Abstract

The purpose of this study was to establish whether digital literacy and insurtech adoption influence insurance inclusion in Uganda. Principally, we sought to determine whether insurtech adoption mediates the nexus between digital literacy and insurance inclusion. This study adopted a cross-sectional and quantitative correlational approach. The study’s sample was 391 individuals who had used digital platforms such as mobile phones and computers to access insurance products and services in Uganda. Data were collected using structured survey questionnaires. Partial Least Squares Structural Equation Modelling (PLSEM) was employed to test the hypothesised relationships. The results demonstrated that both digital literacy and insurtech adoption significantly and positively influence insurance inclusion. We also found digital literacy to be a significant and positive determinant of insurtech adoption. Markedly, it was found that insurtech adoption mediates the association between digital literacy and insurance inclusion in Uganda. However, this study was conducted in a developing country with an underdeveloped insurance market and with low technological advancement. This may affect the generalisation of the study’s findings. This study’s novelty lies in establishing how digital literacy and insurtech adoption interact to influence insurance inclusion in Uganda. This is the first study to examine the effect of digital literacy and insurtech adoption on insurance inclusion.

1. Introduction

Currently, insurance inclusion has caught the attention of development partners and scholars as the missing link to full financial inclusion. This attention emanates from the soaring levels of insurance inclusion. Globally, insurance penetration is estimated at only 7%, and at 2.78% in Africa (IAIS 2022). In Uganda, insurance penetration is estimated at 0.80%. Moreover, 99% of the adult population in Uganda is not insured; yet, the people and businesses are susceptible to lifecycle shocks (Finscope 2018). According to Cheston et al. (2018) “insurance inclusion is the state of access to and use of appropriate and affordable insurance products for the unserved and underserved”. Arguably, existent studies have proved insurance to contribute to economic growth at the macro level and poverty alleviation at the micro level (Bayar et al. 2021; Zulfiqar et al. 2020). Thus, inclusive insurance can enable poverty alleviation through savings mobilisation for entrepreneurship and reducing people’s risk susceptibility (Kim et al. 2018). Despite the numerous benefits of insurance inclusion, vast segments of the population remain uninsured (IAIS 2022).

Prior studies have attributed the low level of insurance inclusion to behavioural and non-behavioural factors (Van der Cruijsen et al. 2021). On the one hand, behavioural factors such as trust, perceived value and insurance literacy have been found to influence insurance inclusion (Kiwanuka and Sibindi 2023; Van der Cruijsen et al. 2021). On the other hand, non-behavioural factors such as transaction costs, documentation requirements and distance have been found to influence insurance inclusion (Demirgüç-Kunt et al. (2018). Despite efforts to deal with the behavioural and non-behavioural deterrents to insurance inclusion, the level of insurance inclusion continues to remain very low, especially in emerging economies (IAIS 2022). As such, developing economies are currently leapfrogging insurtech to broaden insurance inclusion (Holliday 2019). However, insurtech is thought to have improved insurance penetration more in developed economies compared to developing economies (Reddy et al. 2020), hence contributing to the persistence of the insurance inclusion gap between developed and developed countries.

Despite rolling out insurtech in the insurance landscape, African countries are lagging behind in embracing the technology and still grappling with low insurance inclusion (Sibindi 2022). Yet, financial technologies are playing a significant role in creating access for unserved and underserved people, especially in rural areas. According to Gautum and Kanoujiya (2022), governments need to adopt and promote the usage of the financial technologies of mobile money and the like to promote the uptake of financial services. Digital networks render technological platforms through which financial services providers expand their reach to unserved and underserved segments (Kanga et al. 2022). According to Kabakus et al. (2023), technological platforms can only expand financial services’ outreach if the masses can ably utilise the technologies. Thus, the importance of digital literacy in fostering financial inclusion cannot be overemphasised. However, in today’s Fourth Industrial Revolution (4IR), scores of researchers have highlighted the importance of digital financial literacy in fostering financial services uptake (Setiawan et al. 2022; Rahayu et al. 2022). Notwithstanding, these studies have found digital financial literacy to influence financial inclusion. According to Gautum and Kanoujiya (2022), given today’s proliferation of digital financial services, consumers’ financial literacy level alone is not enough to foster financial inclusion. Therefore, significant attention needs to be paid to people’s digital financial literacy.

Although previous studies have emphasised the importance of insurance literacy in fostering insurance inclusion (Kiwanuka and Sibindi 2023; Van der Cruijsen et al. 2021), few studies have investigated the influence of digital literacy on insurance inclusion. Moreover, despite the emphasised importance of insurtech for access to insurance services, barely any studies have explained how digital literacy and insurtech interact to influence insurance inclusion. However, previous studies proffered mixed results on the association between digital literacy and the adoption of technology. Some studies found digital literacy to influence technology adoption (see, for instance, Kabakus et al. 2023; Nikou et al. 2022) while others found digital literacy not to influence technology adoption (see, for instance, Kabakus et al. 2023; Jang et al. 2021). Moreover, the foregoing studies were conducted in work settings and learning institutions. Thus, there is a need to particularly investigate how digital literacy and insurtech influence insurance inclusion.

Against this backdrop, we sought to examine how digital literacy and insurtech influence insurance inclusion in the Ugandan context. Distinctly, we aimed to examine the mediating role of insurtech adoption in the relationship between digital literacy and insurance inclusion. As such, our study cross-sectionally surveyed individuals who have used digital platforms such as mobile phones and computers to access insurance in Uganda. The study hypotheses were tested through PLS-SEM. We found digital literacy and insurance inclusion to be significantly and positively related. Also, insurtech adoption was found to positively influence variations in insurance inclusion. Moreover, digital literacy was found to positively influence insurtech adoption. Furthermore, a significant partial mediation effect of insurtech adoption in the relationship between digital literacy and insurance inclusion in Uganda was found. In addition to prior studies that have found digital financial literacy and financial technologies to influence access to and usage of financial services (see, for instance, Kass-Hanna et al. 2022; Lyons and Kass-Hanna 2021; Lyons et al. 2020; Rahayu et al. 2022; Demirgüç-Kunt et al. 2022; instance Holliday 2019; Rosyadah et al. 2021; Beck 2020; Gautum and Kanoujiya 2022; Kabakus et al. 2023), the current study makes an original contribution by positing that insurtech adoption has a mediating effect on the relationship between digital literacy and insurance inclusion in Uganda. Until now, it has not been known how digital literacy interacts with insurtech to influence insurance inclusion.

