3.2. Overall Electric-Transmission System

Nycander et al. [

22] investigated which curtailment would be needed in the future Nordic power system when wind power becomes a significant part of the total production. The authors built an hourly-dispatch model based on open data. A case study for 2025 was conducted. The curtailment was calculated to be 0.3% of the available power generation with 26 GW wind and 1.7% with 33 GW wind in the Nordic power system.

In

Figure 2, the transmission between different pricing regions in the Nordic countries [

11,

12] on a specific day can be seen. In our study, we focused especially on region SE-3, which contains more than 8 million people. This region will be strongly influenced when nuclear power is shut down, as all Swedish nuclear plants are in this region. This should happen by 2045, but discussions are ongoing to replace it with new nuclear power. The total transmission capacity in the region is 13,385 MW, whereas outside of the region it is 16,775 MW.

SE-3 is linked to SE-4, which has many connections to Denmark, Germany, Poland, and the Baltic states. As both Denmark and Germany already have huge installations of wind power, limitations in transmission capacity are of high importance, according to Klasmann et al. [

23].

Concerning Norway, which has huge hydropower-generation capacities (116–132 TWh/y), there is a huge demand for power transmission through Sweden to Denmark, Germany, and other countries.

The demand and production balances vary, as does the spot price. In

Table 2, the historical average value over several years is shown for the four Swedish regions as SEK/kWh. Especially during 2022, the spot price was very high in SE-3 and SE-4 in southern Sweden due to high prices, especially in Germany.

However, if considering how to make a resilient energy system, local production and storage in all parts of the country must be assured. This means relying not only on good transmission capacities and centralized production in a few large power plants.

3.5. Calculations of How Long Time Periods with Low Wind and Solar Power Last

A total of of 100% of nuclear power is produced in SE-3 for all of Sweden, whereas for hydropower only around 15–20% is produced in SE-3. For wind power, roughly 50% is produced in SE-3. Of the power consumption today, roughly 65% is in SE-3, but the demand in northern Sweden (SE-1 and SE-2) will increase more than in SE-3 over the next 10–20 years, which will reduce the possibility of transmitting it from north to south. More will be consumed locally in the heavy industries in the north.

The production of wind and solar power varied throughout the year. Solar power in particular was approximately eight times higher in July than in January. In

Figure 6, the production of power with different techniques is shown for January, April, July, and October 2022 for SE-3 to show the different patterns.

Consumption of power was significantly lower during holidays and weekends compared to working days, and there was higher demand at midday than at night. For power production, nuclear power operated as the base production, whereas wind and solar varied irregularly. Solar power yielded significant peaks during July, whereas other thermal power, mostly biomass-fueled CHP plants, had the highest production in January.

