Abstract

A comprehensive assessment was conducted for the electricity dispatch in the Mexican National Interconnected System for the 2017–2021 period, as well as the projected period of 2022–2030, with special attention on emissions and the transition to clean energy. The reported official generation data for the 2017–2021 period were compared to the results of both one- and multi-node dispatch modeling. The officially reported generation mix was found to be sub-optimal in terms of costs and emissions. A small part of the differences can be traced back to transmission constraints. Some of the remaining discrepancies can be explained by out-of-merit order dispatch favoring fossil fuel power plants. While transmission constraints were not critical for the 2017–2021 period, an increasing unbalance between regions with cost-effective generation (exporting regions) and importing regions was found, calling for inter-region transmission corridor reinforcements in the near future. The 2022–2030 emissions dramatically depend on the contemplated scenario. The existing project pipeline would allow for a 45% fraction of clean electricity by 2024, but the projection of current policies, with a renewed focus on generation from fossil fuels, makes a reduced generation from clean sources more likely. A clear policy path is required to bring Mexico’s emissions in line with its national and international clean energy and climate change mitigation goals.

1. Introduction

The climate emergency requires coordinated efforts from all countries around the world to reduce greenhouse gas (GHG) emissions, lighten the pressure on natural resources, safeguard biodiversity, and design and implement a clear path into a decarbonized economy. While the countries with the most long-standing history of industrialization have historically contributed far more than their fair share of the global carbon budget, the active participation of all major polluters is key to reaching the goal of containing global warming and the ensuing consequences. Mexico ranks 14th in the list of 193 countries [1], with estimated annual production-based CO-equivalent GHG emissions of 671 Mtons/a, making Mexico a major player in the global community, with similar contributions to Saudi Arabia (723 Mtons/a), South Korea (652 Mtons/a), Germany (720 Mtons/a), the Democratic Republic of the Congo (680 Mtons/a), and Canada (774 Mtons/a) [1]. The Mexican authorities recognized this co-responsibility in 2015 when they submitted their Nationally Determined Contribution (NDC) commitments [2] to the Paris Agreement, where Mexico pledged to reduce its overall GHG emissions by 22% with respect to the business-as-usual (BAU) baseline emissions for 2030. An important part of this commitment was to gradually decarbonize the electricity sector, traditionally heavily dominated by fossil fuel based generation, by setting goals for the clean energy portion of all generation through 2030, with major intermediate milestones of a 35% clean energy fraction for 2024 and a 50% target for 2030 [3]. The 2020 revision of the NDC commitments resulted in a restatement of the 2015 targets, without additional ambitions. The clean electricity fraction target was maintained at 35% for 2024, but corrected downwards from the original 50% [3] to 38.7% for 2030 [4].

Clean energy, in the Mexican context, includes nuclear energy, the emission-free portion of efficient cogeneration [5], and biomass. Mexico’s commitment at the Paris Agreement was an endorsement of earlier national legislation, in particular the Climate Change Law [6] and the Energy Transition Law [7]. The corresponding implementation strategy was enabled by the 2014 Electricity Industry Law (LIE, for its Spanish acronym) [8], following the 2013 constitutional energy reform, which set the stage for the implementation of a competitive wholesale electricity market. Other major tasks of the electricity sector remained largely unchanged, including the transmission and distribution sectors and the supply and commercialization of end-use energy to the bulk of the users (considered basic supply), which fully remained in the hands of the former state monopolist Comisión Federal de Electricidad (CFE). The market was kick-started by large-scale auctions organized by the federal government, conducted in 2015, 2016, and 2017, designed to provide competitive long-term sourcing options for the newly created subsidiary CFE Basic Supply. In order to spur not only competitiveness but also clean energy generation, the energy-associated co-product CEL (clean energy certificate) was introduced in a similar way to how Renewable Energy Credits (RECs) have been instated in other legislations. The auction process led to increasingly competitive offers and finally record-setting wholesale prices averaging about 20 US$/MWh (including charges for CEL and capacity contributions) in 2017, at the time the cheapest electricity on the planet [9].

The 2018 auction was canceled by the incoming federal government, and no additional auctions have been scheduled since. Several administrative, regulatory, and legislative measures were implemented by the new government in the following years, including the April 2020 ban on pre-operational tests on privately owned solar and wind projects close to commercial operation, a regulatory piece issued May 2020 granting CFE planning privileges and preferred grid access, introducing additional permission barriers for private and renewable generation projects, and a reform to the LIE in 2021. The 2021 version of the LIE was the most comprehensive change in energy policy at that point and included a preferred, en bloc, dispatch of all CFE generators, independently of considerations for costs or emissions. All three dispositions mentioned were suspended by federal courts, with final rulings still pending. An additional attempt to undo the 2013 energy reform and particularly rewrite the LIE was undertaken at the end of 2021, when an initiative for a constitutional change was submitted to congress by the government, aiming at reinstating a state monopoly on electricity generation. This initiative failed, however, to obtain the required qualified majorities in both chambers and did not materialize.

The operation of the market has been studied periodically by the private company ESTA International, charged with providing independent monitoring services as required by the LIE and the market rules. ESTA has delivered annual reports covering the years 2017–2020 [10], but the independent monitoring process was suspended by the federal government from 2021 onward. This leaves independent assessments of Mexico’s electricity sector essentially to academic institutions. An assessment of one of the most consequential proposals put forward by the federal government, the priority dispatch for generators owned and operated by state utility CFE, was conducted by Bracho et al. [11], with authors from NREL and modeling company Encoord. The authors studied four scenarios: (1) A reference scenario reflecting the current dispatch practices in the Mexican wholesale electricity market, designed to match the official generation figures published by the system operator CENACE. (2) A CFE priority dispatch scenario where all plants owned and operated by CFE were secured at their minimum levels, and the rest of the load was allowed to be covered by economic dispatch. (3) A similar scenario, where in addition to CFE-owned plants, Independent Power Producers (IPP), i.e., privately owned generators with long-term delivery contracts with CFE, were included in the priority dispatch block. (4) A final scenario, where the utilization of CFE plants was maximized. Unsurprisingly, the participation of CFE plants increased strongly in all scenarios, up to nearly 75% (from the current 40%) in the CFE-maximized scenario. More importantly, both the total cost of generation and the greenhouse gas (GHG) emissions went up sharply in all scenarios, with an increase of over 50% in cost and a 65% GHG emission increase in the CFE-maximized scenario. These projected increases could be traced back to an increased use of fossil fuels in comparison to the referenced scenario. The existing solar and wind capacity would be curtailed by about 90% in the CFE-maximized scenario, although the curtailment fraction was negligible in the other scenarios. The possible impact on the curtailment of wind and solar in scenarios with higher future renewable energy capacities was not studied.

A renewable energy grid integration study for Mexico, with views of the 35% clean electricity target for 2024 set by the Mexican government was conducted by an extended group of authors from NREL and Encoord [12]. The authors concluded that meeting the 35% target was possible, considering the existing wind and solar development pipelines, particularly projects in advanced stages, and could be achieved with only marginal curtailment of renewable generation, providing significant benefits to the system in terms of reduced marginal costs of electricity and reduced emissions. A comprehensive inter-sectoral study was presented by Buira et al. [13], who outlined a deep decarbonization pathway (DDP) for the entire Mexican economy. Two scenarios were studied in detail, one based on current policies in climate change mitigation ambitions, as well as one consistent with the 1.5 °C goal derived from the Paris Climate Agreement. The authors stressed the importance of decarbonizing the electricity sector, given its pivotal role for the decarbonization of other sectors. Not unexpectedly, the DDP scenario calls for a massive increase in wind and solar generation compared to the business-as-usual scenario. A detailed study of the role of energy efficiency measures for the decarbonization of the electricity sector was presented by Ramírez-Sánchez et al. [14]. The authors developed a model of electricity consumption with high spatial resolution, aimed at guiding public policies focused on the efficient use of electricity. Detailed recommendations for achieving the consumption reductions were laid out. Sarmiento et al. [15] studied the impact of natural gas prices on electricity dispatch in both the U.S. and the Mexican power sectors. For the case of Mexico it was concluded that high gas prices would favor an increased participation of coal in the short term, followed by an increase in renewables in the long term. The impact of the COVID-19 pandemic on the Mexican electricity dispatch was studied by González-López and Ortiz-Guerrero [16]. The authors pointed to the scarcity of studies on the Mexican power system and discussed the vulnerability associated with the great dependence on natural gas, as well as the ongoing efforts of the federal government to re-gain a stronger grip on the power sector.

A number of academic studies have recently been conducted on the grid integration of renewables in different contexts. Tian et al. [17] developed a framework for economic dispatch and risk minimization for a grid with a high presence of wind, solar, hydropower, and thermal generation and applied their method to the dispatch of the Qinghai grid. A low-carbon economic dispatch model for coupled electricity–natural gas grids, considering low-carbon generation technologies including renewables, carbon captures systems, and demand response was presented by Xiang et al. [18]. Their formulation was tested on an IEEE 118 power bus system and a 10-node natural gas grid. Their model accounted both for uncertainties in the generation from renewables and the price of carbon emission certificates. Another inter-sector coupling work was presented by Zhao et al. [19]. Their data-driven approach was shown to be more robust than previously introduced methods.

As evidenced by the literature review, in spite of a considerable academic interest in the cost-effective and risk-avoiding grid integration of renewables in general, studies on the Mexican power sector are relatively scarce. In particular, no diagnostic studies have been performed so far. Among the research questions relevant to the measurement of the performance of the power sector and the Mexican energy transition are the following: (1) How close to optimal was the electricity dispatch in Mexico in the 2017–2021 period, i.e., the period during which a wholesale electricity market was operated for the first time in Mexico? Specifically, is the reported electricity generation roughly consistent with economic dispatch? If not, is there a discrepancy in GHG and polluting emissions between the observed dispatch and the one that would be expected from a fully economic dispatch, and how large is it? (2) To what extent can the discrepancy between the ideal and the observed dispatch be explained by power flow restrictions due to the finite capacity of the large transmission corridors? (3) In case of remaining discrepancies, what is the role of out-of-merit dispatch of (fossil fuel) power plants? (4) What is the expected evolution of the electricity dispatch for the 2022–2030 period depending on the policy scenario? What are the factors influencing the different scenarios? Specifically, can Mexico’s clean energy goals be met with any of the plausible scenarios at the time of writing?

The case for a diagnostic study such as the present work is based on the need for accountability by governments and companies in general, and by the Mexican grid operator in particular. While formal commitments with climate change goals are abundant, and a great deal of academic work has been performed on the grid integration of renewables, realities are often different. The present study is intended to contribute to such a data-driven diagnostic view.

In Section 2, the methodology used in this work will be described, including the tasks performed to build a reliable and updated database for electric generators, as well as to build an approximate model of the electricity grid. In Section 3, the results obtained will be reported in some detail. Section 4 will be dedicated to a critical discussion with some root-cause analyses of current drivers in the electricity sector. Section 5 distills the main findings and issues some recommendations with regards to Mexico’s electricity policy for the rest of the current decade.

