The Effects of Crude Oil Price Surprises on National Income: Evidence from India

,

,  and

and

Abstract

1. Introduction

2. Literature Review

2.1. Currency Exchange Rates and Crude Oil

2.2. Crude Oil and GDP

3. Research Methods

3.1. Objectives of the Study

3.2. Hypotheses of the Study

- NH1—There is no normal distribution among the crude oil price shocks on GDP per capita and exchange rates (USD/INR).

- NH2—There is no stationarity among the crude oil price shocks on GDP per capita and exchange rates (USD/INR).

- NH3—There is no causal relationship between the crude oil price shocks and GDP per capita and exchange rates (USD/INR).

- NH4—There is no influence of crude oil price shocks on GDP per capita and exchange rates (USD/INR).

4. Theoretical Background

5. Data Source and Estimation Techniques

5.1. Sample Selection

5.2. Sources of Data

5.3. Variables

6. Analysis and Findings of the Study

- Normality test for the GDP and exchange rate effects of crude oil prices (USD/INR)

- Stationarity for the Effects of Crude Oil Prices on GDP and Exchange Rates (USD/INR)

- Granger Causality Test for the Impact of Oil Prices on GDP and Exchange Rate (USD/INR)

- OLS Regression Test for GDP and exchange rate effects of crude oil prices (USD/INR)

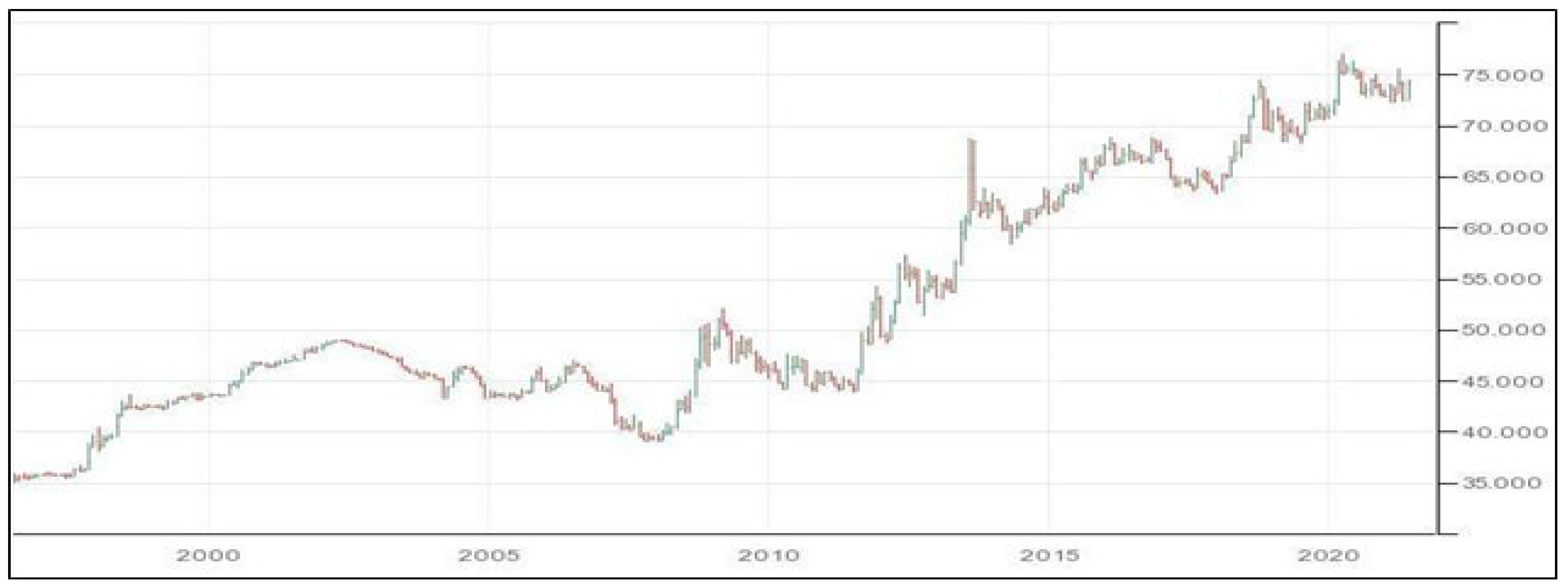

- Graphical Expression for Crude Oil Price on GDP and Exchange Rate (USD/INR)

