The Reporting of SDGs by Quality, Environmental, and Occupational Health and Safety-Certified Organizations

Abstract

1. Introduction

2. Literature Review

2.1. Quality, Environmental, and Health and Safety Management Systems

2.2. Sustainable Development Goals (SDGs)

2.3. The Reporting of SDGs

3. Methodology

3.1. Research Hypotheses

3.2. Data Collection and Sample

3.3. Materials and Methods

- The documents of analysis (corpus), encompassing the companies’ institutional reports (e.g., sustainability reports, integrated reports, environmental reports, management reports, annual reports, governance reports) available on the websites of QEOHS-certified organizations;

- The categories of analysis, in this research, based on the economic environmental and social dimension of SD;

- The units of analysis, as concepts (themes, words, or phrases) that translate SD commitment.

- SDGCI (0,1)—Sustainable Development Goals Communication Index (binary)

- BV—Business volume

- AS—Activity sector

- UM—UNGC NP members

- SR—Sustainability reports

- β—Regression coefficients

- ε—Error term

- logit—Link function

- P—Conditional probability

- j—Organization

4. Results

4.1. Descriptive Analysis

4.2. Univariuate, Bivariate and Multivariate Analysis

5. Discussion and Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| Research Variables | Tests of Normality | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Kolmogorov–Smirnov * | Shapiro–Wilk | ||||||||

| Dependent | Statistic | df | p-Value | Statistic | df | p-Value | |||

| SDG CI | Sustainable Development Goals Communication Index | 0.428 | 235 | 0.000 | 0.603 | 235 | 0.000 | ||

| Independent | Category | Statistic | df | p-Value | Statistic | df | p-Value | ||

| BV | Business volume | 0 | Other | 0.466 | 141 | 0.000 | 0.521 | 141 | 0.000 |

| 1 | Greater | 0.367 | 94 | 0.000 | 0.702 | 94 | 0.000 | ||

| AS | Activity sector | 0 | Other | 0.424 | 103 | 0.000 | 0.609 | 103 | 0.000 |

| 1 | Second sector | 0.431 | 132 | 0.000 | 0.600 | 132 | 0.000 | ||

| UM | UNGC NP members | 0 | No | 0.463 | 190 | 0.000 | 0.501 | 190 | 0.000 |

| 1 | Member | 0.257 | 45 | 0.000 | 0.818 | 45 | 0.000 | ||

| SR | Sustainability reports | 0 | No | 0.498 | 129 | 0.000 | 0.391 | 129 | 0.000 |

| 1 | Disclose | 0.331 | 106 | 0.000 | 0.764 | 106 | 0.000 | ||

| Research Variables | Dependent | Sustainable Development Goals communication index | ||||

|---|---|---|---|---|---|---|

| Statistical Parameters | Tests of Homogeneity of Variance | |||||

| Independent | Levene statistic | df1 | df2 | p-Value | ||

| BV | Business volume | Based on mean | 6.538 | 1 | 233 | 0.011 |

| Based on median | 4.483 | 1 | 233 | 0.035 | ||

| AS | Activity sector | Based on mean | 6.611 | 1 | 233 | 0.011 |

| Based on median | 1.377 | 1 | 233 | 0.242 | ||

| UM | UNGC NP members | Based on mean | 28.161 | 1 | 233 | 0.000 |

| Based on median | 26.969 | 1 | 233 | 0.000 | ||

| SR | Sustainability reports | Based on mean | 30.469 | 1 | 233 | 0.000 |

| Based on median | 19.330 | 1 | 233 | 0.000 | ||

| Research Variables | Correlations Matrix | |||||

|---|---|---|---|---|---|---|

| Independent | Statistical Parameter | BV | AS | UM | SR | |

| BV | Business volume | Pearson correlation | 1 | 0.196 | 0.000 | 0.168 |

| p-Value | ̶ | 0.003 | 1.000 | 0.010 | ||

| N | 235 | 235 | 235 | 235 | ||

| AS | Activity sector | Pearson correlation | 0.196 | 1 | 0.059 | −0.233 |

| p-Value | 0.003 | ̶ | 0.365 | 0.000 | ||

| N | 235 | 235 | 235 | 235 | ||

| UM | UNGC NP members | Pearson correlation | 0.000 | 0.059 | 1 | 0.059 |

| p-Value | 1.000 | 0.365 | ̶ | 0.370 | ||

| N | 235 | 235 | 235 | 235 | ||

| SR | Sustainability reports | Pearson correlation | 0.168 | −0.233 | 0.059 | 1 |

