Determinants of Investments in Energy Sector in Poland

,

,  , ,

, ,

Abstract

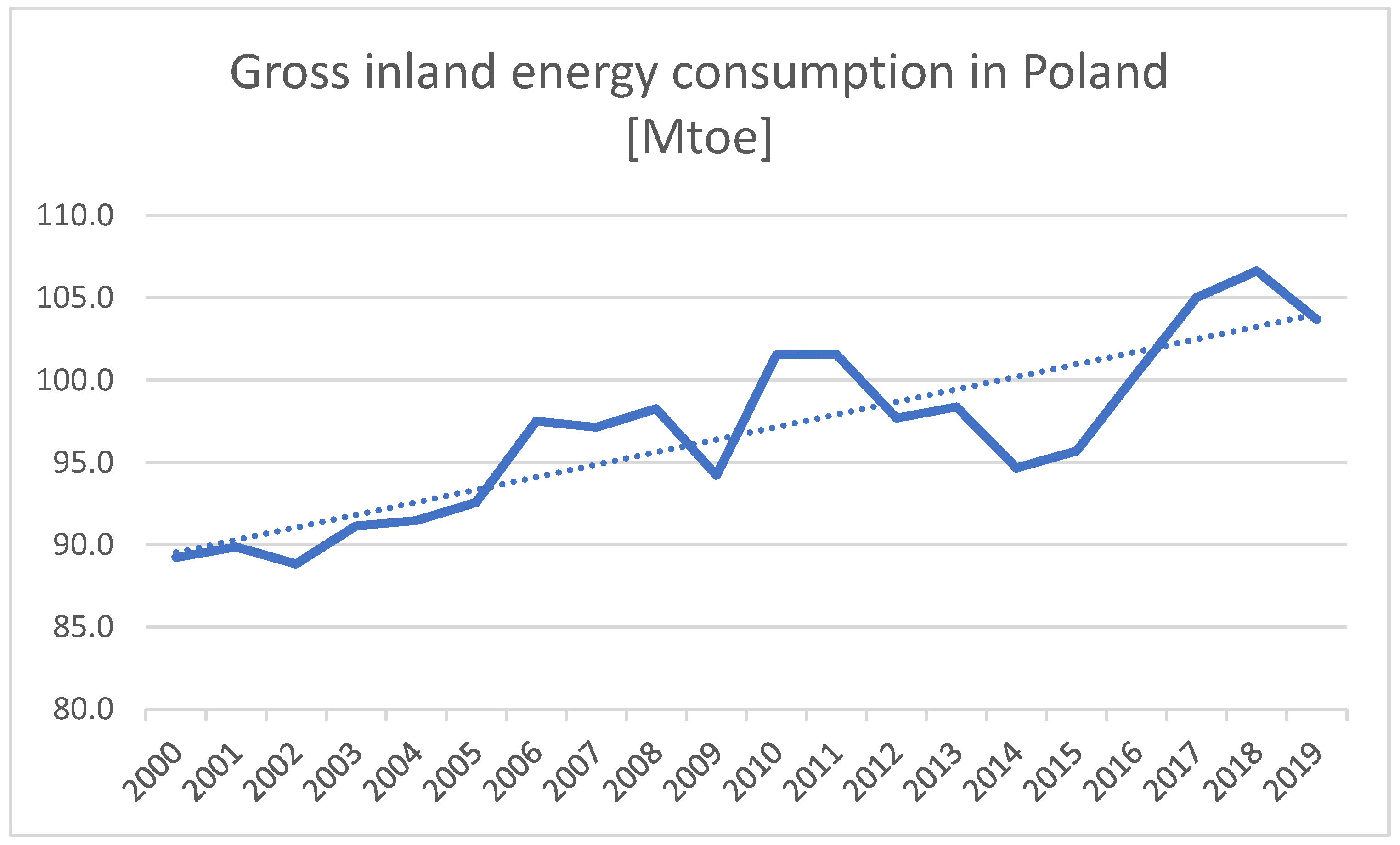

:1. Introduction

- Increase energy efficiency by saving primary energy consumption by 13.6 Mtoe between 2010 and 2020 compared to the 2007 fuel and energy demand forecast;

- Increase the share of RES energy in gross final energy consumption to 15% by 2020;

- Reduce greenhouse gas emissions by 20% (compared to 1990) until 2020 (2005 levels: −21% in EU ETS and −10% non-ETS sectors).