6.1. Normality Test for Crude Oil Price on GDP and Exchange Rate (USD/INR)

6.2. Stationarity for Crude Oil on GDP and Exchange Rate (USD/INR)

6.3. Granger Causality Test for Crude Oil on GDP and Exchange Rate (USD/INR)

6.4. OLS Regression Test for the Returns of Crude Oil Price Shocks on GDP per Capita, and Exchange Rate (USD/INR)

7. Conclusions

8. Limitations of this Study

- Only two crude oil indices, namely, the Dubai index and WTI index, were selected as the sample.

- Only secondary data were used to support the study.

- This study may potentially be subject to the limitations associated with various statistical techniques.

9. Scope for Further Research

- Researchers could attempt to forecast other macro-economic variables, with reference to crude oil price movements.

- A study of this nature could be conducted in comparison with other countries.

- The study can be extended by using other econometric models to accommodate the breakpoints in the data series, which could give more insight into the data.

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Gbatu, A.P.; Wang, Z.; Wesseh, P.K.; Tutdel, I.Y. Asymmetric and dynamic Effects of oil price shocks and exchange rate fluctuations: Evidence from a panel of economic community of West African States (ECOWAS). Int. J. Energy Econ. Policy 2017, 7, 1–3. [Google Scholar]

- Akpan, E.O. Oil price shocks and Nigeria’s macro economy. In Proceedings of the Annual Conference of CSAE Conference, Economic Development in Africa March, Oxford, UK, 17–19 March 2019; pp. 22–24. [Google Scholar]

- Ju, H.; Zhang, R. Optimal resource allocation in full-duplex wireless-powered communication network. IEEE Trans. Commun. 2014, 62, 3528–3540. [Google Scholar] [CrossRef]

- Babu, M.; Lourdesraj, A.A.; Hariharan, C.; Jayapal, G.; Indhumathi, G.; Sathya, J.; Kathiravan, C. Dynamics of Volatility Spillover between Energy and Environmental, Social and Sustainable Indices. Int. J. Energy Econ. Policy 2022, 50–55. [Google Scholar] [CrossRef]

- Akaike, H. A new look at the statistical model identification. IEEE Trans. Autom. Control. 1974, 19, 716–723. [Google Scholar] [CrossRef]

- Bjørnland, H.C. The dynamic effects of aggregate demand, supply and oil price shocks—A comparative study. Manch. Sch. 2000, 68, 578–607. [Google Scholar] [CrossRef]

- Kathiravan, C.; Selvam, M.; Maniam, B.; Venkateswar, S. Relationship between Crude Oil Price Changes and Airlines Stock Price: The Case of Indian Aviation Industry. Int. J. Energy Econ. Policy 2019, 9, 7–13. [Google Scholar] [CrossRef]

- Kathiravan, C.; Selvam, M.; Venkateswar, S. Investor behavior and weather factors: Evidences from Asian region. Ann. Oper. Res. 2021, 299, 349–373. [Google Scholar] [CrossRef]

- Edwards, E.A. Development of a new scale for measuring compulsive buying behavior. Financ. Couns. Plan. 1993, 4, 67–84. [Google Scholar]

- Hem, C.D.; Sundvold-Gjerstad, V.; Granum, S.; Koll, L.; Abrahamsen, G.; Buday, L.; Spurkland, A. T cell specific adaptor protein (TSAd) promotes interaction of Nck with Lck and SLP-76 in T cells. Cell Commun. Signal. 2015, 13, 31. [Google Scholar] [CrossRef]