| p-Value | 0.010 | 0.000 | 0.370 | ̶ | ||

| N | 235 | 235 | 235 | 235 | ||

| Research Variables | Collinearity Statistics | |||

|---|---|---|---|---|

| Independent | Model | Tolerance | Variance Inflation Factor (VIF) | |

| BV | Business volume | 1 | 0.913 | 1.096 |

| AS | Activity sector | 0.883 | 1.133 | |

| UM | UNGC NP members | 0.990 | 1.010 | |

| SR | Sustainability reports | 0.893 | 1.120 | |

| Model | Dimension | Eigenvalue | Condition Index | Variance Proportions | ||||

|---|---|---|---|---|---|---|---|---|

| Constant | BV | AS | UM | SR | ||||

| 1 | 1 | 3.029 | 1.000 | 0.020 | 0.040 | 0.030 | 0.030 | 0.030 |

| 2 | 0.770 | 1.983 | 0.000 | 0.090 | 0.010 | 0.880 | 0.010 | |

| 3 | 0.615 | 2.219 | 0.000 | 0.000 | 0.250 | 0.000 | 0.480 | |

| 4 | 0.419 | 2.690 | 0.070 | 0.870 | 0.110 | 0.090 | 0.060 | |

| 5 | 0.166 | 4.273 | 0.900 | 0.000 | 0.610 | 0.010 | 0.420 | |

References

- World Commission on Environment and Development—WCED. Our Common Future; Oxford University Press: New York, NY, USA, 1987. [Google Scholar]

- International Organization for Standardization. Contributing to the UN SDGs with ISO Standards; International Organization for Standardization: Geneva, Switzerland, 2018. [Google Scholar]

- Tarí, J.J.; Molina-Azorín, J.F.; Heras, I. Benefits of the ISO 9001 and ISO 14001 Standards: A literature review. J. Ind. Eng. Manag. 2012, 5, 297–322. [Google Scholar] [CrossRef]

- Fonseca, L.M.; Domingues, J.P.; Machado, P.B.; Calderón, M. Management system certification benefits: Where do we stand? J. Ind. Eng. Manag. 2017, 10, 476–494. [Google Scholar] [CrossRef]

- Topple, C.; Donovan, J.D.; Masli, E.K.; Borgert, T. Corporate sustainability assessments: MNE engagement with sustainable development and the SDGs. Transnatl. Corp. 2017, 24, 61–71. [Google Scholar] [CrossRef]

- Morioka, S.N.; Bolis, I.; Evans, S.; Carvalho, M.M. Transforming sustainability challenges into competitive advantage: Multiple case studies kaleidoscope converging into sustainable business models. J. Clean. Prod. 2017, 167, 723–738. [Google Scholar] [CrossRef]

- Stafford-Smith, M.; Griggs, D.; Gaffney, O.; Ullah, F.; Reyers, B.; Kanie, N.; Stigson, B.; Shrivastava, P.; Leach, M.; O’Connell, D. Integration: The key to implementing the Sustainable Development Goals. Sustain. Sci. 2017, 12, 911–919. [Google Scholar] [CrossRef]

- Büthe, T.; Mattli, W. The New Global Rulers: The Privatization of Regulation in the World Economy; Princeton University Press: Princeton, NJ, USA, 2011. [Google Scholar]

- International Organization for Standardization. ISO 9001:2015. Quality Management Systems—Requirements; International Organization for Standardization: Geneva, Switzerland, 2015. [Google Scholar]

- International Organization for Standardization. ISO 14001:2015. Environmental Management System: Requirements with Guidance for Use; International Organization for Standardization: Geneva, Switzerland, 2015. [Google Scholar]

- British Standards Institution. OHSAS 18001:2007—Occupational Health and Safety Management Certification; British Standards Institution: London, UK, 2007. [Google Scholar]

- International Organization for Standardization. ISO 45001:2018. Occupational Health and Safety Management System: Requirements with Guidance for Use; International Organization for Standardization: Geneva, Switzerland, 2018. [Google Scholar]

- Fonseca, L.M. From quality gurus and TQM to ISO 9001:2015: A review of several quality paths. Int. J. Qual. Res. 2015, 9, 167–180. [Google Scholar]

- Yahya, S.; Goh, W.K. The implementation of an ISO 9000 quality system. Int. J. Qual. Reliab. Manag. 2001, 18, 941–966. [Google Scholar] [CrossRef]

- Rodríguez-Escobar, J.A.; Gonzalez-Benito, J.; Martínez-Lorente, A.R. An analysis of the degree of small companies’ dissatisfaction with ISO 9000 certification. Total Qual. Manag. Bus. 2006, 17, 507–521. [Google Scholar] [CrossRef]

- Poksinska, B.; Eklund, J.; Jörn, D.; Jens, J. ISO 9001:2000 in small organizations. Int. J. Qual. Reliab. Manag. 2006, 23, 490–512. [Google Scholar] [CrossRef]

- Han, S.B.; Chen, S.K. Effects of ISO 9000 on customer satisfaction. Int. J. Prod. Qual. Manag. 2007, 2, 208–220. [Google Scholar] [CrossRef]

- Singh, P.J. Empirical assessment of ISO 9000 related management practices and performance relationships. Int. J. Prod. Econ. 2008, 113, 40–59. [Google Scholar] [CrossRef]

- Prajogo, D.I. The roles of firms’ motives in affecting the outcomes of ISO 9000 adoption. Int. J. Oper. Prod. Manag. 2011, 31, 78–100. [Google Scholar] [CrossRef]