2. Literature Review and Hypothesis Development

2.1. Theoretical Review

The Technology Acceptance Model (TAM) proposed by Davis (1989) was used to examine whether digital literacy and insurtech adoption influence insurance inclusion. The TAM (Davis 1989) is a theory that explains users’ acceptance and usage of technologies. In this regard, the TAM theory (Davis 1989) postulates that actual technology usage is directly or indirectly influenced by perceived usefulness, perceived ease of use and attitude towards usage of the technology. In the TAM, perceived usefulness implies the extent to which the technology improves a user’s activity performance, while perceived ease of use denotes how the user perceives the technology as effortless. In addition, the attitude towards usage denotes the cause of the intention leading to future behaviour. When a technology is not easy to use, it might not be perceived as useful (Gie and Fenn 2019). Ajzen and Fishbein (2000) state that the usage attitude has an evaluative effect on the positive and negative feelings of people in terms of the performance of a specific behaviour. In the TAM, perceived usefulness, perceived ease of use and attitude towards use predict the actual usage and behavioural intentions of users (Nikou et al. 2022). According to Elkaseh et al. (2016), perceived usefulness and perceived ease of use influence behavioural intention. Accordingly, the TAM (Davis 1989) is adopted in the current study to understand how insurtech adoption influences insurance inclusion, both directly and indirectly, as a mediator in the relationship between digital literacy and insurance inclusion.

2.2. Hypothesis Development

2.2.1. Digital Literacy and Insurance Inclusion

In the wake of the current digital revolution, being digitally literate is considered a vital quality that people must have (Hassan et al. 2022). Presently, almost all financial products and services are provided digitally (Prasad et al. 2018). As such, in addition to traditional financial literacy, digital literacy is increasingly fostered to broaden financial inclusion (Lyons and Kass-Hanna 2021). People can only actively partake in the current digital economy if they are sufficiently knowledgeable and skilled to undertake digital financial transactions (Kass-Hanna et al. 2022). Despite digitisation to foster increased access to financial services, most people are not aware of how to operate digital technologies (Hassan et al. 2022). According to Demirgüç-Kunt et al. (2022), almost two-thirds of the unbanked do not know how to use mobile money accounts. Regardless, Wang et al. (2022) found digital literacy among the elderly and middle-aged people to significantly influence the possibility of participating in financial markets. People without digital literacy are less represented in financial investments. Markedly, in the current digital financial services-based economy, being financially literate alone is inadequate (Chan et al. 2022), hence the need to focus on people’s digital financial literacy. As such, digital financial literacy skills and financial literacy enable efficient usage of financial services and protection against risks (Rahayu et al. 2022). Thus, we hypothesise the following:

H1.

Digital literacy positively influences insurance inclusion in Uganda.

2.2.2. Insurtech Adoption and Insurance Inclusion

Insurtech, a subset of fintech, entails the application of technology to deliver insurance-specific solutions through innovations for traditional and non-traditional market players (Bittini et al. 2022). Although insurtech emerged much later than fintech for the banking sector, it is entrenched in every part of the insurance industry (Lin and Chen 2020). Principally, with the introduction of financial technologies, access to financial services has improved significantly (Asif et al. 2023). As such, Gautum and Kanoujiya (2022) state that governments need to adopt financial technologies to proliferate financial inclusion programmes across all levels. With the Fourth Industrial Revolution, financial technologies are expected to deepen the global financial inclusion index (Rosyadah et al. 2021). According to Beck (2020), mobile phone technologies have enabled developing countries to leapfrog traditional financial services provision models to increase access to financial services and products. Digitalisation enables transactions across larger geographical areas and at faster speeds (Rosyadah et al. 2021). According to Sibindi (2022), it was established that ICT significantly impacts insurance market development in Africa. Particularly, the penetration of mobile phones usage has a significant positive impact on the consumption of life insurance (Asongu and Odhiambo 2020). Accordingly, this study hypothesises the following:

H2.

Insurtech adoption positively influences insurance inclusion in Uganda.