- Bal, D.P.; Rath, B.N. Nonlinear Causality between Crude Oil Price and Exchange Rate: A Comparative Study of China and India. Energy Econ. 2015, 51, 149–156. [Google Scholar] [CrossRef]

- Planning Commission—Government of India. Government of India Planning Commission. 2006, Volume II. Available online: https://nhm.gov.in/images/pdf/publication/Planning_Commission/12th_Five_year_plan-Vol-1.pdf (accessed on 20 May 2021).

- Briefing, U.S. International energy outlook 2013. US Energy Inf. Adm. 2013, 506, 507. [Google Scholar]

- Burbidge, J.; Harrison, A. Testing for the effects of oil-price rises using vector auto regressions. Int. Econ. Rev. 1984, 25, 459–484. [Google Scholar] [CrossRef]

- Ng, S.; Perron, P. Unit root tests in ARMA models with data-dependent methods for the selection of the truncation lag. J. Am. Stat. Assoc. 1995, 90, 268–281. [Google Scholar] [CrossRef]

- Chen, S.S.; Chen, H.C. Oil prices and real exchange rates. Energy Econ. 2007, 29, 390–404. [Google Scholar] [CrossRef]

- Yu, L.; Wang, S.; Lai, K.K. Forecasting crude oil price with an EMD-based neural network ensemble learning paradigm. Energy Econ. 2008, 30, 2623–2635. [Google Scholar] [CrossRef]

- Cunado, J.; De Gracia, F.P. Oil prices, economic activity and inflation: Evidence for some Asian countries. Q. Rev. Econ. Financ. 2005, 45, 65–83. [Google Scholar] [CrossRef]

- Edwards, S. Openness, productivity and growth: What do we really know? Econ. J. 1998, 108, 383–398. [Google Scholar] [CrossRef]

- Wagner, J. Exports and productivity: A survey of the evidence from firm-level data. World Econ. 2007, 30, 60–82. [Google Scholar] [CrossRef]

- Frankel, J.A.; Romer, D.H. Does trade cause growth? Am. Econ. Rev. 1999, 89, 379–399. [Google Scholar] [CrossRef]

- Cunado, J.; Jo, S.; de Gracia, F.P. Macroeconomic impacts of oil price shocks in Asian economies. Energy Policy 2015, 86, 867–879. [Google Scholar] [CrossRef]

- Dabachi, U.M.; Mahmood, S.; Ahmad, A.U.; Ismail, S.; Farouq, I.S.; Jakada, A.H.; Kabiru, K. Energy consumption, energy price, energy intensity environmental degradation, and economic growth nexus in African OPEC countries: Evidence from simultaneous equations models. J. Environ. Treat. Tech. 2020, 8, 403–409. [Google Scholar]

- Almulali, U.; Sab, C.N.B.C. Exploring the impact of oil revenues on OPEC members’ macroeconomy. OPEC Energy Rev. 2013, 37, 416–428. [Google Scholar] [CrossRef]

- Cologni, A.; Manera, M. The asymmetric effects of oil shocks on output growth: A Markov–Switching analysis for the G-7 countries. Econ. Model. 2009, 26, 1–29. [Google Scholar] [CrossRef]

- Mensah, G.A.; Wei, G.S.; Sorlie, P.D.; Fine, L.J.; Rosenberg, Y.; Kaufmann, P.G.; Mussolino, M.E.; Hsu, L.L.; Addou, E.; Engelgau, M.M.; et al. Decline in cardiovascular mortality: Possible causes and implications. Circ. Res. 2017, 120, 366–380. [Google Scholar] [CrossRef]

- Camarero, M.; Tamarit, C. Oil prices and Spanish competitiveness: A cointegrated panel analysis. J. Policy Model. 2002, 24, 591–605. [Google Scholar] [CrossRef]

