Abstract

The regulatory environment for both sustainability and financial reporting is changing as standardisation and digital reporting (e.g., XBRL) are gaining traction within regulators. The measurement methodology and mandatory information content of disclosures are yet to be decided for corporate CO2 reporting by EU regulators and standard-setting organisations. In our study, we reviewed the sustainability reports of three leading German automotive groups by revenue for the period 2016–2020 as a case study. The research methodology was carried out with text-mining-aided content analysis to provide a collection of sustainability standards (GRI and SASB) in the evaluation of emissions reporting. As an addition to prior literature, conditions of relevance and clarity regarding published information were introduced in the evaluation process of compliance to CO2 disclosures. Companies by reporting practice were assigned to different stages of carbon management and actual emissions were evaluated. In the conclusions, discussion of the reliability of reported sustainability information, the applicability of digital reporting is provided through regional perspectives. We found that although analytical methods are available to assess the level of corporate carbon management, their usefulness is limited if the data are not reliable. Significant progress can be expected from analyses using standardised, comparable corporate carbon data.

1. Introduction

Carbon accounting is an emerging field of business economics and covers a wide range of activities, including measurement, calculation, monitoring, reporting, and auditing [1]. Industrial companies use large amounts of energy and materials in their activities and are therefore particularly responsible for greenhouse gas emissions. On the other hand, their technological innovation potential makes them major players in the climate change challenge [2]. According to the recent study of Spreafico, the environmental impact of cars makes up the largest share of the total global impact of passenger transport, due to their ubiquity and high impact per kilometre travelled [3]. To reduce the environmental impact of the car industry, many governments have introduced significant mitigation measures. As a result, all car manufacturers have embarked on wide-ranging interventions to increase sustainability [2]. The pursuit of sustainable development leads companies to react in different ways. Some choose proactive and innovative strategies, while others opt for reactive environmental strategies. A key feature of proactive environmental strategies is the use of modern methods integrated into management systems [4]. Companies should integrate their sustainability goals across the business platform, rather than treating them as separate from their business strategy [2]. Carbon accounting issues need to be integrated into functional areas to support the achievement of corporate and climate policy objectives [1]. Based on the literature review to be presented in Section 2, a research gap was identified in carbon accounting, specifically in its qualitative measurement in non-financial corporate reporting. Theoretical grounding relies on the Resource-based View (RBV) theory, which explains corporate competitive advantage as a mix of non-substitutable resources [5]. The RBV theory itself raises the need to use resources efficiently to achieve sustainable performance [6], yet companies do not see their use of resources as the most efficient, according to business reports. Corporate annual sustainability reports discuss the efficiency of the use of these resources from several perspectives, but the qualitative analysis of these resources has been little discussed in areas of corporate reporting and environmental economics. Digitisation has not previously been utilised directly to measure sustainability qualitatively in this area; in addition to using digitization, we looked at the standardisation guidelines proposed by the current European regulatory environment.

In the current study, we connected prior models of carbon accounting with the European legal obligations of quality (standards for sustainability information content) and format (digital), highlighting cross-connectivity between the two. We conducted exploratory research through case studies, comparing theoretical studies and standard requirements with published sustainability reports of the three largest German automotive OEMs. Our research objective was to generate a validation methodology scale because the actual compliance with the required standards is hard to measure while considering many qualitative factors, therefore this contribution improves the traceability of sustainability attributes based on corporate reporting practices.

2. Literature Review

2.1. Carbon Accounting in Corporate Practice and Regulation

There is a massive body of literature discussing the conceptual framework of corporate carbon accounting [7,8]. Several guides, standards, and norms are available to help organisations disclose information about environmental performance and carbon performance [4]. The most widely used accounting tool is the Greenhouse Gas (GHG) Protocol, serving as a standard for measuring and reporting organisational level direct and indirect greenhouse gas emissions [9]. The GHG Protocol Initiative is a multi-stakeholder partnership of businesses and NGOs, governments, and others convened by the World Resources Institute (WRI), a global research non-profit organisation, and the World Business Council for Sustainable Development (WBCSD), a Geneva-based coalition of 170 international companies. The GHG Protocol Initiative launched in 1998, and the mission is to develop internationally accepted greenhouse gas accounting and reporting standards for business and to promote their broad adoption [10,11].

Although the issue of carbon accounting is widely addressed in the literature, its level of integration in corporate practice varies greatly between businesses and regions. In general, all Environmental, Social, and Governance (ESG) information is gaining significance amongst capital markets and other stakeholder groups, which leads to a financially material effect on company valuations [12]. EU directives set in 2015–2020 are putting pressure on the car industry to meet CO2 emission targets, with potentially significant economic and financial consequences due to the fines that can be imposed for non-compliance [13]. The findings of Szász et al. suggest that even if strategy-driven sustainability practices lead to improved environmental and social performance, these improvements are not reflected in the short-term financial performance of automotive companies [14]. Besides governance and internal assessment (financial materiality or risk) of sustainability-related operations, corporate reporting is also an issue. It means a great effort is required by organisations to ensure that ESG disclosures are meeting quality standards that offer a systematic approach to presenting sustainability information [15] and to mitigate concerns regarding the presentation of non-existent sustainability-related performance [16,17]. Accounting and reporting for GHG emissions can be considered a critical factor in the valuation of automotive companies due to their environmental impacts, such as global warming potential, stratospheric ozone depletion, ecotoxicity and human toxicity, and air quality [18].

2.2. Development of Digital Reporting for Sustainability

Among other internal corporate procedures, sustainability measurement and reporting were affected by the emergence of big data solutions by new taxonomy concepts, new sensory measurement technologies, and the need for transparent disclosures and open discourse [19].

With the traditional unstructured sustainability information format, the measurement of indicators is challenging due to their inconsistent nature between reporting years and entities. Quality assessment of emission-related disclosure can be based on composite indices; however, their reliance is limited due to information loss during the aggregation step, dependencies among criteria, and scoring of qualitative indicators [20]. Due to the textual format of the information, terminology for basic sustainability criteria needs to be standardised as well. Many metrics, indicators, and criteria are thematically overlapping and formulated in different wordings in disclosures [20]. The eXtensible Business Reporting Language (XBRL), as an emerging international business reporting standard, serves as a technical framework for the integration process based on electronic tags for each item of data. Additionally, these specific XBRL tags should be embedded in an interoperable way between the financial and sustainability reports, or comprehensively in an Integrated Report (IR). The disclosed data’s design will enable sustainability Key Performance Indicators (KPIs) to be automatically retrieved and reviewed by computer software [21]. Entity-relevant facts are tied to concepts in one or more relevant taxonomies, therefore the complexity of reported information can be enhanced with the embedded narrative explanation of quantitative items within the text [22].

