Sovereign Credit Risk in Saudi Arabia, Morocco and Egypt

Abstract

:1. Introduction

2. Previous Research

3. Data Description and Methodology

3.1. Data Description

3.2. Methodology

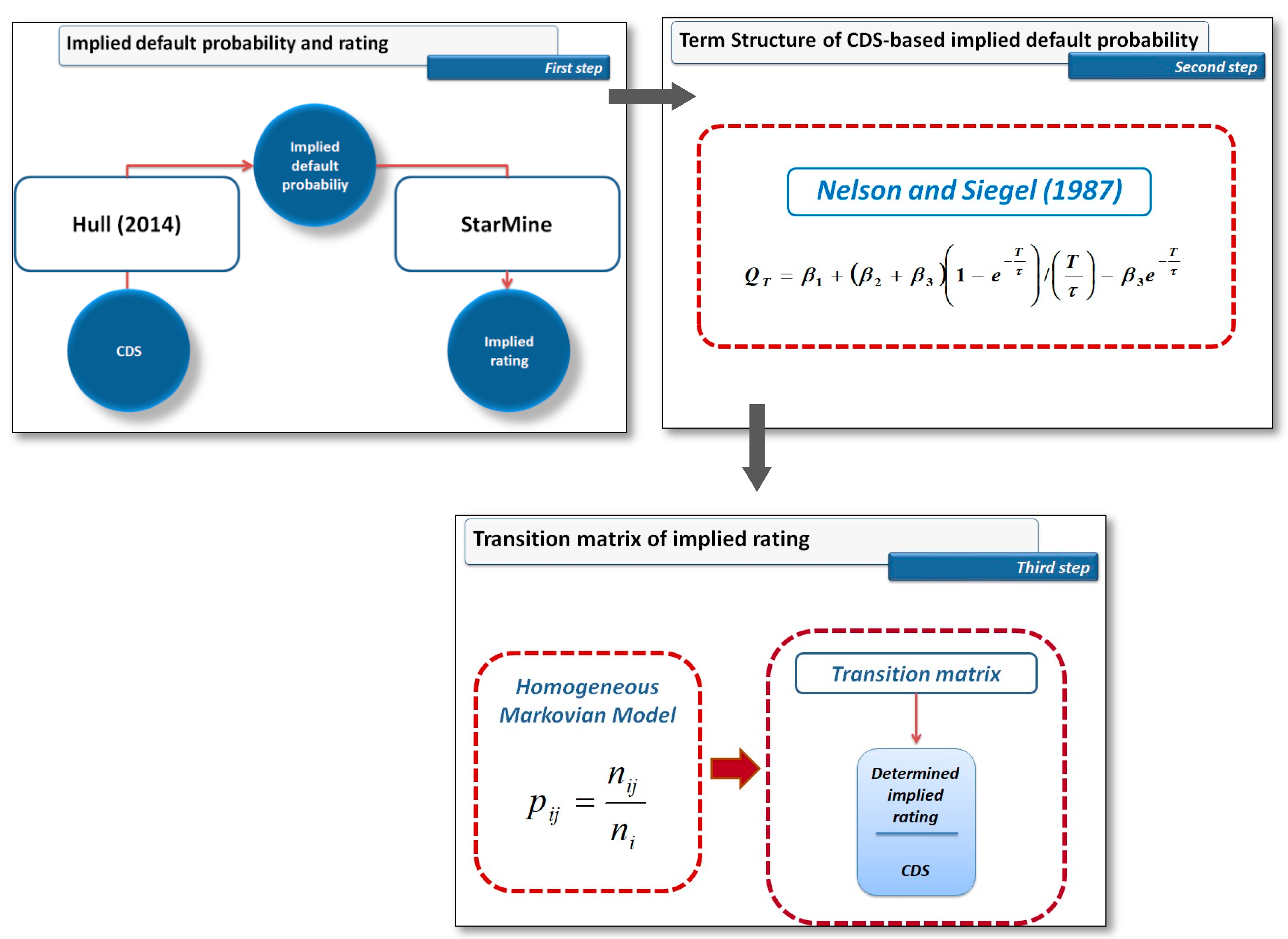

3.2.1. CDS-Based Implied Default Probability and Rating

3.2.2. Term Structure of CDS-Based Implied Default Probability

3.2.3. Transition Matrix of CDS-Based Implied Rating

4. Results Analysis

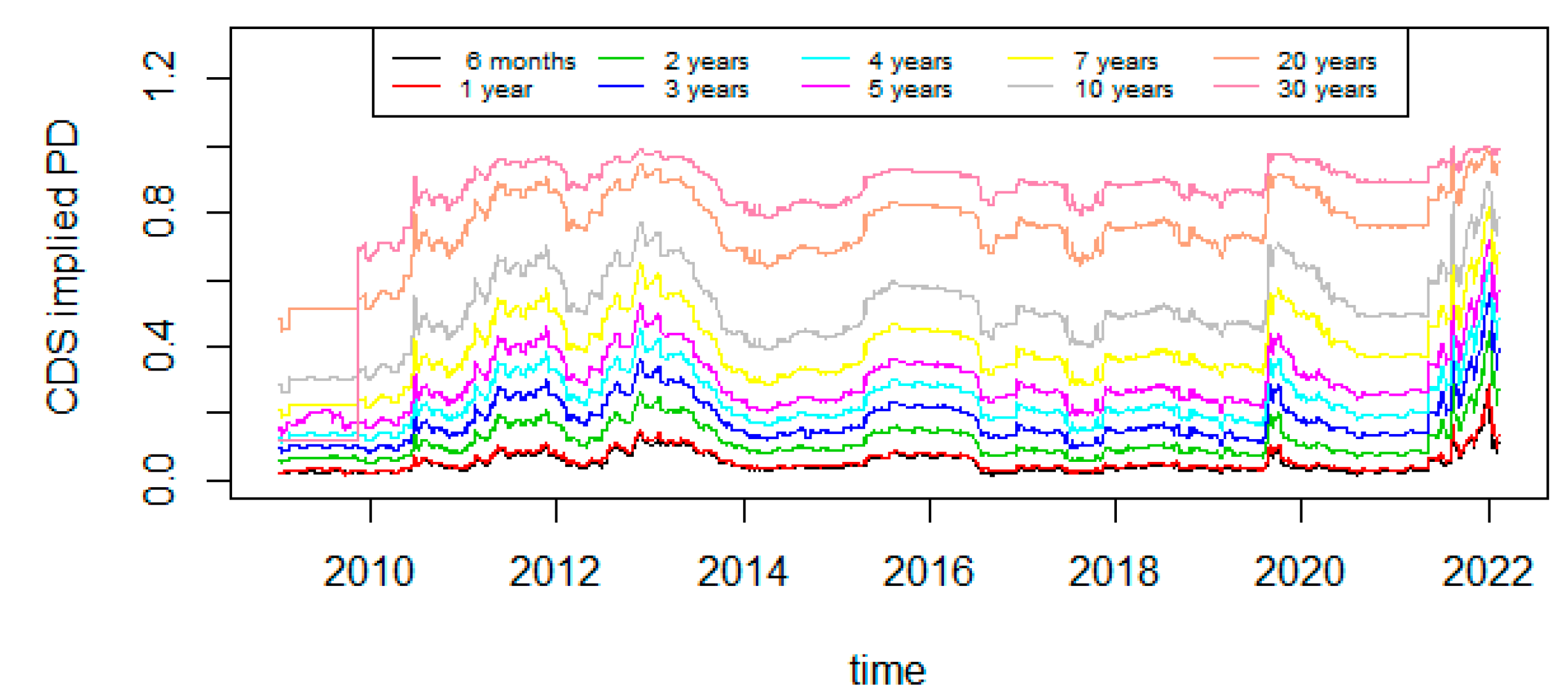

4.1. Implied Default Probability and Implied Rating Results

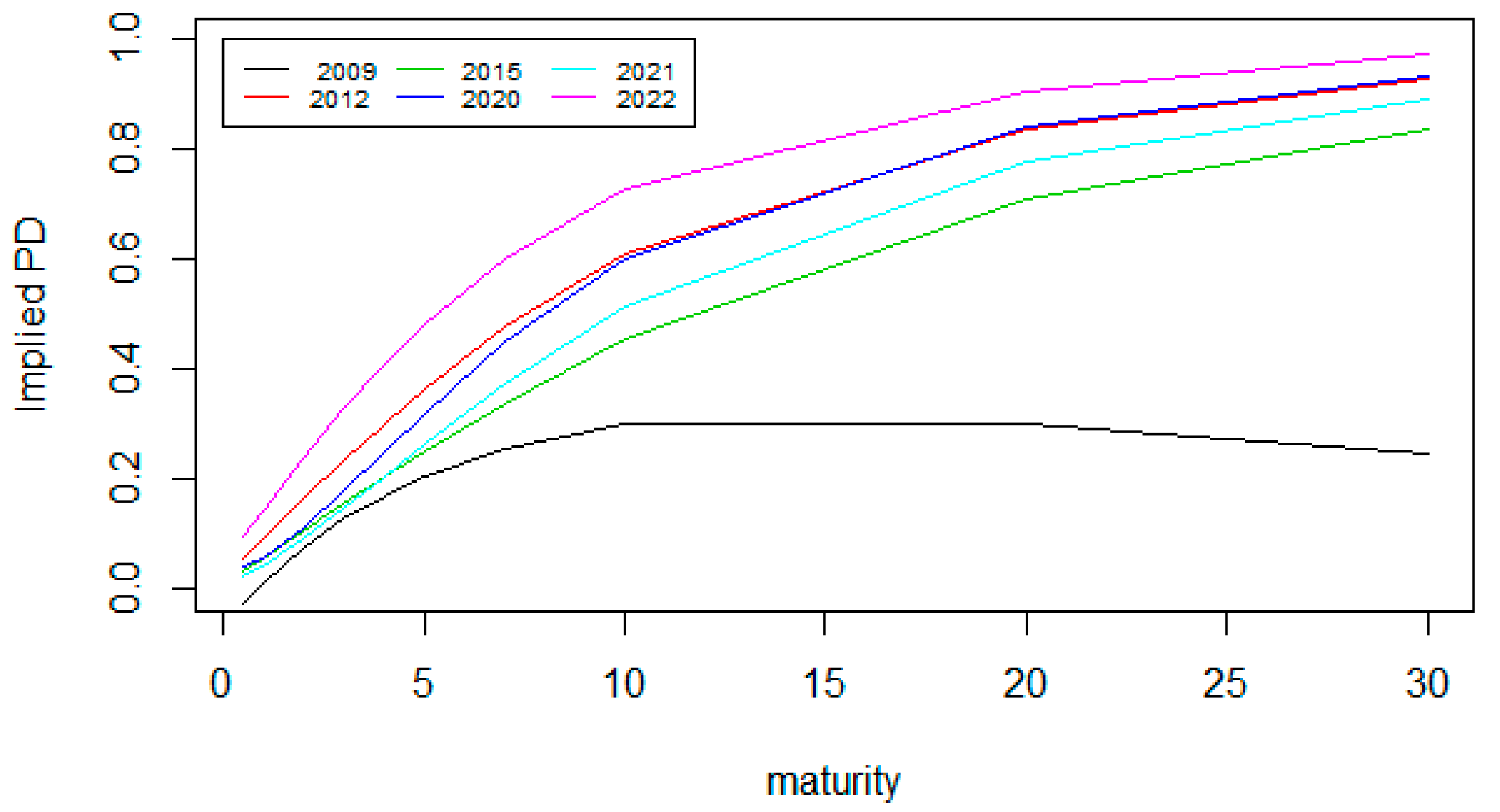

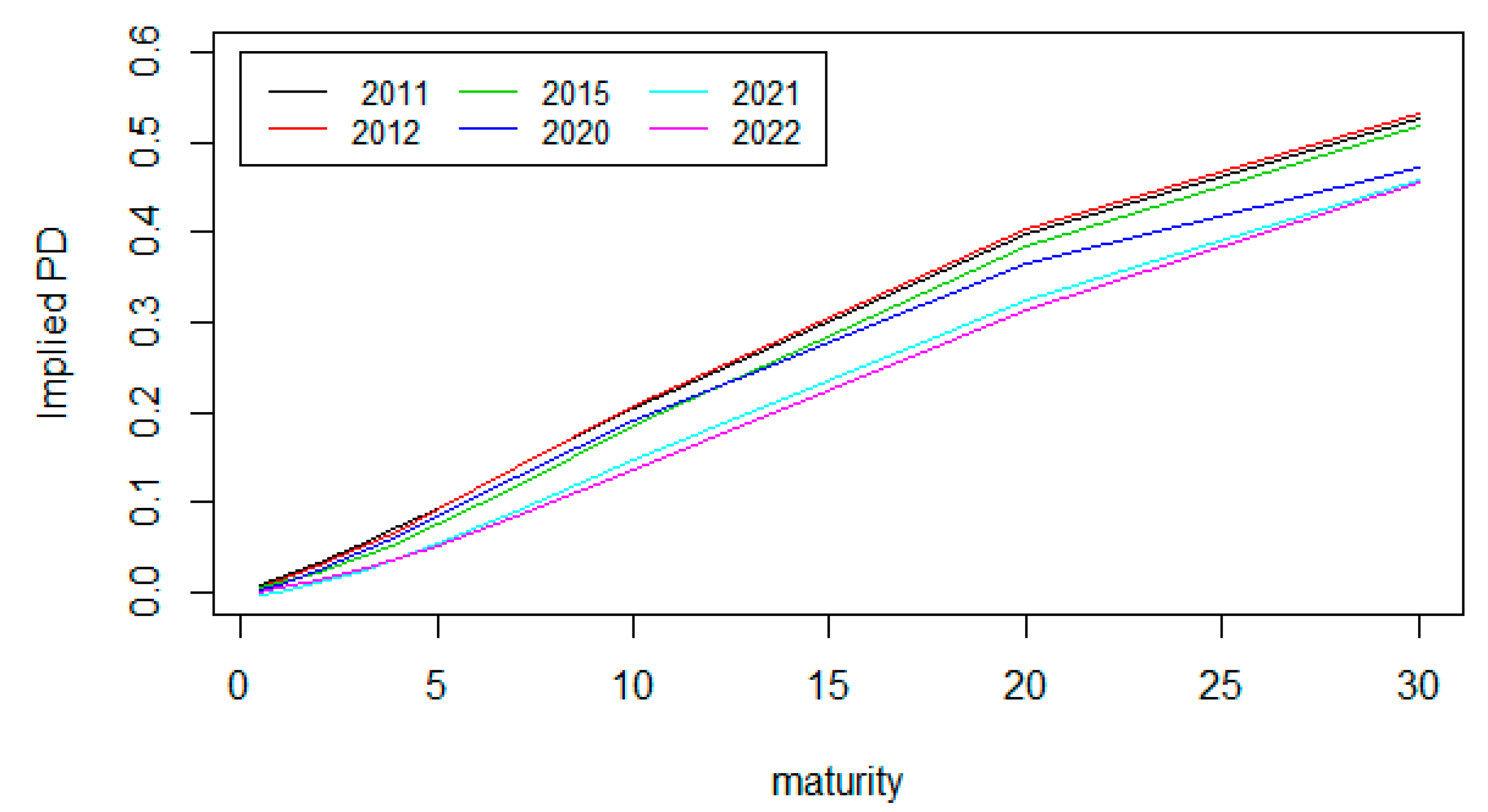

4.2. Term Structure Results

4.3. Rating Transition Matrix Results

5. Conclusions and Creditworthiness Implications

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Abid, Amira, and Abid Fathi. 2023. A methodology to estimate the optimal debt ratio when asset returns, and default probability follow stochastic processes. Journal of Industrial and Management Optimization 19: 7735–52. [Google Scholar] [CrossRef]

- Abid, Amira, Abid Fathi, and Kaffel Bilel. 2020. CDS-based implied probability of default estimation. The Journal of Risk Finance, ahead-of-print. [Google Scholar] [CrossRef]

