Abstract

This paper aims to simulate and evaluate the impacts of increases and decreases in oil price on industrial sectors in China. We develop an oil-economy computable general equilibrium (OE-CGE) model with crude oil as an important factor in production. The transmission mechanism of crude oil price swings to various industrial sectors is described in the model. We calibrate parameters in the model parameters using input-output data. In addition, we simulate the rise and fall of oil prices in the model and assess the impact of crude oil prices on various industrial sectors. The results show that crude oil price changes have the greatest impact on the output and consumption of crude oil and gas extraction products sector, crude oil refined coke products, and processed nuclear fuel products sector. The investment of public utilities sector is the most sensitive to changes in crude oil price. When the price of crude oil changes, its investment drops significantly. Crude oil price stability is extremely important for investment and output stability in all sectors.

1. Introduction

Crude oil price has fluctuated dramatically over the 20th century. Between 1980 and 1997, crude oil price continued to fall and remained low. Between 1997 and 2008, oil price continued to rise during the two financial crises. From 2008 to the present, oil price has fluctuated frequently and there has been massive oil price increases. Large fluctuations in oil prices can affect not only the production costs of related industries but also the investment decisions of capital markets. If risks are not prevented in time, the economies of countries around the world, especially crude oil-importing countries, will be seriously affected.

China is a major importer of crude oil, and crude oil price fluctuations have a huge impact on the Chinese economy. China’s crude oil production has been increasing year by year, but it is still difficult to meet domestic economic activities. Due to the influence of crude oil reserves and exploration and production technologies, the increase in crude oil demand is greater than the increase in crude oil production, and the domestic supply is insufficient. China’s energy market is highly dependent on the international energy market, and rising crude oil price will increase production and operating costs in various domestic industrial sectors and harm production and operating activities, while falling crude oil price will make the market unbalanced. Therefore, the impact of crude oil price fluctuations on various industrial sectors should be taken seriously. Clarifying how crude oil price fluctuations affect various industries can stabilize the economy to a certain extent and help prevent the risk of oil price fluctuations. It can also provide solutions for industries to avoid risks and reduce economic losses in the event of crude oil price fluctuations.

This paper focuses on the impact of crude oil price fluctuations on consumption, investment, and output in China’s industrial sectors. The possible marginal contributions of this paper are as follows: A crude oil-economy computable general equilibrium model is constructed based on the standard computable general equilibrium model with crude oil as the basic factor of production input. Unlike other literature studies that have examined the impact of crude oil price fluctuations on the overall macroeconomy, this paper uses the CGE model to refine the impact of crude oil price changes on the economy to individual industry sectors, which can help each industry sector to reasonably hedge risks associated with crude oil price fluctuations.

This study is structured as follows. In Section 2, we mainly review the relevant literature. Section 3 focuses on model construction by constructing a crude oil-economy computable general equilibrium (OE-CGE) model to build the foundation for conducting numerical simulations later on. The Section 4 mainly calibrates the parameters of Leontief, CES, and CET functions and the propensity to save before simulating the CGE model to provide accurate a priori data for the later numerical simulations. Section 5 derives the corresponding results from the numerical simulations. Section 6 contains conclusions, policy recommendations, and limitations.

2. Literature Review

In recent years, frequent occurrence of conflicts in Middle East, Russia-Ukraine, and other areas have made the crude oil market more volatile than ever. China relies on imported crude oil to sustain high-quality economic development, and the uncertainty in the international crude oil market has heightened the need to asses the impacts of oil price fluctuations on China’s economy. While studies have found that the fluctuations of crude oil market do not have a significant impact on economic growth in the short run [1], they have found that oil price fluctuations clearly impede economic growth in the long run [2]. Specifically, negative oil price fluctuations break the international trade balance and trigger inflation, which in turn threatens the quality development of the economy [3]. A positive oil price uncertainty shock, on the other hand, can lead to a decline in real economic activity, world crude oil production, and world crude oil prices in all countries [4], with the same adverse effects. Studies about the impact of oil price fluctuations on the economy are briefly reviewed as follows.

There are studies on the relationship between crude oil prices and macroeconomic variables. Liu et al. concluded that large increases in oil prices have a significant negative impact on economic growth and money supply and that economic growth responds more persistently than other economic variables [5]. Yildirim and Arifli [3] studied the impact of falling oil prices on the economy and found that falling oil prices worsen the trade balance, lower the real exchange rate, depreciate the currency, increase inflation, and force a recession. Kim et al. [6] had a different conclusion that the foreign exchange market is resistant to crude oil price fluctuations and that external shocks from crude oil price fluctuations can hardly affect the exchange rate market. Mohaddes and Pesaran found a stable negative correlation between oil prices and real dividends and that the crude oil market exhibited significant cyclical fluctuations between low and high oil prices [7]. Mallick et al. [8] noted that shocks from crude oil price volatility have a significant negative impact on private investment. Lorusso [9] found that crude oil price shocks have a non-negligible impact on the UK macroeconomic aggregates, mainly in terms of unemployment, inflation, etc. Guan et al. [1] argued that crude oil price fluctuations may harm economic growth as measured by GDP in resource producing economies in the long run. Jin et al. [10] argued that different levels of crude oil price fluctuations have different dampening effects on the consumer price index and similar effects on GDP. Scholars chose different macroeconomic variables in their studies, but concluded uniformly that significant effects of oil price shocks on the economy do exist.

There are studies on the asymmetric impact of oil price changes on the economy. Nasir et al. [11] reached a similar conclusion that there are significant differences and asymmetries in the response to oil fluctuations in economies with different economic structures. This finding was validated by subsequent studies. Charfeddine [12] found that there is asymmetry in the short-run oil price shocks to the economy, i.e., both real GDP and non-crude oil real GDP respond more to negative shocks than positive shocks. Nusair [13] argued that the impact of higher oil prices on output is more than that of a fall in oil prices, and this asymmetric impact varies by country. In contrast, Cheng et al. [14] reached an opposite conclusion and argued that positive uncertainty shocks of oil prices depress real GDP and investment, while negative uncertainty shocks to oil prices tend to boost the macroeconomy by increasing investment and real GDP.

A series of literature has analyzed factors affecting the economic impact of crude oil price changes. Khan et al. [15] identified the world economic expansion, mismatch of crude oil supply and demand mismatch, and dollar depreciation as the dominant factors of crude oil price fluctuations that shock the economy. Jia et al. [16] identified factor inputs as the main influencing factor for the economic impact effect of crude oil price fluctuations compared to consumer preferences factors. Lorusso and Pieroni [9], on the other hand, explained the impact of oil price fluctuations on the economy in terms of demand and supply shocks and found that specific demand shocks largely affect the growth of the economy, especially the fluctuations in GDP growth and unemployment rate.