- Chatzoglou, P.; Chatzoudes, D.; Kipraios, N. The impact of ISO 9000 certification on firms’ financial performance. Int. J. Oper. Prod. Manag. 2015, 35, 145–174. [Google Scholar] [CrossRef]

- Zimon, D. Influence of quality management system on improving process in small and medium-sized organizations. Qual. Access Success 2016, 17, 61–64. [Google Scholar]

- Fonseca, L.M.; Domingues, J.P. Empirical research of the ISO 9001:2015 transition process in Portugal: Motivations, benefits, and success factors. Qual. Innov. Prosper. 2018, 22, 16–64. [Google Scholar] [CrossRef]

- Fonseca., L.C.M.; Domingues, J.P.; Machado, P.B.; Harder, D. ISO 9001:2015 Adoption: A Multi-Country Empirical Research. J. Ind. Eng. Manag. 2019, 12, 27–50. [Google Scholar] [CrossRef]

- Castka, P.; Corbett, C.J. Management systems standards: Diffusion, impact and governance of ISO 9000, ISO 14000, and other management standards. Found. Trends® Technol. Inf. Oper. Manag. 2015, 7, 161–379. [Google Scholar] [CrossRef]

- Karapetrovic, S.; Casadesús-Fa, M.; Heras-Saizarbitoria, I. What happened to the ISO 9000 lustre? An eight-year study. Total Qual. Manag. 2010, 21, 245–267. [Google Scholar] [CrossRef]

- Casadesús, M.; Giménez, G. The benefits of the implementation of the ISO 9000 standard: Empirical research in 288 Spanish companies. TQM Mag. 2000, 12, 432–441. [Google Scholar] [CrossRef]

- Boiral, O. ISO 9000 and organizational effectiveness: A systematic review. Qual. Manag. J. 2012, 19, 16–37. [Google Scholar] [CrossRef]

- Siva, V.; Gremyr, I.; Bergquist, B.; Garvare, R.; Zobel, T.; Isaksson, R. The support of Quality Management to sustainable development: A literature review. J. Clean. Prod. 2016, 138, 148–157. [Google Scholar] [CrossRef]

- Angell, L.C.; Klassen, R.D. Integrating environmental issues into the mainstream: An agenda for research in operations management. J. Oper. Manag. 1999, 17, 575–598. [Google Scholar] [CrossRef]

- Fonseca, L.M.C.M. ISO 14001:2015 An improved tool for sustainability. J. Ind. Eng. Manag. 2015, 8, 37–50. [Google Scholar] [CrossRef]

- Ann, G.E.; Zailani, S.; Wahid, N.A. A study on the impact of environmental management system (EMS) certification towards firms’ performance in Malaysia. Manag. Environ. Qual. Int. J. 2006, 1, 73–93. [Google Scholar] [CrossRef]

- Saizarbitoria, I.H.; Fa, M.C.; Viadiu, F.M. ISO 9000 and ISO 14000 standards: An international diffusion model. Int. J. Oper. Prod. Manag. 2006, 26, 141–165. [Google Scholar] [CrossRef]

- Oliveira, O.J.; Serra, J.R.; Salgado, M.H. Does ISO 14001 work in Brazil? J. Clean. Prod. 2010, 18, 1797–1806. [Google Scholar] [CrossRef]

- Oliveira, J.A.; Oliveira, O.J.; Ometto, A.R.; Ferraudo, A.S.; Salgado, M.H. Environmental Management System ISO 14001 factors for promoting the adoption of Cleaner Production practices. J. Clean. Prod. 2016, 133, 1384–1394. [Google Scholar] [CrossRef]

- Watson, M.; Emery, A.R.T. Environmental management and auditing systems: The reality of environmental self-regulation. Manag. Audit. J. 2004, 19, 916–928. [Google Scholar] [CrossRef]

- Fortunski, B. Does the environmental management standard ISO 14001 stimulate sustainable development? Manag. Environ. Qual. Int. J. 2008, 19, 204–212. [Google Scholar] [CrossRef]

- Zeng, S.X.; Tam, C.M.; Tam, V.W.Y.; Deng, Z.M. Towards implementation of ISO 14001 environmental management systems in selected industries in China. J. Clean. Prod. 2005, 13, 645–656. [Google Scholar] [CrossRef]

- Fonseca, L.M.; Domingues, J.P. Exploratory Research of ISO 14001:2015 Transition among Portuguese Organizations. Sustainability 2018, 10, 781. [Google Scholar] [CrossRef]

- Fryxell, G.E.; Szeto, A. The influence of motivations for seeking ISO 14001certification: An empirical study of ISO 14001 certified facilities in Hong Kong. J. Environ. Manag. 2002, 65, 223–238. [Google Scholar] [CrossRef]

- Darnall, N.; Carmin, J. Greener and cleaner? The signalling accuracy of U.S voluntary environmental programmes. Policy Sci. 2005, 38, 71–79. [Google Scholar] [CrossRef]

