The Use of Blockchain Technology in Public Sector Entities Management: An Example of Security and Energy Efficiency in Cloud Computing Data Processing

Abstract

1. Introduction

2. Results and Discussion

2.1. Blockchain Technology—Overview

2.2. Methodology

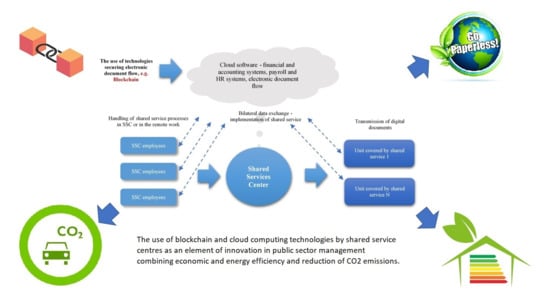

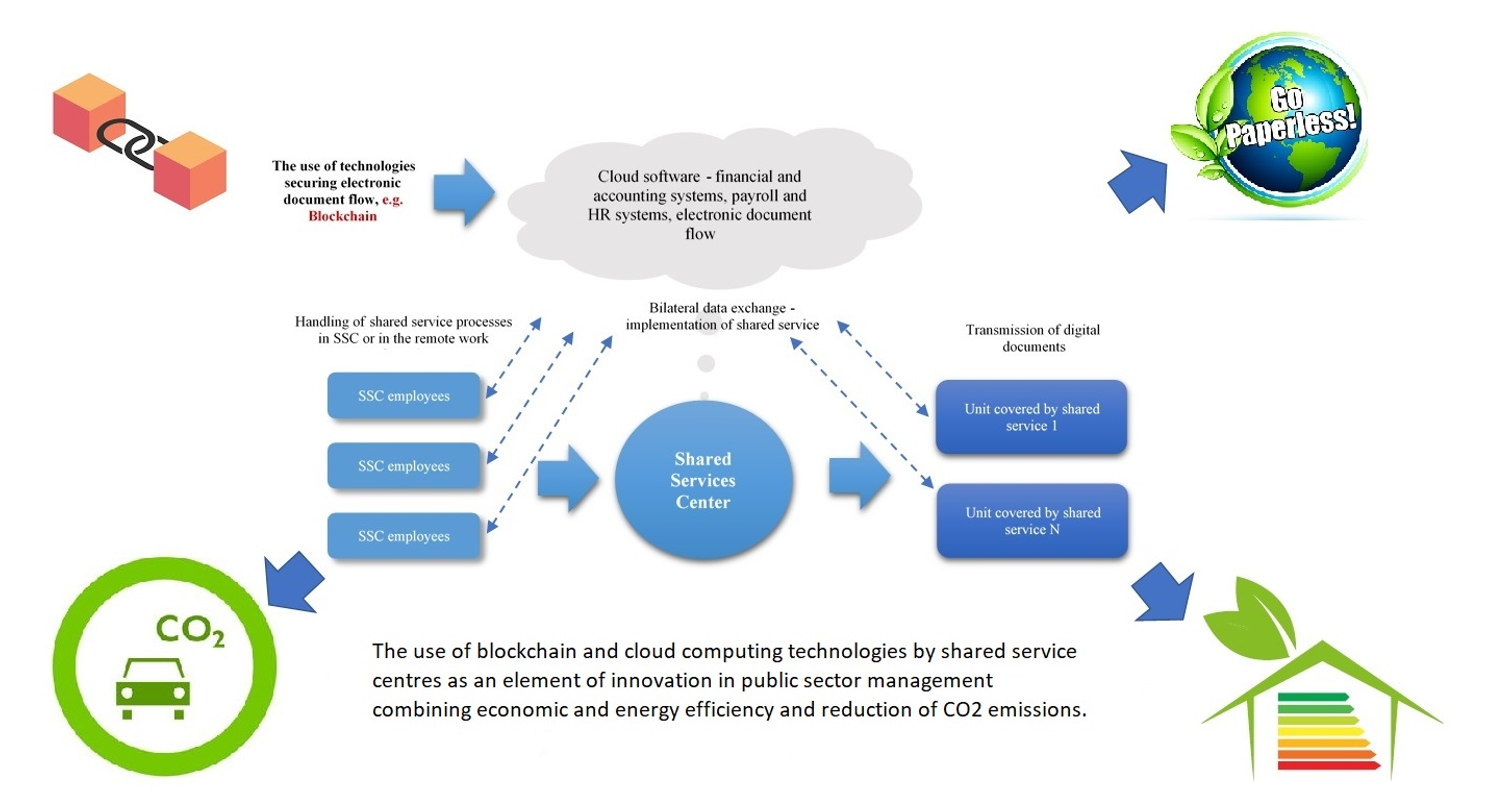

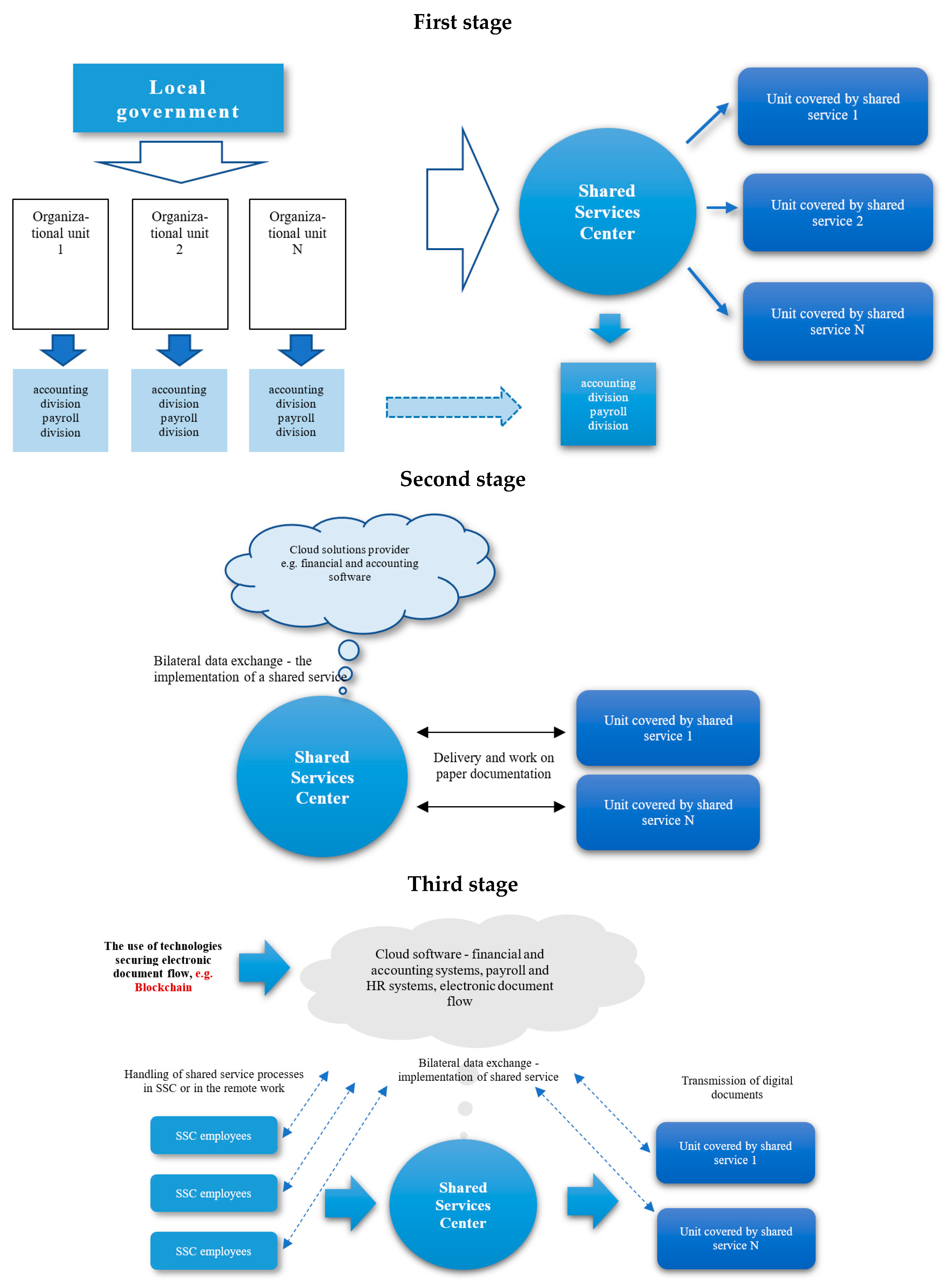

2.3. Shared Services Centres in Public Sector in Poland

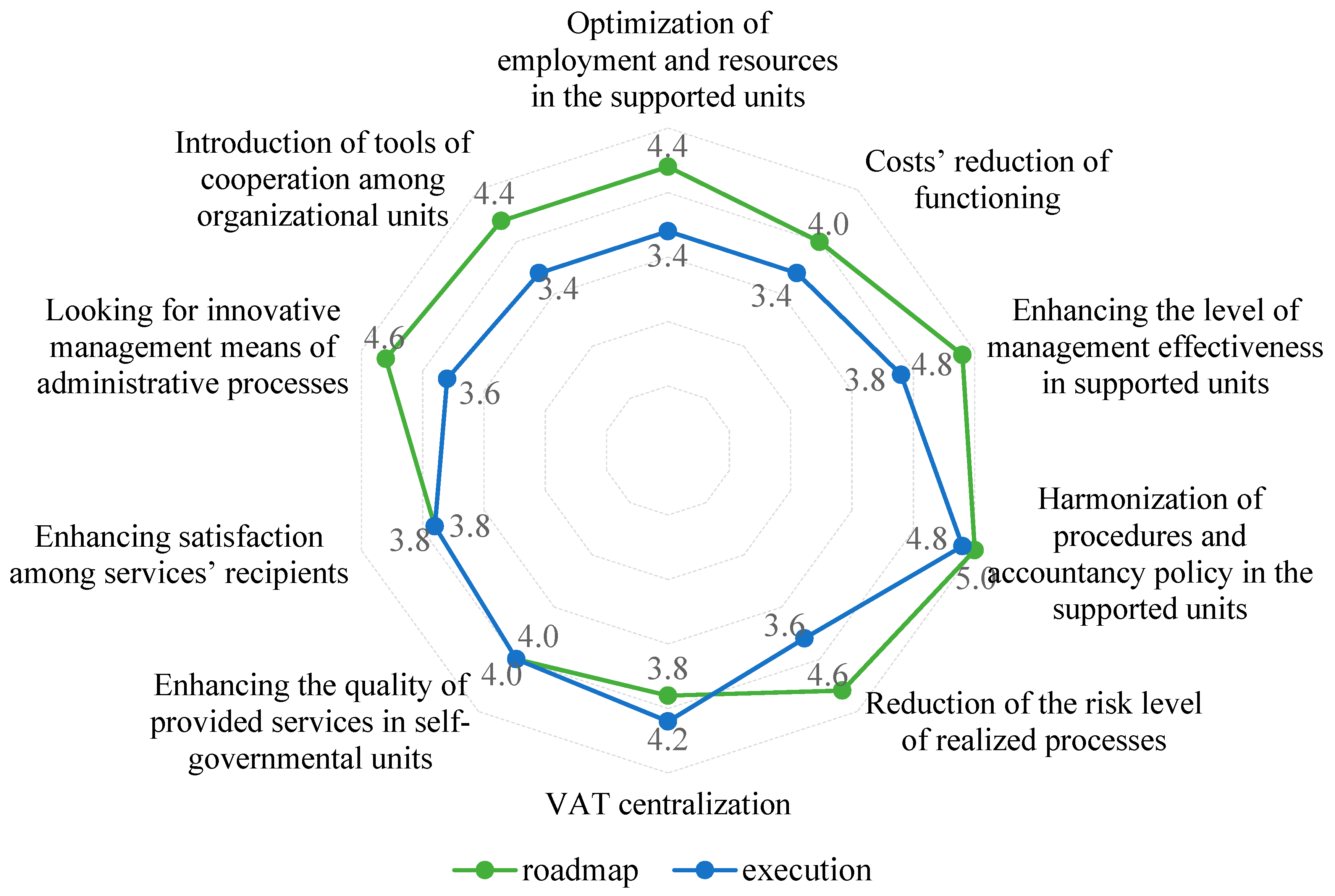

2.4. SSC in Elbląg, Poland—A Case Study

2.5. Modern Technologies—A Tool to Increase Efficiency and Costs/Energy Reduction

3. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Action Plan for Energy Efficiency: Realising the Potential; Communication from the Commission; COM (2006) 545 final; European Commission: Brussels, Belgium, 2006.

- Commission of the European Communities. Green Paper: A European Strategy for Sustainable, Competitive and Secure Energy; COM (2006) 105 final; European Commission: Brussels, Belgium, 2006. [Google Scholar]

- Energy Efficiency Plan 2011; Communication from the Commission to the European Parliament; COM (2011) 109; European Commission: Brussels, Belgium, 2011.

- Report from the Commission to the European Parliament and the Council, Assessment of the Progress Made by Member States towards the National Energy Efficiency Targets for 2020 and towards the Implementation of the Energy Efficiency Directive 2012/27/EU as Required by Article 24 (3) of Energy Efficiency Directive 2012/27/EU; European Commission: Brussels, Belgium, 2015.