- Fair energy transition;

- A zero-emission energy system;

- Good air quality.

2. Hypotheses Development

3. Methodology

3.1. Canonical Analysis

3.2. Linear and Causality Correlations

3.2.1. Test of Kwiatkowski, Philips, Schmidt and Shin

- The expected value (mean value) is steady and neutral in time;

- The variance is steady and neutral in time;

- The covariance among different variables depends only on the case numbers and is autonomous of time.

3.2.2. Pearson’s Linear Correlation Coefficient

3.2.3. Test of Granger

- n is the amount of observations;

- k is the amount of model parameters;

- RSS is the residual sum of squares that result from the statistical model.

3.3. Autocorrelation and Partially Autocorrelation Tests

3.4. Cointegration

- Stationary examination of variables with ADF test (Augmanted Dickey Fuler-test). All variables must be non-stationary;

- Estimating the cointegration vector:

- 3.

- If the rest of the model ut are stationary, then there is cointegration between the variables x and y.

ADF Test

4. Collecting Data and Statistical Analysis

- Changes of total investments of enterprises from the energy sector (d_NIO) are caused by an intermediate consumption (d_ZP) two years ago and total output (d_PG) in the energy sector five years ago;

- Changes in the investments for fixed assets in the energy sector enterprises (d_NST) are caused by the changes of total output in the energy sector (d_PG) five years ago;

- Changes in the investments in machines in the energy sector enterprises (d_NM) are caused by the changes of total output in the energy sector (d_PG) a year ago;

- Despite high correlation coefficients (above 0.9) between the variables d_ NIO, d_NST and d_NM, they do not depend on the same factors;

- Changes in the total output in the energy sector (d_PG) are caused by changes in the gross value of fixed assets obtained from investments by energy sector enterprises (d_WBSTI) up to four years back;

- Changes in the level of intermediate consumption in the energy sector (d_ZP) are caused by changes in the level of investment in machines in energy sector enterprises (d_NM) up to four years back;

- The signs of correlation coefficients (Table 2) suggest that all of the above-mentioned dependencies are simply proportional (positive).

5. Discussion and Conclusions

- In order to increase the effectiveness of investment decisions in the energy sector in Poland, managers should conduct anticipatory analyses, taking into account trends and prospects for economic growth, with particular reference to such macroeconomic indicators as intermediate consumption and total output;

- Due to the increased sensitivity of investments of small energy companies in Poland to changes in public consumption and interest rates, entrepreneurs and managers in these entities should develop methods of financial and relationship risk management. It will be particularly important to use appropriate insurance products and adequate protection of interests through economic contracts;

- An effective way of improving small energy firms’ access to stable, reliable and secure external financing appears to be through institutional reforms addressing weaknesses in the legal and financial systems in Poland;

- Managers of medium and large energy companies in Poland should take a long-term (strategic) perspective in their planning process to ensure the ability of companies to generate the resources necessary to invest in next-generation projects;

- Policies and programs for the development of energy enterprises in Poland should be adjusted to the needs of companies of different sizes to encourage continuous investment and be consistent with an appropriate macroeconomic policy aimed at long-term economic growth.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

References

- European Union. EU Energy in Figures Statistical Pocketbook; Directorate-General for Energy, European Commission: Brussels, Belgium, 2019. [Google Scholar]

- Sharma, N.; Smeets, B.; Tryggestad, C. The Decoupling of GDP and Energy Growth: A CEO Guide; McKinsey: New York, NY, USA, 2019; pp. 1–13. [Google Scholar]

- European Statistical Office, Eurostat (online data code: Prc_ppp_ind). Available online: https://ec.europa.eu/eurostat (accessed on 25 May 2021).