- Murmura, F.; Liberatore, L.; Bravi, L.; Casolani, N. Evaluation of Italian Companies’ Perception about ISO 14001 and Eco Management and Audit Scheme III: Motivations, Benefits and Barriers. J. Clean. Prod. 2018, 174, 691–700. [Google Scholar] [CrossRef]

- Zutshi, A.; Sohal, A.S. A framework for environmental management system adoption and maintenance: An Australian perspective. Manag. Environ. Qual. An. Int. J. 2005, 16, 464–475. [Google Scholar] [CrossRef]

- Da Silva, S.L.C.; Amaral, F.G. Critical factors of success and barriers to the implementation of occupational health and safety management systems: A systematic review of literature. Saf. Sci. 2019, 117, 123–132. [Google Scholar] [CrossRef]

- Albrechtsen, E.; Solberg, I.; Svensli, E. The application and benefits of job safety analysis. Saf. Sci. 2019, 113, 425–437. [Google Scholar] [CrossRef]

- Chen, Q. Sustainable development of occupational health and safety management system—Active upgrading of corporate safety culture. Int. J. Archit. Sci. 2004, 5, 108–113. [Google Scholar]

- Molamohamadi, Z.; Ismail, N. The relationship between occupational safety, health, and environment, and sustainable development: A review and critique. Int. J. Innov. Manag. Technol. 2014, 5, 198–202. [Google Scholar] [CrossRef]

- Rebelo, M.F.; Santos, G.; Silva, R. Integration of individualized management systems (MSs) as an aggregating factor of sustainable value for organizations: An overview through a review of the literature. J. Mod. Account. Audit. 2014, 10, 356–383. [Google Scholar]

- Domingues, J.P.T.; Sampaio, P.; Arezes, P.M. Integrated management systems assessment: A maturity model proposal. J. Clean. Prod. 2016, 124, 164–174. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Oliveira, O.J. Analysis of Integrated Management Systems research: Identifying core themes and trends for future studies. Total Qual. Manag. Bus. Excel. 2018, 1–23. [Google Scholar] [CrossRef]

- Nunhes, T.V.; Bernardo, M.; Oliveira, O.J. Guiding principles of integrated management systems: Towards unifying a starting point for researchers and practitioners. J. Clean. Prod. 2019, 210, 977–993. [Google Scholar] [CrossRef]

- Kopia, J.; Kompalla, A.; Ceausu, I. Theory and practice of integrating management systems with high level structure. Qual. Access Success 2016, 17, 52–59. [Google Scholar]

- Abad, J.; Dalmau, I.; Vilajosana, J. Taxonomic proposal for integration levels of management systems based on empirical evidence and derived corporate benefits. J. Clean. Prod. 2014, 78, 164–173. [Google Scholar] [CrossRef]

- Bernardo, M.; Alexandra, S.; Tarí, J.J.; Molina-Azorín, J.F. Benefits of management systems integration: A literature review. J. Clean. Prod. 2015, 94, 260–267. [Google Scholar] [CrossRef]

- Qi, G.; Zeng, S.; Yin, H.; Lin, H. ISO and OHSAS certifications: How stakeholders affect corporate decisions on sustainability. Manag. Sci. 2013, 51, 1983–2005. [Google Scholar] [CrossRef]

- Rebelo, M.; Santos, G.; Silva, R. Conception of a flexible integrator and lean model for integrated management systems. Total Qual. Manag. Bus. Excel. 2014, 25, 683–701. [Google Scholar] [CrossRef]

- Gianni, M.; Gotzamani, K.; Tsiotras, G. Multiple perspectives on integrated management systems and corporate sustainability performance. J. Clean. Prod. 2017, 168, 1297–1311. [Google Scholar] [CrossRef]

- Elkington, J. Cannibals with Forks: The Triple Bottom Line of 21st Century Business; John Wiley and Sons: London, UK, 1997. [Google Scholar]

- United Nations. Agenda for Development; UN: New York, NY, USA, 1997.

- Govindan, K.; Khodaverdi, R.; Jafarian, A. A fuzzy multi criteria approach for measuring sustainability performance of a supplier based on triple bottom line approach. J. Clean. Prod. 2013, 47, 345–354. [Google Scholar] [CrossRef]

- Robert, K.W.; Parris, T.M.; Leiserowitz, A.A. What is sustainable development? Goals, indicators, values, and practice. Environ. Sci. Policy Sustain. Dev. 2005, 47, 8–21. [Google Scholar] [CrossRef]

- Fonseca, L.; Ferro, R. Does it Pay to be Social Responsible? Portuguese SMEs feedback. Intang. Cap. 2016, 12, 487–505. [Google Scholar] [CrossRef]

- Lo, S.-F. Performance evaluation for sustainable business: A profitability and marketability framework. Corp. Soc. Responsib. Environ. Maneg. 2010, 17, 311–319. [Google Scholar] [CrossRef]

- Schaltegger, S.; Beckmann, M.; Hansen, E.G. Transdisciplinarity in corporate sustainability: Mapping the field. Bus. Strateg. Environ. 2013, 22, 219–229. [Google Scholar] [CrossRef]