2. Methods and Data

The methods used in the present work have been designed to answer the research questions stated above. In order to assess the optimality of the electricity dispatch, first an ideal dispatch model has been set up, limited mostly by the upper and lower generation limits of the power plants, as well as the available resources, particularly solar and wind. This allows for the assessment of whether the reported dispatch was largely driven by economic arguments or if other factors played an important role. It also allowed for the identification of needs for regional reinforcements of transmissions corridors, derived from differential regional growth in demand and cost-effective generation (i.e., the one that would have been dispatched in an ideal economic dispatch case). The explicit consideration of power flow restrictions, conducted in a second phase, was then used to identify deviations from the ideal dispatch and its impact on fuel consumption and emissions. While the main emphasis of this study was the assessment of the past dispatch period 2017–2021, an exploration of the expected dispatch through 2030 under potential scenarios currently considered plausible or achievable has also been conducted.

2.1. The Study Object

The current study focuses on the National Interconnected System (SIN, for the Spanish acronym of Sistema Interconectado Nacional), the fully integrated part of the Mexican electricity system (collectively known as the SEN, Sistema Eléctrico Nacional). Apart from the SIN, the SEN includes three small systems, all located on the Baja California (BC) peninsula. The northern portion (BCA) is interconnected with the Western Electricity Coordinating Council (WECC), but not with the SIN. The southern portion (BCS) is a fully autonomous grid, as well as the middle portion, a still much smaller grid named Mulegé.

In order to avoid complications and contamination of the results by regional subtleties, all results reported in this work will refer to the SIN only.

2.2. Database Construction for Generators

A natural starting point for building a dispatch model is the generator database published alongside the public electricity sector planning document PRODESEN. Unfortunately, the last available version was published in early 2018 and therefore omits (or specifies only vaguely) many of the generators put in operation over the last three or four years. This is particularly critical in the case of solar and wind power plants (built almost exclusively by private developers/investors), which have seen a substantial increase over the last few years. To complete and validate the PRODESEN 2018 information and build a full catalog of generators, the following actions were undertaken:

- A detailed, yet anonymized, list of recent wind power plant projects, including their actual or expected commercial operation dates (CODs), was obtained from the Associación Mexicana de Energía Eólica (AMDEE) for the exclusive purposes of this study.

- A similar list was obtained from the Asociación Mexicana de Energía Solar (ASOLMEX).

- A comprehensive recompilation of all electricity permits granted by the Energy Regulatory Commission (CRE, for its Spanish acronym) was prepared from public information available at the CRE website and provided to the authors by J. Percino-Picazo [20]. Permits include, among other information, the expected CODs and the geographical location of the plant, allowing the generator to be assigned to one of the nodes of the SIN (see Section 2.5).

- Additional validation was conducted for new projects by consulting media coverage announcing progress or commercial operation of certain power plants.

- Supplementary information was obtained from conversations with analysts and stakeholders.

- Information on new projects by the state-owned company CFE was obtained from the public version of the business plan 2021–2025 [21]. Information on a recently announced 1 GW solar photovoltaic project to be built in the municipality of Puerto Peñasco was obtained from media coverage and was validated through conversations with stakeholders.

A representation of the system modeled in this work is shown in Figure 1. The grid is represented by 45 “distributed” nodes, defined by the grid operator CENACE, and their respective interconnections. The latter are straight-line approximations of the transmission corridors and are not geographically accurate. A geographical representation of the line traces can be found in reference [22]. In any case, the grid can be seen to mainly provide robust interconnections between the main load centers and large conventional power stations, particularly combined-cycle, conventional steam, and hydroelectric plants. Solar and wind plants have generally been built near existing transmission corridors; however, important wind and solar resource areas, such as the northern Pacific coast for solar and, for wind, the northern part of Mexico’s portion of the Gulf of Mexico and the southern end of the Isthmus of Tehuantepec (the land bridge between the Pacific Ocean and the Gulf of Mexico), are only weakly interconnected with the main grid. The transmission grid has remained roughly unchanged for about a decade, in spite of significant growth in wind and solar generation capacity, with a particularly notorious stagnation in the last few years.

Figure 1.

Depiction of the National Interconnection System (SIN) modeled in this work. The grid is represented by 45 nodes and their interconnections. Power plants are shown according to their technology, nameplate capacity, and geographic location.

2.3. Solar and Wind Time Series

Solar time series were generated by downloading source data from the National Solar Radiation Database (NSRDB) [23] created and operated by NREL and creating a grid with a 10km spatial resolution. Solar unit output was calculated assuming solar photovoltaic power plants with one-axis tracking of the sun, as implemented in the vast majority of large-scale photovoltaic plants in Mexico. The detailed methodology is described in Salazar [24]. The nearest-neighbor grid location was used for each of the solar PV plants contained in the database built in this work.

The wind time series were downloaded from NREL [25] for the 175 wind farm locations and development sites contained in the database. The available years were 2007 to 2014. The wind speed was extracted for 80m above ground, and an average eight-year yearly wind speed time series was constructed for each location. Wind power generation was calculated assuming the steady-state power curve of a representative wind turbine, corrected for the local air density.

2.4. Ideal Economic Dispatch Model

Following common economic modeling practice [26], a linear programming approach was used to determine optimal generator dispatch. The optimization problem is then given by:

where is the power injected by generator and is the short-term variable cost. This minimization is subject to the equality restriction

where

is the net power injected into node k and is the demand at node n. is the set of generators injecting power into node n. The minimization procedure is also restricted by the inequality conditions.

where and are the minimum and maximum limits for generator g, and .

2.5. Power Flow Modeling and Multinodal Dispatch Model

In the presence of power flow restrictions on the transmission corridors, additional inequality restrictions have to be considered, which can be phrased as follows:

where l runs over the number of transmission lines L connecting the N nodes of the system and is the shift factor matrix, indicating which fraction of the net power injected at node n will flow over line l. Note that the power flow can be either positive or negative, whereas the flow limit is the same for both directions. The construction of the shift factor matrix requires knowledge of both the topology of the grid and the susceptance values of the all transmission lines. can be written as

where is a diagonal matrix collecting the susceptance values of the L transmission lines in the system:

A is a matrix known as the incidence matrix, indicating the connections between nodes (columns) and rows (lines). A (row, column) combination is set to if the line originates at node n and if the lines ends at node n. Note that this requires a prior convention with respect to the orientation of each of the lines of the grid and the corresponding power flows. is a version of the susceptance matrix, now referred to the nodes in the system. It can be calculated with the use of the incidence matrix as:

The apostrophe () symbol, finally, indicates that the column and the row corresponding to the reference node has to be deleted, in the case of the matrix and the column corresponding to the reference node in the case of the matrix .

The equations described above were implemented in a MATLAB environment, with Excel as an input/output facility. The external routine cplexlp was used for improving the performance and convergence of the linear programming problem. The reference node for the Mexican National Interconnected System is the Querétaro Potencia substation, located in Central Mexico. The linear programming approach described in this subsection is a simplified version of the economic dispatch algorithm used by the system operator; the authors claim no innovation with respect to this well-established method.

2.6. Scenario Building

Following the objectives stated at the end of the introduction, the study has been built around two main purposes: (1) Assess how efficiently the market has been operating since its inception up to the end of 2021, i.e., considering the cost- and emission-efficient generation of electricity. (2) Explore the road to 2030 based on plausible scenarios based on recent experiences in the Mexican electricity sector. These scenarios are the following:

- An “optimistic” scenario. In spite of its name, this scenario does not assume any specific impulse to the clean energy transition of the electricity sector by the authorities. In this scenario, it is simply assumed that 90% of all private and renewable energy plants currently contained in the interconnection, construction, or consolidated permitting pipeline will come to fruition between 2022 and 2030. While this seems a relatively low bar, the 90% figure may be viewed by some as too optimistic, given that many investors are likely to write off their assets as stranded given the current political climate towards renewables and private sector participation. Fully built and tested plants, on the other hand, are likely to pursue their quest for commercial operation. In either case, the commercial operation of 90% of the current development pipeline seems to be the most optimistic case which can currently be realistically constructed.

- A “business-as-usual” case, based on the current trend. In this scenario, only 10% of all renewable and private generation projects are allowed to reach commercial operation before 2030.

- A CFE priority dispatch case. This case is based on a scenario that mimics the proposal by the government to prioritize generation by the state utility CFE, independently of economic or environmental merits, assigning only leftover capacity to private generators. Such a proposal was enacted in the reform of the Electricity Industry Law in 2021, but stalled in the courts, with final rulings pending in most cases. The Supreme Court pronounced itself on the issue, but failed to reach the necessary majority to settle the matter, leaving it to the lower courts to decide on the matter on a case-by-case basis. A still more comprehensive reform, based on a proposed modification of the constitution, was put forward by the government in 2022, but failed to gather the necessary qualified majority. This reform would not only have confirmed the priority dispatch for CFE but would have essentially transferred all electricity sector responsibilities to the state utility, abolishing the electricity market and independent oversight. Though the administrative details of any possible implementation of the priority dispatch for CFE are not clear, the general consequences can be well anticipated and have been considered in the proposed alternative dispatch modeled in this work.

3. Results

3.1. Insights into the Dispatch Stack

In order to provide a qualitative understanding of the economic dispatch in the Mexican National Interconnected System, dispatch stacks have been constructed. The year 2020 was chosen for illustrative purposes. The short-term operational costs discussed in Section 2.4 are calculated from the variable operating and maintenance cost plus the fuel cost, calculated from the unit fuel cost and the heat rate. Unit fuel costs for natural gas vary by month and natural gas region. Unit fuel costs for fuel oil, coal, and diesel were used as national averages because there exists little regional variability.

The results are shown in Figure 2 and Figure 3. It should be noted that the dispatch of hydroelectric plants is conducted according to hydro-thermal coordination, where hydro plants are always placed at the top of the current dispatch stack and their marginal cost is calculated according to the last non-hydro plant displaced. In the construction of the figures, the average hydro generation values from January and July of 2020 were used, and all plants were assumed to be operating at the same net capacity factor (NCF). In both figures, combined-cycle plants, representing the bulk of the generation capacity, have been assumed to be operating at the same constant NCF of 80%. Wind and solar were assumed to be operating at their combined P95 value.

Figure 2.

Dispatch stack for January 2020. Left vertical axis: short-term generation cost in Mexican pesos (MXN) per MWh. 1 MXN = 0.05 US$. Right vertical axis: Technology/fuel combination. Technologies: CC: Combined cycle plants. CS: Conventional steam. SC: Single-cycle gas turbines. IC: Internal combustion engines. Cogen: Cogeneration. Fuels: NG: natural gas. FO: fuel oil. Wind and solar have been assumed to be generating at their combined P95 values.