Efimova et al. consider XBRL as the formation of various reporting sources of financial and accounting nature (IFRS, stock exchange listing requirements, managerial accounting systems, Integrated Reporting frameworks), big data, and other disclosures (i.e., sustainability) [23]. The history of existing sustainability taxonomies and methodological questions of currently developed taxonomies were addressed by Beerbaum and Puaschunder, where disclosures of carbon emissions serve as one of the main transition risks [24].

The integration of sustainability standardisation into management accounting control needs to take a strategic focus, as previously companies mainly collected data for lagging indicators [25]. Digitally unified reporting (e.g., XBRL) provides a digital enhancement both to data management and standardised reporting as a twin-track approach to sustainability management [26]. Reporting in such a digital format enables big data that can be used as part of managerial decision-making in the form of predictive tools for reducing environmental pressure [27]. Souza and da Silva presented an integration framework adding the Global Reporting Initiative (GRI) disclosure recommendations into sustainability information reported in the XBRL format usable in analysis and audit processes [28]. As an example for technical usage, the United States Environmental Protection Agency (EPA) published a public database of 2019 Greenhouse Gas (GHG) emissions from large facilities of the U.S., requiring reporters to use its XML-based reporting platform [29].

2.3. Theoretical Models for Corporate Carbon Management

With a comprehensive approach to understanding its role in business models, Suk distinguished 5 stages of carbon management [2]. Stage 1, the passive strategy, is the basic level at which companies may recognise or become aware of the need for energy management, which is limited to energy conservation and management. Stage 2 is the reactive strategy, which involves measuring an organisation’s energy and carbon footprint and implementing an emissions reduction strategy based on international standards. Stage 3, the defensive strategy, is the stage of the process where companies assess their internal options to reduce GHG emissions and respond to government regulations by setting up units or departments. Stage 4 is the adaptative strategy, in which companies seek ways to optimise their carbon emissions potential. They are implementing more innovative carbon management, e.g., by publishing carbon emissions reports. The rationale for corporate carbon reporting can be financial, as well as to differentiate from competitors and gain recognition. Strategies at this stage are more concerned with stakeholders, investors, and consumers. Stage 5 is the proactive strategy, characterised by optimising the trade-offs between costs, time, and carbon emissions, based on accumulated information and solutions, integrating carbon and financial data to deliver financially optimised sustainable business improvements. This phase also involves companies identifying opportunities with the highest return on investment through strategy development and implementation that goes beyond regulations.

According to Ibrahim et al., the number of publications on CO2 management decision making has increased especially in the last decade (2010–2020), with a significant increase in 2017 [30], especially in the automotive sector during the introduction of the Worldwide harmonised Light-duty Test Procedure (WLTP) [31], that consists of several customised models, tools, methods, and frameworks that have been developed to support CO2 management decisions. Similarly, Multi-Criteria Decision-Making (MCDM) methodologies can be used by automotive OEMs to reconcile interrelated decision criteria to make Pareto-optimal decisions [30,32].

Wahyuni and Ratnatunga studied that companies, regardless of the industry type, make choices on allocating scarce resources in their internal corporate carbon management practices [33]. To provide theoretical grounding, the Resource-based View (RBV) was adapted that by prior literature understands companies as first, a bundle of productive resources, and second, an administrative framework that coordinates resource deployment. Their results suggest that traditional organisations, which see business and carbon economics as separate domains, adapt passively, whereas proactive firms are characterised by a holistic approach. They effectively integrate carbon-aware thinking into their business practices for higher and greener profits. The theory of RBV was applied in more studies sustainability-related studies to determine new factors influencing competitive advantage. Zhang et al. analysed the transformation of unique internal and external resources in electric battery supply chain processes [34]. The management of resources was mainly discussed from the perspective of green human resource management practices, and hence was connected to the Social and Governance pillars of ESG reporting [35,36,37]. Rotjanakorn et al. warned however that the theory focuses on the management of resources that are available under normal conditions in the automotive industry [38], therefore dynamic technological development might trigger unexpected resource management.

RBV theory’s application in carbon management research was also contributed to by Shibin et al. with the inclusion of legislated standards for carbon emission, and threats associated with environmentally irresponsible behavior as coercive pressures on positive environmental performance [39]. Methodological research of internal resource measurement was extended by environmental constraints (pollution prevention, product stewardship, and clean technology) by De Stefano et al. to support CO2 emissions measurement [40]. At the same time, recent findings of Bocken and Short address the issues concerning unsustainable business models of the transportation industries [41]. Business models of automotive companies build on the necessity of fossil-fuel-powered transportation, profit from global value chains, and make use of technological investments without correctly pricing environmental impact and stimulation of further fossil-fuel use. Micek et al. analysed the market opportunities and regional competitiveness of automotive firms [42] assuming the aim of German development of Central European automotive manufacturers being to mostly acquire better political and organisational capabilities, which implies the lack of integration of sustainability in business models regarding regional development. In summary, based on the underlying principle of the RBV theory concerning the allocation of resources, carbon accounting, including the release of regular reports on emission data [2] among other factors influence corporate competitiveness. Based on the literature, the RBV theory can be used to distinguish between companies in terms of their level of carbon management.

3. Materials and Methods

For this study, we analysed the biggest three automotive Original Equipment Manufacturers (OEMs) by 2018 net sales revenues [43]. The three selected company groups are the Bayerische Motoren Werke (BMW) AG, Daimler AG, and Volkswagen AG, located in Germany and operating in the passenger cars and other motor vehicle markets. In the European automotive sector, Germany holds a significant leading position, with 579.9 EUR billion of revenues and 46.3% of the total European automotive manufacturing revenues. In 2018, Germany also accounted for 32.2% of the total value of EU exports in automotive products [43]. In Table 1, the most important financial and economic data were listed of the selected three company groups. Due to their high production volume, the selected OEMs have a major impact on the sustainability of automotive manufacturing processes on a global level, along with their extensive supply chains.

Table 1.

Consolidated financial and economic data of sample companies, 2020.

A qualitative content analysis based on the Global Reporting Initiative (GRI) and Sustainability Accounting Standards Board (SASB) standards was carried out on the reported sustainability information of the companies on a 5 year (2016–2020) scale with the sources presented in Table 2. Sustainability reports were primarily used, supplemented with additional information and datasets available on official company websites. In general, the data held an unstructured textual format incorporating external links to online and downloadable data. Based on the samples, the efforts towards compliance to multiple standard systems resulted in an overwhelming stream of information mixed between management, operational, and sustainability facts, decreasing comparability. Notably, ongoing standard-setting discussions and regulatory activity are aiming to solve the current issue with the use of XBRL.

