Expectations for Coal Demand in Response to Evolving Carbon Policy and Climate Change Awareness

Abstract

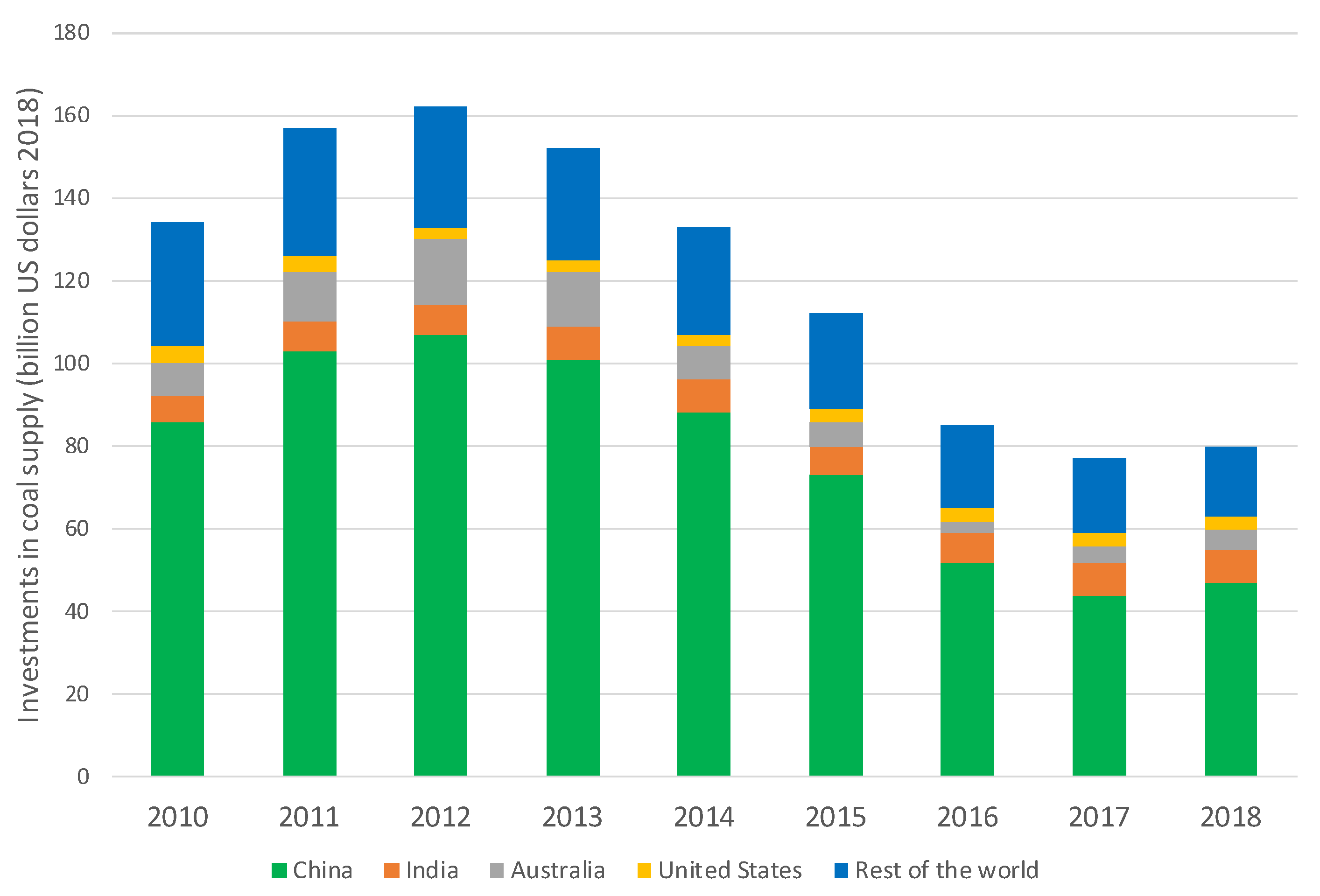

:1. Introduction

2. Coal in the Global Energy and Industrial Supply

2.1. Proportion of Global Energy Supply

2.2. The Effect of Recent External Shocks on Coal Demand

2.2.1. The 2020 COVID-19 Lockdown

2.2.2. A Fast Economic Recovery after the Global Lockdown

2.2.3. The War in Ukraine

2.3. Global CO2 Emissions from Coal

2.4. Long-Term Outlook for Coal

3. Managing GHG Emissions from Coal

3.1. Strategies to Mitigate CO2 Emissions

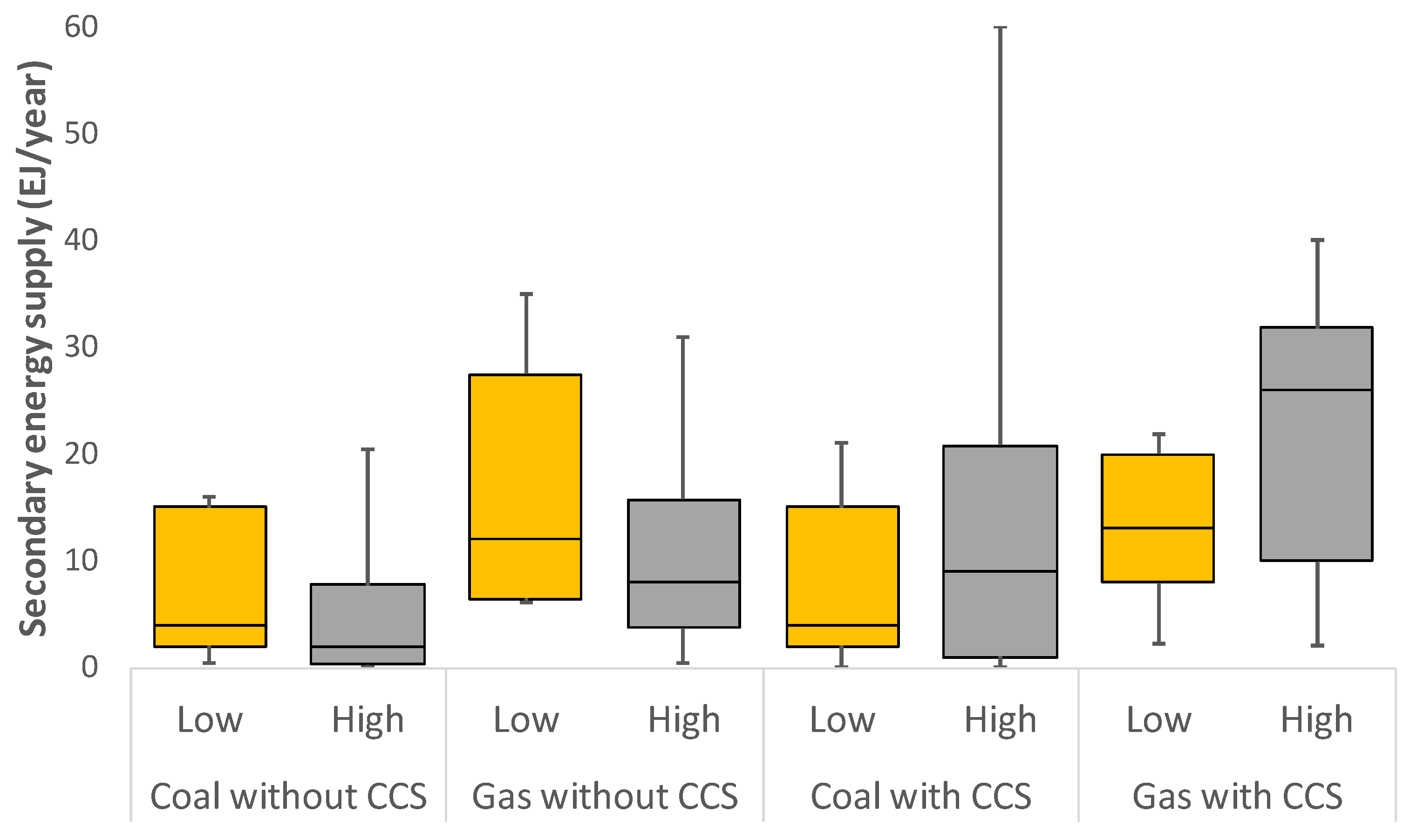

3.2. Carbon Capture, Utilization, and Storage (CCUS)