2.2.3. Digital Literacy and Insurtech Adoption

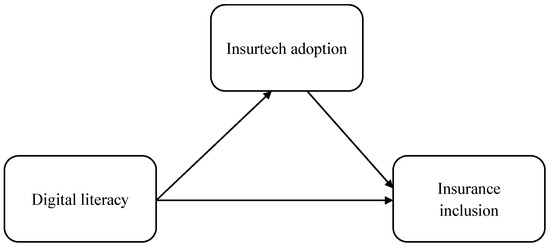

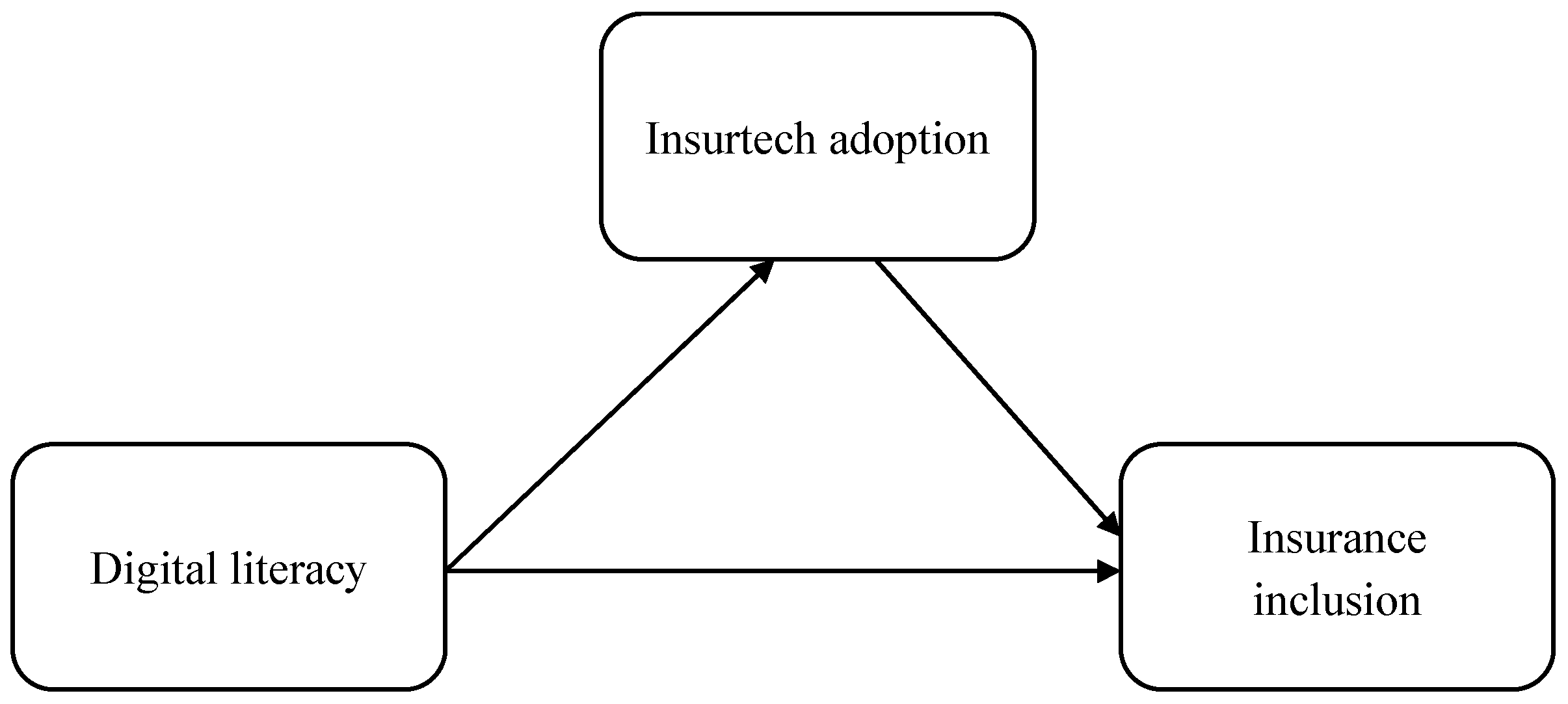

Although financial technologies have been argued to promote financial inclusion (Rosyadah et al. 2021; Beck 2020), Morgan et al. (2019) argue that to achieve increased financial inclusion, it will require higher levels of digital literacy to effectively use financial technologies. Furthermore, Nikou et al. (2022) argue that the obstacle to digitalisation lies in ensuring people know how to use the technology. Thus, the fast introduction of digital technologies has rendered digital skills important (Mikheev et al. 2023). However, the previous literature on the influence of digital literacy and technology adoption has found mixed results. According to Kabakus et al. (2023), digital literacy was found to directly influence perceived ease of use but not perceived usefulness. On the one hand, in their research on higher education institutions in Finland, Nikou and Aavakare (2021) find digital literacy to have no influence on students’ intention to use digital technologies. On the other hand, while investigating the effect of digital literacy on intention to use e-learning among small and medium enterprises, Mohammadyari and Singh (2015) find digital literacy to significantly influence the intention to use or not continue using web 2.0 technologies. On this footing, it can be deduced that the influence of digital literacy on technology adoption is inconclusive. Regardless, prior studies attribute digital exposure to the adoption of technologies (Kabakus et al. 2023; Moenjak et al. 2020). Therefore, based on the foregoing, the current study hypothesises the following as conceptualised in Figure 1:

Figure 1.

Conceptual framework. Source: Authors’ own conceptualisation.

H3.

Digital literacy positively influences insurtech adoption.

H4.

Insurtech adoption mediates the relationship between digital literacy and insurance inclusion.

3. Research Methodology

In this study, we cross-sectionally gathered quantitative data to address the study’s hypotheses. This design was adopted owing to its ability to provide large amounts of data at a given point in time. The data were collected from individuals who have used digital platforms such as mobile phones and computers to access insurance products and services in Uganda. The study participants were clients of three insurance providers (Yeko, Turaco and Prudential) that have adopted insurtech to extend insurance services in Uganda (Insurance Regulatory Authority 2022). The data were collected by distributing questionnaires to the study participants. Overall, a sample of 391 participants partook in the current study. Yamane’s (1973) sample size determination formula [n = N/1 + N (e)2] was adopted to arrive at the sample. The study participants were selected through a single-stage sampling procedure. Accordingly, the study participants were selected using proportionate stratified simple random sampling. This sampling procedure enabled an equal chance of all the participants partaking in the study. A structured questionnaire with response items ranging from 1 = strongly disagree to 5 = strongly agree was adopted to gather the primary data. Prior to data collection, the participants’ consent to partake in the study was sought. Notably, the complete data were tested for robustness. The data were tested for validity and reliability. Accordingly, the discriminant and convergent reliability were assessed. Additionally, the multicollinearity among the variables was tested using the Variance Inflation Factors. The diagnostic findings are presented in the next section. The measurements of the study variables were adopted from previous studies. Digital literacy was measured using knowledge (KNW) and skill (SKL), as adopted from Hassan et al. (2022) and Kass-Hanna et al. (2022). Insurtech adoption was measured by perceived ease of use (PEU) and perceive usefulness (PU), as suggested by Davis (1989). The measures for insurance inclusion were access (ACS) and usage (USG), as suggested by Kiwanuka and Sibindi (2023) and Cheston et al. (2018). The study’s measurement items are shown in Appendix A.

4. Empirical Results Presentation and Analysis

4.1. Diagnostic Results

Diagnostics were run to establish any biases that could compromise the reliability of the research findings. The data were checked for composite reliability, discriminant validity, convergent validity content validity, construct validity and multicollinearity. Cronbach’s alpha (α) coefficient was used to test for composite reliability, where values above 0.70 were accepted (Hair et al. 2019). Similarly, the discriminant validity and convergent validity were tested using the heterotrait–monotrait ratio (HTMT) and average variance extracted (AVE) as guided. Principally, convergent validity shows how construct measures correlate with each other and the extent to which the variance (AVE) in the construct is influenced by the loaded items other than the measurement error. On the other hand, discriminant validity determines whether the measures of insurance inclusion, insurtech adoption and digital literacy are empirically different from each other. The diagnostics revealed that all the study variables had discriminant validity values above the 0.50 cut-off and below the 0.95 upper limit. Hence, the presence of discriminant validity among insurance inclusion, digital literacy and insurtech adoption. Additionally, all the results for the average variance extracted (AVE) were above the 0.5 cut-off. Hence, the presence of convergence validity among the measures of insurance inclusion, digital literacy and insurtech adoption. Similarly, it was established that there was no multicollinearity, since all the variance inflation factors (VIFs) were below 5, as guided by Hair et al. (2019). Table 1 and Table 2 present the results of the diagnostic tests.

Table 1.

Reliability and validity.

Table 2.

Multicollinearity and discriminant validity.