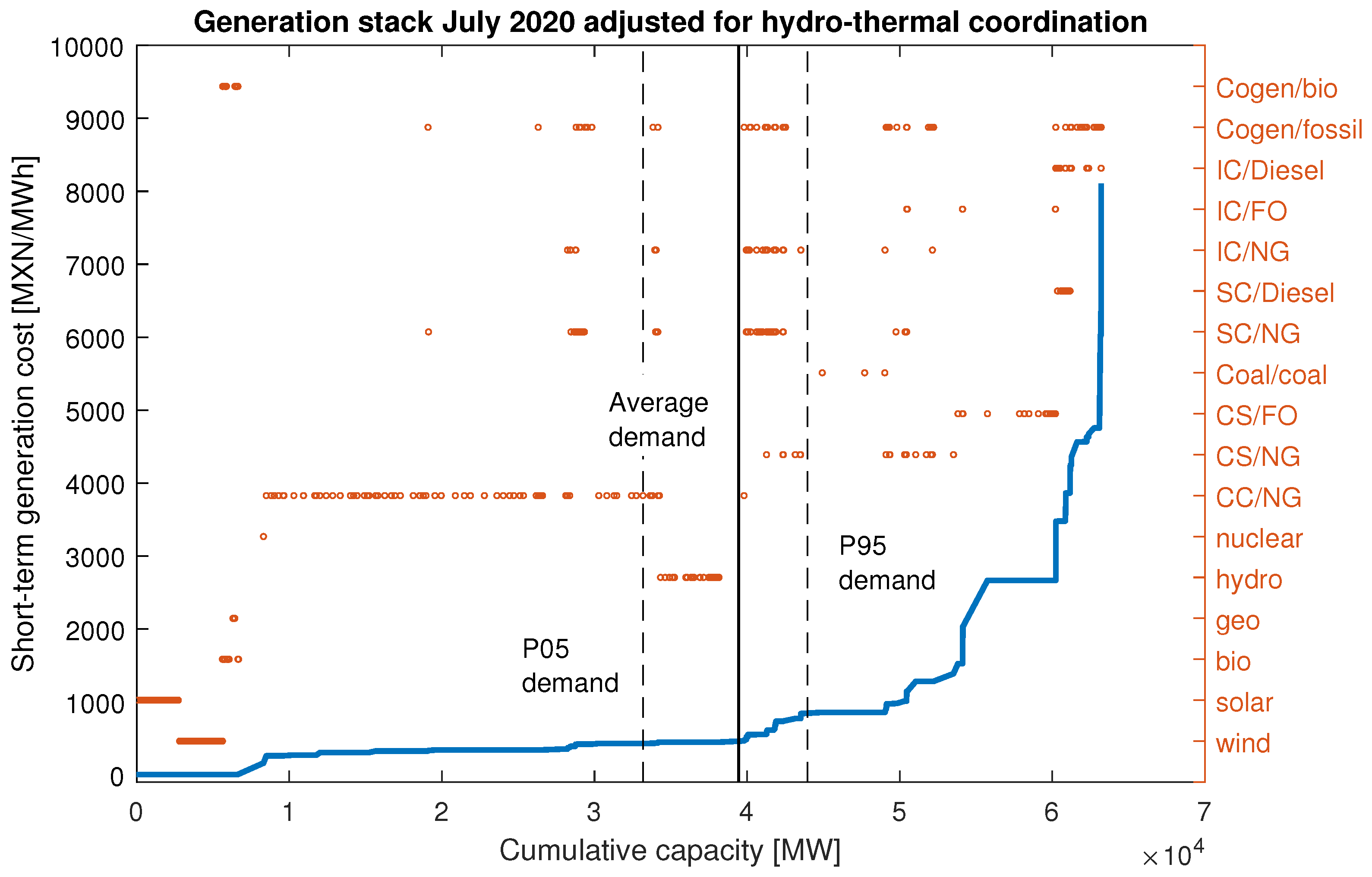

Figure 3.

Dispatch stack for July 2020. See caption of Figure 2 for an explanation of the acronyms.

From the supply curves (blue lines) it can be seen that the bulk of the generation capacity up to a load of about 40 GW generates at around 500 MXN/MWh, or 25 US$/MWh, with the marginal price marked mostly by combined-cycle plants. Next in line are single-cycle gas turbines and internal combustion engines, also operated with natural gas. Coal plants operate at approximately 1000 MXN/MWh, or 50 US$/MWh. Conventional steam plants, particularly if operated with fuel oil, and plants burning diesel, are dramatically more expensive. Based on these qualitative observations, it should be clear that an efficient (economic) dispatch should only see occasional participation from plants other than renewables, combined-cycle plants, and hydro.

For the case of January 2020, it can be seen that for an average monthly load of about 32 GW, assuming that wind and solar are operating at their P95 value, one would expect only wind and solar, hydro, and natural gas fired generation, at a marginal price of electricity of around 500 MXN/MWh or 25 US$/MWh; the P95 and P05 values for the demand are also shown for illustrative purposes. Evidently, with smaller generation from wind and solar the supply curve will be displaced to the left, resulting in a limited opportunity for generation from other technology/fuel combinations. However, given the huge amount of installed combined cycle capacity, this effect is relatively minor, and in most cases, combined cycle plants would be expected to mark the marginal cost of electricity.

As demand grows, as illustrated by the July 2020 dispatch stack in Figure 3, there is an opportunity for generation by single-cycle (SC) gas turbines and internal combustion (IC) engines, as long as they are operated with natural gas. Conventional steam plants, particularly those operating with fuel oil, should be barred from large-scale generation because of cost reasons.

3.2. Reported Official Dispatch Figures

We start our discussion of the electricity generation mix in Mexico with an inspection of the official generation figures, grouped by technology. Table 1 shows the generation numbers for 2017 through 2021, calculated from an hourly time series downloaded from the public area of the electricity market. The year 2016 was not included, because market operations did not start until April 2016. CENACE figures do not distinguish between fuels or permit type, making a detailed validation of the results dependent on additional assumptions. However, a few observations can be readily made: (1) Generation from wind and solar has risen significantly over the five-year period shown, with wind doubling its output and solar almost reaching the levels of wind generation in 2021, when in 2016 its output was still marginal. (2) There is a corresponding reduction in generation from coal and conventional steam plants. However, even in 2021, the generation from these technologies was quite substantial, considering the discussion of the dispatch stack in the previous section. (3) Generation from combined-cycle plants continues to be the main driver of growth.

Table 1.

Electricity dispatch by technology as reported by the system operator (CENACE).

3.3. Official Dispatch vs. Uni-Nodal Model Results

We will now compare the official dispatch figures with the results of the model built in this work. We will start with the results obtained with the uni-nodal dispatch, i.e., the one which does not consider power transfer limits between connected adjacent nodes. Further below we will also discuss the effect of those restrictions.

From Table 2 the following observations can be made:

Table 2.

Reported generation figures compared to the uni-nodal dispatch results of this work.

- Both the solar and the wind energy generation figures predicted by our model are in good agreement with the official dispatch figures. This is not trivial, as the generation was calculated ab initio from wind and solar resource data and models of the wind and solar power plants, with both model components introducing their share of uncertainty. Moreover, the commercial operation dates (COD) of each power plant necessarily have a certain level of uncertainty, given the complexities of the project development process and the dependence on decisions made by government agencies such as CRE and CENACE, as well as the state utility CFE, which participates in the interconnection process. In spite of these uncertainties, the solar generation for all full years (2017 through 2021) is very well predicted by the uni-nodal dispatch model. The wind generation is somewhat overpredicted in the early years, but then converges as the growth curve starts to saturate.

- The model-predicted generation figures for combined-cycle (CC) plants are notoriously higher than the numbers reported by CENACE, though the discrepancy diminishes towards the end of the modeling period (2020, 2021). It can be seen in Table 2 that in 2017 the uni-nodal dispatch model predicted about 202 TWh/a of electricity from combined-cycle plants, compared to the official number of 143 TWh/a, equivalent to an overprediction of 41%. By 2021, this discrepancy had been reduced to 14% (214 TWh/a predicted vs. 184 TWh/a reported).

- Conversely, the true generation from both coal-fired plants and from steam turbines (fired with a combination of natural gas and fuel oil) can be seen to be dramatically higher than the corresponding numbers predicted by the uni-nodal dispatch model in this work. In the case of coal, the values for the year 2017 can be seen to be about five times as high as predicted by the economic dispatch model (nearly 29 TWh/a vs. 4.6 TWh/a), though this discrepancy diminished over the years as the reported dispatch of coal-fired generation dropped to 8.7 TWh/a in 2021 (still twice the economic dispatch figure for 2017 and about six times the economic figure for 2021, which was 1.4 TWh/a). The case of steam-generated electricity’s discrepancy is even more stunning, with 41 TWh/a generated from those (generally inefficient) plants in 2017 vs. only 0.5 TWh/a which would have been economically viable. Similar to coal, the reported steam-fired generation diminished over the years, but still stood at 23 TWh/a in 2021, compared to roughly 1 TWh/a, which would have been in demand for economic reasons. These results are in qualitative agreement with the discussion of the dispatch stack in the previous section.

- The generation from single-cycle gas turbines predicted by the economic dispatch model is very similar to the figures reported by CENACE for all years. Similarly, the generation from internal combustion engines, albeit being a small figure, is well predicted for all years.

- As mentioned before, generation from nuclear and geothermal sources, which are essentially base-line technologies, have not been modeled explicitly and are therefore not subject to an analysis. Similarly, hydroelectricity generation figures were included in the dispatch model as reported.

As revealed by the results of the previous analysis, in spite of good agreements of the predicted generation of several non-trivial categories, such as wind, solar, gas turbines, and internal combustion, there is a notorious discrepancy for combined-cycle plants on the one hand, the generation of which is overpredicted, and the coal and steam, the production of which is underpredicted. One possible explanation for these differences obviously lies with the decision not to include power flow restrictions on the transmission corridors connecting different nodes in this first analysis. The effect of including those restrictions will be discussed in Section 3.4.1.

Before doing so it is, however, instructive to examine both the environmental and the economic impact of the inefficiencies implied by the preferred dispatch of electricity generated in steam plants fired with both coal and natural gas/fuel oil. Independently of whether operational or infrastructure restrictions or non-technical decisions are held accountable for the observed differences it is clear that (1) deviations from the economic merit order necessarily create an additional cost to the system, (2) the use of low-efficiency power plants such as aged coal-fired plants (averaging an efficiency of around 30% in Mexico) and equally aged conventional steam plants (with an average efficiency of around 20%) increases emissions (greenhouse gases and local pollutants) as well as the use of cooling water, and (3) the use of particularly contaminating fuels such as coal and fuel oil create an additional impact on the environment.