3.3. Decarbonization of the Energy Supply

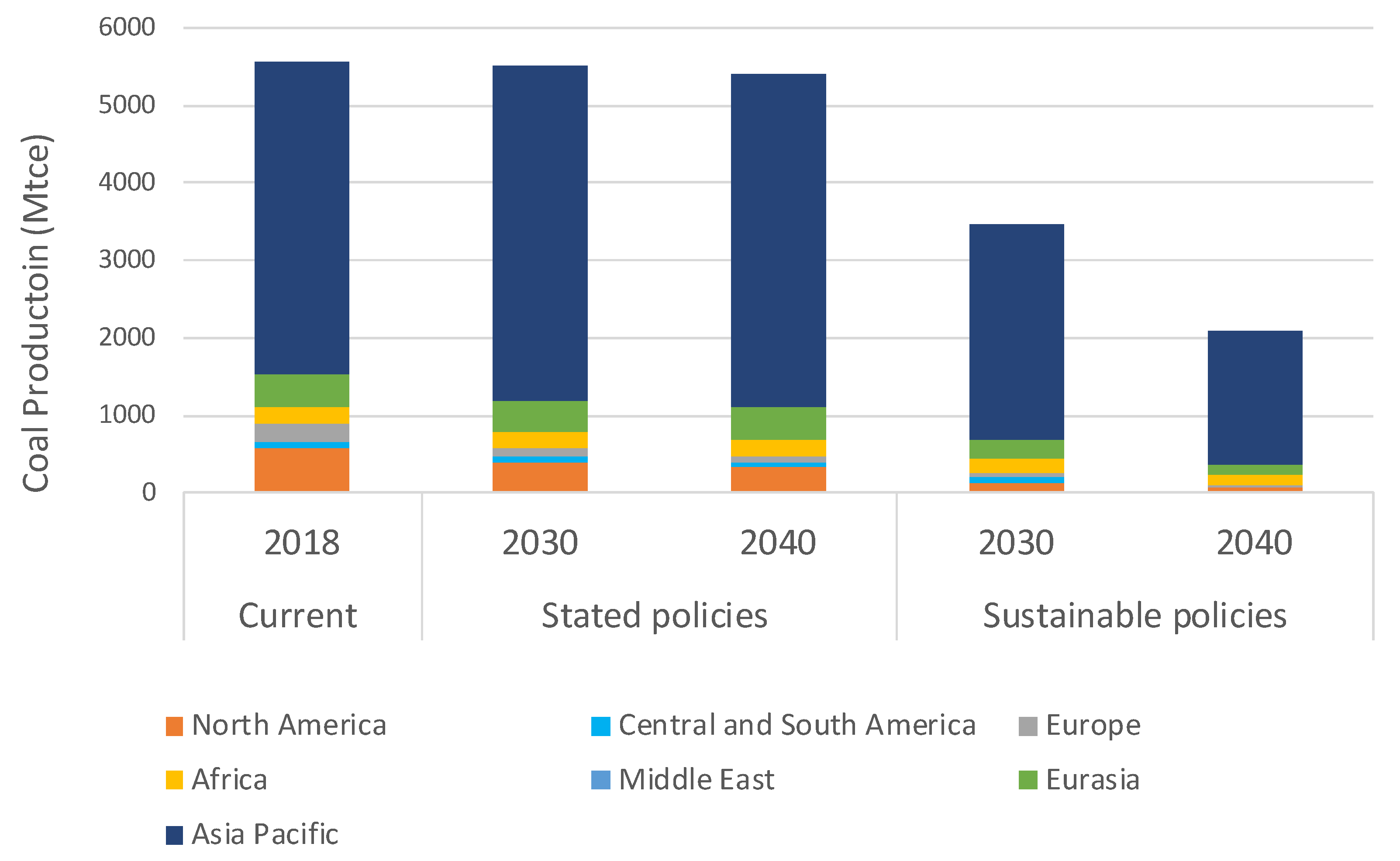

3.4. Effect of GHG Mitigation Strategies on Coal Production

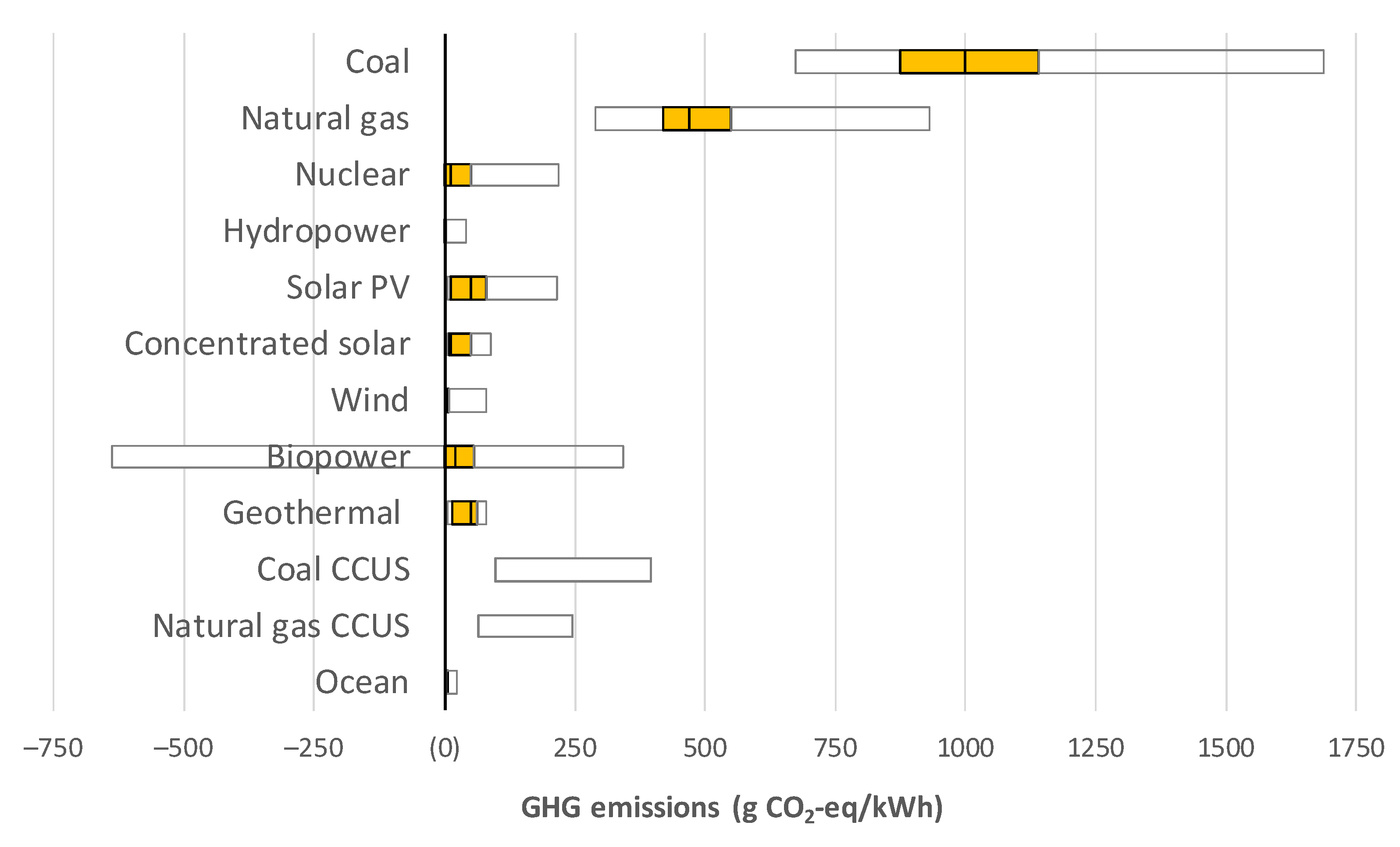

3.5. Effects of Alternative and Renewable Energy Sources

4. Long-Term Prognosis for Coal

5. Conclusions

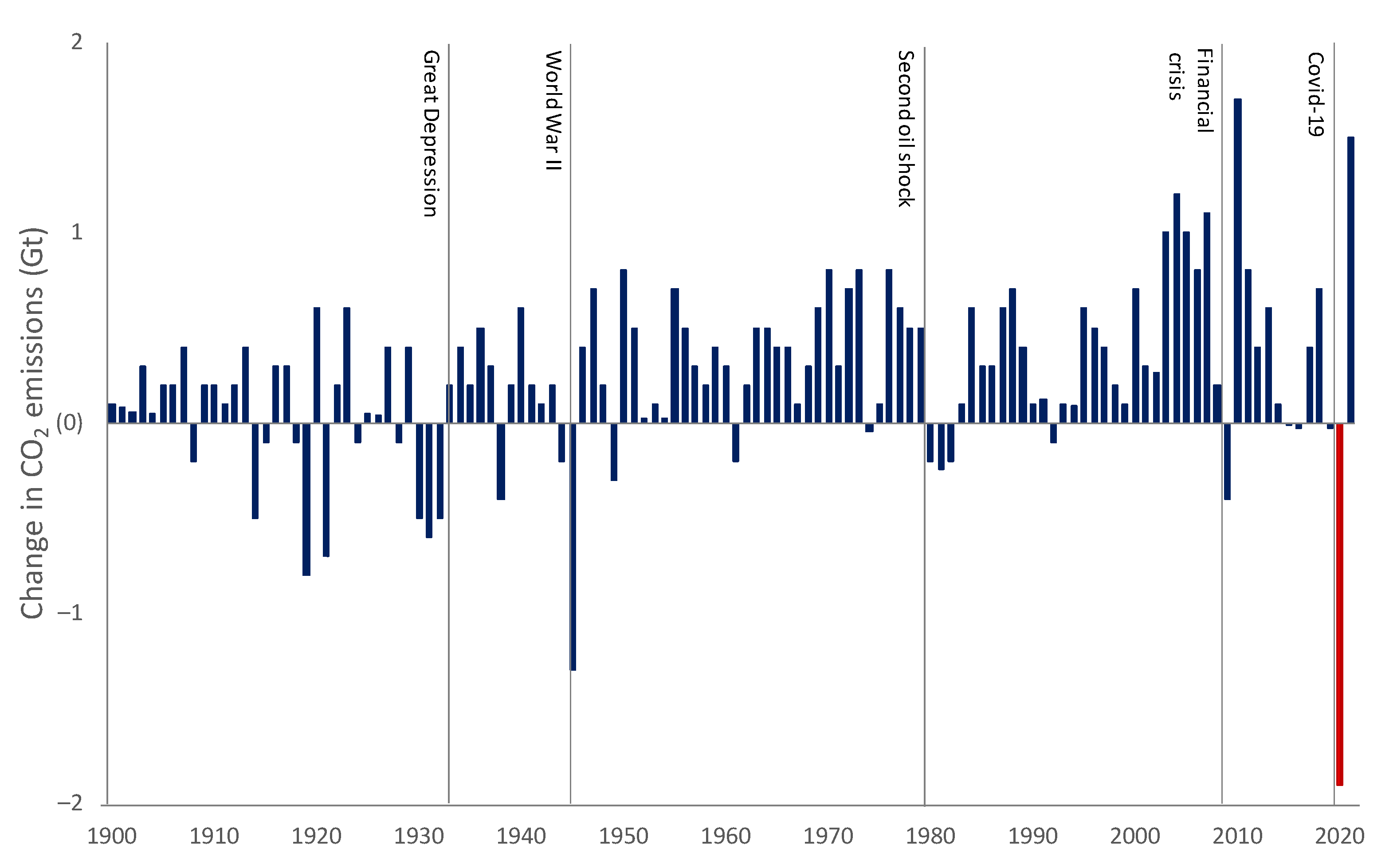

- There is increasing awareness of climate change in society and increasing demand for action. Unprecedented commitments to a lower-carbon future are becoming more common, such as China’s commitment to vehicle electrification, China’s commitment to carbon neutrality, commitments by GM and other manufacturers to vehicle electrification, and commitments by BP, Total, Shell, and ExxonMobil to carbon neutrality. The U.S. is re-engaging in the Paris Agreement and is introducing aggressive legislation to mitigate climate change, and the E.U. has made commitments to reduce GHG emissions by 55% by 2035. Many of these initiatives would have been unlikely 5 years ago but are now expectations. More change and movement towards GHG reductions and climate change moderation should be expected, including additional governmental policy and consumer societal expectations and choices that affect GHG emissions and climate change. The rate of change will also be affected by shocks, such as global health issues, political instabilities, and military conflict.