In this paper, we follow a few studies that analyze the impact of crude oil price fluctuations on the economy across sectors. Thorbecke [17] stated that industries such as airlines, food, and industrial transport are harmed by higher oil prices, while industries such as oil and gas production and exploration are benefited, and the findings apply to most countries. Charfeddine and Barkat [12] argued that non-oil industries recover better than oil industries when crude oil prices generate negative shocks. Quintero [18] argued that production activities are slightly reduced in most sectors by aggregate demand shocks, and the sectors most directly affected are manufacturing, electricity, gas, and water. The findings serve as a validation for other related studies as well. These studies have engaged in a similar analysis of the macroeconomic impact of crude oil price changes but have not paid much attention to the impact on consumption, taxation, and output of specific industry sectors across the chain.

Scholars have studied oil price fluctuations and the national economy from different perspectives, but most of the studies are biased toward macroeconomic aggregates and lack a microscopic perspective. How the entire industry chain will be affected by oil price fluctuations and how each industry should change its production scale and investment strategy through oil price changes are the questions that we want to address in this paper. Therefore, we will study the impact of crude oil price changes on each industry sector by conducting numerical simulations, drawing on previous research by scholars. In this paper, we comprehensively simulate the effects of changes in crude oil price increases and decreases on consumption, investment, and output in each industrial sector and propose preventive policies to cope with future crude oil price shocks in order to stabilize the national economy.

3. Model Description

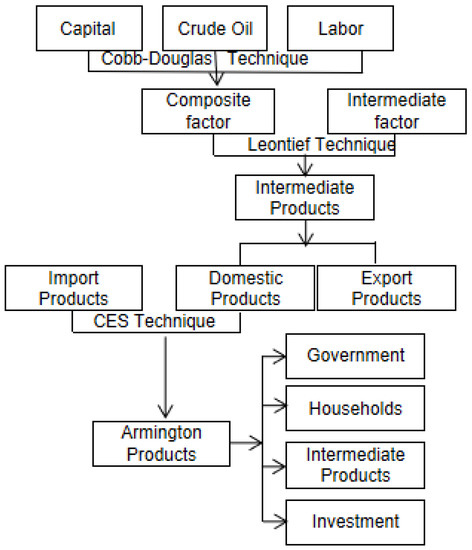

Following the standard computable general equilibrium model [19], we use crude oil as a factor of production in the model. In the OE-CGE model, capital, labor, and crude oil are combined into composite factors using the Cobb–Douglas technique. Then, the composite factor and the products of various industrial sectors as intermediate inputs are produced as intermediate products. In addition to domestic consumption, some intermediate products are used for export. Due to the substitutability between domestic and foreign products, domestic products and imported products are assumed to be synthesized for Armington goods by using a constant elasticity of substitution (CES) technique. Armington goods are final consumer goods for government consumption, household consumption, investment, and intermediate inputs. The structure of OE-CGE model can be descripted as Figure 1.

Figure 1.

Diagram of OE-CGE framework.

3.1. Production in Economy

In this paper, domestic production is divided into two stages. In the first stage, capital, labor, and crude oil are combined into a composite factor for production using the Cobb–Douglas technique. The objection of profit maximum for firm j can be described as follows:

where denotes the profit of producing the composite factor; denotes the quantity of the composite factor used in the second stage; denotes the price of the composite factor j; , , and refer the quantity of capital, labor, and crude oil, respectively, invested in the first stage of production; , , and denote the price of capital, labor, and crude oil, respectively; denotes the input share coefficient of various factors in the composite factor of production; denotes the scale coefficient of the composite factor production function.

In the second stage, the composite factor and the intermediate products are combined to produce total domestic output using Leontief technique. The objection of profit maximization for firm j can be written in the following form:

where denotes the profit of the first stage firm producing the composite factor; denotes the quantity of the intermediate input product i used by firm j; denotes the price of the domestic output product j; denotes the price of the composite product i; and denotes the quantity of i intermediate inputs and j composite factor to produce a unit of product j. The production behavior of an enterprise can be expressed as follows.

3.2. Government Description

We assume that government does not participate in production. The government should maintain a balanced budget. Government revenue comes from taxes on households or companies and tariffs on imported products. All the revenue is used for government consumption and transfers to households or businesses. The direct tax rate on households is , and the tax amount is . The indirect tax on firms is assumed to be , and the tax amount is . The tariff rate imposed on imported goods is . The government’s savings is , and the consumption of government is . The tax revenue and consumption can be expressed as follows:

where is the indirect tax levied on the production of product j; is the tariff levied on the import of product i; is the quantity of imports of product i; represents the quantity of government consumption of product i; refers the saving rate of government. denotes the price of import product i, and is the expenditure share of government consumption of product i .

3.3. Household Description

An important part of the CGE model is to transform residents’ income from factor endowments into product demand. This demand is derived from residents’ utility maximization behavior under budget constraints. The objective utility function is shown as follows:

where represents the quantity of good i consumed by residents; denotes the factor endowment h of residents; represents the savings of residents, and represents the share coefficient in the utility function .

The consumer demand function for good i derived from the above utility maximization problem is as follows:

where is the share coefficient of sector i, . The investment demand function can be expressed as follows:

where is the share of saving for product i ; is trade surplus. The saving of household can be expressed as follows.

3.4. International Trade

We assume that there is imperfect substitutability between the imported products and the domestic products , and the combination of products is called as an Armington product. The profit maximization problem of the Armington i is characterized as the following.

Moreover, it is subject to the following:

where denotes the profit of the Armington composite product i; is the import price of the product i; is the domestic sales price of product i; denotes the quantity of the composite product i; is the quantity of the product i imported; denotes the quantity of domestic demand for product i; is the coefficient of the Armington composite product production function; and denote the import and domestic sales share coefficients of the Armington composite product production function , respectively. Moreover, is the substitution parameter .

Solving Equation (23) yields the demand function for imported consumer commodities and for domestically produced commodities.

Suppose that the firm converts total output into two commodities that are sold in international and domestic markets (exports and domestic sales). Moreover, there is imperfect substitutability between the two commodities in the conversion process. Firm i converts total output into the exported good and the domestically sold good in order to maximize profits .

Moreover, it is subject to the following:

where is the export price of product i; is the conversion coefficient of product i; and are the share coefficients of exports and domestic sales of the conversion function of product i, respectively . is the conversion parameter calculated on the basis of the elasticity of conversion between exports and domestic sales in the production conversion function .

Solving Equation (27) yields a supply function for the exported product and the domestically supplied product.

3.5. Market Equilibrium

Trade equilibrium can be expressed as follows:

where and refer to the values for export and import of crude oil, respectively.

The Armington product market and factor market clearing conditions are shown as follows.