Table 2.

Sustainability standards and disclosure used in the content analysis.

Based on the results of Wahyuni and Ratnatunga [33] regarding contextual factors of carbon strategy adoption by the use of the contingent RBV theory, information disclosed in the sample of reports serves as an official presentation of resource allocation towards different carbon management activities. We investigated whether the automotive companies under study are at the same or different levels of adoption of a corporate carbon strategy based on the proposed framework of Suk [2]. The following questions were examined: Did the automotive companies studied reach at least Stage 4 during the observed period? What motivations led them to enter Stage 4? As the analysed automotive companies carry out their production processes in many countries, we reviewed them through the prior assumption that regional differences in emissions exist and are reflected in sustainability reporting.

As an additional factor, we added relevance and clarity of information parameters to the corporate carbon management model. Based on our hypothesis, the higher stage of the carbon management model presents more relevant and clear information. In other words, the relevance and clarity of information are in direct proportion to the carbon management stages. Based on the findings of Appendix A, we developed a checklist for the testing of the conditions of relevance (R) and clarity (C) of sustainability information. Each of the disclosures was reviewed following the reported references to standards to either the main text or external links. Condition R was considered fulfilled (marked with “X”) when disclosure (main text or intra-document/external reference) was linked to the relevant sustainability (GRI or SASB) standard. Notably, due to the change in standard identifier codes in 2016, some companies used the older version in that year. Condition C was considered fulfilled (marked with “X”) when disclosure contained the clearly definable numeric or textual value (that provides comparability and a level of standardisation according to the relevant standards) and unit of measure. Notably, the condition was not fulfilled, with percentage values of yearly changes displayed without the absolute base value of the comparison. The applied conditions ensure the representation of reality in terms of the quality of reported information. In the analysis of both Conditions R and C, the related textual data were classified in either category of containing (1) verifiable and measurable data, (2) not verifiable data but fitting reporting practice, or (3) data that is not validated nor fitting reporting practice.

As part of the study, we applied text-mining aided methods to attempt to standardise textual data of sustainability standards and reports. A combination of manual content analysis and Natural Language Processing (NLP) tasks were carried out, of which the latter used the Provalis WordStat 8.0.33 software [47]. As a methodological guideline, the prior literature of [48,49,50] was used in the topic of text-mining-based evaluation of sustainability reports. The content analysis steps included (1) textual data retrieval from sustainability reports and supplementary material (additional reference tables, standards) (2) processing of textual data of standards to identify search criteria in reports, (3) quantitative content analysis based on the defined standard categorisation, (4) observation of sustainability disclosure occurrence in main report body text, (5) comparison between years and companies following research questions that were previously discussed.

4. Results

We presented the results in three subtopics. Firstly, we aimed to develop a standard system for the evaluation of Carbon Accounting using corporate sustainability reports. Secondly, we carried out a content analysis on the sample of 3 companies and 5 years of sustainability reports focusing on carbon disclosures and presented the additional parameters of relevance and clarity of data. Thirdly, we reviewed the regional factor of the reported information.

4.1. CO2 and Financial Disclosures’ Compliance to Legal Obligations and Standard (GRI, SASB) Directives

In Table 3, keywords connected to Carbon Accounting are presented based on the GRI Standards Glossary 2020 and SASB Automotive (identified as TR-AU) disclosures. In the next step, the frequencies of the words and phrases were reviewed in every GRI standard individually to determine the relevant standards and disclosures discussing the emission of CO2 and other GHG gases, and propose methodologies of measurement.

Table 3.

Text mining keywords for Carbon Accounting in sustainability reports.

We reviewed all standards proposed by the GRI and SASB focusing on their information content on CO2 emission for automotive companies. As opposed to GRI standards, SASB provides a package specifically for the automotive industry. All textual data of individual standards were reviewed with text-mining aided frequency analysis using snowball-stemming as the text preprocessing methodology. Those standards indicated by the high frequencies of keywords mentioned in Table 3 underwent a final manual selection process. The standards containing valuable guidelines for reporting disclosures for CO2 emissions are listed in Table 4, including some indicative examples for keywords frequencies. Notably, not all standards included keywords directly; GRI 307 however was selected due to the growing significance of legally required compliance to standards.

Table 4.

Selected non-financial reporting standards relevant in reporting CO2 emissions.

Each organisation is responsible for the quality of the information published in corporate reports. The information content of annual reports and financial statements are often limited to the most necessary supplementary information due to the obligation to pass financial audit processes, but this will only be the case for sustainability statements after the future EU legislation is implemented [51]. For instance, the GRI 201-2 disclosure (Financial implications and other risks and opportunities due to climate change) as an ideal set of indicators proving traceability to financial results was under-represented in all 2020 sustainability reports and supplementary GRI index tables. In Table 5, information content is presented where reference to standards was unavailable, while some qualitative details were available in the statements of Daimler and Volkswagen. However, the actual financial impacts in the reporting period were not represented in any text parts or supplementary external material.

Table 5.

Financial traceability by GRI 201-2 disclosures on CO2-related risks, 2020.

4.2. Emission Measurement in Corporate Reporting

After reviewing the carbon emissions model of Suk, an adaptation to the reporting scheme was developed to compare compliance or deviation from the model [2]. Upon the manual review of the corporate sustainability reviews information by the proposed indicators of Carbon Management Activities (CMAs) as presented in Appendix B, it can be implied that the observed companies are at stages 4 and 5 of carbon management. Their disclosed business models reach a stage 4 (accommodative) strategy, as stand-alone or integrated carbon reports were published. The time of adaptation precedes the currently relevant regulatory context [52], i.e., the first carbon report publication date (that should not be taken into account) is before 2016. Companies may disclose the information either because it is financially significant (so they have a legal obligation to disclose it) or because it differentiates them from competitors in a positive way for stakeholders. The companies with the same geographical scope of operation (i.e., operating in Germany) started disclosing certain information before the analysed period, which suggests a lack of external pressure. However, certain disclosures vary in information content, as presented in the sections below.

