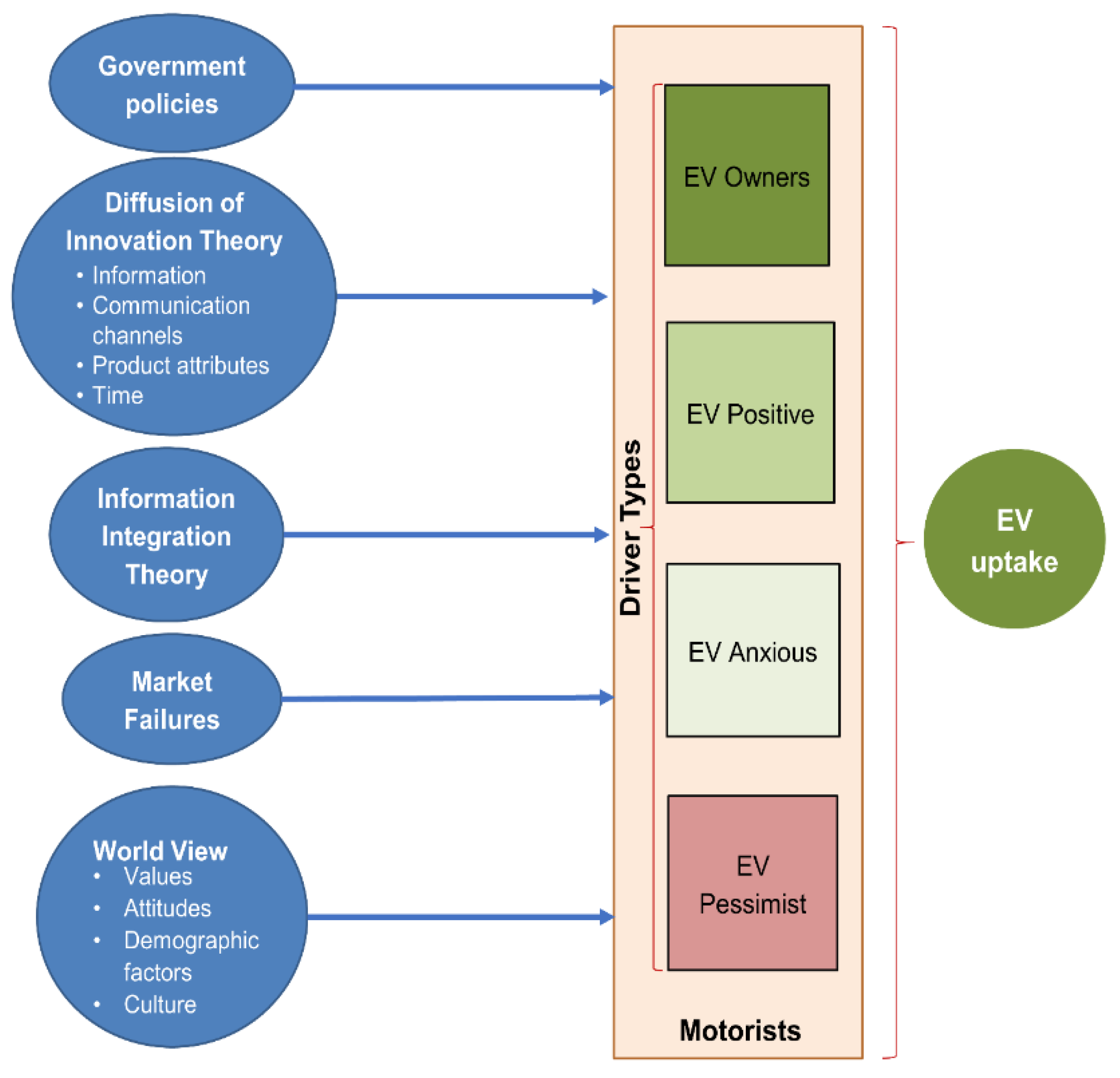

This research aimed to gain greater insights into consumer behavior by investigating differences between different groups of motorists, which could better inform government policy updates. This research ascertained that motorists’ attitudes towards EVs are not homogeneous. Based on previous research (

Section 2) indicating that attitudes to EVs are an important marker for EV readiness, we segmented survey participants based on Driver Types and mapped them against those devised by Rogers (2003) [

27] to represent societal niches (

Section 2), as there are common characteristics. We consider EV Owners as Innovators and Early Adopters; the EV Positives are conceived as the Early Majority; the EV Anxious are conceived as the Late Majority; while the Pessimists correspond with the Laggards.