4. Data and Parameters Calibration

4.1. Data

The National Input–Output Table (2018) of China is utilized as the basic data source. According to the degree of relevance to crude oil, 153 industrial sectors in the input–output table were classified into 17 industrial sectors The industrial sector classification is shown in Table A1. According to the ratio for the tariff to the total import of each industrial sector, the tariff rate of each industrial sector is simply estimated. Following Robinson [20], we apply cross-entropy methods to adjust the social accounting matrix (SAM).

4.2. Parameters Calibration

We calibrate the parameters of the Leontief, Constant elasticityof substitution (CES) and Constant elasticity of transformation (CET) production functions as well as the propensity to save. First, a SAM table is prepared using input–output tables and relevant statistical yearbooks. Second, the calibrated parameters for each industrial sector are obtained using balanced SAM tables and relevant parameter calibration formulas to provide accurate a priori data for later numerical simulations.

4.2.1. Calibration of Cobb-Douglas Production Function

In (34), is the share coefficient in the utility function. It reflects residents’ share of consumption in various goods. This parameter is calculated by converting residential consumption to product prices, and Table A2 shows the calibration results.

is the input coefficient share of the composite factors of production, and the factors of production in this paper are the basic factors of production (labor and capital) plus crude oil, and the following two formulas calculate the input shares of the basic factors of production and crude oil, respectively. The input shares of capital and labor can be obtained by dividing the prices of these two factors by the total number of factor inputs in the first stage, and the input shares of crude oil can be obtained in the same manner.

The composite factor of production is generated through the Cobb Douglas production function; then, denotes the scale factor of the composite factor of production function, obtained by dividing the total output generated from the Leontief production function over the total number of factors.

From Table A2, we can infer that the share parameter of the daily consumption sector in the residents’ utility function on is 0.194, that of the real estate sector in the utility function is 0.205, that of the financial sector in the utility function of residents’ consumption is 0.208, and the corresponding parameter of the public utilities sector is 0.192. The remaining thirteen sectors have a share parameter of less than 0.1 in the residents’ consumption utility function, which indicates that residents’ consumption is most invested in daily consumption, real estate, finance, and public utilities.

From Table A3, we can see that crude oil accounts for the largest input share (0.335) in the sector of crude oil, coking products, and processed nuclear fuel products, followed by the chemical products sector with input share of 0.2, and the crude oil input shares in the sectors of metal and non-metal mining products and mining auxiliary activities, metal and non-metal products, transportation, storage and postal services, and public utilities are, respectively, 0.15, 0.117, 0.136, and 0.175, which are all higher than 0.1.

Labor’s input share is the largest in the daily consumption sector (0.680), and the smallest (0.192) in the crude oil, coke products, and processed nuclear fuel products sector. Capital’s input share is the largest in the crude oil and natural gas extraction products sector (0.710) and the smallest in the public utilities sector (0.181).

As can be seen from Table A4, the scale coefficients of the composite factor production functions in each of the seventeen sectors are close to each other without much difference, with the largest being in the composite factor production function of the chemical products sector (2.826), and the smallest being in the composite factor production function of the crude oil and natural gas extraction products sector (1.906).

4.2.2. Calibration of the Leontief Function

In the following equations, indicates the quantity of intermediate inputs (intermediate input coefficient) corresponding to the ith product to produce a unit of the jth product. It can be obtained by dividing the total output obtained by the number of intermediate inputs of a product over the total output generated from the Leontief production function. indicates the quantity of input corresponding to the jth composite product needed to produce a unit of the jth product, which can be obtained by dividing the number of inputs of the second stage composite product over the total output generated from by having the Leontief production function.

4.2.3. Calibration of the CES Function

The Armington composite product production function contains four unknowns , , , and . The initial values of the endogenous variables , , , , and in the equations containing these unknowns can be obtained directly from the social accounting matrix or set as unit 1. Moreover, assume that the value of the elasticity of substitution for all commodities is 2 (reference works:Textbook of Computable General Equilibrium Modeling); then, and can be estimated.

In the above formula, the initial value of import price is set to 1. After completing the calibration of and , we can obtain the following.

4.2.4. Calibration of CET Function

The calibration process of the CET function pair is similar to the calibration process of the CES function. Set the conversion elasticity at 2, and calibrate the supply function of export commodities and domestic commodities.

The calibration of the scale factor is achieved by substituting the calibrated coefficient values into the CET function.

4.2.5. Calibration of Other Coefficients

and can be simply calculated by the following equations for residential and government savings.

is the share of government consumption, which can be calculated by the formula for government consumption.

5. Results of Simulation

We set two different scenarios of crude oil price changes to ascertain the resulting changes in consumption, output, and investment changes in various departments. In the second scenario, crude oil price increases or decrease by 1%, 5%, 10%, 15%, and 20%, respectively.

5.1. Impact of Crude Oil Price Fluctuations on Consumption

Changes in Household Consumption

As can be seen from Table A11, when the price of crude oil rises, the changes in household consumption in each industrial sector show different characteristics. Household consumption increased in most energy-intensive industries due to rising crude oil prices. The rates of change in households’ consumption of crude oil and natural gas extraction products sector and crude oil, coking products, and processed nuclear fuel products sector are 17.085% and 13.368% when crude oil prices increase by 1%. When crude oil price rises, the change rate of households consumption in textile, clothing, footwear, leather, down products sector, and public utilities sector is negative. The negative rates of change indicates that the rise in crude oil prices reduce households consumption in these industries. The increase in crude oil prices has the greatest impact on the consumption of residents in crude oil and natural gas extraction products, followed by the crude oil, coking products, and processed nuclear fuel products sectors.

Table A12 provides changes in the household consumption of products in each sector after the fall in crude oil price. Household consumption increases in most energy-intensive industries when crude oil price falls. Moreover, the increase in consumption in these sectors is gradually increasing. When crude oil prices increase by 1%, household consumption in crude oil and natural gas extraction products sector and crude oil, coking products, and processed nuclear fuel products sector increase by 17.319% and 13.737%, respectively. Household consumption in these two sectors is extremely sensitive to increases in crude oil prices. When the price of crude oil decreases, household consumption in the textile, clothing, footwear, leather, down, and their products sector, and the public utilities sector keeps decreasing. The rate of change of household consumption in these sector is significantly higher than that in other sectors where consumption decreases. However, the rate of change of consumption in these sectors gradually increases in the process of increasing the decline of crude oil prices.

The fluctuations of crude oil price have the greatest impact on on household consumption in crude oil and natural gas extraction products, followed by crude oil, coking products, and the nuclear fuel processed products sector.

5.2. Impact of Crude Oil Price Fluctuations on Output

Table A13 shows the change in output of each industrial sector after the increase in crude oil prices. As crude oil price rises, the output of non-energy-intensive industrial sectors declines, while that of energy-intensive industrial sectors rises. The rate of change in output of crude oil and natural gas extraction products sector is 23.406% for a 20% increase in the price of crude oil. The industry’s output growth rate has been above 20%, indicating that the crude oil and natural gas extraction products sector is sensitive to the change of crude oil price. When crude oil price rises, the industry is profitable and can earn more profit by expanding production. There are some industrial sectors that reduce output in the process of crude oil price increase, such as textile, clothing, shoes and hats, leather, down products sector, etc.