- Directive 2012/27/EU of the European Parliament and of the Council of 25 October 2012 on Energy Efficiency, Amending Directives 2009/125/EC and 2010/30/EU and Repealing Directives 2004/8/EC and 2006/32/EC (OJ L 315/1); European Commission: Brussels, Belgium, 2012.

- European Commission. Communication from the Commission to the European Parliament and the Council, Energy Efficiency and Its Contribution to Energy Security and the 2030 Framework for Climate and Energy Policy; COM (2014)520; European Commission: Brussels, Belgium, 2014. [Google Scholar]

- European Commission. Communication from the Commission to the European Parliament and the Council, the European Economic and Social Committee, the Committee of the Regions and the European Investment Bank, State of the Energy Union; COM (2015) 572 final; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- European Commission. A Framework Strategy for a Resilient Energy Union with a Forward-Looking Climate Change Policy; Communication from the Commission to the European Parliament and the Council, The European Economic and Social Committee, The Committee of the Regions and the European Investment Bank; COM (2015) 80; European Commission: Brussels, Belgium, 2015. [Google Scholar]

- European Commission. Clean Energy for All Europeans; Communication from the Commission to the European Parliament and the Council, The European Economic and Social Committee, The Committee of the Regions and the European Investment Bank; COM (2016)/860; European Commission: Brussels, Belgium, 2016. [Google Scholar]

- Burger, C.; Kuhlmann, A.; Richard, P.; Weinmann, J. Blockchain in the Energy Transition a Survey among Decision Makers in the German Energy Industry; Deutsche Energie-Agentur GmbH (dena) German Energy Agency: Berlin, Germany, 2016. [Google Scholar]

- Khatoon, A.; Piyush, V.; Southernwood, J.; Massey, B.; Corcoran, P. Blockchain in Energy Efficiency: Potential Applications and Benefits. Energies 2019, 12, 3317. [Google Scholar] [CrossRef]

- Sharma, T. Implementation of Blockchain on Peer-to-Peer Energy Trading. Blockchain Council. 4 March 2018. Available online: https://www.blockchain-council.org/blockchain/what-is-blockchain-how-does-it-relate-top2p/ (accessed on 29 December 2020).

- Schletz, M.; Cardoso, A.; Dias, G.P.; Salomo, S. How Can Blockchain Technology Accelerate Energy Efficiency Interventions? A Use Case Comparison. Energies 2020, 13, 5869. [Google Scholar] [CrossRef]

- World Energy Council. The Developing Role of Blockchain White Paper; World Energy Council: London, UK, 2017. [Google Scholar]

- Davidson, S.; de Filippi, P.; Potts, J. Economics of Blockchain; Public Choice Conference: Fort Lauderdale, FL, USA, 2016; Available online: https://hal.archives-ouvertes.fr/hal-01382002 (accessed on 12 January 2021).

- Lin, Y.-P.; Petway, J.R.; Lien, W.-Y.; Settele, J. Blockchain with Artificial Intelligence to Efficiently Manage Water Use under Climate Change. Environments 2018, 5, 34. [Google Scholar] [CrossRef]

- Yang, Z.; Xie, W.; Huang, L.; Wei, Z. Marine data security based on blockchain technology. In IOP Conference Series: Material Science and Engineering; IOP Publishing: Bristol, UK, 2018; Volume 322. [Google Scholar]

- Shrier, D.; Wu, W.; Pentland, A. Bloclchain & Infrasturucture (Identity, Data Security); Massachusetts Institute of Technology: Cambridge, MA, USA, 2016; Available online: https://www.getsmarter.com/blog/wp-content/uploads/2017/07/mit_blockchain_and_infrastructure_report.pdf (accessed on 12 January 2021).

- Built, I. What is Blockchain Technology? Available online: https://builtin.com/blockchain (accessed on 29 December 2020).

- Yang, X.M.; Li, X.; Wu, H.Q.; Zhao, K.Y. The Application Model and Challenges of Blockchain Technology in Education. Mod. Distance Educ. Res. 2017, 2, 34–45. [Google Scholar]

- Kumar Das, V. How Blockchain Impact Energy Sector. Available online: https://www.blockchain-council.org/blockchain/how-blockchain-impact-energy-sector/ (accessed on 22 February 2021).