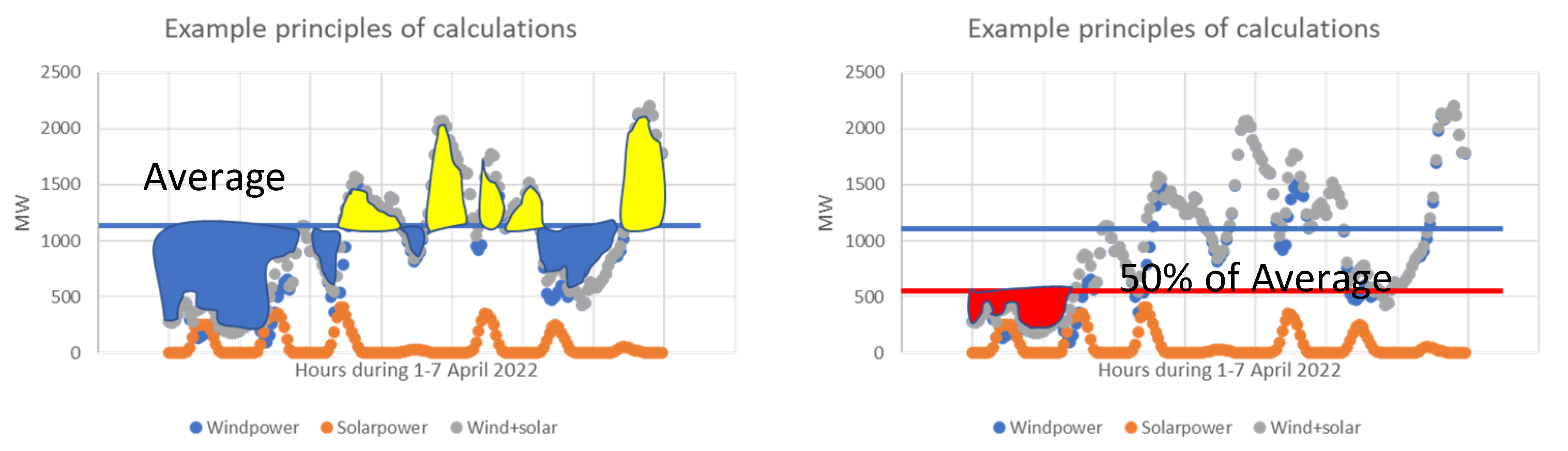

In

Figure 7, periods and accumulated energy (kWh) from solar plus wind power below and above average power are shown for January, April, July, and October 2022. Above average corresponds to battery charging, whereas below average corresponds to discharging batteries. The average power production for 2022 was 1070 MWh/h in SE-3. Above the zero-axis is surplus power for charging batteries, whereas below the axis is deficiency, when battery storage was discharged to maintain a constant power production.

In

Table 1, the time from when the production passed the average production value per month and the accumulated energy in MWh during the period is presented. Negative values below the average are in white and positive values above the average are marked in yellow.

In July, solar power compensated for varying winds. In July, the periods below and above average were generally more frequent and shorter than during January in particular. The longest period with low wind was 76 h once in July, with the second longest period lasting 42 h. For the other months, there were up to 130 h of low wind in January, 114 h in April, and 109 h in October. However, the deficiency was mostly below 60 h, or 2.5 days. The deficiency was then around 35 GWh for SE-3 in January, 28 GWh in April, and 76 GWh in October, but only 20 GWh in July for the second longest time periods. This was for all periods below and above average power production. The figures vary between years, but not much, as both wind and, to some extent, cloudiness were relatively random throughout the year. The difference between seasons was similar, especially with respect to solar-power production.

In

Figure 8, the same data are presented for periods below half of the average power production during 2022.

As shown in

Figure 8, the longest period below average in 2022 during January, April, July, and October lasted 130 h and 100,000 MWh of energy were accumulated. For half of the average, the corresponding longest period lasted 55 h and the maximum accumulated energy was 60,000 MWh.

The question then arises of what the case would be if there was five times as much wind-power production and 15 times as much solar-power production, with same distribution as for 2022. The figures are based on predictions for scenarios generated by the Swedish power board [

18]. In

Figure 9, the result of that calculation is shown for accumulated energy when production is below half of the annual average production of wind plus solar power.

The number of hours was generally the same as for the much lower production in the 2022 case, but the absolute energy was 90,000 MWh compared to 60,000 MWh in the original case for 2022.

There were significant periods with high wind production but also periods with almost zero production.

The wind-power production varied quite rapidly, as shown in

Figure 10 (in SE-3). Production changed from almost zero to 2000 MWh/h for SE-3 in less than 12 h.

As a comparison, hydropower production in SE-3 during the same period of 16–25 May 2021 is shown in

Figure 11. As can be seen, it slowly moved from 1200 to 1500 MW, which is a very different pattern compared to that of wind-power production.

Looking at only two days, 24–25 May 2021, a very strong variation in wind-power production throughout the day for SE-3 can be seen (

Figure 12).