Table A14 shows that production in non-energy intensive industrial sectors falls due to lower crude oil prices, such as daily consumption products sector, textile, clothing, footwear, leather, down products sector, woodworking products, paper printing and cultural, sports and educational supplies sector, hardware and equipment sector, real estate sector, and information transmission, software, and information technology services sector. However, when oil price declines, output in energy-intensive industrial sectors increased, such as coal mining and washing products sector; crude oil and natural gas extraction products sector; metal and non-metal mining products and mining auxiliary activities sector; crude oil, coking products, and processed nuclear fuel products sector; chemical products sector; metal and non-metal products sector; electricity and gas production and supply sector; water production and supply sector; and transportation, storage, and postal services sector. The output of crude oil and natural gas extraction products sector is increasing by 27.039%, when crude oil prices fall by 1%. The rate of change in output of this sector is still greater than the rate of change in oil price when crude oil price falls by 20%. Crude oil price changes have the greatest impact on crude oil and natural gas extraction products sector.

5.3. Impact of Crude Oil Price Fluctuations on Investment

Table A15 shows that rising crude oil price leads to a decline in its investment with the exception of crude oil and natural gas extraction products sector, and crude oil and processed products sector. The rising crude oil price boosts the profit in the two industrial sectors. With the increases in oil price, the output of remaining sectors decreases, indicating that higher crude oil price leads to lower profits.

Table A16 shows the impact of the fall in crude oil price on investment in each industrial sector. Falling crude oil price leads to decreasing investment in most industrial sectors, with the exception of crude oil and natural gas extraction products sector and the crude oil, coking products, and processed nuclear fuel products sector. With decreases in crude oil price, investments in crude oil and natural gas extraction products sector and crude oil, coking products, and processed nuclear fuel products sector gradually increases.

We can conclude that fluctuations have the greatest impact on the public utilities sector, followed by textile, clothing, footwear, leather, down products sector; crude oil and natural gas extraction products sector; processed wood products, paper printing and cultural, sports and educational supplies sector; and hardware and equipment sector.

6. Conclusions

In this paper, we develop an oil economy computable general equilibrium (OE-CGE) model to capture the mechanisms by which oil price volatility affects various industrial sectors. The paper comprehensively investigates the impact of crude oil price fluctuations on output, investment, and consumption in various industrial sectors. From the simulation results, we can draw the conclusion as follows.

As crude oil price rises, household demand for energy-intensive products increases. When it falls, household consumption expenditures increase in most industrial sectors. It is an effective way to increase household consumption expenditure by reducing the price of crude oil. Investments in most industrial sectors decrease when crude oil prices change. Stable oil prices help to reduce the risk of investment in various industrial sectors. Crude oil price stability is extremely important for increased investment.

The mechanism of influence between crude oil prices and industrial sectors output is complex. Fluctuations in crude oil prices can lead to the increased value of output in most industrial sectors. When crude oil prices fall, production in various industrial sectors increases due to lower production costs. The rise in crude oil price pushes up the prices of various products, which indirectly increases the output value of various industrial sectors. Although higher oil price increases the output of various industrial sectors, it is still necessary to maintain stable low oil prices. The government should intervene appropriately in the event of unanticipated fluctuations in crude oil price to ensure the stability of the domestic market.

In the OE-CGE model, we simulate the impact of crude oil price changes on households consumption, output, and investment in industiral sectors. We assume that the price of products in each industrial sector is fixed, which cannot reflect the impact of the changes on prices of products. In future research, it is possible to consider how product price can be incorporated into changes into the model.

Author Contributions

Methodology and software, Z.S.; writing—original draft preparation, X.C.; writing—review and editing, W.-C.H.; funding acquisition, Z.S. All authors have read and agreed to the published version of the manuscript.

Funding

The authors acknowledge funding supported from Shaanxi Education Department Key Research Base Project of Philosophy and Social Science (grant No. 19JZ047) and China Scholarship Council Fund (CSC: 201908610028).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data availability.

Conflicts of Interest

The authors declare no conflict of interest.

Abbreviations

The following abbreviations are used in this manuscript:

| CGE | Computable General Equilibrium; |

| SAM | Social Accounting Matrix; |

| CES | Constant Elasticity of Substitution; |

| CET | Constant Elasticity of Transformation. |

Appendix A

Table A1.

Industry Sector Classification.

Table A1.

Industry Sector Classification.

| Number | Industry Calssification | Sector Code |

|---|---|---|

| 1 | Daily consumption products | 01001, 02002, 03003, 04004, 05005, 13012, 13013, 13014, 13015, 13016, 13017, 13018, 14019, 14020, 14021, 14022, 15023, 15024, 15025, 16026, 51105, 52106, 61119, 62120 |

| 2 | Coal mining and washing products | 06006 |

| 3 | Crude oil and gas extraction products | 07007 |

| 4 | Metal, non-metallic mining products, and mining auxiliary activities | 08008, 09009, 10010, 11011 |

| 5 | Textile, clothing, shoes, and hats, leather, down products | 17027, 17028, 17029, 17030, 17031, 18032, 19033, 19034 |

| 6 | Woodworking products, paper printing, and cultural and educational supplies | 20035, 21036, 22037, 23038, 24039, 24040 |

| 7 | Crude oil, refined coke products, and processed nuclear fuel products | 25041, 25042 |

| 8 | Chemical products | 26043, 26044, 26045, 26046, 26047, 26048, 26049, 27050, 28051, 29052, 29053 |

| 9 | Metal, non-metallic products | 30054, 30055, 30056, 30057, 30058, 30059, 30060, 31061, 31062, 31063, 32064, 32065, 33066 |

| 10 | Hardware and equipment | 34067, 34068, 34069, 34070, 34072a, 34071, 34072b, 35073, 35074, 35075, 35076a, 35076b, 36077, 36078, 37079, 37080, 37081, 38082, 38083, 38084, 38085, 38086, 38087, 39088, 39089, 39090, 39091, 39092, 39093, 40094, 41095, 42096, 43097 |

| 11 | Electricity, gas production, and supply | 44098, 45099 |

| 12 | Water production and supply | 46100 |

| 13 | Real estate | 47101a, 47101b, 48102a, 48102b, 49103, 50104, 70129 |

| 14 | Transportation, storage, and postal | 53107, 53108, 54109, 54110, 55111, 55112, 56113, 56114, 57115, 58116, 59117, 60118 |

| 15 | Information transmission, software, and information technology services | 63121, 63122, 64123, 65124, 65125 |

| 16 | Finance | 66126, 67127, 68128 |

| 17 | Public utilities | 71130, 72131, 73132, 74133, 75134, 76135, 77136, 78137, 80138, 81139, 83140, 84141, 85142, 86143, 87144, 88145, 89146, 90147, 94148, 91149 |

Note: The Sector Code is derived from the Input–Output Table of China.