4.2. Sample Characteristics

The results in Table 3 show that there were more females accessing insurance via digital platforms compared to their male counterparts. The female respondents comprised 57.1% of the sample, while the males were 42.9% of the sample. The findings also indicate most of the respondents to be in the age range of 34–49 years, with a 49.7% sample representation. Additionally, 45.7% of the respondents were in the age range of 18–33 years. Only 4.6% of the study sample was in the age range of 50–65 years. In terms of the level of education, the majority of the respondents indicated themselves to be degree holders at 65.7% of the sample, followed by diploma holders at 14.6% of the sample. Furthermore, 10.7% of the respondents held masters’ degrees, while only 5.1% and 2.6% of the respondents had advanced level UACE and UCE, respectively. Also, the results show that only 1.3% of the respondents had PhDs, while there were no respondents with Primary Leaving Certificates. Lastly, 91.6% of the respondents indicated themselves to have used a mobile phone platform to access insurance services, while 8.4% of the respondents had used a computer to digitally access insurance products and services.

Table 3.

Sample characteristics.

4.3. Correlational Analysis

We used the Pearson’s correlation to establish the relationship between digital literacy, insurtech adoption and insurance inclusion. The correlation results are indicated in Table 4. The results show digital literacy to be positively and significantly associated with insurance inclusion (r = 0.525, p < 0.01). The results suggest that positive variances in digital literacy lead to positive variances in insurance inclusion. Also, the results reveal a significant positive relationship between insurtech adoption and insurance inclusion (r = 0.683, p < 0.01). This suggests that as insurtech adoption increases, insurance inclusion increases significantly. Lastly, the correlational results show that digital literacy is positively associated with insurtech adoption (r = 0.532, p < 0.01). This finding suggests that positive changes in digital literacy are associated with positive changes in insurance inclusion. Given that insurtech adoption is positively associated with both digital literacy and insurance inclusion, it is an indication that insurtech adoption can mediate the digital literacy and insurance inclusion nexus. Based on Hair et al. (2019), a mediation effect suffices when the mediating variable is associated with both the independent and the dependent variables.

Table 4.

Correlation results.