With an average of approximately 1000 MW over two days in SE-3 (actual average value was 1070 MW 2022), it would have been beneficial to store energy in, e.g., batteries; use it on 24 May; and then recharge the batteries on 25 May. In this case, the storage capacity should have been 24 h * 1000 MW = 24,000 MWh, or 24 GWh. A shift of 500 MW from 12 p.m.–9 p.m. (9 h) would mean reducing the peak deficiency by approximately half, or 12 GWh. Looking at the solar power produced in SE-3 during the period of 16–25 May 2021, it appeared as shown in

Figure 13.

The main balancing resource was hydropower. In

Figure 14, the production in MW during one year from 1 June 2020 to 1 June 2021 is shown for SE-3.

Solar plus wind power followed hydropower, whereas other thermal power was either reduced or kept at a low level. This means that the balancing resources were not utilized. It can also be seen that when solar plus wind power was reduced, consumption was reduced. It should be noted that the price went up during these time periods, which shows that a shifting load can be as efficient as using storage to compensate for reduced power (see

Table 1 and the discussion related to this).

In

Figure 15, hydropower production for Sweden as a whole and for SE-3 in 2022 is shown. The production in SE-3 was much lower than in Sweden as a whole, which makes it important to be able to import from northern Sweden. Without nuclear power in SE-3, it would be a problem to supply what is needed in the region.

The production in SE-3 was only 10–15% of the total hydropower production in Sweden (approximately 1000 MW compared to 8000 MW on average). It is more difficult to store larger volumes in southern Sweden than in the north, as well.

On the other hand, there was much more other thermal power in SE-3 than in the other regions. This was mostly CHP production. The installed capacity was approximately 5000 MW, whereas only about 900 MW were used in the summertime in all of Sweden, and normally less than 2000 MW were used even in midwinter, when the production was at its maximum. In

Figure 16, the monthly production and consumption for the first half of 2022 are presented.

The total production this year was 11.1 TWh

el hydropower for SE-3 and 73.6 TWh

el for all of Sweden (see

Figure 15). There was lower production from June to October, but it increased during the winter until March. Generally, the production relates to how much rain falls, and in the spring it relates to how much snow melts. There is normally a possibility to vary power production within a day or a few days in the SE-3 region, but not long term in this densely populated region without the possibility of storing larger volumes of water. Still, this time horizon is normally acceptable to compensate for significant wind-power fluctuations, but with a limited amount of MWh. This capacity varies with the present situation, as weather conditions vary continuously. Whereas wind power is affected by the wind, hydropower production is affected by the rain.

Figure 17 shows solar-power production during a period in May. As can be seen, there was a variation between day and night, as well as a significant variation from one day to the next depending on cloudiness. The solar-power pattern was generally possible to predict throughout the year and day by day, but varied throughout this span of time due to varying cloudiness. Still, the intensity and hours per day were much higher during summer than during winter (see

Figure 16).

Wind power varied more irregularly, although normally there was more wind during spring and autumn.

Low wind with less than 500 MW production was quite frequent throughout the year for periods of up to approximately 48 h. Longer periods of 100 h or more below 500 MW occurred only five times from June 2020 to May 2021 (

Figure 18).

PV production can generally be calculated as a function of the day of the year and the kWh/h.m2 for a certain site. This value is multiplied by a factor 0.5–1, where 1 means that there are no clouds and 0.5 means that it is very cloudy. Hourly values were summarized per month. For a region like SE-3, these values were multiplied by the number of m2 PV cells in the area. For wind power, the total wind-power production was multiplied by the dimensional wind. This was then multiplied by the predicted actual wind speed divided by the nominal wind speed for an average plant. This was multiplied by the number of hours to obtain the kWh produced during a certain period. Hydropower production was predicted from the average production for each month based on the season and adjusted for rain in relation to the average amount of rain for the season per month. For CHP and nuclear plants, total flexibility was assumed up to the maximum production.

Wind-power production was multiplied by different probabilities to obtain the average wind in the region for the next 24 h, 48 h, 120 h, and 240 h. For solar power, cloudiness values were predicted from weather forecasts for the same time periods. From these estimations, the production from wind plus solar power was calculated for an average case. The accuracy of the prediction relies on how correct the weather forecasts are. The tool can be used to estimate demand for storage capacity and demand for load shift.