Table A2.

The results of calibration of .

Table A2.

The results of calibration of .

| Sector | |

|---|---|

| Daily consumption products | 0.194 |

| Coal mining and washing products | |

| Crude oil and gas extraction products | |

| Metal, non-metallic mining products, and mining auxiliary activities | |

| Textile, clothing, shoes and hats, leather, down products | 0.026 |

| Woodworking products, paper printing and cultural and educational supplies | 0.013 |

| Crude oil, refined coke products, and processed nuclear fuel products | 0.004 |

| Chemical products | 0.022 |

| Metal, non-metallic products | 0.002 |

| Hardware and equipment | 0.066 |

| Electricity, gas production, and supply | 0.012 |

| Water production and supply | 0.002 |

| Real estate | 0.205 |

| Transportation, storage, and postal | 0.028 |

| Information transmission, software, and information technology services | 0.026 |

| Finance | 0.208 |

| Public utilities | 0.192 |

Table A3.

The results of calibration of .

Table A3.

The results of calibration of .

| Sector | |||

|---|---|---|---|

| Daily consumption products | 0.006 | 0.680 | 0.314 |

| Coal mining and washing products | 0.010 | 0.551 | 0.439 |

| Crude oil and gas extraction products | 0.010 | 0.280 | 0.710 |

| Metal, non-metallic mining products, and mining auxiliary activities | 0.150 | 0.471 | 0.378 |

| Textile, clothing, shoes and hats, leather, down products | 0.010 | 0.588 | 0.402 |

| Woodworking products, paper printing, and cultural and educational supplies | 0.017 | 0.503 | 0.480 |

| Crude oil, refined coke products, and processed nuclear fuel products | 0.335 | 0.192 | 0.472 |

| Chemical products | 0.200 | 0.321 | 0.479 |

| Metal, non-metallic products | 0.117 | 0.361 | 0.523 |

| Hardware and equipment | 0.010 | 0.493 | 0.496 |

| Electricity, gas production, and supply | 0.060 | 0.325 | 0.615 |

| Water production and supply | 0.003 | 0.495 | 0.503 |

| Real estate | 0.028 | 0.472 | 0.499 |

| Transportation, storage, and postal | 0.136 | 0.433 | 0.431 |

| Information transmission, software, and information technology services | 0.003 | 0.395 | 0.602 |

| Finance | 0.007 | 0.513 | 0.480 |

| Public utilities | 0.175 | 0.644 | 0.181 |

Table A4.

The results of calibration of .

Table A4.

The results of calibration of .

| Sector | |

|---|---|

| Daily consumption products | 1.926 |

| Coal mining and washing products | 2.086 |

| Crude oil and gas extraction products | 1.906 |

| Metal, non-metallic mining products, and mining auxiliary activities | 2.738 |

| Textile, clothing, shoes and hats, leather, down products | 2.066 |

| Woodworking products, paper printing, and cultural and educational supplies | 2.155 |

| Crude oil, refined coke products, and processed nuclear fuel products | 2.823 |

| Chemical products | 2.826 |

| Metal, non-metallic products | 2.606 |

| Hardware and equipment | 2.103 |

| Electricity, gas production, and supply | 2.299 |

| Water production and supply | 2.032 |

| Real estate | 2.230 |

| Transportation, storage, and postal | 2.709 |

| Information transmission, software, and information technology services | 1.993 |

| Finance | 2.071 |

| Public utilities | 2.453 |

Table A5.

The results of calibration of and .

Table A5.

The results of calibration of and .

| Sector | ||

|---|---|---|

| Daily consumption products | 0.957 | 0.043 |

| Coal mining and washing products | 0.934 | 0.066 |

| Crude oil and gas extraction products | 0.417 | 0.583 |

| Metal, non-metallic mining products, and mining auxiliary activities | 0.957 | 0.043 |

| Textile, clothing, shoes and hats, leather, down products | 0.944 | 0.056 |

| Woodworking products, paper printing, and cultural and educational supplies | 0.943 | 0.057 |

| Crude oil, refined coke products, and processed nuclear fuel products | 0.938 | 0.062 |

| Chemical products | 0.910 | 0.090 |

| Metal, non-metallic products | 0.956 | 0.044 |

| Hardware and equipment | 0.847 | 0.153 |

| Electricity, gas production, and supply | 1.000 | |

| Water production and supply | 1.000 | |

| Real estate | 0.998 | 0.002 |

| Transportation, storage, and postal | 0.941 | 0.059 |

| Information transmission, software, and information technology services | 0.968 | 0.032 |

| Finance | 0.943 | 0.057 |

| Public utilities | 0.982 | 0.018 |

Table A6.

The results of calibration of .

Table A6.

The results of calibration of .

| Sector | |

|---|---|

| Daily consumption products | 4.907 |

| Coal mining and washing products | 3.989 |

| Crude oil and gas extraction products | 2.032 |

| Metal, non-metallic mining products, and mining auxiliary activities | 4.451 |

| Textile, clothing, shoes and hats, leather, down products | 4.352 |

| Woodworking products, paper printing, and cultural and educational supplies | 4.271 |

| Crude oil, refined coke products, and processed nuclear fuel products | 3.741 |

| Chemical products | 3.248 |

| Metal, non-metallic products | 4.611 |

| Hardware and equipment | 2.781 |

| Electricity, gas production, and supply | 63.439 |

| Water production and supply | 248,545.736 |

| Real estate | 25.148 |

| Transportation, storage, and postal | 3.751 |

| Information transmission, software, and information technology services | 5.646 |

| Finance | 4.281 |

| Public utilities | 6.461 |

Table A7.

The results of calibration of and .

Table A7.

The results of calibration of and .

| Sector | ||

|---|---|---|

| Daily consumption products | 0.960 | 0.040 |

| Coal mining and washing products | 0.999 | 0.001 |

| Crude oil and gas extraction products | 0.997 | 0.003 |

| Metal, non-metallic mining products, and mining auxiliary activities | 0.993 | 0.007 |

| Textile, clothing, shoes and hats, leather, down products | 0.814 | 0.186 |

| Woodworking products, paper printing, and cultural and educational supplies | 0.892 | 0.108 |

| Crude oil, refined coke products and processed nuclear fuel products | 0.978 | 0.022 |

| Chemical products | 0.939 | 0.061 |

| Metal, non-metallic products | 0.957 | 0.043 |

| Hardware and equipment | 0.830 | 0.170 |

| Electricity, gas production, and supply | 0.999 | |

| Water production and supply | 1.000 | |

| Real estate | 0.998 | 0.002 |

| Transportation, storage, and postal | 0.948 | 0.052 |

| Information transmission, software, and information technology services | 0.976 | 0.024 |

| Finance | 0.998 | 0.002 |

| Public utilities | 0.990 | 0.010 |

Table A8.