- Fanning, K.; Centers, D.P. Blockchain and its coming impact on financial services. J. Corp. Account. Financ. 2016, 27, 53–57. [Google Scholar] [CrossRef]

- Haferkorn, M.; Quintana Diaz, J.M. Seasonality and Interconnectivity within Cryptocurrencies—An Analysis on the Basis of Bitcoin, Litecoin and Namecoin; Springer International Publishing: Cham, Switzerland, 2015; pp. 106–120. [Google Scholar]

- Nguyen, Q.K. Blockchain, A Financial Technology for Future Sustainable Development. In Proceedings of the 2016 3rd International Conference on Green Technology and Sustainable Development (GTSD), Kaohsiung, Taiwan, 24–25 November 2016; pp. 51–54. [Google Scholar]

- Nijeholt, H.L.A.; Oudejans, J.; Erkin, Z. DecReg: A framework for preventing double-financing using blockchain technology. In Proceedings of the ACM Workshop on Blockchain, Cryptocurrencies and Contracts, Abu Dhabi, United Arab Emirates, 2–6 April 2017; ACM: New York, NY, USA, 2017; pp. 29–34. [Google Scholar]

- Paech, P. The governance of blockchain financial networks. Mod. Law Rev. 2017, 80, 1073–1110. [Google Scholar] [CrossRef]

- Peters, G.W.; Panayi, E. Understanding Modern Banking Ledgers through Blockchain Technologies: Future of Transaction Processing and Smart Contracts on the Internet of Money; New Economic Windows: Cham, Switzerland, 2016; pp. 239–278. [Google Scholar]

- Casino, F.; Dasaklis, T.K.; Patsakis, C. A systematic literature review of blockchain-based applications: Current status, classification and open issues. Telemat. Inform. 2019, 36, 55–81. [Google Scholar] [CrossRef]

- Lakshmi, N.; Sricharan, S. Blockchain: Single Source of truth in Shared Services? An Empirical Paper on the Relevance of Blockchain for Shared Services. Int. J. Recent Technol. Eng. 2019, 7, 1783–1788. [Google Scholar]

- Pajooh, H.H.; Rashid, M.; Alam, F.; Demidenko, S. Multi-Layer Blockchain-Based Security Architecture for Internet of Things. Sensors 2021, 21, 772. [Google Scholar] [CrossRef]

- Alenezi, M.; Almustafa, K.; Meerja, K.A. Cloud based SDN and NFV architectures for IoT infrastructure. Egypt. Inform. J. 2018, 20. [Google Scholar] [CrossRef]

- Dorrell, S. Public Sector Change Is a Worldwide Movement; Speech by the Financial Secretary to the Treasury; Chartered Institute of Public Finance and Accountancy: London, UK, 1993. [Google Scholar]

- Dunleavy, P.; Margetts, H.; Bastow, S.; Tinkler, J. New public management is dead-long live digital-era governance. J. Public Adm. Res. Theory 2006, 80, 3–22. [Google Scholar] [CrossRef]

- Ellinas, A.; Suleiman, E. Reforming the Commission: Between Modernization and Bureaucratization. J. Eur. Public Policy 2008, 15, 708–725. [Google Scholar] [CrossRef]

- Kelly, G.; Mulgan, G.; Muers, S. Creating Public Value: An Analytical Framework for Public Service Reform; Discussion paper prepared by the Cabinet Office Strategy Unit; Cabinet Office: London, UK, 2002.

- Osborne, S. (Ed.) Public-Private Partnerships: Theory and Practice in International Perspective; Routledge: London, UK, 2000. [Google Scholar]

- Osborne, S. (Ed.) The New Public Governance: Emerging Perspective on the Theory and Practice of Public Governance; Routledge: London, UK; Taylor and Francis: New York, NY, USA, 2010. [Google Scholar]

- Bergeron, B. Essentials of Shared Services; John Wiley & Sons: Hoboken, NJ, USA, 2003. [Google Scholar]

- Boroughs, A.; Saunders, J. Shared services the work for the business: Implementing shared service models that realize genuine business benefits. Strateg. HR Rev. 2007, 6, 28–31. [Google Scholar] [CrossRef]

- Craike, A.; Singh, P.J. Shared services: A conceptual model for adoption, implementation and use. Int. J. Inf. Syst. Chang. Manag. 2006, 1, 223–240. [Google Scholar] [CrossRef]

- Janssen, M.; Joha, A. Motives for establishing shared service centers in public administrations. Int. J. Inf. Manag. 2006, 26, 102–116. [Google Scholar] [CrossRef]

- Janssen, M.; Joha, A. Understanding IT governance for the operation of shared services in public service network. Int. J. Netw. Virtual Organ. 2007, 4, 20–34. [Google Scholar] [CrossRef]

- Janssen, M.; Joha, A. Emerging shared service organizations and the service-oriented enterprise: Critical management issues. Strateg. Outsourcing Int. J. 2008, 1, 35–49. [Google Scholar] [CrossRef]

- Modrzyński, P. Local Government Shared Services Centers. Management and Organization; Emerald Publishing Limited: Bingley, UK, 2020. [Google Scholar]

- Deloitte. Shared Services Handbook. Hit the Road. A Practical Guide to Implementing Shared Services. 2011. Available online: https://www2.deloitte.com/content/dam/Deloitte/dk/Documents/finance/SSC-Handbook-%20Hit-the-Road.pdf (accessed on 22 December 2020).