5.1. Profiling Driver Types

Analysis of Driver Types confirms New Zealand’s motorists are heterogeneous in their attitudes towards EVs. Each Driver Type displays different characteristics. There is strong evidence of an association between Driver Type and their likelihood to buy a BEV and most other factors (

Table 2). However, no significant differences between groups appear for whether motorists bought vehicles new or used, and their preferences when researching cars, whether in magazines or newspapers. More than 94% of NZ motorists surveyed could park their car off-street with levels similar among Driver Types, indicating other factors were likely to be more important when considering the type of car to buy. Hereafter follows a more detailed discussion of the findings for each Driver Type.

5.1.1. EV Owners

Most EV Owners were enthusiastic about EVs, with 80.7% choosing the attitudinal option “It’s about time, why wouldn’t you” with a further 16.4% choosing “Yes please, it would save how much fuel” (

Table S1), indicating a high degree of enthusiasm for the technology. Most EV Owners were much more likely to buy a BEV next time they buy a car rather than a PHEV (

Figure 2 and

Table S6). High BEV ownership (94.1%) could explain these very different scores for the two types of EVs. Further demonstrating enthusiasm for EVs, more than half would have bought an EV regardless of any initiatives offered (

Table 4), such as removing EVs first registration tax or ride and drive showcase events.

Interviewee EV#27 gave a typical response when asked if he would buy a BEV again: “Oh, 100%”, but to a PHEV “No”, while he had “managed to convince three people to buy an electric car at my old school that I taught at.”

Compared to all other Driver Types, EV Owners had the lowest proportion of school-only educated people; were more likely to spend more than NZ

$30,000 on their next car, and to own multiple vehicles (82.6%) including at least one ICEV (76.1%); and more frequently drove further than 150 km on individual trips (

Table S2).

5.1.2. EV Positives

In contrast to most EV Owners, EV Positives were more likely to identify cost savings as a reason to buy an EV in the future, with more than twice as many ICEV drivers (

Table 3) choosing “Yes please, it would save how much fuel?” rather than “It’s about time, why wouldn’t you.” The Positives were only slightly more likely to buy a BEV compared to a PHEV. A representative response about potential EV purchase was Interviewee ICEV#12:

“I would definitely buy an EV. The car we’ve got now, we got it in 2017, we could have gone electric car potentially, just above the price range, but we weren’t quite there yet, but if we were doing it again now then we would definitely be able to” and “I would like to say for the environment, but probably the costs, it’s much cheaper to run.”

5.1.3. EV Anxious

Results (

Table 3) show that EV Anxious preferred PHEVs rather than BEVs: over half of the EV Anxious thought EVs were a good idea, but would prefer PHEVs for now, while the remainder expressed concerns about recharging facilities, despite most having access to off-street parking (

Table S6). Potentially, concerns include anxiety about charging generally, including rechargeability away from home. Such concern is consistent with Norwegian research findings, where ICEV owners were three times more worried about charging issues than EV owners [

48].

These two “Anxious” interviewees exemplified the following concerns:

Interviewee ICEV#2: “Just hearing their stories of how friends had to stop and plug in and recharge, and that just put us off, and nice that we could get this car [petrol hybrid] and the price wasn’t too bad. That’s a better option for us.”

Interviewee ICEV#4: “How far I am going, without needing recharging every day, I don’t want a car shorting out on me constantly.”

Messaging from EV owners could be used to counteract such apprehensions. Previous research indicates EV owners usually recharge at home [

49] and prefer home recharging rather than filling up an ICEV at petrol stations [

50]. At-home recharging may be an unexpected bonus that could be used in marketing.

Interviewee EV#11 expressed that sentiment well: “

And I really like the fact that I can just plug it into the wall at home. I think that’s the most underestimated advantage of them.”

5.1.4. EV Pessimists

The Pessimists were a small group (

Table 3), with most drivers skeptical of EVs; 85.4% chose “Will they save the planet, I don’t think so” (Option 6). The remainder could not envisage themselves as identifying with EVs, selecting “I would never be seen in one of those” (Option 7). Of the ICEV motorists, Pessimists were least likely to buy either a BEV (

Figure 2) or PHEV (

Table S6 A15–2).

Interviewee ICEV#21 was representative, and was not amenable to EVs, “to be honest electric cars don’t do anything for me” and was skeptical “The thing that puts me off mostly is all the hype that goes on around the whole electric car thing. They market them as if it’s a be all and end all, and they’re not.”