4.4. Structural Equation Modelling Results

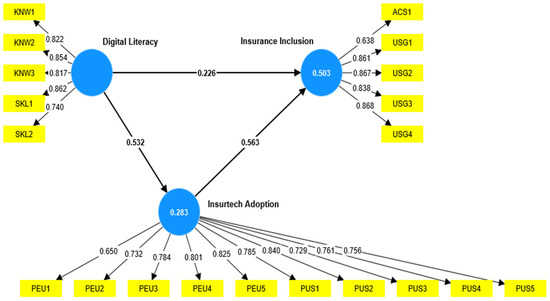

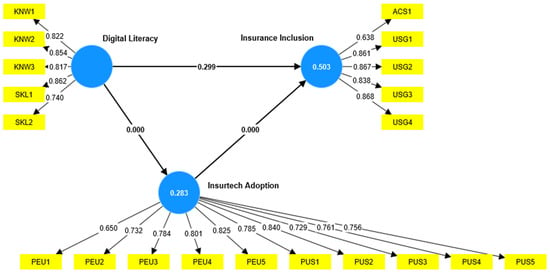

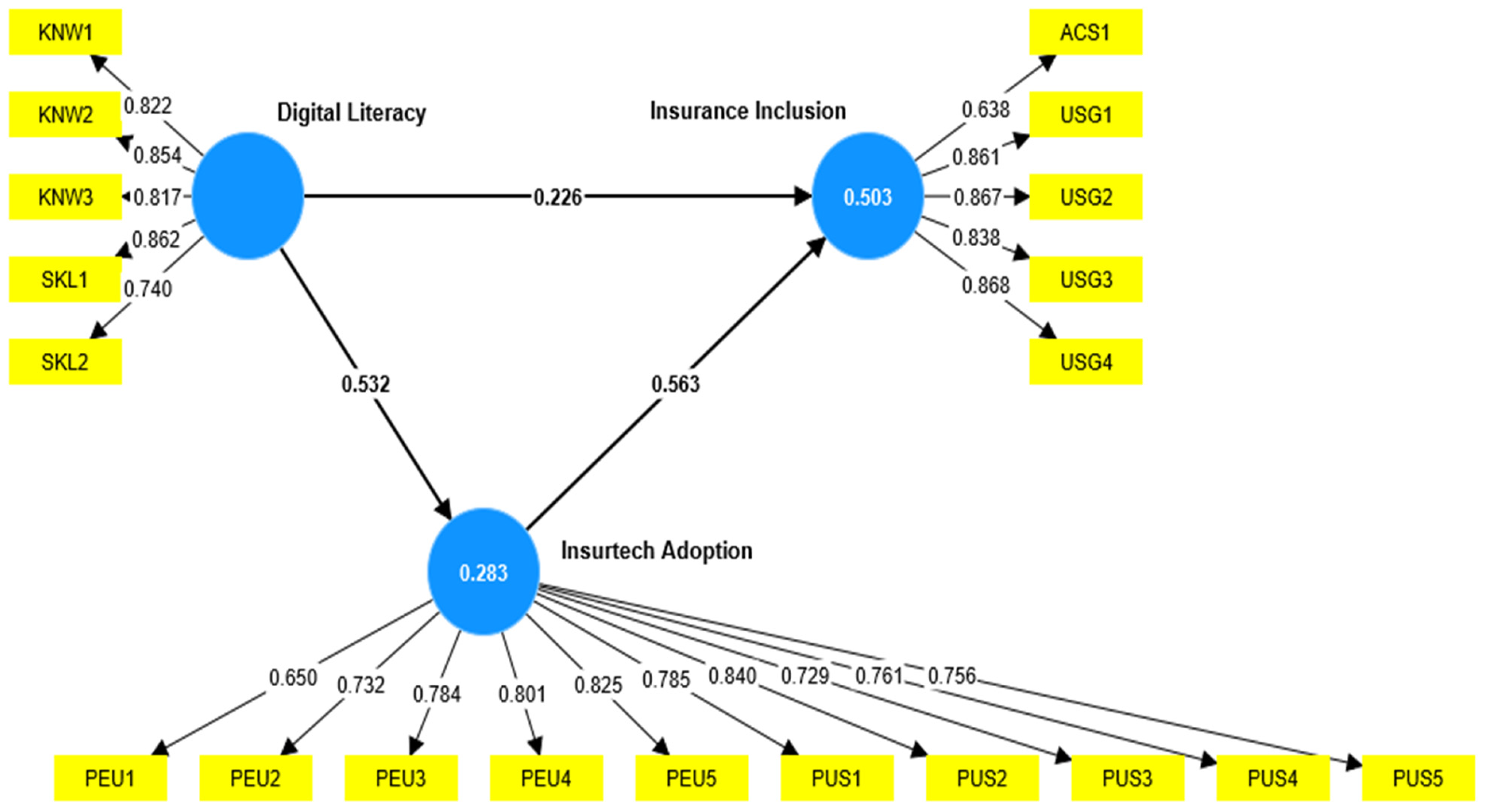

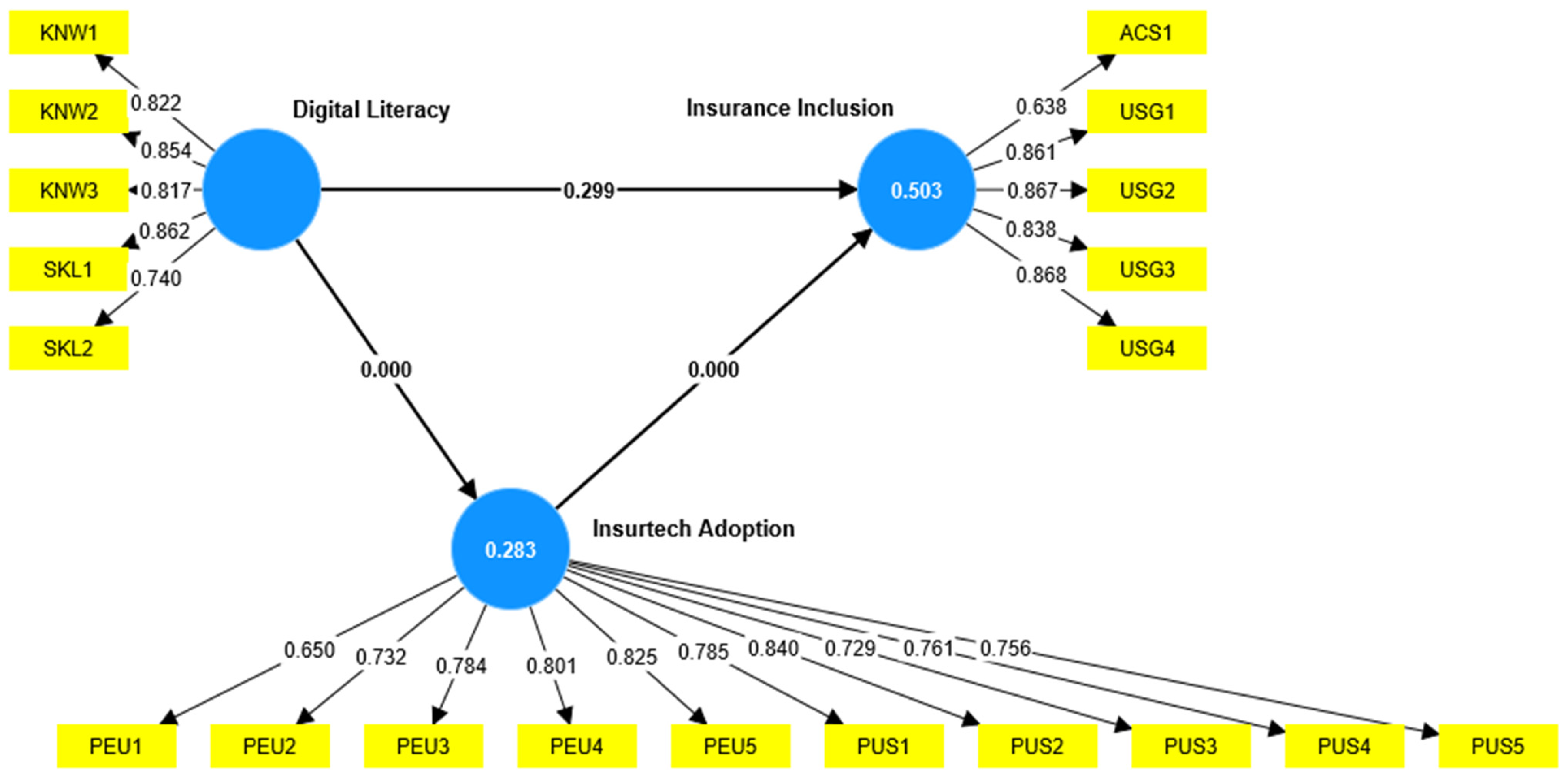

This study sought to establish the effect of digital literacy and insurtech adoption on insurance inclusion. Moreover, this study sought to establish the mediating role of insurtech adoption in the relationships between digital literacy and insurance inclusion in Uganda. As such, PLS-SEM was adopted to test the study hypotheses. PLS-SEM was adopted given its ability to perform exploratory and confirmatory statistical modelling for theory testing. According to Hair et al. (2019), PLS-SEM can estimate multivariate relationships while addressing the issue of measurement error. Furthermore, variance-based SEM was employed, given its predictive power compared to covariance-based SEM. The PLS-SEM results reveal that digital literacy significantly and positively (β = 0.226; t = 3.940; p < 0.0001) influences insurance inclusion in Uganda. A one unit change in digital literacy leads to a 0.266 positive change in insurance inclusion. This finding supports the hypothesis (H1). Furthermore, the findings reveal insurtech adoption has a significant positive impact (β = 0.563; t = 12.634; p < 0.0001) on insurance inclusion in Uganda. A one unit change in insurtech adoption leads to a 0.563 positive change in insurance inclusion. Hence, the hypothesis (H2) is supported. Additionally, the study’s findings reveal that digital literacy significantly and positively influences insurtech adoption in Uganda (β = 0.532; t = 13.526; p < 0.0001). A one unit change in digital literacy leads to a 0.532 positive change in insurtech adoption. Hence, the hypothesis (H3) is supported. Particularly, the results reveal that insurtech adoption partially mediates the relationship between digital literacy and insurance inclusion in Uganda (β = 0.299; t = 8.884; p < 0.0001). Significant portions (β = 0.299) of the direct effect of digital literacy go through insurtech adoption to influence insurance inclusion. The hypothesis testing results are presented in Table 5. Overall, the findings reveal that the direct and indirect effects of digital literacy and insurtech adoption explain 50.3% of the variance in insurance inclusion, as depicted in Figure 2 and Figure 3. According to Hair et al. (2019), an R2 of 0.26 and above shows a substantial effect of the predictors on the exogenous variable. Thus, it can be inferred that in the current model, digital literacy and insurtech adoption sufficiently predict insurance inclusion in Uganda.

Table 5.

Hypothesis testing results.

Figure 2.

PLS-SEM algorithm with direct effects and factor loadings.

Figure 3.

PLS-SEM algorithm with indirect effects.

5. Discussion

This study sought to establish the influence of digital literacy and insurtech adoption on insurance inclusion in Uganda. As such, the study was anchored on four hypotheses that were all supported by the findings.