3.8. Storage Size

Concerning battery storage, power companies now invest in quite large battery storage to compete with the frequency market. Uppsala has invested in 5 MW, 20 MWh storage [

30]. Other cities have planned larger batteries with a 20+ MW capacity, which can be used for both voltage and frequency control (oral communication with Eskilstuna Strängnäs Energy and Environment and Stockholm Exergi).

Table 2.

Nordpool historical spot prices in SEK/kWh in 2018–2022 [

31].

Table 2.

Nordpool historical spot prices in SEK/kWh in 2018–2022 [

31].

| Year | SE1 | SE2 | SE3 | SE4 |

|---|

| 2022 | 0.634 | 0.664 | 1.379 | 1.62 |

| 2021 | 0.432 | 0.433 | 0.67 | 0.817 |

| 2020 | 0.15 | 0.15 | 0.221 | 0.269 |

| 2019 | 0.401 | 0.401 | 0.406 | 0.421 |

| 2018 | 0.454 | 0.454 | 0.458 | 0.476 |

Figure 18.

Time periods with less than 535 MW wind-power production in SE-3 compared to the average of 1070 MW from 1 June 2020 to 31 May 2021 [

31].

Figure 18.

Time periods with less than 535 MW wind-power production in SE-3 compared to the average of 1070 MW from 1 June 2020 to 31 May 2021 [

31].

From the previous calculations, it was determined that the appropriate size of battery storage for SE-3 is not self-evident. For the situation in 2022, the average production from wind plus solar power was 1070 MW, and half of that is 535 MW. For a scenario in 2045 with five times more wind and 15 times more solar production, the average production for wind plus solar power would be 6137 MW, and half of that is 3069 MW. For the first case, the accumulated deficiency, which is the area below the line halfway between average and zero production, for the periods of January, April, July, and October was the longest at 55 h and 60 GWh. For 2045, the storage demand for the longest period below half of the average would be 90 GWh and would have a longest deficiency period of 63 h. It would be reasonable to determine the amount below half of the average for a battery and/or H2/FC. The rest should be balanced with hydropower, other thermal power, and reduced consumption during low-wind periods through different types of financial agreements with industry and increased prices in general, which proved to be efficient during 2022.

The alternatives with 12 or 24 GWh storage capacity for the 2022 case and 6.4 or 37 GWh predicted for 2045 for periods below the 50% average yielded values proportional to the calculations for 60 and 90 GWh for periods below average. At least for today’s case, 12 or 24 GWh may be more realistic, but for the 2045 case the alternative with 37–90 GWh would probably be more realistic, as the proportion of wind plus solar power would then be much larger, whereas hydropower and CHP would probably be the same as today. On the other hand, much of the new demand will be for industries that may solve many of the balancing problems internally with large amounts of H2 storage.

Technical data for H

2 production, NH

3 production, and battery storage are provided in, e.g., [

32,

33].

The storage volume and weight are shown in

Table 3 per m

3 and ton, respectively. In

Table 4, the total weight and volume for the case with the longest period below half of the distance between the average annual production and zero production is presented: 60 GWh (2022 case) and 90 GWh (2045 scenario). In

Table 5, the case with 50% of the average power over the year for 12 h is presented: 6.4 GWh (2022 case) and 37 GWh (2045 scenario).

For electrolyzers, there may be 82% efficiency in the future and 80% for fuel cells. To compress the gas to 700 bars would consume at least 10% of the heating value of the hydrogen, which would be converted to heat. This would yield a system efficiency of 0.82*0.8*0.9 = 58%. However, today it is closer to 0.6*0.6*0.9 = 32% system efficiency, at least for the next few years. For the combination of batteries with EVs there would more likely be 0.8*0.8 = 64% to potentially 0.9*0.9 = 81% system efficiency, with the potential to become even higher.