Interviewee ICEV#11 asked about buying an EV, “doesn’t interest me, well, you know, the charging, I am not happy about the disposal of the batteries, they try and hide that.” And “I don’t know if there is leakage of the charge if you don’t use the vehicle.”

Pessimists were more likely to be one-car owners, were not as well educated, had lower proportions in the younger age groups, and drove long distances less frequently compared to other Driver Types (

Table S5).

5.2. Valuing the Environment

Evidence supports that for EV Owners, the vehicles’ environmental credentials were a strong motivation for purchase. Respondents were asked about the importance to them of three factors: economy, environment and society, and results show that EV Owners had a strong environmental regard in their hopes for the future state of NZ (

Figure S2). Furthermore, regard for the environment was the most important factor for EV Owners motivating EV purchase (

Tables S3 and S5).

Interviewee EV#29 summed up environmental regard: “I think the primary motivation is concern for the environment, we wanted a cleaner way of moving around.”

Interviews revealed that EV Owners in multi-car households tended to use their EV more often than their other cars to maximize the advantages of owning one. For example, Interviewee EV#3, owner of seven vehicles: “If the e-Golf is available, the Golf is the first vehicle out the gate every day. It changes the way you think when you’ve got an electric vehicle, we think who is going to do the most kilometers in town to maximize the savings by having that electric vehicle.…It does 95% of our vehicle usage, that particular vehicle…In five years’ time all my vehicles will be electric.”

Such sentiments are consistent with Norwegian research, demonstrating that in households with both electric and conventional cars, EVs replaced 82% of ICEV use [

51].

5.3. Identifying Concerns and Potential Barriers to EV Adoption

Potential barriers to adoption were revealed by responses to questions regarding motorists’ EV concerns. There is strong evidence for an association between Driver Type and the importance of individual vehicle attributes (

p < 0.0001). For the EV Positives, the most important of the vehicle attributes were the expected life of an EV’s battery and purchase price followed by range (

Table S6,

Figures S4 and S5). Having a network of rechargers right around NZ was only slightly less important (

Figure S6), whereas the attributes of ‘Total ownership costs’, ‘availability of a model EV to suit their needs’ and that ‘electric cars have fewer servicing requirements’ were of less concern.

For most factors, EV Owners, with practical experience and research to inform them, were the least concerned, which is consistent with findings previously demonstrated among Norwegian motorists [

48].

Potential barriers to EV adoption for non-owners were further explored with ICEV drivers (

Table S4), who were asked to complete the statement: “

I would be more likely to buy an EV if…” Responses revealed that ICEV drivers were very concerned about purchase price, with Positives more worried by this than any other factor. Pessimists were the only group explicitly stating that they would not buy an EV (21%), complementing results from other questions: “

I would not buy an EV” (A23-12) and with their limited likelihood of buying BEVs or PHEVs (

Figure 2).

An EV Owner’s quote exemplifies the importance of range anxiety when choosing which EV model to buy:

Interviewee EV#30: “The protocol in our house is who’s going to be driving the most that day, and the furthest, and who is going to be doing the most driving takes the EV… That’s how I managed to convince him [partner], because he was the one with the anxiety about the range. You know, he wants [the range] to go to 450 kms. And I said, even if we get this one, we won’t be charging it up maybe once a fortnight, which is what it has turned out.”

5.4. Information Acquisition When Buying Cars

Access to information is regarded as an important influence on motorists when choosing cars (

Section 2). Our results from two sets of tests support this finding, as the likelihood of EV ownership diminished, engagement with written sources about cars declined (

Table 5,

Figure 2 and

Figure 3). There is strong evidence of an association between Driver Type and: level of research undertaken when buying cars (A8:

p < 0.0001); primary source of information when buying cars (

Figure S1); use of international online sites or social media (A14 − 11 + 12:

p < 0.0001); claims that the respondent ‘rarely, if ever, read about cars’; and a lack of awareness about initiatives to encourage EV uptake (

Table 2). Further statistical testing provides evidence of a correlation between Likelihood to buy a BEV (across all motorists) and these same factors (

Table 5).

EV Owners were the most likely to undertake research when buying a car, with most (95.7%) claiming they did a lot of research. EV Owners mainly used written sources focusing on online sources, including international and social media to update their knowledge about cars (

Figure S1), and had the lowest proportion of drivers claiming they rarely, if ever, read about cars. EV Owners were the least likely to claim they were unaware of any EV initiatives (

Table 4,

Figure S3). These results may be the result of targeting the EV Owners Association of NZ Facebook page or Better NZ Trust webpage to obtain respondents, as these people were already engaged in online participation, compared to the randomly sampled ICEV motorists. However, it is possible that EV Owners generally, being innovators and early adopters (

Section 2), are enthusiastic and better informed about EVs than non-EV motorists.