- Annaert, Jan, Anouk G. P. Claes, Mark J. K. De Ceuster, and Hairui Zhang. 2013. Estimating the spot rate curve using the Nelson-Siegel model: A ridge regression approach. International Review of Economics and Finance 27: 482–96. [Google Scholar] [CrossRef]

- Annaert, Jan, and Marc Ceuster. 2000. Modelling European Credit Spreads, 3rd ed. Prinsstraat: Universiteit Antwerpen. [Google Scholar]

- Augustin, Patrick, Valeri Sokolovski, Marti G. Subrahmanyam, and Davide Tomio. 2022. How sovereign is sovereign credit risk? Global prices, local quantities. Journal of Monetary Economics 131: 92–111. [Google Scholar] [CrossRef]

- Badr, Osama M., and Ahmed F. El-khadrawi. 2016. Macroeconomic Variables, Government Effectiveness and Sovereign Credit Rating: A Case of Egypt. Applied Economics and Finance 3: 29–36. [Google Scholar] [CrossRef]

- Baranovski, Alexander, Carsten von Lieres und Wilkau, and André Wilch. 2009. New Recipes for Estimating Default Intensities. Discussion Paper 2009-004, Eurobanking SFB 649. Berlin: Humboldt University of Berlin, Collaborative Research Center 649. [Google Scholar]