Firstly, the study’s findings revealed that digital literacy significantly and positively influences insurance inclusion in Uganda. This finding suggests that when consumers are knowledgeable about how to use digital devices such as computers, smart phones and other related devices, they can obtain an insurance policy using such digital devices. Additionally, consumers’ digital literacy enables them to ably navigate and search for insurance information on the internet and other digital platforms. As well, when consumers are aware of the threats and risks associated with online transactions, they can have the confidence to buy insurance products and seek insurance services through digital insurance platforms. The finding that digital literacy is associated with insurance inclusion is consistent with Kass-Hanna et al. (2022), who argue that people can only actively partake in the current digital economy when they are sufficiently knowledgeable and skilled to undertake digital finance transactions. Moreover, prior studies suggest that in addition to traditional financial literacy, there is a need to foster digital financial literacy to broaden financial inclusion (Lyons and Kass-Hanna 2021; Lyons et al. 2020). When people lack digital knowledge and skills, they will not be financially included (Demirgüç-Kunt et al. 2022). The study’s findings are also in agreement with Rahayu et al. (2022), who argue that digital and financial literacies enable efficient usage of financial services and protection against risks. Also, Kass-Hanna et al. (2022) find digital literacy to be helpful in building inclusive and financial resilience among unserved and underserved population.

Secondly, the results revealed a significant association between insurtech adoption and insurance inclusion. This finding suggests that when consumers experience ease in learning and using digital insurance platforms, they can subsequently obtain insurance digitally. Furthermore, it was revealed that when digital insurance platforms are user-friendly, clients are encouraged to use them to access insurance products and services. This finding resonates with previous studies that indicate financial technologies to have the potency to influence or foster access to financial services (Asif et al. 2023; Sahay 2020). However, such studies have been conducted mainly in the areas of fintech and financial inclusion. In line with the current study, Holliday (2019) argues that insurtech has the potential to boost economic growth by closing the protection gap from a developing country perspective. This argument is in agreement with the current study’s finding that when clients can easily buy insurance policies through digital platforms such as mobile phones, they can obtain various digital insurance products and services, hence fostering insurance inclusion. The mobile phone network has enabled emerging countries to increase access to financial services and at faster speeds (Rosyadah et al. 2021; Beck 2020). Our findings further indicated that the efficiency of digital insurance platforms encourages individuals to continue using insurance in the future and also to recommend others obtain insurance. Therefore, governments need to adopt financial technologies to proliferate financial inclusion programmes across all levels (Gautum and Kanoujiya 2022).

Thirdly, this study’s findings revealed that digital literacy has a significant positive relationship with insurtech adoption. In this regard, this finding suggests that when individuals know how to use digital devices such as smart phones, computers and other related devices, they can easily utilise insurance technologies. Insurance technologies require individuals to have the ability to navigate and evaluate digital platforms. Accordingly, someone’s digital literacy will enable them to execute insurtech tasks such as obtaining insurance products, making insurance claims and logging insurance complaints through insurtech platforms. This finding is consistent with some of the literature on the one hand and inconsistent with some of the literature on the other hand. On the one hand, this finding is in agreement with Kabakus et al. (2023), who find digital literacy to influence the adoption of technologies. They find digital literacy to be associated with perceived ease of use. Nevertheless, although we find digital literacy to influence both perceived usefulness and perceived ease of use, Kabakus et al. (2023) do not find digital literacy to influence perceived usefulness. Additionally, this study’s findings are in agreement with Mohammadyari and Singh (2015), who find digital literacy to influence intention to or not to use web 2.0 technologies. On the other hand, the current study’s findings are inconsistent with Nikou et al. (2022), who find digital literacy not to have a positive effect on technology usage in the TAM context. Notwithstanding, the current study advances that, based on the TAM context, digital literacy influences insurtech adoption.

Fourthly, this study found that insurtech adoption mediates the digital literacy and insurance inclusion relationship. In this regard, this study makes an original contribution by positing that for a client’s digital knowledge and skills to influence insurance inclusion, significant portions of their digital literacy go through insurtech adoption. Moreover, the findings revealed that digital literacy alone has a weak effect on insurance inclusion compared to its effect on insurtech adoption. Therefore, insurtech adoption mediates the relationship between digital literacy and insurance inclusion.

6. Conclusions

This study sought to establish whether digital literacy and insurtech adoption can significantly influence insurance inclusion in Uganda. Also, the study sought to establish whether insurtech adoption mediates the digital literacy and insurance inclusion nexus. With the aid of PLS-SEM, we found significant positive effects of digital literacy on insurance inclusion; insurtech adoption on insurance inclusion; and digital literacy on insurtech adoption. Furthermore, it was established that insurtech adoption mediates the digital literacy and insurance inclusion nexus. This study confirms that digital literacy and insurtech adoption can influence insurance inclusion in the TAM context. To the best of our knowledge, our study is the first to examine the mediating effect of insurtech adoption in the digital literacy and insurance inclusion nexus. Moreover, our study is the first to examine the effect of digital literacy and insurtech adoption on insurance inclusion. Previous studies have examined the influence of digital financial literacy and fintech on financial inclusion. Yet, when insurance inclusion is not addressed, attainment of full financial inclusion will remain impossible. Therefore, our study’s novelty lies in establishing how digital literacy and insurtech adoption interact to influence insurance inclusion in the Ugandan context.

The findings of this study are significant for policy makers, insurance providers and development partners alike. As such, it is recommended that in addition to tradition financial literacy programmes, policy makers should include the aspect of digital financial literacy. The Bank of Uganda should revise the national financial inclusion strategy to include a digital literacy training agenda in the framework. The current strategy focuses on financial literacy without digital literacy, meaning that plausibility of the programme may not suffice in the wake of digital financial products and services. Additionally, as insurance providers role out insurtech, they should consider extending digital insurance literacy training to enhance insurance inclusion through digital insurance platforms. Furthermore, insurance providers and insurtech start-ups should design seamless and user-friendly insurtech to encourage insurtech adoption for insurance inclusion.

Notwithstanding, this study is not without limitations. Firstly, the current study was conducted in a developing country with an underdeveloped insurance market and with low technological advancement. This may affect the generalisation of the study’s findings. Therefore, future studies could be performed from a developed economy’s perspective. Furthermore, this study was cross-sectional and quantitative. Future studies could adopt longitudinal designs with mixed-methods approaches to gather deeper insights into how digital literacy and insurtech adoption interact to influence insurance inclusion.