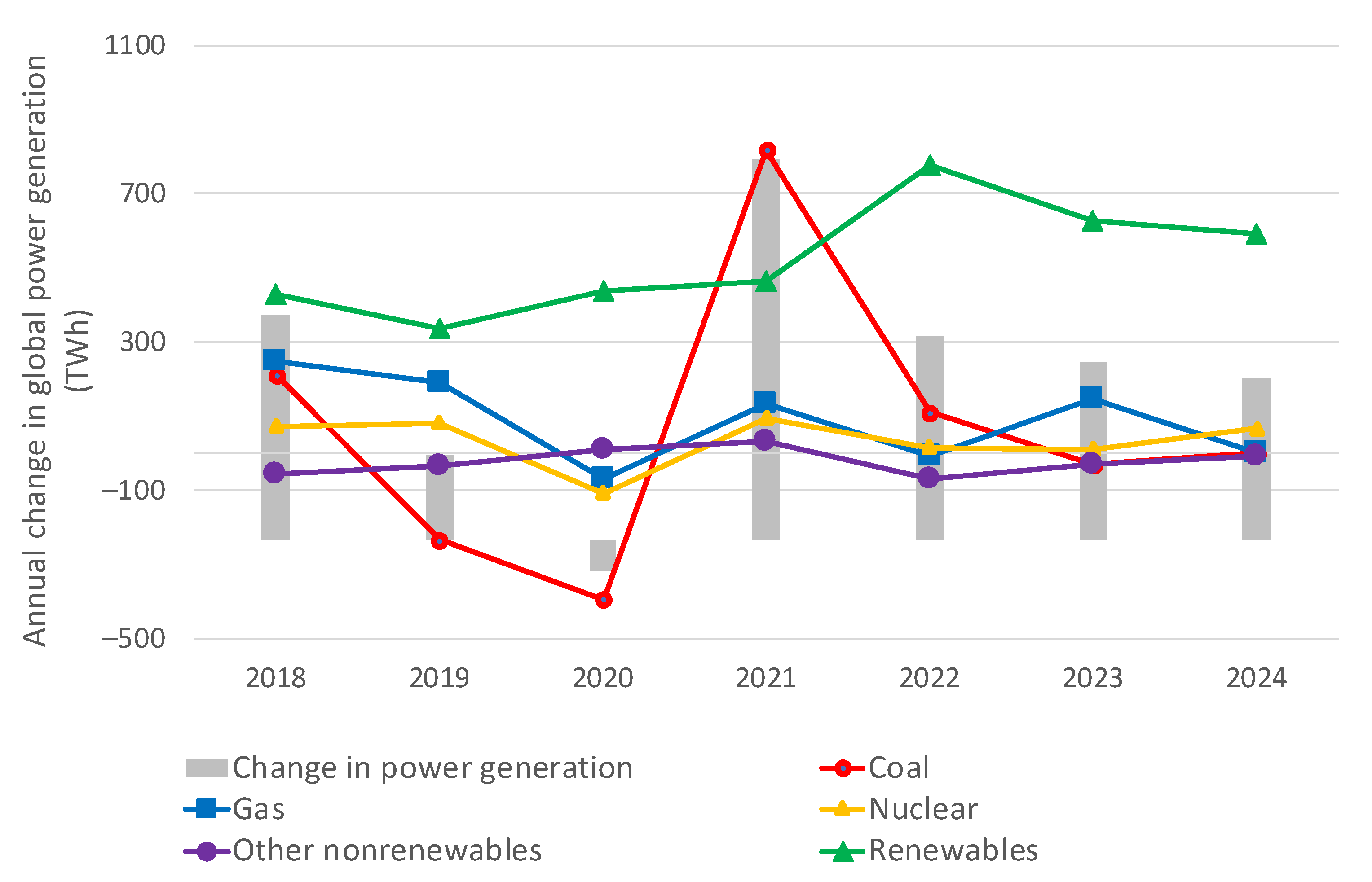

- The COVID-19 pandemic has provided insight into what will likely happen in energy markets as climate policy evolves and public demand for climate action accelerates. The public has observed that rapid reductions in GHG emissions can be achieved by altering society’s use of energy for industry and transportation. This tangible outcome provides an understanding of what is practical by changing technologies, altering energy sources, and changing human behavior. As public demand for climate action increases, conversion to energy sources with lower GHG intensity will accelerate, and the share of renewable energy sources in the energy portfolio will increase rapidly. However, the increase in demand for coal in 2021, with projected increases to last until 2024 and reductions afterwards, has put the net zero by 2050 trajectory further.