- Barry, Ibrahim. 2022. Arabie saoudite-situation économique et financière en 2022. Riyad: Ambassade de France en Arabie Saudite—Service économique de Riyad. [Google Scholar]

- Ben Hassen, T. 2022. The GCC Economies in the Wake of COVID-19: Toward Post-Oil Sustainable Knowledge-Based Economies? Sustainability 14: 11251. [Google Scholar] [CrossRef]

- Blair, David. 2013. Counterparty Credit Risk. In Financial Derivatives. Working Paper. Hoboken: John Wiley & Sons, Inc. [Google Scholar] [CrossRef]

- Blümke, Oliver. 2018. A Markov Chain Approximation of Transition Matrices with Applications to Credit Ratings. SSRN Electronic Journal. Available online: https://ssrn.com/abstract=3124116 (accessed on 10 May 2024). [CrossRef]

- Boumahdi, Mohamed Amine. 2022. Fiche Pays Egypte; Paris: Ministère de l’Economie des Finaces et de la Souvraineté Industrielle et Numérique, Service Economique du Caire, Direction Générale du Trésort.

- Caldeira, João F., Guilherme V. Moura, André AP Santos, and Fabricio Tourrucôo. 2016. Forecasting the yield curve with the Arbitrage-Free dynamic Nelson–Siegel model: Brazilian evidence. EconomiA 17: 221–37. [Google Scholar] [CrossRef]