- Dyllick, T.; Hockerts, K. Beyond the business case for corporate sustainability. Bus. Strateg. Environ. 2002, 11, 130–141. [Google Scholar] [CrossRef]

- Fonseca, L.; Lima, V. Countries three Wise Men: Sustainability, Innovation, and Competitiveness. J. Ind. Eng. Manag. 2015, 8, 1288–1302. [Google Scholar] [CrossRef]

- Rosati, F.; Faria, L.G.D. Addressing the SDGs in sustainability reports: The relationship with institutional factors. J. Clean. Prod. 2019, 215, 1312–1326. [Google Scholar] [CrossRef]

- Gupta, J.; Vegelin, C. Sustainable development goals and inclusive development. Int. Environ. Agreements Polit. Law Econ. 2016, 16, 1–16. [Google Scholar] [CrossRef]

- United Nations Global Compact. How Your Company Can Advance Each of the SDGs. Available online: https://www.unglobalcompact.org/sdgs/17-global-goals (accessed on 13 August 2019).

- Sullivan, K.; Thomas, S.; Rosano, M. Using industrial ecology and strategic management concepts to pursue the Sustainable Development Goals. J. Clean. Prod. 2018, 174, 237–246. [Google Scholar] [CrossRef]

- Global Reporting Initiative About Sustainability Reporting. Available online: https://www.globalreporting.org/information/sustainabilityreporting/Pages/default.aspx (accessed on 13 August 2019).

- Fonseca, L.; Ferro, R. Influence of firms’ environmental management and community involvement programs in their employees and in the community. FME Trans. 2015, 43, 370–376. [Google Scholar] [CrossRef]

- Lozano, R. Addressing stakeholders and better contributing to sustainability through game theory. J. Corp. Citizensh. 2011, 43, 45–62. [Google Scholar] [CrossRef]

- United Nations Global Compact. Reporting on the SDGs—Shape the Future of Corporate Reporting on the SDGs. Available online: https://www.unglobalcompact.org/take-action/action/sdg-reporting (accessed on 12 August 2019).

- Schramade, W. Investing in the UN Sustainable Development Goals: Opportunities for companies and investors. J. Appl. Corp. Financ. 2017, 29, 87–99. [Google Scholar] [CrossRef]

- Rosati, F.; Faria, L.G.D. Business contribution to the Sustainable Development Agenda: Organizational factors related to early adoption of SDG reporting. Corp. Soc. Resp. Environ. Manag. 2019, 26, 588–597. [Google Scholar] [CrossRef]

- Carvalho, F.; Domingues, P.; Sampaio, P. Communication of commitment towards sustainable development of certified Portuguese organisations: Quality, environment and occupational health and safety. Int. J. Qual. Reliab. Manag. 2019, 36, 458–484. [Google Scholar] [CrossRef]

- Krippendorff, K. Content Analysis: An Introduction to its Methodology, 2nd ed.; Sage Publications: Thousand Oaks, CA, USA, 2004. [Google Scholar]

- Branco, M.C.; Rodrigues, L.L. Factors influencing social responsibility disclosure by Portuguese companies. J. Bus. Ethics 2008, 83, 685–701. [Google Scholar] [CrossRef]

- Gill, D.L.; Dickinson, S.J.; Scharl, A. Communicating sustainability: A web content analysis of North American, Asian and European firms. J. Commun. Manag. 2008, 12, 243–262. [Google Scholar] [CrossRef]

- Tagesson, T.; Blank, V.; Broberg, P.; Collin, S.O. What explains the extent and content of social and environmental disclosures on corporate websites: A study of social and environmental reporting in Swedish listed corporation. Corp. Soc. Resp. Environ. Manag. 2009, 16, 352–364. [Google Scholar] [CrossRef]

- Lee, K.H.; Barker, M.; Mouasher, A. Is it even espoused? An exploratory study of commitment to sustainability as evidenced in vision, mission, and graduate attribute statements in Australian universities. J. Clean. Prod. 2013, 48, 20–28. [Google Scholar] [CrossRef]

- Amran, A.; Lee, S.P.; Devi, S.S. The influence of governance structure and strategic corporate social responsibility toward sustainability reporting quality. Bus. Strateg. Environ. 2014, 23, 217–235. [Google Scholar] [CrossRef]

- Bardin, L. Análise de Conteúdo, 6th ed.; Edições 70: Lisboa, Portugal, 2015. [Google Scholar]

- Gallego, I. The use of economic, social and environmental indicators as a measure of sustainable development in Spain. Corp. Soc. Resp. Environ. Manag. 2006, 13, 78–97. [Google Scholar] [CrossRef]

- Ho, L.-C.J.; Taylor, M.E. An empirical analysis of triple bottom-line reporting and its determinants: Evidence from the United States and Japan. J. Int. Financ. Manag. Account. 2007, 18, 123–150. [Google Scholar] [CrossRef]

- Carvalho, F.; Santos, G.; Gonçalves, J. The disclosure of information on sustainable development on the corporate website of the certified Portuguese organizations. Int. J. Qual. Res. 2018, 12, 253–276. [Google Scholar] [CrossRef]

- Carvalho, F. The Communication of Results on Sustainable Development in the Certified Portuguese Organizations in Quality, Environment and Safety. Master’s Thesis, School of Engineering, Porto, Portugal, 2019. [Google Scholar]

- United Nations Global Compact. Available online: https://www.unglobalcompact.org/participation/join/commitment (accessed on 18 August 2019).