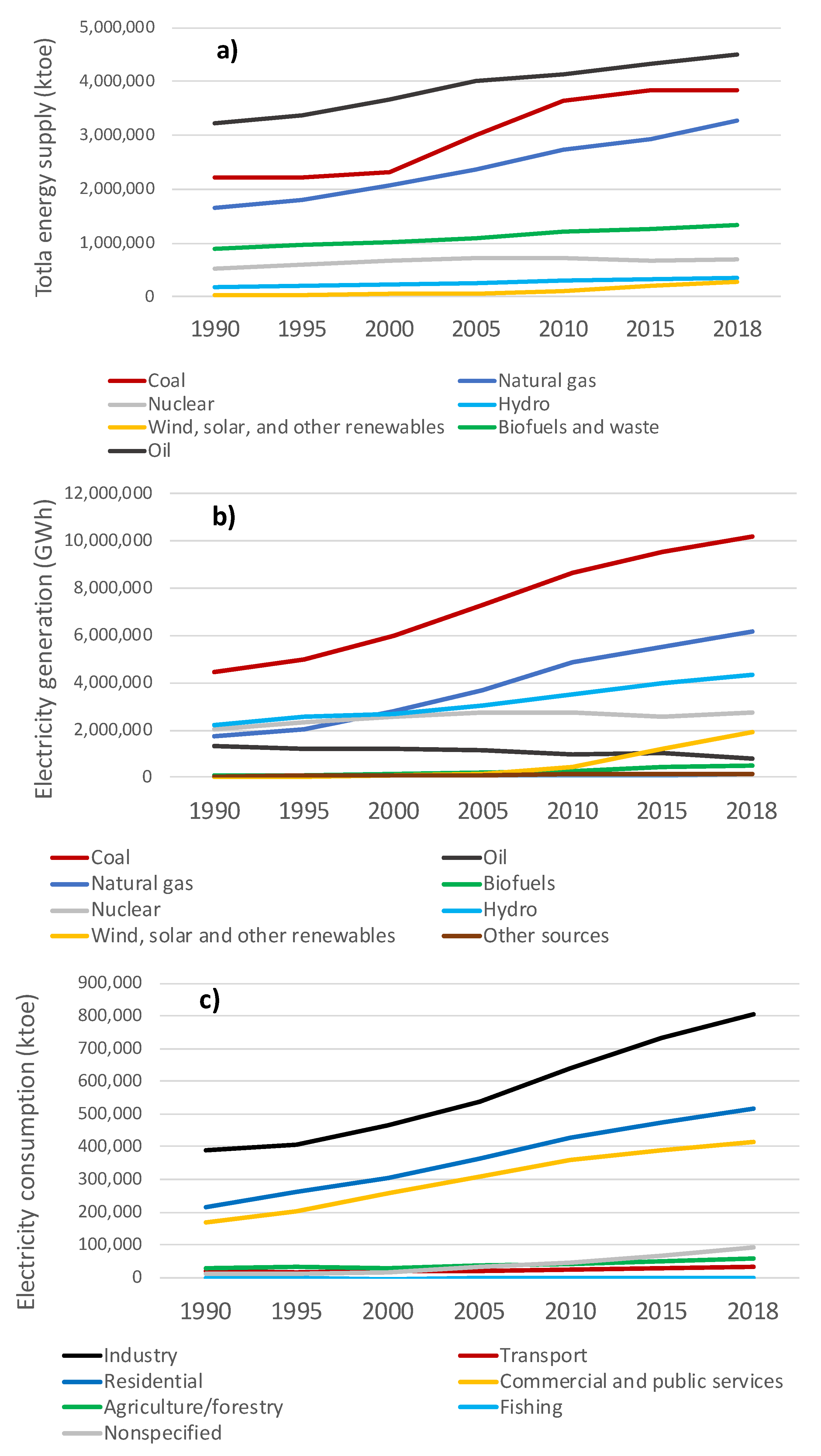

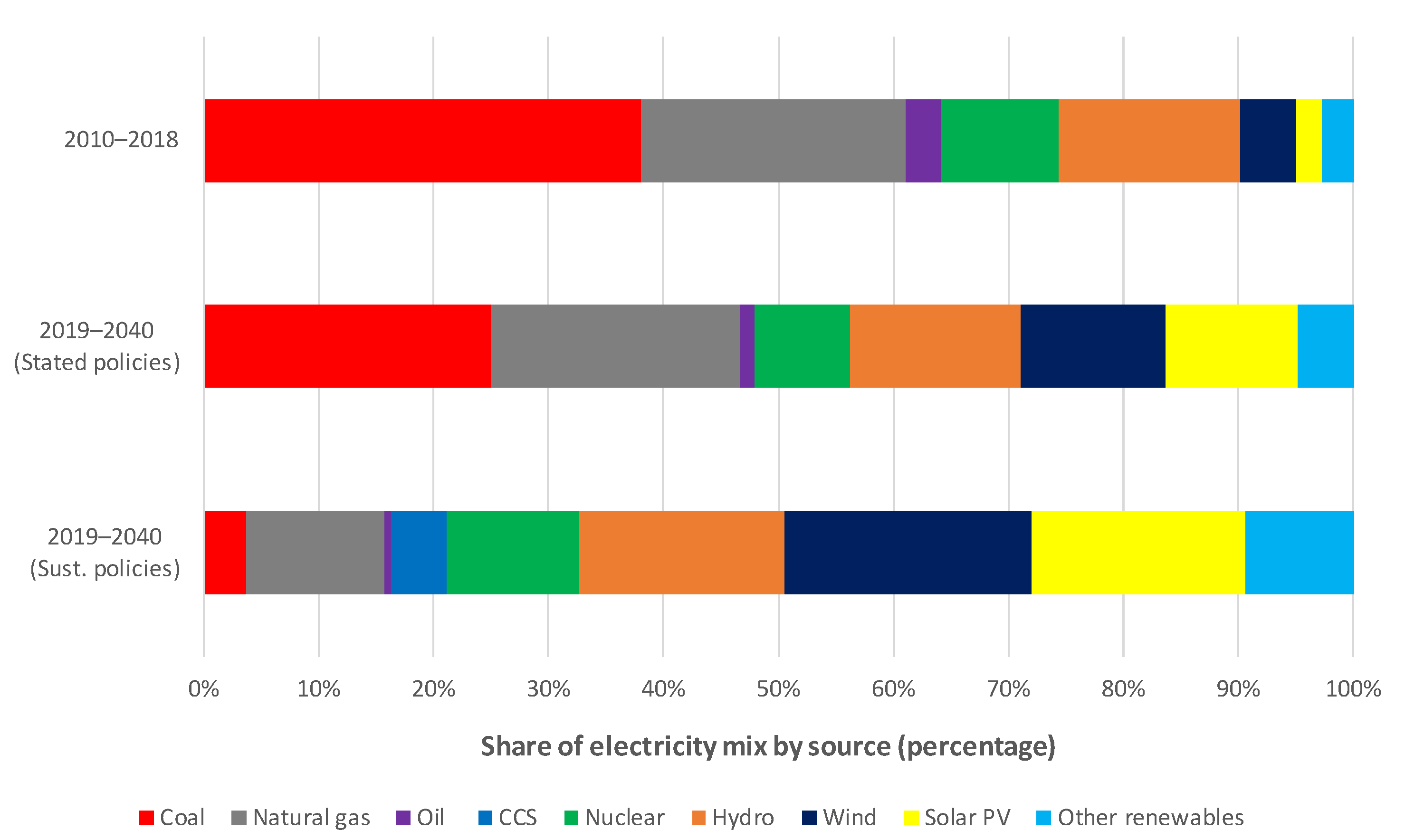

- Commitments to a low-carbon future will require decarbonization of the energy supply mix for electrical production and industrial processes. Replacing coal with less-GHG-intensive energy supplies is now practical and attractive, with natural gas being an abundant alternative that has lower cost and lower GHG intensity. Conversion from coal to gas will accelerate as LNG transport and distribution becomes more widespread and common. This transformation has already begun in the U.S. and the E.U., as coal plants are being replaced by gas-fired plants at an unprecedented pace. This will accelerate in developing countries as LNG becomes more readily available.

- Coal’s predominance in the energy matrix has reached a peak, and a decline in coal demand is expected after 2024 and will continue in the future. The decline of coal’s share will accelerate as China focuses on carbon neutrality goals, the U.S. re-engages in the Paris Agreement and implements new climate legislation, the E.U. progresses towards its emission reduction targets, and India moves to a lower-carbon future. Coal demand should diminish greatly by 2060, when China meets its carbon neutrality goal.