- Zhang, Y.J.; Fan, Y.; Tsai, H.T.; Wei, Y.M. Spillover effect of us dollar exchange rate on oil prices. J. Policy Model. 2008, 30, 973–991. [Google Scholar] [CrossRef]

- Ghosh, S. Examining crude oil price-exchange rate nexus for India during the period of extreme oil price volatility. Appl. Energy 2011, 88, 1886–1889. [Google Scholar] [CrossRef]

- Turhan, M.I.; Sensoy, A.; Hachihasanoglu, E. A comparative analysis of the dynamic relationship between oil prices and exchange rates. J. Int. Financ. Mark. Inst. Money 2014, 32, 397–414. [Google Scholar] [CrossRef]

- Mork, K.A. Oil and the macroeconomy when prices go up and down: An extension of Hamilton’s results. J. Political Econ. 1989, 97, 740–744. [Google Scholar] [CrossRef]

- Ferderer, J.P. Oil price volatility and the macroeconomy. J. Macroecon. 1996, 18, 1–26. [Google Scholar] [CrossRef]

- Kilian, L. The economic effects of energy price shocks. J. Econ. Lit. 2008, 46, 871–909. [Google Scholar] [CrossRef]

- Rahman, S.; Serletis, A. Oil price uncertainty and the Canadian economy: Evidence from a VARMA, GARCH-in-Mean, asymmetric BEKK model. Energy Econ. 2012, 34, 603–610. [Google Scholar] [CrossRef]

- Narayan, P.K.; Sharma, S.S. Firm return volatility and economic gains: The role of oil prices. Econ. Model. 2014, 38, 142–151. [Google Scholar] [CrossRef]

- Hamilton, J.D. Oil and the macroeconomy since World War II. J. Political Econ. 1983, 91, 228–248. [Google Scholar] [CrossRef]

- Kathiravan, C.; Selvam, M.; Kannaiah, D.; Lingaraja, K.; Thanikachalam, V. On the relationship between weather and Agricultural Commodity Index in India: A study with reference to Dhaanya of NCDEX. Qual. Quant. 2019, 53, 667–683. [Google Scholar] [CrossRef]

- Lorusso, M.; Pieroni, L. Causes and consequences of oil price shocks on the UK economy. Econ. Model. 2018, 72, 223–236. [Google Scholar] [CrossRef]

- Basak, S.; Pavlova, A. A model of financialization of commodities. J. Financ. 2016, 71, 1511–1556. [Google Scholar] [CrossRef]

- Kilian, L. Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. Am. Econ. Rev. 2009, 99, 1053–1069. [Google Scholar] [CrossRef]

- Cavalcanti, T.; Jalles, J.T. Macroeconomic effects of oil price shocks in Brazil and in the United States. Appl. Energy 2013, 104, 475–486. [Google Scholar] [CrossRef]

- Loungani, P. Oil price shocks and the dispersion hypothesis. Rev. Econ. Stat. 1986, 68, 536–539. [Google Scholar] [CrossRef]

- Filis, G.; Degiannakis, S.; Floros, C. Dynamic correlation between stock market and oil prices: The case of oil-importing and oil-exporting countries. Int. Rev. Financ. Anal. 2011, 20, 152–164. [Google Scholar] [CrossRef]

- Murshed, M. An empirical analysis of the non-linear impacts of ICT-trade openness on renewable energy transition, energy efficiency, clean cooking fuel access and environmental sustainability in South Asia. Environ. Sci. Pollut. Res. 2020, 27, 36254–36281. [Google Scholar] [CrossRef] [PubMed]

- Jiménez-Rodríguez, R.; Sánchez, M. Oil price shocks and real GDP growth: Empirical evidence for some OECD countries. Appl. Econ. 2005, 37, 201–228. [Google Scholar] [CrossRef]