The results of calibration of .

Table A8.

The results of calibration of .

| Sector | |

|---|---|

| Daily consumption products | 4.936 |

| Coal mining and washing products | 24.371 |

| Crude oil and gas extraction products | 12.601 |

| Metal, non-metallic mining products, and mining auxiliary activities | 10.934 |

| Textile, clothing, shoes and hats, leather, down products | 2.568 |

| Woodworking products, paper printing, and cultural and educational supplies | 3.146 |

| Crude oil, refined coke products, and processed nuclear fuel products | 5.840 |

| Chemical products | 4.008 |

| Metal, non-metallic products | 4.760 |

| Hardware and equipment | 2.587 |

| Electricity, gas production, and supply | 30.416 |

| Water production and supply | 165,222.099 |

| Real estate | 19.963 |

| Transportation, storage, and postal | 4.468 |

| Information transmission, software, and information technology services | 6.504 |

| Finance | 20.880 |

| Public utilities | 9.854 |

Table A9.

The results of calibration of and .

Table A9.

The results of calibration of and .

| Sector | ||

|---|---|---|

| Daily consumption products | 0.012 | 0.028 |

| Coal mining and washing products | ||

| Crude oil and gas extraction products | ||

| Metal, non-metallic mining products, and mining auxiliary activities | ||

| Textile, clothing, shoes and hats, leather, down products | 0.001 | |

| Woodworking products, paper printing, and cultural and educational supplies | 0.008 | |

| Crude oil, refined coke products, and processed nuclear fuel products | ||

| Chemical products | 0.003 | |

| Metal, non-metallic products | 0.007 | |

| Hardware and equipment | 0.202 | |

| Electricity, gas production, and supply | ||

| Water production and supply | ||

| Real estate | 0.661 | |

| Transportation, storage, and postal | 0.018 | 0.009 |

| Information transmission, software, and information technology services | 0.041 | |

| Finance | 0.023 | |

| Public utilities | 0.948 | 0.039 |

Table A10.

The results of calibration of and .

Table A10.

The results of calibration of and .

| Sector | ||

|---|---|---|

| Daily consumption products | 0.040 | 0.044 |

| Coal mining and washing products | 0.146 | 0.014 |

| Crude oil and gas extraction products | 0.454 | 0.008 |

| Metal, non-metallic mining products, and mining auxiliary activities | 0.134 | 0.012 |

| Textile, clothing, shoes and hats, leather, down products | 0.001 | 0.023 |

| Woodworking products, paper printing, and cultural and educational supplies | 0.025 | 0.010 |

| Crude oil, refined coke products, and processed nuclear fuel products | 0.169 | 0.014 |

| Chemical products | 0.044 | 0.017 |

| Metal, non-metallic products | 0.034 | 0.018 |

| Hardware and equipment | 0.028 | 0.022 |

| Electricity, gas production, and supply | 0.041 | 0.061 |

| Water production and supply | 0.066 | 1.000 |

| Real estate | 0.057 | 0.016 |

| Transportation, storage, and postal | 0.010 | 0.016 |

| Information transmission, software, and information technology services | 0.014 | 0.014 |

| Finance | 0.056 | 0.014 |

| Public utilities | 0.011 | 0.014 |

Table A11.

Household consumption change rate after the rise in crude oil price.

Table A11.

Household consumption change rate after the rise in crude oil price.

| Sector | 1% | 5% | 10% | 15% | 20% |

|---|---|---|---|---|---|

| Daily consumption products | −0.707 | −0.908 | −1.150 | −1.384 | −1.610 |

| Coal mining and washing products | 1.313 | 1.091 | 0.822 | 0.563 | 0.312 |

| Crude oil and gas extraction products | 17.085 | 16.623 | 16.061 | 15.514 | 14.980 |

| Metal, non-metallic mining products, and mining auxiliary activities | 4.708 | 4.131 | 3.440 | 2.780 | 2.147 |

| Textile, clothing, shoes and hats, leather, down products | −7.533 | −7.684 | −7.864 | −8.036 | −8.199 |

| Woodworking products, paper printing, and cultural and educational supplies | −3.350 | −3.537 | −3.763 | −3.980 | −4.187 |

| Crude oil, refined coke products, and processed nuclear fuel products | 13.368 | 12.648 | 11.780 | 10.944 | 10.137 |

| Chemical products | 5.279 | 4.687 | 3.977 | 3.297 | 2.644 |

| Metal, non-metallic products | 2.081 | 1.625 | 1.078 | 0.555 | 0.053 |

| Hardware and equipment | −3.122 | −3.368 | −3.665 | −3.949 | −4.223 |

| Electricity, gas production, and supply | 1.376 | 1.079 | 0.721 | 0.377 | 0.046 |

| Water production and supply | −0.323 | −0.548 | −0.818 | −1.080 | −1.332 |

| Real estate | −0.324 | −0.670 | −1.087 | −1.487 | −1.872 |

| Transportation, storage, and postal | 2.322 | 1.804 | 1.184 | 0.591 | 0.023 |

| Information transmission, software, and information technology services | −1.494 | −1.663 | −1.867 | −2.064 | −2.254 |

| Finance | −0.431 | −0.659 | −0.936 | −1.203 | −1.461 |

| Public utilities | −9.015 | −9.654 | −10.418 | −11.149 | −11.849 |

Table A12.

Household consumption change rate after the decline in crude oil price.

Table A12.

Household consumption change rate after the decline in crude oil price.

| Sector | −1% | −5% | −10% | −15% | −20% |

|---|---|---|---|---|---|

| Daily consumption products | −0.604 | −0.394 | −0.120 | 0.166 | 0.467 |

| Coal mining and washing products | 1.427 | 1.660 | 1.963 | 2.279 | 2.611 |

| Crude oil and gas extraction products | 17.319 | 17.797 | 18.413 | 19.050 | 19.712 |

| Metal, non-metallic mining products, and mining auxiliary activities | 5.005 | 5.617 | 6.420 | 7.270 | 8.171 |

| Textile, clothing, shoes and hats, leather, down products | −7.455 | −7.294 | −7.083 | −6.858 | −6.620 |

| Woodworking products, paper printing, and cultural and educational supplies | −3.253 | −3.054 | −2.794 | −2.521 | −2.231 |

| Crude oil, refined coke products, and processed nuclear fuel products | 13.737 | 14.494 | 15.480 | 16.512 | 17.598 |

| Chemical products | 5.583 | 6.209 | 7.028 | 7.893 | 8.807 |

| Metal, non-metallic products | 2.315 | 2.799 | 3.432 | 4.101 | 4.809 |

| Hardware and equipment | −2.995 | −2.734 | −2.393 | −2.035 | −1.656 |

| Electricity, gas production, and supply | 1.529 | 1.843 | 2.252 | 2.682 | 3.136 |

| Water production and supply | −0.208 | 0.027 | 0.332 | 0.652 | 0.988 |

| Real estate | −0.146 | 0.220 | 0.698 | 1.200 | 1.730 |

| Transportation, storage, and postal | 2.589 | 3.138 | 3.859 | 4.622 | 5.430 |

| Information transmission, software, and information technology services | −1.408 | −1.231 | −1.002 | −0.762 | −0.511 |

| Finance | −0.314 | −0.074 | 0.236 | 0.561 | 0.901 |

| Public utilities | −8.687 | −8.010 | −7.122 | −6.183 | −5.187 |

Table A13.