By contrast, the Positives and Anxious groups showed similar patterns for level of research—their primary information source relied more heavily on word of mouth and other information sources than for EV Owners (

Figure S1). These two groups used online resources similarly, less than EV Owners, and, with higher proportions of those who ‘rarely, if ever, read about cars’ compared to EV Owners.

Pessimists were the least engaged of all groups with finding out about cars. Few pessimists claimed they did a lot of research (A8); they were most likely to be uninterested in finding out about cars (A13); they were least likely to use online sources to update their knowledge of cars (A14 11 + 12) (

Figure S1); and they were most likely to claim they ‘rarely, if ever, read about cars’ (A14–14). Pessimists were least likely to be aware of EV initiatives (

Figure S7, A22–11).

5.6. Incentivizing EV Uptake

Ten initiatives were presented to motorists (

Table 4), with respondents asked to nominate up to three initiatives they most preferred. The analysis revealed the most preferred overall was ‘provision of a network of fast chargers around the country’, appealing most to the Anxious (56.2%), then the EV Owners (53.4%) and Positives (48.1%). Public installation of fast chargers has twice the impact on EV sales, compared to slower chargers [

53], and are considered essential [

54] for enabling longer trips than an EV’s range, thus increasing a motorist’s self-efficacy.

The government-developed ‘Smartphone App, used to locate rechargers’, (called EV Roam) was most popular with the Anxious (36.8%). Increasing knowledge about the availability of this program could help allay fears and reduce range anxiety. A very low proportion of EV Owners (3.6%) selected this option in their top three. A low proportion of EV Owners had heard of EV Roam (27.9%), and a possible explanation is that they use other apps to locate rechargers on long trips (e.g., Plugshare).

The recommended, but not implemented, ‘Clean Car Discount’ [

55] as a bonus-malus scheme, which is cost-neutral to the government, is a policy designed to ensure vehicle buyers pay more for the first registration of high-emission cars and less when registering low- or zero-emission vehicles. This incentive potentially provides a financial reward for enacting low-emission behavior by reducing EV upfront costs to consumers, thereby narrowing the purchase price differential to ICEVs. Although unavailable to date, this policy was most appealing to Positives (51.3%) and the Anxious (42.8%) and less to the Pessimists (31.5%). EV Owners (29.2%) were least likely to favor this initiative, but as many would have bought an EV regardless of incentives (52.1%) and already owned an EV, this choice perhaps indicates no future advantage to them personally. The ‘Discount’ could help change perceptions (

Section 5.7) that EVs are “expensive” and could help reinforce the “economical” perceptions held by many motorists. Reducing the higher costs to either buy or run an EV has been utilized by many governments as a policy measure to attract EV uptake [

6], and any action that potentially increases the price of EVs, for example by introducing road user taxes on EVs to provide income for governments could be considered counterproductive.

More important to EV Owners (40.7%) than the discount was the policy enabling ‘importation of second-hand EVs’ from Japan and the UK (

Table 4), which is consistent with the high percentage of EV Owners who had bought second-hand imported EVs (83.3%, discounting the ‘

didn’t know’). As there was no significant difference for the association between Driver Type and whether a motorist buys new or used vehicles (

Table 2), it could be argued that this is an economically rational measure appealing to all Driver Types.

If the aim of providing incentives is to increase rates of EV ownership among NZ motorists, it is reasonable to suggest that the two most helpful incentives we investigated were: 1. Increasing national deployment of fast chargers, thereby increasing convenience and reducing range anxiety, and 2. Reducing EVs upfront price, either through cheaper second-hand imports or via financial support such as the ‘Clean Car Discount’ policy. Previous observations [

20], found minimizing the cost differential between EVs and ICEVs, was very important to encourage uptake, which our research has demonstrated is important to New Zealanders. Additionally, the introduction of the ‘Clean Car Standard’, while not popular with many motorists (

Table 4), has the potential to encourage manufacturers to increase the number of EVs imported to NZ to reduce their brand’s overall emissions burden, and therefore, avoid any potential penalties attached to that measure, as occurs in the European Union [

56].

5.7. Perceptions about EVs

Asking motorists for three words that popped into their heads they associated with EVs revealed interesting perceptions of EVs. There is a strong association (

Table 2) with Driver Type and motorists choosing certain concepts (at least one negative word; ‘Expensive’; ‘Economical’; ‘Low-range’; ‘Ecofriendly’; and ‘Fun’:

p < 0.0001).