- Renewable energy sources play a major role in the future of global energy supply. The levelized cost of energy for renewables has been dropping rapidly, making broad adoption of renewable energy sources (e.g., solar, wind) practical and economical. This reduction in cost, combined with increasing societal expectations for action to affect climate change, will accelerate decarbonization of the global energy mix. Coal demand likely will decrease more rapidly than other fossil energy sources, replaced by natural gas and renewable energy sources that have lower GHG intensity and will be available readily and economically.

- Carbon capture and storage technologies can reduce GHG emissions from coal as an energy source. These technologies are now viable, but they have high capital cost and high operating cost. These costs have been much higher than anticipated during planning and design. The success of CCUS operations has been mixed, with some CCUS plants being decommissioned due to high operating costs. The higher costs of CCUS were practical when coal was a lower-cost energy source. They may not be practical with the low cost and low GHG intensity of gas and the rapidly dropping cost of renewable energy sources.

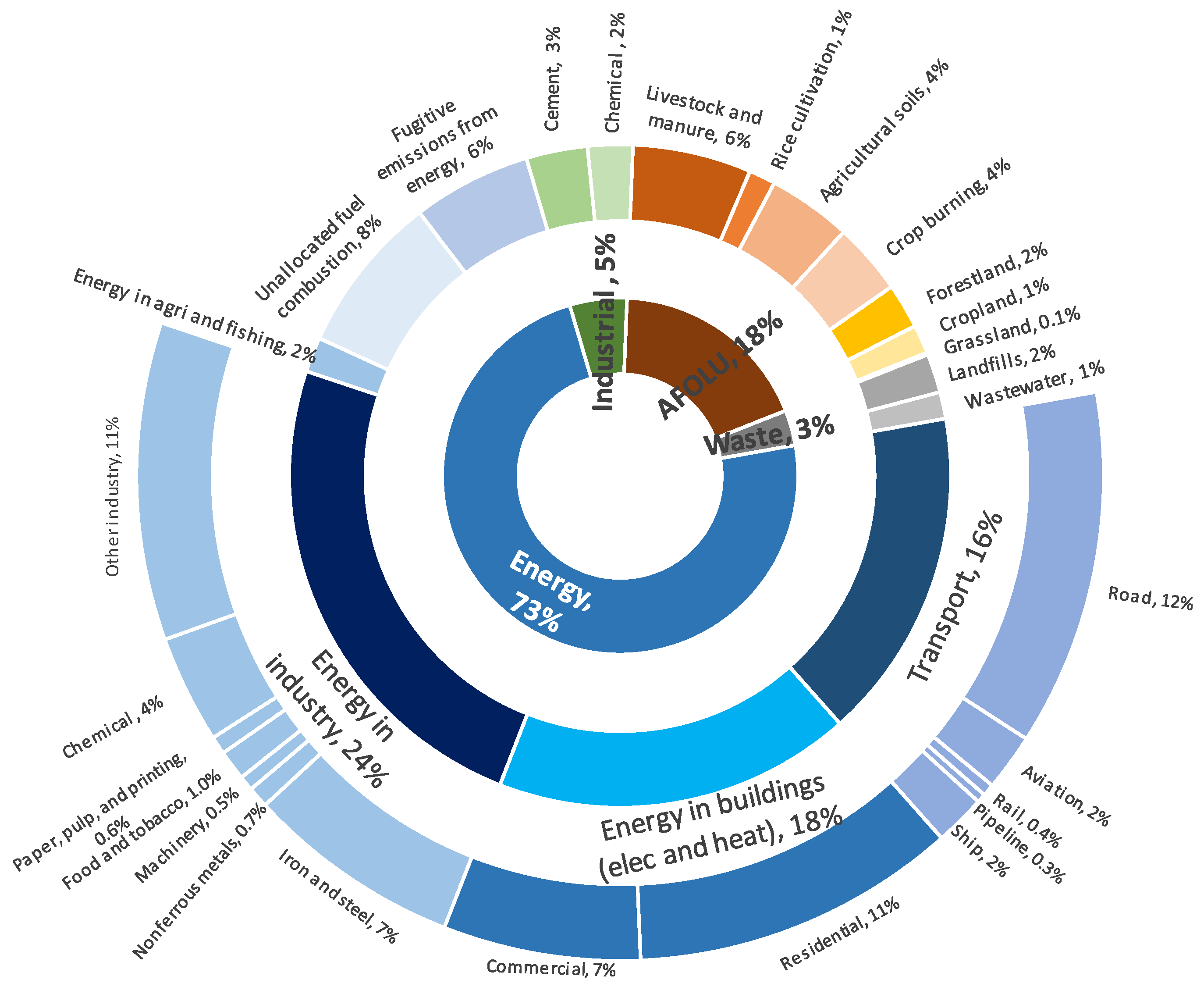

- Power generation from coal is a major source of GHG emissions, but is one of the several contributors to climate change. Emissions associated with combustion of other fossil fuels, for transportation and energy generation (such as natural gas and oil), are higher than the overall emissions from coal-power generation. Moreover, agriculture, forestry, and other land-use activities are also important as they are the main sources of methane and nitrous oxide, which are potent GHGs. Achieving substantial global emission reductions will need interventions and change of practices in all sectors to effectively mitigate GHGs.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- National Oceanic and Atmospheric Administration (NOAA). Global Climate Report-Annual 2021. Available online: https://www.ncei.noaa.gov/access/monitoring/monthly-report/global/202113 (accessed on 26 April 2022).

- Ritchie, H.; Roser, M. CO₂ and Greenhouse Gas Emissions. Available online: https://ourworldindata.org/co2-and-other-greenhouse-gas-emissions#how-have-global-co2-emissions-changed-over-time (accessed on 3 March 2022).

- Climate Watch. Historical GHG Emissions. Available online: https://www.climatewatchdata.org/ghg-emissions (accessed on 12 January 2021).

- Ritchie, H. Sector by Sector: Where do Global Greenhouse gas Emissions Come from? Available online: https://ourworldindata.org/ghg-emissions-by-sector (accessed on 12 January 2021).

- Intergovernmental Panel on Climate Change (IPCC). Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Edenhofer, O., Pichs-Madruga, R., Sokona, Y., Farahani, E., Kadner, S., Seyboth, K., Adler, A., Baum, I., Brunner, S., Eickemeier, P., et al., Eds.; Cambridge University Press: Cambridge UK; New York, NY, USA, 2014. [Google Scholar]

- U.S. Environmental Protection Agency (U.S. EPA). Inventory of U.S. Greenhouse Gas. Emissions and Sinks: 1990–2019; United States Environmental Protection Agency: Washington, DC, USA, 2021. [Google Scholar] [CrossRef]

- Tabeta, S. China Plans to Phase out Conventional Gas-Burning Cars by 2035. Nikkei Asia. 27 October 2020. Available online: https://asia.nikkei.com/Business/Automobiles/China-plans-to-phase-out-conventional-gas-burning-cars-by-2035 (accessed on 5 March 2022).