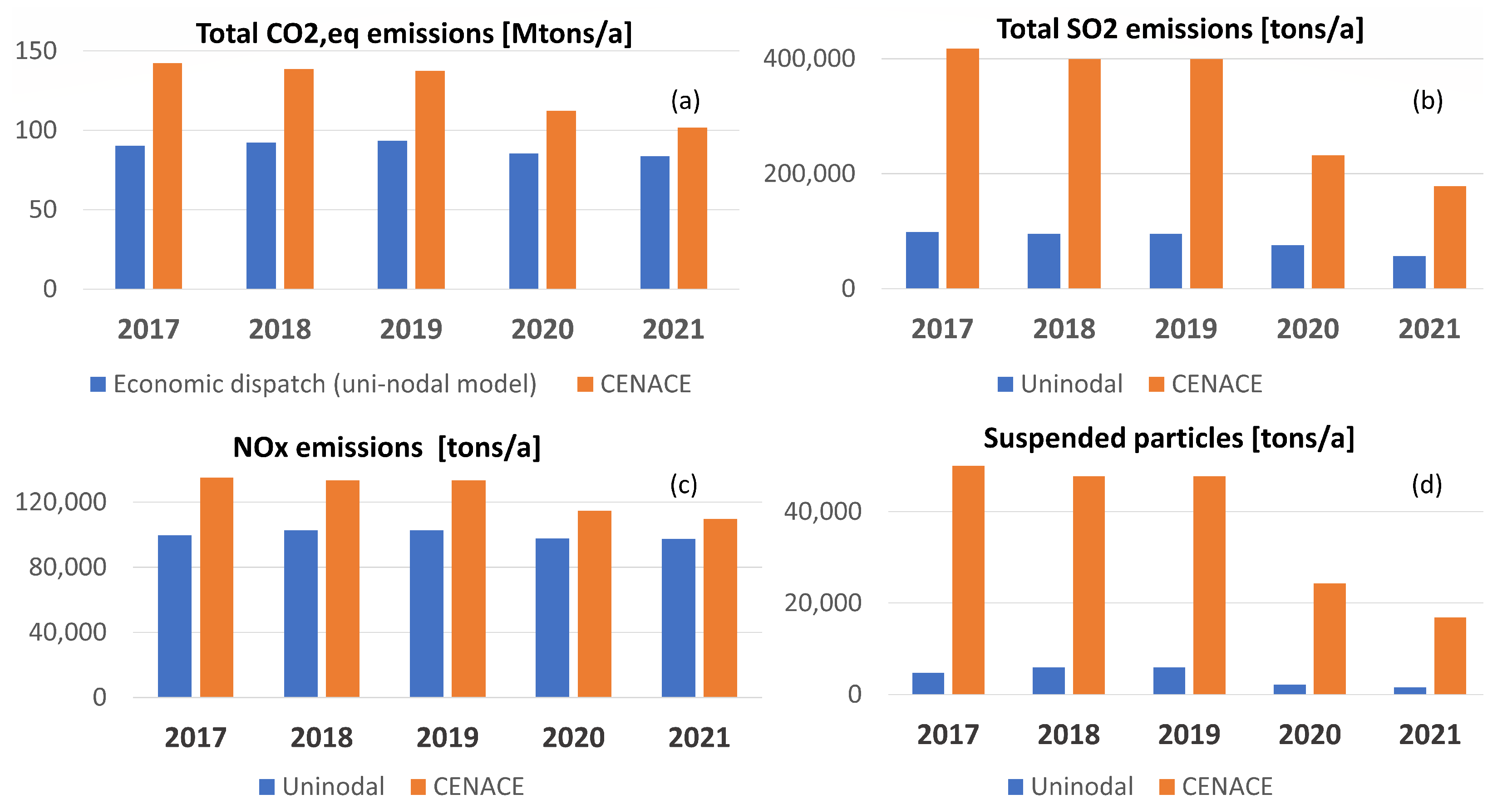

It can be seen from Figure 4 that both greenhouse gases and local/regional emissions are significantly higher in practice than expected from an ideal dispatch based on economic merit alone. As shown in Figure 4a, the CO emissions were about 50% higher in 2017 compared to the economic dispatch emissions, at about 142 Mtons/a, compared to 90 Mtons/a for the economic dispatch. In the following years, this discrepancy diminished, as the real dispatch by CENACE reflected a stronger participation by wind and solar. Regarding SO emissions, the difference between the ideal case and the real dispatch is quite abysmal; while the emissions for the optimal case would have amounted to approximately 50,000 tons of SO per year in 2017, the power plants actually dispatched produced an estimated flow of SO emissions of over 400,000 tons/year. Evidently, this large discrepancy between the ideal and the real case can be traced back to the much larger generation by steam plants, both coal-fired plants and (partially) those fired with fuel oil. Given this out-sized impact of these fuel/technology combinations, the benefits of reducing their participation in electricity generation is also particularly large. This occurred during 2020 and 2021 when a large fraction of the coal-fired and other steam generation was displaced by the increasing generation of wind and solar.

Figure 4.

Comparison of the total system emissions for the actual dispatch (CENACE) and the ideal (one-node) economic dispatch: (a) CO emissions. (b) SO emissions. (c) NO emissions. (d) Particle emissions.

It should be noted, however, that the reduction in SO emissions due to the partial displacement of coal and other steam generation may be somewhat optimistic, as in all cases shown in Figure 4 it has been assumed that the fuel mix used at steam plants was maintained at approximately 85% natural gas and 15% fuel oil. As will be argued in the discussion section, this may not be true, because the government during recent years has strongly campaigned in favor of burning fuel oil instead of natural gas in steam plants.

The discrepancy between the ideal and the real case is even more pronounced for particle (PM10) emissions, where the 2017 flow of particles was towering at approximately 50,000 tons/a, approximately 10 times higher than amount that would have been emitted in the ideal dispatch case (approximately 5000 tons/a).

3.4. Evolution of Regional Generation Demand Balances

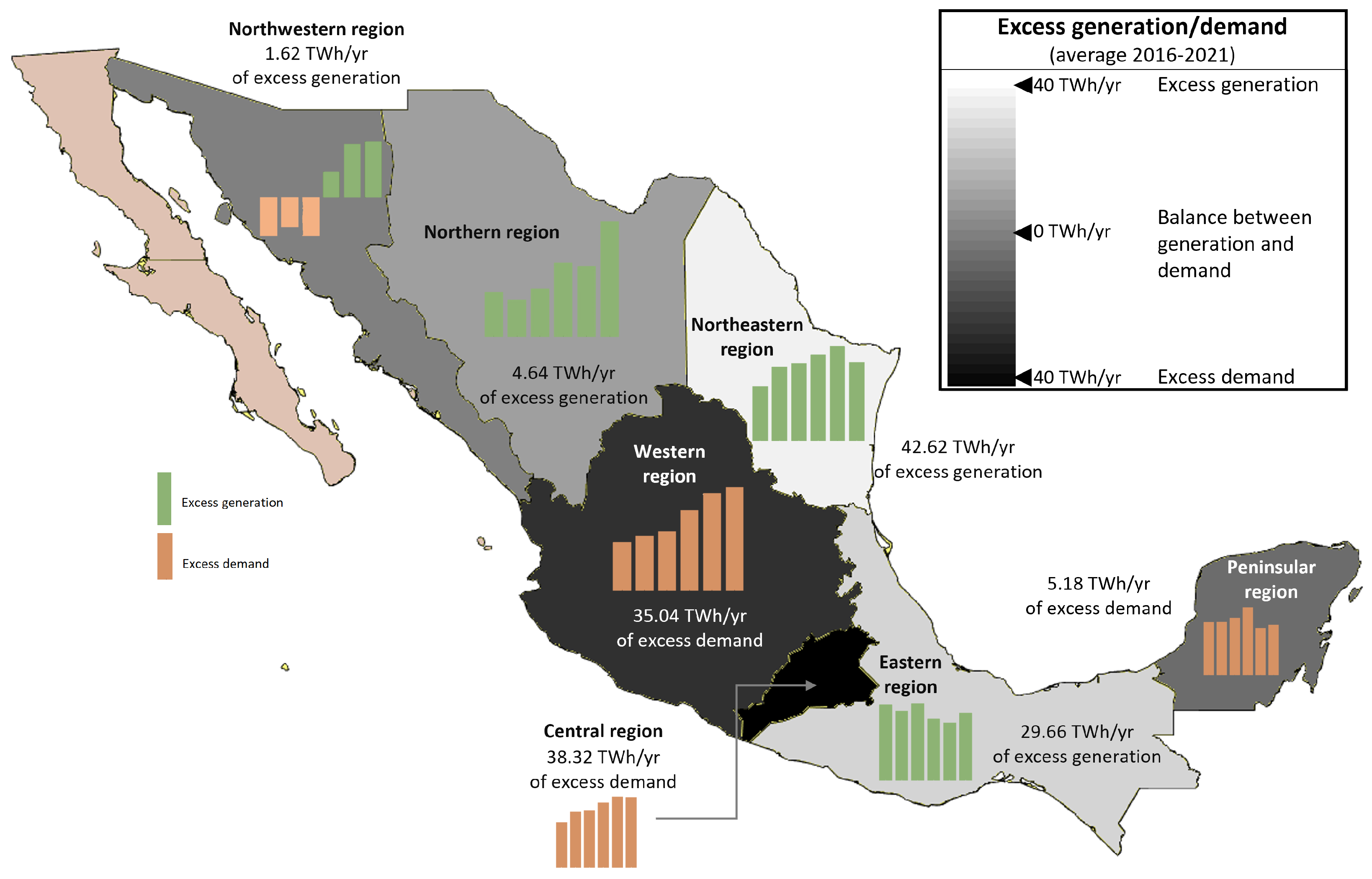

Before turning to the effect of transmission restrictions on the economic dispatch of generation, it is instructive to study where cost-effective generation capacity has emerged over the last five years, and what conclusions can be drawn from these observations with regards to transmission upgrades. Figure 5 depicts the seven regions which make up the National Interconnected System (SIN) together with bar graphs showing the evolution of the dispatched generation, again without considering existing transmission constraints. This represents a baseline view of where transmission reinforcements would have to be built if the existing efficient generation were to be honored.

Figure 5.

Evolution of the generation in each of the regions of the SIN (2017–2021).

It can be seen that, in general, regions 2 and 6 stand out in their roles of cost-effective providers of electricity. In region 2 (“East”), large-scale hydro has long been the main technology, more recently enhanced by large-scale wind capacity, located mostly in the La Ventosa area in the Isthmus of Tehuantepec region. Mexico’s only nuclear power station is also located in this region. Region 6 (“Northeast”), on the other hand, has long been characterized by combined-cycle plants operating with generally cheap natural gas, most of which is nowadays imported from the US. The northeast has also seen a significant deployment of wind farms in recent years.

Other regions that have experienced significant growth in cost-effective generation capacity, as evidenced by their strongly increased participation in the unrestricted economic dispatch, are region 4 (“Northwest”) and 5 (“North”). Region 4 has grown both in combined cycle plants, spurred by the proximity of the US border and the availability of cheap imported natural gas, as well as in solar photovoltaic power plants. Region 5 has both combined cycle plants, and a number of recently installed wind farms.

The increase in economic dispatch in the aforementioned regions, to the extent that it does not fuel the general consumption growth, necessarily has to be compensated by reductions in dispatch of power plants with higher marginal cost. As evidenced by Figure 5, these reductions occur both in region 3 (“West”) and region 1 (“Central”). This insinuates that stronger transmission ties between the growth regions in the north and the de-growth regions in the center might be called for.

A stronger case for this argument can be built if not only the dispatched generation but also the balance between generation and demand within each of the regions is considered. As shown by Figure 6, regions 1 (central), 3 (west), and the peninsular region 7 have indeed evolved into net importers of (cheap) electricity, or at least would be if an unrestricted system-wide dispatch were to be applied. This evolution in the availability evidently calls for a reinforcement of the transmission corridors to facilitate the flow of cheap electricity from net exporting to net importing regions.

Figure 6.

Net balance between generation and demand by region for the 2020–2021 period and the unrestricted economic dispatch case).

3.4.1. The Impact of Flow Restrictions

To this point, all reported results corresponded to an ideal economic dispatch where power is allowed to flow freely between nodes in order to minimize the total cost function of the system. In the presence of flow restrictions, the results of economic dispatch were expected to change. The results of the corresponding analyses are reported in Table 3 for the years 2017–2019 and in Table 4 for 2020 and 2021. It can be seen from the tables that consideration of the flow restrictions reduces the differences between the reported dispatch, allowing for some generation from steam plants to become economically viable. In the case of coal-fired generation, the participation increases to about 3% in most years if the multi-node model is used, up from typical values of approximately 1% in the case of the ideal (one-node) dispatch. In the case of steam-based generation (using either natural gas or fuel oil), the ideal economic dispatch had practically no participation of this technology, whereas in the multi-node case its participation node fares at approximately 3%.