- Transforming our World: The 2020 Agenda for Sustainable Development; United Nations General Assembly: New York, NY, USA, 2015.

- Haniffa, R.M.; Cooke, T.E. The impact of culture and governance on corporate social reporting. J. Account. Public Policy 2005, 24, 391–430. [Google Scholar] [CrossRef]

- Kleinbaum, D.G.; Klein, M. Logistic Regression: A Self-Learning Text, 3rd ed.; Springer: New York, NY, USA, 2010. [Google Scholar] [CrossRef]

- Hair, J.F.; Black, J.W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 7th ed.; Pearson Education Limited: Edinburgh, UK, 2014. [Google Scholar]

- Laureano, R.M.S. Testes de Hipóteses Com o SPSS: O Meu Manual de Consulta Rápida, 1st ed.; Edições Sílabo: Lisboa, Portugal, 2011. [Google Scholar]

- Pestana, M.H.; Gageiro, J.N. Análise de Dados Para Ciências Sociais. A Complementaridade do SPSS, 6st ed.; Edições Sílabo: Lisboa, Portugal, 2014. [Google Scholar]

- OECD. Enhancing the Contributions of SMEs in a Global and Digitalized Economy. In Proceedings of the Meeting of the OECD Council at Ministerial Level, Paris, France, 7–8 June 2017; Available online: https://www.oecd.org/mcm/documents/C-MIN-2017-8-EN.pdf (accessed on 9 October 2019).

- OECD. 2017. Available online: https://oecd-development-matters.org/2017/04/03/unlocking-the-potential-of-smes-for-the-sdgs/ (accessed on 9 October 2019).

- Busu, M. Assessment of the Impact of Bioenergy on Sustainable Economic Development. Energies 2019, 12, 578. [Google Scholar] [CrossRef]

- Nilsson, M.; Griggs, D.; Visbeck, M. Policy: Map the interactions between Sustainable Development Goals. Nat. News 2016, 534, 320. [Google Scholar] [CrossRef] [PubMed]

| Corpus of Analysis (Documents of Analysis) | Categories and Subcategories of Analysis Sustainable Development Goals (SDGs) | Units of Analysis |

|---|---|---|

| Institutional reports disclosed on the institutional website of the organization (i.e., the corpus of analysis). Institutional reports, such as sustainability reports; social responsibility reports; environmental reports; occupational health and safety reports; management reports; accounts and reports; accounts and management reports; financial reports; corporate governance reports; integrated reports) | 01. No poverty 02. Zero hunger 03. Good health and well-being 04. Quality education 05. Gender equality 06. Clean water and sanitation 07. Affordable and clean energy 08. Decent work and economic growth 09. Industry, innovation, and infrastructure 10. Reduced inequalities 11. Sustainable cities and communities 12. Responsible consumption and production 13. Climate action 14. Life below water 15. Life on land 16. Peace, justice and strong institutions 17. Partnerships for the goals | Concept (i.e., the theme, word and/or phrase) |

| Variables | Description (the organization is classified dichotomously (i.e., in binary form) according to…) |

|---|---|

| Business volume (BV) | … the business volume, in euros (€), obtained in 2017. When the business volume (i.e., turnover) of an organization is among the top 1000 in Portugal, the organization is classified as “Greater” (1); otherwise, it is classified as “Other” (0) |

| Activity sector (AS) | … the activity sector. When the activity sector (i.e., economic sector or industrial sector) of an organization is framed on the secondary sector (second sector), the organization is classified as “Second sector” (1); otherwise, it is classified as “Other” (0) |

| UNGC NP members (UM) | … the relationship with the UNGC NP. When the organization belongs to an economic group that assumes a relationship (i.e., member) with the UNGC NP, the organization is classified as “Member” (1); otherwise, it is classified as “No” (0) |

| Sustainability reports (SR) | … the disclosure of the sustainability reports on the institutional website. If the organization has disclosed a sustainability report on their website, the organization is classified as “Disclose” (1); otherwise, it is classified as “No” (0) |