- NPR. U.S. Officially Rejoins Paris Agreement on Climate Change. Environment NPR. 19 February 2021. Available online: https://www.npr.org/2021/02/19/969387323/u-s-officially-rejoins-paris-agreement-on-climate-change (accessed on 5 March 2022).

- Meredith, S. Big Oil CEO Says Going Green ‘Will Have a Cost for Everybody’—and Governments Need to Explain That. CNBC. 3 February 2021. Available online: https://www.cnbc.com/2021/02/03/oil-total-ceo-says-going-green-will-have-a-cost-for-everybody.html (accessed on 5 March 2022).

- Matthews, C.M. Exxon to Create ‘Low Carbon’ Business Unit as It Faces Activists. Wall Street J. 1 February 2021. Available online: https://www.wsj.com/articles/exxon-to-create-low-carbon-business-unit-as-it-faces-activists-11612219400 (accessed on 5 March 2022).

- Fleeson, W. ExxonMobil Unveils Vision for $100-bil Texas Carbon Capture Hub. Available online: https://cleanenergynews.ihsmarkit.com/research-analysis/exxonmobil-unveils-vision-for-100billion-carbon-capture-hub.html (accessed on 26 April 2022).

- McDonald, M. Rockefeller Foundation Plans to Divest Fossil Fuel Holdings. Bloom. N. 18 December 2020. Available online: https://www.bloomberg.com/news/articles/2020-12-18/rockefeller-foundation-plans-to-divest-fossil-fuel-holdings (accessed on 19 February 2022).

- Wayland, M. General Motors Plans to Exclusively Offer Electric Vehicles by 2035. CNBC. 28 January 2021. Available online: https://www.cnbc.com/2021/01/28/general-motors-plans-to-exclusively-offer-electric-vehicles-by-2035.html (accessed on 5 March 2022).

- Boston, W. Electric Vehicles Make Up More Than a Third of Volvo’s Sales in Europe. Wall Street J. 4 February 2021. Available online: https://www.wsj.com/articles/electric-vehicles-make-up-more-than-a-third-of-volvos-sales-in-europe-11612448847 (accessed on 5 March 2022).

- Campbell, P. Aston Martin Promises to Make Electric Models in UK. Financ. Times. 6 March 2021. Available online: https://www.ft.com/content/6127125e-fbe5-4900-bd8d-54cc01d8922b (accessed on 26 April 2022).

- International Energy Agency (IEA). Data and Statistics. 2020. Available online: https://www.iea.org/ (accessed on 24 January 2021).

- International Energy Agency (IEA). Coal 2020. Available online: https://www.iea.org/reports/coal-2020 (accessed on 19 November 2021).

- Slav, I.U.S. Natural Gas Prices Get Caught Up in Perfect Storm. Oil Price. 9 May 2022. Available online: https://oilprice.com/Energy/Gas-Prices/US-Natural-Gas-Prices-Get-Caught-Up-In-Perfect-Storm.html (accessed on 11 May 2022).

- National Renewable Energy Laboratory (NREL). Life Cycle Greenhouse Gas Emissions from Electricity Generation: Update. Available online: https://www.nrel.gov/analysis/life-cycle-assessment.html (accessed on 5 October 2021).

- International Energy Agency (IEA). Global Energy Review. 2020. Available online: https://www.iea.org/reports/global-energy-review-2020 (accessed on 19 November 2021).

- International Energy Agency (IEA). Coal 2021. Available online: https://www.iea.org/reports/coal-2021 (accessed on 27 April 2022).

- International Monetary Fund (IMF). World Economic Outlook: A Long and Difficult Ascent; International Monetary Fund: Washington, DC, USA, 2020. [Google Scholar]

- International Energy Agency (IEA). Electricity Market Report-January 2022. Available online: https://www.iea.org/reports/electricity-market-report-january-2022 (accessed on 5 May 2022).

- Hook, L.; Hume, N. Will the Ukraine War Derail the Green Energy Transition? Financ. Times. 8 March 2022. Available online: https://www.ft.com/content/93eb06ec-ba6c-4ad2-8fae-5b66235632b2 (accessed on 9 May 2022).

- Strasburg, J.; Dvorak, P. Ukraine War Drives Countries to Embrace Renewable Energy–but Not Yet. Wall Street J. 4 April 2022. Available online: https://www.wsj.com/articles/oil-gas-russia-renewable-energy-solar-wind-power-europe-11649086062 (accessed on 9 May 2022).

- Curry, A. How the Ukraine War Is Accelerating Germany’s Renewable Energy Transition. Natl. Geogr. 6 May 2022. Available online: https://www.nationalgeographic.com/environment/article/how-the-ukraine-war-is-accelerating-germanys-renewable-energy-transition (accessed on 9 May 2022).

- Tollefson, J. What the War in Ukraine Means for Energy, Climate and Food. Nature 2022, 604, 232–233. [Google Scholar] [CrossRef] [PubMed]

- Campbell, M. Renewable Energy Prices Soar as Ukraine War Is the “Last Straw” for the Sector. Eur. N. 13 April 2022. Available online: www.euronews.com/green (accessed on 9 May 2022).

- International Energy Agency (IEA). Global Energy Review. 2021. Available online: https://www.iea.org/reports/global-energy-review-2021/co2-emissions (accessed on 26 April 2022).

- Burnham, A.; Han, J.; Clark, C.E.; Wang, M.; Dunn, J.B.; Palou-Rivera, I. Life-Cycle Greenhouse Gas Emissions of Shale Gas, Natural Gas, Coal, and Petroleum. Environ. Sci. Technol. 2012, 46, 619–627. [Google Scholar] [CrossRef] [PubMed]

- Aguirre-Villegas, H.A.; Benson, C.H. Case History of Environmental Impacts of an Indonesian Coal Supply Chain. J. Clean. Prod. 2017, 157. [Google Scholar] [CrossRef]

- Bruckner, T.; Bashmakov, I.A.; Mulugetta, Y.; Chum, H.; Navarro Ad Edmonds, J.; Faaij, A.; Fungtammasan, B.; Garg, A.; Hertwich, E.; Honnery, D. 2014: Energy Systems. In Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change; Edenhofer, O., Pichs-Madruga, R., Sokona, Y., Farahani, E., Kadner, S., Seyboth, K., Adler, A., Baum, I., Brunner, S., Eickemeier, P., et al., Eds.; Cambridge University Press: Cambridge, UK; New York, NY, USA, 2014. [Google Scholar]

- International Energy Agency (IEA). Greenhouse Gas Emissions from Energy Data Explorer. Available online: https://www.iea.org/articles/greenhouse-gas-emissions-from-energy-data-explorer (accessed on 5 December 2021).