Table 3.

Reported generation figures compared to the results of the economic dispatch model developed in this work for 2017 through 2019. CENACE = official reported dispatch. One-node: results of the model without flow restrictions. Multi-node: results of the model with flow restrictions.

Table 4.

Reported generation figures compared to the results of the economic dispatch model developed in this work for 2020 and 2021. CENACE = official reported dispatch. One-node: results of the model without flow restrictions. Multi-node: results of the model with flow restrictions.

In the case of wind and solar, it can be seen that the generation figures from the multi-node case almost exactly match the official figures (with the exception of the wind generation in 2017 and 2018 which are still slightly higher than the reported numbers, albeit closer than in the one-node case). Similarly, the generation figures for single-cycle gas turbines (generally used to generate during peak hours) are a very good match with the official numbers.

Before turning to a systematic discussion it worth restating the quite general conclusions that can already be drawn from the findings so far:

- The available generation mix in Mexico would have allowed the generation of electricity with significantly lower emissions, both of greenhouse gases and local/regional pollutants, if power plants had been dispatched based on economic criteria alone.

- The restrictions in power transfer capacity between the nodes of the National Transmission Grid do explain some of the discrepancies, but fail to explain the still substantial generation in conventional steam plants, both based on coal firing, and on natural gas and fuel oil, respectively.

- The growth in cost-effective generation capacity in the northwestern, northern, and northeastern regions of the National Electric System, a major portion of which correspond to wind and solar generation in high-resource areas, calls for a reinforcement of the transmission grid in order to approach cheap and clean(er) electricity to the major load of the central area of Mexico and the western area, where a large part of the population is located.

3.4.2. Exploring the Effect of Out-of-Merit Order Dispatch

While the systematic exploration of congestion in the system is not part of the scope of the present study it is interesting to briefly explore the effect of possible out-of-merit order dispatch actions. As shown above, coal-fired power plants would be hardly dispatched based on economic merit alone (Table 2). If transmission restrictions are figured in, some coal generation is allocated, but even in this scenario the dispatched energy remains far below the officially reported figures (Table 3 and Table 4). As reported by the Secretary of Energy in the 2018–2032 version of their sector planning document PRODESEN [27], two transmission corridors connected to coal-fired plants are pointed out as being frequently congested: (1) The corridor connecting the node “Río Escondido”, located near the Mexico–US border with its two coal-fired power stations (José López Portillo and Carbón II), with the node “Chihuahua” to the west, and (2) the corridor connecting the node “Lázaro Cárdenas”, located at the Pacific coast with its coal power station complex Petacalco with its total installed capacity of about 2000 MW and the conventional steam power plant complex Francisco Pérez Ríos, with a total installed capacity of 1500 MW, with the node “Central” [27]. Both corridors appear uncongested in our simulations. If, however, these fossil fuel-powered generation complexes at nodes “Río Escondido” and “Lázaro Cárdenas” are forced to operate at about 80% of their installed capacity, then congestion can be seen to occur.

Security constraints in the Mexican grid are accounted for in the AUGC process (the Spanish acronym for reliability-based unit commitment, the methodology and results of which are not in the public domain). It is therefore theoretically possible to attribute the unusually high dispatch levels of fossil fuel power stations to concerns about dispatch security, such as voltage stability, but the proof cannot be made unless the information is made available to public scrutiny. In any case, the generation levels required to produce the reported congestion in transmission corridors far exceed plausible levels required for voltage control and other reliability concerns.

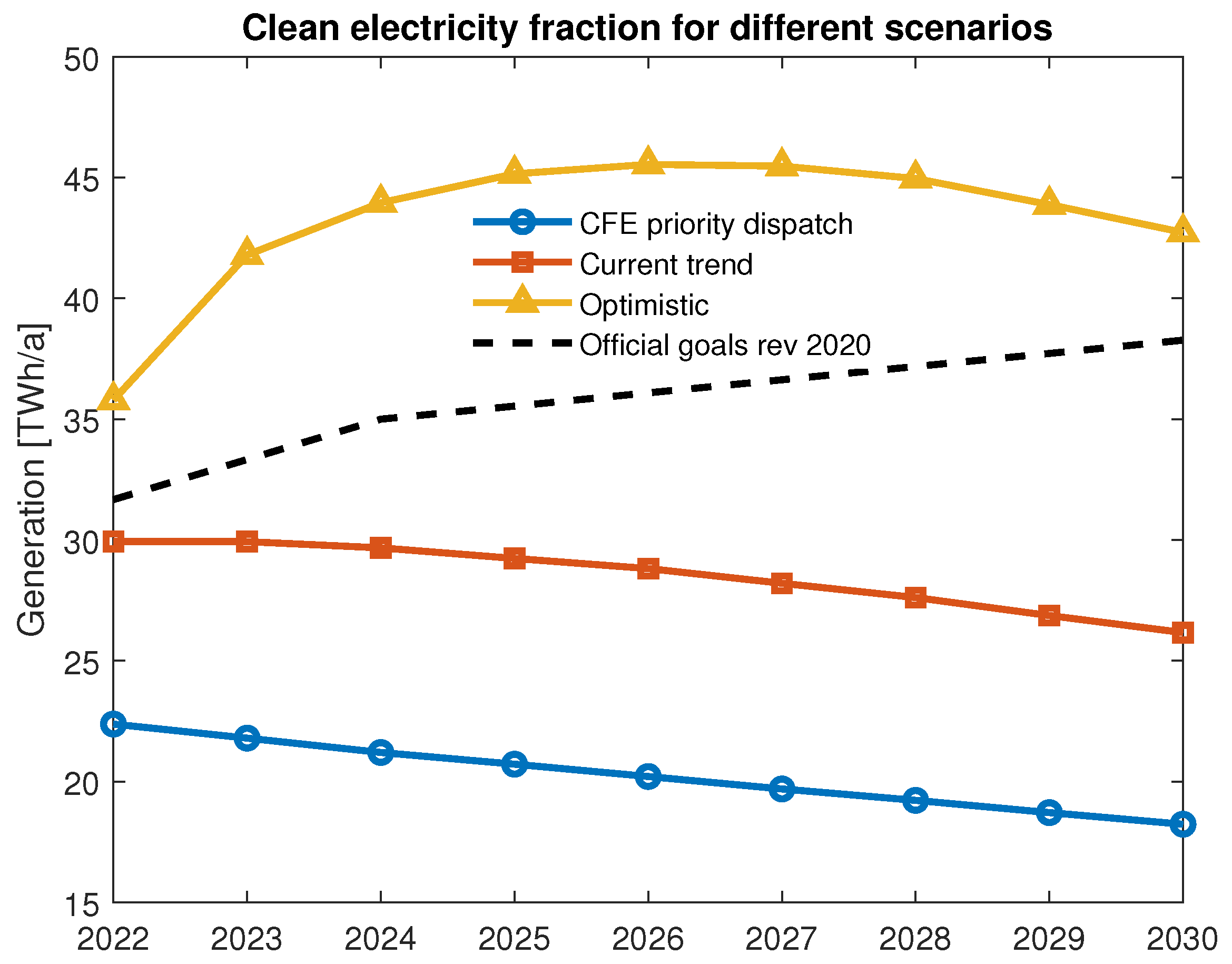

3.5. Future Scenarios

3.5.1. Projected Evolution by Technology

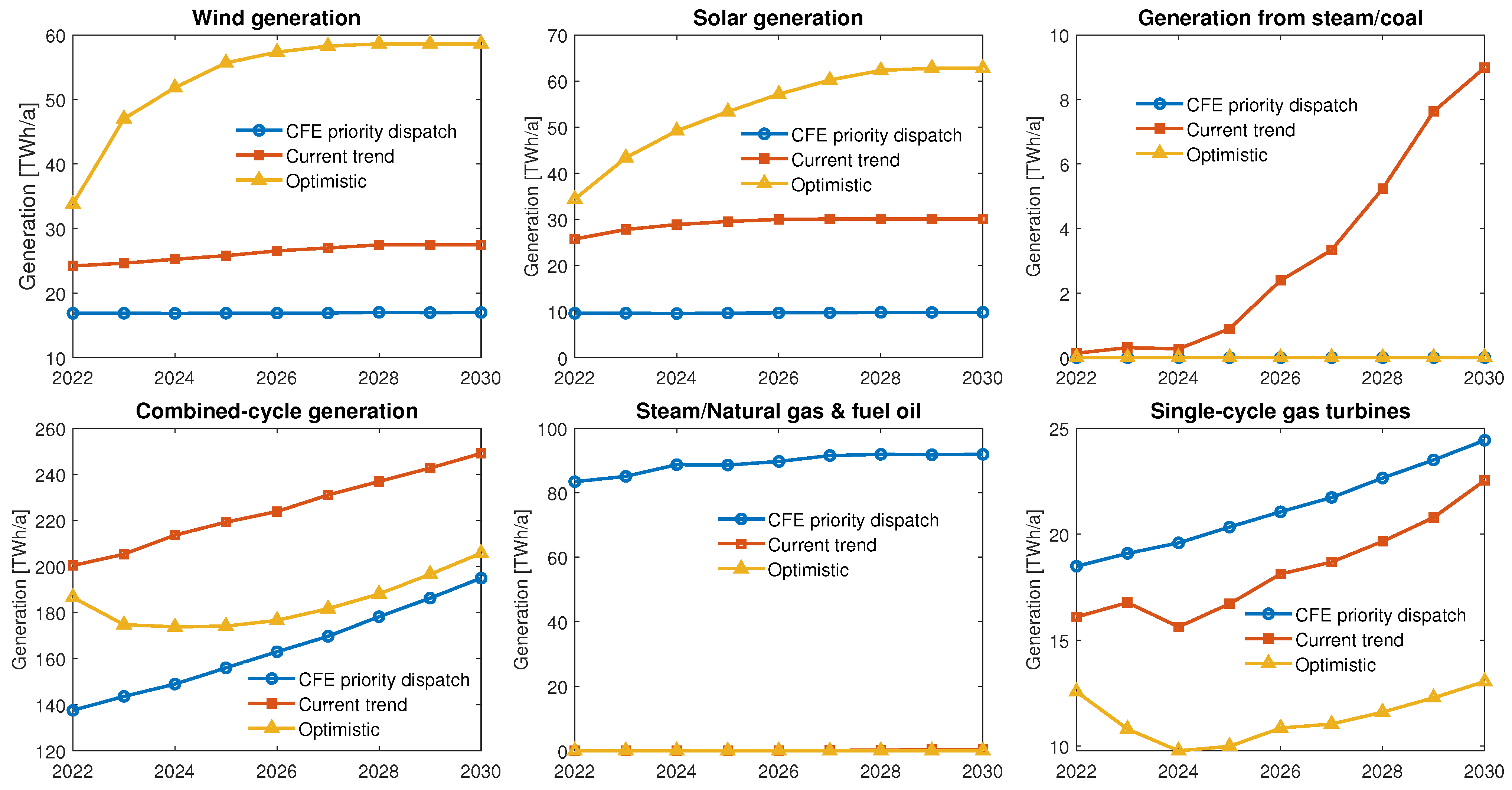

As described in the methodology section, three scenarios for the relatively near future, i.e., for 2022 through 2030 have been analyzed in this work. This period is generally recognized as critical to the global effort of limiting exposure of the world economy and global ecosystems to the effects of climate change. The baseline scenario (tagged “current trend” in Figure 7) corresponds to a continuation of the situation where new permits for privately financed generation projects, and therefore most of potential renewable energy pipeline, is blocked by the federal authorities and already ready-to-operate projects are not allowed to enter commercial operation. As shown by Figure 7, under this scenario the generation from wind energy would moderately grow from about 24 TWh/a in 2022 to about 28 TWh/a in 2028 and then reach saturation. Solar generation would continue to climb somewhat from its 2022 value of about 26 TWh/a, reaching 30 TWh/a by 2026/2027 and staying constant from thereon.