- Ratti, R.A.; Vespignani, J.L. Why are crude oil prices high when global activity is weak? Econ. Lett. 2013, 121, 133–136. [Google Scholar] [CrossRef]

- Lingaraja, K.; Mohan, C.; Selvam, M.; Raja, M.; Kathiravan, C. Exchange rate volatility and causality effect of Sri Lanka (LKR) with Asian emerging countries currency against USD. Int. J. Manag. 2020, 11. [Google Scholar]

- Nazlioglu, S.; Gupta, R.; Bouri, E. Movements in international bond markets: The role of oil prices. Int. Rev. Econ. Financ. 2020, 68, 47–58. [Google Scholar] [CrossRef]

- Sreenu, N. A Study of Advance Capital Assets Pricing Model (CAPM) and Three Factor Model of FAMA: The France Context. IPE J. Manag. 2016, 6, 1. [Google Scholar]

- Gbatu, A.P.; Wang, Z.; Wesseh, P.K., Jr.; Tutdel, I.Y. The impacts of oil price shocks on small oil-importing economies: Time series evidence for Liberia. Energy 2017, 139, 975–990. [Google Scholar] [CrossRef]

- Usman, M.; Kousar, R.; Yaseen, M.R.; Makhdum, M.S. An empirical nexus between economic growth, energy utilization, trade policy, and ecological footprint: A continent-wise comparison in upper-middle-income countries. Environ. Sci. Pollut. Res. 2020, 27, 38995–39018. [Google Scholar] [CrossRef]

- Widarjono, A.; Anto, M.; Fakhrunnas, F. Financing Risk in Indonesian Islamic Rural Banks: Do Financing Products Matter? J. Asian Financ. Econ. Bus. 2020, 7, 305–314. [Google Scholar] [CrossRef]

- Kathiravan, C.; Selvam, M.; Maniam, B.; Dharani, M. Effect of weather on stock market: A literature review and research agenda. Cogent Econ. Financ. 2021, 9, 1971353. [Google Scholar] [CrossRef]

- Anashasy, E.A.; Bradley, M.D.; Joutz, F. Evidence on the Role of Oil Prices in Venezuela’s Economics Performance (1950–2001); Working Paper; University of Washington: Seattle, WA, USA, 2005. [Google Scholar]

- El Anshasy, A. Oil prices and economic growth in oil-exporting countries. In Proceedings of the 32nd International IAEE Conference, San Francisco, CA, USA, 21–24 June 2009. [Google Scholar]

- Farzanegan, M.R.; Markwardt, G. The effects of oil price shocks on the Iranian economy. Energy Econ. 2009, 31, 134–151. [Google Scholar] [CrossRef]

- Mendoza, O.; Vera, D. The asymmetric effects of oil shocks on an oil-exporting economy. Cuad. Econ. 2010, 47, 3–13. [Google Scholar] [CrossRef]

- Fezzani, B.; Nartova, D. Oil prices fluctuation impact on Iraq’s economy. Eur. J. Soc. Sci. 2011, 26, 626–633. [Google Scholar]

- Moshiri, S.; Banihashem, A. Asymmetric effects of oil price shocks on economic growth of oil-exporting countries. SSRN 2012, 2006763. [Google Scholar] [CrossRef]

- Ito, K. The impact of oil price volatility on the macroeconomy in Russia. Ann. Region. Sci. 2012, 48, 695–702. [Google Scholar] [CrossRef]

- Alkhathlan, K.; Javid, M. Energy consumption, carbon emissions and economic growth in Saudi Arabia: An aggregate and disaggregate analysis. Energy Policy 2013, 62, 1525–1532. [Google Scholar] [CrossRef]

- Nwani, C.; Orie, J.B. Economic growth in oil-exporting countries: Do stock market and banking sector development matter? Evidence from Nigeria. Cogent Econ. Financ. 2016, 4, 1153872. [Google Scholar] [CrossRef]