- Carraro, C.; Favero, A.; Massetti, E. Investments and public finance in a green, low carbon, economy. Energy Econ. 2012, 34, S15–S28. [Google Scholar] [CrossRef]

- Armeanu, D.Ş.; Vintilă, G.; Gherghina, Ş.C. Does Renewable Energy Drive Sustainable Economic Growth? Multivariate Panel Data Evidence for EU-28 Countries. Energies 2017, 10, 381. [Google Scholar] [CrossRef]

- Soava, G.; Mehedintu, A.; Sterpu, M.; Raduteanu, M. Impact of renewable energy consumption on economic growth: Evidence from European Union countries. Technol. Econ. Dev. Econ. 2018, 24, 914–932. [Google Scholar] [CrossRef]

- Hanif, I. Impact of economic growth, nonrenewable and renewable energy consumption, and urbanization on carbon emissions in Sub-Saharan Africa. Environ. Sci. Pollut. Res. 2018, 25, 15057–15067. [Google Scholar] [CrossRef] [PubMed]

- Asiedu, B.A.; Hassan, A.A.; Bein, M.A. Renewable energy, non-renewable energy, and economic growth: Evidence from 26 European countries. Environ. Sci. Pollut. Res. 2021, 28, 11119–11128. [Google Scholar] [CrossRef] [PubMed]

- Grijó, T.; Soares, I. Solar photovoltaic investments and economic growth in EU: Are we able to evaluate the nexus? Environ. Dev. Sustain. 2016, 18, 1415–1432. [Google Scholar] [CrossRef]

- Gródek-Szostak, Z.; Suder, M.; Kusa, R.; Szeląg-Sikora, A.; Duda, J.; Niemiec, M. Renewable Energy Promotion Instruments Used by Innovation Brokers in a Technology Transfer Network. Case Study of the Enterprise Europe Network. Energies 2020, 13, 5752. [Google Scholar] [CrossRef]

- Krugman, P.; Wells, R. Macroeconomics, 4th ed.; Worth Publishers: Warszawa, Poland, 2015. [Google Scholar]

- Kasahara, T. Severity of financing constraints and firms’ investments. Rev. Financ. Econ. 2008, 17, 112–129. [Google Scholar] [CrossRef]

- Zubair, S.; Kabir, R.; Huang, X. Does the financial crisis change the effect of financing on investment? Evidence from private SMEs. J. Bus. Res. 2020, 110, 456–463. [Google Scholar] [CrossRef]

- Akbar, S.; Rehman, S.U.; Ormrod, P. The impact of recent financial shocks on the financing and investment policies of UK private firms. Int. Rev. Financ. Anal. 2013, 26, 59–70. [Google Scholar] [CrossRef]

- Balduzzi, P.; Brancatib, E.; Schiantarellic, F. Financial markets, banks’ cost of funding, and firms’ decisions: Lessons from two crises. J. Financ. Intermediat. 2018, 36, 1–15. [Google Scholar] [CrossRef] [Green Version]

- Vermoesen, V.; De Loof, M.; Laveren, E. Long-term debt maturity and financing constraints of SMEs during the Global Financial Crisis. Small Bus. Econ. 2013, 41, 433–448. [Google Scholar] [CrossRef]

- Farina, L.; Prego, P. Investment Decisions and Financial Standing of Portuguese Firms—Recent Evidence, Financial Stability Report; Banco de Portugal: Lisboa, Portugal, 2013; pp. 105–125. [Google Scholar]

- Perić, M.; Đurkin, J. Determinants of investment decisions in a crisis: Perspective of Croatian small firms. Management 2015, 20, 115–133. [Google Scholar]

- Giebel, M.; Kraft, K. The impact of the financial crisis on capital investments in innovative firms. Ind. Corp. Chang. 2018, 28, 1–24. [Google Scholar] [CrossRef]