- Christensen, Jens H. E., Ernst Hansen, and David Lando. 2004. Confidence sets for continuous-time rating transition probabilities. Journal of Banking and Finance 28: 2575–602. [Google Scholar] [CrossRef]

- Cizel, Janko. 2013. Are credit rating announcements contagious? Evidence on the transmission of information across industries in credit default swap markets. The Journal of Fixed Income 23: 27–60. [Google Scholar] [CrossRef]

- Diebold, Francis X., and Canlin Li. 2006. Forecasting the term structure of government bond yields. Journal of Econometrics 130: 337–64. [Google Scholar] [CrossRef]

- Dwyer, Douglas, Zan Li, Shisheng Qu, Heather Russell, and Jing Zhang. 2010. CDS-Implied EDF TM credit measures and Fair-Value spreads. Moody’s Analytics, 1–43. [Google Scholar] [CrossRef]

- El-Bassiouny, Dina, and Peter Letmathe. 2020. Political instability and corporate social responsibility: The case of Egypt. Social Responsibility Journal 16: 745–67. [Google Scholar] [CrossRef]

- Engelmann, Bernd, and Konstantin Ermakov. 2011. Transition matrices: Properties and estimation methods. In The Basel II Risk Parameters: Estimation, Validation, Stress Testing-with Applications to Loan Risk Management. Berlin/Heidelberg: Springer, pp. 103–16. [Google Scholar]