- Nusair, S.A. The effects of oil price shocks on the economies of the Gulf Co-operation Council countries: Nonlinear analysis. Energy Policy 2016, 91, 256–267. [Google Scholar] [CrossRef]

- Benramdane, A. Oil price volatility and economic growth in Algeria. Energy Sources Part B Econ. Plan. Policy 2017, 12, 338–343. [Google Scholar] [CrossRef]

- Sadeghi, A. Oil Price Shocks and Economic Growth in Oil-Exporting Countries: Does the Size of Government Matter? Int. Monet. Fund 2017. [Google Scholar] [CrossRef]

- Vohra, R. The impact of oil prices on GCC economies. Int. J. Bus. Soc. Sci. 2017, 8, 7–14. [Google Scholar]

- Foudeh, M. The long run effects of oil prices on economic growth: The case of Saudi Arabia. Int. J. Energy Econ. Policy 2017, 7, 171. [Google Scholar]

- Alekhina, V.; Yoshino, N. Impact of world oil prices on an energy exporting economy including monetary policy. ADBI Work. Pap. 2018. [Google Scholar]

- Taghizadeh-Hesary, F.; Yoshino, N.; Rasoulinezhad, E.; Chang, Y. Trade linkages and transmission of oil price fluctuations. Energy Policy 2019, 133, 110872. [Google Scholar] [CrossRef]

- Balashova, S.; Serletis, A. Oil prices shocks and the Russian economy. J. Econ. Asymm. 2020, 21, e00148. [Google Scholar] [CrossRef]

- Abdelsalam, M.A. Oil price fluctuations and economic growth: The case of MENA countries. Rev. Econ. Political Sci. 2020. [Google Scholar] [CrossRef]

- Jahangir, S.R.; Dural, B.Y. Crude oil, natural gas, and economic growth: Impact and causality analysis in Caspian Sea region. Int. J. Manag. Econ. 2018, 54, 169–184. [Google Scholar] [CrossRef]

- Jiménez-Rodríguez, R. Oil price shocks and stock markets: Testing for non-linearity. Empir. Econ. 2015, 48, 1079–1102. [Google Scholar] [CrossRef]

- Mukhtarov, S.; Aliyev, S.; Mikayilov, J.I.; Ismayilov, A.; Rzayev, A. The FDI-CO2 nexus from the sustainable development perspective: The case of Azerbaijan. Int. J. Sustain. Dev. World Ecol. 2021, 28, 246–254. [Google Scholar] [CrossRef]

- Mankiw, N.G.; Romer, D.; Weil, D.N. A contribution to the empirics of economic growth. Q. J. Econ. 1992, 107, 407–437. [Google Scholar] [CrossRef]

- Demirer, R.; Jategaonkar, S.P.; Khalifa, A.A. Oil price risk exposure and the cross-section of stock returns: The case of net exporting countries. Energy Econ. 2015, 49, 132–140. [Google Scholar] [CrossRef]

- Silvapulle, P.; Smyth, R.; Zhang, X.; Fenech, J.P. Nonparametric panel data model for crude oil and stock market prices in net oil importing countries. Energy Econ. 2017, 67, 255–267. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Authors Details | Country | Crude Oil Impact on GDP |

|---|---|---|

| El Anshasy (2009) [55] | 15 oil-exporting countries | Positive effect |

| Farzanegan, M.R (2009) [56] | Iran | Positive effect |

| Mendoza and Vera (2010) [57] | Venezuela | Positive effect |

| Fezzani and Nartova (2011) [58] | Iraq | Positive effect |

| Moshiri and Banihashem (2012) [59] | Kuwait and Saudi Arabia | Negative effect |

| Ito (2012) [60] | Russia | Negative effect |

| Alkhathlan (2013) [61] | Saudi Arabia | Negative effect |

| Nwani and Orie (2016) [62] | Nigeria | Positive effect |

| Nusair (2016) [63] | Gulf Cooperation Council (GCC) countries | Positive effect |