- Laperche, B.; Lefebvre, G.; Langlet, D. Innovation strategies of industrial groups in the global crisis: Rationalization and new paths. Technol. Forecast. Soc. Chang. 2011, 78, 1319–1331. [Google Scholar] [CrossRef]

- Archibugi, D.; Filippetti, A.; Frenz, M. The impact of the economic crisis on innovation: Evidence from Europe. Technol. Forecast. Soc. Chang. 2013, 80, 1247–1260. [Google Scholar] [CrossRef] [Green Version]

- Karafolas, S.; Ragias, V. Economic crisis effects on investment plans: The case of the LEADER program in the region of West Macedonia, Greece. In Proceedings of the 13th International Conference of “Economies of the Balkan and Eastern European Countries”, EBEEC 2021, Pafos, Cyprus, 14–16 May 2021. [Google Scholar]

- Ministerstwo Energii. Polityka Państwa do Roku 2040; Ministerstwo Energii: Warszawa, Poland, 2018. [Google Scholar]

- Główny Urząd Statystyczny. 2020. Available online: https://stat.gov.pl (accessed on 25 May 2021).

- Sultan, Z.A.; Haque, M.I. The estimation of the cointegration relationship between growth, domestic investment and exports: The Indian economy. Int. J. Econ. Financ. 2011, 3, 226–232. [Google Scholar] [CrossRef]

- Inessa, S.; Artem, S.; Wielki, J. Analysis of Macroeconomic Factors Affecting the Investment Potential of an Enterprise. Eur. Res. Stud. J. 2019, XXII, 140–167. [Google Scholar] [CrossRef] [Green Version]

- Wozniak, M.; Lisowski, R.; Dudek, M. Relationships between Macroeconomics Indicators and Investments of Enterprises: Evidence from Poland. Eur. Res. Stud. J. 2021, XXIV, 555–567. [Google Scholar] [CrossRef]

- Harris, R.J. The invalidity of partitioned U tests in canonical correlation and multivariate analysis of variance. Multivar. Behav. Res. 1976, 11, 353–365. [Google Scholar] [CrossRef]

- Barcikowski, R.; Stevens, J.P. A Monte Carlo study of the stability of canonical correlations, canonical weights, and canonical variate-variable correlations. Multivar. Behav. Res. 1975, 10, 353–364. [Google Scholar] [CrossRef] [PubMed]

- Engle, R.F.; Granger, C.W.J. (Eds.) Long-Run Economic Relationships; Oxford University Press: Oxford, UK, 1992. [Google Scholar]

- Charemza, W.W.; Deadman, D.F. Nowa Ekonometria; PWE: Warszawa, Poland, 1997. [Google Scholar]

- Osińska, M. Ekonometria Współczesna; TNOiK Dom Organizatora: Toruń, Poland, 2007. [Google Scholar]

- Aaker, D.A.; Kumar, V.; Leone, P.R.; Day, S.G. Marketing Research, 11th ed.; John Wiley & Sons: Hoboken, NJ, USA, 2013. [Google Scholar]

- Akaike, H. A new look at the statistical model identification. IEEE Trans. Autom. Control 1974, 19, 716–723. [Google Scholar] [CrossRef]

- Stone, M. Comments on Model Selection Criteria of Akaike and Schwarz. J. R. Stat. Soc. Ser. B 1979, 41, 276–278. [Google Scholar] [CrossRef]

- Lisowski, R.; Woźniak, M.; Wójtowicz, T. Impact of Fiscal Instruments on Investments of Industrial Enterprises in Poland W: Functioning and Development of Enterprises: Contemporary Challenges; Duda, J., Skalna, I., Eds.; Wydawnictwa AGH: Kraków, Poland, 2019; pp. 63–69. [Google Scholar]

- Główny Urząd Statystyczny, Rocznik Statystyczny Rzeczypospolitej Polskiej 2001–2020, Zakład Wydawnictw Statystycznych, Warszawa, 2001–2020. Available online: https://stat.gov.pl/obszary-tematyczne/roczniki-statystyczne/roczniki-statystyczne/rocznik-statystyczny-rzeczypospolitej-polskiej-2020,2,20.html (accessed on 25 May 2021).