To store energy as NH3, first H2 and N2 must react to form NH3. The conversion efficiency for H2 to NH3 is about 61–68.5%. This means that with an 82% electrolyzer efficiency and an 80% fuel-cell efficiency the total would be, assuming 68.5% H2-to-NH3 efficiency, a system efficiency = 68.5*82*80 = 45%. For batteries we calculated 90% and for H2/FC 82*80% = 65.6%.

For the case with the longest period below half of the distance between the average annual production and zero production we calculated the size of storage to be 60 GWh for 2022 and 90 GWh for the predicted 2045 scenario.

The size with respect to storage in weight in tons and volume in m

3 is the total. How much local storage there should be is not clear—either a few large storage facilities connected to some large production sites, a large number of local storage facilities connected to local production, or a combination of the two. The latter is the most probable.

Table 5 shows the case with short-term storage over 12 h but with significant power, half of the power based on the average, and half of the average for the 2022 and 2045 cases.

For the first case the difference between the 2022 case and the 2045 scenario was quite small but was significant for the 12 h storage.

As can be seen, H

2 takes up less space, but to build huge storage facilities requires digging out deep cylinders in the rock to provide support to the steel vessel. Concrete is then filled in between the cylinder and the rock wall. This is currently being demonstrated in Luleå with the Hybrit project [

34]. For batteries, State Grid in China together with Rongke Power just built a 100 MW/400 MWh vanadium sulphate/vanadiumoxidesulphate redox flow. This shows the possibility of building large-scale batteries [

35]. This is a USD 266 M investment. Pump storage had an installed capacity of 160 GW and 8500 GWh in 2020 globally. This accounted for 90% of global electricity storage [

36]. As a comparison, the battery factory in Skellefteå, Sweden, built by NorthVolt, will have a capacity of 60 GWh/year when full capacity is reached within a few years [

37].

Concerning costs, NREL [

38] made some estimates for lithium-ion batteries with 4 h storage capacity, as shown in

Table 6.

The figures are high, but in proportion to other infrastructure investments they are reasonable.

As is shown, there are several alternatives that will have advantages and disadvantages. The most probable scenario is a combination of all type of solutions. For batteries, it can be noted that a capacity of 5 million EVs with 100 kWh/vehicle would be 500 GWh. Today, there are 5 million personal cars in Sweden, which could be predicted to be all EVs in some capacity in the future, and 100 kWh/car should be a realistic size in the future. This suggests some proportions of the size for grid support with charging infrastructure and power supply.

3.9. Balancing with CHP

Concerning CHP (combined heat and power) with biomass or waste as the fuel, most power production is carried out during the winter, when there is a high heat demand. It is possible to produce more electric power by condensing steam with sea water or air if the electricity demand and price are high. For Sweden, there was an estimate made by Svebio [

39] that about 35 TWh/y could be produced from existing plants compared to 12 TWh/y produced today, due to financial conditions.

In

Figure 16, it can be seen that the relative-capacity factor for hydropower and nuclear power was highest from January to March. For solar power and PV, the maximum was in May–July, whereas wind power showed the opposite trend, as it was highest during January–March and lower during summer. For thermal power other than nuclear, mostly CHP, high production was evident during winter in January–April, but it dropped significantly during the summer, when the heat demand was lower.

Table 7 shows the actual figures in GWh/month for January–July 2022 with respect to power production and consumption.

The production and consumption proportions were similar for SE-3, despite all nuclear being produced in SE-3 but only 15% of hydropower. Hydropower outside of SE-3 was used to balance demand in SE-3. In

Table 3, the installed capacity and the maximum power for each month during the same time is shown. In

Table 8, the relative-capacity factor C

p,r is shown to vary for the different technologies.

The relative-capacity factor Cp,r is calculated as the ratio of the maximum power during one month divided by the power produced for each month. For wind and PV the Cp,r is based on the weather, whereas hydropower can be controlled to some extent. Nuclear power normally operates at the maximum possible capacity continuously, and thus reduced Cp,r is due to technical problems. For thermal, mostly CHP, a low Cp,r is seen during warm periods.