- Flannery, Mark J., Joel F. Houston, and Frank Partnoy. 2010. Credit default swap spreads as viable substitutes for credit ratings. University of Pennsylvania Law Review 158: 2085–123. [Google Scholar]

- Frydman, Halina, and Til Schuermann. 2008. Credit rating dynamics and Markov mixture models. Journal of Banking and Finance 32: 1062–75. [Google Scholar] [CrossRef]

- Gavalas, Dimitris, and Theodore Syriopoulos. 2014. Bank credit risk management and rating migration analysis on the business cycle. International Journal of Financial Studies 2: 122–43. [Google Scholar] [CrossRef]

- Hilscher, Jens, and Mungo Wilson. 2017. Credit ratings and credit risk: Is one measure enough? Management Science 63: 3414–37. [Google Scholar] [CrossRef]

- Hua, Jian. 2015. Term structure modeling and forecasting using the Nelson-Siegel model. In Handbook of Financial Econometrics and Statistics. Greer: Springer, pp. 1093–103. [Google Scholar]

- Hull, John C. 2014. Options, Futures and Other Derivatives, Pearson. London: Pearson. [Google Scholar]

- Hull, John C., and Alan White. 2000. Valuing credit default swaps I: No counterparty default risk. The Journal of Derivatives 8: 29–40. [Google Scholar] [CrossRef]

- Hull, John C., Mirela Predescu, and Alan White. 2004. The relationship between credit default swap spreads, bond yields, and credit rating announcements. Journal of Banking and Finance 28: 2789–811. [Google Scholar] [CrossRef]

- Hung, Chi-Hsiou, Banerjee Anuarg, and Meng Qingrui. 2017. Corporate financing and anticipated credit rating changes. Review of Quantitative Finance and Accounting 48: 893–915. [Google Scholar] [CrossRef]

- International Monetary Fund. 2013. Chapter 2: A New Look at the Role of Sovereign Credit Default Swaps. Global Financial Stability Report. Washington, DC: IMF, pp. 57–92. [Google Scholar]

- Jacobs, Michael, Jr., Ahmet K. Karagozoglu, and Dina Naples Layish. 2016. Credit risk signals in CDS market vs agency ratings. The Journal of Risk Finance 17: 194–217. [Google Scholar] [CrossRef]

- Jarrow, Robert A. 2001. Default parameter estimation using market prices. Financial Analysts Journal 57: 75–92. [Google Scholar] [CrossRef]

- Jarrow, Robert A., David Lando, and Stuart M. Turnbull. 1997. A Markov model for the term structure of credit risk spreads. Review of Financial Studies 10: 481–523. [Google Scholar] [CrossRef]

- Jones, Matthew T. 2005. Estimating Markov Transition Matrices Using Proportions Data: An Application to Credit Risk. IMF Working Paper. pp. 1–27. Available online: https://ssrn.com/abstract=888088 (accessed on 10 May 2024). [CrossRef]

- Lando, David. 2010. Rating transition matrices. In Encyclopedia of Quantitative Finance. Hoboken: John Wiley and Sons. [Google Scholar]

- Lazrak, Mohammed. 2023. Moroccan-African Religious Diplomacy: Prospects and Challenges. International Journal of Religious and Cultural Studies 5: 75–86. [Google Scholar] [CrossRef]

- Liu, Lily Y. 2017. Estimating Loss Given Default from CDS under Weak Identification. Risk and Policy Analysis Unit Paper RPA 17-1, Federal Reserve Bank of Boston. Available online: https://ssrn.com/abstract=3033354 (accessed on 10 May 2024).

- Longstaff, Francis A., Lasse H. Pedersen Jun Pan, and Kenneth J. Singleton. 2011. How Sovereign Is Sovereign Credit Risk? American Economic Journal: Macroeconomics 3: 75–103. [Google Scholar] [CrossRef]

- Maher, Mohamed, and Yanzhi Zhao. 2021. Do Political Instability and Military Expenditure Undermine Economic Growth in Egypt? Evidence from the ARDL Approach. Defence and Peace Economics 33: 956–79. [Google Scholar] [CrossRef]

- Malik, Madhur, and Lyn C. Thomas. 2012. Transition matrix models of consumer credit ratings. International Journal of Forecasting 28: 261–72. [Google Scholar] [CrossRef]

- Merton, Robert C. 1974. On the pricing of corporate debt: The risk structure of interest rates. The Journal of Finance 29: 449–70. [Google Scholar]

- Muvingi, Jacob, and Takudza Kwinjo. 2014. Estimation of term structures using Nelson- Siegel and Nelson-Siegel-Svensson: A case of a Zimbabwean bank. Journal of Applied Finance and Banking 4: 155–90. [Google Scholar]

- Nelson, Charles R., and Andrew F. Siegel. 1987. Parsimonious modeling of yield curves. The Journal of Business 60: 473–89. [Google Scholar] [CrossRef]

- Oldenburg, Michel, Anais Boitiere, Sarah Jiquel, Mohamed Amin Boumahdi, and Antoine Cosson. 2022. La Lettre Economique d’Egypte. Caire: Ambassade de France en Republique Arabe d’Egypte—Service économique du Caire. [Google Scholar]