- Deloitte. Blockchain for Financial Leaders: Opportunity vs. Reality. 2018. Available online: https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Audit/gx-fsi-fei-blockchain-report-future-hr.pdf (accessed on 27 December 2020).

- Deloitte. Deloitte’s 2019 Global Blockchain Survey. Blockchain Gets Down to Business. 2019. Available online: https://www2.deloitte.com/content/dam/Deloitte/se/Documents/risk/DI_2019-global-blockchain-survey.pdf (accessed on 25 December 2020).

- Deloitte. 2019 Global Shared Services Survey Report—Executive Summary, 11th Biennial ed.; Deloitte Development LLC, London 2019. Available online: https://www2.deloitte.com/content/dam/Deloitte/us/Documents/process-and-operations/2019-global-shared-services-survey-results.pdf (accessed on 10 December 2020).

- City of Wodonga. A Business Case for a Shared Energy Efficiency Officer. Available online: https://www.localgovernment.vic.gov.au/__data/assets/pdf_file/0021/334236/Wodonga-Indigo-EESS-Business-Case-FINAL.pdf (accessed on 30 December 2020).

- Modrzyński, P.; Gawłowski, R.; Modrzyńska, J. Local Shared Service Centers. Analysis of Functioning and Evaluation of Provided Service Effectiveness; Warsaw, Poland, 2019; p. 14. Available online: https://www.portalsamorzadowy.pl/pliki-download/134596.html (accessed on 10 December 2020).

- Gawłowski, R.; Modrzyński, P. Shared services centres in the public and private sectors: The case study of the United Kingdom. J. Corp. Responsib. Leadersh. 2017, 4, 25–42. [Google Scholar] [CrossRef]

- Gawłowski, R.; Modrzyński, P. Finance Management in Local Government Shared Services Centres in Poland—Primary Experiences. Probl. Zarządzania Manag. Issues 2018, 16, 143–159. [Google Scholar] [CrossRef]

- Modrzyński, P.; Karaszewski, R.; Reuben, A. Process management in local government Shared Services Centres—From an inventory of Shared Service Processes to SLA designing. Acta Sci. Pol. Oeconomia 2018, 17, 63–73. [Google Scholar] [CrossRef]

- Herbert, I.; Seal, W. Shared Business Services and the Evolution of the Multi-Divisional Corporation; E-Leader Singapore: Singapore, 2010. [Google Scholar]

- McIvor, R.; McCracken, M.; McHugh, M. Creating outsourced shared services arrangements: Lessons from the public sector. Eur. Manag. J. 2011, 29, 448–461. [Google Scholar] [CrossRef]

- Quinn, J.B.; Hilmer, F.G. Make versus buy: Strategic outsourcing. Sloan Manag. Rev. 1994, 35, 43–55. [Google Scholar]

- Inoue, A.; Masuda, K. Energy Conservation and CO2 Reduction by Conversion of Paper Document to Electronic Document using High Speed Color Multifunction Device with Document Flow Software. In Proceedings of the 2005 4th International Symposium on Environmentally Conscious Design and Inverse Manufacturing, Tokyo, Japan, 12–14 December 2005. [Google Scholar] [CrossRef]

- Ates, Z.; Büttgen, M. Corporate social responsibility in the public service sector: Towards a sustainability balanced scorecard for local public enterprises. J. Public Nonprofit Serv. 2011, 346–360. [Google Scholar] [CrossRef]

- Act of March 8, 1990 on the commune self-government), (Dz. U. z 2019 r., poz. 506, 1309, 1571, 1696, 1815). Available online: http://isap.sejm.gov.pl/isap.nsf/download.xsp/WDU19900160095/U/D19900095Lj.pdf (accessed on 15 January 2021).