The results (

Table S5) demonstrate that with increasing aversion to EVs by Driver Type, there is an increasing use of at least one negative concept, with ‘expensive’ as the most outstanding. Only the EV Owners did not see ‘expensive’ as noteworthy. Five years earlier, it was reported [

57] that EVs’ relatively high upfront cost presented a considerable hurdle for New Zealand motorists, with testing revealing it was only if the purchase price became half of conventional cars that all motorists were convinced to change. Our results show for ICEV drivers this perception of ‘expensive’ is still strong. However, our results also demonstrated positive perceptions: EV Positives were equally likely as EV Owners to regard EVs as ‘Economical’, and more likely to consider them ‘Ecofriendly’.

Marketing cars involves careful branding to convey positive imagery that suits the emotions, desires and needs of the target markets (

Section 2). Therefore, to create a more positive perception for EVs, reframing the language to show EVs as representing the ‘good life’ [

58], adoption of EV Owners’ language could be beneficial. Comparing the language of Positives and EV Owners, the chief difference is that Positives perceive EVs as ‘expensive’, whereas EV Owners think they are ‘fun’. Both groups agree they are ‘economical’ and ‘ecofriendly’, and such sentiments may be useful in marketing campaigns.

The language used by some of the EV Owners expresses well the advantages they perceived about EVs:

Interviewee EV#22: “So the last time I updated my spreadsheet (…) was probably the beginning of this year and I had saved $24,000 in my car over two and a half years, and it cost me $32,000 [to buy]. So, I was well ahead. It’s raised my standard of living well, of course. That’s the whole point, it not only raises everybody’s standard living because you’re not spewing out fumes, but you’re improving your own standard of living, and New Zealand’s because they’re not importing the fuel. And somebody in New Zealand’s got a job because you do that.”

Interviewee EV#5: “It’s around the ethics of it. It’s around the green credentials. Then the cost savings associated with it are amazing…I was in a car yard in town, [with] a Leaf parked out front. And I took it for a drive just for fun, really. And I was blown away by the performance and in the way it handled and the quietness of it.”

Interviewee EV#8: “So partially environmental, partially cost. It was a case of, actually, the driving experiences are all nicer.”

Our results demonstrate there are differences among Driver Types. To market EVs to the most EV ready, in this case the Positives, then a positive image ought to be promoted. The Positives could use EV Owners as role models, who can provide evidence that the product is viable. It has been suggested [

59] that for the next marketing niche to accept a product, they need a compelling reason to change. EVs could be promoted by creating a value proposition that this product is better than competing alternatives, in this case ICEVs.

While the ‘Clean Car Standard’ was not especially popular with motorists (

Table 4), it could encourage car dealers to increase the number of EVs they import at no cost to the government, and therefore, taxpayers (See

Section 5.6). Similarly, growing procurement by organizations would improve sales and potentially expand model availability, an important measure for the EV Positives (

Table S6, A17_4). Additional procurement could increase communications about EVs through the channel of employees who may speak to their contacts about their experiences. Such actions could provide evidence that governments and other large organizations think EVs are a suitable option, as has been demonstrated in Norwegian research that showed government procurement fostered EV sales [

60].

Government policies encourage uptake of EVs [

6], and the government ought to provide a clear lead, being seen to act [

61]. Our results provide evidence to contend that one action the NZ government could take—which would likely increase EV sales—is to implement earlier policy suggestions [

55], namely, one of the most popular incentives, the ‘Clean Car Discount’, helping reduce the price differential between EVs and ICEVs, and counteracting EVs’ negative image of ‘expensive’, potentially creating a positive value proposition and rewarding good behavior. However, not only should there be a positive value proposition, opposing forces need to be considered.

Noel et al. (2019) [

62] suggested conservative forces propagate perverse concepts to oppose change by promulgating and reinforcing range anxiety. To counteract such an effect, consideration that the second most popular incentive for EV Positives was a network of fast chargers (

Figure S6) suggests further work needs to be done, not only deploying more rechargers, but increasing messaging about how to find them via smartphone apps. Our results suggest that ICEV motorists’ knowledge about initiatives supporting EVs is limited (

Table 4,

Figures S3 and S7), and that likelihood to buy an EV diminishes as the awareness of initiatives diminishes (

Figure 4). Thus, updating policies aiming to increase awareness of incentives could be a valuable strategy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}