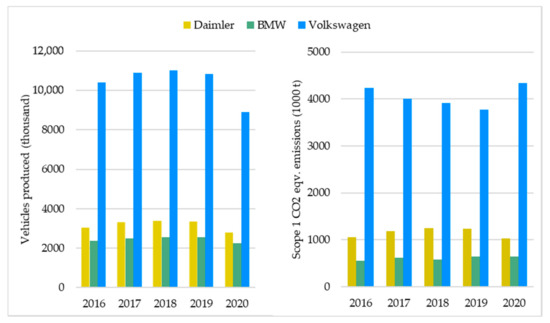

The highest stage strategy (stage 5) is proactive, where compliance with a public expectation or standard not being the reason for disclosure. Another important element is that the company integrates carbon emissions data into its financial reporting, i.e., creates a link between financial and non-financial data. At this stage, it can also be observed that the company is adapting to the internal market, which it can exploit to gain a competitive advantage. The fulfillment of requirements of the strategic stage is not possible with current reporting systems, as there are no common measurements of such internal processes. To gain more insight into the nature of emissions, the links between vehicle production and different scopes of CO2 emissions were reviewed. In Figure 1 the negative impact of the ongoing pandemic on production volumes can be seen, along with the changes in the direct emission values.

Figure 1.

Vehicles produced and direct (Scope 1) CO2 emissions, 2016–2020.

From 2016 to 2018, steady growth was reported in production volumes with an average 1.35% drawback in 2019. In 2020, Q4 productions were in many cases disrupted or held back which resulted in an average 16.59% decrease in vehicles produced for the year. In contrast, Scope 1 emissions directly controlled by companies stagnated for BMW and moved conically for Daimler during the years, but showed a 15.12% increase for Volkswagen. As the information on the emissions by scope per vehicle was reported in “custom” formats—therefore low-quality conditions—we included the calculations of Table 6 to review lifecycle emissions of produced vehicles as well.

Table 6.

Reported emissions by scope, per vehicle produced, tons of CO2 equivalents.

It can be seen that while Scope 2 emissions have seen a significant reduction (an average of 20.42% per year), Scope 1 and Scope 3 emissions per vehicle varied in trends. According to the definition of the GRI 305: Emissions standard, other indirect emissions are a consequence of an organisation’s activities but occur from sources not owned or controlled by the organisation [53]. Both upstream (e.g., value-chain operations, business travel, or waste generated in operations) and downstream (e.g., distribution, use of products sold, or end-of-like treatment) emissions are included by the indicator.

A total of 20 disclosures were examined from the checklist, of which a summary table was created consolidating CO2 disclosures by companies and years, presented in Table 7. Typically an advancement in compliance with the conditions was seen other than in the case of Volkswagen, where earlier years (2017–2018) provided compliance with a higher number of standards (GRI, SASB). This trend of decreasing relevance and clarity over the years of Volkswagen regarding the CO2 emission in sustainability reports might be related and can be a logical consequence to the fact of the legal proceedings happening in these years. The most accurately reported disclosures were the GRI 305-1/2/3 emission standards fulfilling both relevance and clarity criteria.

Table 7.

Compliance of CO2 disclosures with the relevance and clarity conditions in %, 2016–2020.

4.3. Reporting on a Regional Scale: Do Companies Deliver Regional Distinction in Emission Disclosures?

As the GRI 305: Emissions standard recommends: where it aids transparency or comparability over time, provide a breakdown of the GHG (Scope 1, 2 and 3) emissions by [53]:

- business unit or facility;

- country;

- type of source (stationary combustion, process, fugitive);

- type of activity.

Automotive OEMs typically operate with a wide range of suppliers ranging from Tier 1–3. Germany as the European centre of the automotive industry, and especially the analysed three biggest OEMs by realised sales revenues, can be considered as a centre of supplier chains involving various manufacturing processes before the finished product. However, regional differentiation in emission data was less commonly discussed. As an example, Volkswagen provided differentiation in the number of vehicles produced in the last 5 years between Germany and other countries (in an aggregated format); however, this was provided separately from the sustainability data in the annual report. All of the observed years’ production complete abroad was above 87%, therefore such a differentiation would be also recommended to comply with future sustainability regulations and the transition towards a transparent carbon management system.

The introductory study of Thun and Müller reviewed German automotive manufacturers from the viewpoint of green supply chains [54]. Their findings revealed that at the time, OEMs were aware of environmental issues but were moving slowly towards realise the full potential of green supply chains, with the goal mainly of complying with legal regulations. Green supply chains were not viewed as increasing a comparative advantage. The more common ecological programs are mostly internally focused on corporate strategic planning, not covering environmental effects in different regions of operations. According to Böttcher and Müller, for German automotive suppliers, firm size played a significant role in the perceived importance of CO2 emissions reduction [55], based on which the analysed companies are in a favourable position.

5. Conclusions and Discussion

The current study serves as a contribution to the literature review on the non-financial reporting disclosures of automotive companies, especially on the topic of CO2 emissions. Prior work has focused mainly on the industrial side of the topic in the form of questionnaires on the perceived importance of sustainability disclosures from the corporate side. Our study attempted to cover the area from the viewpoint of reviewing sustainability reports and connected material that acts as legal obligation for the analysed German automotive manufacturers. We provided an assessment of currently available sustainability standards that play a role in the corporate reporting of CO2 emissions, along with their proposals for measurement methodologies. In contrast to that, we also carried out a content analysis on the sample’s reports in the last 5 year period.

Our research objective was to generate a validation methodology scale of carbon accounting information disclosed in corporate sustainability reports. To this end, based on the results presented in Section 4.2, Suk’s (2018) methodology does not show significant differences between the German car manufacturers studied. Problems in recording sustainability information are not apparent based on the methodology for internal management processes, showing that despite minor differences, the companies are at the same sustainability stage. Almost all of the activities required by Stage 4 are fulfilled and reported, but most of the requirements of Stage 5 are not presented. Disclosing textual information that differs in quality and clarity is, in the RBV theory’s view, a way of communicating the provision of resources and its role in internal carbon management that includes its CO2 emissions performance. For these high-level CO2 abatement activities, companies do not allocate resources based on the descriptions in their annual reports.

In addition to the quality and clarity of the sustainability information reported, there is a relatively clear difference in the absolute Scope 1–2–3 CO2 emissions between the companies analysed. While Scope 1–2 is a well-measured and manageable category due to its direct and indirect link to the manufacturing process, Scope 3 is outside the scope of manufacturing activities. The communication of information on resources is the weakest in this case, and although the criterion for reporting figures is met, there is no improvement in quality between years. Based on the conclusions, we provide a discussion of three topics as follows.

