledge, there are no studies that specifically examine the impact of GPR on FDI for Vietnam. Therefore, this study adds to theliterature by using the ARDL model to investigate the effects of GPR on Vietnam’s FDI inflows.

{kind=link}

{kind=link}

{kind=link}

{kind=link}