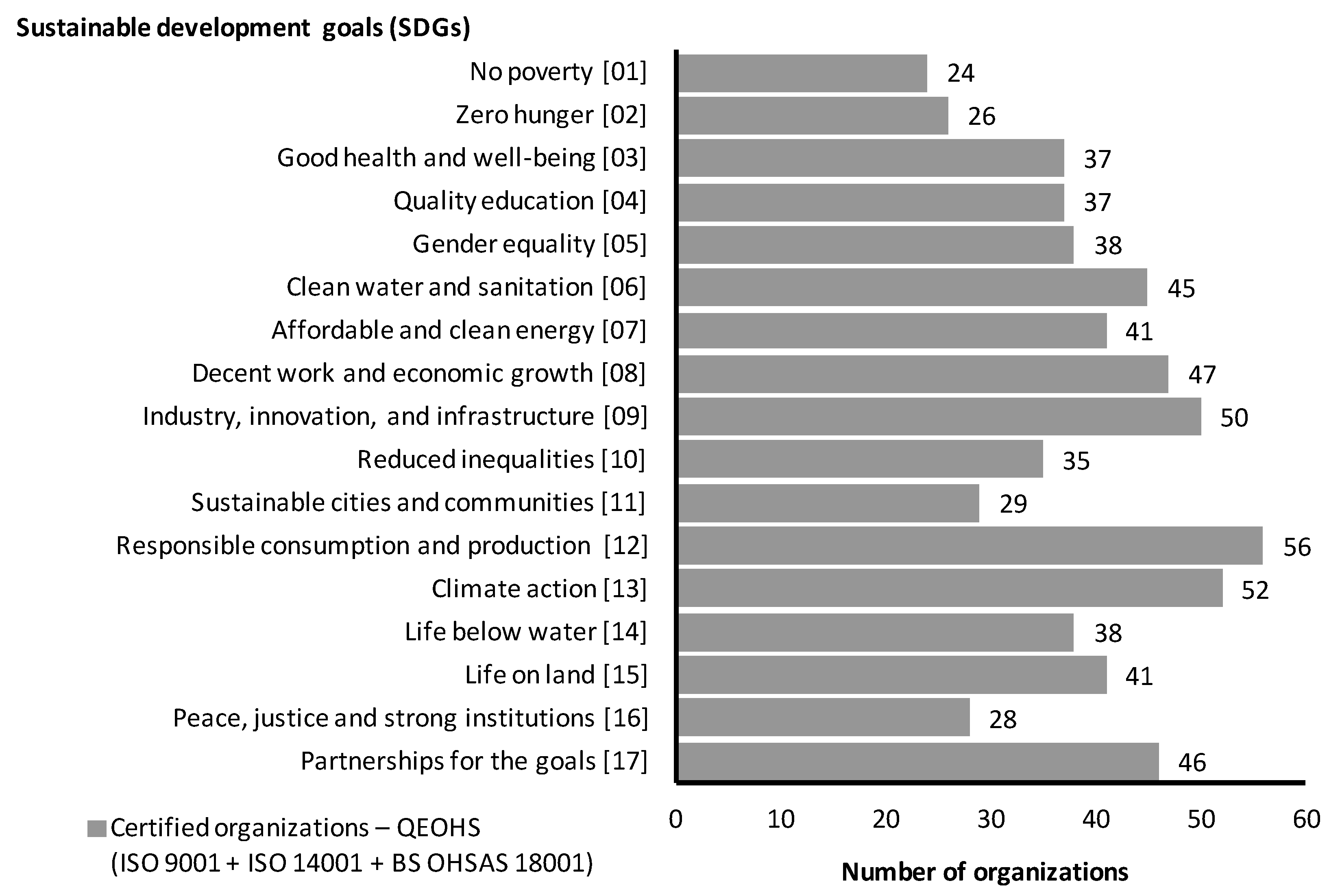

| Sustainable Development Goals (SDGs) | SD DIM | N | % |

|---|---|---|---|

| SDG 01. No poverty | SOC | 24 | 10.2 |

| SDG 02. Zero hunger | SOC | 26 | 11.1 |

| SDG 03. Good health and well-being | SOC | 37 | 15.7 |

| SDG 04. Quality education | SOC | 37 | 15.7 |

| SDG 05. Gender equality | ECO and SOC | 38 | 16.2 |

| SDG 06. Clean water and sanitation | ENV and SOC | 45 | 19.1 |

| SDG 07. Affordable and clean energy | ECO and ENV | 41 | 17.4 |

| SDG 08. Decent work and economic growth | ECO and SOC | 47 | 20.0 |

| SDG 09. Industry, innovation, and infrastructure | ECO | 50 | 21.3 |

| SDG 10. Reduced inequalities | ECO and SOC | 35 | 14.9 |

| SDG 11. Sustainable cities and communities | ENV and SOC | 29 | 12.3 |

| SDG 12. Responsible consumption and production | ECO and SOC | 56 | 23.8 |

| SDG 13. Climate action | ENV | 52 | 22.1 |

| SDG 14. Life below water | ENV | 38 | 16.2 |

| SDG 15. Life on land | ENV | 41 | 17.4 |

| SDG 16. Peace, justice and strong institutions | SOC | 28 | 11.9 |

| SDG 17. Partnerships for the goals | ECO, ENV and SOC | 46 | 19.6 |

| Dependent Variable | N | Minimum | Maximum | Sum | Mean | SD | Variance |

|---|---|---|---|---|---|---|---|

| Sustainable Development Goals Communication Index (SDGCI) | 235 | 0.000 | 1.000 | 39.412 | 0.168 | 0.306 | 0.093 |