- Paret, Anne Charlotte, and Gilles Dufrénot. 2015. Sovereign Default in Emerging Market Countries: A Transition Model Allowing for Heterogeneity. Amundi Asset Management Working Paper, WP-049-2015. Paris: Amundi Asset Management. [Google Scholar]

- Piccolo, Alessio, and Joel Shapiro. 2022. Credit Ratings and Market Information. The Review of Financial Studies 35: 4425–73. [Google Scholar] [CrossRef]

- Rodríguez, Ivan M., Krishnan Dandapani, and Edward R. Lawrence. 2019. Measuring sovereign risk: Are CDS spreads better than sovereign credit ratings? Financial Management 48: 229–56. [Google Scholar] [CrossRef]

- Thornary, Baptiste, Anne Sophie Fèvre, Adriana Meyer, Victor Lequillerier, Sabrina El Kasmi, Laetitia Morin, and Thomas Laboureau. 2022a. Direction de l’évaluation des études et de la prospective—Fiche Maroc. Maisons-Alfort: Bpifrance. [Google Scholar]

- Thornary, Baptiste, Anne Sophie Fèvre, Adriana Meyer, Victor Lequillerier, Sabrina El Kasmi, Laetitia Morin, and Thomas Laboureau. 2022b. Direction de l’évaluation des études et de la prospective—Fiche pays Arabi Saudite. Maisons-Alfort: Bpifrance. [Google Scholar]

- Tourabi, Abdellah, and Lamia Zaki. 2011. Maroc: Une révolution royale? Mouvements 2: 98–103. Available online: https://www.cairn.info/revue-mouvements-2011-2-page-98.htm (accessed on 10 May 2024).

- Vieira, Maria, and George Bonne. 2016. Starmine Sovereign Risk Model. Refinitiv, RE105787/12-19. Available online: https://solutions.refinitiv.com/StarMineNAsia-Whitepapers (accessed on 10 May 2024).

- Zhu, Haibin. 2006. An Empirical Comparison of Credit Spreads between the Bond Market and the Credit Default Swap Market. Journal of Financial Services Research 29: 211–35. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Egypt | ||||||||||

| Maturity | 0.5 | 1 | 2 | 3 | 4 | 5 | 7 | 10 | 20 | 30 |

| Min | 80 | 90 | 147 | 167 | 175 | 162 | 175 | 176 | 175 | 25 |

| Mean | 264.3 | 298.8 | 345.8 | 375.2 | 394.9 | 413.6 | 430.6 | 440.5 | 447.9 | 440.3 |

| Max | 1608.8 | 1458.5 | 1390.1 | 1309.6 | 1492.8 | 1458.5 | 1390.1 | 1309.6 | 1290.0 | 1284.4 |

| Sd | 170.2483 | 177.1297 | 176.8832 | 172.1435 | 168.1435 | 164.1476 | 161.9315 | 157.1423 | 153.7284 | 175.2815 |

| Morocco | ||||||||||

| Maturity | 0.5 | 1 | 2 | 3 | 4 | 5 | 7 | 10 | 20 | 30 |

| Min | 0.77 | 9.90 | 27.99 | 43.44 | 61.62 | 79.82 | 98.55 | 104.2 | 99.71 | 93.45 |

| Mean | 81.05 | 94.37 | 116.12 | 133.45 | 151.01 | 165.38 | 179.50 | 189.8 | 197.03 | 199.68 |

| Max | 259.14 | 265.00 | 276.58 | 304.54 | 327.72 | 335.00 | 335.00 | 339.4 | 353.23 | 361.41 |

| Sd | 48.31051 | 49.06547 | 50.05776 | 52.24454 | 53.44148 | 54.20382 | 53.30555 | 54.69647 | 56.10721 | 56.69838 |

| Saudi Arabia | ||||||||||

| Maturity | 0.5 | 1 | 2 | 3 | 4 | 5 | 7 | 10 | 20 | 30 |

| Min | 1.03 | 0.34 | 11.16 | 15.66 | 28.74 | 43.30 | 61.31 | 77.38 | 81.49 | 76.3 |

| Mean | 29.66 | 35.08 | 46.27 | 59.15 | 74.42 | 89.92 | 111.94 | 126.76 | 140.11 | 146.2 |

| Max | 184.79 | 188.61 | 196.79 | 206.42 | 218.29 | 232.39 | 253.67 | 265.42 | 277.61 | 286.7 |

| Sd | 28.80631 | 30.56741 | 31.73342 | 32.14856 | 32.67511 | 33.57039 | 32.5189 | 31.82552 | 34.19131 | 35.4292 |

| If the One-Year PD (%) Is Greater Than | And the One-Year PD (%) Is Less Than or Equal to | Then the Rating Is |