5.1. Reliability of Sustainability Information

External and intra-document references were not consistent in all cases and could not be followed from the viewpoints of relevance to international sustainability standards, and clarity in proposed information content. As such, multiple pages of text were assigned to individual standards, as well as in reverse, i.e., multiple standards were assigned to a multiple page text without assigning a specific “fact” value to them. This can be explained by internal sustainability assessments of German automakers mainly being used for reporting, instead of retrospectively evaluating development, and using findings to improve marketed products [56]. Reported units of KPIs are rarely consistent within an industry, especially for metrics that are harder to quantify [57]. The possibility of customised emission indicators (changes between direct/indirect and Scope 1/2/3 emission approaches) decreases comparability. Gallego–Álvarez identified certain environmental indicators that are included in the GRI 305 (Emissions) standard and compared their presence in the analysed sample [58]. Certain sectors such as raw materials pay more attention overall to the GRI 300 environmental indicators compared to other industries. In addition, Ordonez–Ponce and Khare attempted to harmonise GRI 300 disclosures and Sustainable Development Goals (SDGs) established by the UN, with findings of Germany being among the best performers with a consensus value of 90% of total emission standards reported [59]. In our study, the most commonly referenced standards and disclosures were highlighted in the carbon reporting of the biggest European automotive companies, with the addition of the relevance and clarity factors as part of the evaluation concept. Both factors can be strengthened by the steady development towards XBRL format reporting that supports the removal of replicated or backup accounting data—both financial and non-financial—to build a unified system of collecting and processing information [60]. We propose the further research area of integrating the five stage model of carbon management activities in text-mining based evaluation. Based on the methodological experience gained, disclosures on carbon accounting could be analysed on a larger scale, involving the entire population of automotive manufacturers on a certain regional level. Such research would provide essential contribution in the form to the development of the ongoing regulatory process of sustainability reporting in the EU.

5.2. Role of Integrated Reporting and Digitalalisation of Reports

Integrated reporting is gaining traction as BMW has published its first integrated annual report in 2020, containing both financial and non-financial information. Considering the expected arrival of digitally standardised reporting (XBRL, or ESEF as called by the European Commission) this implies corporate opening to clearly defined linkages between the two kinds of information with the double materiality concept [51]. Currently, there is an ongoing regulatory discussion regarding draft standards by the responsible organisation of the European Union, the European Financial Reporting Advisory Group (EFRAG). In April 2021, the technological recommendations were published along with a timetable for the development of current sustainability reporting standards [61]. The regulation process aims to review and develop the current European Non-Financial Reporting Directive (NFRD) active since 2018 [52]. In Appendix A, a detailed description was provided of the relevant sustainability standards and disclosures to be used and adopted by future legislation. The result serves as the basis for further evaluation of corporate sustainability information and can be used as a validator for similar content analyses carried out in the current study.

5.3. Regional Assessment of Emissions in Reporting

The regional questions of emissions reporting are generally not addressed in scientific literature; however, some proposals are given that can be reflected in regionalisation. Mitigation of emissions could be carried out by evaluating which improvements to car components can most reduce their environmental impacts [3]. The issue relies on internal processes; however, manufacturing of car parts is carried out in different specialised manufacturing units globally. Carbon accounting, as part of corporate reporting, is capable of recognising aggregate emission of manufacturing processes by regions, therefore the mitigation of certain environmentally overloaded regions is possible, but its economic benefits are questionable and case-dependent.

The conceptual framework of Böttcher and Müller categorises the drivers of low-carbon operations to (1) low carbon products, (2) low carbon production, and (3) low carbon logistics [55]. These categories are available to link existing internal managerial accounting systems to sustainability costs from a regional perspective. Additionally, XBRL has the potential to embed land cover data, e.g., GIS data on ecosystem extent and condition to offer a feasible solution to regional linkages [62].

As a future research area, we aim to extend the methodology of the current study to a wider international sample of automotive OEMs and to develop the hereby presented relevance and clarity conditions of sustainability disclosures to a multivariate model. With an extended data source, differences in carbon accounting practices and their reporting could be detected on the level of countries or continents.

Author Contributions

Conceptualisation, Á.T., C.S. and A.S.; methodology, Á.T., C.S. and A.S.; software, A.S.; validation, Á.T. and C.S.; formal analysis, A.S.; investigation, Á.T.; resources, C.S. and A.S.; writing—original draft preparation, A.S. and C.S.; writing—review and editing, Á.T. and C.S.; visualization, A.S.; supervision, Á.T. and C.S.; project administration, Á.T.; funding acquisition, Á.T. All authors have read and agreed to the published version of the manuscript.

Funding

The research presented in this paper was funded by the “National Laboratories 2020 Program—Artificial Intelligence Subprogram—Establishment of the National Artificial Intelligence Laboratory (MILAB) at Széchenyi István University (NKFIH-870-21/2020)” project.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

All data was retrieved from the official website of publicly available corporate reports (annual and sustainability reports) of the analysed companies.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses, or interpretation of data; in the writing of the manuscript, or in the decision to publish the results.

Appendix A

Table A1.

Collection of standards and disclosures in corporate reporting of emissions.

Table A1.

Collection of standards and disclosures in corporate reporting of emissions.

| ID | Standard/Disclosure Description | Proposed Unit of Measure/Methods |

|---|---|---|

| GRI 201 | Economic Performance 2016 | |

| 201-2 | Financial implications and other risks and opportunities due to climate change | Carbon capture and storage; Fuel switching; Use of renewable and lower carbon footprint energy; Improving energy efficiency; Flaring, venting, and fugitive emission reduction; Renewable energy certificates; Use of carbon offsets. |

| GRI 302 | Energy 2016 | |

| 302-1 | Energy consumption within the organisation | Joules, watt-hours, or multiples |

| 302-2 | Energy consumption outside of the organisation | |

| 302-3 | Energy intensity | Intensity ratios: products, services, sales (energy consumed per unit) Organisation-specific metrics (denominators): units of product, production volume (MWh), plant size, employee number, monetary units |

| 302-4 | Reduction of energy consumption | Joules or multiples, including base year or baseline for reductions |

| 302-5 | Reductions in energy requirements of products and services | |

| GRI 305 | Emissions 2016 | |

| 305-1 | Direct (Scope 1) GHG emissions | Metric tons of CO2 equivalent; Base year for calculation; Source of emission factors and GWP rates used |

| 305-2 | Energy indirect (Scope 2) GHG emissions | |

| 305-3 | Other indirect (Scope 3) GHG emissions | |

| 305-4 | GHG emissions intensity | Intensity ratios: products, services, sales (in metric tons of CO2 emission per unit) Organisation-specific metrics (denominators): units of product, production volume (MWh), plant size, employee number, monetary units |