The rate of change in output after the rise in crude oil price.

Table A13.

The rate of change in output after the rise in crude oil price.

| Sector | 1% | 5% | 10% | 15% | 20% |

|---|---|---|---|---|---|

| Daily consumption products | −0.199 | −0.455 | −0.763 | −1.057 | −1.340 |

| Coal mining and washing products | 7.113 | 6.750 | 6.315 | 5.898 | 5.498 |

| Crude oil and gas extraction products | 26.668 | 25.944 | 25.068 | 24.223 | 23.406 |

| Metal, non-metallic mining products, and mining auxiliary activities | 11.004 | 10.652 | 10.230 | 9.825 | 9.437 |

| Textile, clothing, shoes and hats, leather, down products | −11.294 | −11.435 | −11.600 | −11.754 | −11.898 |

| Woodworking products, paper printing, and cultural and educational supplies | −2.435 | −2.697 | −3.009 | −3.308 | −3.593 |

| Crude oil, refined coke products, and processed nuclear fuel products | 10.693 | 10.223 | 9.660 | 9.121 | 8.605 |

| Chemical products | 7.222 | 6.837 | 6.375 | 5.933 | 5.510 |

| Metal, non-metallic products | 2.054 | 1.772 | 1.435 | 1.113 | 0.804 |

| Hardware and equipment | −4.270 | −4.482 | −4.735 | −4.976 | −5.205 |

| Electricity, gas production, and supply | 4.889 | 4.566 | 4.178 | 3.807 | 3.451 |

| Water production and supply | 0.508 | 0.233 | −0.098 | −0.415 | −0.720 |

| Real estate | −1.419 | −1.711 | −2.061, | −2.396 | −2.717 |

| Transportation, storage, and postal | 8.402 | 8.018 | 7.559 | 7.121 | 6.700 |

| Information transmission, software, and information technology services | −0.417 | −0.664 | −0.961 | −1.245 | −1.519 |

| Finance | 1.916 | 1.641 | 1.309 | 0.989 | 0.680 |

| Public utilities | 2.695 | 2.180 | 1.562 | 0.972 | 0.407 |

Table A14.

The rate of change in output after the decline in crude oil price.

Table A14.

The rate of change in output after the decline in crude oil price.

| Sector | −1% | −5% | −10% | −15% | −20% |

|---|---|---|---|---|---|

| Daily consumption products | −0.068 | 0.203 | 0.557 | 0.930 | 1.325 |

| Coal mining and washing products | 7.299 | 7.683 | 8.185 | 8.715 | 9.276 |

| Crude oil and gas extraction products | 27.039 | 27.800 | 28.789 | 29.824 | 30.911 |

| Metal, non-metallic mining products, and mining auxiliary activities | 11.185 | 11.558 | 12.045 | 12.559 | 13.103 |

| Textile, clothing, shoes and hats, leather, down products | −11.221 | −11.069 | −10.865 | −10.646 | −10.409 |

| Woodworking products, paper printing, and cultural and educational supplies | −2.300 | −2.022 | −1.657 | −1.270 | −0.859 |

| Crude oil, refined coke products, and processed nuclear fuel products | 10.934 | 11.432 | 12.084 | 12.773 | 13.503 |

| Chemical products | 7.421 | 7.830 | 8.365 | 8.932 | 9.532 |

| Metal, non-metallic products | 2.199 | 2.498 | 2.890 | 3.304 | 3.744 |

| Hardware and equipment | −4.161 | −3.935 | −3.637 | −3.321 | −2.984 |

| Electricity, gas production and supply | 5.055 | 5.398 | 5.847 | 6.321 | 6.823 |

| Water production and supply | 0.649 | 0.939 | 1.318 | 1.716 | 2.137 |

| Real estate | −1.269 | −0.960 | −0.556 | −0.129 | 0.322 |

| Transportation, storage, and postal | 8.599 | 9.006 | 9.539 | 10.102 | 10.700 |

| Information transmission, software, and information technology services | −0.290 | −0.029 | 0.313 | 0.672 | 1.053 |

| Finance | 2.057 | 2.346 | 2.722 | 3.117 | 3.531 |

| Public utilities | 2.960 | 3.507 | 4.223 | 4.981 | 5.785 |

Table A15.

The rate of change in investment after the rise in crude oil price.

Table A15.

The rate of change in investment after the rise in crude oil price.

| Sector | 1% | 5% | 10% | 15% | 20% |

|---|---|---|---|---|---|

| Daily consumption products | −6.109 | −6.183 | −6.270 | −6.352 | −6.430 |

| Coal mining and washing products | −4.199 | −4.290 | −4.399 | −4.503 | −4.603 |

| Crude oil and gas extraction products | 10.714 | 10.415 | 10.051 | 9.695 | 9.348 |

| Metal, non-metallic mining products, and mining auxiliary activities | −0.989 | −1.412 | −1.917 | −2.398 | −2.857 |

| Textile, clothing, shoes and hats, leather, down products | −12.564 | −12.598 | −12.636 | −12.668 | −12.696 |

| Woodworking products, paper printing, and cultural and educational supplies | −8.608 | −8.672 | −8.747 | −8.817 | −8.881 |

| Crude oil, refined coke products, and processed nuclear fuel products | 7.200 | 6.652 | 5.991 | 5.355 | 4.742 |

| Chemical products | −0.449 | −0.885 | −1.408 | −1.907 | −2.384 |

| Metal, non-metallic products | −3.473 | −3.785 | −4.157 | −4.511 | −4.849 |

| Hardware and equipment | −8.392 | −8.512 | −8.654 | −8.788 | −8.915 |

| Electricity, gas production, and supply | −4.139 | −4.302 | −4.495 | −4.679 | −4.855 |

| Water production and supply | −5.746 | −5.842 | −5.955 | −6.063 | −6.166 |

| Real estate | −5.747 | −5.958 | −6.210 | −6.450 | −6.679 |

| Transportation, storage, and postal | −3.245 | −3.615 | −4.056 | −4.476 | −4.877 |

| Information transmission, software, and information technology services | −6.854 | −6.898 | −6.949 | −6.997 | −7.042 |

| Finance | −5.848 | −5.947 | −6.066 | −6.180 | −6.289 |

| Public utilities | −13.966 | −14.463 | −15.058 | −15.625 | −16.168 |

Table A16.