|---|---|---|

| 0.000% | 0.123% | AAA |

| 0.123% | 0.332% | AA |

| 0.332% | 0.851% | A |

| 0.851% | 1.879% | BBB |

| 1.879% | 4.107% | BB |

| 4.107% | 12.052% | B |

| 12.052% | 20.973% | CCC |

| 20.973% | 100.0% | CC |

| Years | Egypt | Morocco | Saudi Arabia |

|---|---|---|---|

| 2009 | BB | BB | - |

| 2010 | BB | BBB | - |

| 2011 | B | BB | BBB |

| 2012 | B | BB | BBB |

| 2013 | B | BB | AA |

| 2014 | B | BB | AA |

| 2015 | B | BB | BBB |

| 2016 | B | BB | BBB |

| 2017 | BB | BBB | AA |

| 2018 | BB | BBB | A |

| 2019 | B | BBB | A |

| 2020 | B | A | BBB |

| 2021 | BB | BBB | AA |

| 2022 | CCC | BBB | A |

| Rating Code | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

|---|---|---|---|---|---|---|---|---|

| CDS-based implied rating | AAA | AA | A | BBB | BB | B | CCC | CC |

| Date | (p-Value) | (p-Value) | (p-Value) | |

|---|---|---|---|---|

| 2009 | 0.01646 (0.9459) | −0.08428 (0.6952) | 1.12635 (0.0885) | 0.1379506 |

| 2012 | 1.111116 (1.22 × 10−12) * | −1.087499 (2.08 × 10−12) * | −0.705117 (1.79 × 10−7) * | 0.3260436 |

| 2015 | 1.130770 (9.05 × 10−13) * | −1.124164 (4.57 × 10−13) * | −0.642330 (7.22 × 10−8) * | 0.1992737 |

| 2020 | 1.114850 (9.26 × 10−15) * | −1.081379 (3.36 × 10−14) * | −1.095824 (1.22 × 10−10) * | 0.3985108 |

| 2021 | 1.122746 (5.96 × 10−13) * | −1.116183 (7.06 × 10−13) * | −0.950938 (9.33 × 10−9) * | 0.298877 |

| 2022 | 1.100861 (9.88 × 10−13) * | −1.045899 (6.55 × 10−12) * | −0.688646 (4.26 × 10−7) * | 0.4483072 |

| Date | (p-Value) | (p-Value) | (p-Value) | |

|---|---|---|---|---|

| 2009 | 1.03071 (1.39 × 10−10) * | −1.02755 (6.27 × 10−11) * | −0.45770 (1.08 × 10−5) * | 0.1195632 |

| 2012 | 1.081930 (1.94 × 10−12) * | −1.078795 (9.02 × 10−13) * | −0.768440 (2.79 × 10−8) * | 0.1887807 |

| 2015 | 0.93849 (5.07 × 10−11) * | −0.92918 (2.25 × 10−11) * | −0.58453 (1.11 × 10−6) * | 0.1630265 |

| 2020 | 0.92524 (5.84 × 10−11) * | −0.91462 (2.68 × 10−11) * | −0.60202 (1.09 × 10−6) * | 0.1707952 |

| 2021 | 0.95609 (1.27 × 10−11) * | −0.95872 (5.10 × 10−12) * | −0.75129 (4.37 × 10−8) * | 0.1494588 |

| 2022 | 1.01311 (1.90 × 10−11) * | −1.01986 (7.44 × 10−12) * | −0.69407 (1.68 × 10−7) * | 0.1494588 |

| Date | (p-Value) | (p-Value) | (p-Value) | |

|---|---|---|---|---|

| 2011 | 0.898359 (9.37 × 10−12) * | −0.897360 (3.91 × 10−12) * | −0.708039 (2.44 × 10−8) * | 0.1379506 |

| 2012 | 0.866858 (8.90 × 10−12) * | −0.863565 (3.74 × 10−12) * | −0.718352 (2.12 × 10−8) * | 0.1494588 |

| 2015 | 0.881929 (3.40 × 10−1) * | −0.879378 (1.42 × 10−12) * | −0.812071 (3.91 × 10−9) * | 0.1494588 |

| 2020 | 0.74595 (4.64 × 10−10) * | −0.74943 (1.87 × 10−10) * | −0.62122 (1.33 × 10−6) * | 0.1630265 |

| 2021 | 0.86406 (8.33 × 10−10) * | −0.87079 (3.37 × 10−10) * | −0.79250 (5.67 × 10−7) * | 0.1280884 |

| 2022 | 0.98457 (1.83 × 10−10) * | −0.98722 (8.68 × 10−11) * | −0.88249 (7.82 × 10−8) * | 0.1055055 |

| Implied Rating | BB | B | CCC |

|---|---|---|---|

| BB | 0.3113525 (0.02560048 *) (0.2692434 **) (0.3534615 ***) | 0.4971895 (0.03173144 *) (0.4449959 **) (0.5493831 ***) | 0.1914580 (0.02351212 *) (0.1527840 **) (0.2301320 ***) |

| B | 0.2542111 (0.01719046 *) (0.2259354 **) (0.2824869 ***) | 0.7457889 (0.01719046 *) (0.7175131 **) (0.7740646 ***) | 2.069027 × 10−315 (0.00000000 *) (2.069027 × 10−315 **) (2.069027 × 10−315 ***) |