Author Contributions

Conceptualisation, A.K. and A.B.S.; methodology, A.K.; software, A.K.; validation, A.K. and A.B.S.; formal analysis, A.K.; investigation, A.K.; resources, A.K. and A.B.S.; data curation, A.K.; writing—original draft preparation, A.K.; writing—review and editing, A.K. and A.B.S.; visualisation, A.K. and A.B.S.; supervision, A.B.S.; project administration, A.K. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

The study was conducted in accordance with the Declaration of Helsinki. The Low risk application was reviewed by the DFRB Ethics Review Committee 17 March 2022 in compliance with the Unisa Policy on Research Ethics and the Standard Operating Procedure on Research Ethics Risk Assessment.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

Data available on request.

Conflicts of Interest

The authors declare no conflicts of interest.

Correction Statement

Due to an error by the Editorial Office, the Institutional Review Board Statement was not included in the originally published version of this article. This has now been added accordingly.

Appendix A. Study Measurement Items

| Digital Literacy | |

| Knowledge | |

| KNW1 | I know how to use digital devices such as smart phones, computers and tablets. |

| KNW2 | I am aware of the threats and risks associated with online services. |

| KNW3 | I know the importance of digital security such as having strong passwords. |

| Skills | |

| SKL1 | I can ably navigate and search for information on the internet |

| SKL2 | I can ably evaluate the credibility of online information |

| Insurtech adoption | |

| Perceived ease of use | |

| PEU1 | I find digital insurance platforms easy to use. |

| PEU2 | I easily learn to use digital insurance platforms. |

| PEU3 | I am confident when using digital insurance platforms. |

| PEU4 | The interface of the digital insurance platform is friendly. |

| PEU5 | I easily learned how to use the digital insurance platform. |

| Perceived Usefulness | |

| PUS1 | The digital insurance platform made purchasing insurance easy. |

| PUS2 | I easily monitor my insurance policy on the digital insurance platform. |

| PUS3 | Digital insurance has made the insurance process efficient. |

| PUS4 | The digital platform has increased the transparency of the insurance provider. |

| PUS5 | Overall, the digital insurance platform has improved my experience with the insurance provider. |

| Insurance inclusion | |

| Access | |

| ACS1 | Digital insurance platforms provide convenient access to insurance products and services. |

| Usage | |

| USG1 | I intend to continue using digital insurance services. |

| USG2 | I would recommend others to buy insurance using digital platforms. |

| USG3 | The digital insurance platform has a wide variety of insurance products and services. |

| USG5 | I feel good about my decision to buy insurance through a digital platform. |

References

- Ajzen, Icek, and Martin Fishbein. 2000. Attitudes and the attitude-behaviour relation: Reasoned and automatic processes. European Review of Social Psychology 11: 1–33. [Google Scholar] [CrossRef]

- Asif, Mohammad, Mohd Naved Khan, Sadhana Tiwari, Showkat K. Wani, and Firoz Alam. 2023. The impact of fintech and digital financial services on financial inclusion in India. Journal of Risk and Financial Management 16: 122. [Google Scholar] [CrossRef]

- Asongu, Simplice A., and Nicholous M. Odhiambo. 2020. Insurance policy thresholds for economic growth in Africa. European Journal of Development Research 32: 672–89. [Google Scholar] [CrossRef]

- Bayar, Yilmaz, Marius Dan Gavriletea, and Dan Constantine Danuletiu. 2021. Does the insurance sector really matter for economic growth? Evidence from Central and Eastern European countries. Journal of Business Economics and Management 22: 695–713. [Google Scholar] [CrossRef]

- Beck, Thorsten. 2020. Fintech and Financial Inclusion: Opportunities and Pitfalls. Retrieved from Social Science Premium Collection. Tokyo: Asian Development Bank Institute. Available online: https://search.proquest.com/docview/2487312988 (accessed on 11 September 2023).

- Bittini, Javier Sada, Salvador Cruz Rambaud, Joaquin Lopez Pascual, and Roberto Moro-Visconti. 2022. Business models and sustainability plans in the FinTech, Insurtech, and PropTech industry: Evidence from Spain. Sustainability 14: 12088. [Google Scholar] [CrossRef]

- Chan, Rebecca, Indrit Troshani, Sally Rao Hill, and Arvid Hoffmann. 2022. Towards an understanding of consumers’ FinTech adoption: The case of open banking. International Journal of Bank Marketing 40: 886–917. [Google Scholar] [CrossRef]

- Cheston, Susy, Sonja Kelly, Allyse McGrawth, Conan French, and Dennis Ferenzy. 2018. Insurance Inclusion: Closing the Protection Gap for Emerging Customers. Washington, DC: Center for Financial Inclusion. [Google Scholar]

- Davis, D. Fred. 1989. Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly 13: 319–40. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, Leora Klapper, Dorothe Singer, and Saniyar Ansar. 2022. The Global Findex Database 2021. Chicago: World Bank Publications. [Google Scholar] [CrossRef]

- Demirgüç-Kunt, Asli, Leora Klapper, Dorothe Singer, Saniyar Ansar, and Jake Hess. 2018. The Global Findex Database 2017, 1st ed. Washington, DC: World Bank Publications. [Google Scholar] [CrossRef]

- Elkaseh, Ali Mohamed, Kok Wai Wong, and Chun Che Fung. 2016. Perceived ease of use and perceived usefulness of social media for e-learning in Libyan higher education: A structural equation modelling analysis. International Journal of Information and Education Technology 6: 192–99. [Google Scholar] [CrossRef]

- Finscope. 2018. Finscope Survey: Top Line Findings Summary Report. Kampala: Financial Sector Deepening Uganda. [Google Scholar]

- Gautum, Rahul Singh, and Jagjeevan Kanoujiya. 2022. Role of regional rural banks in rural development and its influences on digital literacy in India. IRE Journals 5: 92–101. [Google Scholar]

- Gie, Tung An, and Chung Jee Fenn. 2019. Technology acceptance model and digital literacy of first-year students in a private institution of higher learning in Malaysia. Berjaya Journal of Services & Management 11: 103–16. [Google Scholar]

- Hair, Joseph F., William C. Black, Barry J. Babin, and Rolph E. Anderson. 2019. Multivariate Data Analysis, 8th ed. Boston: Cengage Learning, EMEA. [Google Scholar]

- Hassan, Rashedul, Muhammad Ashfaq, Tamiza Parveen, and Ardi Gunardi. 2022. Financial inclusion—Does digital financial literacy matter for women entrepreneurs. International Journal of Social Economics 20: 1085–104. [Google Scholar] [CrossRef]

- Holliday, Susan. 2019. How Insurtech Can Close the Protection Gap in Emerging Markets. Washington, DC: International Finance Corporation. Available online: http://hdl.handle.net/10986/32366 (accessed on 5 June 2023).