| 305-5 | Reduction of GHG emissions | Metric tons of CO2 equivalent; Base year for calculation; Scope 1/2/3 categorisation |

| 305-6 | Emissions of ozone-depleting substances (ODS) | Metric tons of CFC-11 equivalent |

| 305-7 | Nitrogen oxides (NOX), sulfur oxides (SOX), and other significant air emissions | Kilograms or multiples in standard categories of air emissions |

| GRI 307 | Environmental Compliance 2016 | |

| 307-1 | Non-compliance with environmental laws and regulations | Total monetary value of significant fines; Total number of non-monetary sanctions; Cases brought through dispute resolution mechanisms. |

| SASB | Automobiles | |

| TR-AU-410a.1 | Sales-weighted average passenger fleet fuel economy, by region | Mpg, L/km, gCO2/km, km/L |

| TR-AU-410a.2 | Number of (1) zero-emission vehicles (ZEV), (2) hybrid vehicles, and (3) plug-in hybrid vehicles sold | Number |

| TR-AU-410a.3 | Discussion of strategy for managing a fleet fuel economy and emissions risks and opportunities | n/a |

| TR-AU-440a.1 | Description of the management of risks associated with the use of critical materials | |

| TR-AU-000.A | Number of vehicles manufactured | Number |

| TR-AU-000.B | Number of vehicles sold |

Appendix B

Table A2.

Description of carbon management activities (CMAs) and public availability in SRs, 2020.

Table A2.

Description of carbon management activities (CMAs) and public availability in SRs, 2020.

| Item [2] | Carbon Management Activities | Values (0/1) | |||

|---|---|---|---|---|---|

| BMW | Daimler | VW | |||

| Stage 1 | CMA01 | Collecting information on policy related to energy savings and GHG emissions reduction | 1 | 1 | 1 |

| CMA02 | Regular in-house training program for energy saving and GHG emission reduction | 1 | 1 | 1 | |

| CMA03 | Encouraging daily energy-saving activities in the office (e.g., turning off lights) | 1 | 1 | 1 | |

| CMA04 | Participating in training programs for energy saving and GHG emissions reduction held by the government/local government | 1 | 1 | 1 | |

| Stage 2 | CMA05 | Short and long-term targets for energy savings and GHG emission reductions in place | 1 | 1 | 1 |

| CMA06 | Analysing energy use and GHG emissions to identify potential areas for energy savings and emissions reduction | 1 | 1 | 1 | |

| CMA07 | Installing monitoring equipment on energy-consuming facilities | 1 | 1 | 1 | |

| CMA08 | Enhancing daily facility maintenance for energy saving and GHG emissions reduction | 1 | 1 | 1 | |

| Stage 3 | CMA09 | Setting up an internal standard for energy savings and GHG emissions reduction management | 1 | 1 | 1 |

| CMA10 | Establishing a unit or department for emissions trading | 0 | 0 | 0 | |

| CMA11 | Purchase new production facilities to save energy and reduce GHG emissions | 1 | 1 | 1 | |

| CMA12 | Investing in R&D to improve production processes for energy savings and emission reduction | 1 | 1 | 1 | |

| Stage 4 | CMA13 | Enhancing optimisation in transporting materials and goods | 1 | 1 | 1 |

| CMA14 | Making adjustments to the energy mix to use more clean energy sources | 1 | 1 | 1 | |

| CMA15 | Releasing sustainability reports regularly that contain data for energy consumption and GHG emissions | 1 | 1 | 1 | |

| CMA16 | Set up strategic carbon management (plan-do-check-act) | 1 | 1 | 1 | |

| Stage 5 | CMA17 | Setting up a plan and allocating budget for purchasing permits and trading | 0 | 0 | 0 |

| CMA18 | Establishing decision-making process for carbon trading (e.g., purchase, sell, price projection, etc.) | 0 | 0 | 0 | |

| CMA19 | Establishing carbon management strategy based on regular analysis of carbon market | 1 | 1 | 1 | |

| CMA20 | Adopting a green or carbon management accounting system | 0 | 0 | 0 | |

Note: Values of 0 indicate the lack of representation, while 1 indicate clear representation of information on CMAs. Source: Suk (2018) [2], Sustainability Reports, 2020.

References

- Csutora, M.; Harangozo, G. Twenty Years of Carbon Accounting and Auditing—A Review and Outlook. Soc. Econ. 2017, 39, 459–480. [Google Scholar] [CrossRef]

- Suk, S. Determinants and Characteristics of Korean Companies’ Carbon Management under the Carbon Pricing Scheme. Energies 2018, 11, 966. [Google Scholar] [CrossRef]

- Spreafico, C. Can Modified Components Make Cars Greener? A Life Cycle Assessment. J. Clean. Prod. 2021, 307, 127190. [Google Scholar] [CrossRef]

- Radu, C.; Caron, M.-A.; Arroyo, P. Integration of Carbon and Environmental Strategies within Corporate Disclosures. J. Clean. Prod. 2020, 244, 118681. [Google Scholar] [CrossRef]

- Barney, J. Firm Resources and Sustained Competitive Advantage. J. Manag. 1991, 17, 99–120. [Google Scholar] [CrossRef]

- Huo, B.; Gu, M.; Wang, Z. Green or Lean? A Supply Chain Approach to Sustainable Performance. J. Clean. Prod. 2019, 216, 152–166. [Google Scholar] [CrossRef]

- Schaltegger, S.; Csutora, M. Carbon Accounting for Sustainability and Management. Status Quo and Challenges. J. Clean. Prod. 2012, 36, 1–16. [Google Scholar] [CrossRef]

- Stechemesser, K.; Guenther, E. Carbon Accounting: A Systematic Literature Review. J. Clean. Prod. 2012, 36, 17–38. [Google Scholar] [CrossRef]

- Harangozo, G.; Szigeti, C. Corporate Carbon Footprint Analysis in Practice—With a Special Focus on Validity and Reliability Issues. J. Clean. Prod. 2017, 167, 1177–1183. [Google Scholar] [CrossRef]

- WRI; WBCSD. The Greenhose Gas Protocol—A Corporate Accounting and Reporting Standard (Revised Edition); WRI and WBCSD: Geneva, Switzerland, 2004; p. 116. [Google Scholar]

- WRI; WBCSD. The Greenhouse Gas Protocol—Corporate Value Chain (Scope 3); WRI and WBCSD: Geneva, Switzerland, 2011; p. 152. [Google Scholar]