What is of special interest is that the maximum power for thermal power other than nuclear was approximately four times higher than what was produced during spring and summer. This demonstrates great potential to use bio-CHP to balance the lower wind-power production seen during spring and summer. In addition, new PV-cell systems on the roofs of buildings will be expanded and will provide another opportunity to complement wind power during summer. In absolute figures, CHP using biomass and waste could double the production compared to today during winter if heat can be utilized for other applications. Existing CHP plants could be complemented with pyrolysis to produce bio-oil and gasification for the production of H

2 and CH

4. This would provide the opportunity to increase wind power significantly and still maintain balancing power, as the focus can be on electric-power production during the time periods of a lack of power from wind. In

Table 9, the installed and max capacity per energy type and month in January–July 2022 are shown.

To store 500 MW for 48 h a capacity of 24 GWh is needed and for 12 h a capacity of 6 GWh is needed for the SE-3 region in today’s conditions (2022). Looking at the demand for all of Sweden, the corresponding figure would be three times as high, or about 72 GWh. Going from 33 TWh/y in wind power as today to about 90–120 TWh/y within 20 years as discussed, the demand for storage capacity may increase to 80–100 GWh for 48 h. On the other hand, if hydrogen is produced for industrial use, at least half of this may be covered by H2 storage if conversion efficiencies are increased and costs decreased for H2 storage. The CHP plants could yield a maximum of 4399 MW * 48 h = 211 GWh for 48 h. If some of that potential is used together with batteries, a very promising balancing potential would be achieved.

Looking at

Figure 18, it can be seen that 48 h storage was enough in most cases over the year. However, on one occasion the low wind lasted for 250 h. This would be difficult to cover completely with stores of batteries or H

2. From an economic perspective it would be reasonable to restrict the power demand during this time by increasing the price or by shutting down some demand during shorter time periods. However, production by CHP could cover much of that demand, especially if it happens during the winter season. There is also a potential to increase hydropower production during at least the winter season by some 1000 MW * 48 h = 48 GWh for a couple of days, and if it is rainy perhaps for all 10 days. However, during dry weather conditions this may be difficult. Where the demand is in relation to where the production is must also be considered. CHP plants are well distributed in SE3, where there is high heat demand from many people, whereas hydropower is mostly in the northern part of Sweden. By distributing battery storage close to where the potentially high demand is, it would be easier to balance without having to expand the grid capacity significantly.

Another aspect is the cost for different storage alternatives. It is not obvious what the cost would be for pump storage, as it would vary a lot depending on the situation. The company Mine Power is looking into using old mines for pump power with high potential in the SE-3 region. As for batteries, the average cost for new battery packs was in the range of USD 150/kWh in 2022, according to Blomberg News [

40]. The cost for just the cells was at average of USD 115/kWh. An interesting alternative is to use second-life batteries. It is not easy to know exactly where the price for these will end up. If it is assumed that 80% of the original capacity is still in the battery after its first life, potentiallya bout 10–30% could be used before the end of its life. This will vary with the battery chemistry. NMC batteries usually have a relatively flat degradation rate for a certain number of cycles but then start to drop rapidly. For LFP batteries, the degradation rate is slower but lasts more cycles; however, they are much heavier in weight per kWh storage capacity. There is a demand to determine the state of health (SoH), and from this the remaining useful life (RUL) for second-life applications. If this can be determined in a reliable way and the batteries can be used without reconfiguration, the price should be significantly lower for each stored kWh in a second-life battery than for a first-life battery. How much that would be is a guess, but it would perhaps be in the range of half of that for first life. However, the cost of new batteries has been decreasing, although it flattened out during 2022 [

40]. The cost for battery materials is increasing due to short supply, but the interest in recycling batteries for new first-life batteries is high, and most batteries are expected to end up this way. If new batteries are too inexpensive, it will be of less interest to use them in a second-life application. There will also be additional costs for the installation and operation of battery packs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}