The rate of change in investment after the decline in crude oil price.

Table A16.

The rate of change in investment after the decline in crude oil price.

| Sector | −1% | −5% | −10% | −15% | −20% |

|---|---|---|---|---|---|

| Daily consumption products | −6.071 | −5.992 | −5.888 | −5.777 | −5.658 |

| Coal mining and washing products | −4.151 | −4.054 | −3.925 | −3.789 | −3.644 |

| Crude oil and gas extraction products | 10.867 | 11.176 | 11.575 | 11.987 | 12.414 |

| Metal, non-metallic mining products, and mining auxiliary activities | −0.770 | −0.319 | 0.275 | 0.905 | 1.577 |

| Textile, clothing, shoes and hats, leather, down products | −12.545 | −12.505 | −12.449 | −12.385 | −12.312 |

| Woodworking products, paper printing, and cultural and educational supplies | −8.574 | −8.503 | −8.408 | −8.304 | −8.191 |

| Crude oil, refined coke products, and processed nuclear fuel products | 7.482 | 8.059 | 8.811 | 9.599 | 10.429 |

| Chemical products | −0.224 | 0.239 | 0.848 | 1.491 | 2.174 |

| Metal, non-metallic products | −3.312 | −2.979 | −2.541 | −2.076 | −1.580 |

| Hardware and equipment | −8.330 | −8.201 | −8.030 | −7.847 | −7.651 |

| Electricity, gas production, and supply | −4.055 | −3.882 | −3.653 | −3.410 | −3.151 |

| Water production and supply | −5.697 | −5.595 | −5.462 | −5.320 | −5.168 |

| Real estate | −5.638 | −5.413 | −5.117 | −4.804 | −4.472 |

| Transportation, storage, and postal | −3.054 | −2.659 | −2.138 | −1.586 | −0.997 |

| Information transmission, software, and information technology services | −6.831 | −6.783 | −6.719 | −6.650 | −6.576 |

| Finance | −5.797 | −5.691 | −5.552 | −5.405 | −5.250 |

| Public utilities | −13.709 | −13.180 | −12.485 | −11.749 | −10.967 |

References

- Guan, L.; Zhang, W.W.; Ahmad, F.; Naqvi, B. The volatility of natural resource prices and its impact on the economic growth for natural resource-dependent economies: A comparison of oil and gold dependent economies. Resour. Policy 2021, 72, 102125. [Google Scholar] [CrossRef]

- van Eyden, R.; Difeto, M.; Gupta, R.; Wohar, M.E. Oil price volatility and economic growth: Evidence from advanced economies using more than a century’s data. Appl. Energy 2019, 233, 612–621. [Google Scholar] [CrossRef] [Green Version]

- Yildirim, Z.; Arifli, A. Oil price shocks, exchange rate and macroeconomic fluctuations in a small oil-exporting economy. Energy 2021, 219, 119527. [Google Scholar] [CrossRef]

- Xu, Q.; Fu, B.; Wang, B. The effects of oil price uncertainty on China’s economy. Energy Econ. 2022, 107, 105840. [Google Scholar] [CrossRef]

- Liu, D.; Meng, L.; Wang, Y. Oil price shocks and Chinese economy revisited: New evidence from SVAR model with sign restrictions. Int. Rev. Econ. Financ. 2020, 69, 20–32. [Google Scholar] [CrossRef]

- Kim, S.; Kim, S.Y.; Choi, K. Effect of Oil Prices on Exchange Rate Movements in Korea and Japan Using Markov Regime-Switching Models. Energies 2020, 13, 4402. [Google Scholar] [CrossRef]

- Mohaddes, K.; Pesaran, M.H. Oil prices and the global economy: Is it different this time around? Energy Econ. 2017, 65, 315–325. [Google Scholar] [CrossRef] [Green Version]

- Mallick, H.; Mahalik, M.K.; Sahoo, M. Is crude oil price detrimental to domestic private investment for an emerging economy? The role of public sector investment and financial sector development in an era of globalization. Energy Econ. 2018, 69, 307–324. [Google Scholar] [CrossRef]

- Lorusso, M.; Pieroni, L. Causes and consequences of oil price shocks on the UK economy. Econ. Model. 2018, 72, 223–236. [Google Scholar] [CrossRef] [Green Version]

- Jin, S.; Hamori, S. The Response of US Macroeconomic Aggregates to Price Shocks in Crude Oil vs. Natural Gas. Energies 2020, 13, 2603. [Google Scholar]

- Nasir, M.A.; Naidoo, L.; Shahbaz, M.; Amoo, N. Implications of oil prices shocks for the major emerging economies: A comparative analysis of BRICS. Energy Econ. 2018, 76, 76–88. [Google Scholar] [CrossRef]

- Charfeddine, L.; Barkat, K. Short- and long-run asymmetric effect of oil prices and oil and gas revenues on the real GDP and economic diversification in oil-dependent economy. Energy Econ. 2020, 86, 104680. [Google Scholar] [CrossRef]

- Nusair, S.A.; Olson, D. Asymmetric oil price and Asian economies: A nonlinear ARDL approach. Energy 2021, 219, 119594. [Google Scholar] [CrossRef]

- Cheng, D.; Shi, X.; Yu, J.; Zhang, D. How does the Chinese economy react to uncertainty in international crude oil prices? Int. Rev. Econ. Financ. 2019, 64, 147–164. [Google Scholar] [CrossRef]

- Khan, K.; Su, C.W.; Umar, M.; Yue, X.G. Do crude oil price bubbles occur? Resour. Policy 2021, 71, 101936. [Google Scholar] [CrossRef]

- Jia, Z.; Wen, S.; Lin, B. The effects and reacts of COVID-19 pandemic and international oil price on energy, economy, and environment in China. Appl. Energy 2021, 302, 117612. [Google Scholar] [CrossRef] [PubMed]

- Thorbecke, W. How oil prices affect East and Southeast Asian economies: Evidence from financial markets and implications for energy security. Energy Policy 2019, 128, 628–638. [Google Scholar] [CrossRef]

- Otero, J.D.Q. Not all sectors are alike: Differential impacts of shocks in oil prices on the sectors of the Colombian economy. Energy Econ. 2020, 86, 104691. [Google Scholar] [CrossRef]

- Nobuhiro, H.; Gasawa, K.; Hashimoto, H. Textbook of Computable General Equilibrium Modelling: Programming and Simulations; Springer: Berlin/Heidelberg, Germany, 2010. [Google Scholar]

- Robinson, S.; Cattaneo, A.; El-Said, M. Updating and estimating a social accounting matrix using cross entropy methods. Econ. Syst. Res. 2001, 13, 47–64. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).