- Taliento, M.; Favino, C.; Netti, A. Impact of Environmental, Social, and Governance Information on Economic Performance: Evidence of a Corporate ‘Sustainability Advantage’ from Europe. Sustainability 2019, 11, 1738. [Google Scholar] [CrossRef]

- Morgadinho, L.; Oliveira, C.; Martinho, A. A Qualitative Study about Perceptions of European Automotive Sector’s Contribution to Lower Greenhouse Gas Emissions. J. Clean. Prod. 2015, 106, 644–653. [Google Scholar] [CrossRef]

- Szász, L.; Csíki, O.; Rácz, B.-G. Sustainability Management in the Global Automotive Industry: A Theoretical Model and Survey Study. Int. J. Prod. Econ. 2021, 235, 108085. [Google Scholar] [CrossRef]

- AICPA; CIMA. Key Actions for Establishing Effective Governance over ESG Reporting; Chartered Institute of Management Accountants: London, UK, 2021. [Google Scholar]

- Kravchenko, M.; Pigosso, D.C.A.; McAloone, T.C. Towards the Ex-Ante Sustainability Screening of Circular Economy Initiatives in Manufacturing Companies: Consolidation of Leading Sustainability-Related Performance Indicators. J. Clean. Prod. 2019, 241, 118318. [Google Scholar] [CrossRef]

- Szennay, Á.; Szigeti, C.; Kovács, N.; Szabó, D.R. Through the Blurry Looking Glass—SDGs in the GRI Reports. Resources 2019, 8, 101. [Google Scholar] [CrossRef]

- Jasiński, D.; Meredith, J.; Kirwan, K. A Comprehensive Framework for Automotive Sustainability Assessment. J. Clean. Prod. 2016, 135, 1034–1044. [Google Scholar] [CrossRef]

- Seele, P. Envisioning the Digital Sustainability Panopticon: A Thought Experiment of How Big Data May Help Advancing Sustainability in the Digital Age. Sustain. Sci. 2016, 11, 845–854. [Google Scholar] [CrossRef]

- Büyüközkan, G.; Karabulut, Y. Sustainability Performance Evaluation: Literature Review and Future Directions. J. Environ. Manag. 2018, 217, 253–267. [Google Scholar] [CrossRef]

- Bonsón, E.; Bednárová, M. CSR Reporting Practices of Eurozone Companies. Rev. Contab. 2015, 18, 182–193. [Google Scholar] [CrossRef]

- Debreceny, R.; Farewell, S.; Piechocki, M.; Felden, C.; Gräning, A. Does It Add up? Early Evidence on the Data Quality of XBRL Filings to the SEC. J. Account. Public Policy 2010, 29, 296–306. [Google Scholar] [CrossRef]

- Efimova, O.; Rozhnova, O.; Gorodetskaya, O. XBRL as a Tool for Integrating Financial and Non-financial Reporting. In Digital Science 2019; Antipova, T., Rocha, Á., Eds.; Advances in Intelligent Systems and Computing; Springer International Publishing: Cham, Switzerland, 2020; Volume 1114, pp. 135–147. ISBN 978-3-030-37736-6. [Google Scholar]

- Beerbaum, D.; Puaschunder, J.M. Towards an XBRL-Enabled Sustainability Taxonomy—A Behavioral Accounting Approach. Spec. Issue J. Appl. Res. Digit. Econ. 2019, 2, 17. [Google Scholar]

- Maas, K.; Schaltegger, S.; Crutzen, N. Advancing the Integration of Corporate Sustainability Measurement, Management and Reporting. J. Clean. Prod. 2016, 133, 859–862. [Google Scholar] [CrossRef]

- Seele, P. Digitally Unified Reporting: How XBRL-Based Real-Time Transparency Helps in Combining Integrated Sustainability Reporting and Performance Control. J. Clean. Prod. 2016, 136, 65–77. [Google Scholar] [CrossRef]

- Seele, P. Predictive Sustainability Control: A Review Assessing the Potential to Transfer Big Data Driven ‘Predictive Policing’ to Corporate Sustainability Management. J. Clean. Prod. 2017, 153, 673–686. [Google Scholar] [CrossRef]

- Souza, D.C.; da Silva, P.C. A Framework for Auditing Xbrl Documents Based on the Gri Sustainability Guidelines. Adv. Intell. Syst. Comput. 2018, 558, 523–531. [Google Scholar] [CrossRef]

- Cong, Y.; Freedman, M.; Park, J.D. Mandated Greenhouse Gas Emissions and Required SEC Climate Change Disclosures. J. Clean. Prod. 2020, 247, 119111. [Google Scholar] [CrossRef]

- Ibrahim, N.; Cox, S.; Mills, R.; Aftelak, A.; Shah, H. Multi-Objective Decision-Making Methods for Optimising CO2 Decisions in the Automotive Industry. J. Clean. Prod. 2021, 314, 128037. [Google Scholar] [CrossRef]

- Pavlovic, J.; Marotta, A.; Ciuffo, B. CO2 Emissions and Energy Demands of Vehicles Tested under the NEDC and the New WLTP Type Approval Test Procedures. Appl. Energy 2016, 177, 661–670. [Google Scholar] [CrossRef]

- Mzougui, I.; Carpitella, S.; Certa, A.; El Felsoufi, Z.; Izquierdo, J. Assessing Supply Chain Risks in the Automotive Industry through a Modified MCDM-Based FMECA. Processes 2020, 8, 579. [Google Scholar] [CrossRef]

- Wahyuni, D.; Ratnatunga, J. Carbon Strategies and Management Practices in an Uncertain Carbonomic Environment—Lessons Learned from the Coal-Face. J. Clean. Prod. 2015, 96, 397–406. [Google Scholar] [CrossRef]

- Zhang, Y.; Rysiecki, L.; Gong, Y.; Shi, Q. A SWOT Analysis of the UK EV Battery Supply Chain. Sustainability 2020, 12, 9807. [Google Scholar] [CrossRef]

- Malik, S.Y.; Cao, Y.; Mughal, Y.H.; Kundi, G.M.; Mughal, M.H.; Ramayah, T. Pathways towards Sustainability in Organizations: Empirical Evidence on the Role of Green Human Resource Management Practices and Green Intellectual Capital. Sustainability 2020, 12, 3228. [Google Scholar] [CrossRef]

- Sobaih, A.E.E.; Hasanein, A.; Elshaer, I. Influences of Green Human Resources Management on Environmental Performance in Small Lodging Enterprises: The Role of Green Innovation. Sustainability 2020, 12, 10371. [Google Scholar] [CrossRef]