| Variables | Dependent | |||||||

|---|---|---|---|---|---|---|---|---|

| Sustainable Development Goals Communication Index | ||||||||

| H | Independent | N | Minimum | Maximum | Sum | Mean | SD | Variance |

| H1 | Business volume | |||||||

| (0) Other | 141 | 0.000 | 1.000 | 18.824 | 0.134 | 0.288 | 0.083 | |

| (1) Greater | 94 | 0.000 | 1.000 | 20.588 | 0.219 | 0.325 | 0.106 | |

| H2 | Activity sector | |||||||

| (0) Other | 103 | 0.000 | 1.000 | 20.000 | 0.194 | 0.341 | 0.116 | |

| (1) Second sector | 132 | 0.000 | 1.000 | 19.412 | 0.147 | 0.275 | 0.075 | |

| H3 | UNGC NP members | |||||||

| (0) No | 190 | 0.000 | 1.000 | 20.882 | 0.110 | 0.252 | 0.063 | |

| (1) Member | 45 | 0.000 | 1.000 | 18.529 | 0.412 | 0.386 | 0.149 | |

| H4 | Sustainability reports | |||||||

| (0) No | 129 | 0.000 | 1.000 | 11.765 | 0.091 | 0.259 | 0.067 | |

| (1) Disclose | 106 | 0.000 | 1.000 | 27.647 | 0.261 | 0.332 | 0.110 | |

| Variables | Dependent | |||||

|---|---|---|---|---|---|---|

| Sustainable Development Goals Communication Index | ||||||

| H | Independent (Categories) | N | Sum of Ranks | Mean of Ranks | Mann–WhitneyU Test | p-Value (One-Tailed) |

| H1 | Business volume | |||||

| (0) Other | 141 | 15574.000 | 110.450 | 5563.000 | 0.005 | |

| (1) Greater | 94 | 12156.000 | 129.320 | |||

| H2 | Activity sector | |||||

| (0) Other | 103 | 12414.000 | 120.520 | 6538.000 | 0.263 | |

| (1) Second sector | 132 | 15316.000 | 116.030 | |||

| H3 | UNGC NP members | |||||

| (0) No | 190 | 20555.000 | 108.180 | 2410.000 | 0.000 | |

| (1) Member | 45 | 7175.000 | 159.440 | |||

| H4 | Sustainability reports | |||||

| (0) No | 129 | 13124.000 | 101.740 | 4739.000 | 0.000 | |

| (1) Disclose | 106 | 14606.000 | 137.790 | |||

| H | Independent Variables | β | SE | Exp(β) | Wald | p-Value |

|---|---|---|---|---|---|---|

| H1 | Business volume | 0.770 | 0.355 | 2.159 | 4.704 | 0.030 |

| H2 | Activity sector | −0.032 | 0.360 | 0.968 | 0.008 | 0.928 |

| H3 | UNGC NP members | 2.003 | 0.407 | 7.413 | 24.270 | 0.000 |

| H4 | Sustainability reports | 1.671 | 0.367 | 5.319 | 20.721 | 0.000 |

| Constant | −2.638 | 0.396 | 0.071 | 44.335 | 0.000 | |

| Statistical parameters of the binary logistic regression model: | Statistics | p-Value | ||||

| Overall statistics—Chi-square (χ2) | 57.353 | 0.000 | ||||

| Overall percentage—Percentage correct (%) | 79.100 | – | ||||

| Omnibus tests of model coefficients—Chi-square (χ2) | 59.837 | 0.000 | ||||

| −2 Log likelihood | 219.228 | – | ||||

| Cox and Snell—R-square (R2) | 0.225 | – | ||||

| Nagelkerke—R-square (R2) | 0.323 | – | ||||

| Hosmer and Lemeshow test—Chi-square (χ2) | 6.624 | 0.469 | ||||

| Research Hypotheses Tested with the Binary Logistic Regression Model | |||

|---|---|---|---|

| H1 | H2 | H3 | H4 |

| Accept | Reject | Accept | Accept |

© 2019 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Fonseca, L.; Carvalho, F. The Reporting of SDGs by Quality, Environmental, and Occupational Health and Safety-Certified Organizations. Sustainability 2019, 11, 5797. https://doi.org/10.3390/su11205797

Fonseca L, Carvalho F. The Reporting of SDGs by Quality, Environmental, and Occupational Health and Safety-Certified Organizations. Sustainability. 2019; 11(20):5797. https://doi.org/10.3390/su11205797

Chicago/Turabian StyleFonseca, Luis, and Filipe Carvalho. 2019. "The Reporting of SDGs by Quality, Environmental, and Occupational Health and Safety-Certified Organizations" Sustainability 11, no. 20: 5797. https://doi.org/10.3390/su11205797

APA StyleFonseca, L., & Carvalho, F. (2019). The Reporting of SDGs by Quality, Environmental, and Occupational Health and Safety-Certified Organizations. Sustainability, 11(20), 5797. https://doi.org/10.3390/su11205797