| CCC | 0.1663335 (0.02734657 *) (0.1213524 **) (0.2113146 ***) | 0.6847605 (0.04000309 *) (0.6189613 **) (0.7505597 ***) | 0.1489060 (0.02146092 *) (0.1136059 **) (0.1842061 ***) |

| Implied Rating | A | BBB | BB |

|---|---|---|---|

| A | 0.10587950 (0.02691508 *) (0.06160814 **) (0.15015086 ***) | 0.8181818 (0.03942772 *) (0.7533290 **) (0.8830347 ***) | 0.07593868 (0.02188393 *) (0.03994281 **) (0.1119345 ***) |

| BBB | 0.30579660 (0.02320965 *) (0.26762012 **) (0.34397308 ***) | 0.4585097 (0.02922030 *) (0.4104466 **) (0.5065728 ***) | 0.23569367 (0.02123178 *) (0.20077050 **) (0.2706168 ***) |

| BB | 0.05717599 (0.01549908 *) (0.03168227 **) (0.08266971 ***) | 0.2966108 (0.02808647 *) (0.2504127 **) (0.3428089 ***) | 0.64621323 (0.02753047 *) (0.60092963 **) (0.6914968 ***) |

| Implied Rating | AA | A | BBB |

|---|---|---|---|

| AA | 0.21647619 (0.02456264 *) (0.176074249 **) (0.25687813 ***) | 0.57869048 (0.02901252 *) (0.530969134 **) (0.62641182 ***) | 0.2048333 (0.02519096 *) (0.1633979 **) (0.2462688 ***) |

| A | 0.02525253 (0.01313296 *) (0.003650722 **) (0.04685433 ***) | 0.43083213 (0.02797203 *) (0.384822233 **) (0.47684203 ***) | 0.5439153 (0.02992910 *) (0.4946864 **) (0.5931443 ***) |

| BBB | 0.61758521 (0.02618239 *) (0.574519002 **) (0.66065141 ***) | 0.02538071 (0.01313296 *) (0.003778907 **) (0.04698251 ***) | 0.3570341 (0.02412102 *) (0.3173585 **) (0.3967096 ***) |

| Implied Rating | BB | B | CCC |

|---|---|---|---|

| BB | 0.2640805 * 0.2640806 ** 0.2640806 *** | 0.6765132 * 0.6765132 ** 0.6765132 *** | 0.05940630 * 0.05940629 ** 0.05940629 *** |

| B | 0.2640806 * 0.2640806 ** 0.2640806 *** | 0.6765132 * 0.6765132 ** 0.6765132 *** | 0.05940628 * 0.05940629 ** 0.05940629 *** |

| CCC | 0.2640805 * 0.2640806 ** 0.2640806 *** | 0.6765132 * 0.6765132 ** 0.6765132 *** | 0.05940628 * 0.05940629 ** 0.05940629 *** |

| Implied Rating | A | BBB | BB |

|---|---|---|---|

| A | 0.1606010 * 0.1450128 ** 0.1310481 *** | 0.4097178 * 0.3700540 * 0.3344178 *** | 0.2906625 * 0.2629896 ** 0.237664 *** |

| BBB | 0.1688395 * 0.1525207 ** 0.1378330 *** | 0.4308033 * 0.3892133 ** 0.3517321 *** | 0.3059074 * 0.2766059 ** 0.249969 *** |

| BB | 0.1721708 * 0.1557422 ** 0.1407444 *** | 0.4394966 * 0.3974342 ** 0.3591617 *** | 0.3129858 * 0.2824490 ** 0.255249 *** |

| Implied Rating | AA | A | BBB |

|---|---|---|---|

| AA | 0.3032896 * 0.3033764 ** 0.3033764 *** | 0.3250668 * 0.3250228 ** 0.3250227 *** | 0.3716434 * 0.3716005 ** 0.3716005 *** |

| A | 0.3034091 * 0.3033764 ** 0.3033764 *** | 0.3249418 * 0.3250228 ** 0.3250227 *** | 0.3716489 * 0.3716005 ** 0.3716005 *** |

| BBB | 0.3034187 * 0.3033764 ** 0.3033764 *** | 0.3250579 * 0.3250228 ** 0.3250227 *** | 0.3715233 * 0.3716005 ** 0.3716005 *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Abid, A.; Abid, F. Sovereign Credit Risk in Saudi Arabia, Morocco and Egypt. J. Risk Financial Manag. 2024, 17, 283. https://doi.org/10.3390/jrfm17070283

Abid A, Abid F. Sovereign Credit Risk in Saudi Arabia, Morocco and Egypt. Journal of Risk and Financial Management. 2024; 17(7):283. https://doi.org/10.3390/jrfm17070283

Chicago/Turabian StyleAbid, Amira, and Fathi Abid. 2024. "Sovereign Credit Risk in Saudi Arabia, Morocco and Egypt" Journal of Risk and Financial Management 17, no. 7: 283. https://doi.org/10.3390/jrfm17070283

APA StyleAbid, A., & Abid, F. (2024). Sovereign Credit Risk in Saudi Arabia, Morocco and Egypt. Journal of Risk and Financial Management, 17(7), 283. https://doi.org/10.3390/jrfm17070283