- Insurance Regulatory Authority. 2022. Annual Insurance Market Report. Kampala: Insurance Regulatory Authority. [Google Scholar]

- International Association of Insurance Supervisors. 2022. IAIS Global Insurance Market Report 2022 Highlights Key Risks and Trends Facing the Global Insurance Sector. Targeted News Service. Available online: https://search.proquest.com/docview/2754850078 (accessed on 16 December 2022).

- Jang, Monkyoung, Milla Aavakare, Shahrokh Nikou, and Seongcheol Kim. 2021. The impact of literacy on intention to use digital technology for learning: A comparative study of Korea and Finland. Telecommunications Policy 45: 102154. [Google Scholar] [CrossRef]

- Kabakus, Ahmet Kamil, Ekrem Bahcekapili, and Ahmet Ayaz. 2023. The effect of digital literacy on technology acceptance: An evaluation on administrative staff in higher education. Journal of Information Science. [Google Scholar] [CrossRef]

- Kanga, Desire, Christine Oughton, Laurence Harris, and Victor Murinde. 2022. The diffusion of fintech, financial inclusion and income per capita. The European Journal of Finance 28: 108–36. [Google Scholar] [CrossRef]

- Kass-Hanna, Josephine, Angella C. Lyons, and Fan Liu. 2022. Building financial resilience through financial and digital literacy in south Asia and sub-Saharan Africa. Emerging Markets Review 51: 100846. [Google Scholar] [CrossRef]

- Kim, Minjin, Hanan Zoo, Heejin Lee, and Juhee Kang. 2018. Mobile financial services, financial inclusion, and development: A systematic review of academic literature. The Electronic Journal of Information Systems in Developing Countries 84: e12044. [Google Scholar] [CrossRef]

- Kiwanuka, Archillies, and Atheni Bongani Sibindi. 2023. Insurance inclusion in Uganda: Impact of perceived value, insurance literacy and perceived trust. Journal of Risk and Financial Management 16: 81. [Google Scholar] [CrossRef]

- Lin, Lin, and Christopher Chen. 2020. The promise and perils of Insurtech. Singapore Journal of Legal Studies 2020: 115–42. [Google Scholar] [CrossRef]

- Lyons, Angela C., and Josephine Kass-Hanna. 2021. A methodological overview to defining and measuring “digital” financial literacy. Financial Planning Review 4: e1113. [Google Scholar] [CrossRef]

- Lyons, Angela C., Josephine Kass-Hanna, and Andrew Greenlee. 2020. Impacts of Financial and Digital Inclusion on Poverty in South Asia and Sub-Saharan Africa. SSRN. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3684265 (accessed on 11 November 2023). [CrossRef]

- Mikheev, Alexey, Yana Serkina, and Alexander Vasyaev. 2023. Current trends in the digital transformation of higher education institutions in Russia. Education and Information Technologies 26: 4537–51. [Google Scholar] [CrossRef]

- Moenjak, Thammarak, Anyarat Kongprajya, and Chompoonoot Monchaitrakul. 2020. FinTech, Financial Literacy, and Consumer Saving and Borrowing: The Case of Thailand. Retrieved from Social Science Premium Collection. Tokyo: Asian Development Bank Institute. Available online: https://search.proquest.com/docview/2423771629 (accessed on 7 October 2023).

- Mohammadyari, Soheila, and Harminder Singh. 2015. Understanding the effect of e-learning on individual performance: The role of digital literacy. Computers and Education 82: 11–25. [Google Scholar] [CrossRef]

- Morgan, Peter, Long Trinh, and Bihong Huang. 2019. The Need to Promote Digital Financial Literacy for the Digital Age. Washington, DC: International Monetary Fund. [Google Scholar]

- Nikou, Shahrokh, and Milla Aavakare. 2021. An assessment of the interplay between literacy and digital technology in higher education. Education and Information Technologies 26: 3893–915. [Google Scholar] [CrossRef]

- Nikou, Shahrokh, Mark De Reuver, and Matin Mahboob Kanafi. 2022. Workplace literacy skills—How information and digital literacy affect adoption of digital technology. Journal of Documentation 78: 371–91. [Google Scholar] [CrossRef]

- Prasad, Hanuma, Devendra Meghwal, and Vijay Dayama. 2018. Digital financial literacy: A study of households of Udaipur. Journal of Business and Management 5: 23–32. [Google Scholar] [CrossRef]

- Rahayu, Ritah, Syahril Ali, Amalda Aulia, and Retnoningrum Hidayah. 2022. The current digital financial literacy and financial behaviour in Indonesian millennial generation. Journal of Accounting and Investment 23: 78–94. [Google Scholar] [CrossRef]

- Reddy, Pritika, Bibhya Sharma, and Kaylash Chaudhary. 2020. Digital literacy: A review of literature. International Journal of Techno Ethics 11: 65–94. [Google Scholar] [CrossRef]

- Rosyadah, Khairina, Budiandriani Budiandriani, and Tasrik Hasrat. 2021. The role of fintech: Financial inclusion in MSMEs (case study in Makassar city). Jurnal Manajemen Bisnis 8: 268–75. [Google Scholar] [CrossRef]

- Sahay, Ratna. 2020. The Promise of Fintech. Washington, DC: International Monetary Fund. [Google Scholar]

- Setiawan, Maman, Nury Effendi, Teguh Santoso, Vera Intanie Dewi, and Militcyano Samuel Sapulette. 2022. Digital financial literacy, current behavior of saving and spending and its future foresight. Economics of Innovation and New Technology 31: 320–38. [Google Scholar] [CrossRef]

- Sibindi, Athenia Bongani. 2022. Information and communication technology adoption and life insurance market development: Evidence from Sub-Saharan Africa. Journal of Risk and Financial Management 15: 568. [Google Scholar] [CrossRef]

- Van der Cruijsen, Carin, Jacob de Haan, and Ria Roerink. 2021. Financial knowledge and trust in financial institutions. Journal of Consumer Affairs 55: 680–714. [Google Scholar] [CrossRef]

- Wang, Qing, Chengjun Liu, and Sai Lan. 2022. Digital literacy and financial market participation of middle-aged and elderly adults in China. Economic and Political Studies, 1–28, ahead-of-print. [Google Scholar]

- Yamane, Tarro. 1973. Statistics, 3. ed., 1. print. ed. Manhattan: Harper & Row. [Google Scholar]

- Zulfiqar, Umera, Sajid MohY-Ul-Din, Ayman Abu-Rumman, Ata E. M. Al-Shraah, and Israr Ahmed. 2020. Insurance-growth nexus: Aggregation and disaggregation. The Journal of Asian Finance, Economics, and Business 7: 665–75. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).