Figure 7.

Generation scenarios through 2030.

Most of the projected demand growth in this baseline scenario would be carried by fossil fuel fired plants, the generation of which would increase from 200 TWh/a in 2022 to approximately 250 TWh/a at the end of the decade. Coal-fired generation would also see a significant increase (albeit at low levels), reaching approximately 9 TWh/a by 2030. Generation from single-cycle gas turbines would also increase from about 16 TWh/a in 2022 to over 22 TWh/a in 2030. Generation from steam plants, fueled by natural gas and fuel would remain unimportant. It should be noted that the model assumptions with regards to fuel oil fired plants in this baseline scenario may be somewhat too optimistic to reflect the actual current status. See the discussion for further details.

The “optimistic” scenario, as the reader may recall from the methodology section, is somewhat less bright than the name appears to imply. In this case, it is still assumed that the current policies, focused on pushing back on private-sector generation, will remain in place. However, it is assumed that most of the (considerable) renewable energy pipeline (both fully constructed plants and projects in advanced stages) will eventually come into operation. As shown by Figure 7, in this scenario most wind and solar generation will continue to rise steeply for a few years and then reach a saturation line at generation levels of about 60 TWh/a for either technology, or a combined renewable energy generation of 120 TWh/a, about half of the projected generation from natural gas-fired combined-cycle generation in 2030.

In the final analysis, the results for a scenario where the dispatch would be determined not on economic grounds, but based on plant ownership, with plants owned by the state-owned utility CFE receiving priority rights and privately owned plants relegated to picking up the slack. In this case, wind and solar generation would be severely curtailed to about 35–45% of its theoretical generation. This would evidently be a severe blow to those facilities, most of which have been built in recent years and therefore still have long-term financial liabilities. Given the considerable uncertainties associated with this scenario, no attempt was made to model the additional reductions that might occur due to bankruptcy and premature shutdown of some of the affected wind and solar plants.

The greatest winners of the priority dispatch for the state utility CFE would be the thermal power plants based on steam cycles, many of which are currently burning fuel oil, the production of which would increase at the expense of both the renewable energy generation and, somewhat surprisingly, also some of the combined-cycle generation. The reason for this lies with the fact that a substantial portion of the combined-cycle plants of the Mexican electricity system is owned and operated by private companies under the legacy schemes known as Independent Power Producers (IPPs, see the methodology section for further details). Even though IPPs have long-term contracts with the exclusive purpose of generating for CFE, under the reformed Electricity Industry Law of 2021 their dispatch would have been subject to a new approval process by CFE, and their place in the dispatch stack would likely be after all of CFE-owned assets.

3.5.2. Clean Energy Fractions and Emissions

A relevant question is, of course, how these projected generation scenarios translate into the fraction of electricity that is generated from clean technologies, in terms of the Electricity Industry Law. It should be recalled that nuclear power is explicitly included as a source of clean electricity in the Mexican context. Based on this assumption, the generation results shown above, and the fuel mix used (see the methodology section and the discussion for further information) a prediction of the clean electricity fraction can be made. The results are shown in Figure 8.

Figure 8.

Clean electricity fractions in the different scenarios.

It can be seen from the figure that the results vary quite drastically between the three scenarios. Only in the optimistic scenario are Mexico’s clean electricity goals met for 2024 (35% goal) and 2030 (approximately 38%). In this case, the inertia associated with the projects that are either in advanced stages of their development or are already ready to operate would allow a maximum clean electricity fraction of around 45% by the mid-decade, followed by a decrease afterwards caused by the continuing growth of electricity consumption and a stalled development of clean electricity plants.

In the more realistic scenario based on current policies, the clean energy fraction would continuously fall from its highest figure at the beginning of the modeling period to about 26% at the end of the decade, missing the target by about 12 points.

In the CFE priority dispatch case, the situation would be significantly worse, with only about 22% percent of the electricity coming from clean sources immediately after CFE priority dispatch has been enacted and dropping to approximately 18% at the end of the decade. Similar to the baseline case, the role of clean, particularly renewable, energy would gradually lose importance, albeit at an even lower level due to the curtailment of wind and solar plants.

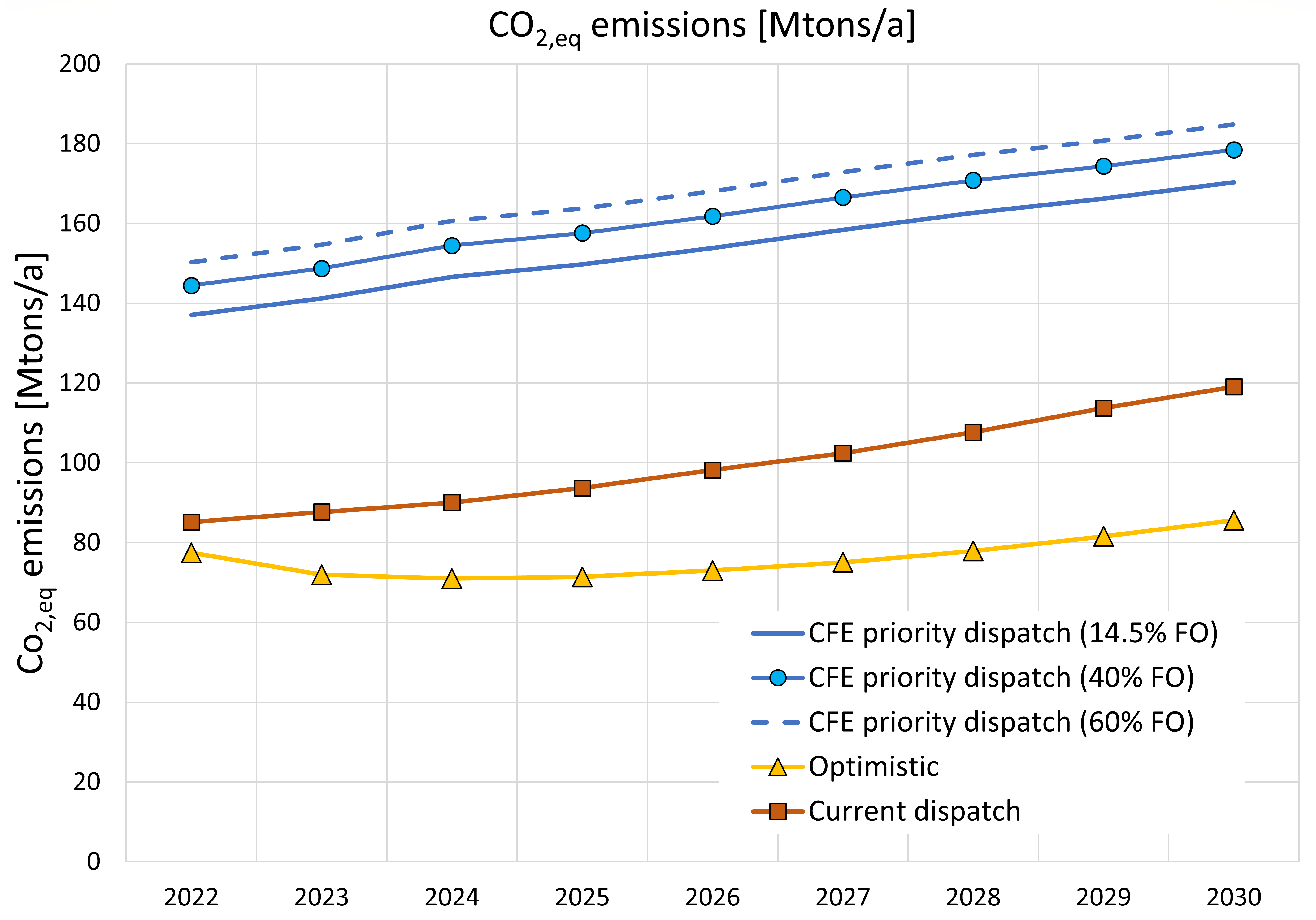

Figure 9 shows how the different dispatch policies and scenarios translate into the projected greenhouse gas (GHG) emissions for the 2022–2030 period. The main apparent difference is the large gap between the scenarios associated with CFE priority dispatch, given the strong focus of the CFE fleet on fossil fueled power plants and the old ages of many of the conventional steam plants and their associated high heat rates. Not unexpectedly, the usage of heavy fuel oil also has a large impact on GHG emissions, but the differences are much smaller than the gap between the CFE priority dispatch and the other scenarios. It is clear that any legislation enabling such a priority dispatch of the state utility would dramatically increase Mexico’s GHG emissions. It is worth noting, however, that even in the most optimistic scenario, Mexico’s GHG emissions would only slightly decrease, and only through 2025, after which emissions would increase again. Further investments in clean generation beyond the existing pipeline are therefore necessary for a lasting contribution by Mexico to the shared mitigation responsibility.

Figure 9.

Projected CO emissions in the different scenarios.

4. Discussion

As shown in the results section, Mexico is currently on track to dramatically missing its domestic clean electricity targets for the rest of the decade. Consequently, it is also likely to fail to comply with the nationally determined contributions (NDCs) to climate change mitigation established as part of the Paris Climate Accords, given that Mexico’s NDCs heavily rely on the (partial) decarbonization of the electricity sector; however, a discussion of the non-electricity portion of those targets is beyond the scope of this work.