- Główny Urząd Statystyczny, Wyniki Finansowe Przedsiębiorstw Niefinansowych, Zakład Wydawnictw Statystycznych, Warszawa, 2006–2019. Available online: https://stat.gov.pl/obszary-tematyczne/podmioty-gospodarcze-wyniki-finansowe/przedsiebiorstwa-niefinansowe/wyniki-finansowe-przedsiebiorstw-niefinansowych-i-vi-2020,11,23.html (accessed on 9 October 2020).

- Główny Urząd Statystyczny. Available online: https://stat.gov.pl/wskazniki-makroekonomiczne/ (accessed on 26 May 2021).

- Narodowy Bank Polski. Available online: https://www.nbp.pl/home.aspx?f=/statystyka/pieniezna_i_bankowa/oprocentowanie.html (accessed on 25 May 2021).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| N = 20 | Canonical R: 0.99708 Chi 2 (72) = 119.43 p = 0.00039 | |

|---|---|---|

| Group A—Left | Group C—Right | |

| Number of variables | 9 | 8 |

| Extracted variance | 99.1134% | 100.000% |

| Total redundancy | 90.6513% | 91.4633% |

| Variable | d_PG | d_ZP | d_KZ | d_SP | d_K1 | d_K1_5 | d_K5 | d_KO |

|---|---|---|---|---|---|---|---|---|

| d_IME | 0.560486 | 0.533543 | 0.757241 | 0.734336 | 0.661062 | 0.716984 | ||

| d_NIO | 0.546799 | 0.532638 | - | - | - | - | - | - |

| d_NST | 0.543874 | 0.524437 | - | - | - | - | - | |

| d_NM | 0.596575 | 0.575515 | - | - | - | - | - | - |

| d_WBSTI | 0.490708 | - | - | - | - | - | - | - |

| Explained variable | Explanatory variables | |

| d_ZP | d_PG | |

| d_NIO | 0.0891 VAR (2) | 0.0640 VAR (1.3.5) |

| d_NST | - | 0.1004 VAR (1.3.5) |

| d_NM | - | 0.0 451 VAR (1) |

| Explained variable | Explanatory variables | |

| d_WBSTI | ||

| d_PG | 0.0744 VAR (4) | |

| d_NM | ||

| d_ZP | 0.0778 VAR (4) | |

| Variable | ACF Delay | PACF Delay | Significance Level |

|---|---|---|---|

| d_ISiDE | 2 years | 0.10 | |

| d_NBB | 2 years | 2 years | 0.10 |

| Dependent Variable | Independent Variable | |

| ZP | PG | |

| NIO | 0.14 | 0, 6694 |

| NST | 0.6887 | |

| NM | 0.522 | |

| Dependent variable | Independent variable | |

| WBSTI | ||

| PG | 0.3726 | |

| NM | ||

| ZP | 0.6564 | |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lisowski, R.; Woźniak, M.; Jastrzębski, P.; Karafolas, S.; Matejun, M. Determinants of Investments in Energy Sector in Poland. Energies 2021, 14, 4526. https://doi.org/10.3390/en14154526

Lisowski R, Woźniak M, Jastrzębski P, Karafolas S, Matejun M. Determinants of Investments in Energy Sector in Poland. Energies. 2021; 14(15):4526. https://doi.org/10.3390/en14154526

Chicago/Turabian StyleLisowski, Robert, Maciej Woźniak, Paweł Jastrzębski, Simeon Karafolas, and Marek Matejun. 2021. "Determinants of Investments in Energy Sector in Poland" Energies 14, no. 15: 4526. https://doi.org/10.3390/en14154526