- Roser, M.H.R. Greenhouse Gas Emissions. Available online: https://ourworldindata.org/greenhouse-gas-emissions (accessed on 5 December 2021).

- Gonzales, V.; Krupnick, A.; Dunlap, L. Carbon Capture and Storage 101. Available online: https://media.rff.org/documents/CCS_101.pdf (accessed on 3 July 2021).

- Taft, M. Available online: https://gizmodo.com/the-only-carbon-capture-plant-in-the-u-s-just-closed-1846177778 (accessed on 3 July 2021).

- International Energy Agency (IEA). About CCUS. Available online: https://www.iea.org/reports/about-ccus (accessed on 5 October 2021).

- Schmelz, W.J.; Hochman, G.; Miller, K.G. Total Cost of Carbon Capture and Storage Implemented at a Regional Scale: Northeastern and Midwestern United States. Interface Focus 2020, 10, 20190065. [Google Scholar] [CrossRef] [PubMed]

- ExxonMobil. ExxonMobil Low Carbon Solutions to Commercialize Emission-Reduction Technology. 2021. Available online: https://corporate.exxonmobil.com/News/Newsroom/News-releases/2021/0201_ExxonMobil-Low-Carbon-Solutions-to-commercialize-emission-reduction-technology (accessed on 25 January 2022).

- European Commission. EU Emissions Trading System (EU ETS). Available online: https://ec.europa.eu/clima/eu-action/eu-emissions-trading-system-eu-ets_en (accessed on 5 October 2021).

- European Commission. Carbon Capture, Use and Storage. Available online: https://ec.europa.eu/clima/eu-action/carbon-capture-use-and-storage_en (accessed on 5 October 2021).

- International Energy Agency (IEA). World Energy Outlook. 2019. Available online: https://www.iea.org/reports/world-energy-outlook-2019 (accessed on 25 January 2021).

- Curtis, T.L.; Buchanan, H.; Heath, G.; Smith, L.; Shaw, S. Solar Photovoltaic Module Recycling: A Survey of U.S. Policies and Initiatives; National Renewable Energy Laboratory: Golden, CO, USA, 2021. [Google Scholar]

- Cross, J.; Murray, D. The Afterlives of Solar Power: Waste and Repair off the Grid in Kenya. Energy Res. Soc. Sci. 2018, 44, 100–109. [Google Scholar] [CrossRef]

- Majdi, A.; Alqahtani, M.D.; Almakytah, A.; Saleem, M. Fundamental Study Related to the Development of Modular Solar Panel for Improved Durability and Repairability. IET Renew. Power Gener. 2021, 15, 1382–1396. [Google Scholar] [CrossRef]

- Lai, C.S.; Jia, Y.; Lai, L.L.; Xu, Z.; McCulloch, M.D.; Wong, K.P. A Comprehensive Review on Large-Scale Photovoltaic System with Applications of Electrical Energy Storage. Renew. Sustain. Energy Rev. 2017, 78, 439–451. [Google Scholar] [CrossRef]

- Ware, J. End of Coal in Sight at COP26. United Nations Clim. Chang. 4 November 2021. Available online: https://unfccc.int/news/end-of-coal-in-sight-at-cop26 (accessed on 5 March 2022).

- Thomas, H. Glencore’s ‘Deadly Addiction’ Will Keep Causing Problems. Financ. Times. 19 April 2022. Available online: https://www.ft.com/content/74e67088-0ca5-4f17-a557-6bb7389f522e (accessed on 9 May 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Mitigation Strategy | Mitigation Impacts |

| GHG emission intensity reduction | Greater deployment of renewable energy, nuclear energy, and bioenergy with carbon capture, utilization, and storage (BECCUS); fuel switching within the group of fossil fuels; reduction of fugitive (methane) emissions in the fossil fuel chain |

| Energy intensity reduction by improving technical efficiency | Extraction, transport, and conversion of fossil fuels; electricity/heat/fuel transmission, distribution, and storage; Combined heat and power (CHP) or cogeneration |

| Production and resource efficiency improvement | Energy embodied in the manufacturing of energy extraction, conversion, transmission, and distribution technologies |

| Structural and systems efficiency improvement | Addressing integration needs |

| Activity change (final energy use) | Behavioral change (e.g., thermostat setting, appliance use); lifestyle change (e.g., per capita dwelling size, adaptive comfort); reduced demand for, for example, products such as clothing; alternative forms of travel leading to reduced demand for car manufacturing |

| Energy Source Replacing Coal | Effects | |||

|---|---|---|---|---|

| Economic | Social | Environmental | Other | |

| Nuclear energy | > Energy security (reduced exposure to fuel price volatility) > Local employment (but uncertain net effect) > Legacy cost of waste and abandoned reactors | Health impact via < Air pollution and coal mining accidents > Nuclear accidents and waste treatment, uranium mining and milling > Safety and waste concerns | Ecosystem impact via < Air pollution and coal mining > Nuclear accidents | Proliferation risk |

| Renewable energy * | > Energy security (resource sufficiency, diversity in the near/medium term) > Local employment impact (but uncertain net effect) > Irrigation, flood control, navigation, water availability (for multipurpose use of reservoirs and regulated rivers) > Extra measures to match demand (for PV, wind, and some concentrated solar) | Health impact via < Air pollution (except bioenergy) < Coal mining accidents > Contribution to (off-grid) energy access > Project-specific public acceptance concerns (e.g., visibility of wind) > Threat of displacement (for large hydro) | Ecosystem impact via < Air pollution (except bioenergy) < Coal mining > Habitat impact (for some hydro) > Landscape and wildlife impact (for wind) < Water use (for wind and PV) > Water use (for bioenergy, concentrated solar, geothermal, and reservoir hydro) | Higher use of critical metals for PV and direct drive wind turbines |

| Fossil fuels with CCUS | > Preservation and > lock-in of human and physical capital in the fossil industry | Health impact via > Risk of CO2 leakage > Upstream supply-chain activities > Safety concerns (CO2 storage and transport) | > Ecosystem impact via upstream supply-chain activities > Water use | Long-term monitoring of CO2 storage |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aguirre-Villegas, H.A.; Benson, C.H. Expectations for Coal Demand in Response to Evolving Carbon Policy and Climate Change Awareness. Energies 2022, 15, 3739. https://doi.org/10.3390/en15103739

Aguirre-Villegas HA, Benson CH. Expectations for Coal Demand in Response to Evolving Carbon Policy and Climate Change Awareness. Energies. 2022; 15(10):3739. https://doi.org/10.3390/en15103739

Chicago/Turabian StyleAguirre-Villegas, Horacio Andres, and Craig H. Benson. 2022. "Expectations for Coal Demand in Response to Evolving Carbon Policy and Climate Change Awareness" Energies 15, no. 10: 3739. https://doi.org/10.3390/en15103739