- Modrzyński, P.; Gawłowski, R.; Modrzyńska, J. Samorządowe Centra Usług Wspólnych. Założenia i Praktyka, (Local Government Shared Service Centres. Assumptions and Practice); C.H. Beck: Warszawa, Poland, 2018. [Google Scholar]

- Resolution No. VIII/240/2019 of the City Council in Elbląg of 28 November 2019, on the Creation of a Local Government Organizational Unit “Elbląskie Centrum Usług Wspólnych”, Granting its Statute and Joint Service of Organizational Units of the City of Elbląg. Available online: http://um-elblag.samorzady.pl/art/id/56490 (accessed on 5 January 2020).

- Modrzyński, P. COVID-19 and What’s Next? Challenges of Local Government Administration in the 21st Century; Wspólnota: Warsaw, Poland, 2020; pp. 50–53. [Google Scholar]

- Hodge, B. Blockchain in Shared Services, the Shared Services and Outsourcing Network (SSON). Available online: https://www.ssonetwork.com/rpa/articles/how-to-guide-blockchain (accessed on 21 February 2021).

- World Economic Forum. How Will Blockchain Technology Transform Financial Services? Available online: https://www.weforum.org/agenda/2015/11/how-will-blockchain-technology-transform-financial-services/ (accessed on 19 February 2021).

- Deloitte. Over the Horizon. Blockchain and the Future of Financial Infrastructure, Report. 2016. Available online: https://www2.deloitte.com/content/dam/Deloitte/nl/Documents/financial-services/deloitte-nl-fsi-blockchain-and-the-future-of-financial-infrastructure.pdf (accessed on 20 February 2021).

- Bhowmik, D.; Feng, T. The multimedia blockchain: A distributed and tamper-proof media transaction framework. In Proceedings of the 2017 22nd International Conference on Digital Signal Processing (DSP), London, UK, 23–25 August 2017. [Google Scholar]

- Dupont, Q. Blockchain identities: Notational technologies for control and management of abstracted entities. Metaphilosophy 2017, 48, 634–653. [Google Scholar] [CrossRef]

- Jamthagen, C.; Hell, M. Blockchain-based publishing layer for the keyless signing infrastructure. In Proceedings of the 2016 Intl IEEE Conferences on Ubiquitous Intelligence and Computing, Advanced and Trusted Computing, Scalable Computing and Communications, Cloud and Big Data Computing, Internet of People, and Smart World Congress, Toulouse, France, 18–21 July 2016; pp. 374–381. [Google Scholar]

- Zikratov, I.; Kuzmin, A.; Akimenko, V. Ensuring data integrity using blockchain technology. In Proceedings of the 2017 20th Conference of Open Innovations Association (FRUCT), St. Petersburg, Russia, 3–7 April 2017. [Google Scholar] [CrossRef]

- Reijers, W.; O’Brolcháin, F.; Haynes, P. Governance in blockchain technologies & social contract theories. Ledger 2016, 1, 134–151. [Google Scholar]

- Regulation (EU) 2019/631 of the European Parliament and of the Council of 17 April 2019, Setting CO2 Emission Performance Standards for New Passenger Cars and for New Light Commercial Vehicles, and Repealing Regulations (EC) No 443/2009 and (EU) No 510/2011; European Commission: Brussels, Belgium, 2019.

- Kiprop, J. How Many Trees Does It Take to Make 1 Ton of Paper? Available online: https://www.worldatlas.com/articles/how-many-trees-does-it-take-to-make-1-ton-of-paper.html (accessed on 6 January 2021).

- Modrzyński, P.; Gawłowski, R. Shared Services Centres in the Polish Counties 2018; Report was prepared in cooperation with Polish County Association; Polish Country Association: Warsaw, Poland, 2018; Available online: http://www.forumsamorzadowe.pl/files/file/Raport_PCUW_31_03_2018_Modrzyski_Gawowski.pdf (accessed on 21 February 2021).

- Modrzyński, P. Global Trends in Public Management—Example of Shared Services Centers; Organization and Management, Series No. 129; Silesian University of Technology: Gliwice, Poland, 2018; pp. 297–311. [Google Scholar]