| Benramdane (2017) [64] | Algeria | Positive effect |

| Sadeghi (2017) [65] | 28 oil-exporting countries | Positive effect |

| Vohra (2017) [66] | Gulf Cooperation Council (GCC) countries | Positive effect |

| Foudeh (2017) [67] | Saudi Arabia | Positive effect |

| Alekhina and Yoshino (2018) [68] | Non-OPEC countries | Positive effect |

| Taghizadeh-Hesary et al. (2019) [69] | oil exporting Countries | Positive effect |

| Balashova, and Serletis (2020) [70] | Russia | Positive effect |

| Abdelsalam (2020) [71] | MENA countries | Positive effect |

| Variables | GDP (USD) | Exchange Rate (USD/INR) | Sample Crude Oils | ||

|---|---|---|---|---|---|

|

Descriptive Statistics | Dubai Crude (USD) | WTI (USD) | |||

| Mean | −0.054688 | 0.007888 | −0.001579 | 0.05494 | |

| Max. | 0.212836 | 0.200351 | 0.886789 | 0.581721 | |

| Mini. | −0.215476 | −0.170664 | −0.345377 | −0.476589 | |

| Std. Dev. | 0.080218 | 0.089152 | 0.276779 | 0.237845 | |

| Skew. | 0.882229 | 0.109226 | 1.352391 | −0.071378 | |

| Kurt. | 5.61316 | 2.696174 | 4.975049 | 2.812809 | |

| Jarque-Bera | 12.4274 | 8.175039 | 14.02083 | 9.069275 | |

| Prob. | 0.002002 | 0.006201 | 0.000902 | 0.005956 | |

| ADF | PP | ||||

|---|---|---|---|---|---|

| GDP (USD) | t-Statistic | Prob. | t-Statistic | Prob. | |

| −6.281444 | 0 | −6.375143 | 0 | ||

| Test critical values: | 1% level | −3.679322 | −3.679322 | ||

| 5% level | −2.967767 | −2.967767 | |||

| 10% level | −2.622989 | −2.622989 | |||

| Exchange rate (USD/INR) | t-Statistic | Prob. | t-Statistic | Prob. | |

| −3.921206 | 0.0056 | −3.956364 | 0.0051 | ||

| Test critical values: | 1% level | −3.679322 | −3.679322 | ||

| 5% level | −2.967767 | −2.967767 | |||

| 10% level | −2.622989 | −2.622989 | |||

| WTI (USD) | t-Statistic | Prob. | t-Statistic | Prob. | |

| −4.808928 | 0.0006 | −4.775808 | 0.0006 | ||

| Test critical values: | 1% level | −3.679322 | −3.679322 | ||

| 5% level | −2.967767 | −2.967767 | |||

| 10% level | −2.622989 | −2.622989 | |||

| Dubai Crude (USD) | t-Statistic | Prob. | t-Statistic | Prob. | |

| −4.799945 | 0.0006 | −4.793186 | 0.0006 | ||

| Test critical values: | 1% level | −3.679322 | −3.679322 | ||

| 5% level | −2.967767 | −2.967767 | |||

| 10% level | −2.622989 | −2.622989 | |||

| Lag | LogL | LR | FPE | AIC | SC | HQ |

|---|---|---|---|---|---|---|

| 0 | 70.64681 | NA | 5.68 × 10−8 | −5.331745 | −5.136725 | −5.277655 |

| 1 | 106.3954 | 57.19778 | 1.20 × 10−8 | −6.911634 | −5.936533 | −6.641183 |

| 2 | 117.6304 | 14.38080 | 1.96 × 10−8 | −6.530434 | −4.775253 | −6.043622 |

| 3 | 134.0805 | 15.79209 | 2.59 × 10−8 | −6.566442 | −4.031180 | −5.863268 |

| 4 | 154.4214 | 13.01814 | 3.85 × 10−8 | −6.913709 | −3.598367 | −5.994174 |

| 5 | 225.7380 | 22.82132 | 2.95 × 10−9 | −11.33904 | −7.243617 | −10.20314 |

| Null Hypothesis (H0) | F-Statistic | Prob. | Decision |

|---|---|---|---|

| Exchanges does not Granger Cause Dubai Crude | 2.18417 | 0.1354 | Don’t Reject H0 |