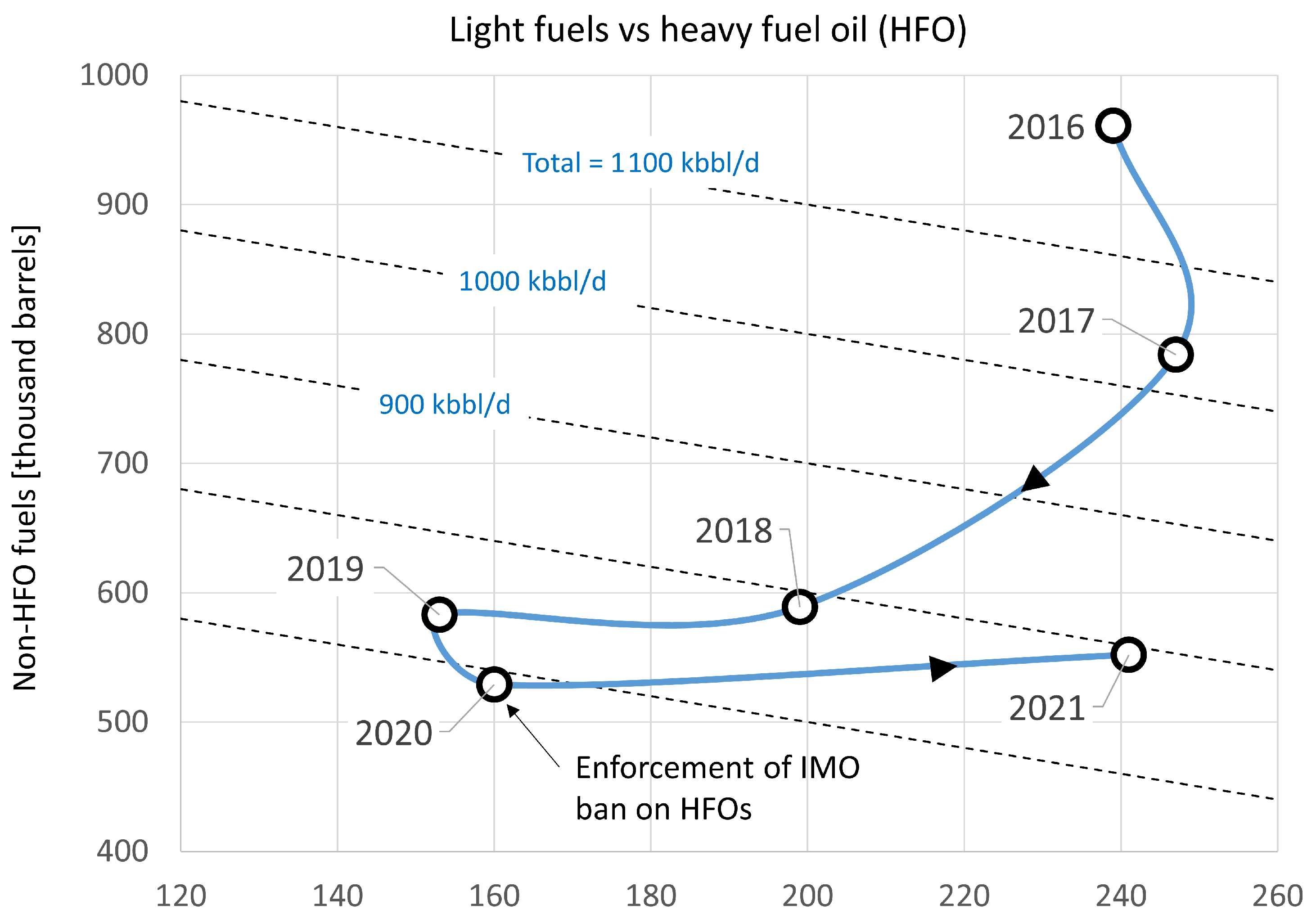

This complete change of strategy for the development of the electricity sector can largely be attributed to the crackdown on private investments in the sector, which have largely (albeit not exclusively) focused on wind and solar projects. The stalling of renewable energy projects is therefore mostly collateral damage of the government’s attempt to undo the effects of the 2014 electricity sector reform, which allowed for competition in generation and a limited participation in commercialization of electricity (through the qualified user/supplier scheme). This is, however, only part of the story; the other driver behind the obstruction of renewable energy participation appears to lie with the surplus production of excess heavy fuel oil (HFO) originating from ambitious refining targets in the absence of adequate infrastructure for refining heavy crude oils.

The results of this situation can be shown empirically by tracking the reported quantities of refined barrels of crude oil and their breakdown. As shown in Figure 10, where the evolution of the refinery results have been visualized as a trajectory in a plane spanned by light fuels (gasoline, diesel fuel, kerosene, LP gas, and others) vs. fuel oil. Fuel oil is generally considered a residue, and is typically kept under 1% in state-of-the-art refineries [28]. As demonstrated by Figure 10, the total volume of refined crude oil (as measured by the set of dotted straight lines) has been falling monotonically from 2016 through 2020, when a little under 700 kbbl/day of crude oil was refined, compared to approximately 1200 kbbl/day in 2016, while the overall throughput had declined during this period; at least during part of the period a drastic reduction in the production of fuel oil had also been achieved. Between 2017 and 2019, the fuel oil output fell from nearly 250 kbbl/day to a little over 150 kbbl/day (a reduction of approximately 40%), even though the production in light fuels had diminished only by approximately 25%, a clear gain in efficiency. This trend was reversed during 2019–2021, with a dramatic jump in fuel oil production from 2020 to 2021. In 2021, about 30% of all refinery products (240 kbbl/day out of approximately 800 kbbl/day) were fuel oil. This potentially creates a surplus situation, because one of the traditional markets, large maritime vessels, is now largely barred from using high-sulfur fuel oil (HSFO) since the International Maritime Organization (IME) started enforcing its ban on HSFO (i.e., fuel with a sulfur content higher than 0.5%) in 2020. While some shippers appear to be installing scrubbers and others may be willing to pay the fine for compliance, it does imply a drastic reduction in possible off-take options.

Figure 10.

Fuel oil trajectory for the period from 2016 to 2021, showing the production of light fuels (gasoline, diesel fuel, kerosene, LP gas, and others) vs. the production of heavy fuel oil (HFO). Data from [29].

It is instructive to assess the combined impact of energy policy and fuel usage on emissions in different scenarios. In addition to the three policy scenarios discussed previously, three fuel oil scenarios have been introduced. This accounts for the fact that it is difficult to anticipate how much of the excess fuel oil produced at PEMEX refineries will end up being burned in the conventional steam plants operated by CFE. Based on the name-plate specifications and the costs of fuel oil and natural gas, the fuel oil consumption in the base case can be estimated to be around 20 kbbl/day, or around 14.5 % of all fuel consumed in conventional steam plant. This is only about 10 % of the 240 kbbl/day of fuel produced by PEMEX refineries in 2021. Under current dispatch rules, based on security-restricted economic dispatch, it would be difficult to justify higher percentages of fuel oil use in power plants, unless either (1) PEMEX were to offer their fuel oil well below historical market prices or (2) CENACE were instructed to assign fuel oil operated power plants using the “out-of-merit order” dispatch option specified in the grid code and allowing CENACE to modify the (security-constrained) economic dispatch on the grounds of (quite generically specified) reliability reasons. Based on media coverage [30], a combination of both may already be happening. According to Barnés de Castro and Salazar [31], even the coal power plant at Petacalco is now burning fuel oil.

If some version of a CFE priority dispatch were to be enabled, however, power plants burning fuel oil could be dispatched quite generally, with no need for resorting to special commercial agreements between PEMEX and CFE or reliability arguments. It would be then the sole decision of CFE to use these fuels or not. It is then easily imaginable that higher fractions of the surplus fuel, depending on the conditions of alternative offtake markets and the progress with the modernization of the refinery industry in Mexico, would be used in power plants. In order account for the uncertainties mentioned, three scenarios for the fuel oil fraction used in conventional steam plants were considered in this study: (1) 14.5%, (2) 40%, and (3) 60%. No sustained fuel oil usage in coal plants was considered because this use is believed to create irreversible damage in coal plants, which is why coal plants cannot be realistically operated with fuel oil during extended periods of time.

The results for emissions of CO and polluting gases (SO, NO, and suspended particles) are shown in the tables below. Given the high sulfur content of Mexican heavy fuel oil, the increase in SO emissions in the CFE priority dispatch case is the most notorious effect (Table 5). Emissions in this case are orders of magnitude higher than in the cases where economic dispatch is still the rule (“current dispatch”) and where additionally the renewable energy pipeline is allowed to reach commercial operation (“optimistic”).

Table 5.

SO emissions [ktons/a] for the 2022–2030 period, considering the different scenarios and different fuel oil usages.

Similarly, emissions of NO (Table 6) and suspended particles (Table 7) can be seen to rise dramatically in such a scenario. This would disproportionately affect cities and communities already suffering poor air quality, some of which had seen some improvements in the past because of the substitution of fuel oil by natural gas. One example is the conventional steam plant in Tula and the adjacent refinery, which have shown to collectively account for a large fraction of the load of polluting gases in the nearby Mexico City, in addition to heavily affecting the local air quality [32].

Table 6.

NO emissions [ktons/a] for the 2022–2030 period, considering the different scenarios and different fuel oil usages.

Table 7.

Total emissions of suspended particles [ktons/a] for the 2022–2030 period, considering the different scenarios and different fuel oil usages.

While the continued use of conventional steam plants, even those than had been scheduled in the past for retirement, because of old age and low efficiency, can be expected in any scenario, the use of fuel oil can be expected to decline over time given the ambitious modernization activities in the refinery sector carried out by the federal government. Providing PEMEX refineries with improved capabilities for refining heavy crude oils is among the stated objectives of federal energy policy, so the fraction of fuel oil output from Mexican refineries can be expected to come down gradually over the years. It should be noted, however, that such a reduction would be subject to discretionary decisions by CFE and PEMEX, rather than responding to the workings of the electricity market or to environmental concerns.

5. Conclusions and Policy Recommendations

A detailed assessment of the electricity dispatch in the Mexican National Interconnected System has been conducted for the 2017–2021 period, corresponding to the first full five years of operation of the wholesale electricity market introduced after the electricity sector reform in 2013/2014. A comprehensive generator database was constructed from public and non-public sources and extensively cross-validated. The database contains both operational generators and those sitting at some point of the permitting pipeline, including those with fully built-out infrastructure and completed functional tests. This information on the potential future generation capacity allowed us to conduct some realistic explorations of future pathways. Our assessment of the 2017–2021 dispatch data reveals that conventional steam plants (operating with either natural gas or fuel oil) and coal-fired plants have been dispatched at far higher levels than expected from (ideal) economic dispatch, even though their dispatch has declined over the years as wind and solar generation have made their way into the system. It was possible to show that part of this economic (and environmental) inefficiencies can be explained by transmission constraints, as the transmission-constrained dispatch called for somewhat higher participation of conventional steam and coal-fired plants. Our analysis does not evidence significant curtailment of wind and solar generation during the modeling period, as the officially reported and the modeled wind and solar generation figures are roughly consistent.

Though the extension of the supply of natural gas has traditionally been a priority in electricity sector expansion planning, the present appears to be marked rather by the oversupply of fuel oil, leading to the substitution of natural gas in conventional steam plants that had in the past been equipped for duel fuel use, with the priority given to natural gas, by fuel oil. The same appears to be happening at least one coal power plant. A greater use of fuel would be critical in the case of the priority dispatch for the state utility CFE put forward by the federal government because this scheme would allow CFE to use the amount of fuel oil deemed convenient without restrictions from economic dispatch or environmental concerns. The increase in polluting emissions, particularly SO, NO, and suspended particles, would be staggering, with emission levels several orders of magnitude larger than in scenarios with economic dispatch, strongly affecting the regional air quality in large population centers, including the Mexico City area.

As for clean electricity targets, in none of the scenarios studied deemed plausible or realistic at the time of writing is there a clear pathway towards decarbonization in compliance with the Paris climate change mitigation process. In the “optimistic” scenario modeled, where 90% of all clean electricity projects currently in the development pipeline would eventually come to fruition, the 2024 clean electricity target (35%) would be met, as well as the revised 2030 target (38.7%), though not the original 50% target for 2030 established in the first version of the Energy Transition Law. However, the clean electricity fraction would start declining again by the middle of the decade. In the case of the other scenarios (current dispatch, but with great difficulties for new projects to enter the market) and the CFE priority dispatch scenario, the situation is much worse, with the clean electricity targets being missed by large margins. In the case of the CFE priority dispatch scenario, the clean electricity level would drop consistently over the decade, finishing at about 18%.