- Aidara, S.; Mamun, A.A.; Nasir, N.A.; Mohiuddin, M.; Nawi, N.C.; Zainol, N.R. Competitive Advantages of the Relationship between Entrepreneurial Competencies and Economic Sustainability Performance. Sustainability 2021, 13, 864. [Google Scholar] [CrossRef]

- Rotjanakorn, A.; Sadangharn, P.; Na-Nan, K. Development of Dynamic Capabilities for Automotive Industry Performance under Disruptive Innovation. JOItmC 2020, 6, 97. [Google Scholar] [CrossRef]

- Shibin, K.T.; Dubey, R.; Gunasekaran, A.; Hazen, B.; Roubaud, D.; Gupta, S.; Foropon, C. Examining Sustainable Supply Chain Management of SMEs Using Resource Based View and Institutional Theory. Ann. Oper. Res. 2020, 290, 301–326. [Google Scholar] [CrossRef]

- De Stefano, M.C.; Montes-Sancho, M.J.; Busch, T. A Natural Resource-Based View of Climate Change: Innovation Challenges in the Automobile Industry. J. Clean. Prod. 2016, 139, 1436–1448. [Google Scholar] [CrossRef]

- Bocken, N.M.P.; Short, S.W. Unsustainable Business Models—Recognising and Resolving Institutionalised Social and Environmental Harm. J. Clean. Prod. 2021, 312, 127828. [Google Scholar] [CrossRef]

- Micek, G.; Guzik, R.; Gwosdz, K.; Domański, B. Newcomers from the Periphery: The International Expansion of Polish Automotive Companies. Energies 2021, 14, 2617. [Google Scholar] [CrossRef]

- Schlumbohm, M.; Sánchez, O.; Muñoz-Giraldo, L.; Zeppernick, M. Manufacturing: Automotive Industry—NACE 29; Statista Industry Report—Europe; Statista: Hamburg, Germany, 2020. [Google Scholar]

- BMW Group Investor Relations. Integrated Report and Prior Sustainable Value Reports. Available online: https://www.bmwgroup.com/en/investor-relations/company-reports.html (accessed on 15 June 2021).

- Daimler Sustainability Report 2020: Download Center. Available online: https://sustainabilityreport.daimler.com/2020/servicepages/downloads.html (accessed on 15 June 2021).

- VW Group the Volkswagen Group Sustainability Report 2020. Available online: https://www.volkswagenag.com/en/sustainability/reporting.html (accessed on 15 June 2021).

- Provalis WordStat v8.0.33 [Software]; Provalis Research: Montreal, QC, Canada, 2021.

- Shin, S.-H.; Kwon, O.K.; Ruan, X.; Chhetri, P.; Lee, P.T.-W.; Shahparvari, S. Analyzing Sustainability Literature in Maritime Studies with Text Mining. Sustainability 2018, 10, 3522. [Google Scholar] [CrossRef]

- Valverde-Berrocoso, J.; Garrido-Arroyo, M.d.C.; Burgos-Videla, C.; Morales-Cevallos, M.B. Trends in Educational Research about E-Learning: A Systematic Literature Review (2009–2018). Sustainability 2020, 12, 5153. [Google Scholar] [CrossRef]

- Tóth, Á.; Suta, A.; Szauter, F. Interrelation between the Climate-Related Sustainability and the Financial Reporting Disclosures of the European Automotive Industry. Clean Technol. Environ. Policy 2021. [Google Scholar] [CrossRef]

- O’Se, C.; Holland, C. Corporate Sustainability Reporting Directive: What the New CSRD Means for You; KPMG Ireland: Dublin, Ireland, 2021. [Google Scholar]

- Lai, A.; Stacchezzini, R. Organisational and Professional Challenges amid the Evolution of Sustainability Reporting: A Theoretical Framework and an Agenda for Future Research. MEDAR 2021. ahead-of-print. [Google Scholar] [CrossRef]

- Global Reporting Initiative. GRI 305: Emissions 2016; Global Sustainability Standards Board: Amsterdam, The Netherlands, 2018; ISBN 978-90-8866-108-2. [Google Scholar]

- Thun, J.-H.; Müller, A. An Empirical Analysis of Green Supply Chain Management in the German Automotive Industry. Bus. Strategy Environ. 2010, 19, 119–132. [Google Scholar] [CrossRef]

- Böttcher, C.F.; Müller, M. Drivers, Practices and Outcomes of Low-Carbon Operations: Approaches of German Automotive Suppliers to Cutting Carbon Emissions: Drivers, Practices and Outcomes of Low-Carbon Operations. Bus. Strat. Environ. 2015, 24, 477–498. [Google Scholar] [CrossRef]

- Held, M.; Weidmann, D.; Kammerl, D.; Hollauer, C.; Mörtl, M.; Omer, M.; Lindemann, U. Current Challenges for Sustainable Product Development in the German Automotive Sector: A Survey Based Status Assessment. J. Clean. Prod. 2018, 195, 869–889. [Google Scholar] [CrossRef]

- Bernard, S.; Abdelgadir, S.; Belkhir, L. Does GRI Reporting Impact Environmental Sustainability? An Industry-Specific Analysis of CO2 Emissions Performance between Reporting and Non-Reporting Companies. JSD 2015, 8, 190. [Google Scholar] [CrossRef]

- Gallego-Álvarez, I.; Lozano, M.B.; Rodríguez-Rosa, M. An Analysis of the Environmental Information in International Companies According to the New GRI Standards. J. Clean. Prod. 2018, 182, 57–66. [Google Scholar] [CrossRef]

- Ordonez-Ponce, E.; Khare, A. GRI 300 as a Measurement Tool for the United Nations Sustainable Development Goals: Assessing the Impact of Car Makers on Sustainability. J. Environ. Plan. Manag. 2021, 64, 47–75. [Google Scholar] [CrossRef]

- Astafeva, O.V.; Astafyev, E.V.; Khalikova, E.A.; Leybert, T.B.; Osipova, I.A. XBRL Reporting in the Conditions of Digital Business Transformation. Lect. Notes Netw. Syst. 2020, 84, 373–381. [Google Scholar] [CrossRef]

- EFRAG. Proposals for a Relevant and Dynamic EU Sustainability Reporting Standard-Setting; European Financial Reporting Advisory Group: Brussels, Belgium, 2021. [Google Scholar]

- Houdet, J.; Ding, H.; Quétier, F.; Addison, P.; Deshmukh, P. Adapting Double-Entry Bookkeeping to Renewable Natural Capital: An Application to Corporate Net Biodiversity Impact Accounting and Disclosure. Ecosyst. Serv. 2020, 45, 101104. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).