| Dubai Crude does not Granger Cause Exchanges | 4.93553 | 0.0165 | Reject H0 |

| GDP does not Granger Cause Dubai Crude | 2.25433 | 0.1276 | Don’t Reject H0 |

| Dubai Crude does not Granger Cause GDP | 1.08634 | 0.3541 | Don’t Reject H0 |

| WTI does not Granger Cause Dubai Crude | 0.20226 | 0.8183 | Don’t Reject H0 |

| Dubai Crude does not Granger Cause WTI | 68.7768 | 2.0010 | Don’t Reject H0 |

| GDP does not Granger Cause EXCHANGES | 0.3751 | 0.6913 | Don’t Reject H0 |

| Exchanges does not Granger Cause GDP | 0.17172 | 0.8433 | Don’t Reject H0 |

| WTI does not Granger Cause Exchanges | 1.62921 | 0.2179 | Don’t Reject H0 |

| Exchanges does not Granger Cause WTI | 6.79922 | 0.0048 | Reject H0 |

| WTI does not Granger Cause GDP | 1.03775 | 0.3703 | Don’t Reject H0 |

| GDP does not Granger Cause WTI | 3.60339 | 0.0435 | Reject H0 |

| Variables | Coefficient | Std. Error | t | Sig. |

|---|---|---|---|---|

| (Constant) | 0.0978 | 0.0932 | −3.756 | 0.000 |

| GDP per capita | 0.0012 | 0.0048 | 0.0025 | 0.954 |

| Exchange rate | 0.0003 | 0.0002 | 0.0005 | 0.006 |

| R-squared | 0.7909 | F-statistic | 1.0669 | |

| Durbin–Watson stat | 2.1255 | Prob (F-statistic) | 0.3743 | |

| Dependent Variable: Dubai crude oil price | ||||

| Variables | Coefficient | Std. Error | t | Sig. |

|---|---|---|---|---|

| (Constant) | 0.00785 | 0.00049 | 2.0544 | 0.01701 |

| GDP per capita | −0.00601 | 0.02004 | 2.62209 | 0.0600 |

| Exchange rate | 0.00109 | 0.01805 | 2.09305 | 0.0120 |

| R-squared | 0.6926 | F-statistic | 1.0563 | |

| Durbin–Watson stat | 2.2255 | Prob (F-statistic) | 0.6474 | |

| Dependent Variable: WTI crude oil price | ||||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kathiravan, C.; Selvam, M.; Maniam, B.; Dana, L.P.; Babu, M. The Effects of Crude Oil Price Surprises on National Income: Evidence from India. Energies 2023, 16, 1148. https://doi.org/10.3390/en16031148

Kathiravan C, Selvam M, Maniam B, Dana LP, Babu M. The Effects of Crude Oil Price Surprises on National Income: Evidence from India. Energies. 2023; 16(3):1148. https://doi.org/10.3390/en16031148

Chicago/Turabian StyleKathiravan, Chinnadurai, Murugesan Selvam, Balasundram Maniam, Leo Paul Dana, and Manivannan Babu. 2023. "The Effects of Crude Oil Price Surprises on National Income: Evidence from India" Energies 16, no. 3: 1148. https://doi.org/10.3390/en16031148

APA StyleKathiravan, C., Selvam, M., Maniam, B., Dana, L. P., & Babu, M. (2023). The Effects of Crude Oil Price Surprises on National Income: Evidence from India. Energies, 16(3), 1148. https://doi.org/10.3390/en16031148