A clear strategy for the deep decarbonization of the electricity sector and the Mexican economy is required to bring Mexico in line with its national and international commitments and to rejoin the Paris process for the protection of the global climate and the interests of current and future generations. While a recent announcement at COP27 [33] appears to point to somewhat increased ambitions, the practical impacts remain to be seen. As shown in this work, leveraging the considerable renewable energy development pipeline would go a long way towards meeting Mexico’s recently announced ambitions. The full realization of this potential is likely to require significant investments in the transmission sector (see [34] for a comprehensive review of grid integration costs), so establishing clear policies for assigning profits of the state transmission company, as well as for private sector participation in the transmission sector is vital.

The present work was designed as a diagnostic study, with a focus on the performance of the Mexican power sector in terms of its clean electricity fraction and emissions, as opposed to a grid integration and expansion study. It can, however, be expanded to study specific grid expansion scenarios, discuss the role of congestion, and guide the decarbonization of the Mexican power sector under the light of the recent announcements at COP27. These tasks will be tackled in follow-up work.

Author Contributions

Conceptualization, O.P. and A.L.-T.; methodology, O.P. and A.V.T.-S.; software, K.M. and O.P.; validation, O.P., K.M. and A.V.T.-S.; investigation, K.M., A.V.T.-S. and O.P.; data curation, K.M. and O.P.; writing—original draft preparation, O.P.; writing—review and editing, O.P.; visualization, K.M. and O.P.; supervision, O.P. and A.L.-T. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

Anonymized versions of the databases, if not explicitly covered by confidentiality agreements, can be requested from the corresponding author (oprobst@tec.mx).

Acknowledgments

K.M. is grateful for a CONACYT M.Sc. stipend and to Tecnológico de Monterrey for granting a full tuition waver for the M.Sc. program in Engineering Sciences. O.P. and A.L. appreciate support from the School of Engineering and Sciences at Tecnológico de Monterrey. A.T. acknowledges the time granted by V-iridium Oak Creek Renewables for contributing to this research.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Climate Watch. Historical GHG Emissions. Data Explorer. Available online: https://www.climatewatchdata.org/data-explorer/ (accessed on 8 October 2022).

- SEMARNAT. Compromisos de Mitigación y Adaptación 2020–2030. Available online: https://www.gob.mx/semarnat/articulos/compromisos-de-mitigacion-y-adaptacion-2020-2030 (accessed on 8 October 2022).

- SEGOB. Diario Oficial de la Federación, 2016. Acuerdo por el que la Secretaría de Energía Aprueba y Publica la Primera Estrategia de Transición para Promover el Uso de Tecnologías y Combustibles más Limpios, en términos de la Ley de Transición Energética. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5463923&fecha=02/12/2016#gsc.tab=0 (accessed on 8 October 2022).

- SEGOB. Diario Oficial de la Federación 2020. Acuerdo por el que la Secretaría de Energía Aprueba y Publica la Actualización de la Primera Estrategia de Transición para Promover el Uso de Tecnologías y Combustibles más Limpios, en téRminos de la Ley de Transición Energética. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5585823&fecha=07/02/2020#gsc.tab=0 (accessed on 8 October 2022).

- Llamas, A.; Probst, O. On the role of efficient cogeneration for meeting Mexico’s clean energy goals. Energy Policy 2018, 112, 173–183. [Google Scholar] [CrossRef]

- SEGOB. Diario Oficial de la Federación. Ley General de Cambio Climático; 2012. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5249899&fecha=06/06/2012#gsc.tab=0 (accessed on 8 October 2022).

- SEGOB. Diario Oficial de la Federación. Ley de Transición Energética; 2015. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5421295&fecha=24/12/2015#gsc.tab=0 (accessed on 8 October 2022).

- SEGOB. Diario Oficial de la Federación. Ley de la Industria Eláctrica; 2014. Available online: https://www.dof.gob.mx/nota_detalle.php?codigo=5355986&fecha=11/08/2014#gsc.tab=0 (accessed on 8 October 2022).

- Updated: Mexico’s Energy Auction Just Logged the Lowest Solar Power Price on the Planet. November 2017. Available online: https://www.greentechmedia.com/articles/read/mexico-auction-bids-lowest-solar-wind-price-on-the-planet (accessed on 8 October 2022).

- Reportes Sobre el Desempeño y la Evaluación del Mercado Eléctrico Mayoristas (2017–2020). Available online: https://www.gob.mx/cre/documentos/reportes-sobre-el-desempeno-y-la-evaluacion-del-mercado-electrico-mayorista (accessed on 8 October 2022).

- Bracho, R.; José, O.; Fernández, G.; Brancucci, C.; Peluso, A.; Alvarez, J.D.; Flammini, M.; Bracho, R.; José, O.; Fernández, G.; et al. Impacts Analysis of Amendments to Mexico’s Unit Commitment and Dispatch Rules; Technical Report; NREL: Golden, CO, USA, 2022.

- Bracho, R.; Alvarez, J.; Aznar, A.; Brancucci, C.; Brinkman, G.; Cooperman, A.; Flores-Espino, F.; Frazier, W.; Gearhart, C.; José, O.; et al. Mexico Clean Energy Report—Executive Summary; Technical Report; NREL: Golden, CO, USA, 2021.

- Buira, D.; Tovilla, J.; Farbes, J.; Jones, R.; Haley, B.; Gastelum, D. A whole-economy Deep Decarbonization Pathway for Mexico. Energy Strat. Rev. 2021, 33, 100578. [Google Scholar] [CrossRef]

- Ramirez-Sanchez, E.; Evangelista-Palma, G.; Gutierrez-Navarro, D.; Kammen, D.M.; Castellanos, S. Impacts and savings of energy efficiency measures: A case for Mexico’s electrical grid. J. Clean. Prod. 2022, 340, 130826. [Google Scholar] [CrossRef]

- Sarmiento, L.; Molar-Cruz, A.; Avraam, C.; Brown, M.; Rosellón, J.; Siddiqui, S.; Rodríguez, B.S. Mexico and U.S. power systems under variations in natural gas prices. Energy Policy 2021, 156, 112378. [Google Scholar] [CrossRef]

- González-López, R.; Ortiz-Guerrero, N. Integrated analysis of the Mexican electricity sector: Changes during the COVID-19 pandemic. Electr. J. 2022, 35, 107142. [Google Scholar] [CrossRef]

- Tian, Y.; Chang, J.; Wang, Y.; Wang, X.; Zhao, M.; Meng, X.; Guo, A. A method of short-term risk and economic dispatch of the hydro-thermal-wind-PV hybrid system considering spinning reserve requirements. Appl. Energy 2022, 328, 120161. [Google Scholar] [CrossRef]

- Xiang, Y.; Wu, G.; Shen, X.; Ma, Y.; Gou, J.; Xu, W.; Liu, J. Low-carbon economic dispatch of electricity-gas systems. Energy 2021, 226, 120267. [Google Scholar] [CrossRef]

- Zhao, B.; Qian, T.; Tang, W.; Liang, Q. A data-enhanced distributionally robust optimization method for economic dispatch of integrated electricity and natural gas systems with wind uncertainty. Energy 2022, 243, 123113. [Google Scholar] [CrossRef]

- Percino-Picazo, J.C.; Llamas-Terrés, A.R.; Viramontes-Brown, F.A. Analysis of Restructuring the Mexican Electricity Sector to Operate in a Wholesale Energy Market. Energies 2021, 14, 3331. [Google Scholar] [CrossRef]

- Plan de Negocios CFE 2021–2025. Available online: https://www.cfe.mx/finanzas/Documents/Plan%20de%20Negocios%20CFE%202021.pdf (accessed on 8 October 2022).

- Tarín-Santiso, A.V.; Llamas, A.; Probst, O. Assessment of the potential for dynamic uprating of transmission lines in the Mexican National Electric Grid. Electr. Power Syst. Res. 2019, 171, 251–263. [Google Scholar] [CrossRef]

- NREL National Solar Radiation Data Base. Available online: https://nsrdb.nrel.gov/ (accessed on 10 October 2022).

- Mauricio Salazar-García. Optimality of Mexico’s Long-Term Clean Power Auctions & Future Renewable Energy Deployment Planning. Master’s Thesis, Tecnológico de Monterrey, Monterrey, Mexico, December 2019.

- NREL Wind Tool Kit—Mexico. Available online: https://developer.nrel.gov/docs/wind/wind-toolkit/mexico-wtk.download/. (accessed on 10 October 2022).

- Spyros Chatzivasileiadis. Optimal Power Flow (DC-OPF and AC-OPF). DTU Summer School 2018. Available online: https://www.energy-markets-school.dk/wp/wp-content/2018/Presentations/DC_ACOPF_SummerSchool2018.pdf (accessed on 10 October 2022).

- SENER. Programa de Desarrollo del Sector Eléctrico. 2018–2032. Available online: https://www.gob.mx/sener/acciones-y-programas/programa-de-desarrollo-del-sistema-electrico-nacional-33462 (accessed on 8 October 2022).

- Oil and Petroleum Products Explained—Refining Crude Oil. Available online: https://www.eia.gov/energyexplained/oil-and-petroleum-products/refining-crude-oil-inputs-and-outputs.php (accessed on 10 October 2022).

- Karla García, Octavio Amador. Combustóleo Escala a la Cima en Producción de refineríAs de Pemex. El Economista, 8 October 2021. Available online: https://www.eleconomista.com.mx/empresas/Combustoleo-escala-a-la-cima-en-produccion-de-refinerias-de-Pemex-20211008-0028.html (accessed on 10 October 2022).

- MC Denuncia a CFE por el Uso de Combustóleo que Afecta al Valle de México. Expansión Política. 7 May 2022. Available online: https://politica.expansion.mx/mexico/2022/05/07/mc-denuncia-a-cfe-por-el-uso-de-combustoleo-que-afecta-al-valle-de-mexico (accessed on 10 October 2022).

- Barnés de Castro, F.; Salazar, F. Clean Energy Cost-Savings: A Study of Mexico’s Federal Electricity Commission (CFE); White Paper; The Institute of Americas: La Jolla, CA, USA, 2022. [Google Scholar]

- Iniciativa Climática México Estudio Sobre la Influencia de la Termoeléctrica de Tula, Hidalgo, en la Calidad del Aire Regional. Technical Report. Available online: https://www.iniciativaclimatica.org/wp-content/uploads/2021/03/Central-Termoele%cc%81ctrica-Tula.pdf (accessed on 10 October 2022).

- Reuters. Mexico to Raise Climate Emissions Target for First Time since 2016. 8 November 2022. Available online: https://www.reuters.com/business/cop/mexico-raise-climate-emissions-target-first-time-since-2016-2022-11-08/ (accessed on 15 November 2022).

- Heptonstall, P.J.; Gross, R.J.K. A systematic review of the costs and impacts of integrating variable renewables into power grids. Nat. Energy 2021, 6, 72–83. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).