- Sangiorgi, D. Designing for public sector innovation in the UK: Design strategies for paradigm shifts. Foresight 2015, 17, 332–348. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | |

|---|---|---|---|---|---|---|---|---|---|

| European Union | 139.6 | 135.3 | 132.0 | 126.4 | 123.1 | 119.1 | 117.6 | 118.0 | 119.6 |

| Belgium | 133.4 | 127.2 | 128.0 | 124.0 | 121.3 | 117.9 | 115.9 | 115.9 | 119.4 |

| Denmark | 126.2 | 125.0 | 117.0 | 112.7 | 110.2 | 106.2 | 106.0 | 107.1 | 109.5 |

| Germany | 151.1 | 145.6 | 141.6 | 136.1 | 132.5 | 128.3 | 126.9 | 127.2 | 129.5 |

| Greece | 143.7 | 132.7 | 121.1 | 111.9 | 108.2 | 106.4 | 106.3 | 108.8 | 111.1 |

| Spain | 137.9 | 133.8 | 128.7 | 122.4 | 118.6 | 115.3 | 114.4 | 115.0 | 118.1 |

| France | 130.5 | 127.7 | 124.4 | 117.4 | 114.2 | 111.0 | 109.8 | 110.4 | 112.1 |

| Italy | 132.7 | 129.6 | 126.2 | 121.1 | 118.1 | 115.2 | 113.3 | 113.3 | 115.6 |

| Hungary | 147.4 | 141.6 | 140.8 | 134.4 | 133.0 | 129.6 | 125.9 | 125.6 | 129.0 |

| Netherlands | 135.8 | 126.1 | 118.6 | 109.1 | 107.3 | 101.2 | 105.9 | 108.3 | 105.5 |

| Austria | 144.0 | 138.7 | 135.7 | 131.6 | 128.5 | 123.7 | 120.4 | 120.7 | 123.1 |

| Poland | 146.2 | 144.5 | 141.3 | 138.1 | 132.9 | 129.3 | 125.8 | 127.6 | 127.8 |

| Portugal | 127.2 | 122.8 | 117.6 | 112.2 | 108.8 | 105.7 | 104.7 | 104.7 | 106.1 |

| Sweden | 151.3 | 141.8 | 135.9 | 133.2 | 131.0 | 126.3 | 123.1 | 122.3 | 122.2 |

| United Kingdom | 144.2 | 138.0 | 132.9 | 128.3 | 124.6 | 121.3 | 120.1 | 121.1 | 124.7 |

| Shared Services Center | Month | Average Number of Purchase Invoices | The Number of Supported Unit | The Number of Purchase Invoices Per Unit Supported | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | ||||

| SSC 1 | 4441 | 5870 | 6905 | 6154 | 7269 | 6256 | 4168 | 4850 | 6371 | 8269 | 9209 | 10,224 | 6666 | 133 | 50.1 |

| SSC 2 | 3418 | 3338 | 4384 | 3797 | 3962 | 3597 | 2100 | 2536 | 4143 | 4311 | 4339 | 6028 | 3829 | 69 | 55.5 |

| SSC 3 | 2269 | 2719 | 3620 | 3120 | 3428 | 3276 | 2380 | 2257 | 3841 | 4128 | 4597 | 5385 | 3418 | 61 | 56.0 |

| SSC 4 | 2356 | 3357 | 3698 | 3365 | 3856 | 3352 | 3128 | 2929 | 5753 | 4256 | 4578 | 6183 | 3901 | 69 | 56.5 |

| SSC 5 | 10,078 | 12,960 | 15,408 | 12,891 | 16,380 | 14,057 | 9305 | 9215 | 14,109 | 18,645 | 19,864 | 22,950 | 14,655 | 276 | 53.1 |

| SSC 6 | 2974 | 3219 | 4501 | 3147 | 3651 | 3874 | 2479 | 2567 | 4671 | 4960 | 4570 | 4644 | 3771 | 68 | 55.5 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Karaszewski, R.; Modrzyński, P.; Modrzyńska, J. The Use of Blockchain Technology in Public Sector Entities Management: An Example of Security and Energy Efficiency in Cloud Computing Data Processing. Energies 2021, 14, 1873. https://doi.org/10.3390/en14071873

Karaszewski R, Modrzyński P, Modrzyńska J. The Use of Blockchain Technology in Public Sector Entities Management: An Example of Security and Energy Efficiency in Cloud Computing Data Processing. Energies. 2021; 14(7):1873. https://doi.org/10.3390/en14071873

Chicago/Turabian StyleKaraszewski, Robert, Paweł Modrzyński, and Joanna Modrzyńska. 2021. "The Use of Blockchain Technology in Public Sector Entities Management: An Example of Security and Energy Efficiency in Cloud Computing Data Processing" Energies 14, no. 7: 1873. https://doi.org/10.3390/en14071873

APA StyleKaraszewski, R., Modrzyński, P., & Modrzyńska, J. (2021). The Use of Blockchain Technology in Public Sector Entities Management: An Example of Security and Energy Efficiency in Cloud Computing Data Processing. Energies, 14(7), 1873. https://doi.org/10.3390/en14071873